*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Fix and Flip Loans: The Ultimate Guide to Finding & Comparing Lenders

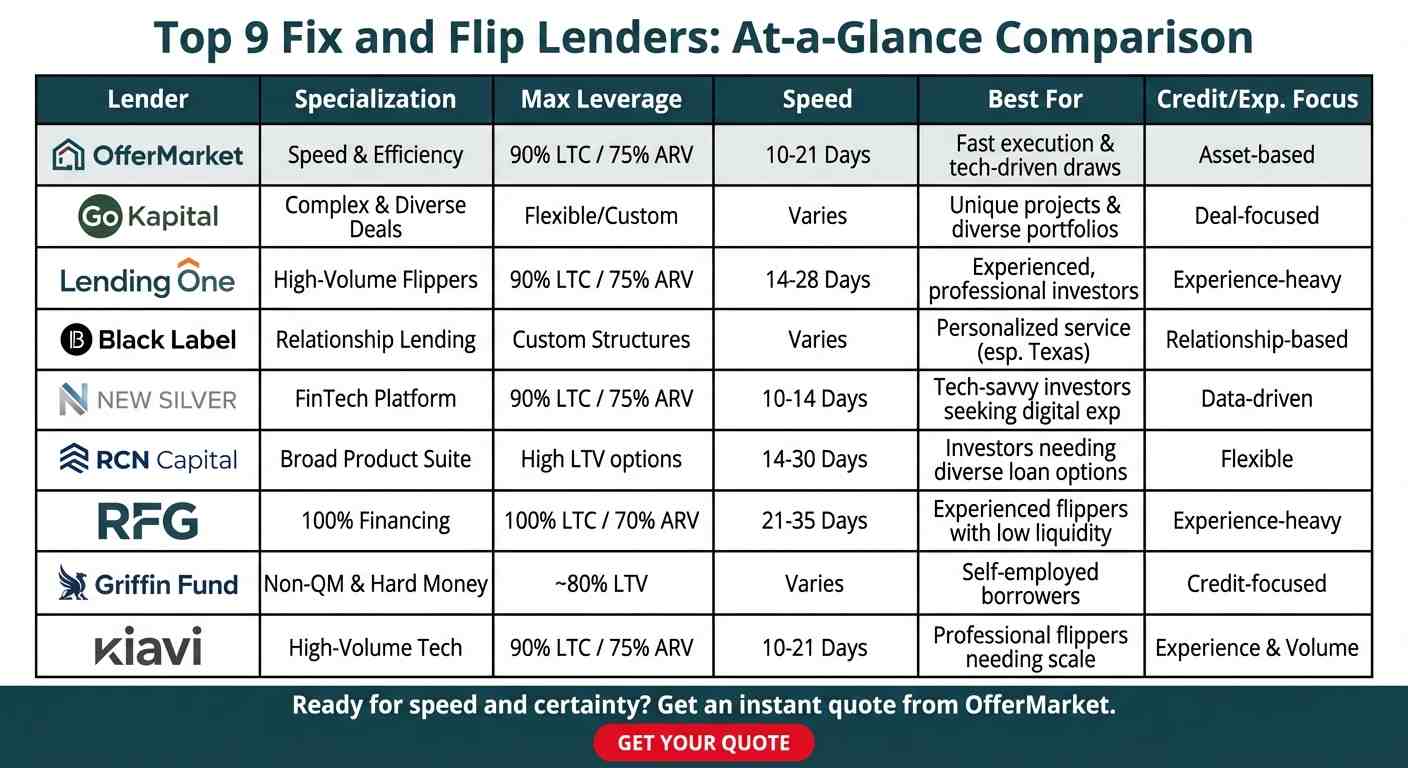

Choosing the right lender is as critical as choosing the right property. The terms, speed, and reliability of your financing partner can make or break your project's profitability. Below is a detailed comparison of nine leading fix and flip lenders, each with unique strengths, to help you identify the best fit for your investment strategy.

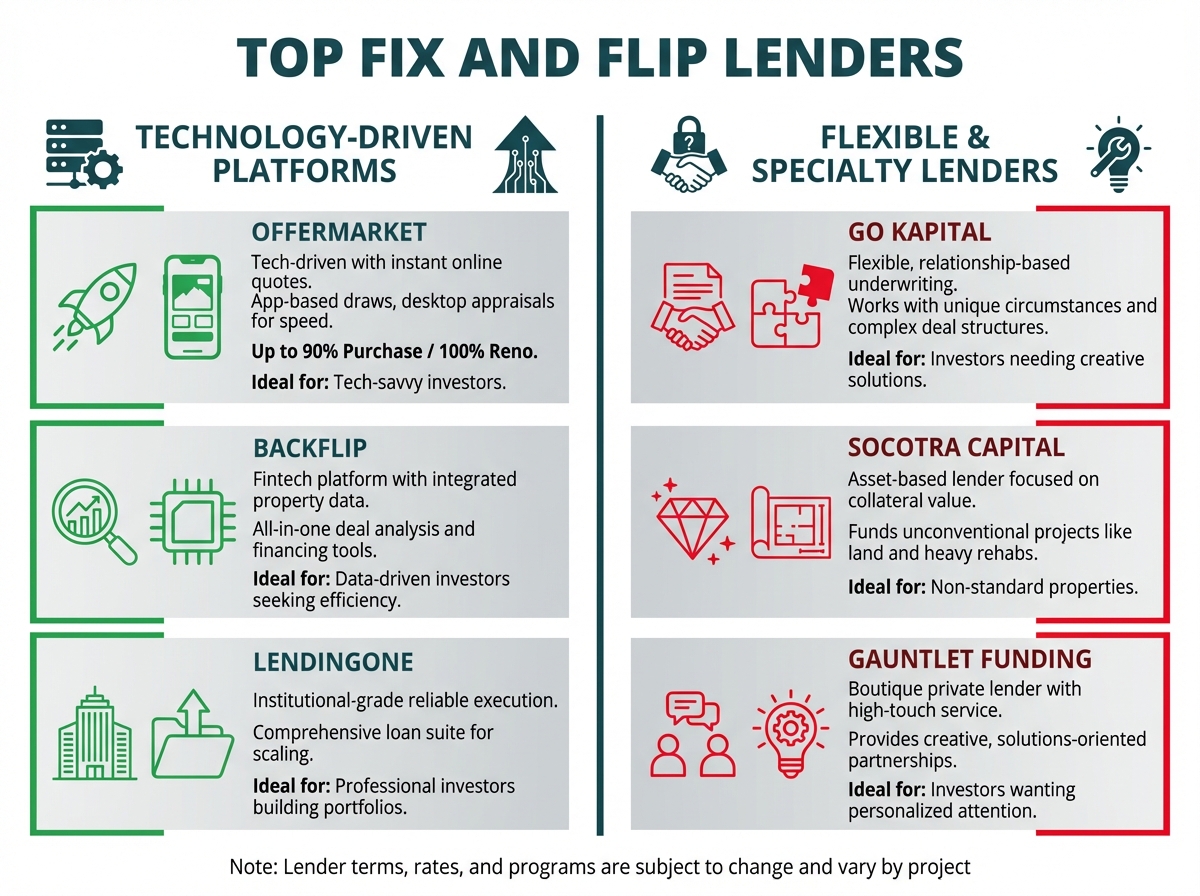

OfferMarket

OfferMarket is engineered for real estate investors who prioritize speed, efficiency, and certainty of execution. By leveraging technology and focusing on asset-based underwriting, we eliminate the hurdles common with traditional and even other private lenders. Our process is designed to get you from application to the closing table faster, so you can secure competitive deals in a fast-moving market.

Loan Products and Specializations: Specializes in fix and flip loans, rental loans, new construction financing, Slow Flip and HELOANs. The core focus is on short-term bridge financing for value-add projects.

Interest Rates, Fees, and Typical Points: Rates are competitive and market-driven. Points typically range from 1-2%, with a strong emphasis on transparent, no-junk-fee term sheets.

LTV, LTC, and ARV Lending Limits: Offers up to 90% Loan-to-Cost (LTC) and up to 75% After Repair Value (ARV). This structure allows experienced investors to maximize leverage while keeping projects profitable.

Minimum Credit Score and Experience Requirements: While credit is a factor, the primary focus is on the asset's quality and the deal's viability. A minimum credit score of 680 is typical, and experience is preferred but not always required for investors with a strong team and a solid project plan. The asset-based approach means the property itself is the most important part of the application.

Key Differentiators: The use of desktop appraisals and an app-based draw process dramatically accelerates the timeline. Investors can get funds for rehab work in days, not weeks. The typical closing timeline of 10-21 days is a significant competitive advantage.

Go Kapital

Go Kapital positions itself as a versatile lender capable of handling a wide array of financing needs, from standard residential flips to more complex commercial projects. Their flexibility makes them a go-to option for investors with diverse portfolios or unique deal structures that don't fit into a rigid lending box.

Loan Products and Specializations: Offers a broad suite including hard money loans, commercial bridge loans, and long-term financing. They are adept at funding mixed-use properties, multi-family units, and other commercial assets in addition to standard 1-4 unit residential properties.

Interest Rates, Fees, and Typical Points: Rates and fees are determined on a case-by-case basis, reflecting the customized nature of their loans. Expect terms to be tailored to the project's specific risk and complexity.

LTV, LTC, and ARV Lending Limits: Lending parameters are flexible. They can structure loans based on LTV, LTC, or ARV depending on the deal, often accommodating requests that other lenders might decline.

Minimum Credit Score and Experience Requirements: Go Kapital is more relationship and deal-focused than strictly numbers-driven. While they review credit and experience, a compelling project with a clear exit strategy can often overcome lower credit scores or a lack of extensive flipping history.

Lending One

Lending One is a large, national direct private lender known for its reliability and streamlined processes. They cater to experienced investors who need a dependable source of capital for standard fix and flip, rental, and new construction projects. Their platform is built for efficiency and scale.

Loan Products and Specializations: Primarily focuses on fix and flip loans, rental portfolio loans, and new construction. They are well-equipped to handle high-volume flippers and landlords.

Interest Rates, Fees, and Typical Points: Offers competitive institutional-quality rates. Their pricing is typically straightforward, appealing to professional investors who value predictability.

LTV, LTC, and ARV Lending Limits: Generally provides up to 90% LTC and 75% ARV. Their rental loan programs also offer competitive LTVs for buy-and-hold investors.

Minimum Credit Score and Experience Requirements: Tends to work with more experienced investors. A solid track record of successful projects and a good credit score (typically 660+) are important factors in their underwriting.

Black Label Capital

Black Label Capital operates as a boutique lender, emphasizing personalized service and strong relationships. They are an excellent choice for investors who want a high-touch experience and a financing partner who understands the nuances of their local market, particularly in Texas.

Loan Products and Specializations: Specializes in customized loan structures for fix and flip, new construction, and bridge loans. Their deep market knowledge in Texas gives them an edge in that region.

Interest Rates, Fees, and Typical Points: Pricing is customized to the deal. They work closely with borrowers to structure terms that align with the project's specific needs, which may involve more creative financing solutions.

LTV, LTC, and ARV Lending Limits: Loan structures are flexible and tailored to the individual deal. They pride themselves on finding ways to fund good projects, even if they don't fit standard guidelines.

Minimum Credit Score and Experience Requirements: Places a high value on the borrower's character and the strength of the deal. They are more willing to work with investors on a relationship basis rather than relying solely on automated underwriting metrics.

New Silver

New Silver is a fintech lender that leverages technology to provide a fast and seamless borrowing experience. Their platform is designed for tech-savvy investors who appreciate speed, transparency, and the ability to manage their loans digitally.

Loan Products and Specializations: Offers fix and flip, rental, and ground-up construction loans. Their platform features tools like instant term sheets and a "proof of funds" letter generator.

Interest Rates, Fees, and Typical Points: Utilizes technology to offer competitive, transparent pricing. The digital application process helps reduce overhead, which can translate into better terms for the borrower.

LTV, LTC, and ARV Lending Limits: Standard lending limits apply, typically up to 90% LTC and 75% ARV. Their technology helps to quickly validate project numbers and ARV estimates.

Minimum Credit Score and Experience Requirements: Their platform is accessible to both new and experienced investors. A minimum credit score around 650 is generally required. The streamlined, data-driven approach is ideal for investors who are comfortable with a digital-first process.

RCN Capital

RCN Capital is a major nationwide lender with one of the most extensive product menus in the industry. They are a powerhouse in the private lending space, often working through mortgage brokers and partners to fund a high volume of loans across the country.

Loan Products and Specializations: Offers a vast suite of loans for short-term flips, long-term rentals, new construction, and multi-family properties. They have products that require no income or asset verification, focusing solely on the property.

Interest Rates, Fees, and Typical Points: As a large-scale lender, their rates are highly competitive. They offer a variety of pricing tiers based on credit, experience, and loan product.

LTV, LTC, and ARV Lending Limits: Provides a wide range of leverage options, including high-LTV products for qualified borrowers and projects.

Minimum Credit Score and Experience Requirements: With a diverse product set, they have options for investors across the experience spectrum. Some loan programs have no minimum experience requirements, while others are designed for seasoned professionals.

Rehab Financial Group

Rehab Financial Group (RFG) has carved out a unique niche by specializing in 100% financing for both the purchase and renovation of a property. This makes them an exceptional option for experienced flippers who have a great deal lined up but are short on liquid capital for the down payment.

Loan Products and Specializations: Their flagship product is the 100% financing loan, which covers both purchase and rehab costs. They also offer more traditional fix and flip loans.

Interest Rates, Fees, and Typical Points: Due to the higher leverage and risk associated with 100% financing, their rates and points are typically higher than conventional hard money loans. However, the ability to enter a deal with no money down on the purchase can be invaluable.

LTV, LTC, and ARV Lending Limits: They can fund up to 100% of the purchase and rehab costs, provided the total loan amount does not exceed 70% of the ARV. The borrower is typically responsible for closing costs and interest reserves.

Minimum Credit Score and Experience Requirements: This product is designed for experienced investors. RFG heavily scrutinizes the borrower's track record and the viability of the deal itself. A strong history of successful flips is usually required.

Griffin Funding

Griffin Funding operates in the space between traditional banking and hard money lending, offering non-QM (Non-Qualified Mortgage) loans alongside hard money options. This makes them a great fit for self-employed investors or those who may not qualify for conventional loans due to income documentation challenges.

Loan Products and Specializations: Specializes in non-QM loans, including bank statement loans and asset-based lending for investment properties. They also provide hard money fix and flip loans.

Interest Rates, Fees, and Typical Points: Rates on their non-QM products are generally lower than hard money but higher than conventional loans. Hard money rates are competitive within that specific market.

LTV, LTC, and ARV Lending Limits: LTVs are typically more conservative than pure hard money lenders, often capping around 80% LTV or LTC.

Minimum Credit Score and Experience Requirements: They cater to borrowers with good credit (often 680+) who have non-traditional income situations. Their underwriting focuses on ability-to-repay through alternative documentation like bank statements.

Kiavi

Kiavi, formerly known as LendingHome, is a dominant force in the fix and flip lending space, leveraging a powerful technology platform to serve high-volume, professional investors. Their model is built on speed, predictability, and data-driven decision-making.

Loan Products and Specializations: Primarily focuses on fix and flip and rental loans for experienced investors. Their platform is optimized for repeat borrowers who need consistent and reliable funding for multiple projects per year.

Interest Rates, Fees, and Typical Points: Their scale allows them to offer some of the most competitive rates in the industry, especially for repeat clients. They have a tiered system that rewards experience and volume with better pricing.

LTV, LTC, and ARV Lending Limits: Offers high leverage, often up to 90% LTC and 75% ARV, for qualified borrowers.

Minimum Credit Score and Experience Requirements: Kiavi is best suited for professional real estate investors with a proven track record. While they have options for newer investors, their best terms are reserved for high-volume flippers who can move quickly through their tech-driven process.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →How to Choose the Right Fix and Flip Lender

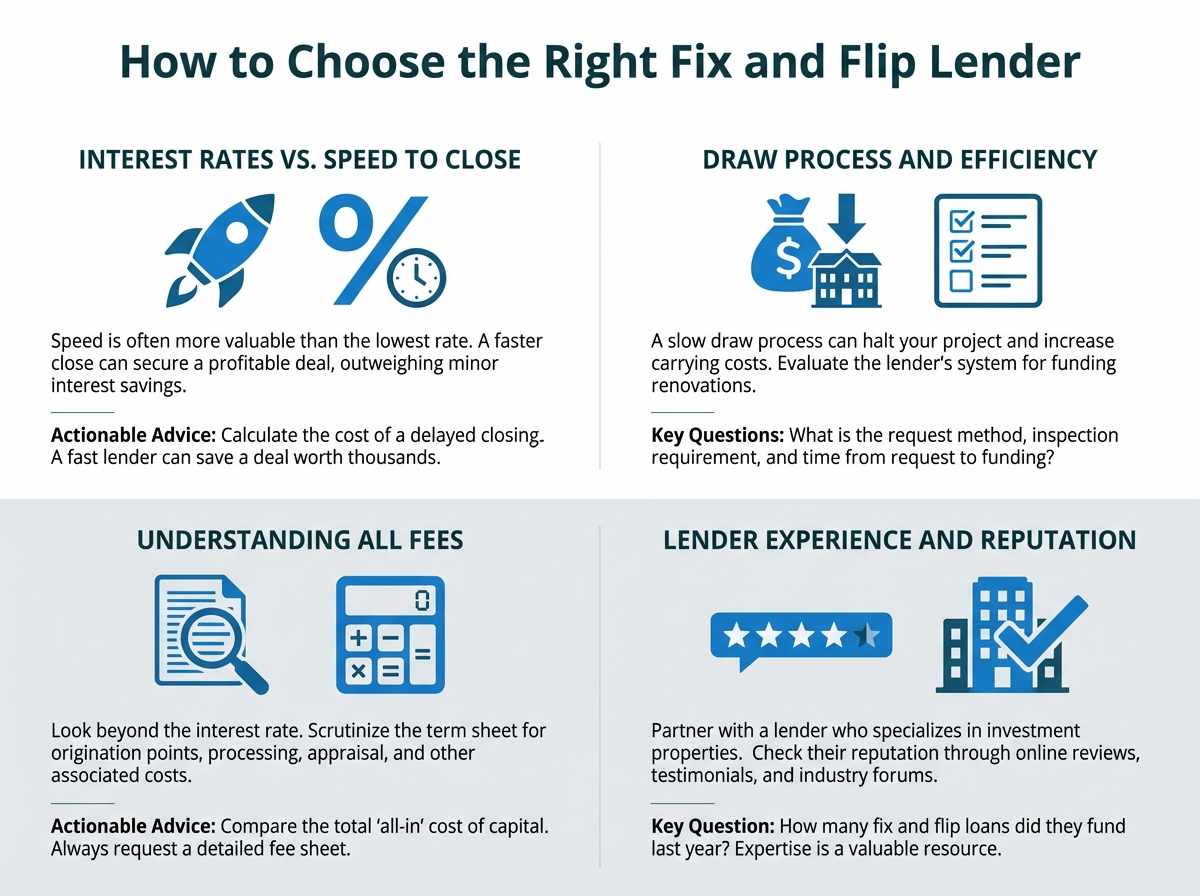

With so many options, selecting the right lender can feel overwhelming. The "best" lender is subjective and depends entirely on your priorities as an investor. A first-time flipper with limited capital has different needs than a seasoned professional flipping 20 houses a year. Focus on these four key areas to make an informed decision.

Comparing Interest Rates vs. Speed to Close

It's tempting to shop for the lowest interest rate, but in the world of flipping, speed is often more valuable. A lower rate from a slow, bureaucratic lender could cause you to lose a deal in a competitive market. A slightly higher rate from a lender who can close in 10 days might secure you a property with a massive profit margin.

- Actionable Advice: Calculate the real cost of a delayed closing. If a 30-day delay means losing a deal with a potential $50,000 profit, paying an extra half-point in interest to a lender who can close in 15 days is a smart business decision. Always ask a potential lender for their average closing time and get references if possible.

Evaluating a Lender’s Draw Process and Efficiency

Your loan doesn't just cover the purchase; it funds the renovation. A slow, inefficient draw process can halt your project, leaving contractors unpaid and extending your holding period. This directly eats into your profits through increased interest payments and other carrying costs.

- Actionable Advice: Ask lenders to detail their draw process.

- How do you request a draw? (Email, portal, app?)

- What inspection is required? (In-person, virtual, photos/videos?)

- How long does it take from request to funding?

- A lender like OfferMarket, with an app-based draw request and rapid funding, provides a significant advantage by keeping your project moving forward without costly delays.

Understanding All Fees: Origination, Processing, and Exit Fees

Interest rates and points are just part of the cost. Scrutinize the term sheet for all associated fees. These can include:

Origination Points: An upfront fee calculated as a percentage of the loan amount (e.g., 2 points = 2%).

Processing/Underwriting Fees: Flat fees for preparing and evaluating your loan file.

Appraisal and Inspection Fees: Costs for property valuation and construction progress checks.

Legal/Doc Prep Fees: Fees for drawing up the loan documents.

Exit Fees or Prepayment Penalties: A fee charged when you pay off the loan. While less common on short-term fix and flip loans, it's crucial to confirm.

Actionable Advice: Always request a detailed fee sheet or term sheet from any potential lender. Compare the total "all-in" cost of capital, not just the advertised interest rate. A loan with a lower rate but high ancillary fees might be more expensive overall.

Assessing Lender Experience and Market Reputation

Work with a lender who specializes in investment properties. A lender who primarily deals with owner-occupied mortgages may not understand the urgency and unique structure of a fix and flip deal. Check their reputation through online reviews, testimonials, and industry forums like BiggerPockets.

- Actionable Advice: Ask a potential lender how many fix and flip loans they funded last year. An experienced lender will have a deep understanding of construction budgets, ARV calculations, and the common challenges that arise during a renovation project. Their expertise can be a valuable resource.

How Fix and Flip Loans Work: Core Mechanics

Fix and flip loans, often referred to as hard money or bridge loans, are short-term financing instruments designed specifically for purchasing and renovating properties. Unlike traditional mortgages, they are underwritten based on the property's value and potential, not just the borrower's personal income.

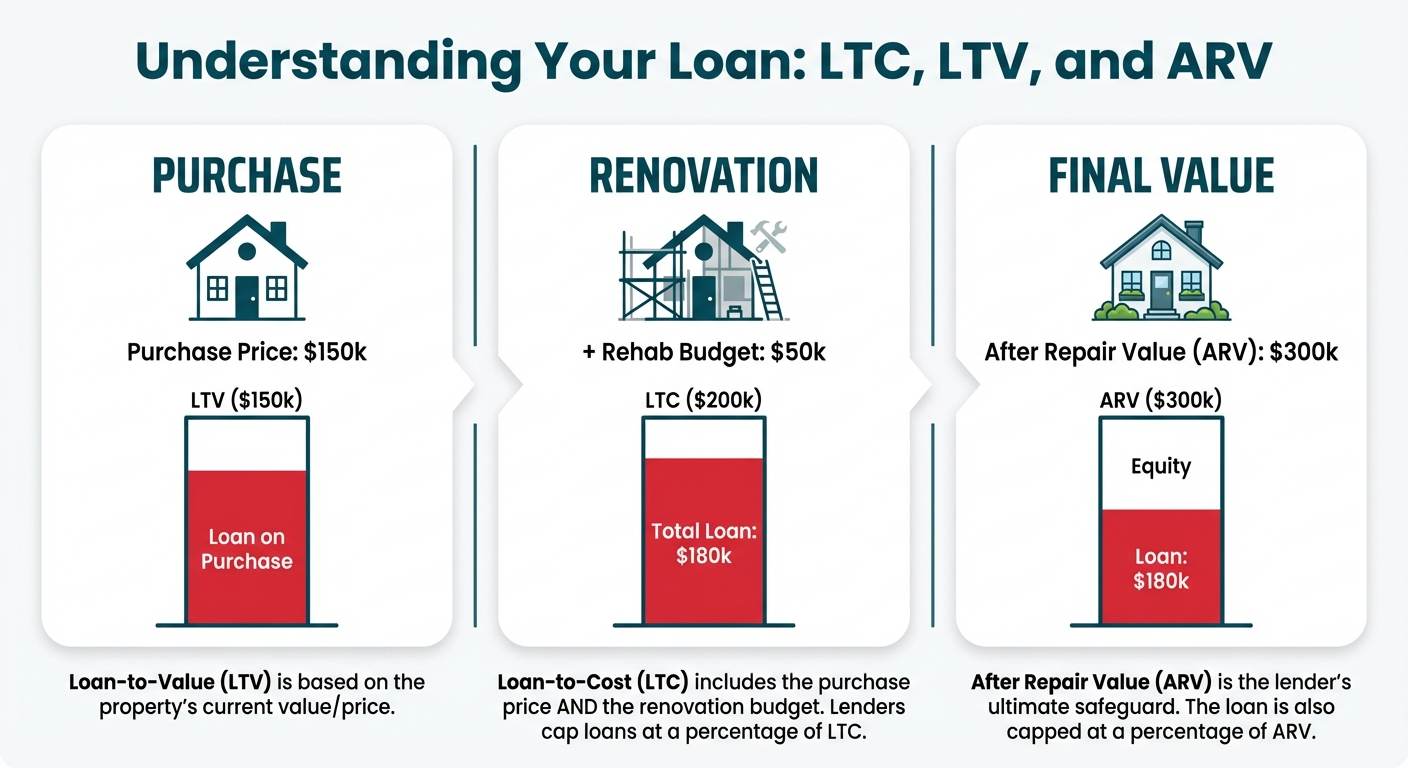

Loan-to-Cost (LTC) vs. Loan-to-Value (LTV)

These two metrics are fundamental to understanding how your loan is structured.

Loan-to-Cost (LTC): This is the loan amount divided by the total project cost (purchase price + renovation budget). For example, if you buy a property for $150,000 and have a $50,000 rehab budget, your total cost is $200,000. An 85% LTC loan would provide you with $170,000.

Loan-to-Value (LTV): This is the loan amount divided by the property's current appraised value. For a purchase, this is often simply the purchase price. LTV is more commonly used for refinancing existing properties.

Most fix and flip lenders base their loans on LTC for the initial purchase and renovation funding.

The Role of After Repair Value (ARV)

ARV is the estimated value of the property after all renovations are complete. This is the most critical number in fix and flip lending. Lenders use the ARV to determine the maximum loan amount they are willing to offer, ensuring the project is profitable and that there is sufficient equity to protect their investment.

- Example: A lender might offer up to 90% LTC, but they will also cap the total loan amount at 75% of the ARV.

- Purchase Price: $150,000

- Rehab Budget: $50,000

- Total Cost: $200,000

- Estimated ARV: $300,000

- Max Loan based on 90% LTC: $200,000 * 0.90 = $180,000

- Max Loan based on 75% ARV: $300,000 * 0.75 = $225,000

- In this case, the lender would approve a loan up to $180,000, as it is the lower of the two calculations. You can use a fix and flip calculator to run these scenarios.

The Rehab Budget and Construction Draw Process

The portion of the loan allocated for renovations is not given to you in a lump sum at closing. Instead, it is held in an escrow account by the lender. You access these funds through a process called a "draw."

- Complete a Phase of Work: You (or your contractor) complete a portion of the renovation outlined in your initial Scope of Work (e.g., demolition and framing).

- Request a Draw: You submit a draw request to the lender for the cost of the completed work.

- Inspection: The lender sends an inspector (or uses a virtual/photo-based system) to verify that the work has been completed to a satisfactory standard.

- Funding: Once verified, the lender releases the funds from escrow to reimburse you for the work.

This process protects both the borrower and the lender by ensuring loan funds are used as intended and the project is progressing as planned.

Typical Loan Terms, Interest Rates, and Points

Loan Term: Typically short-term, ranging from 6 to 24 months, with 12 months being the most common.

Interest Rates: Rates are higher than conventional mortgages, reflecting the shorter term and higher risk. They can range from 9% to 15%+, depending on the lender, borrower experience, and market conditions. Most loans are interest-only, meaning you only pay the interest each month, with the full principal balance due at the end of the term (when you sell or refinance).

Points (Origination Fees): An upfront fee, typically 1-4% of the total loan amount, charged at closing.

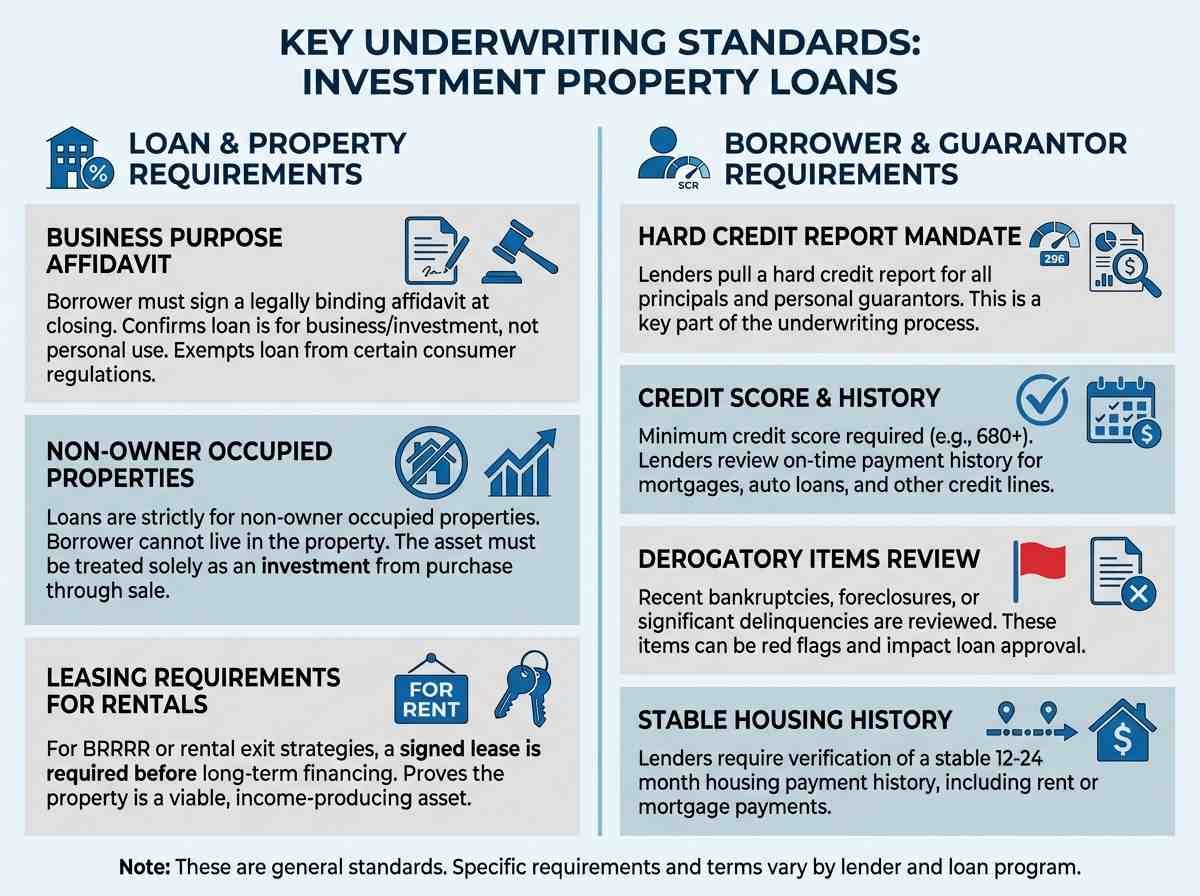

Key Underwriting Standards for Investment Properties

Fix and flip loans are for a specific business purpose, and lenders have strict standards to ensure they comply with regulations and mitigate risk. These loans are not for personal housing.

Business Purpose Affidavit Requirement

Every borrower must sign a "Business Purpose Affidavit" at closing. This is a legally binding document stating that the loan will be used exclusively for business or investment purposes (i.e., to renovate and sell for a profit or hold as a rental property) and not for personal, family, or household use. This declaration is critical for exempting the loan from certain consumer protection regulations like those outlined by the Consumer Financial Protection Bureau (CFPB).

Loan Eligibility for Non-Owner Occupied Properties

These loans are strictly for non-owner occupied properties. You cannot live in the property you are flipping using this type of financing, even for a short period during the renovation. The property must be treated solely as an investment asset from purchase through sale.

Leasing Requirements for Income-Producing Properties

If your exit strategy is to refinance into a long-term rental loan (the "BRRRR" method), the property must be leased to a qualified tenant before the long-term loan can be finalized. Lenders will require a copy of the signed lease agreement and often the first month's rent and security deposit to be in the bank. This proves the property is a viable, income-producing asset.

Borrower and Guarantor Credit Report Mandates

While the property is the primary collateral, the borrower's credit history is still a key part of underwriting. Lenders will pull a hard credit report for the borrowing entity's principals and any personal guarantors on the loan. They look for:

- Credit Score: A minimum score is usually required (e.g., 680+).

- Payment History: On-time payments for mortgages, car loans, etc.

- Derogatory Items: Recent bankruptcies, foreclosures, or significant delinquencies can be red flags.

- Housing History: Lenders want to see a stable housing payment history (rent or mortgage) for the past 12-24 months.

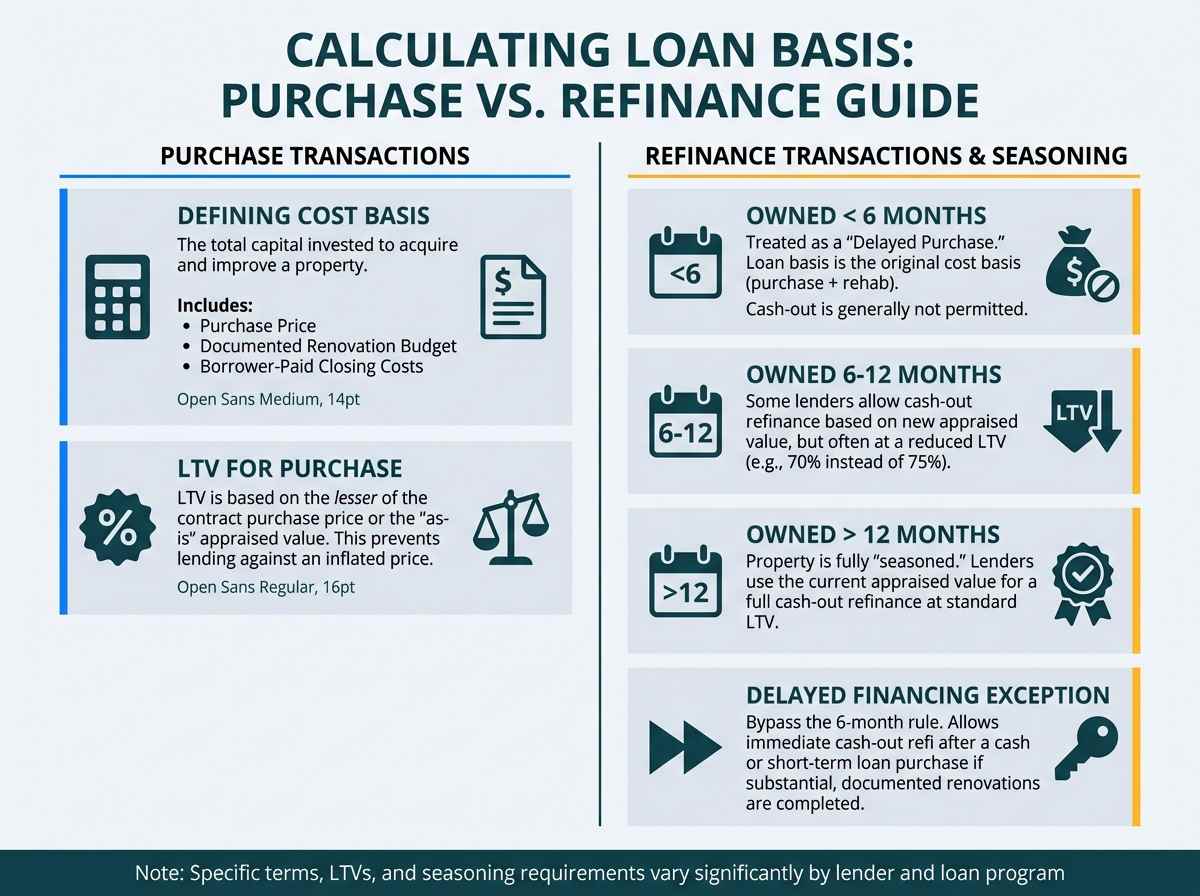

Calculating Loan Basis: LTV and Cost Basis Rules

How a lender calculates the basis for your loan depends on whether you are purchasing a new property or refinancing one you already own.

Defining Cost Basis: Purchase Price, Rehab Costs, Closing Fees

For a new purchase, the Cost Basis is the total amount of capital invested to acquire and improve the property. This includes:

- The contract purchase price.

- The documented renovation budget.

- Closing costs paid by the borrower at the time of purchase.

LTV for Purchase Transactions: Lesser of Price or Appraised Value

For a purchase, the lender will base the LTV on the lesser of the contract purchase price or the "as-is" appraised value. They do this to prevent lending against an inflated purchase price. For example, if you agree to buy a house for $200,000 but it only appraises for $190,000, the lender will use $190,000 as the value for their LTV calculation.

Seasoning Rules for Refinancing: 6 and 12 Month Thresholds

"Seasoning" refers to how long you have owned a property. Lenders have different rules for refinancing based on seasoning.

Owned less than 6 months: Most lenders will not allow a cash-out refinance. The loan will be treated as a "delayed purchase," with the loan basis being the original cost basis (what you paid for it + documented rehab).

Owned 6 to 12 months: Some lenders will allow a cash-out refinance based on the new appraised value, but often at a reduced LTV (e.g., 70% instead of 75%).

Owned over 12 months: The property is considered fully "seasoned." Lenders are generally comfortable using the current appraised value for a full cash-out refinance at their standard LTV.

Bypassing the 6-month seasoning requirement to accelerate capital velocity

The cornerstone of the Fast-Track method is leveraging the Delayed Financing Exception, a provision within conventional lending guidelines established by Fannie Mae. While many lenders are either unaware of this rule or unwilling to implement it, specialized lenders have built processes around it. This exception allows a borrower to execute a cash-out refinance immediately after purchasing a property with cash or a short-term loan (like a hard money loan), provided certain conditions are met. The key is proving that substantial renovations were completed, which justifies the new, higher appraised value. This turns a six-month cycle into a two- or three-month cycle, potentially tripling the number of deals an investor can complete in a year with the same pool of capital.

Cost Basis vs. Appraised Value for Properties Owned Under 12 Months

The key takeaway is that if you have owned a property for less than a year, your refinance loan amount will likely be based on your cost basis, not the new, higher appraised value. Lenders implement this rule to prevent investors from getting a loan based on a speculative value increase without having completed significant, value-add renovations.

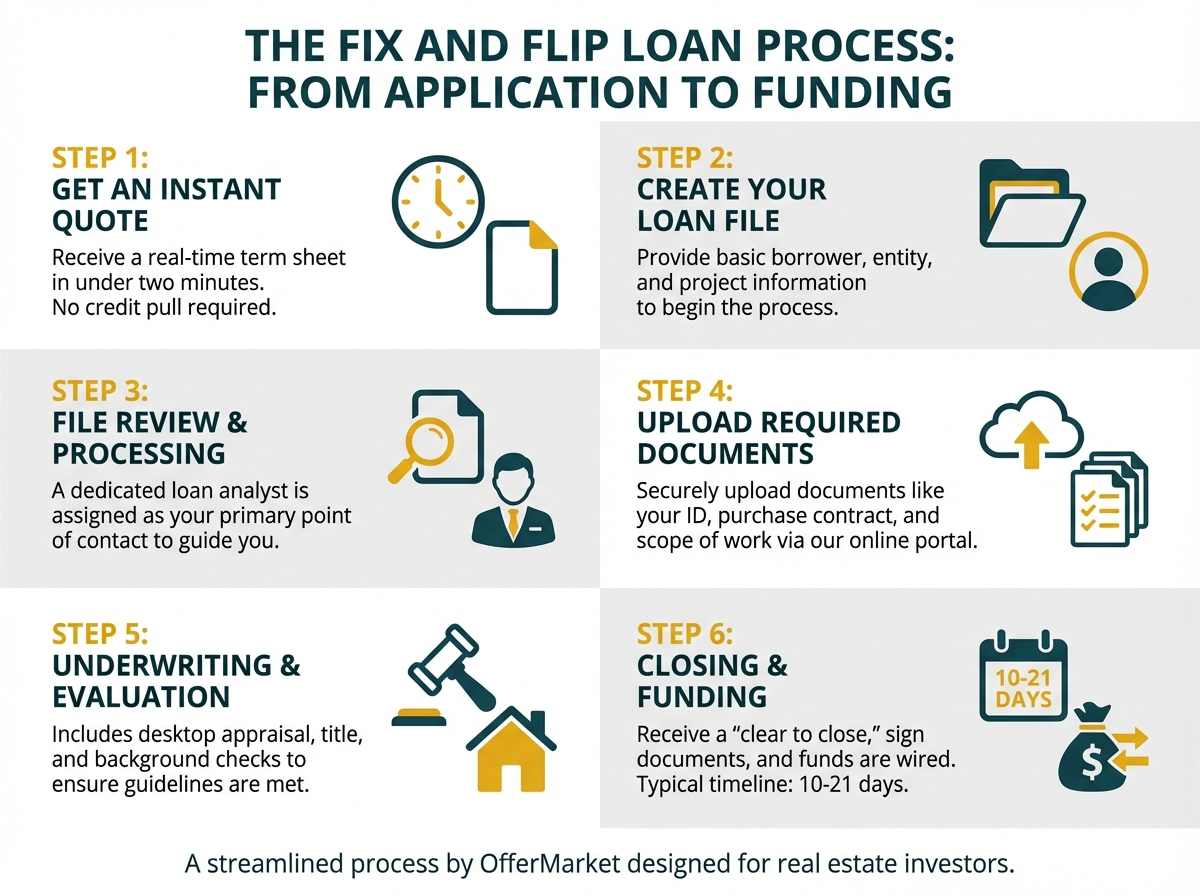

The Fix and Flip Loan Application and Funding Process

While each lender has its own nuances, the journey from application to funding generally follows a clear path. At OfferMarket, we've streamlined this process to maximize efficiency.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Closing and Funding

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

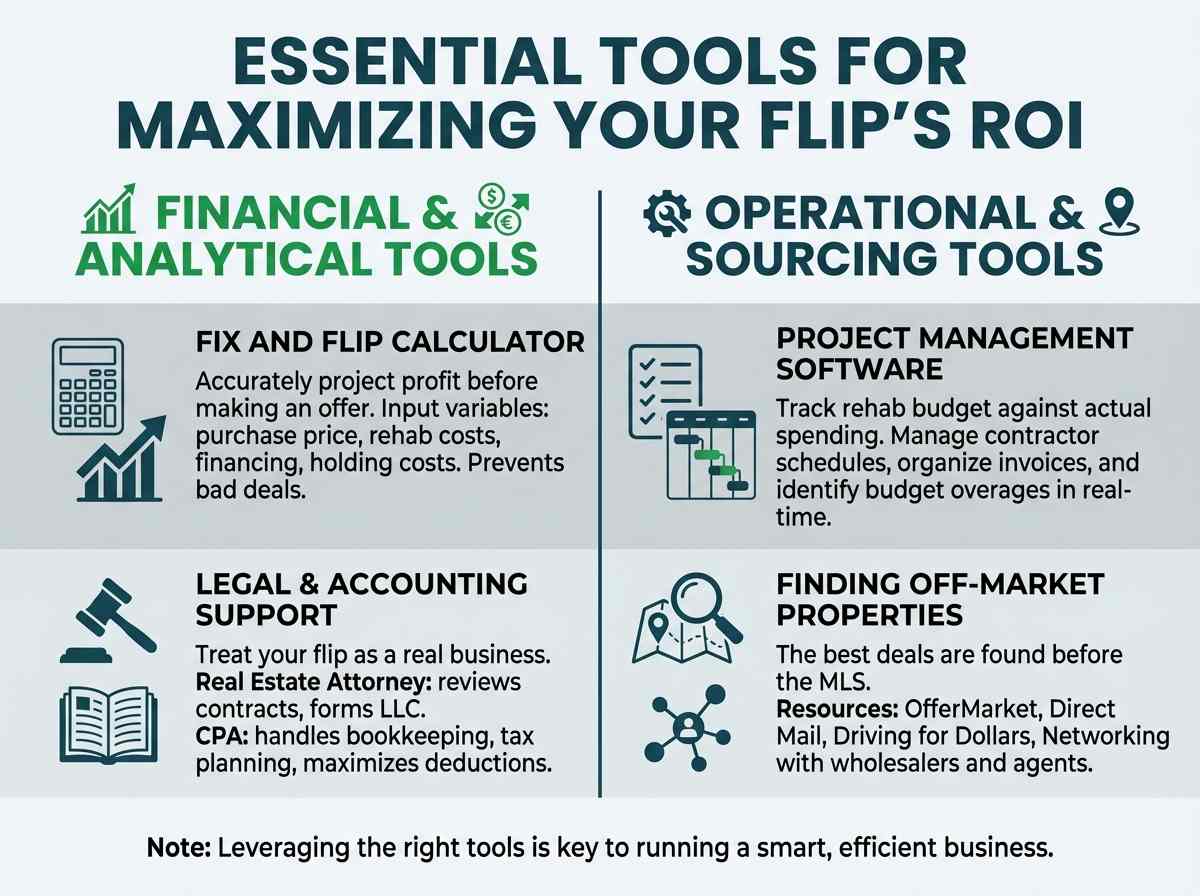

Essential Tools for Maximizing Your Flip's ROI

Successful flipping is about more than just construction; it's about running a smart, efficient business. Leveraging the right tools can significantly impact your bottom line.

Using a Fix and Flip Calculator to Analyze Deals

Before you even make an offer, you need to run the numbers. A comprehensive fix and flip calculator is your most important tool. It allows you to input all your variables—purchase price, rehab costs, financing terms, holding costs, and selling expenses—to accurately project your potential profit. This prevents you from entering into a bad deal and helps you structure your financing correctly.

Project Management Software for Tracking Rehab Budgets

A detailed rehab budget is useless if you don't track your actual spending against it. Project management tools like Trello, Asana, or specialized construction management apps can help you:

- Track expenses in real-time.

- Manage contractor schedules and deadlines.

- Keep all your receipts and invoices organized in one place.

- Quickly identify areas where you are over budget.

Resources for Finding Off-Market Properties

The best deals are often found before they hit the MLS. Building a network and using tools to find off-market properties is a key strategy for seasoned investors. Resources include:

- OfferMarket Marketplace: The Hub for Verified Deals: Unlike general listing sites, OfferMarket is a dedicated platform for distressed assets, wholesale deals, and turnkey rentals.

- Direct Mail Campaigns: Targeting absentee owners or homeowners in pre-foreclosure.

- Driving for Dollars: Identifying distressed properties in target neighborhoods.

- Networking: Building relationships with wholesalers, real estate agents, and attorneys.

- Online Platforms: Websites that aggregate auction, pre-foreclosure, and off-market listings.

Legal and Accounting Support for Your Business

Treat your flipping business like a real business. Having the right professional support is crucial for long-term success and protection.

- Real Estate Attorney: To review purchase contracts, form your LLC, and advise on legal matters.

- Accountant/CPA: To help you with bookkeeping, tax planning, and ensuring you are maximizing your deductions. As your business grows, their advice on tax strategy becomes invaluable. You can find qualified professionals through resources like the American Institute of CPAs (AICPA).

Get an Instant Quote for Your Next Project

In real estate investing, speed and reliable financing are your biggest competitive advantages. While other investors are waiting on slow lenders, you can be closing deals and starting your renovations.

See Your Personalized Rates and Terms in Minutes

Don't guess what your financing will cost. Use our simple online tool to get a transparent, no-obligation quote tailored to your specific project. You'll see your potential interest rate, loan amount, and required cash-to-close in minutes.

Leverage OfferMarket’s Speed to Secure Your Next Deal

With a process built on technology—from desktop appraisals to an app-based draw system—we can close your loan in as few as 10-21 days. This speed gives you the power to negotiate better terms with sellers and beat out competing offers that are contingent on slower, traditional financing.

Start the Application Process Online

Ready to fund your next flip? The first step is to get your instant quote. See for yourself how our streamlined, asset-based approach can help you scale your real estate investment business.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull