*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Everything You Need to Know About Hard Money Real Estate Loans

Hard money real estate loans are asset-based loans used by investors for short-term financing needs, typically for properties that are being renovated or stabilized. The primary criteria for approval are the property's value and the borrower's experience, rather than personal income or credit scores. This makes them an ideal tool for fix and flip or BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategies. The key to successfully using hard money is partnering with a lender that offers competitive terms, transparency, and a clear path to a long-term exit.

OfferMarket distinguishes itself by integrating technology with deep real estate expertise to provide investors with a superior lending experience. We focus on the metrics that directly impact your profitability: rate, leverage, and fees. By optimizing these components, we empower you to maximize your returns on every project.

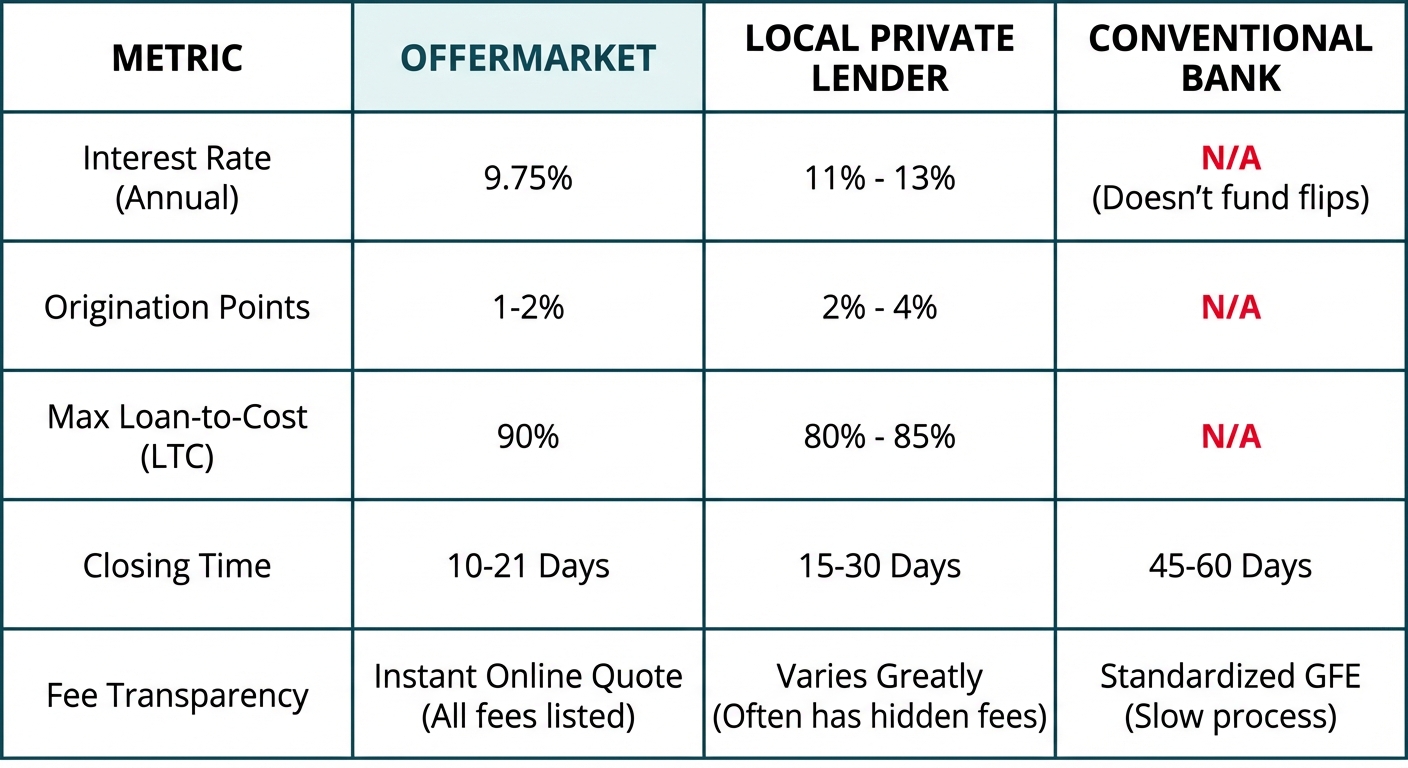

Lowest Rates and Highest Leverage Products

Your profit margin on a real estate deal is directly squeezed by financing costs. We engineer our loan products to be among the most competitive in the industry. By operating on a modern tech stack and maintaining lean operational overhead, we pass those savings on to you in the form of lower interest rates and origination fees. Furthermore, we offer aggressive leverage, providing up to 90% of the purchase price and 100% of the renovation costs. This high Loan-to-Cost (LTC) allows you to preserve your capital for future deals, scaling your investment portfolio faster. For example, on a $200,000 purchase with a $50,000 renovation budget, securing 90% LTC means you only need to bring $20,000 plus closing costs to the table, instead of the $50,000+ required by more conservative lenders.

The 1-Minute Instant Quote for Unmatched Transparency

The traditional hard money lending process is often a black box. You submit an application and wait days, or even weeks, for a vague term sheet that may hide exorbitant fees. We eliminate this uncertainty. Our 1-minute instant online quote provides a detailed, transparent breakdown of your interest rate, points, LTV, LTC, and all associated fees. This allows you to underwrite your deal with real numbers from the very beginning, ensuring your profit projections are accurate and achievable. There are no hidden "junk fees" or last-minute surprises at the closing table.

A Streamlined Tech Platform for Fast Closings

In real estate investing, speed is a competitive advantage. The ability to close quickly can be the deciding factor in winning a deal, especially in a competitive market. Our proprietary technology platform digitizes and automates much of the loan origination and underwriting process. From document submission to appraisal and title coordination, our system is designed for maximum efficiency. This allows us to consistently fund loans in as little as 10-21 days, compared to the 30-45 day timeline common with traditional banks.

Loan Products Specifically Designed for Flippers and BRRRR Investors

We are not a generalist lender. We are real estate investment specialists. Our fix and flip loans are structured to provide the high leverage and construction financing you need to execute a successful renovation. More importantly, we understand that for BRRRR investors, the hard money loan is just the first step. We have a seamless transition to our long-term DSCR (Debt Service Coverage Ratio) loan product, allowing you to refinance out of the short-term bridge loan and into a stabilized, cash-flowing rental property. This integrated approach prevents the common pitfalls that can trap investors in high-interest debt.

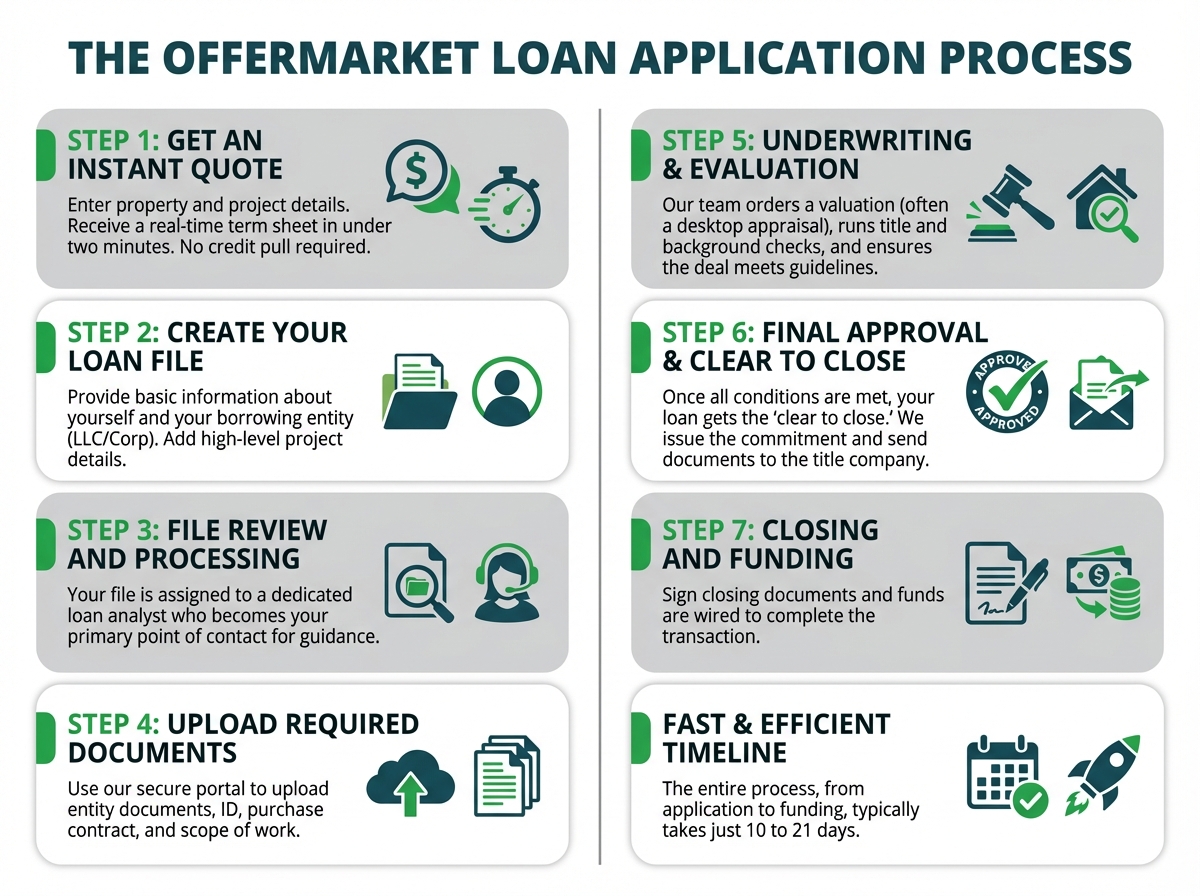

The OfferMarket Workflow: From Quote to Close

Our process is designed to be intuitive, transparent, and fast. We've eliminated the friction points and administrative hurdles common in traditional lending to get you from application to funding as quickly as possible.

Step 1: Get an Instant Online Quote for Your Project

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create a Loan File to See All Estimated Fees

Once you're satisfied with the initial quote, you can proceed to create a loan file within our secure online portal. This is where you'll upload necessary documentation, such as the purchase agreement, your entity documents (like an LLC operating agreement), and a detailed scope of work for the renovation.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

The Investor's Due Diligence Checklist for Hard Money Lenders

Choosing the right lending partner is one of the most critical decisions you'll make as a real estate investor. While a low advertised interest rate might be tempting, it's only one piece of the puzzle. A thorough investigation requires a holistic analysis of a lender's terms, processes, and expertise. Use this checklist to systematically evaluate and compare potential hard money lenders.

Analysis of Interest Rates, Points, and Origination Fees

The total cost of a loan is more than just the interest rate. You must analyze the three core components of loan pricing:

- Interest Rate: The annualized cost of borrowing the money, paid in monthly installments.

- Points (or Origination Fees): An upfront fee charged by the lender to process the loan, calculated as a percentage of the total loan amount. One point equals 1% of the loan amount.

- Other Fees: These can include processing fees, underwriting fees, legal fees, and administrative charges.

A lender might advertise a very low interest rate but compensate with high points or a dozen smaller "junk fees." Always demand a term sheet that clearly itemizes every single cost. The best way to compare offers is to calculate the total loan cost over your expected holding period. A loan with a 10% rate and 1 point might be cheaper for a 6-month project than a loan with a 9% rate and 3 points. Use an ARV calculator to model these different scenarios and see their impact on your net profit.

Comparing Leverage: LTV, LTC, and ARV Metrics

Leverage is a measure of how much of the project's total cost the lender is willing to finance. Understanding the key metrics is crucial:

Loan-to-Value (LTV): The loan amount as a percentage of the property's current appraised value. This is more relevant for refinances or purchases without a renovation component.

Loan-to-Cost (LTC): The loan amount as a percentage of the total project cost (purchase price + renovation budget). This is the most important metric for fix and flip investors. Higher LTC means less cash out of your pocket.

After Repair Value (ARV): The estimated market value of the property after all renovations are complete. Lenders will typically cap their total loan amount at 70-75% of the ARV to ensure they have a protective equity cushion.

When comparing lenders, ask for their maximum LTC and their maximum loan-to-ARV. A lender offering 90% LTC but capping the loan at 65% of ARV may not be as attractive as one offering 85% LTC but going up to 75% of ARV. The optimal structure depends on the specifics of your deal.

Evaluating Speed and Certainty of Execution

In the world of off-market deals and real estate auctions, the ability to close quickly and reliably is paramount. A "proof of funds" letter from a reputable hard money lender can give your offer a significant advantage over those contingent on slow, conventional financing.

When evaluating a lender, ask about their typical closing time. Can they close in under 2-3 weeks? Ask for references from other investors who have recently closed loans with them. A lender's certainty of execution is their promise to fund the deal as agreed upon, without last-minute changes to the terms or surprise requirements. A lender who is not a direct source of capital but rather a broker may add delays and uncertainty to the process.

Demanding Full Transparency on All Fees and Loan Terms

A trustworthy lender provides a clear, easy-to-understand term sheet and closing statement. Scrutinize these documents for any vague or hidden fees.

Common red flags include:

- High "processing" or "underwriting" fees.

- Prepayment penalties that punish you for finishing your project ahead of schedule.

- Expensive extension fees if your project runs longer than expected.

- Unreasonable draw inspection fees.

A transparent lender like OfferMarket will provide an itemized list of all costs upfront, allowing you to underwrite your deal with confidence.

Lender Specialization in Fix and Flip, BRRRR, and Construction

Real estate investing is not one-size-fits-all. A lender who primarily finances stabilized commercial buildings will not understand the unique needs and timelines of a fix and flip project. Partner with a lender who specializes in investment property financing. They will have a deeper understanding of renovation budgets, draw schedules, and the appraisal process for distressed properties.

Crucially, if your strategy is BRRRR, you need a lender who not only provides the initial bridge loan but also has a seamless, in-house refinance program, like a DSCR loan, to help you transition to long-term financing. This vertical integration is a massive strategic advantage.

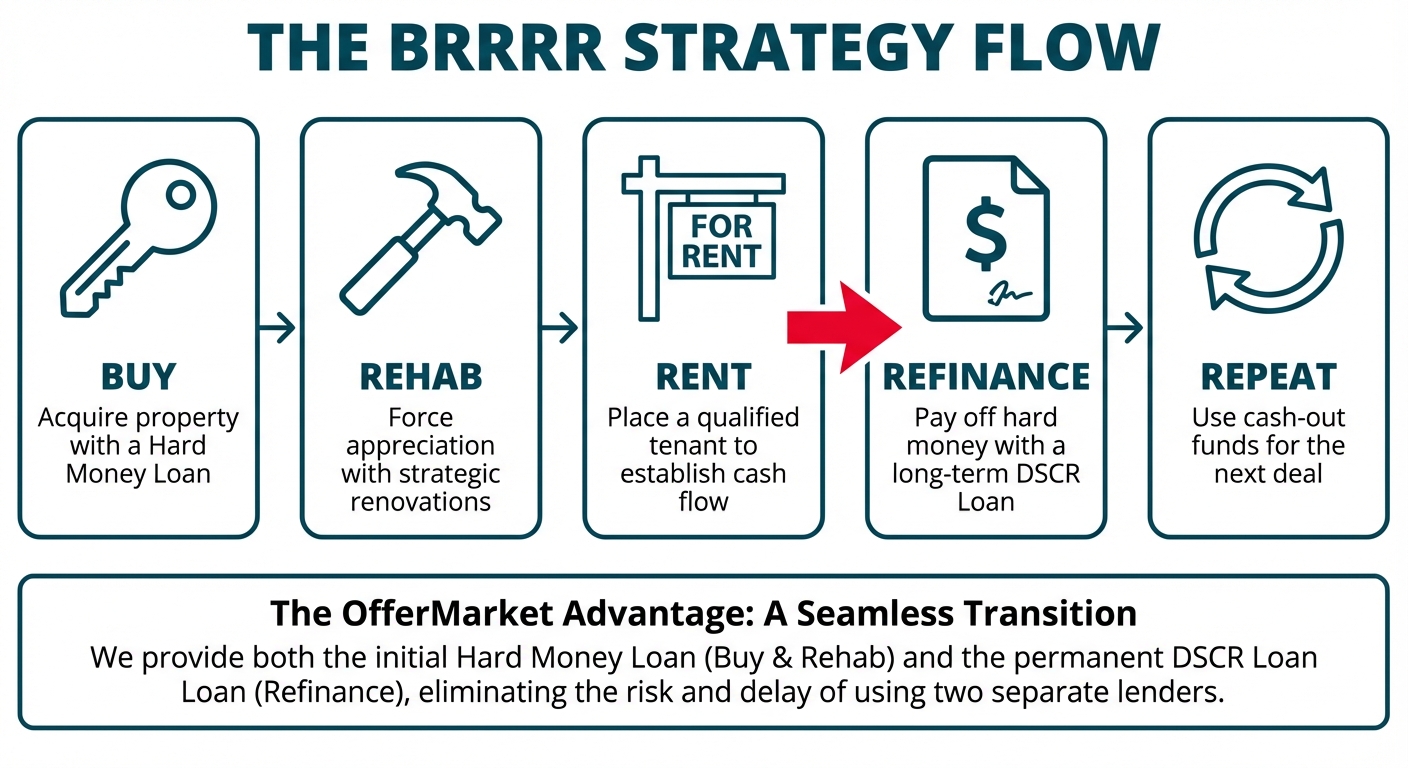

Mastering the BRRRR Strategy: The Critical Refinance Phase

The BRRRR method is a powerful wealth-building strategy, but its success hinges entirely on the final "R": the Refinance. This is the moment you transition from a short-term, high-interest hard money loan to a long-term, lower-cost, fixed-rate mortgage, pulling out the capital you invested to use on your next deal. Mismanaging this step can derail the entire strategy.

The Goal: Transitioning from Short-Term to Long-Term Debt

The hard money loan is a tool to acquire and renovate the property quickly. It's the bridge that gets you from a distressed asset to a stabilized, income-producing one. The goal of the refinance is to pay off that expensive bridge loan and replace it with permanent financing. An ideal refinance accomplishes two things:

Recoups Capital: It allows you to do a "cash-out" refinance based on the new, higher appraised value (the ARV), returning your initial down payment, closing costs, and sometimes even a portion of your profit.

Secures Cash Flow: It locks in a low, fixed interest rate for 30 years, ensuring the property's rental income comfortably covers the new mortgage payment (PITIA) and other operating expenses, generating positive monthly cash flow.

OfferMarket's Seamless DSCR Refinance Advantage

The most significant risk in the BRRRR strategy is using two different, disconnected lenders for the acquisition and the refinance. The hard money lender who funded your purchase may not offer long-term rental loans, forcing you to shop for a new lender at a critical time. This new lender will have to start from scratch, re-underwriting the entire deal, which can cause delays and uncertainty.

OfferMarket eliminates this risk by offering a vertically integrated lending platform. We provide the initial hard money loan for the acquisition and rehab and then seamlessly transition you into our own DSCR loan for the long-term hold. Because we've been with you from the start, we already have your entity documents, financial information, and property details. This makes the refinance process faster, smoother, and more reliable.

The Risks of a Disconnected Lending Process

When your hard money lender doesn't offer a DSCR refinance, you introduce significant risk into your project. You might finish your renovation and have a tenant in place, only to find out that you don't qualify for a refinance with a new lender due to a different set of underwriting guidelines. This can force you to:

Extend your hard money loan: This means paying high interest rates (e.g., 12-14%) and expensive extension fees for several more months while you search for a new lender.

Accept unfavorable terms: In a desperate situation, you may be forced to take a refinance loan with a higher rate, lower leverage, or a prepayment penalty.

Sell the property: In the worst-case scenario, if you cannot secure a refinance, you may have to sell the property, forfeiting the long-term cash flow and appreciation that was the entire point of the BRRRR strategy.

Underwriting Shift: From After Repair Value to In-Place Cash Flow

This is the most misunderstood aspect of the BRRRR process. The two loans are underwritten on completely different principles.

Hard Money Loan (The "Buy"): This is an asset-based loan. The lender's primary concern is the After Repair Value (ARV). They ask: "If the borrower defaults, can we take the property, finish the renovation, and sell it for a profit?" Your personal income is secondary; the value of the deal is paramount.

DSCR Loan (The "Refinance"): This is a cash-flow-based loan. The lender's primary concern is the Debt Service Coverage Ratio (DSCR). They ask: "Does the property's monthly rental income cover the proposed new mortgage payment?" They calculate this using the formula: DSCR = Monthly Rent / Monthly PITIA (Principal, Interest, Taxes, Insurance and HOA). A DSCR above 1.20x is typically required for the best terms. The ARV is still important for LTV purposes, but a high value cannot save a deal with negative cash flow.

Failing to plan for this fundamental shift in underwriting is what traps investors. The next section details the specific pitfalls that arise from this disconnect.

Critical Pitfalls: Navigating the Fix and Flip to DSCR Loan Transition

The transition from a short-term fix and flip loan to a long-term DSCR loan is where many BRRRR strategies fail. While the hard money loan focuses on the property's potential value (ARV), the DSCR loan is ruthlessly focused on its current, verifiable income and condition. Understanding and planning for the DSCR lender's stringent underwriting requirements before you even buy the property is the key to a successful and repeatable BRRRR process. Here are the seven most common traps and how to avoid them.

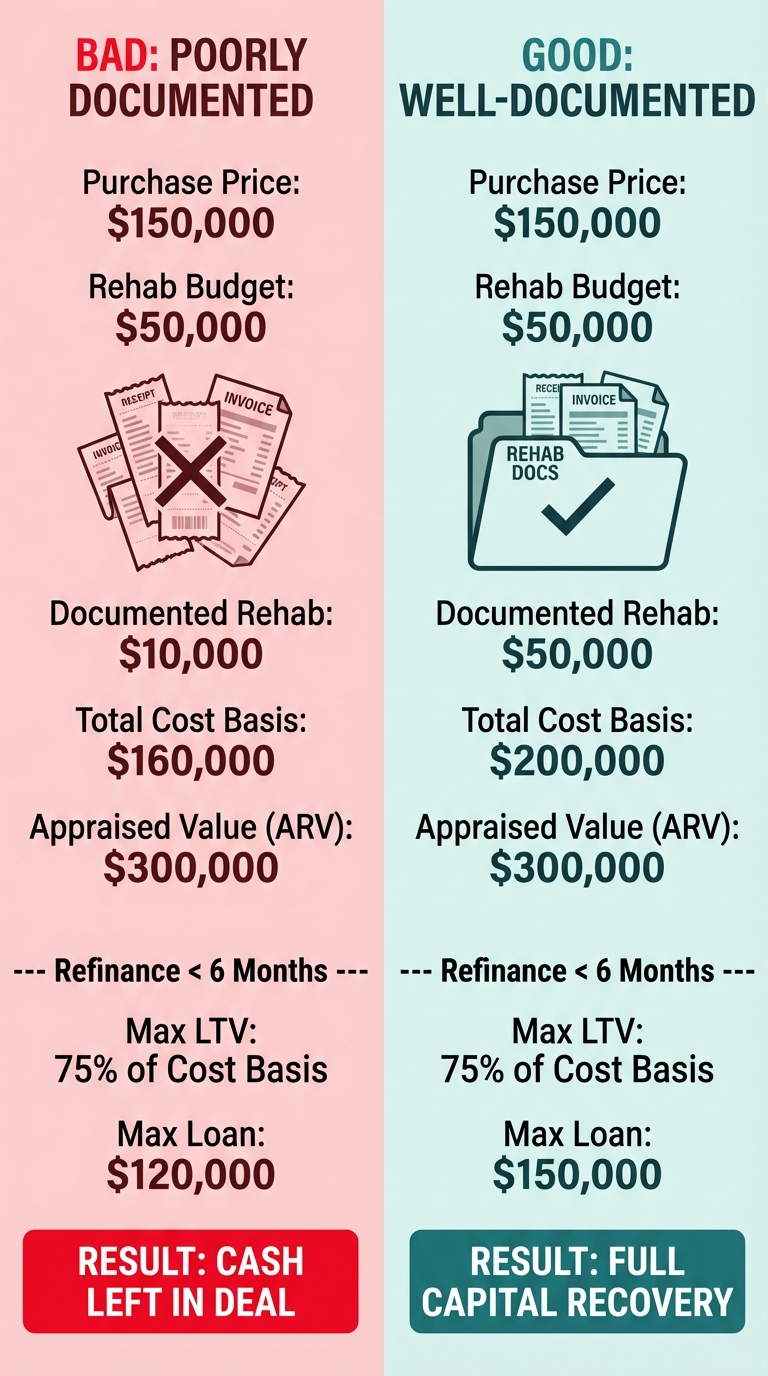

1. The 6-Month Seasoning and Cost Basis Trap

Many DSCR lenders have a "seasoning" requirement. If you attempt to do a cash-out refinance on a property you've owned for less than six months, they will cap the new loan amount based on your cost basis (purchase price + documented renovation costs), not the new, higher appraised value.

The Pitfall: This rule is designed to prevent fraudulent property flips with inflated appraisals. If you bought a property for $150,000, spent $50,000 on renovations, and it now appraises for $300,000, you've created $100,000 in equity. However, if you refinance at month four and can only provide receipts for $30,000 of the rehab, your documented cost basis is only $180,000 ($150k + $30k). The lender will cap your loan at 75% of this $180,000 basis ($135,000), not 75% of the $300,000 appraised value ($225,000). This prevents you from pulling your cash out and kills the "Repeat" step of the BRRRR method.

Actionable Advice: Keep meticulous records of every single project expense. Use a dedicated business bank account or credit card. Get detailed invoices and receipts from every contractor and supplier. This documentation is non-negotiable proof of your increased cost basis, allowing you to access the equity you've created. Alternatively, plan your project timeline to exceed the six-month seasoning period.

2. The Unleased Vacant Property Haircut

DSCR lenders view vacant properties as higher risk. To mitigate this, they apply a mandatory LTV reduction, often 5%, for any property that is not leased at the time of the refinance application. For example, the maximum LTV might drop from 80% to 75%.

The Pitfall: The penalty is twofold. Not only is the LTV reduced, but the income used to calculate the DSCR is also penalized. Instead of using the full market rent estimated by the appraiser, the lender will only give you credit for 75-90% of that amount. If the appraiser estimates rent at $2,000/month, the lender may only use $1,500 ($2,000 x 75%) in their DSCR calculation. This lower income figure can easily push your DSCR below the required threshold (typically 1.20x), jeopardizing the entire refinance or forcing you into a lower leverage loan with a sub-1.00x DSCR penalty.

Actionable Advice: Do not apply for the DSCR refinance until you have a signed lease agreement and a security deposit in hand. The ideal scenario is to have the tenant already moved in. This provides the lender with concrete, verifiable income, allowing you to qualify for the highest possible leverage and the best terms.

3. The Short-Term Rental (STR) Documentation Trap

Many investors purchase properties intending to operate them as high-income short-term rentals (e.g., Airbnb, Vrbo). However, to use this higher STR income for DSCR qualification, most lenders require a verifiable 12-month track record of revenue for that specific property.

The Pitfall: If you just completed a renovation, you won't have this 12-month history. The lender will then default to using the much lower long-term market rent for their underwriting. A property that generates $6,000/month as an STR might only command $3,000/month as a traditional rental. If your loan payment is based on the higher value created for an STR, using the lower LTR income will likely result in a DSCR well below 1.00x, killing the deal. Furthermore, even with a track record, lenders apply a significant "expense haircut" (often 20% or more) to gross STR income to account for management, vacancies, and operating costs.

Actionable Advice: If your exit strategy relies on STR income, you must plan for a 12-month seasoning period after renovation. Alternatively, ensure the deal also works based on long-term rental rates. You can use a tool like AirDNA to get revenue estimates, but be aware that lenders will require actual performance history, not just projections.

4. The 100% Complete Property Condition Trap

DSCR loans are for stabilized, rent-ready properties. Appraisers for these loans assign a condition rating from C1 (new) to C6 (uninhabitable). To qualify for a DSCR loan, the property must typically have a rating of C4 ("average condition with some minor deferred maintenance") or better.

The Pitfall: Unlike hard money loans, DSCR loans do not have a mechanism for construction or repair holdbacks. The property must be 100% complete at the time of the final appraisal. A small, seemingly insignificant issue—like a missing appliance, uninstalled light fixtures, or a patch of unpainted wall—can lead the appraiser to give a C5 rating or make the appraisal "subject to completion" of these items. This will halt the entire refinance process until you complete the work out-of-pocket and pay for a re-inspection.

Actionable Advice: Before ordering the refinance appraisal, conduct your own final walkthrough and create a detailed punch list. Ensure every item from your scope of work is complete. Take photos of the finished kitchen, bathrooms, and mechanicals. Providing the appraiser with a fully finished and clean property is the surest way to get a clean C1-C4 rating and a smooth closing.

5. The Sub-1.00x DSCR Penalties

While most lenders target a DSCR of 1.20x or higher, some will allow a loan to close with a DSCR below 1.00x (meaning the rent does not fully cover the mortgage payment). However, this comes with severe penalties.

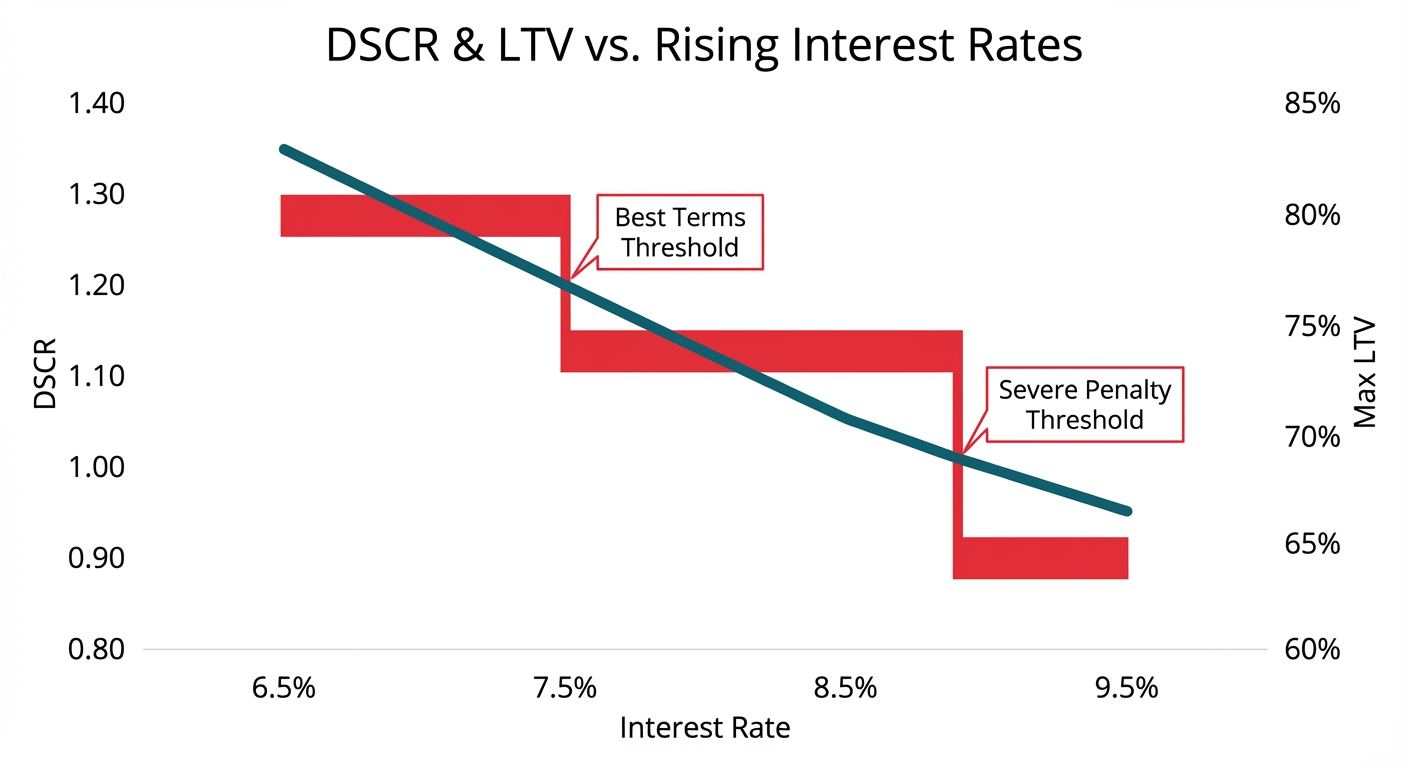

The Pitfall: A sub-1.00x DSCR triggers a cascade of negative consequences. First, the LTV is typically capped at a much lower level, such as 65-70%, forcing you to leave a significant amount of cash in the deal. Second, you will be required to bring a substantial liquidity reserve to closing, often 6-12 months of PITIA payments, held in an escrow account. Third, you are usually forbidden from using STR income to qualify or having the property be vacant. This trap is especially dangerous in a rising interest rate environment. A deal that underwrote perfectly at a 1.25x DSCR when you started the rehab could easily fall to 0.95x DSCR if rates rise by 1-2% during your 6-month project.

Actionable Advice: Be conservative in your initial analysis. Use a DSCR calculator to stress-test your deal against higher potential interest rates. If your deal only works with today's best-case-scenario rates, it's a risky project. Aim for a projected DSCR of 1.40x or higher to build a buffer against market fluctuations.

6. The First-Time Investor Exclusion

Lenders view first-time investors as inherently riskier. To mitigate this risk, they impose stricter underwriting guidelines on borrowers who have not completed a certain number of projects (typically 1-3) in the last 24-36 months.

The Pitfall: If you are a first-time investor, you will likely face a lower maximum LTV, often capped at 75% even on a cash-out refinance. You will almost certainly be forbidden from using projected STR income to qualify and will not be eligible for programs that allow for a sub-1.00x DSCR. This makes the BRRRR strategy more capital-intensive for new investors, as they will be unable to pull out 100% of their initial investment.

Actionable Advice: New investors should underwrite their deals more conservatively, planning to leave some cash in the property after the refinance. Partnering with an experienced investor on your first few deals can provide access to better financing terms and invaluable mentorship. Build a track record of successful projects to graduate to the more favorable terms offered to seasoned professionals.

7. Entity and Title Continuity Traps

DSCR loans are commercial loans made to a business entity, not an individual. The borrowing entity (usually an LLC) must be in good standing with the state, and the title to the property must have a clear and logical chain.

The Pitfall: Several issues can arise here. If you buy the property in your personal name and then try to transfer it to an LLC right before the refinance (a "quitclaim deed"), some lenders will flag this as a violation of title continuity and restart the seasoning clock. If your LLC is not in "good standing" (e.g., you failed to file an annual report), it can delay or kill the loan. Furthermore, all principal owners of the LLC must provide a full-recourse personal guaranty. If you have a partner whose credit score has dropped or who has had a recent credit event (like a bankruptcy or foreclosure), it can negatively impact the application for the entire entity.

Actionable Advice: From the very beginning, purchase the property in the name of a dedicated, single-purpose business entity (like an LLC) that will hold the title throughout the life of the loan. Ensure this entity remains in good standing. Thoroughly vet all partners on a deal, understanding that their financial standing is tied to yours for the purpose of the loan guaranty. Consult with a real estate attorney to ensure your entity is structured correctly, as outlined by legal resources like Nolo.

Your Strategic Next Step: Diagnose Your Deal with OfferMarket

Navigating the complexities of hard money and DSCR lending requires a partner who offers not just capital, but clarity. The pitfalls are real, but they are also avoidable with the right tools and a transparent lending process. By understanding the underwriting requirements for your exit strategy before you even make an offer, you transform a speculative risk into a calculated investment.

Get Your 1-Minute Instant Quote for Fix and Flip or Construction

Stop relying on vague estimates and outdated term sheets. Start your analysis with real, transparent numbers. Our instant quote tool gives you a comprehensive breakdown of the rates, points, and fees for your specific project, allowing you to underwrite with confidence.

Use OfferMarket Calculators to Analyze Deal Profitability

Stress-test your assumptions. How will a change in interest rates affect your DSCR? What is the true ARV needed to hit your profit target? Our free online calculators are designed to help you answer these critical questions.

- Analyze your cash flow with the DSCR Loan Calculator

- Estimate your profit with the Fix and Flip Calculator

Run a Diagnostic on Your Current Project for a DSCR Refinance

If you're currently in a hard money loan and nearing the end of your renovation, now is the time to plan your exit. Use our DSCR quote tool to see the long-term financing options available to you and ensure a smooth transition out of your short-term debt.

Secure Your Next Loan with Speed and Transparency

In real estate investing, the right financing is your most powerful tool. Partner with a lender that combines institutional-grade products with the speed and innovation of a technology company. At OfferMarket, we provide the capital and clarity you need to scale your portfolio.

OfferMarket Loans

Check your rate

60 seconds · no credit pull