*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Hard Cash Loans: A Real Estate Investors Guide

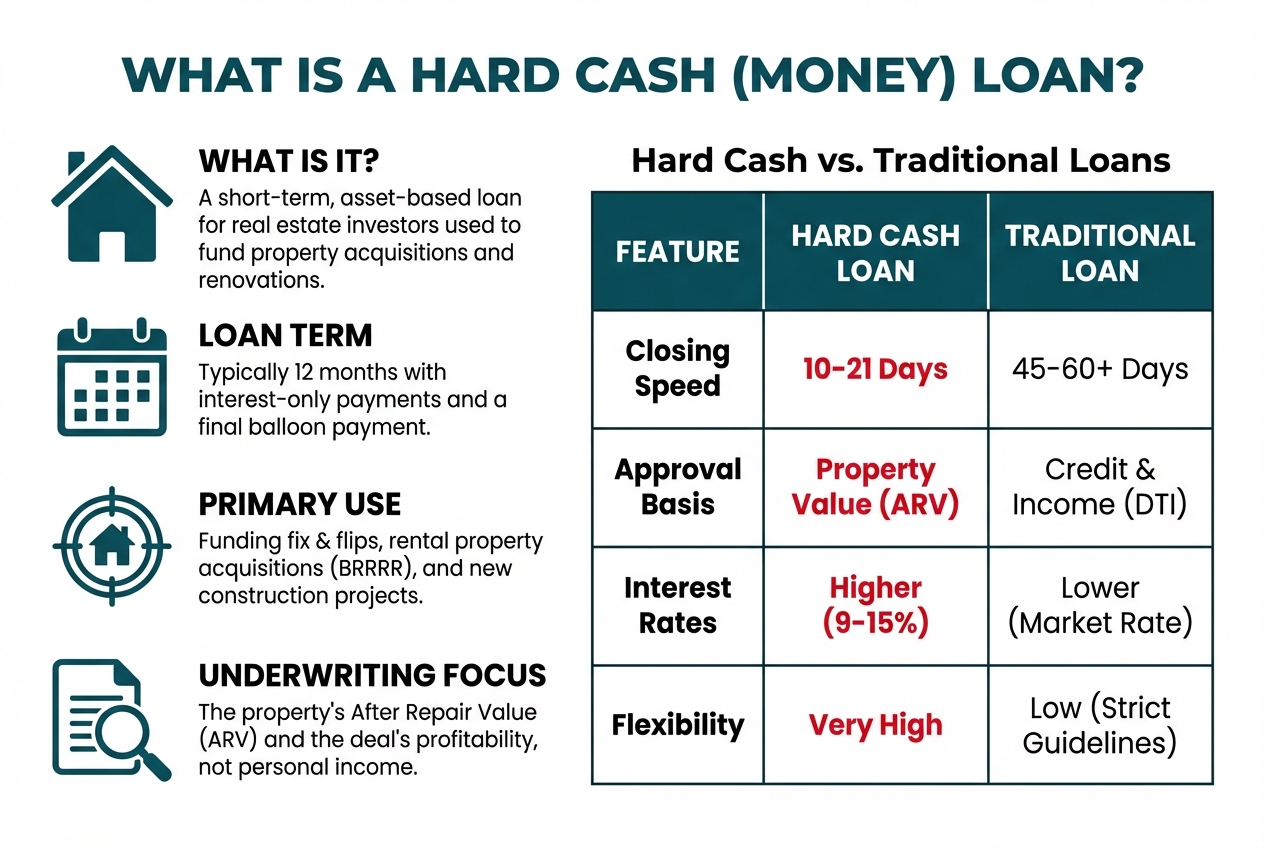

A hard cash loan, more commonly known as a hard money loan, is a short-term, non-conforming loan secured by real estate. Unlike traditional mortgages that are underwritten based on a borrower's creditworthiness and income, hard cash loans are asset-based. This means the lender's primary consideration is the value of the property (the "hard" asset) that serves as collateral. These loans are almost exclusively used by real estate investors for the acquisition and renovation of investment properties, particularly those that are distressed and would not qualify for conventional financing.

The two main categories for this type of financing are Fix & Flip loans, designed for properties that will be renovated and sold quickly, and Bridge loans, which provide short-term financing to "bridge" a gap until a long-term solution like a sale or conventional refinance is secured. The core principle is that the underwriting focuses on the economic viability of the real estate deal itself—its purchase price, renovation budget, and After Repair Value (ARV)—rather than the borrower's personal financial statements. This asset-centric model allows for significantly faster funding, enabling investors to capitalize on time-sensitive opportunities in a competitive market.

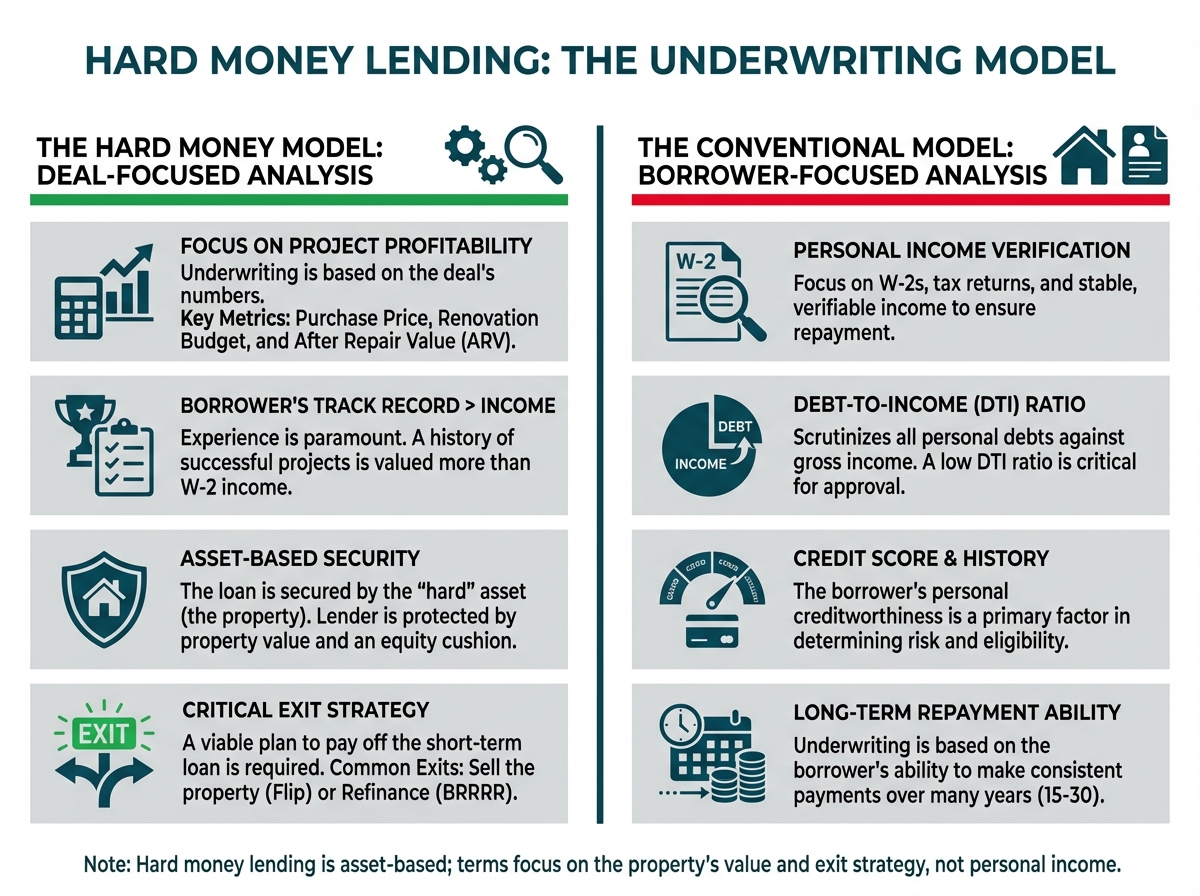

The Core Underwriting Model: The Deal vs. The Borrower

The fundamental difference between hard cash lending and conventional banking lies in the underwriting philosophy. Traditional lenders, like banks and credit unions, follow a borrower-centric model. They scrutinize your personal financial health, focusing on metrics like your credit score, debt-to-income (DTI) ratio, and verifiable income (W-2s, tax returns). Their primary concern is your personal ability to repay the loan over a long period.

Hard cash lending flips this model on its head. It is an asset-based lending approach where the deal, not the borrower, is the star of the show.

Focus on Project Profitability

A hard money lender's first question isn't "What's your income?" but "What's the deal?" They underwrite the loan based on the potential profitability of the investment project. The key components they analyze are:

- Purchase Price: The price you are paying for the property.

- Renovation Budget: A detailed breakdown of the costs to improve the property.

- After Repair Value (ARV): The projected market value of the property after all renovations are complete. This is the most critical number in the entire equation.

The lender's goal is to determine if there is a sufficient profit margin to ensure the loan can be repaid upon the sale or refinance of the property. Their risk is secured by the asset, so they need to be confident in its value.

Borrower's Track Record Over Personal Income

While personal income is not the primary focus, the borrower's experience is paramount. Lenders want to see a demonstrated track record of successfully completing similar projects. A borrower with a history of profitable flips is seen as a much lower risk than a complete novice. This experience is often more valuable to a hard money lender than a high W-2 income. An experienced investor knows how to manage a budget, hire contractors, and navigate the renovation process, which directly impacts the project's success and the lender's security.

Asset-Based Lending: The "Hard" Asset Secures the Loan

The term "hard money" comes from the fact that the loan is secured by a "hard" asset—the physical real estate. If the borrower defaults, the lender can foreclose on the property to recoup their investment. This is why the property's value, particularly its ARV, is so heavily scrutinized. The loan amount is calculated as a percentage of the property's value, creating an equity cushion that protects the lender. If the ARV is $300,000 and the lender's maximum loan is 75% of that ($225,000), there is a $75,000 equity cushion protecting their capital.

Exit Strategy Analysis

A hard cash loan is a short-term solution. Therefore, a critical part of the underwriting process is a thorough analysis of the borrower's exit strategy. The lender must be convinced that the borrower has a viable and realistic plan to pay off the loan's balloon payment at maturity (typically in 12 months). The two most common exit strategies are:

- Sale of the Property: The investor sells the renovated property on the open market, using the proceeds to pay off the hard money loan and realize their profit. This is the standard exit for a fix-and-flip project.

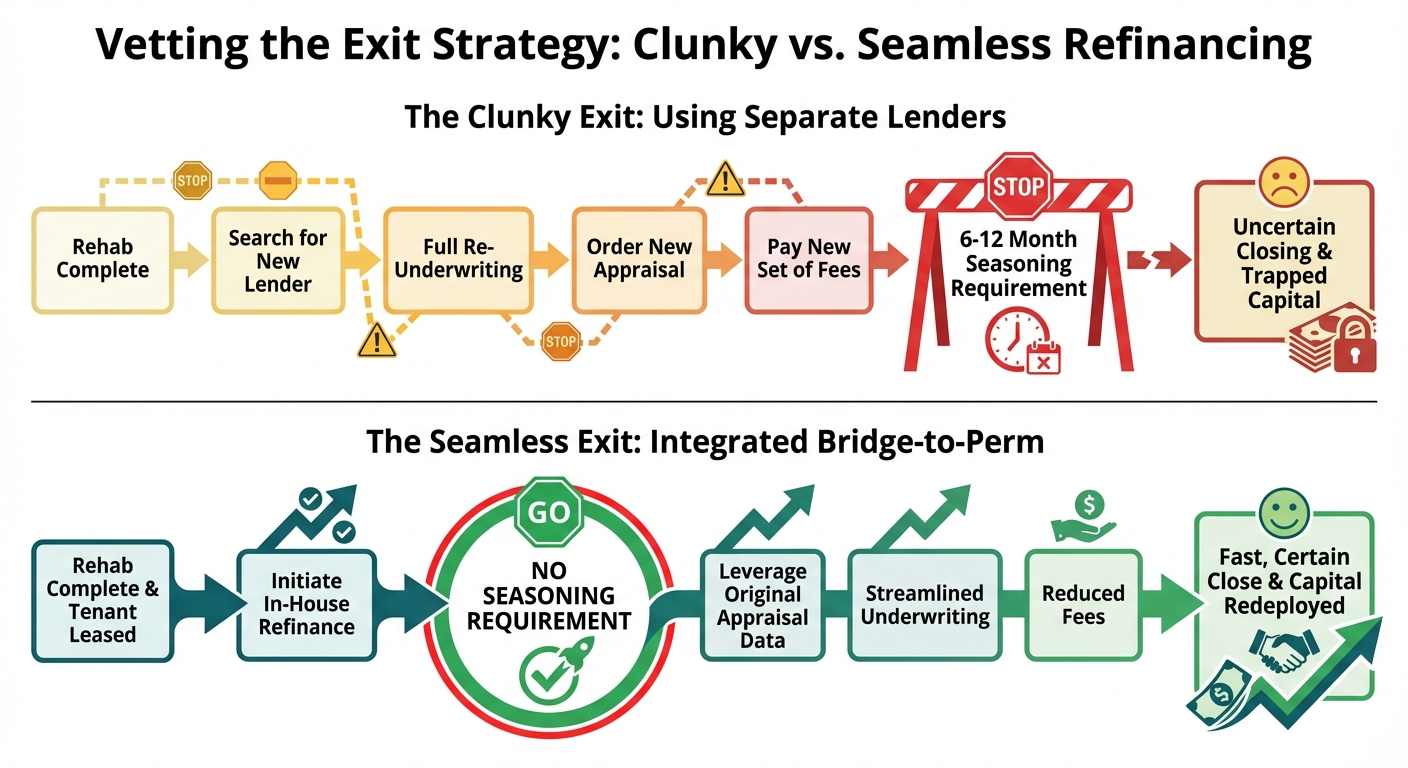

- Refinance into a Long-Term Loan: The investor refinances the hard money loan into a traditional, long-term mortgage, such as a DSCR loan for a rental property. This is the cornerstone of the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

The lender will assess the local market conditions, comparable sales, and rental demand to verify that the proposed exit strategy is achievable within the loan term.

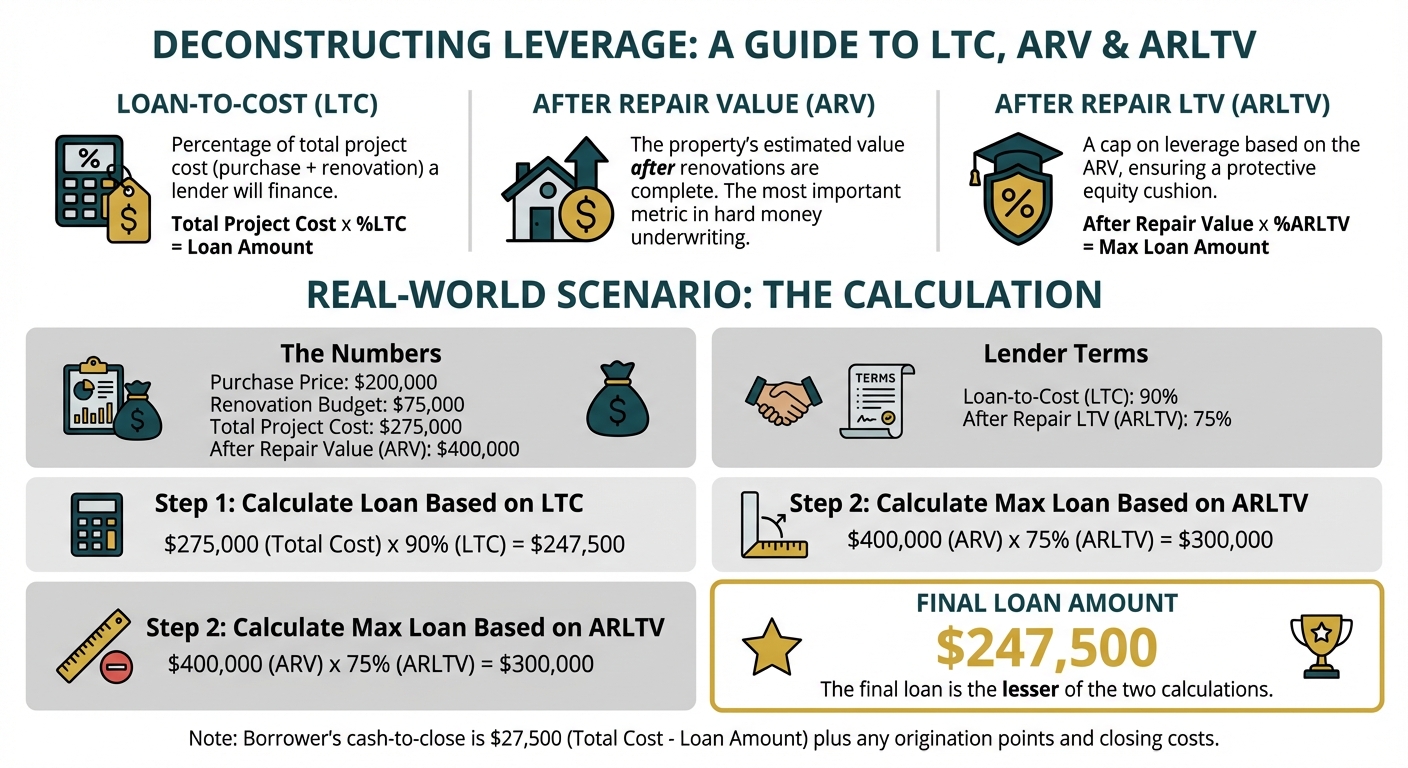

Deconstructing Leverage: LTC, ARV, and the Capital Stack

Leverage is the use of borrowed capital to increase the potential return of an investment. In hard cash lending, leverage is defined by a few key acronyms that every investor must understand: LTC, ARV, and ARLTV. These metrics determine how much money a lender will provide and how much cash the borrower needs to bring to the closing table.

Loan-to-Cost (LTC)

Loan-to-Cost (LTC) is the percentage of the total project cost that the lender is willing to finance. The total project cost is the sum of the property's purchase price and the total renovation budget.

Formula: Initial Loan Amount / Purchase Price

For example, if an investor is buying a property for $150,000 and has a renovation budget of $50,000, the total project cost is $200,000. If the lender offers 90% LTC, the loan amount would be $180,000. The remaining 10% ($20,000) plus closing costs would be the borrower's required cash-to-close.

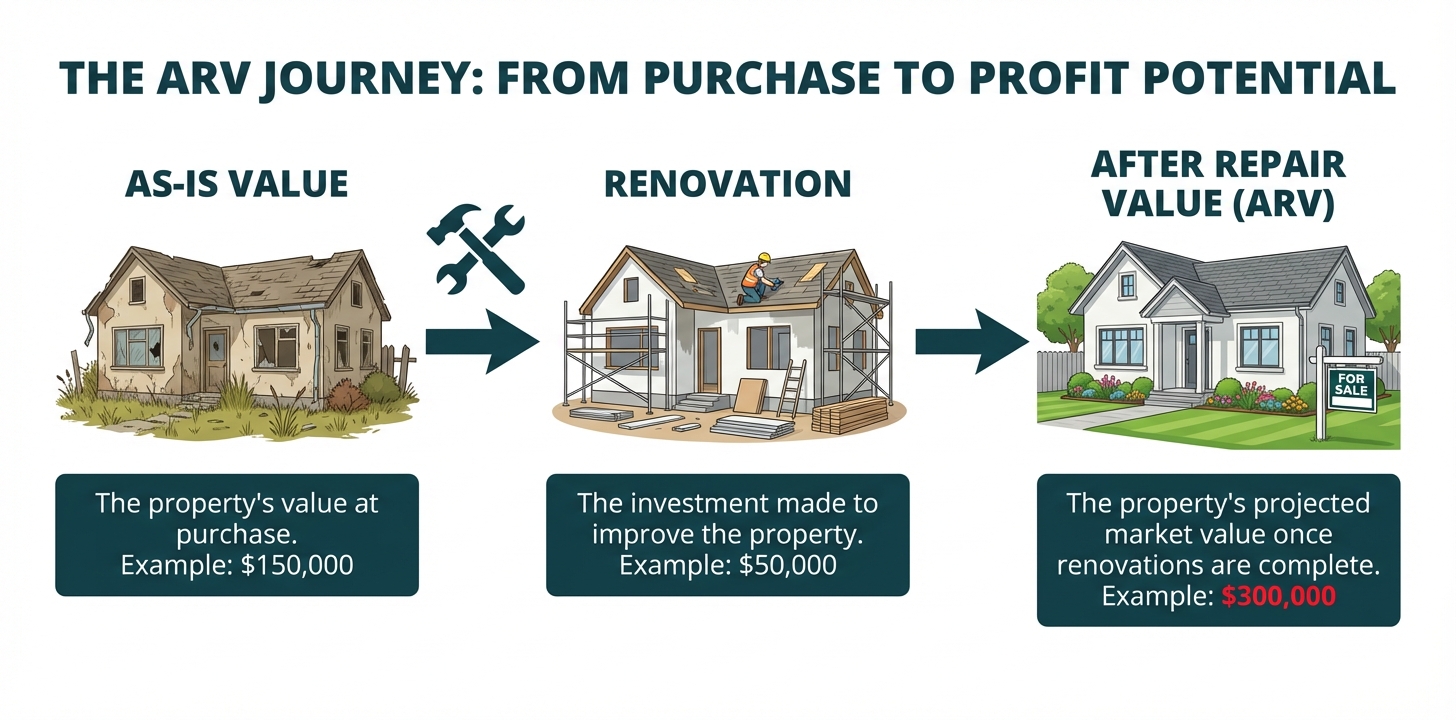

After Repair Value (ARV)

After Repair Value (ARV) is the estimated value of the property after all proposed renovations are completed. This value is determined by a professional appraiser who analyzes comparable recent sales (comps) of similar, renovated properties in the immediate vicinity. The ARV is arguably the single most important metric in hard money underwriting, as it represents the ultimate value of the asset securing the loan.

Maximum Leverage and After Repair Loan-to-Value (ARLTV)

While LTC determines the loan amount based on your costs, there is a crucial cap on leverage determined by the ARV. This is called the After Repair Loan-to-Value (ARLTV), sometimes referred to as Loan-to-ARV. Most hard money lenders cap their ARLTV at 70% to 75%. This ensures a protective equity cushion remains in the property even after it's fully leveraged.

Formula: ` Total Loan Amount / After-Repair Value

The final loan amount you receive will be the lesser of the LTC calculation and the ARLTV calculation.

Putting It All Together: A Capital Stack Example

Let's walk through a real-world scenario to see how these metrics interact.

- Purchase Price: $200,000

- Renovation Budget: $75,000

- Total Project Cost: $275,000

- After Repair Value (ARV): $400,000

The lender offers the following terms:

- Loan-to-Cost (LTC): 90%

- After Repair Loan-to-Value (ARLTV): 75%

Step 1: Calculate the loan amount based on LTC.

$275,000 (Total Cost) x 90% (LTC) = $247,500

Step 2: Calculate the maximum loan amount based on ARLTV.

$400,000 (ARV) x 75% (ARLTV) = $300,000

Step 3: Determine the final loan amount.

The lender will fund the lesser of the two calculations. In this case, the final loan amount is $247,500.

Step 4: Calculate the borrower's cash-to-close.

$275,000 (Total Cost) - $247,500 (Loan Amount) = $27,500

In this scenario, the investor needs to bring $27,500 to the closing table, plus any origination points and closing costs. This investor contribution is their "skin in the game" and represents the bottom of the capital stack.

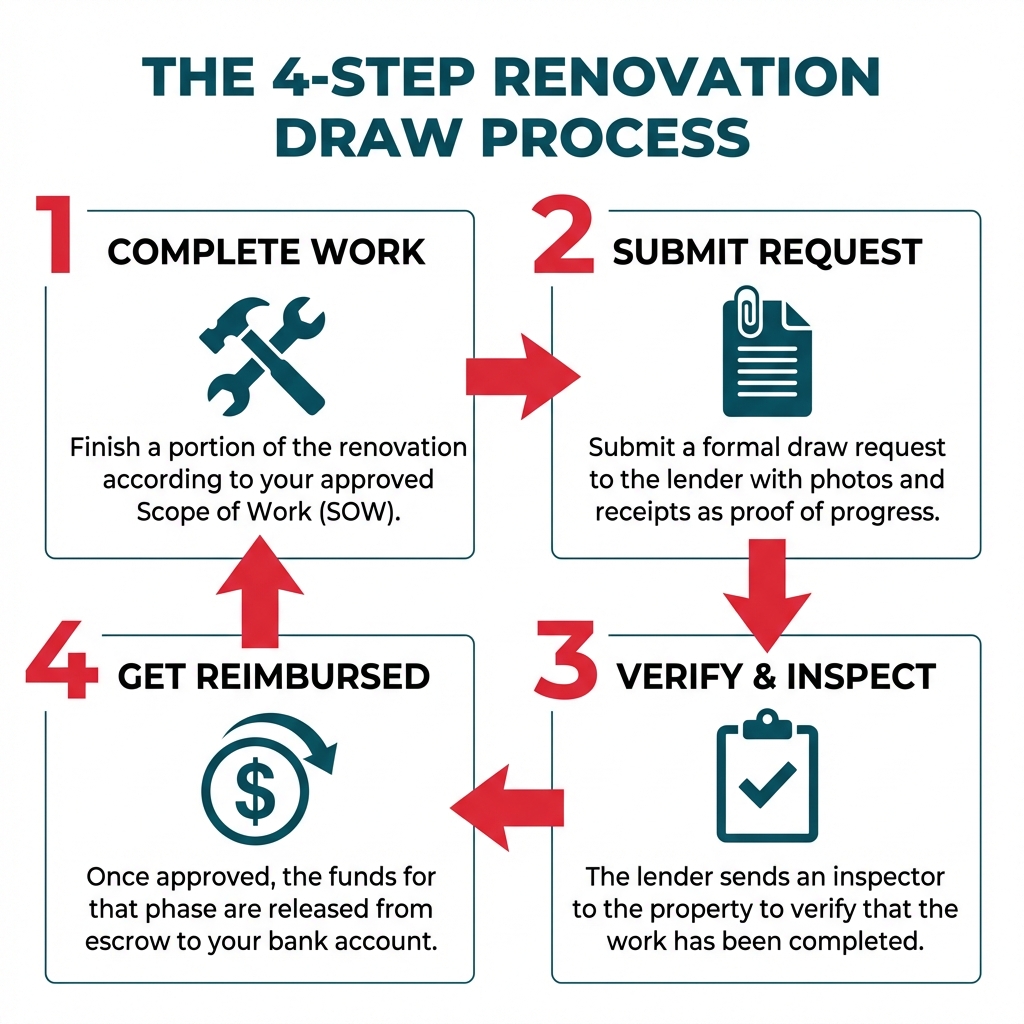

The Renovation Draw Process Explained

When you get a hard cash loan that includes financing for renovations, the lender doesn't just hand you a check for the full rehab budget at closing. Instead, renovation funds are held in a lender-controlled escrow account and disbursed in stages as work is completed. This process is known as the draw process, and it's designed to protect both the lender and the borrower.

Escrow and the Scope of Work (SOW)

At the beginning of the loan process, you will submit a detailed Scope of Work (SOW) to the lender. This document, often created using a template like the AIA G702 form, breaks down the entire renovation into line items with associated costs (e.g., "Kitchen Cabinets - $5,000," "Interior Paint - $3,000"). This SOW becomes the blueprint for the project. Once approved, the total renovation budget is placed into an escrow account controlled by the lender.

How Draws Work: Reimbursement for Completed Work

The draw process is a reimbursement system. This means you (the borrower) typically have to pay your contractors for the work first, and then you request a draw from the lender to be reimbursed.

The process generally follows these steps:

- Complete a Phase of Work: You complete a portion of the project as outlined in your SOW. For example, you finish the demolition and framing.

- Submit a Draw Request: You fill out a draw request form, indicating which line items from the SOW have been completed and providing supporting documentation like photos, videos, and receipts.

- Lender Orders an Inspection: The lender sends a third-party inspector to the property to verify that the work you claimed is complete has actually been done and meets a reasonable standard of quality.

- Funds are Disbursed: Once the inspection report is approved, the lender releases the corresponding funds from the escrow account directly to your bank account. This typically takes a few business days.

This cycle repeats until the project is finished and all renovation funds have been disbursed.

Why the Draw Process is Crucial

While it can seem cumbersome, the draw process serves a vital purpose. It prevents borrowers from taking the renovation money and using it for other purposes, abandoning the project mid-way. This ensures that the lender's capital is being used to increase the value of their collateral, moving the property closer to the projected ARV. For the borrower, it enforces discipline, ensuring the project stays on budget and on schedule according to the pre-approved plan.

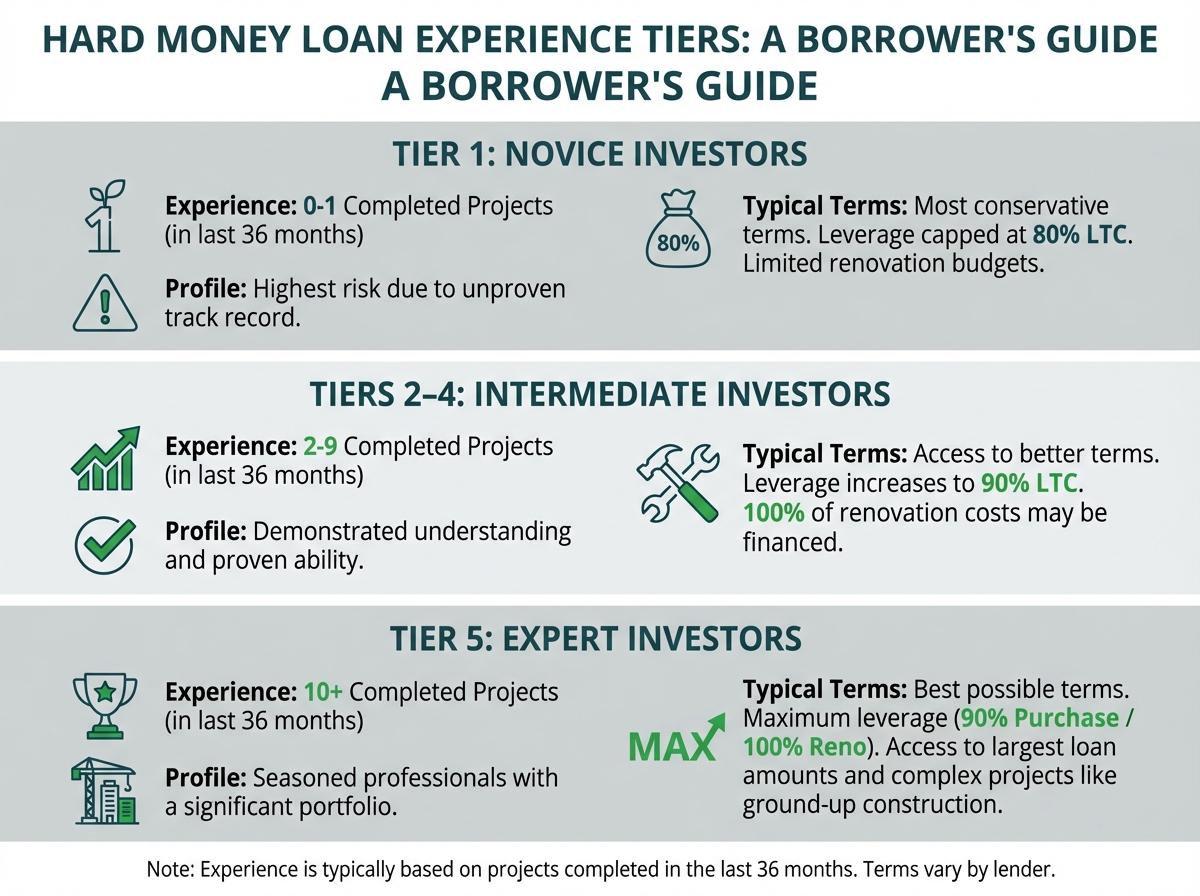

Experience-Based Underwriting Tiers

Hard cash lenders heavily weigh a borrower's real estate investing experience when determining loan terms. More experienced investors represent a lower risk because they have a proven ability to manage projects successfully and navigate unforeseen challenges. To standardize this, lenders like OfferMarket often use an experience-based tier system. This system typically categorizes investors based on the number of successful projects (acquisitions and sales or refinances) they have completed within a recent timeframe, usually the last 36 months.

Tier 1: Novice Investors

- Experience: 0-1 completed projects in the last 3 years.

- Profile: This tier is for individuals who are new to real estate investing or have very limited experience. Lenders view this group as the highest risk due to their unproven track record.

- Typical Terms: Novice investors receive the most conservative terms. Leverage is often capped at 80% LTC, meaning they need to bring more cash to closing. Renovation budgets are also typically limited to prevent them from taking on projects that are too complex.

Tiers 2-4: Intermediate Investors

- Experience: 2-9 completed projects in the last 3 years.

- Profile: These investors have a few projects under their belt and have demonstrated a basic understanding of the process. They have proven they can successfully manage a project from acquisition to exit.

- Typical Terms: As investors move up through these tiers, they gain access to better terms. Leverage can increase to 90% LTC, and lenders may be willing to finance 100% of the renovation costs. The size and complexity of allowable renovation budgets also increase.

Tier 5: Expert Investors

- Experience: 10+ completed projects in the last 3 years.

- Profile: These are seasoned professionals who invest in real estate full-time or have a significant portfolio. They have a well-established system for finding, renovating, and exiting deals.

- Typical Terms: Expert investors receive the best possible terms. This can include maximum leverage (e.g., 90% of purchase price and 100% of renovation costs), access to the largest loan amounts, and approval for highly complex projects, including ground-up construction, additions, or major structural changes. They are considered the lowest risk and therefore get the most favorable pricing and flexibility.

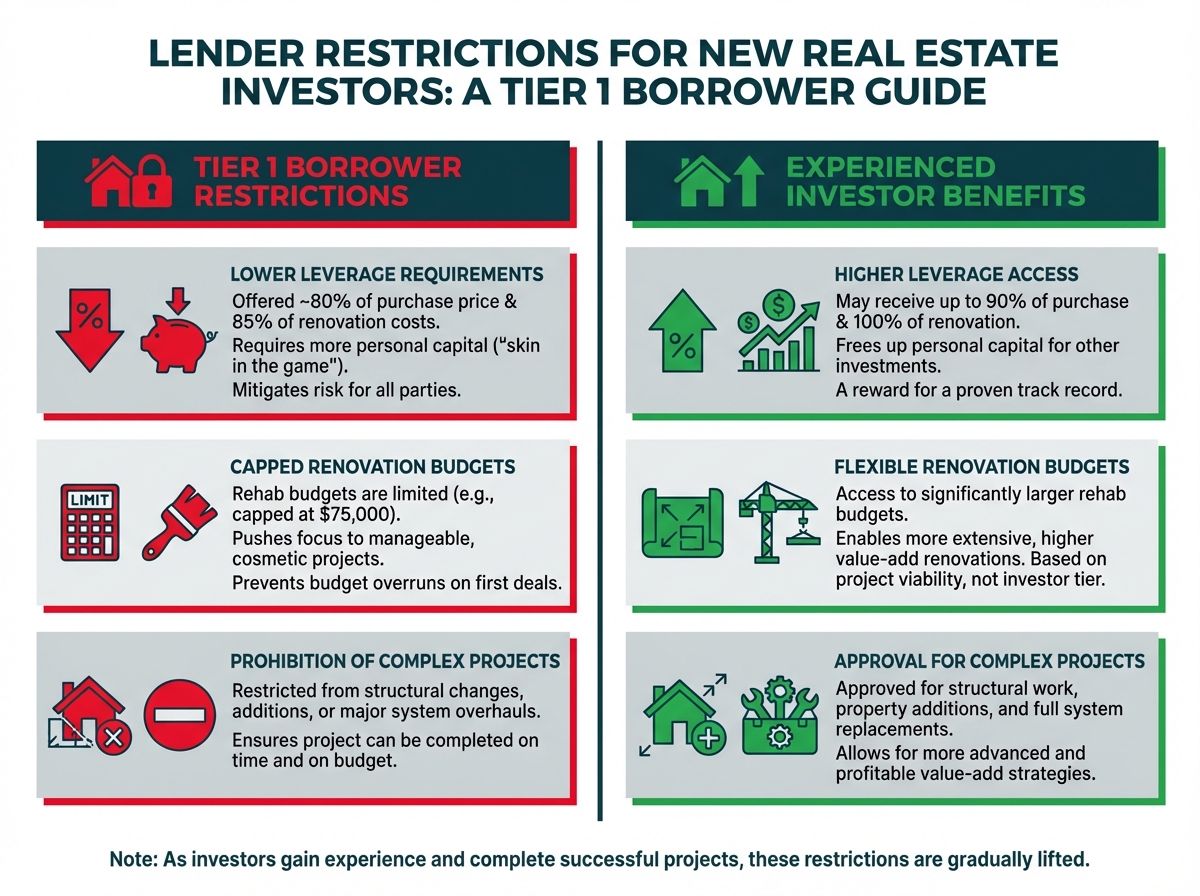

Limitations for Inexperienced Investors

Lenders implement specific restrictions for Tier 1 (novice) borrowers as a form of risk mitigation. While it might seem restrictive, these limitations are designed to protect both the lender from default and the new investor from getting in over their head on a project they aren't equipped to handle.

Lower Leverage Requirements

The most significant limitation is on leverage. A typical Tier 1 borrower might be offered 80% of the purchase price and 85% of the renovation costs. This is a stark contrast to an experienced investor who might receive 90% of the purchase and 100% of the renovation. This lower LTC means the novice investor must contribute more of their own capital, ensuring they have significant "skin in the game" and are financially committed to the project's success.

Capped Renovation Budgets

Inexperienced investors are often limited to projects with smaller, more manageable renovation budgets. A lender might cap the rehab budget at a certain percentage of the purchase price or a fixed dollar amount (e.g., $75,000). This pushes them toward projects that are primarily cosmetic in nature. The goal is to avoid situations where a new investor underestimates the cost and complexity of a major renovation, leading to budget overruns and project failure.

Prohibition of Complex Projects

Lenders will generally not approve novice investors for projects involving major complexity. Prohibited work often includes:

- Structural Changes: Moving load-bearing walls, altering the foundation.

- Additions: Adding a second story or expanding the property's footprint.

- Major System Overhauls: Complete replacement of electrical or plumbing systems that require extensive permits and specialized contractors.

By restricting new investors to simpler, cosmetic rehabs (like new paint, flooring, kitchens, and baths), lenders reduce the number of variables that could go wrong and ensure the project has a higher probability of being completed on time and on budget. As investors gain experience and move up the tiers, these restrictions are gradually lifted.

Anatomy of Hard Cash Loan Terms

Hard cash loans have a distinct structure that is very different from a conventional 30-year mortgage. Understanding these terms is essential for managing your cash flow and planning your exit strategy.

Standard Term Length

The most common term for a hard cash loan is 12 months. This timeframe is considered sufficient for most fix-and-flip or BRRRR projects, allowing for a few months of acquisition and planning, 3-6 months of renovation, and a few months for marketing and selling the property or securing a refinance.

Extended Terms for Larger Projects

For more complex or extensive projects, some lenders may offer extended terms of 18 or 24 months. These longer terms are typically reserved for:

- Large-scale Renovations: Projects with budgets exceeding $100,000 or requiring significant structural work.

- ADU (Accessory Dwelling Unit) Construction: Building a new unit on an existing property.

- Conversions: Converting a single-family home into a duplex or vice-versa.

- New Construction: Ground-up development projects that naturally have a longer timeline.

These extended terms come with the understanding that the project's scope necessitates more time for completion and a successful exit.

Interest-Only Monthly Payments

A defining feature of hard cash loans is their payment structure. They are almost always interest-only. This means your monthly payment to the lender only covers the interest that has accrued on the outstanding loan balance for that month. You are not paying down any of the principal. This structure is designed to keep monthly carrying costs as low as possible for the investor during the renovation phase when the property is not generating any income.

The Balloon Payment

Because the monthly payments are interest-only, the entire principal loan amount remains due at the end of the term. This lump-sum repayment is known as a balloon payment. For example, if you borrowed $250,000 for 12 months, you would make 11 interest-only payments, and then on the 12th month, you would owe the final interest payment plus the entire $250,000 principal. This is why having a solid, well-timed exit strategy is not just important—it's non-negotiable. You must sell the property or refinance it before the maturity date to make this balloon payment.

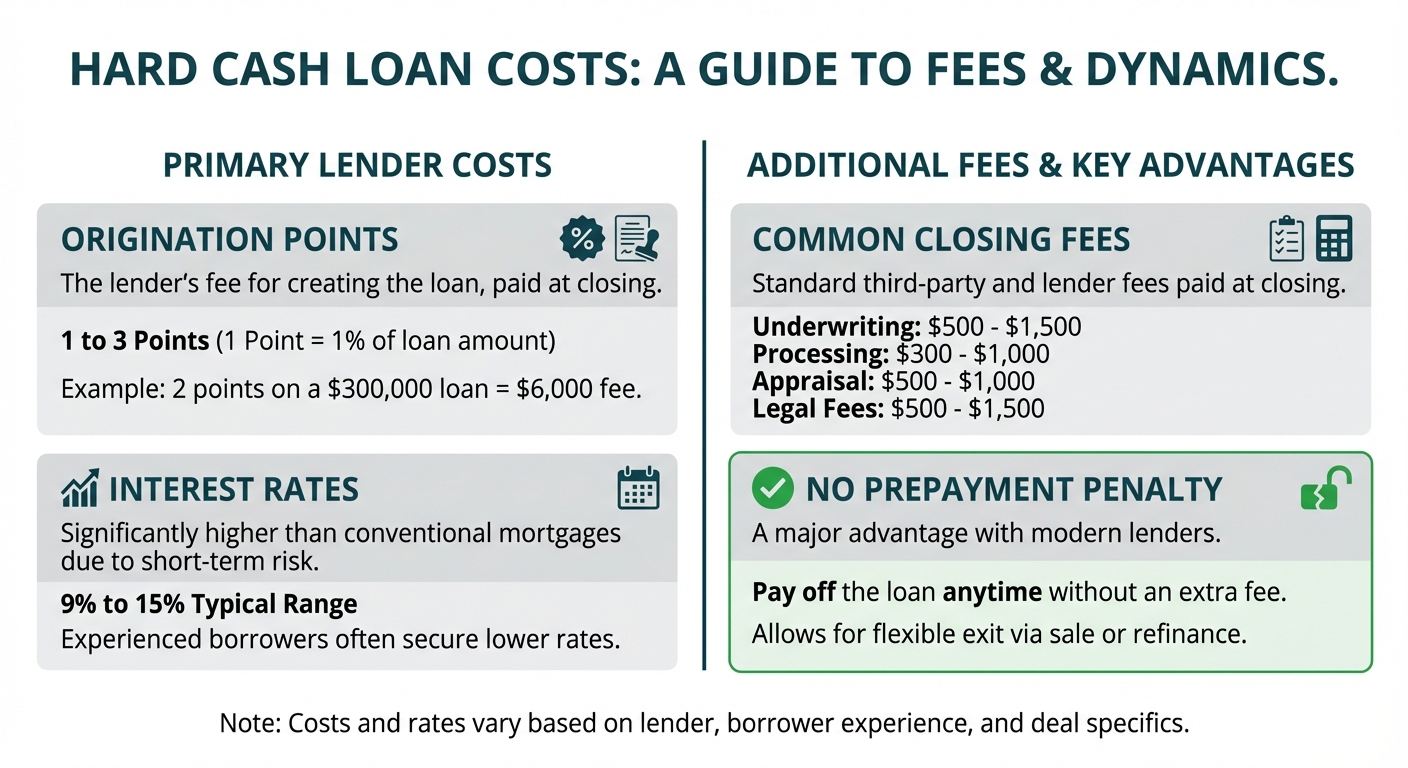

Costs, Fees, and Closing Dynamics

Hard cash loans provide speed and flexibility, but this convenience comes at a higher cost compared to traditional financing. Investors need to factor these costs into their deal analysis to accurately project their net profit.

Origination Points

The primary fee charged by a hard money lender is origination points. One "point" is equal to 1% of the total loan amount. Lenders typically charge 1 to 3 points for a hard cash loan. These points are a fee for creating, or "originating," the loan and are usually paid at closing, often by being deducted from the loan proceeds.

- Example: On a $300,000 loan, 2 origination points would equal a fee of $6,000 (

$300,000 x 0.02).

The number of points charged often depends on the borrower's experience, the loan size, and the perceived risk of the deal.

Interest Rates

Interest rates for hard cash loans are significantly higher than for conventional mortgages. This reflects the higher risk the lender is taking on, the short-term nature of the loan, and the lack of regulation that governs conventional lending. As of late 2023, typical hard money interest rates range from 9% to 15%, depending on the lender, the borrower's experience tier, and overall market conditions. A more experienced borrower will almost always secure a rate on the lower end of that spectrum.

Common Fees

In addition to points and interest, borrowers should expect to pay several other third-party and lender fees at closing. These can include:

- Underwriting Fee: A fee for the lender's time and resources to analyze and approve the deal. ($500 - $1,500)

- Processing Fee: An administrative fee for handling the paperwork. ($300 - $1,000)

- Appraisal Fee: The cost of the independent appraisal to determine the property's As-Is value and After Repair Value (ARV). ($500 - $1,000)

- Legal Fees: Fees for the lender's attorney to draft the loan documents. ($500 - $1,500)

- Title and Escrow Fees: Standard real estate closing costs paid to the title company.

No Prepayment Penalty

A major advantage of working with modern, reputable hard money lenders like OfferMarket is the absence of a prepayment penalty. This means you can sell or refinance the property and pay off the loan at any time without incurring an extra fee. Some old-school lenders may include a "minimum interest earned" clause, requiring you to pay a certain number of months' interest even if you pay the loan off early. It's a critical question to ask any potential lender.

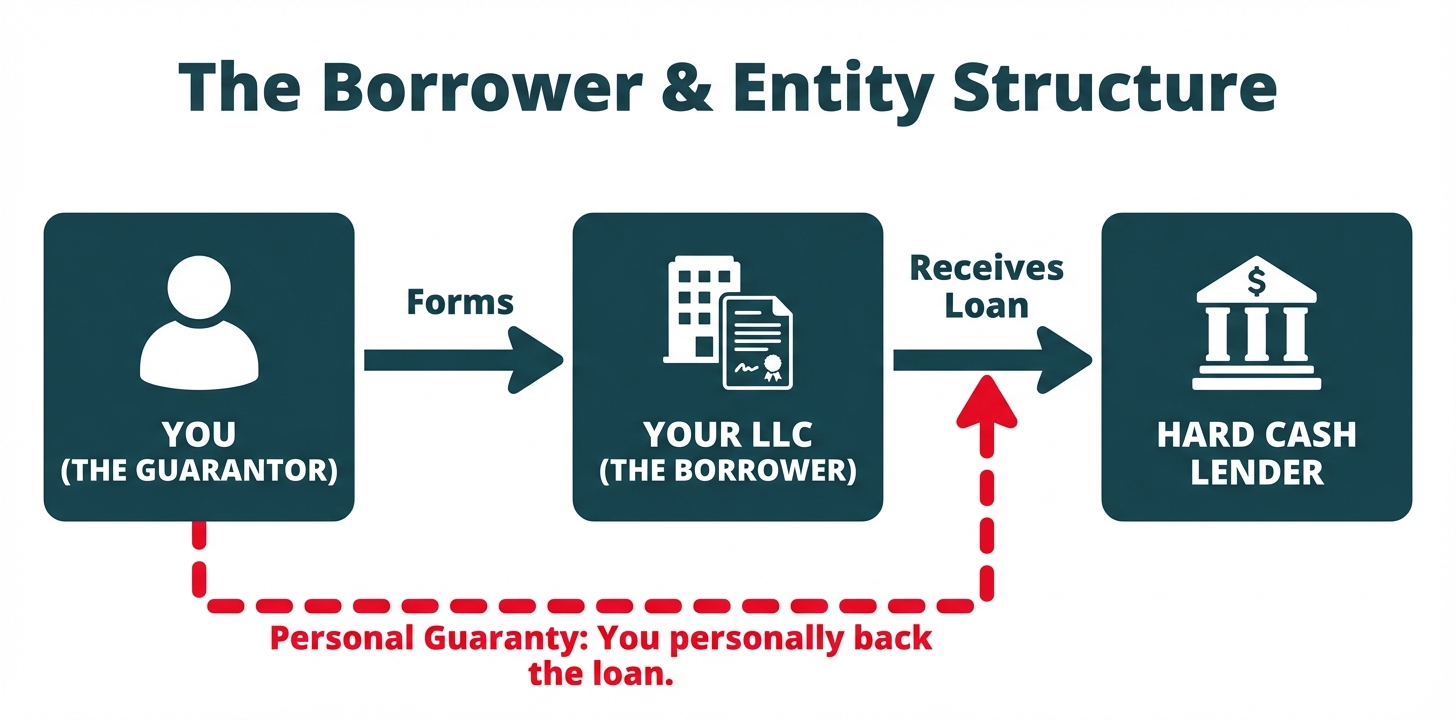

Borrower and Entity Requirements

Hard cash loans are commercial loans, not consumer loans. This legal distinction carries several important requirements for the borrower.

Loans Must Be Made to a Business Entity

Due to lending regulations like the Dodd-Frank Act, hard cash loans for investment purposes cannot be made to an individual in their personal name. They must be made to a legally registered business entity. This protects lenders from a host of consumer protection laws that are not intended for business-purpose loans.

The most common entities used by real estate investors are:

- Limited Liability Company (LLC): This is the most popular choice, as it provides liability protection for the owner's personal assets while offering pass-through taxation.

- S-Corporation (S-Corp): Another common option that provides liability protection and can sometimes offer tax advantages.

Investors must have their entity set up and in good standing before they can close on a hard cash loan.

The Full-Recourse Personal Guaranty

Even though the loan is made to a business entity, the lender still requires the principal owner(s) of that entity to sign a full-recourse personal guaranty (PG). This is a critical legal document that links your personal assets to the loan.

By signing a PG, you are personally guaranteeing the repayment of the debt. If the business entity defaults on the loan and the sale of the property is not enough to cover the outstanding balance, the lender has the legal right to pursue your personal assets—such as your primary residence, bank accounts, or other investments—to satisfy the debt. This clause mitigates the lender's risk and ensures the borrower is fully committed to the project's success.

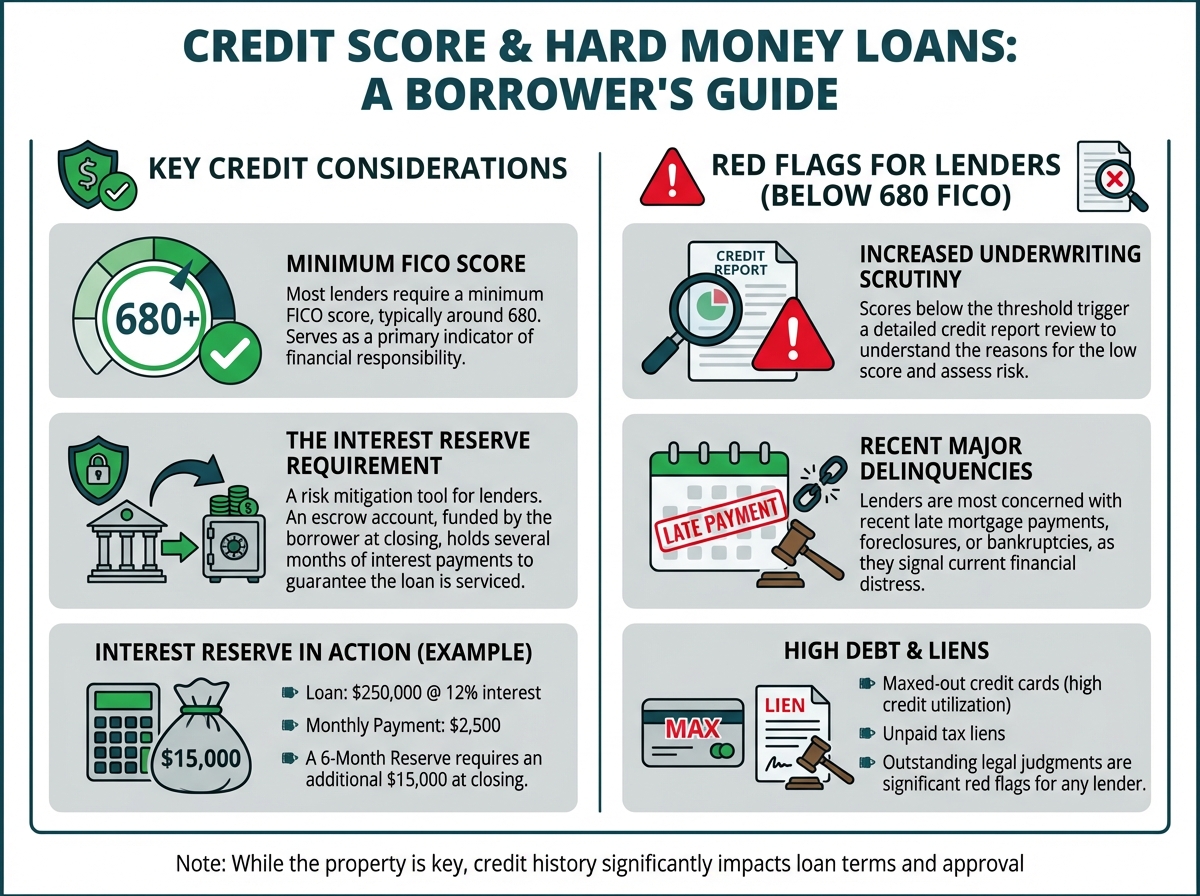

The Role of Credit Score in Hard Money

A common misconception is that credit scores don't matter at all in hard money lending. While it's true that the property is the primary focus, your credit score still plays a role, serving as an indicator of your financial responsibility.

Minimum FICO Score

Most hard money lenders have a minimum FICO score requirement, typically around 680. A score below this threshold can make it very difficult to secure a loan, as it may signal a history of financial mismanagement or unpaid debts, which is a red flag for any lender.

Increased Scrutiny Below 680

Borrowers with scores below 680 often face significant underwriting scrutiny. The lender will likely conduct a detailed review of your credit report to understand the reasons for the low score. They will look for:

- Recent major delinquencies: Late mortgage payments, foreclosures, or bankruptcies.

- High credit utilization: Maxed-out credit cards.

- Judgments or liens: Unpaid legal settlements or tax liens.

A low score due to minor issues like a few late credit card payments years ago is less concerning than a recent foreclosure.

The Interest Reserve Requirement

To mitigate the risk associated with a lower credit score (or sometimes for very large loans), a lender may require the borrower to fund an interest reserve at closing. An interest reserve is an escrow account funded by the borrower that holds a predetermined number of months' worth of interest payments.

- Example: Your loan is $250,000 at a 12% annual interest rate. Your monthly interest-only payment is $2,500 (

($250,000 * 0.12) / 12). If the lender requires a 6-month interest reserve, you would need to bring an additional $15,000 ($2,500 x 6) to closing.

Each month, the lender will automatically draw the monthly payment from this reserve account instead of you paying it out of pocket. This guarantees to the lender that the loan payments will be made on time for the first several months of the project, regardless of any financial issues the borrower might face.

Strategic Use Cases for Hard Cash Loans

Hard cash loans are versatile tools designed for specific investment strategies where speed and flexibility are paramount.

Fix and Flip

This is the quintessential use case for hard money. An investor finds an undervalued, distressed property, uses a hard cash loan to purchase it and fund the renovation, and then sells the improved property for a profit. The short 12-month term, interest-only payments, and inclusion of renovation financing are perfectly suited for the quick turnaround time of a flip.

Bridge Loans

A bridge loan is used to "bridge" a financial gap. For example, an investor wants to buy a new property but needs to pull equity out of an existing property to do so. A traditional cash-out refinance could take months. Instead, they can get a hard money bridge loan against their existing property in a matter of days, pull out the cash, buy the new property, and then pay off the bridge loan once the original property is sold or refinanced conventionally.

Rental Property Acquisition (The BRRRR Method)

Investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy use hard money for the first two steps. They use a hard cash loan to quickly acquire and renovate a property that wouldn't qualify for a conventional mortgage. Once the rehab is complete and the property is stabilized with a tenant, they refinance into a long-term, conventional mortgage (like a DSCR loan). This refinance pays off the hard money loan, and ideally, allows the investor to pull out most or all of their initial cash investment, which they can then "repeat" on a new project.

New Construction

For experienced developers, hard money can be used to fund ground-up new construction projects. These loans are more complex and are structured with a draw schedule tied to construction milestones (e.g., foundation poured, framing complete, etc.). They provide the capital needed to take a project from a vacant lot to a finished home.

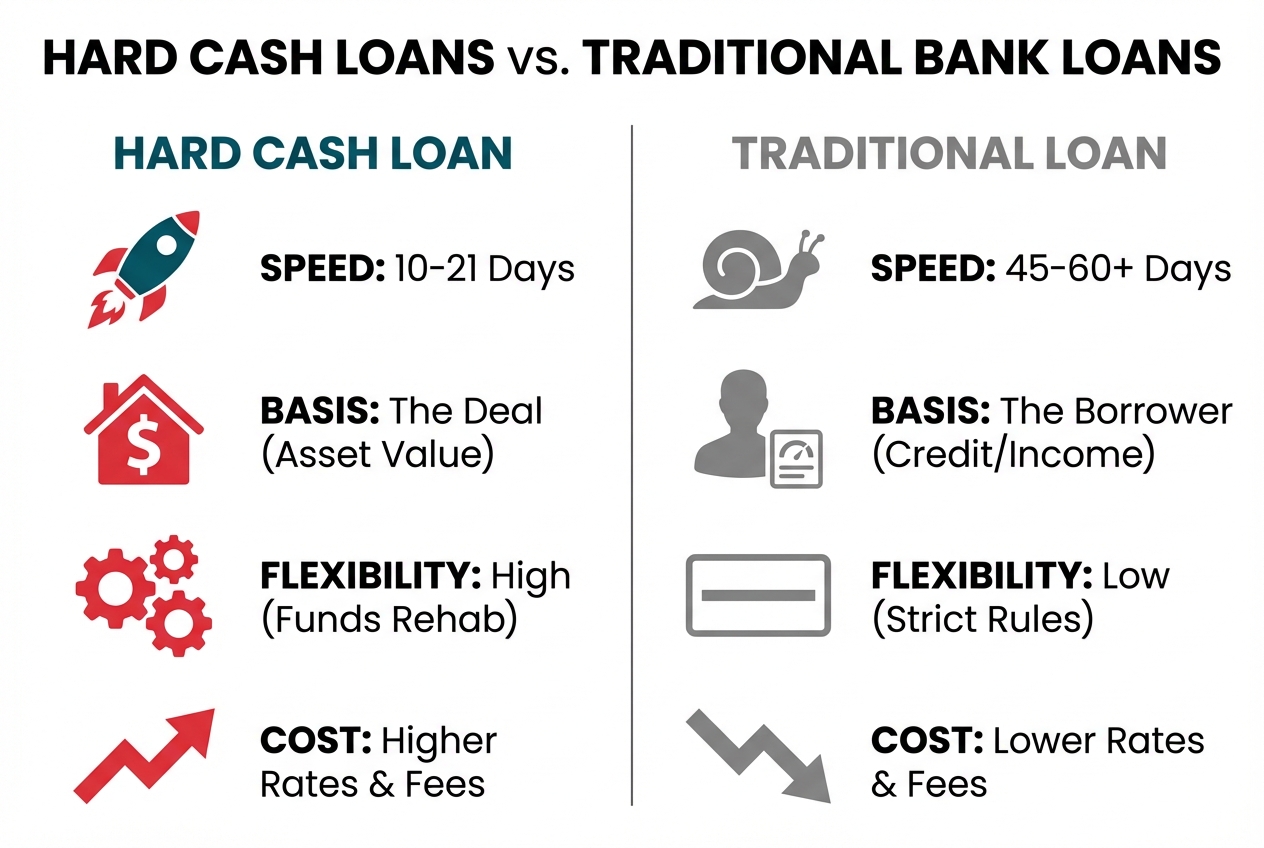

Hard Cash vs. Traditional Bank Loans

Understanding the key differences between hard cash and traditional bank loans is crucial for choosing the right financing for your project.

| Feature | Hard Cash Loan | Traditional Bank Loan |

|---|---|---|

| Closing Speed | 10-21 Days | 45-60+ Days |

| Approval Basis | Property's Value (ARV) & Investor Experience | Borrower's Credit, Income & DTI |

| Flexibility | High (Can fund distressed properties, includes rehab) | Low (Strict property condition standards, no rehab funds) |

| Interest Rates | Higher (e.g., 9-15%) | Lower (e.g., 6-8%) |

| Loan Term | Short-Term (12-24 months, interest-only) | Long-Term (15-30 years, amortizing) |

| Fees | Higher (1-3 origination points) | Lower (0-1 origination points) |

| Best For | Time-sensitive deals, distressed properties, flips | Stabilized, move-in ready properties, long-term holds |

The trade-off is clear: with hard cash, you pay a premium in rates and fees in exchange for unparalleled speed and the flexibility to purchase and renovate properties that banks simply won't touch.

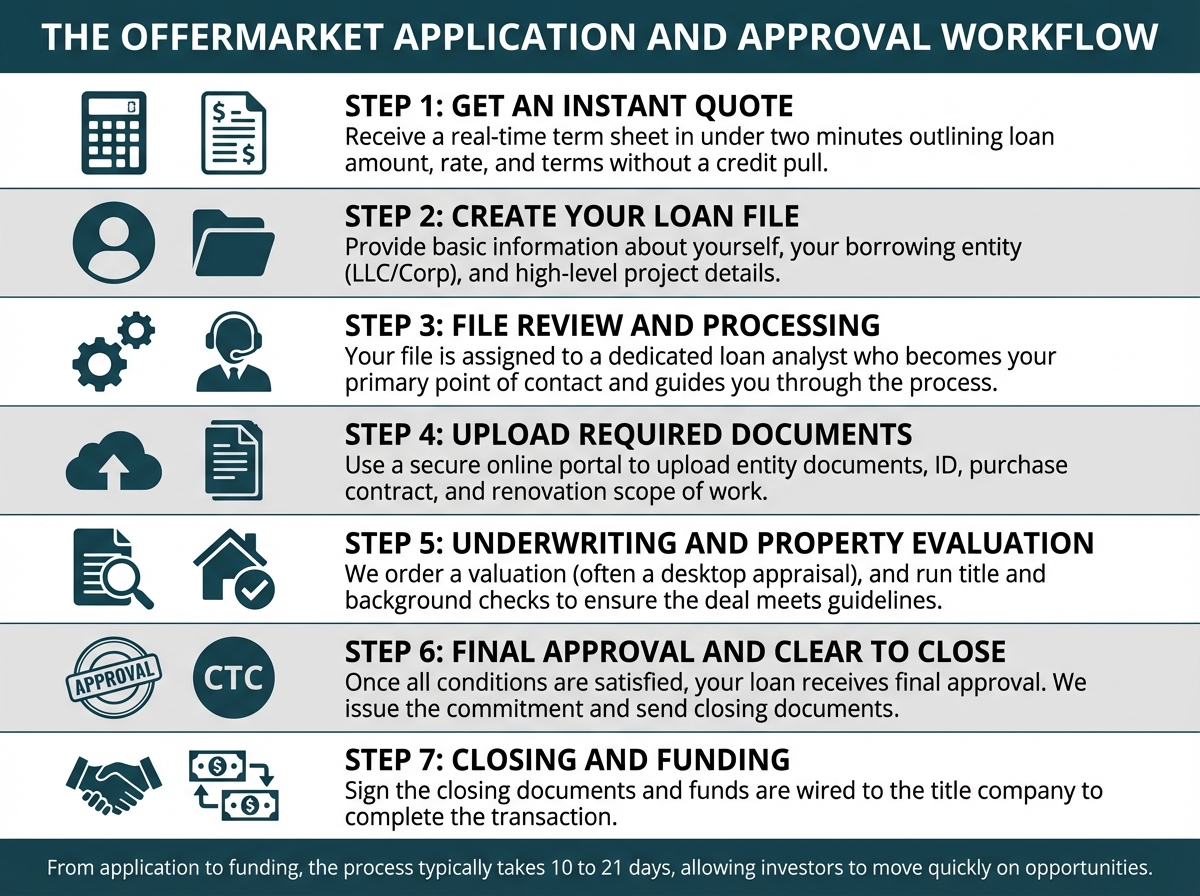

The OfferMarket Application and Approval Workflow

While significantly faster than a bank, the hard money application and approval process still follows a structured workflow to ensure the deal is properly vetted.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Get Your Instant Hard Cash Loan Quote

Understanding the theory behind hard cash loans is the first step. The next is seeing how it applies to your specific deal. With modern lending platforms, you no longer have to wait days for a generic quote.

You can use an online Fix and Flip calculator to get an immediate estimate of your potential loan amount, monthly payments, and cash-to-close requirements. By providing basic information about your property, budget, FICO score, and investing experience, you can see the precise terms you qualify for based on your Experience Tier.

Ready to see your numbers? Get a customized, instant quote for your specific fix-and-flip, rental, or bridge loan scenario.

OfferMarket Loans

Check your rate

60 seconds · no credit pull