*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding the Core Mechanics of a Flip Loan

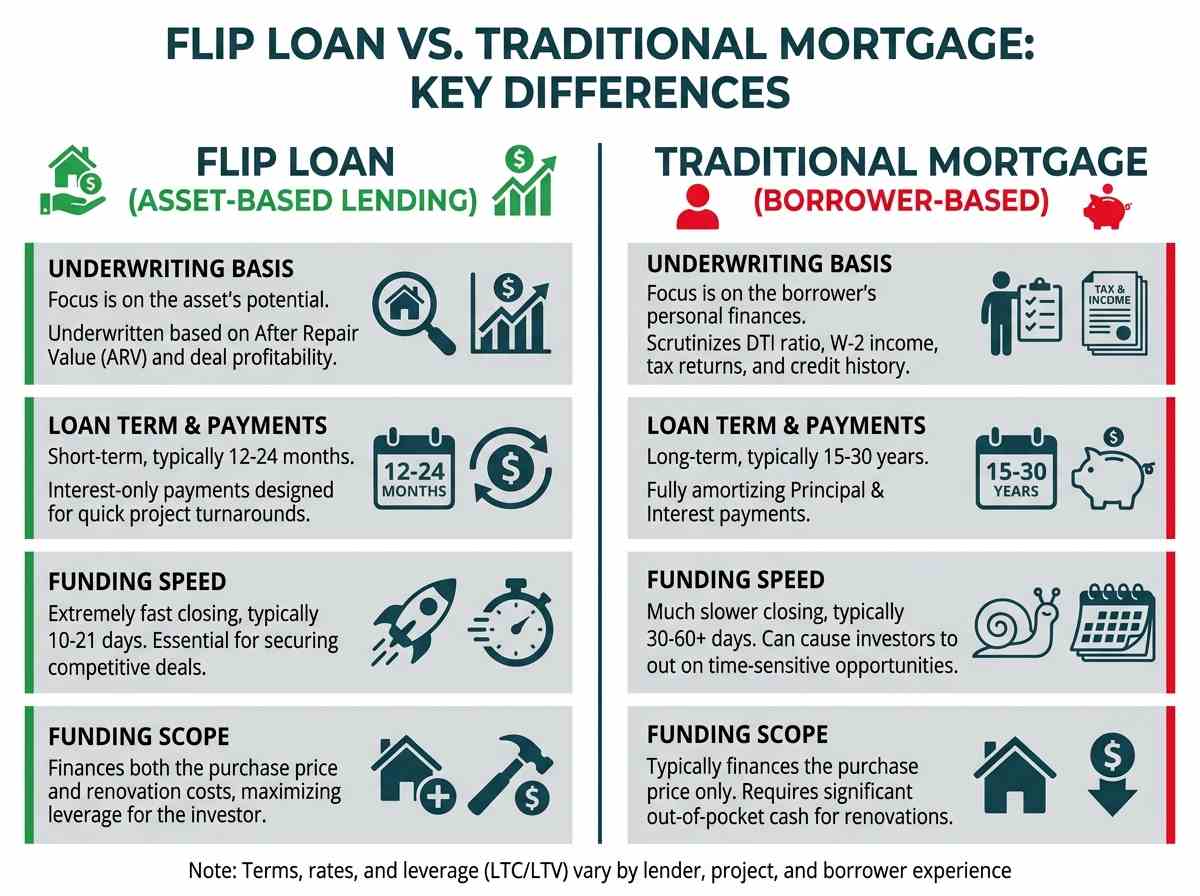

A fix and flip loan is a short-term financing instrument designed specifically for real estate investors to purchase and renovate a property before selling it for a profit. Unlike traditional mortgages that are underwritten based on a borrower's personal income and have long repayment terms (15-30 years), a flip loan is an asset-based loan. This means the lender's primary focus is on the viability of the real estate deal itself—specifically, the property's After Repair Value (ARV)—rather than the investor's W-2 income.

These loans, often provided by hard money lenders like OfferMarket, are structured to accommodate the unique needs of a renovation project. They typically cover a significant portion of both the purchase price and the renovation budget, with loan terms ranging from 12 to 24 months. The underwriting process is significantly faster than a conventional loan, allowing investors to close on properties quickly, which is a major advantage in a competitive real estate market. The core principle is that the property, once renovated, will be valuable enough to repay the loan and generate a substantial profit for the investor upon its sale.

Understanding the Core Mechanics of a Flip Loan

To fully grasp the power of a flip loan, it's essential to understand how it differs from other types of financing and the principles upon which it operates. This knowledge allows you to position your projects for success and speak the same language as your lender.

Key differences from traditional mortgages and conventional loans

The most significant distinction lies in the underwriting philosophy. A traditional mortgage from a bank or conventional lender is primarily concerned with you, the borrower. They scrutinize your personal financial history, including your debt-to-income (DTI) ratio, W-2 income, tax returns, and credit history. The loan is long-term, fully amortizing, and designed for owner-occupants.

A flip loan, on the other hand, is primarily concerned with the asset. While the investor's experience and financial stability are important, the lender's main focus is the property's potential.

| Feature | Flip Loan (Hard Money) | Traditional Mortgage (Conventional) |

|---|---|---|

| Purpose | Short-term investment (purchase & rehab) | Long-term primary residence or rental |

| Underwriting Basis | Asset-based (ARV, deal profitability) | Borrower-based (DTI, income, credit) |

| Loan Term | 12-24 months | 15-30 years |

| Interest | Interest-only payments, higher rates | Principal & Interest payments, lower rates |

| Funding Speed | 10-21 days | 30-60+ days |

| Funding Scope | Purchase price + renovation costs | Purchase price only (typically) |

| Lender Type | Private/Hard Money Lenders | Banks, credit unions, mortgage companies |

The role of hard money lenders like OfferMarket

Hard money lenders are private lenders or funds that specialize in short-term, asset-based real estate loans. They fill a critical gap in the market that traditional banks cannot serve. Because they use private capital, they are not bound by the same strict regulations that govern conventional lending, allowing them to be more flexible and significantly faster.

OfferMarket operates in this space, but with a modern, technology-driven approach. We combine the speed and flexibility of traditional hard money with the efficiency and transparency of a fintech platform. This means investors get:

Speed: The ability to get an instant quote and close in days, not months.

Leverage: Funding for both the purchase and the renovation, allowing you to do more with less of your own capital.

Expertise: Working with a lender that exclusively serves real estate investors and understands the intricacies of a flip project.

Focus on asset-based lending vs. personal income

The concept of asset-based lending is the engine of the fix-and-flip industry. Instead of asking, "Can your personal income support this debt for 30 years?", an asset-based lender like OfferMarket asks, "Does this deal make sense?"

The underwriting process revolves around a few key questions about the property:

- What is the purchase price?

- What is the estimated renovation budget?

- What is the After Repair Value (ARV)? This is the most critical number. It's the estimated value of the property after all renovations are complete.

The loan amount is calculated as a percentage of these figures—specifically, Loan-to-Cost (LTC) and Loan-to-Value (LTV). If the numbers show a clear and profitable path to a successful exit, the loan is likely to be approved, even for an investor who might not qualify for a traditional mortgage on paper. This approach empowers investors to scale their business based on their ability to find good deals, not just their personal income.

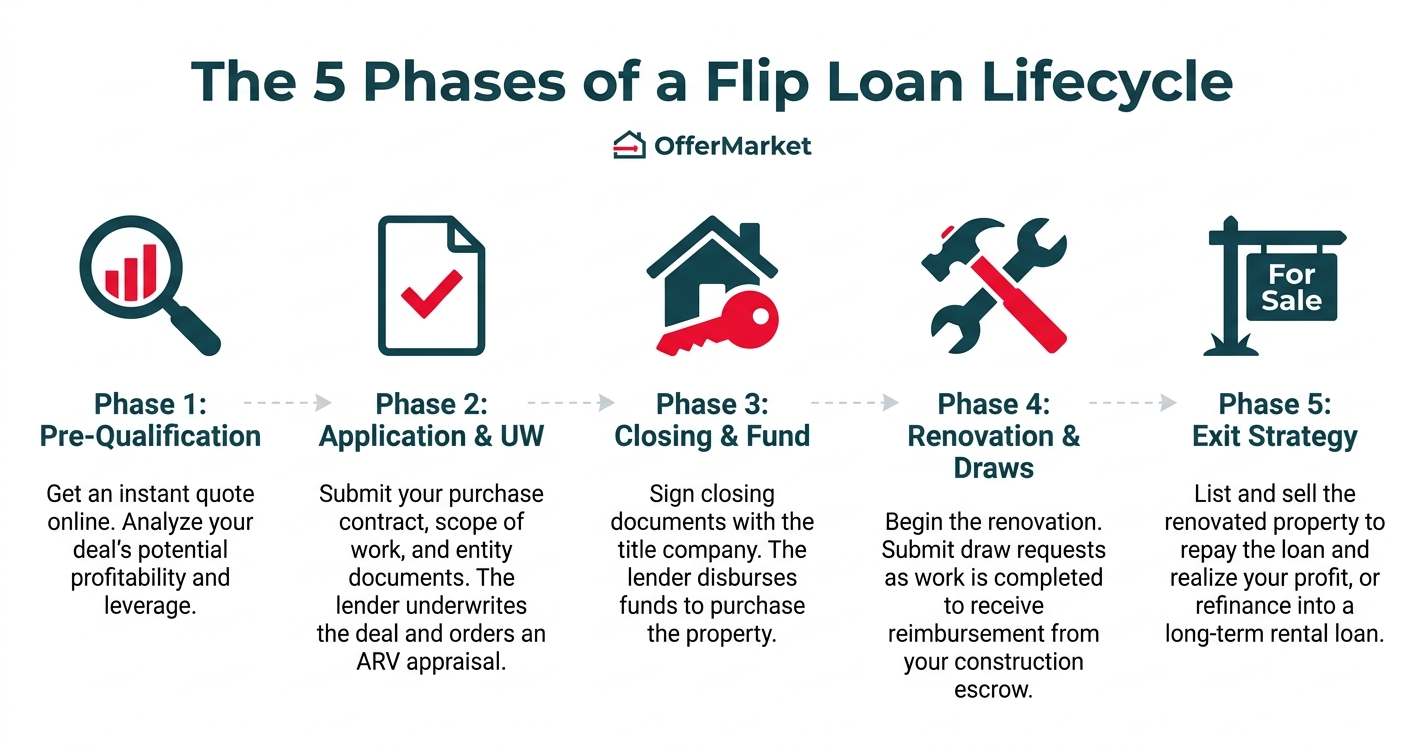

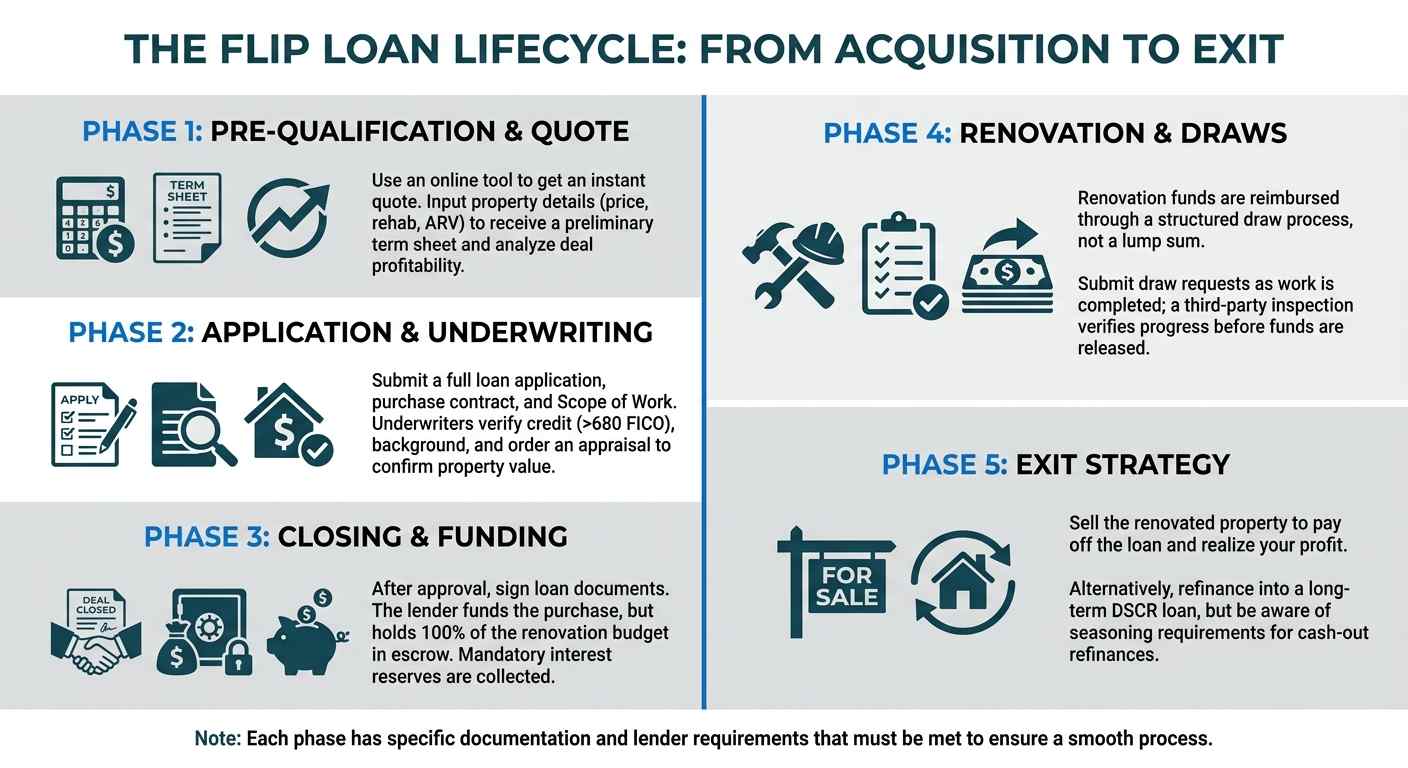

The Flip Loan Lifecycle: From Acquisition to Exit

Navigating a flip loan is a structured process. Understanding each phase helps you prepare accordingly, avoid delays, and manage your project efficiently from start to finish.

Phase 1: Pre-Qualification and Instant Quote

This is the exploratory phase where you vet the deal and the lender. Before you even put a property under contract, you should have a clear idea of your financing options.

Action: Use an online tool like OfferMarket's instant quote generator.

Process: You will input key details about the property (purchase price, rehab budget, estimated ARV) and yourself (experience level, estimated credit score).

Outcome: Within seconds, you receive a preliminary term sheet outlining potential interest rates, points, LTV/LTC limits, and estimated monthly payments. This allows you to quickly analyze the deal's profitability and determine if it meets your investment criteria.

Phase 2: Application, Underwriting, and Appraisal

Once you have a property under contract, the formal loan process begins.

Application: You will complete a full loan application and upload necessary documents. Critical documents include the fully executed purchase contract, a detailed Scope of Work (SOW), a verifiable track record of past projects, and proof of liquidity demonstrating a minimum net worth equal to at least 10% of the loan amount. You must also provide complete entity documents, including the LLC Operating Agreement, EIN, and a recent Certificate of Good Standing. If you are an inexperienced investor or entering a new market, a General Contractor agreement is also required.

Underwriting: The underwriting team reviews your entire file to ensure profitability and mitigate risk. They will pull a tri-merge credit report to verify a minimum 680 FICO score and ensure that any past bankruptcies or foreclosures are seasoned for greater than 4 years. A background check is also conducted to confirm there are no financial crimes, serious felonies, or outstanding tax liens greater than $50,000.

Appraisal and Valuation: The lender will order an independent, third-party appraisal to determine the property's "As-Is" value and After Repair Value (ARV). Crucially, the lender will also order an Appraisal Risk Review (ARR) or Collateral Desktop Analysis (CDA) as a secondary valuation. If the ARR/CDA returns a value that is more than 10% lower than the original appraisal, the lender will strictly use the lower value to determine your maximum loan amount. Furthermore, if your total loan amount exceeds $1,500,000, two full independent appraisals are mandatory.

Phase 3: Closing and Funding the Purchase

Once the appraisal is approved and underwriting clears the file, the loan moves to closing. After all loan documents are signed and your required cash-to-close is wired, the lender funds the transaction.

While the initial loan disbursement goes toward the purchase price, private lenders strictly retain 100% of the approved renovation budget in a construction holdback escrow account. Additionally, lenders mandate the collection of interest reserves at closing (ranging from 1 to 12 months, depending on your FICO score and credit depth) to ensure your initial monthly payments are covered while the project gets off the ground.

Phase 4: The Renovation and Draw Schedule

Renovation funds are not disbursed as an upfront lump sum. Instead, you are reimbursed through a structured draw process based on the exact line items completed in your approved Scope of Work (SOW):

The Draw Process: As you complete specific components of the project, you submit a draw request. The lender then orders a third-party inspection to verify the quality and completion of the work.

Component-Based Reimbursement: To maximize your cash flow, your SOW must be broken down by specific trades and materials (e.g., separating "Rough Plumbing" from "Finish Plumbing") rather than submitting room-by-room estimates. Once the inspector verifies a specific line item is 100% complete, the lender releases the funds allocated to that component.

Valuation Limits: To ensure the project funding remains balanced from beginning to end, lenders strictly cap early-stage scopes: Demolition, Soft Costs, and Contingency line items cannot exceed 10% of the total budget each.

Phase 5: The Exit Strategy - Selling or Refinancing

A fix-and-flip loan is a short-term bridge requiring a clear exit strategy:

Selling the Property: Upon project completion, you sell the property on the open market. The sale proceeds pay off the outstanding unpaid principal balance (the purchase funds plus any drawn renovation funds) and any accrued fees, leaving you with the net profit.

Refinancing (The BRRRR Exception): If you intend to keep the property as a rental, you will refinance into a long-term DSCR loan. However, you cannot automatically pull out maximum cash based on the new appraised value immediately. If you attempt to cash-out refinance within the first 6 months of ownership, underwriters will normally restrict your loan to your total Cost Basis.

To use the newly increased appraised value instead, you must pass strict exception hurdles: you must provide the original pre-renovation photos or appraisal to prove the initial condition, obtain a new full appraisal detailing the improvements, and pass a strict secondary collateral review (such as a CU score of 2.5 or less). Even with these approvals, your maximum leverage will be penalized with a 5% LTV reduction. Furthermore, if the property is still vacant at the time of the cash-out refinance, you face severe overlays, including a mandatory 740 minimum FICO score, a 1.20x minimum DSCR, and a minimum property value of $350,000.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Eligibility and Qualifying Criteria for Investors

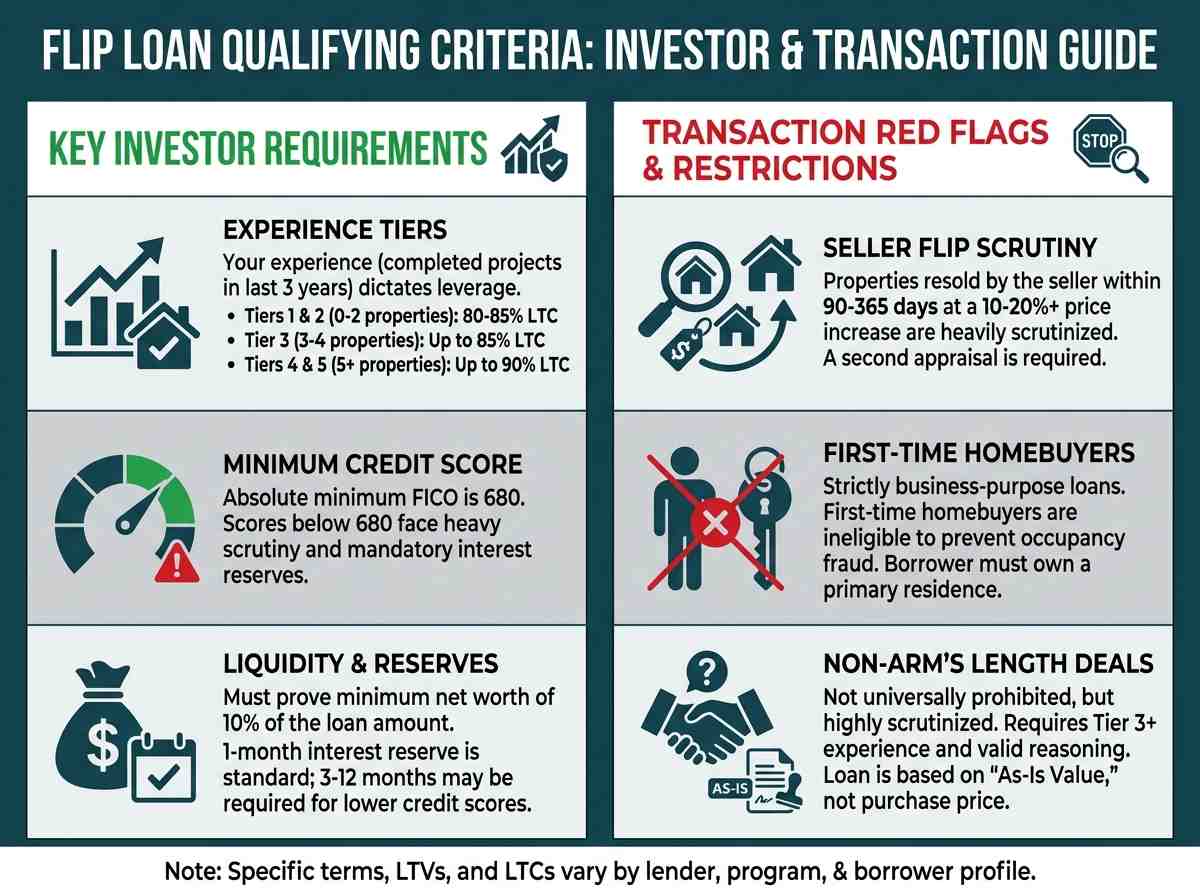

While flip loans are asset-based, lenders enforce strict qualifying criteria focusing on the borrower’s track record, financial stability, and the legitimacy of the transaction to mitigate risk.

The arm's length transaction requirement

While an arm's length transaction is standard, the claim that lenders "universally require" it is incorrect. Non-arm's length transactions (e.g., buying from family or a business affiliate) can be financed, but they are highly scrutinized and must pass a Senior Underwriter pre-screen. To qualify, the borrower must provide valid reasoning, hold an Experience Tier 3 or higher, and the maximum loan amount will be strictly capped against the property's "As-Is Value" rather than the purchase price.

Prohibitions on patterns of previous flipping activity

In underwriting, "flip transaction" restrictions apply to the property seller. Lenders heavily scrutinize properties that the seller acquired within the last 90 to 365 days and is now reselling to you at a 10% to 20%+ price increase. If the property was purchased for less within a 3-year period, the lender will require documented proof of capital expenditures made by the seller; otherwise, the lender will base your loan amount on that previous lower sale price. Lenders require a second full appraisal on these seller flips to prevent artificially inflated values.

Restrictions for first-time homebuyers in certain loan programs

Flip loans are strictly business-purpose loans, making first-time homebuyers completely ineligible. Lenders enforce this to prevent occupancy fraud (where a borrower uses an investment loan to secretly purchase a primary residence). A borrower must generally own a primary residence to be eligible for these programs.

Typical investor requirements: experience, credit score, and liquidity

To secure the best terms, investors should be prepared to meet certain minimum standards.

Experience Tiers: Lenders calculate your exact experience based on completed projects in the last 3 years, which dictates your leverage.

- Tiers 1 & 2 (0-2 properties): Limited to 80% or 85% Loan-to-Cost (LTC).

- Tier 3 (3-4 properties): Eligible for up to 85% LTC.

- Tiers 4 & 5 (5+ properties): Unlocks the maximum 90% LTC.

Credit Score: The absolute minimum FICO score is 680. However, borrowers with scores under 680 face heavy scrutiny and mandatory interest reserves.

Liquidity: Borrowers must prove a minimum net worth equal to at least 10% of the loan amount. Additionally, while a 1-month interest reserve is standard at closing, underwriters will mandate 3 to 12 months of upfront interest reserves for borrowers with lower credit scores (e.g., a 660 FICO requires 12 months of reserves) or limited tradeline history.

Decoding LTV Ratios and Property Valuation

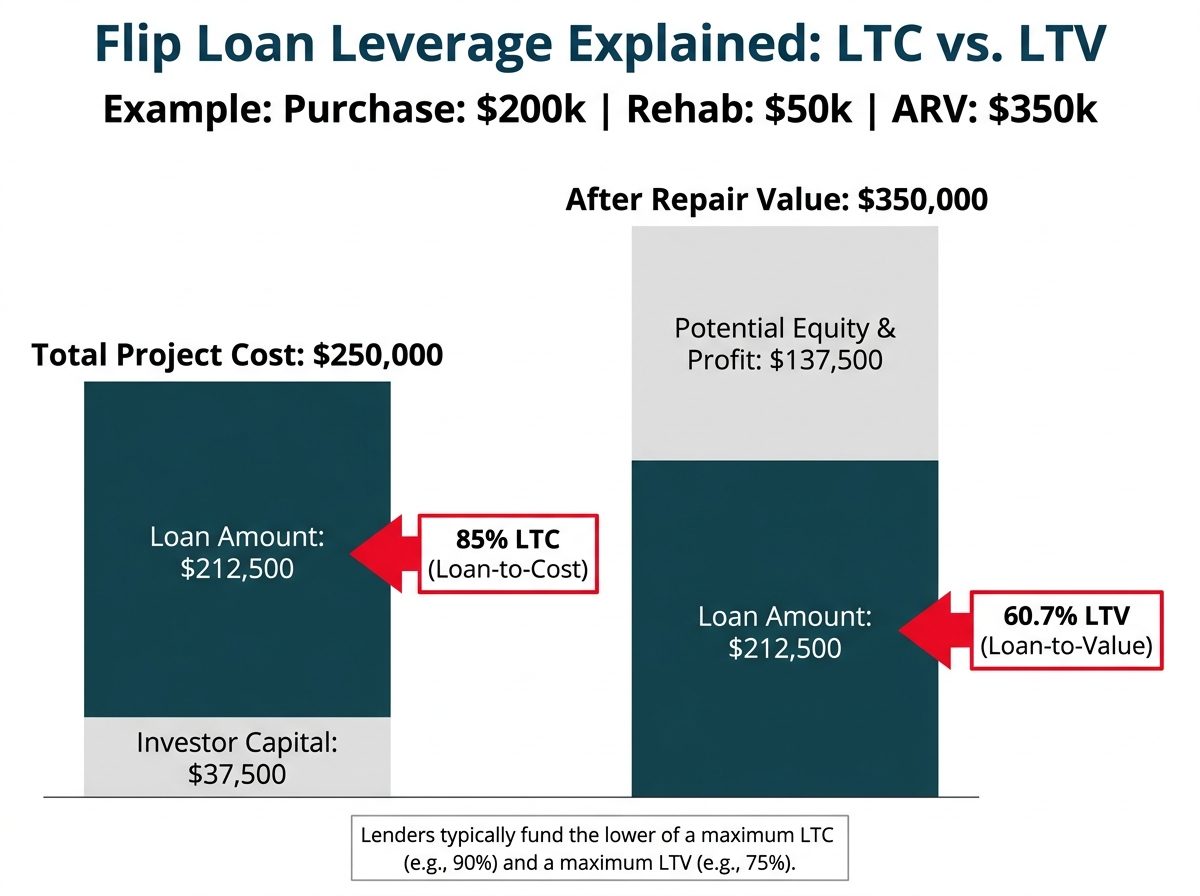

Loan-to-Value (LTV) is a cornerstone metric in all real estate lending, but it has unique applications in the context of fix-and-flip financing. Lenders use it, along with Loan-to-Cost (LTC), to determine the maximum loan amount they are willing to offer on a project.

Cost Basis vs. Appraised Value: The fundamental calculation

It's crucial to understand the two values your loan is based on:

Total Project Cost (or Cost Basis): This is the total amount of capital required for the project. It's calculated as:

Purchase Price + Total Renovation Costs.After Repair Value (ARV) (or Appraised Value): This is the market value of the property after the renovation is complete, as determined by an independent appraiser.

Lenders set maximums for both LTC and ARV. For example, a lender might offer up to 90% LTC and 75% ARV. They will then lend you the lesser of the two calculations.

Example:

- Purchase Price: $200,000

- Renovation Costs: $50,000

- Total Project Cost: $250,000

- After Repair Value (ARV): $350,000

Lender's Terms: Max 90% LTC, Max 75% ARV

- LTC Calculation: $250,000 (Total Cost) * 0.90 (90%) = $225,000

- ARV Calculation: $350,000 (ARV) * 0.75 (75%) = $262,500

In this scenario, the lender will use the lower of the two figures, resulting in a maximum loan amount of $225,000.

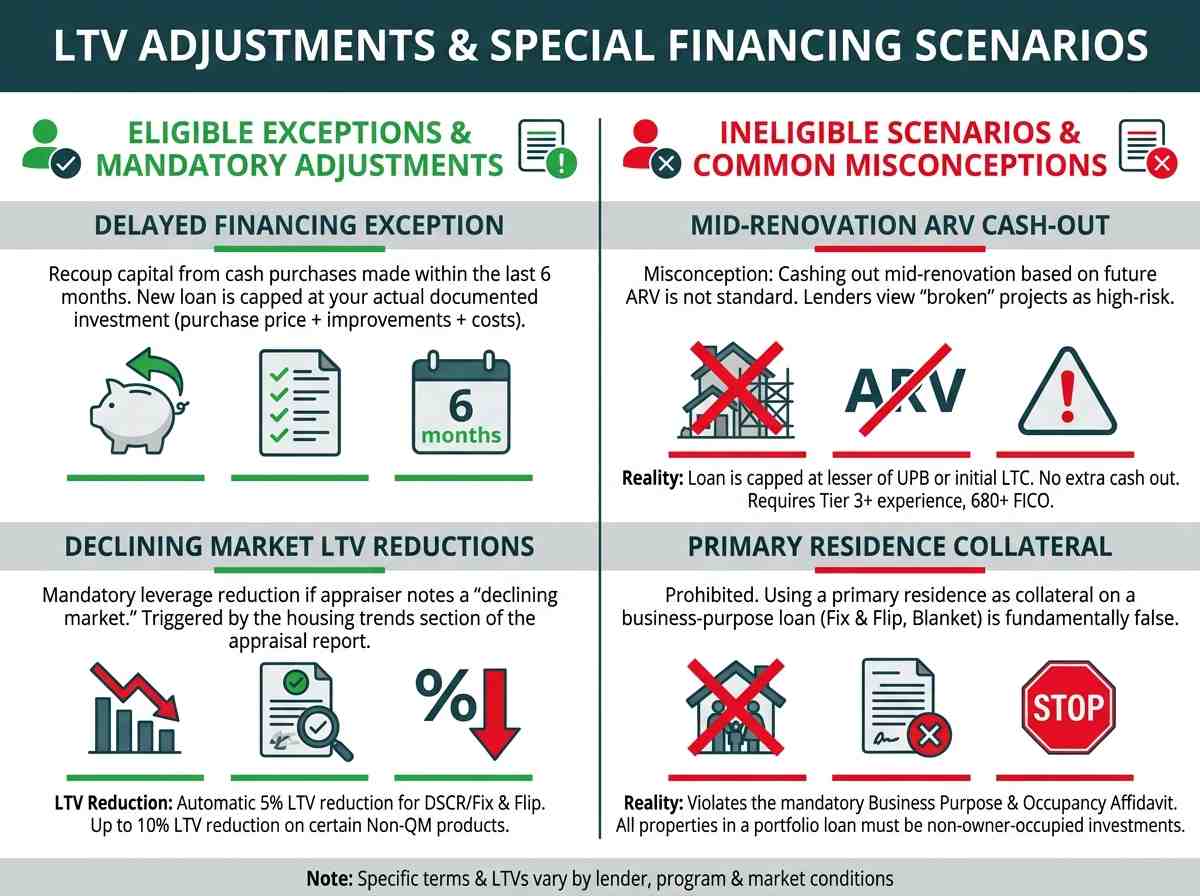

LTV rules for properties owned 6 months or less

If you have owned a property for less than 6 months, cash-out refinances are strictly based on the lesser of the current appraised value or your previous purchase price plus documented improvements.

However, there is a specific "fast-track" exception: the new appraised value can be used under 6 months if the property was substantially renovated, provided you supply original pre-renovation photos or a prior appraisal to prove the initial condition, a new full appraisal reflecting the improvements, and a passing secondary valuation (such as a Clear Capital CDA or a CU score of 2.5 or less).

LTV rules for properties owned 12 months or less

This is not a gray area; guidelines are explicit. Once a property has been owned for over 6 months, the new appraised value can generally be used to determine the LTV rather than the cost basis. However, to mitigate risk, lenders apply strict overlays on these newly seasoned properties, such as capping the maximum cash-out LTV at 65% or 75% of the current value and requiring secondary collateral reviews.

How LTV calculations differ for blanket loans

While a blanket loan does aggregate the values of multiple properties, the crucial underwriting factor is the average ownership seasoning of the portfolio. If the average ownership period of all properties included in the blanket loan is less than the required seasoning threshold (e.g., 6 or 12 months depending on the program), the lender will force the LTV calculation to use the lower of the Cost Basis or appraised value for all properties in the portfolio. Additionally, the final loan amount is proportionally allocated to each property based on its appraised value, not just pooled together.

Get an Instant Fix and Flip Insurance Quote

Protect your investment property with competitive rates — quote in minutes.

Get Insurance Quote →Special Valuation Scenarios and LTV Adjustments

While standard leverage limits cover most transactions, underwriters apply strict overlays for properties mid-renovation, cash purchases, and shifting market conditions.

Renovation cash out transactions and appraisal use

The claim that you can easily execute a cash-out refinance mid-renovation based on a future ARV is incorrect.

Lenders view "broken" or mid-flight projects as highly risky. To qualify for a mid-construction refinance, the property must have been purchased within the last 12 months, and the project must be at least 50% complete with only light-to-moderate renovation remaining.

Furthermore, the new initial loan amount is strictly capped at the lesser of the current loan's Unpaid Principal Balance (UPB) or the standard initial Loan-to-Cost (LTC), meaning the borrower cannot pull out extra cash and must pay closing costs out of pocket. To qualify, the borrower must hold an Experience Tier 3 or higher, have a 680+ FICO, and the project must demonstrate a minimum 30% ROI at the full timeframe.

Delayed financing rules for properties owned free and clear

If an investor purchased a property with cash within the last 6 months (180 days) without existing debt, they can utilize the "Delayed Purchase" or "Delayed Financing" exception to immediately recoup capital.

To qualify:

- The original purchase must have been an arm's-length transaction.

- The settlement statement must confirm no mortgage financing was used, and the initial source of funds must be fully documented (gift funds are ineligible).

- The new loan amount cannot exceed the borrower's actual documented initial investment (original purchase price plus documented, paid improvements) plus the new closing costs, prepaid fees, and points. Standard maximum cash-out limits do not apply here.

Primary residence considerations and CLTV reductions

The claim that an investor can cross-collateralize a primary residence into a flip or blanket loan at a reduced CLTV is fundamentally false.

Fix & Flip and blanket portfolio loans are strictly business-purpose loans for non-owner-occupied properties. A primary residence is completely ineligible to be used as collateral on these programs, and attempting to include one violates the mandatory Business Purpose & Occupancy Affidavit signed at closing. All properties in a cross-collateralized loan must be investment properties.

Required LTV reductions in declining markets

Lenders constantly adjust risk tolerance based on market conditions. If the appraiser indicates in the housing trends section of their report that the subject property is located in a "declining market" (e.g., an over-supply of homes or declining property values), mandatory leverage reductions are triggered.

For standard DSCR and Fix & Flip programs, this results in an automatic 5% LTV/CLTV reduction from the maximum allowable leverage. For certain Non-QM products, this penalty increases to a 10% maximum LTV/CLTV reduction.

Flip Loan Costs: Interest Rates and Fees

Fix and flip loans are more expensive than conventional mortgages, which is a trade-off for the speed, leverage, and flexibility they provide. Understanding the complete cost structure is essential for accurately calculating your project's profitability.

Typical interest rate structures for flip loans

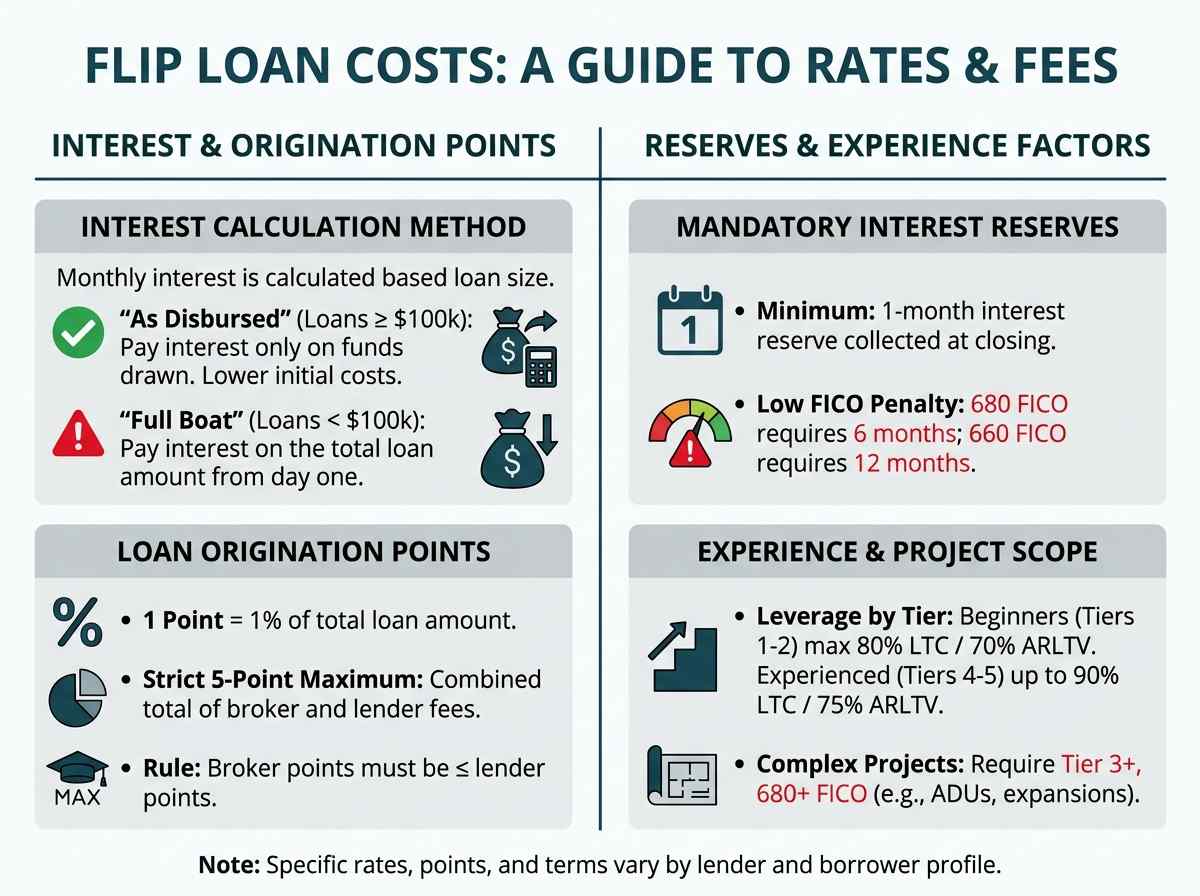

Flip loans require interest-only payments culminating in a balloon payment at maturity (typically 12 months). However, the way your monthly interest is calculated depends strictly on your loan size:

"As Disbursed" Interest (Loans >= $100,000): You are only charged interest on the unpaid principal balance (the initial purchase funds plus any renovation draws you have actually taken). This keeps your initial holding costs lower during the renovation phase.

"Full Boat" Interest (Loans < $100,000): You are charged interest on the total loan amount (including the un-drawn construction holdback) from day one.

Understanding loan origination points

Points represent fees charged for originating the loan, paid at closing. One point equals 1% of the total loan amount.

- The Cap: Lenders enforce a strict absolute maximum of 5 total points per loan.

- Broker vs. Lender Fees: This 5-point maximum is the combined total of both broker and lender fees. Furthermore, any points charged by a broker must be less than or equal to the points charged by the lender.

Common fees: processing, underwriting, and appraisal

In addition to standard third-party closing costs (like appraisals and title fees), the most significant upfront cost investors must prepare for is Interest Reserves.

All flip loans require a mandatory minimum 1-month interest reserve to be collected at closing (calculated on the "Full Boat" amount).

Borrowers with lower FICO scores face heavy reserve penalties. For example, a 680 FICO requires 6 months of reserves, and a 660 FICO requires a massive 12 months of reserves collected upfront.

How project scope and investor experience influence costs

Your maximum leverage and allowable project scope are rigidly dictated by your "Experience Tier" (calculated by your completed projects in the last 3 years):

Investor Experience: Beginners (Tiers 1 & 2) are strictly capped at 80% Loan-to-Cost (LTC) and 70% After Repair Value (ARLTV). Highly experienced investors (Tiers 4 & 5) unlock maximum leverage up to 90% LTC and 75% ARLTV.

Project Scope: Lenders restrict complex projects. If your project includes an expansion, addition, conversion, or ADU, you cannot be a beginner; you must be an Experience Tier 3 or higher, hold a 680+ FICO, and these projects are capped at 70% ARLTV.

The OfferMarket Advantage: Streamlining Your Financing

In a competitive market, your choice of lender can be the difference between securing a great deal and watching it slip away. OfferMarket is built from the ground up to provide real estate investors with a financing partner that understands their needs and empowers their growth.

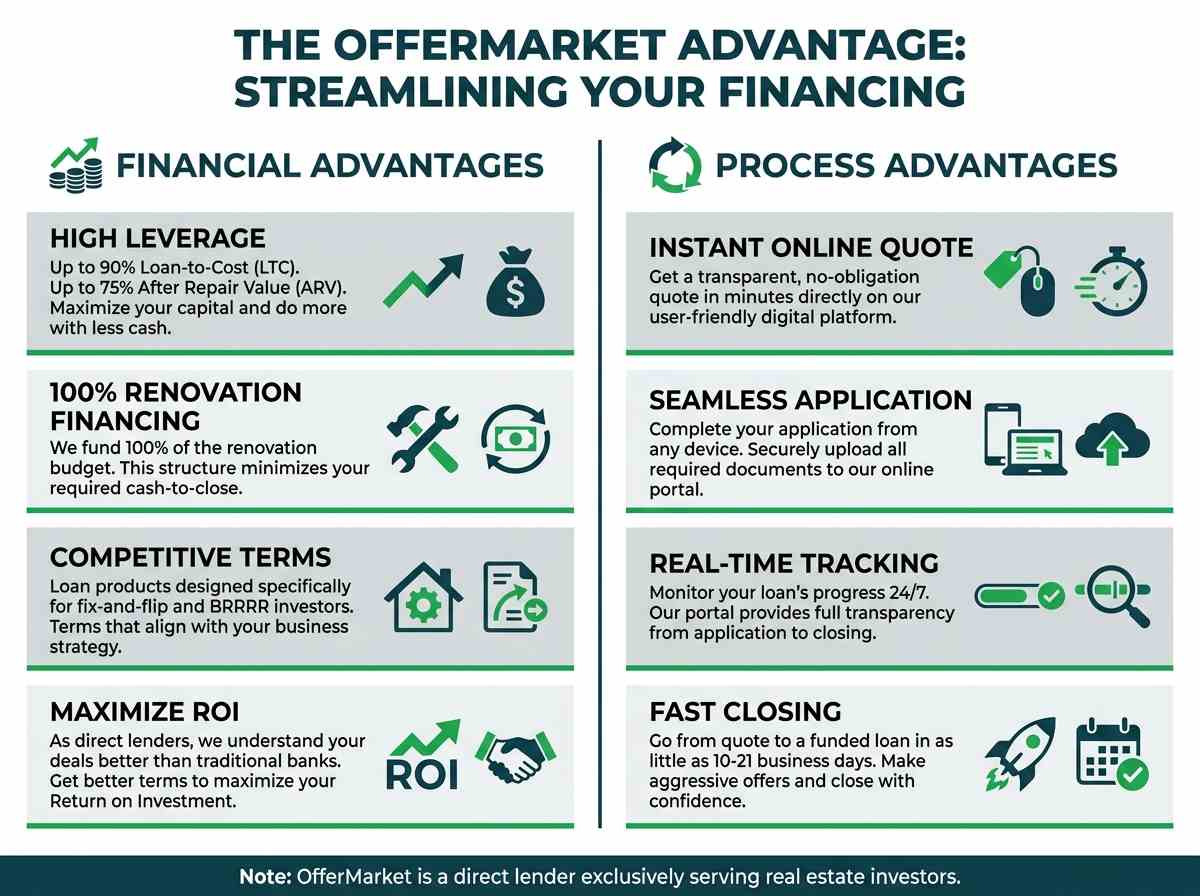

High leverage to maximize your capital and ROI

We provide high-leverage financing to help you do more with your capital. By funding a significant portion of both the purchase and renovation, we allow you to keep more of your cash liquid for the next opportunity. Our programs often feature:

- Up to 90% Loan-to-Cost (LTC)

- Up to 75% After Repair Value (ARLTV)

- 100% financing of renovation costs

This structure minimizes your cash-to-close and maximizes your potential Return on Investment (ROI).

A seamless, user-friendly online application process

We've replaced outdated, paper-heavy processes with a streamlined digital platform. Our online portal makes it easy to:

- Get an instant, transparent quote in minutes.

- Complete your application from any device.

- Securely upload all required documents.

- Track your loan's progress in real-time.

This technology-first approach eliminates friction and saves you valuable time.

Competitive terms tailored for real estate investors

Our loan products are not one-size-fits-all. They are specifically designed for the fix-and-flip and BRRRR models. We offer competitive interest rates and flexible terms that align with your project timelines and business strategy. Because we are direct lenders who only serve investors, we understand the nuances of your deals better than a traditional bank ever could.

Speed and efficiency from quote to closing

Speed is your competitive advantage, and it's our specialty. Our efficient underwriting and technology-driven process mean we can move from initial quote to a funded loan in as little as 10-21 business days. This allows you to make aggressive, confident offers and close on properties before your competition.

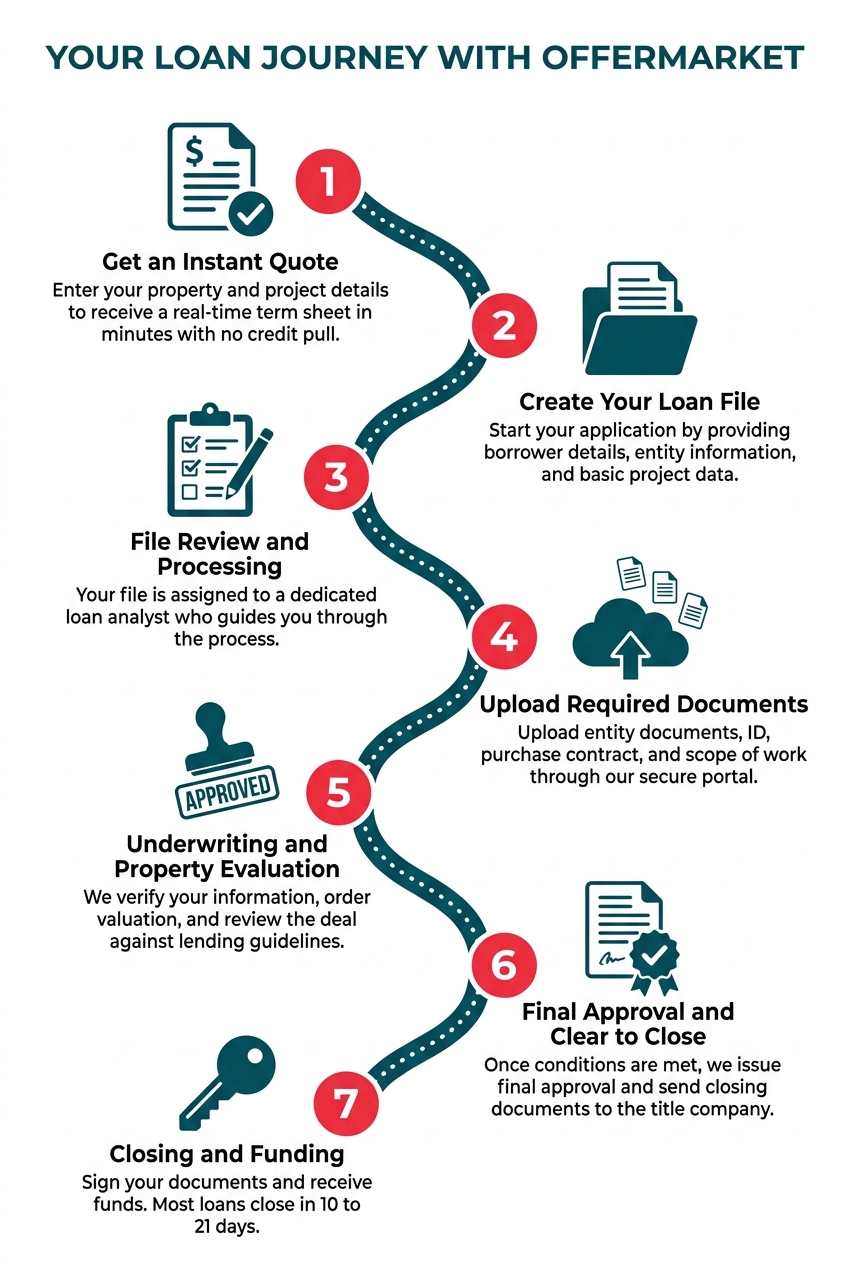

The OfferMarket Loan Process Step-by-Step

We've designed our lending platform to be fast, transparent, and intuitive for real estate investors. Our goal is to get you from application to closing as efficiently as possible.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Take Action: Calculate Your Terms and Get Funded

Knowledge is the first step, but action is what builds your portfolio. Now that you understand the mechanics of a flip loan, it's time to see how the numbers work for your specific project.

Get an instant quote from OfferMarket

The fastest way to vet a potential deal is to see the financing terms. Don't guess what your costs will be.

Get Your Instant Flip Loan Quote Now

Our free tool will provide you with a detailed, preliminary term sheet in under two minutes. There's no obligation and no impact on your credit score.

See your potential interest rates and monthly payments

Your instant quote will break down your potential interest rate, total loan amount, required cash to close, and estimated monthly interest-only payments. This is the critical data you need to accurately calculate your holding costs and project your net profit.

Use our flip loan calculator to model your deal

For a more in-depth analysis, use our comprehensive flip loan calculator. This tool allows you to:

- Model different purchase and rehab scenarios.

- Adjust variables like interest rates and loan terms.

- Estimate your total profit and return on investment.

It's the perfect resource for fine-tuning your numbers before you commit to a property.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull