*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

#9 Best Fix and Flip Lenders of 2026 (Rates & Terms Compared)

This table provides a high-level overview of the top fix and flip lenders for 2026. Use this as a starting point to identify which lenders align with your project needs, experience level, and financing goals. OfferMarket is highlighted as our Top Pick for its superior blend of technology, speed, and investor-friendly terms.

Top Fix and Flip Lenders for 2026

| Lender | Interest Rates | Loan Fees | Max Leverage (LTC / ARLTV) | Min. Credit Score | Funding Time | Our Rating |

|---|---|---|---|---|---|---|

| OfferMarket (Top Pick) | Starting at 9.75% | 1.5 - 2 pts | 90% / 75% | 680 | 10 - 21 Days | ★★★★☆ |

| Go Kapital | Starting at 9.50% | 2.0 - 3.0 pts | 85% / 70% | 660 | 14 - 28 Days | ★★★★☆ |

| Lending One | Starting at 9.25% | 2.0 - 3.0 pts | 90% / 75% | 680 | 14 - 21 Days | ★★★★☆ |

| Kiavi | Starting at 9.00% | 1.5 - 4.0 pts | 90% / 80% | 660 | 7 - 14 Days | ★★★★☆ |

| Lima One Capital | Starting at 9.75% | 2.0 - 3.5 pts | 90% / 75% | 660 | 21 - 30 Days | ★★★☆☆ |

| CoreVest Finance | Starting at 9.99% | 2.5 - 4.0 pts | 85% / 70% | 680 | 21 - 35 Days | ★★★☆☆ |

| RCN Capital | Starting at 10.25% | 2.5 - 5.0 pts | 90% / 75% | 620 | 14 - 21 Days | ★★★☆☆ |

| FundThatFlip | Starting at 9.49% | 2.0 - 4.0 pts | 90% / 70% | 660 | 7 - 14 Days | ★★★☆☆ |

| New Silver | Starting at 9.00% | 1.8 - 2.5 pts | 90% / 80% | 650 | 7 - 10 Days | ★★★★☆ |

In-Depth Reviews of the 9 Best Fix and Flip Lenders

Choosing the right lending partner is one of the most critical decisions a real estate investor makes. The right lender acts as a strategic partner, providing the speed and flexibility needed to capitalize on opportunities, while the wrong one can lead to delays, lost deals, and eroded profits.

Our methodology for this ranking is based on a comprehensive analysis of the factors that matter most to fix and flip investors:

- Pricing: Interest rates and origination fees (points).

- Leverage: The maximum Loan-to-Cost (LTC) and After-Repair Loan-to-Value (ARLTV) offered.

- Speed: The time from application to closing.

- Technology: The use of modern tools for applications, appraisals, and draw requests.

- Flexibility: Underwriting guidelines, prepayment penalty policies, and borrower requirements.

- Customer Support: The quality and accessibility of the lending team.

Based on these criteria, we've identified the top 9 lenders who are setting the standard for the industry in 2026.

1. OfferMarket: Best Overall

OfferMarket earns our top spot as the best overall fix and flip lender for 2026. The company has masterfully blended cutting-edge technology with flexible, investor-centric loan products to create a financing experience that is unparalleled in its efficiency and transparency. For the modern real estate investor who values speed, data-driven decisions, and maximizing return on investment (ROI), OfferMarket is the definitive choice. Their platform is designed from the ground up to eliminate the friction points common in traditional private money lending, empowering investors to close more deals with greater confidence.

Key Features

OfferMarket's competitive advantage lies in its suite of technology-driven features that directly address investor pain points:

App-Based Draw Requests: Gone are the days of cumbersome paperwork and slow inspection scheduling. OfferMarket's mobile app allows you to submit draw requests directly from the job site with photos and videos, leading to approvals and funding in as little as 24 hours.

Desktop Appraisals: In many cases, OfferMarket can utilize desktop appraisals, which are significantly faster and more cost-effective than traditional in-person appraisals. This can shave a week or more off the closing timeline, a critical advantage in a competitive market.

No Prepayment Penalties: Unlike many lenders who lock you into a minimum interest period, OfferMarket has no prepayment penalties. This gives you the flexibility to sell your property as soon as it's ready, maximizing your annualized ROI without being penalized for efficiency.

Transparent, Low Fees: OfferMarket is known for its straightforward fee structure, typically charging between 1 to 2 points with no hidden junk fees. This transparency is crucial for accurately calculating your project's profitability.

100% Renovation Financing: Like the best lenders, OfferMarket finances 100% of your renovation budget, which is held in a construction holdback and released to you as you complete work.

Rates and Terms

- Interest Rates: Starting at 9.75% for experienced investors on standard projects.

- Max Leverage: Up to 90% of the purchase price (LTC) and 75% of the After-Repair loan to Value (ARLTV).

- Loan Amount: From $50k to $3.5M.

- Minimum Credit Score: A reasonable 680 FICO score.

- Funding Time: A reliable 10-21 day closing window.

Ideal For: OfferMarket is the ideal partner for both new and seasoned investors who want a lender that functions like a modern tech company. If you prioritize speed, efficiency, transparent terms, and tools that help you manage your projects more effectively, OfferMarket's platform is built for you. Their combination of competitive pricing and tech-forward features provides a clear path to scaling your fix and flip business.

2. Go Kapital: Best for Flexible Underwriting

Go Kapital has carved out a niche for itself by focusing on relationship-based lending and flexible, common-sense underwriting. While many larger lenders rely on rigid algorithms, Go Kapital takes a more holistic view of each deal and borrower. They understand that not every great investment opportunity fits neatly into a standard box, and their team is skilled at structuring loans for more complex or unique projects.

Key Features:

- Relationship-Focused: Go Kapital prides itself on providing a high-touch experience. Borrowers often work with the same loan officer across multiple deals, building a rapport that can be invaluable for navigating tricky situations.

- Complex Deal Structures: They are more willing than most to consider deals with unusual characteristics, such as mixed-use properties, properties with unpermitted additions, or borrowers with complex income situations.

- Case-by-Case Analysis: Their underwriting process involves a deep dive into the specifics of the property, the borrower's experience, and the local market, rather than just checking boxes on a generic scoresheet.

Rates and Terms:

- Interest Rates: Typically start around 9.50%, which can be slightly higher to compensate for their increased flexibility.

- Max Leverage: Generally up to 85% LTC and 70% ARLTV, though this can vary significantly based on the deal's merits.

- Minimum Credit Score: A more accessible minimum FICO of 660.

- Funding Time: 14-28 days, as their manual underwriting process can take longer than tech-driven platforms.

Ideal For: Investors with unique projects that might be rejected by more automated lenders. If you have a property with a complicated history, are a self-employed investor with non-traditional income documentation, or simply value a personal relationship with your lender, Go Kapital is an excellent choice.

3. LendingOne: Best for Experienced Investors

LendingOne is a well-established national lender that has built a strong reputation for reliability and scalability, particularly among high-volume flippers. They offer a comprehensive suite of loan products for real estate investors, and their processes are highly refined to cater to the needs of professionals managing multiple projects. Their parent company, CoreVest Finance, further enhances their stability and product depth.

Key Features:

- Streamlined Process for Repeat Borrowers: LendingOne excels at creating efficiencies for their existing clients. Once you've closed one loan with them, subsequent deals are often faster and require less documentation.

- Diverse Loan Programs: Beyond fix and flip, they offer rental loans, portfolio loans, and new construction financing, making them a one-stop shop for investors with diverse strategies.

- Certainty of Execution: As a large, well-capitalized lender, LendingOne provides a high degree of confidence that they will be able to close the loans they approve, a crucial factor for experienced investors making non-contingent offers.

Rates and Terms:

- Interest Rates: Competitive rates starting at 9.25% for top-tier borrowers.

- Max Leverage: Up to 90% LTC and 75% ARLTV for investors with a proven track record.

- Minimum Credit Score: A standard 680 FICO score.

- Funding Time: A consistent 14-21 day closing timeframe.

Ideal For: Seasoned investors and real estate professionals who are flipping multiple properties per year. If you have a strong portfolio and need a reliable, institutional-quality lender that can keep pace with your deal flow and support your growth into other real estate strategies, LendingOne is a top contender.

4. Kiavi: Best for Technology and Speed

Kiavi (formerly LendingHome) is a fintech pioneer in the private lending space. They have built their entire business around using technology and data analytics to streamline the loan process, resulting in some of the fastest funding times in the industry. Their online platform provides a user-friendly experience from pre-approval to closing, making them a favorite among tech-savvy investors in a time crunch.

Key Features:

- Data-Driven Valuations: Kiavi leverages vast amounts of property data to generate its own valuations, which can often speed up the appraisal process or, in some cases, replace the need for a full appraisal with an AVM (Automated Valuation Model).

- Online Platform: Their intuitive online portal allows borrowers to apply for a loan, upload documents, and track their progress 24/7 without needing to speak to a loan officer for every minor update.

- Rapid Pre-Approvals: Investors can get a pre-approval letter from Kiavi in minutes, which is a powerful tool for making competitive offers in fast-moving markets.

Rates and Terms:

- Interest Rates: Rates can be very competitive, starting around 9.00%, but can vary based on the data-driven risk assessment of the deal.

- Loan Fees: Fees can have a wider range, from 1.5% to 4.0%, depending on the project and borrower profile.

- Max Leverage: Strong leverage up to 90% LTC and an industry-leading 80% ARLTV on some products.

- Minimum Credit Score: A relatively low entry point of 660 FICO.

- Funding Time: Their key selling point is speed, with closings possible in as few as 7-14 days.

Ideal For: Investors who prioritize speed above all else. If you operate in a market where deals are won or lost in a matter of hours, Kiavi's ability to provide rapid pre-approvals and close loans quickly can give you a significant competitive edge.

5. Lima One Capital: Best for New Construction

While Lima One Capital offers a solid fix and flip loan product, they truly stand out for their comprehensive suite of financing solutions that extend into new construction. For investors looking to transition from renovating existing properties to building from the ground up, Lima One provides a clear and supportive pathway. They have deep expertise in the complexities of construction lending, making them a reliable partner for more extensive projects.

Key Features:

- Fix-and-Flip to New Construction Bridge: They are one of the few lenders that actively cater to investors making the leap into ground-up construction, offering specialized loan products and underwriting that understands the unique timelines and draw schedules involved.

- Broad Product Suite: In addition to fix and flip and new construction, they offer long-term rental loans and financing for multifamily properties, allowing investors to manage their entire portfolio with a single lender.

- National Coverage with Local Expertise: Despite being a large national lender, they have a reputation for understanding the nuances of local markets.

Rates and Terms:

- Interest Rates: Generally start a bit higher, around 9.75%, to account for the added risk and complexity of construction projects.

- Max Leverage: Up to 90% LTC and 75% ARLTV for fix and flip; construction loan leverage is typically based on Loan-to-Cost.

- Minimum Credit Score: 660 FICO.

- Funding Time: Their process is more thorough, especially for construction, so funding times are longer, typically 21-30 days.

Ideal For: Ambitious investors who are either currently involved in new construction or are planning to expand their business from fix and flips into ground-up development. Their expertise in this area provides a level of security and understanding that many other fix and flip lenders cannot match.

6. CoreVest Finance: Best for Portfolio Loans

CoreVest Finance, the parent company of LendingOne, is a giant in the business-purpose lending space. While they offer single-asset fix and flip loans, their primary strength lies in providing portfolio-based financing solutions. For investors who are scaling up and managing multiple fix and flip projects simultaneously, CoreVest offers blanket loans that can simplify financing and unlock better terms.

Key Features:

Portfolio Blanket Loans: CoreVest allows you to finance multiple properties under a single loan, which can be more efficient to manage than numerous individual loans. This structure can also offer more favorable overall terms.

Credit Facilities for High-Volume Flippers: For large-scale operators, CoreVest can provide revolving lines of credit, giving them the flexibility to acquire properties quickly without needing to secure a new loan for each individual purchase.

Institutional-Grade Partner: As one of the largest lenders in the space, they have the capital and infrastructure to handle very large and complex portfolios, providing a level of stability that is attractive to serious investors.

Rates and Terms:

- Interest Rates: Starting around 9.99% for their portfolio products.

- Max Leverage: Typically up to 85% LTC and 70% ARLTV on their portfolio fix and flip loans.

- Minimum Credit Score: A firm 680 FICO is usually required.

- Funding Time: Portfolio loans are more complex to underwrite, so closing times are longer, ranging from 21 to 35 days.

Ideal For: Investors who are operating at scale. If you are managing five or more fix and flip projects at a time and are looking for a more sophisticated financing solution than individual hard money loans, CoreVest's portfolio products are designed specifically for your needs.

7. RCN Capital: Best for Broad Eligibility

RCN Capital has built its brand on being an accessible and accommodating lender. They are known for their willingness to work with a wider range of borrower profiles and property types than many of their competitors. This flexibility makes them a go-to option for investors who may not meet the strict criteria of other institutions, whether due to credit score, experience level, or citizenship status.

Key Features:

- Lower Credit Score Acceptance: RCN Capital will consider borrowers with FICO scores as low as 620, which is significantly lower than the industry standard of 660-680.

- Foreign National Program: They have a well-established program for financing investment properties for non-U.S. citizens, an area many lenders avoid.

- Wide Range of Property Types: They are open to financing unique property types, including mixed-use buildings and smaller multifamily properties.

Rates and Terms:

- Interest Rates: To compensate for the higher risk associated with their flexible guidelines, their rates are higher, starting at 10.25% and going up from there.

- Loan Fees: Points are also on the higher end, typically ranging from 2.5 to 5.0.

- Max Leverage: They still offer strong leverage, up to 90% LTC and 75% ARLTV, but may require more liquidity or a higher down payment for lower-credit borrowers.

- Funding Time: They maintain a respectable funding time of 14-21 days.

Ideal For: Investors who have been turned down by other lenders. This includes investors with bruised credit, those who are just starting out and have no track record, or foreign nationals looking to invest in the U.S. real estate market. The trade-off for this accessibility is higher borrowing costs.

8. FundThatFlip: Best for Crowdfunded Speed

FundThatFlip operates on a crowdfunding model, connecting real estate investors who need capital with a network of accredited investors looking to fund real estate debt. This model allows them to make decisions and fund loans very quickly, as their primary focus is on the viability of the deal itself. If the numbers on the project make sense, they can often find the capital for it rapidly.

Key Features:

- Deal-Centric Underwriting: Their process is heavily weighted towards the economics of the fix and flip project—the purchase price, renovation budget, and ARV. A strong deal can often overcome minor weaknesses in a borrower's profile.

- Fast Funding: By tapping into their network of ready investors, they can often fund loans in as little as 7-14 days, making them competitive with other tech-focused lenders.

- Simple Application Process: Their online application is straightforward and designed to quickly gather the essential information needed to evaluate a deal for funding.

Rates and Terms:

- Interest Rates: Starting at 9.49%.

- Loan Fees: Points typically range from 2.0% to 4.0%.

- Max Leverage: Up to 90% LTC and 70% ARLTV.

- Minimum Credit Score: 660 FICO.

Ideal For: Investors with a great deal who need to close quickly. If your project has a strong potential ROI and you need a lender who will focus on the asset and fund the loan fast, FundThatFlip's crowdfunding platform is a compelling option.

9. New Silver: Best for Instant Proof of Funds

New Silver is another tech-forward lender that leverages artificial intelligence and machine learning to offer a remarkably fast and seamless borrowing experience. Their standout feature is the ability to provide an instant, verifiable Proof of Funds (POF) letter, which is a game-changer for investors who need to make offers on the spot.

Key Features:

- AI-Powered Underwriting: Their proprietary technology can analyze a deal and a borrower's information to provide a term sheet and conditional approval in under 10 minutes.

- Instant Proof of Funds: The ability to generate a POF letter immediately after receiving terms allows investors to submit offers with confidence, knowing their financing is lined up.

- FlipScout Deal Analysis Tool: New Silver provides a tool that helps investors analyze potential deals by providing comps and estimating ARV, integrating the deal analysis and financing processes.

Rates and Terms:

- Interest Rates: Starting at 9.00%.

- Loan Fees: A competitive 1.8% to 2.5% in points.

- Max Leverage: High leverage of up to 90% LTC and 80% ARLTV.

- Minimum Credit Score: An accessible 650 FICO.

- Funding Time: They are among the fastest, with closings in 7-10 days.

Ideal For: Investors who use the "driving for dollars" strategy or need to make multiple offers quickly. If your business model relies on speed and the ability to instantly prove you have the financial backing for an offer, New Silver's technology provides a significant advantage.

Get Your 2026 Term Sheet in 2 Minutes

Instantly compare today’s lowest rates and max LTVs — no hard credit pull required.

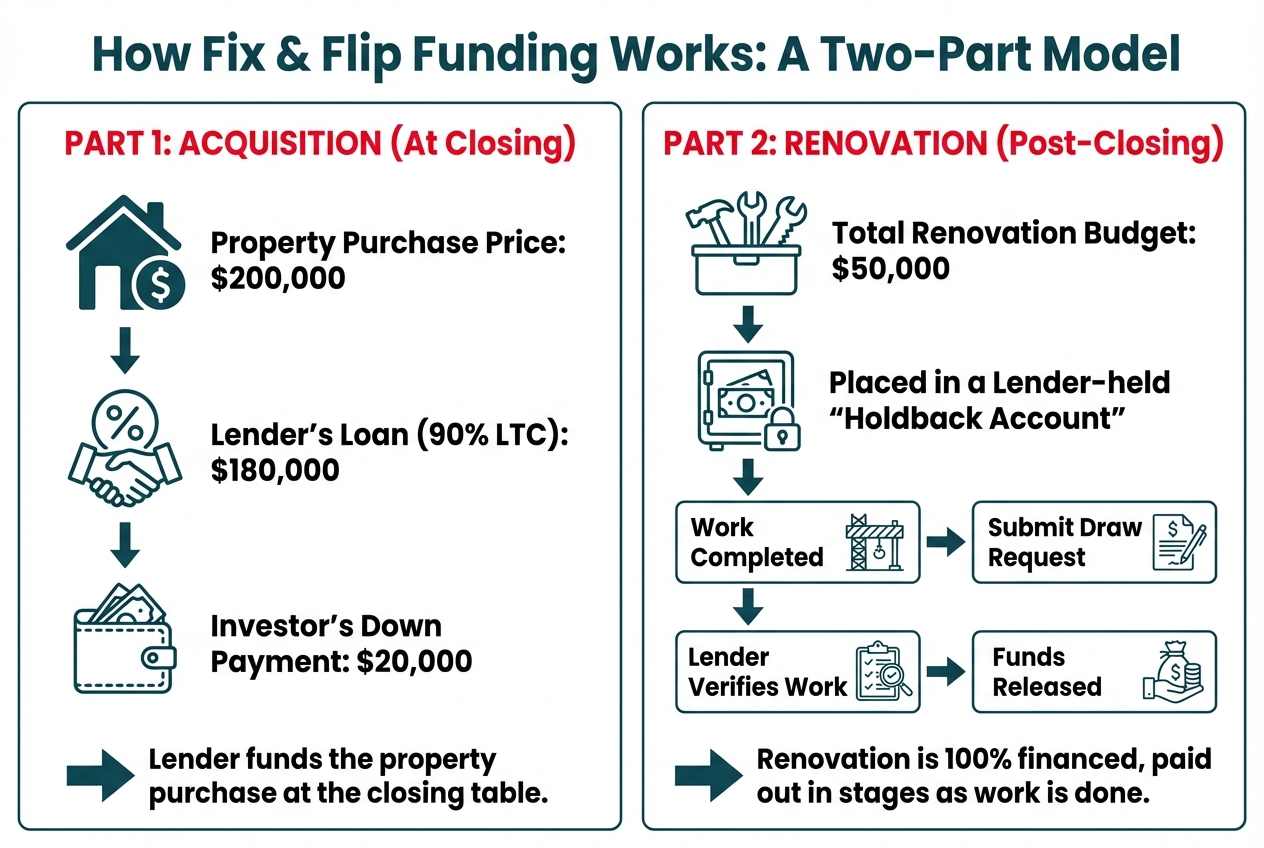

Get Your Quote →How Fix and Flip Loans Work: The Two-Part Funding Model

Understanding the funding structure of a fix and flip loan is crucial for managing your project's cash flow. The loan is not disbursed as a single lump sum at closing. Instead, it operates on a two-part model that separates the funds for acquisition from the funds for renovation.

Part 1: Acquisition Funds at Closing

At the closing table, the lender provides the funds necessary to purchase the property. This amount is based on a percentage of the purchase price, known as the Loan-to-Cost (LTC). For example, if a lender offers 90% LTC on a $200,000 property, they will provide $180,000 at closing. The investor is responsible for the remaining $20,000 down payment, plus any closing costs.

Part 2: The Renovation Holdback Account

The second part of the loan—the entire renovation budget—is not given to you at closing. Instead, the lender places these funds into a separate escrow or "construction holdback" account. This is a critical risk management tool for the lender. It ensures that their capital is being used specifically for the intended renovations that will increase the property's value and secure their investment.

As you complete phases of the renovation, you request funds from this holdback account through a process called a draw request. You might, for example, complete the demolition and framing and then submit a draw request for the funds needed to pay your contractors for that work. The lender will then verify the work is complete (often through an inspection or photos/videos) and release that portion of the renovation funds to you. This process repeats until the project is finished and the entire renovation budget has been disbursed. This model ensures that 100% of the renovation is financed by the lender, but you only receive the money as you create value.

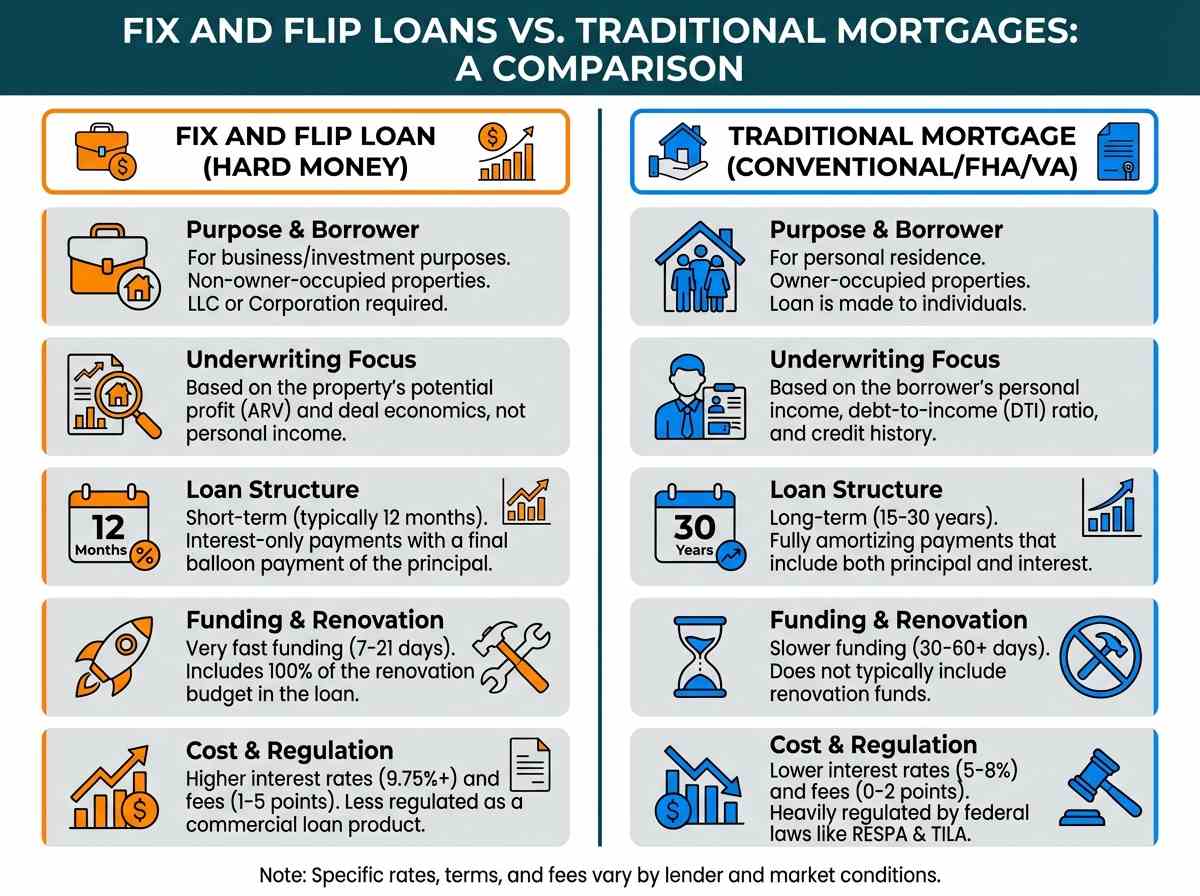

Key Differences from Traditional Mortgages

Investors new to the space often confuse fix and flip loans with the conventional mortgages they might have for their own homes. However, they are fundamentally different products designed for entirely different purposes. Understanding these distinctions is key to navigating the world of real estate investment financing.

Fix and Flip Loan (Hard Money) Vs Traditional Mortgage (Conventional/FHA/VA)

| Feature | Fix and Flip Loan (Hard Money) | Traditional Mortgage (Conventional/FHA/VA) |

|---|---|---|

| Purpose | Business/Investment. For non-owner-occupied properties. | Personal Residence. For owner-occupied properties. |

| Borrower Entity | LLC or Corporation is required by most lenders. | Individual(s). |

| Underwriting Focus | The property's potential profit (ARV) and the deal's economics. | Borrower's personal income, debt-to-income (DTI) ratio, and credit history. |

| Loan Term | Short-term: Typically 12 months. | Long-term: 15, 20, or 30 years. |

| Amortization | Interest-Only. The principal is not paid down monthly. | Fully Amortizing. Each payment includes both principal and interest. |

| Maturity | Balloon Payment. The entire principal balance is due at the end of the term. | The loan is fully paid off at the end of the term through regular payments. |

| Renovation Funds | Includes 100% of the renovation budget in the loan amount. | Does not typically include renovation funds (except for specific products like FHA 203k). |

| Funding Speed | Fast: 7-21 days. | Slow: 30-60 days or more. |

| Interest Rates | Higher: 9.75% - 12%+. | Lower: 5% - 8% (market dependent). |

| Fees | Higher: 1 - 5 points (1 point = 1% of loan amount). | Lower: 0 - 2.0 points. |

| Regulation | Less regulated, as they are commercial loans. | Heavily regulated by federal laws like RESPA and TILA. |

The most significant difference lies in the underwriting philosophy. A traditional mortgage lender, like those reviewed by the Consumer Financial Protection Bureau (CFPB), asks, "Can this person afford to make payments on this home for the next 30 years based on their personal income?" A fix and flip lender asks, "Is this project likely to be profitable enough for the investor to repay the loan within 12 months after the property is sold?" This asset-centric approach is what allows for faster approvals and funding.

Deconstructing Key Leverage Metrics

When you receive a term sheet from a fix and flip lender, you will see several acronyms that define your leverage: LTC, LTFC, and ARLTV. Lenders use a "lesser of" calculation between these metrics to determine your final loan amount. It's essential to understand what each one means and how they interact.

LTC (Loan-to-Cost)

LTC stands for Loan-to-Cost. This metric is almost always used to refer specifically to the purchase price of the property. If a lender offers "up to 90% LTC," it means they will finance up to 90% of the acquisition cost. The investor must cover the remaining 10% as a down payment.

- Formula:

LTC = (Loan Amount / (Purchase Price + Renovation Costs)

LTFC (Loan-to-Total-Cost)

Some lenders may use LTFC, or Loan-to-Total-Cost. This is a more comprehensive metric that includes both the purchase price and the renovation budget. It represents the percentage of the entire project cost that the lender is financing. Since fix and flip loans typically finance 100% of the renovation, a 90% LTC on the purchase often translates to a higher overall LTFC.

- Formula:

LTFC = (Total Loan Amount) / (Purchase Price + Renovation Budget)

ARLTV (After-Repair Loan-to-Value)

ARLTV stands for After-Repair Loan-to-Value. This is the ultimate cap on your loan amount. It compares the total loan amount (purchase + renovation) to the projected value of the property after the renovation is complete. Most lenders cap their ARLTV at 75%. This ensures there is a significant equity cushion (25% or more) in the project, protecting both the lender and the investor from market fluctuations or budget overruns.

- Formula:

ARLTV = (Total Loan Amount) / (After-Repair Value)

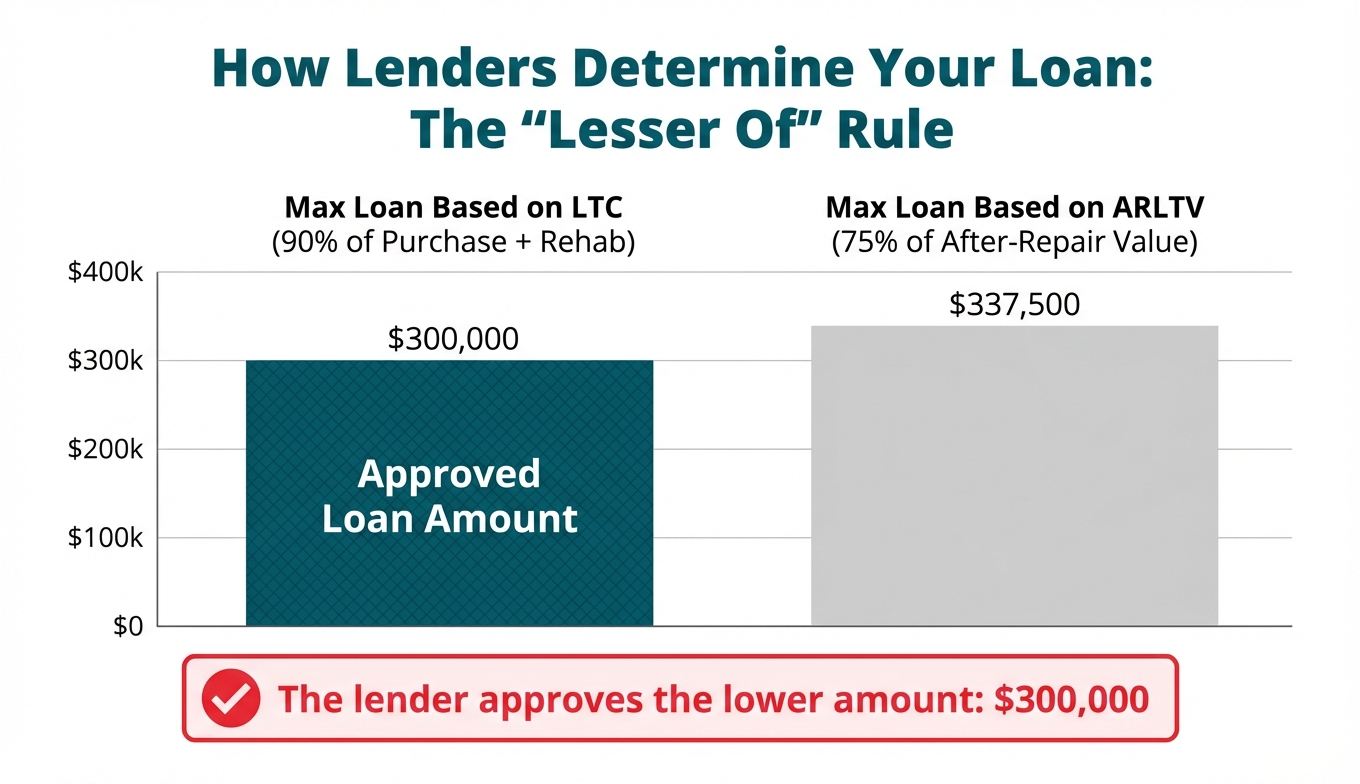

How Lenders Use the "Lesser Of" Calculation

A lender will calculate your maximum loan amount based on all their leverage constraints and offer you the lowest of the resulting figures.

Example: Let's say you're an experienced investor looking at a property with the following numbers:

- Purchase Price: $250,000

- Renovation Budget: $75,000

- After-Repair Value (ARV): $450,000

Your lender, like OfferMarket, offers terms of 90% LTC and 75% ARLTV. Here's how the calculation works:

LTC Calculation (Purchase Only):

- 90% of $250,000 (Purchase Price) = $225,000

- This is the maximum amount they will lend for the purchase.

Total Potential Loan Amount (Based on LTC):

- $225,000 (for purchase) + $75,000 (100% of renovation) = $300,000

ARLTV Calculation (The Hard Cap):

- 75% of $450,000 (ARV) = $337,500

- This is the absolute maximum total loan amount the lender will provide for this project.

The "Lesser Of" Decision:

- The loan amount based on LTC is $300,000.

- The loan amount based on ARLTV is $337,500.

- The lender will approve the lesser of the two, which is $300,000.

In this scenario, your deal fits comfortably within the lender's guidelines. The investor would be responsible for a $25,000 down payment (10% of purchase) plus closing costs.

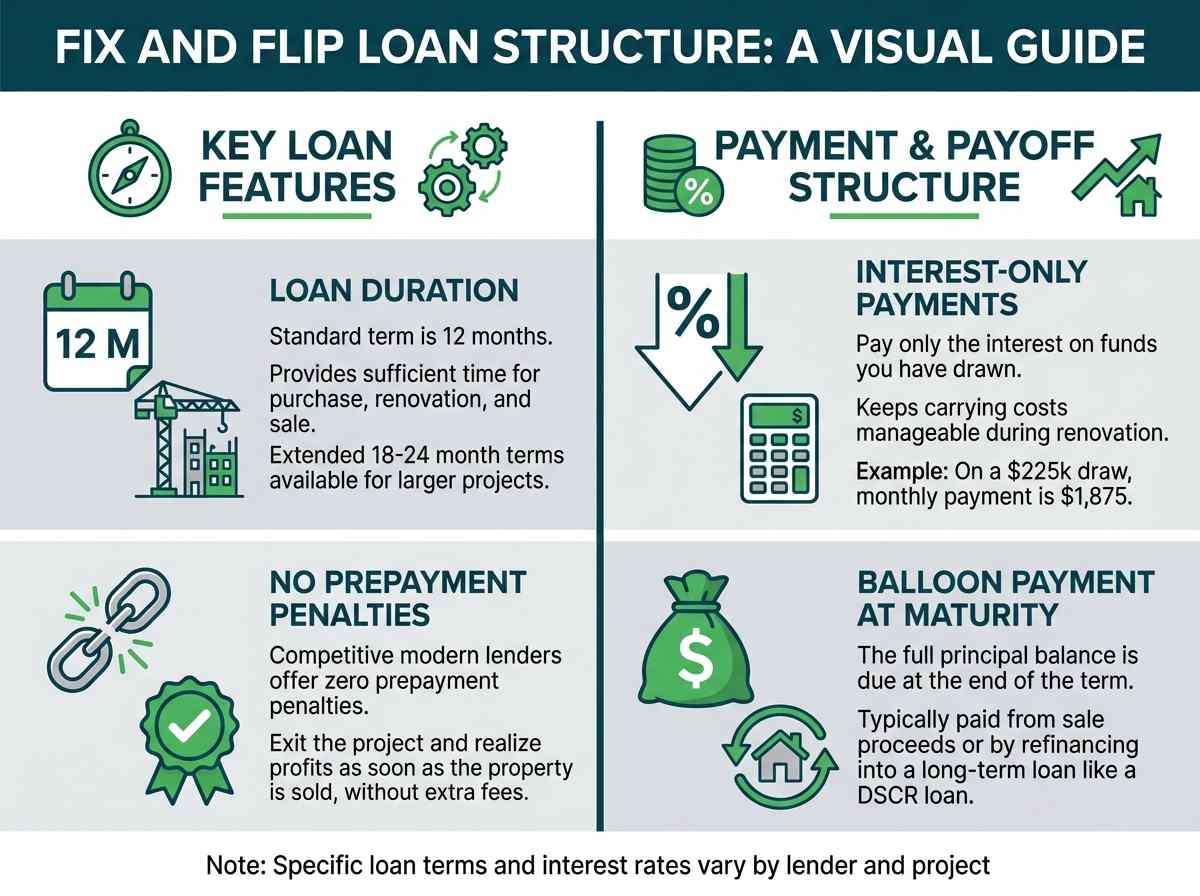

Typical Loan Terms and Structure

While terms can vary between lenders, most fix and flip loans follow a similar structure designed for the short lifecycle of a renovation project.

Duration of the Fix and Flip Loan

The standard loan term is 12 months. This is generally considered sufficient time to purchase, renovate, market, and sell a standard single-family property. For larger, more complex projects (e.g., gut renovations or small additions), lenders may offer 18 or 24-month terms, often at a slightly higher interest rate.

- Payments: As mentioned, payments are interest-only. You are only required to pay the accrued interest each month on the funds you have drawn. For example, if you have a $300,000 loan at 10% annual interest, but have only drawn $225,000 for the purchase and initial work, your monthly payment would be based on the $225,000 balance (

($225,000 * 0.10) / 12 = $1,875), not the full loan amount. This keeps carrying costs manageable during the renovation phase.

Maturity and Payoff

At the end of the 12-month term, the loan "matures," and the full principal balance is due in a single balloon payment. This payment is typically made from the proceeds of selling the property. If an investor decides to keep the property as a rental, they would pay off the fix and flip loan by refinancing into a long-term, amortizing DSCR loan.

Penalties

Historically, hard money loans often came with prepayment penalties or a minimum number of months of interest. For example, a "6-month lock" would mean that even if you sold the property in 3 months, you'd still have to pay 6 months of interest. However, the modern, competitive lending landscape has largely eliminated these. Top-tier lenders like OfferMarket have no prepayment penalties, giving you the freedom to exit the project and realize your profits as quickly as possible.

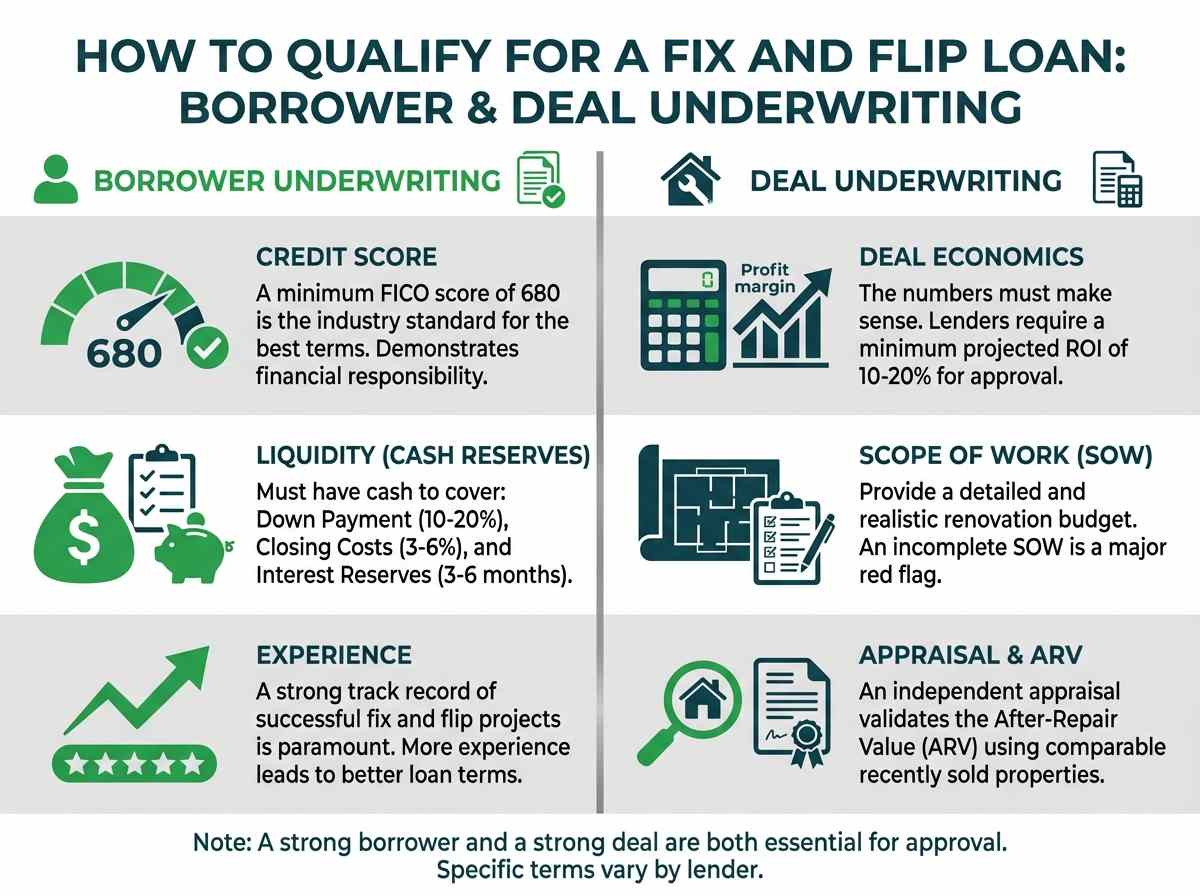

How to Qualify: Borrower and Deal Underwriting

Lenders evaluate two main components when underwriting a fix and flip loan: the borrower (you) and the deal (the property). A strong borrower with a weak deal may be denied, just as a weak borrower with a great deal might be.

Borrower Underwriting

This is where the lender assesses your ability to successfully execute the project and manage the loan.

Credit Score: A minimum FICO score of 680 is the industry standard for the best terms. A strong credit history demonstrates financial responsibility.

Liquidity: This is one of the most important factors. You must have enough cash on hand—"liquid" assets in a bank account—to cover several key items:

- Down Payment: Typically 10-20% of the purchase price.

- Closing Costs: Lender fees, appraisal, title, insurance, etc., which can amount to 3-6% of the loan amount.

- Interest Reserves: Most lenders require you to prove you have enough cash to cover 3-6 months of interest payments. This ensures you can handle the carrying costs even if the project takes longer than expected.

Experience: Your track record as a real estate investor is paramount. Lenders want to see that you have successfully completed fix and flip projects in the past. The more experience you have, the better terms you will receive.

Deal Underwriting

This is where the lender analyzes the property itself to ensure it's a sound investment.

Deal Economics: The numbers must make sense. The lender will run their own analysis on your purchase price, renovation budget, and projected ARV. They will look for a healthy potential profit margin. Most lenders require the project to have a minimum projected ROI of 10-20% to be approved. You can analyze your own deals using a fix and flip calculator to see if they meet these thresholds.

Scope of Work (SOW): You will need to provide a detailed renovation budget and SOW that outlines all the work you plan to do, from materials to labor costs. The lender will review this for reasonableness. An unrealistic or incomplete budget is a major red flag.

Appraisal and ARV: The lender will order an independent appraisal to validate your projected After-Repair Value. The appraiser will look at your SOW and then find comparable recently sold properties (comps) in the area that have been renovated to a similar standard. A deal can fall apart if the appraisal comes in significantly lower than your projection, as it will reduce your maximum loan amount.

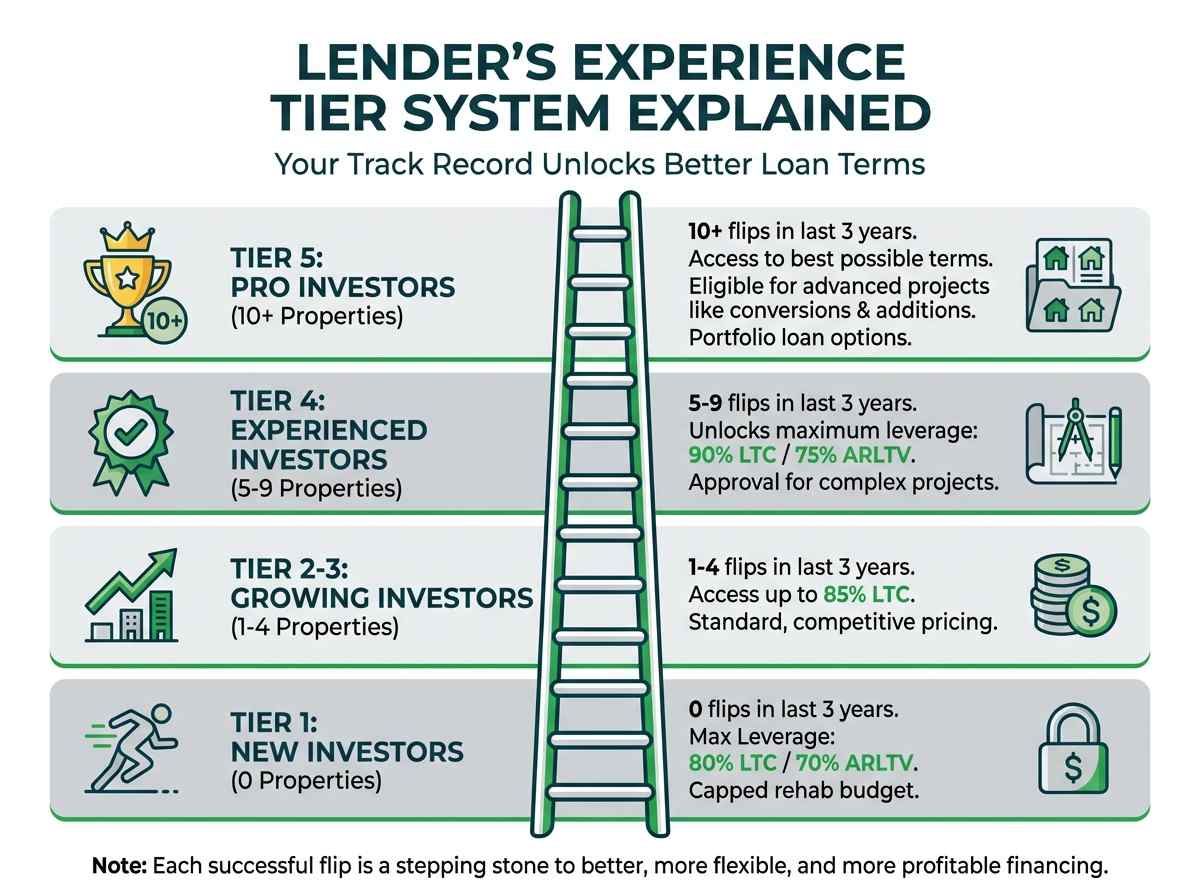

The Lender's Experience Tier System Explained

Your real estate investing experience directly impacts the loan terms you can access. Lenders use a tier system to classify borrowers based on the number of successful projects (purchased, renovated, and sold) they have completed in the last 24-36 months. More experience equals less risk for the lender, which translates into better leverage, lower rates, and access to more complex loan products.

Here is a typical experience tier structure:

Tier 1: New Investors (0 properties)

- Experience: 0 flips completed in the last 3 years.

- Max Leverage: Capped at 80% LTC and 70% ARLTV.

- Rehab Budget: Often capped at a certain percentage of the purchase price (e.g., 100%) or a fixed dollar amount (e.g., $100,000). Lenders are hesitant to fund massive renovations for first-time flippers.

- Rates/Fees: May be slightly higher than for experienced borrowers.

Tier 2-3: Growing Investors (1-4 properties)

- Experience: 1 to 4 flips completed in the last 3 years.

- Max Leverage: Can often access up to 85% LTC, but may still be subject to a 75% ARLTV cap.

- Rehab Budget: Caps on the renovation budget are often relaxed or removed.

- Rates/Fees: Qualify for standard, competitive pricing.

Tier 4: Experienced Investors (5-9 properties)

- Experience: 5 to 9 flips completed in the last 3 years.

- Max Leverage: Unlocks the maximum leverage available, typically 90% LTC and 75% ARLTV.

- Complexity: Can get approved for more complex projects, like those requiring structural changes.

Tier 5: Pro Investors (10+ properties)

- Experience: 10 or more flips completed in the last 3 years.

- Max Leverage: Access to the best possible terms.

- Advanced Projects: Eligible for financing on more complex projects, such as property additions, conversions (e.g., single-family to duplex), and sometimes even ground-up construction.

- Portfolio Options: Can qualify for HELOANs or portfolio loans to manage multiple projects more efficiently.

This tier system is why it's so important to build a strong track record. Each successful flip you complete is a stepping stone to better, more flexible, and more profitable financing on your future deals.

Get Your Personalized Fix and Flip Loan Quote

The data and reviews in this guide provide a strong foundation, but the only way to know the exact terms a lender can offer you is to get a personalized quote. The rates and leverage you qualify for will depend on your specific experience, credit profile, and the economics of your next deal.

As our top-rated lender for 2026, OfferMarket provides an unmatched combination of speed, technology, and transparent, investor-friendly terms. Take the next step and see what you qualify for.

Get an Instant Quote from OfferMarket: Get a real, data-backed loan quote in minutes. See your personalized interest rate, fees, and total loan amount without impacting your credit score.

Analyze Your Next Deal with Our Fix and Flip Calculator: Use our free calculator to stress-test your numbers. Input your purchase price, rehab costs, and ARV to project your potential profit, ROI, and cash-on-cash return.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull