*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Top 10 Blanket Mortgage Lenders for Investors (2026)

A blanket mortgage is a single loan that covers multiple properties, allowing real estate investors to consolidate financing, streamline management, and scale their portfolios more efficiently. Instead of juggling numerous individual loans, you secure one loan with one monthly payment, underwritten based on the collective cash flow and value of your entire portfolio. This financing tool is essential for investors looking to unlock equity, purchase a new group of properties, or simplify their debt structure.

The key to a successful blanket mortgage is the lender. The right partner offers competitive terms, a smooth process, and the flexibility to accommodate your investment strategy. A crucial feature is the partial release clause, which allows you to sell individual properties from the portfolio without having to refinance the entire loan, providing essential flexibility as you manage your assets.

Lender Comparison at a Glance

For investors who need a quick overview, this table compares the top blanket mortgage lenders on the metrics that matter most. It highlights key differences in credit requirements, leverage, and unique features to help you shortlist the best financing partner for your portfolio.

| Lender | Best For | Min Credit Score | Max LTV | Standout Feature |

|---|---|---|---|---|

| OfferMarket | Speed & Technology | 680 | 80% | Fast 10-21 day closing, app-based draws, desktop appraisals |

| Go Kapital | Creative Financing | Varies | Varies | Flexible structures for unique residential & commercial portfolios |

| Lima One Capital | Large Portfolios | 660 | 80% | Institutional-grade financing for experienced investors |

| Visio Lending | Buy-and-Hold Rentals | 680 | 80% | Deep specialization in 1-4 unit long-term rental properties |

| Bankrate | Rate Comparison | N/A | N/A | Aggregator to compare initial offers from multiple lenders |

| SoFi | Fintech Integration | Varies | Varies | Modern platform, good for existing SoFi customers |

| New Silver | Quick Approvals | 650 | 80% | Technology-driven underwriting for rapid closing needs |

| RCN Capital | Complex Deals | 660 | 80% | Experience with short-term rentals and mixed-use portfolios |

| Griffin Funding | Non-QM Solutions | 620 | 80% | Mix of conventional and private lending options |

| Kiavi | Fix-and-Flip Investors | 660 | 90% (ARV) | Tech-centric platform with a focus on short-term bridge loans |

Top 10 Blanket Mortgage Lenders for 2026

Choosing the right lender is as critical as choosing the right properties. Each lender has its own strengths, weaknesses, and ideal client profile. This in-depth review covers the top 10 blanket mortgage lenders to help you find the perfect fit for your real estate investment strategy.

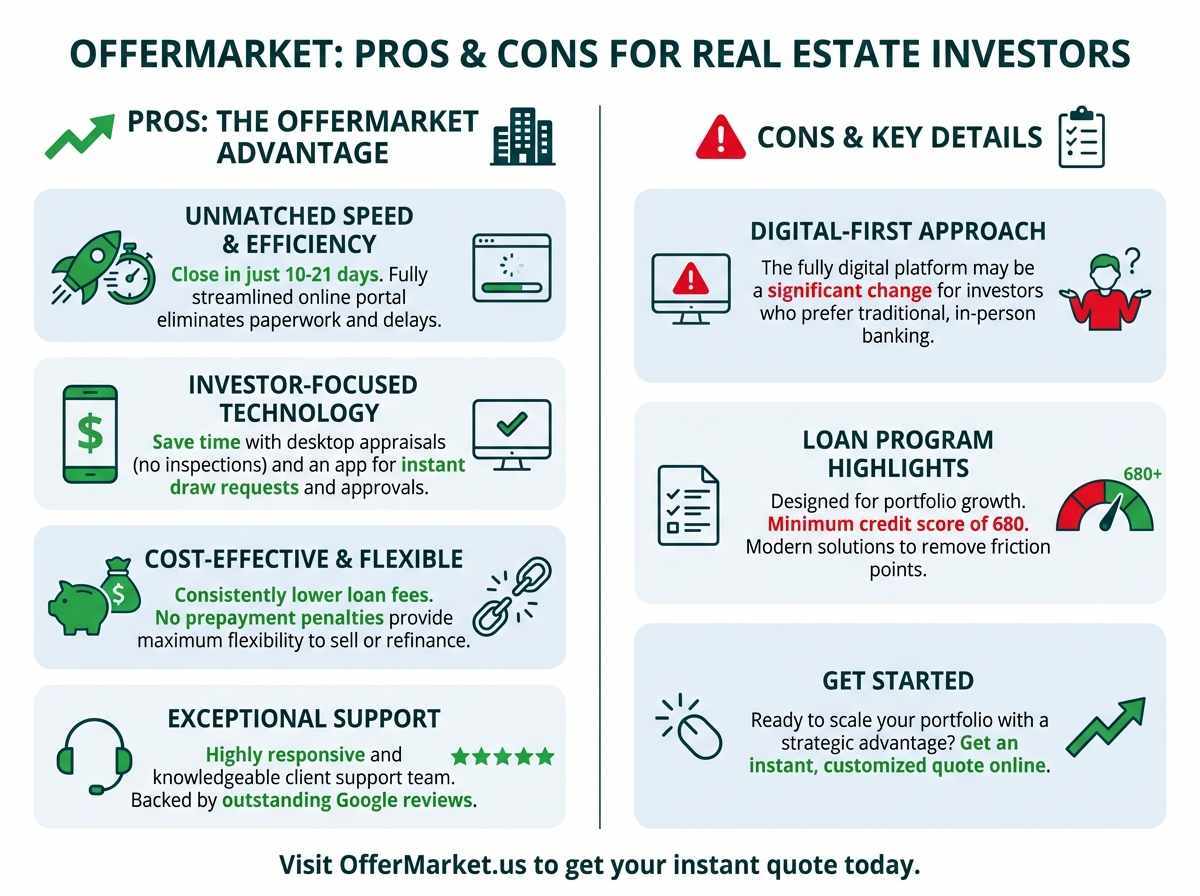

1. OfferMarket: The Top Choice

OfferMarket has established itself as the premier technology-driven lender for modern real estate investors. By integrating technology at every step, from application to draw management, they have created a lending experience that prioritizes speed, efficiency, and transparency. Their platform is designed from the ground up to meet the specific needs of investors who are actively scaling their portfolios and cannot afford the delays and paperwork common with traditional lenders.

Pros and Cons of working with OfferMarket

Pros:

Unmatched Speed: With a closing timeline of just 10-21 days, OfferMarket is one of the fastest lenders in the industry, allowing investors to capitalize on opportunities quickly.

Streamlined Online Process: The entire loan process is managed through a user-friendly online portal, eliminating the need for hard paperwork and cumbersome email chains.

Cost-Effective: OfferMarket consistently offers lower loan fees compared to many competitors, directly improving the investor's bottom line.

Investor-Focused Technology: Features like desktop appraisals (which avoid scheduling physical inspections) and an app for instant draw requests and approvals demonstrate a deep understanding of what investors need to operate efficiently.

Exceptional Support: Despite being a tech-forward company, OfferMarket is known for its responsive and knowledgeable client support, backed by outstanding Google reviews.

Favorable Terms: No prepayment penalties provide investors with maximum flexibility to sell or refinance properties as their strategy evolves.

Cons:

- Digital-First Approach: Investors who are less comfortable with technology or prefer in-person meetings may find the fully digital platform to be a significant change from traditional banking.

Key Details

OfferMarket's blanket loan program is designed for growth. With a minimum credit score of 680, they offer a highly competitive product that combines speed and convenience. Their use of modern solutions removes common friction points, making portfolio management smoother and more profitable. For investors ready to scale, OfferMarket's platform is a strategic advantage. Get an instant quote to see your customized terms.

2. Go Kapital

Go Kapital is a direct private lender that prides itself on offering flexible and creative financing solutions. They cater to a wide range of investors and property types, including those that might not fit the strict criteria of more conventional lenders. Their focus is on asset-backed lending for both residential and commercial properties.

Pros:

Financing Flexibility: Go Kapital is often willing to look at unique portfolios and structure loans creatively to meet specific investor needs.

Broad Asset Focus: They provide financing for a diverse set of real estate assets, which is beneficial for investors with mixed portfolios.

Cons:

Potentially Higher Rates: As a private lender offering more flexible terms, their interest rates and fees may be higher than those from more institutional sources.

Less Transparency: Details on specific terms like LTV, credit score minimums, and fees are not as readily available on their website, requiring direct contact for information.

Key Details:

Go Kapital is a strong choice for experienced investors with unconventional properties or complex financing requirements that fall outside the box of traditional underwriting. Their ability to customize loan structures makes them a valuable partner for opportunistic acquisitions.

3. Lima One Capital

As one of the largest and most established national lenders for real estate investors, Lima One Capital has a long track record of financing investment properties. They offer a comprehensive suite of loan products, including blanket mortgages, for investors at all stages of growth.

Pros:

Extensive Experience: Lima One has deep experience in underwriting and servicing large, complex portfolios, providing a sense of security for investors.

Wide Range of Products: They offer various loan types, including fix-and-flip, new construction, and rental portfolio loans, making them a potential one-stop shop.

Cons:

Less Personalized Process: Due to their size, the loan process can feel more corporate and less personalized compared to smaller, tech-focused lenders.

Potentially Slower Pace: Larger institutions can sometimes have more bureaucracy, which may lead to longer closing times compared to more agile competitors.

Key Details:

Lima One Capital is an excellent option for investors seeking an institutional-grade financing partner with a proven history. They are particularly well-suited for professional investors managing substantial portfolios who value stability and a broad product offering.

4. Visio Lending

Visio Lending has carved out a niche by focusing exclusively on financing for buy-and-hold rental properties. Their entire process and product suite are tailored to the needs of landlords, making them experts in underwriting long-term rental income.

Pros:

Landlord Specialization: Their deep expertise in the 1-4 unit residential rental market means they understand the nuances of tenant income, leases, and property management.

Streamlined for Rentals: The application and underwriting process is specifically designed for rental properties, which can make it more efficient for buy-and-hold investors.

Cons:

Limited Property Scope: They may not be the right fit for investors with portfolios that include short-term rentals, vacant properties undergoing renovation, or commercial assets.

Stricter Guidelines: Their specialization can lead to stricter guidelines for properties or scenarios that fall outside their core focus.

Key Details:

For an investor whose portfolio consists solely of 1-4 unit long-term residential rentals, Visio Lending is a top-tier choice. Their specialized knowledge and tailored process provide significant value for landlords looking to grow their holdings.

5. Bankrate

Bankrate is not a direct lender but a well-known financial marketplace. It allows users to compare rates and terms from a variety of lenders that offer investment property loans, including, at times, those who provide blanket mortgages.

Pros:

Easy Comparison: Bankrate provides a convenient platform to see multiple loan offers side-by-side, giving you a broad view of the market.

Useful Research Tool: It's an excellent starting point for initial research to get a general idea of current interest rates and terms.

Cons:

Middleman Role: You are not dealing with the direct source of capital. The process involves being handed off to the actual lender, which can add steps and potential miscommunication.

Not a Specialist: Bankrate is a general financial aggregator, not a specialist in investor financing. The nuances and complexities of blanket mortgages may not be fully represented.

Key Details:

Bankrate is best used as a preliminary research tool. It can help you gauge the market, but for a complex product like a blanket mortgage, it's crucial to move on to a direct, specialized lender for the actual application and closing process.

6. SoFi

SoFi is a major fintech company that has expanded its product offerings from student loan refinancing to a wide array of financial services, including mortgages. They are gradually making inroads into the investment property loan space.

Pros:

Modern Technology: SoFi's platform is known for being sleek, user-friendly, and mobile-first, which can appeal to tech-savvy investors.

Potentially Competitive Rates: As a large-scale fintech lender, they may offer competitive rates, especially for borrowers with strong credit profiles.

Cons:

Lack of Specialization: Real estate investment loans are not their core business. Their teams may lack the deep, hands-on expertise found at dedicated investor lenders like OfferMarket.

Less Flexibility: Their underwriting is often more automated and may be less accommodating of unique property portfolios or investor situations.

Key Details:

SoFi could be a good option for investors who already have a relationship with the company for other financial products and have a straightforward, easy-to-underwrite portfolio. However, those needing specialized knowledge may be better served elsewhere.

7. New Silver

New Silver is a fintech lender that has built its reputation on speed, particularly in the short-term financing world of fix-and-flip loans. They leverage technology to provide rapid approvals and funding.

Pros:

Exceptional Speed: Their technology-driven underwriting platform can provide loan approvals in minutes and closings in a matter of days.

Focus on Technology: Similar to OfferMarket, they prioritize a streamlined, digital experience for the borrower.

Cons:

Focus on Short-Term Loans: Their expertise and most competitive products are often in the fix-and-flip and bridge loan space. Their long-term rental or blanket loan offerings may be less developed.

May Not Be Best for Stabilized Portfolios: Their model is optimized for transactional speed, which may be less of a priority (and potentially more expensive) for investors seeking to refinance a stable, long-term portfolio.

Key Details:

New Silver is an ideal lender for investors who need to close on a portfolio acquisition with extreme urgency. Their speed is a major asset in competitive bidding situations.

8. RCN Capital

RCN Capital is a large, national, direct private lender with a well-established presence in the real estate investor market. They offer a broad suite of loan products for various investor needs.

Pros:

Reputation for Closing: They have a strong reputation for being able to fund complex deals that other lenders might turn down.

Broad Product Suite: RCN offers financing for short-term rentals, multifamily properties, and mixed-use portfolios, making them versatile.

Cons:

Slower Process: As a larger, more established institution, their process can sometimes be slower and more document-intensive than newer, tech-focused lenders.

Less Flexibility on Some Terms: Their size can sometimes translate to more rigid underwriting guidelines on certain deal points.

Key Details:

RCN Capital is a reliable choice for seasoned investors with diverse portfolios, especially those including short-term rentals or mixed-use properties. Their experience in handling complexity is a significant advantage.

9. Griffin Funding

Griffin Funding operates in both the conventional and non-QM (Non-Qualified Mortgage) lending spaces. Their non-QM offerings include products tailored for real estate investors, such as DSCR loans and blanket mortgages.

Pros:

Non-QM Expertise: They are strong in the non-QM space, which is where most blanket mortgages fall. This means they are experienced with asset-based underwriting.

Variety of Solutions: They can offer both government-backed and private lending solutions, providing a range of options for borrowers.

Cons:

Not Their Sole Focus: Blanket loans are just one of many products they offer. This can mean their teams are less specialized compared to a lender that focuses exclusively on investor loans.

Process Can Vary: The experience can differ depending on whether you are pursuing a conventional or non-QM loan path within their system.

Key Details: Griffin Funding is a solid contender for investors who may also need other types of non-QM financing. Their expertise in DSCR underwriting is a key benefit for those financing cash-flowing rental properties.

10. Kiavi

Kiavi, formerly known as LendingHome, is a major technology-centric lender in the real estate investment space. Their primary focus has historically been on fix-and-flip and bridge loans, where their speed and online platform shine.

Pros:

Excellent Technology: Kiavi's online platform is widely regarded as one of the best in the industry, offering a smooth and transparent user experience.

Extremely Fast Funding: Like New Silver, they are built for speed and can close loans very quickly, which is a major advantage for acquisitions.

Cons:

Blanket Loans are Secondary: Their core business is short-term financing. While they offer rental portfolio loans, these products may be a secondary focus and less competitive than their bridge loan offerings.

May Not Be Ideal for Refinancing: Their model is better suited for the fast pace of acquisitions rather than the more nuanced needs of a portfolio refinance.

Key Details:

Kiavi is an excellent choice for investors who are also active in the fix-and-flip space and appreciate a top-tier technology platform. Their speed is a powerful tool for investors who need to move fast.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Scaling Your Portfolio: What is a Blanket Mortgage?

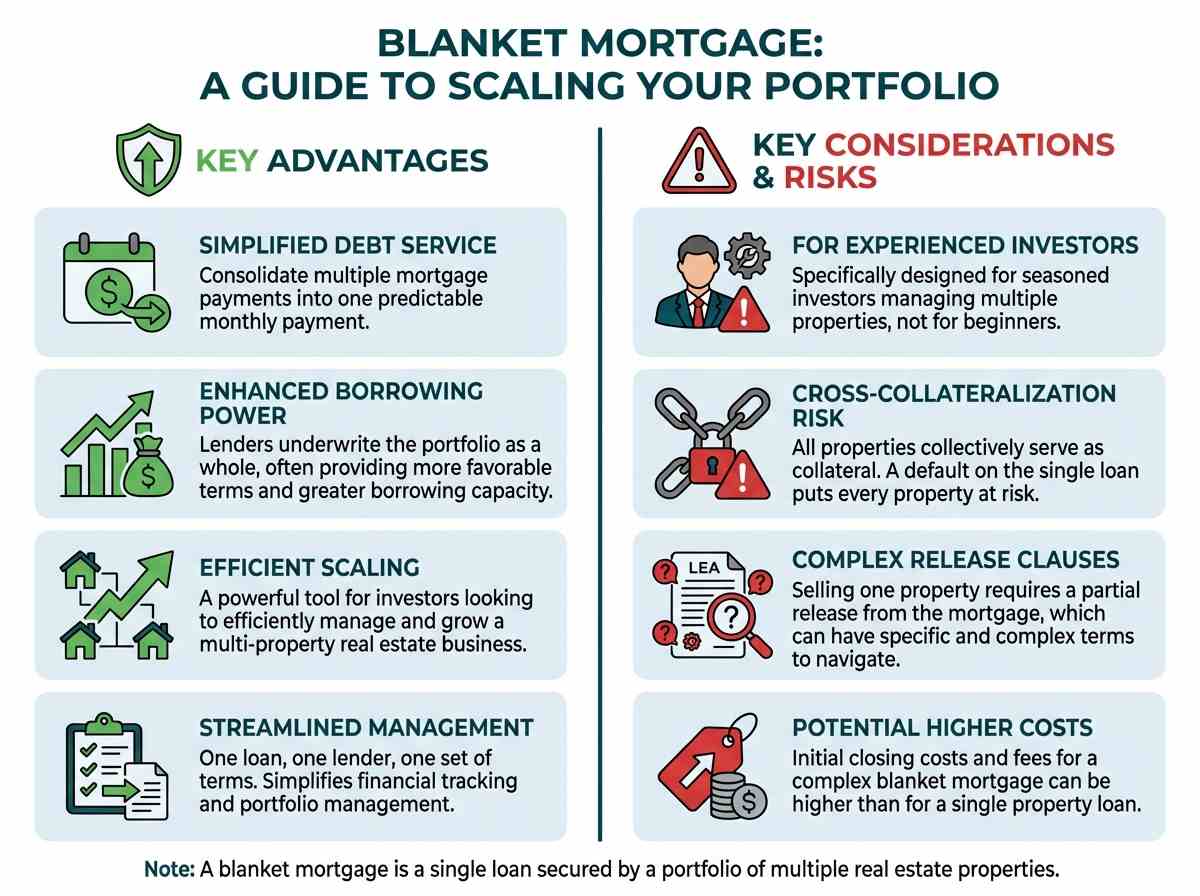

A blanket mortgage is a single loan secured by a portfolio of multiple real estate properties. Instead of obtaining an individual mortgage for each property—each with its own payment, interest rate, and terms—an investor can use a blanket mortgage to consolidate financing. This structure utilizes a concept called cross-collateralization, where the equity in all properties within the portfolio collectively serves as collateral for the single loan.

This type of financing is specifically designed for experienced real estate investors who are managing or looking to acquire multiple properties. It simplifies debt service by consolidating numerous mortgage payments into one predictable monthly payment. By underwriting the portfolio as a whole, lenders can often provide more favorable terms and greater borrowing power, making it a powerful tool for efficiently managing and scaling a real estate business.

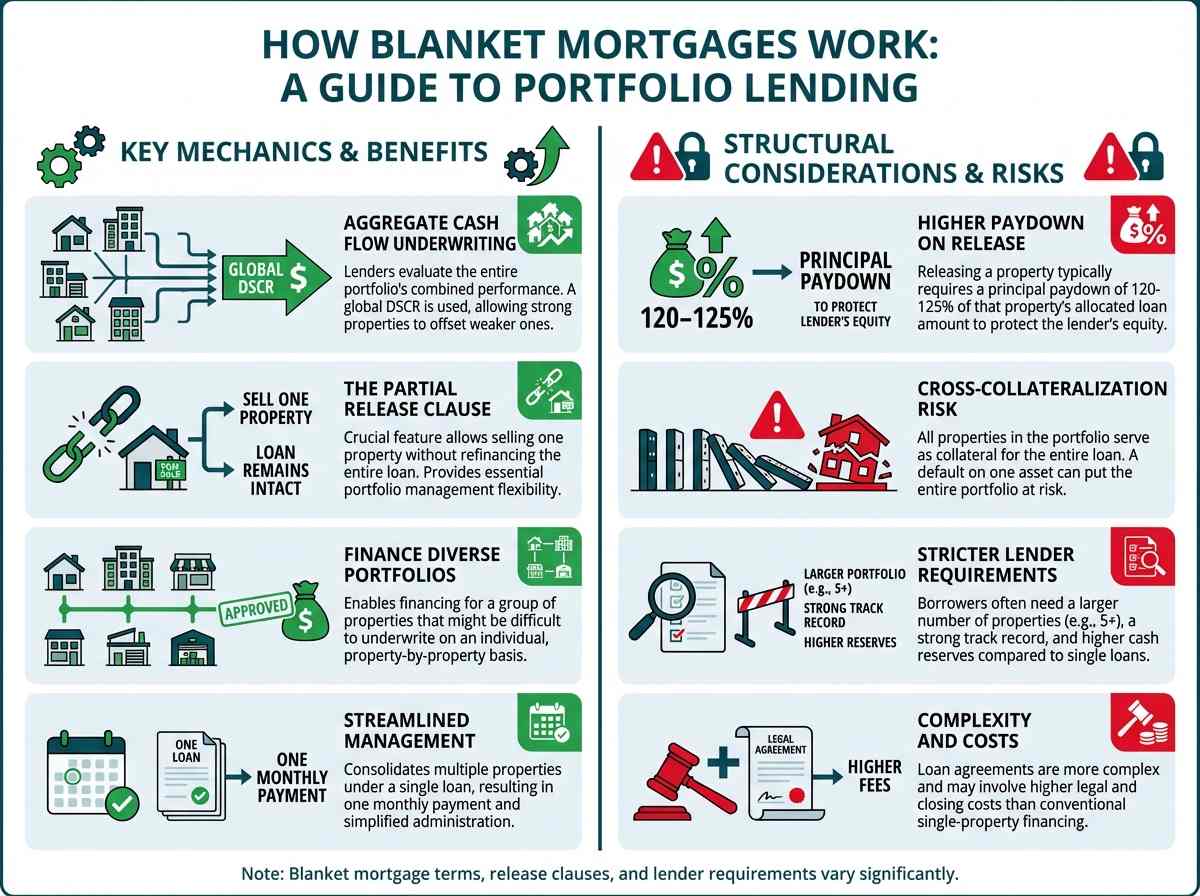

How Blanket Mortgages Work: The Mechanics of Portfolio Lending

The underwriting and structure of a blanket mortgage differ significantly from a conventional single-property loan. The focus shifts from a single asset's performance to the health of the entire portfolio.

Aggregate Cash Flow Underwriting

Instead of analyzing each property in isolation, lenders evaluate the aggregate performance of the entire portfolio. The primary metric used is the global Debt Service Coverage Ratio (DSCR), which measures the portfolio's total rental income against its total debt obligations (including principal, interest, taxes, insurance, and HOA fees). A strong-performing property can help offset a weaker one, allowing investors to finance a diverse portfolio that might be difficult to finance on a property-by-property basis. You can use a DSCR calculator to analyze your portfolio's performance.

The Partial Release Clause

This is arguably the most critical feature of a blanket mortgage. A partial release clause is a provision in the loan agreement that allows the borrower to sell one or more properties from the portfolio without triggering a due-on-sale clause for the entire loan. This gives the investor crucial flexibility. To release a property, the lender typically requires a paydown of the loan principal that is greater than the value of the property being sold, often around 120-125% of the allocated loan amount for that specific property. This overpayment serves to increase the lender's equity cushion in the remaining collateral.

Qualifying for a Blanket Mortgage: Underwriting Checklist

Qualifying for a blanket mortgage is more complex than for a single-family rental loan. Lenders assess the investor's experience, the quality of the portfolio, and key financial metrics.

Investor Experience Requirements

Track Record: Lenders typically require investors to have a demonstrated history of successfully owning and managing investment properties. This is often quantified as a minimum number of properties currently owned (e.g., 2-4) or a minimum number of completed flips in the last 24-36 months.

Financial Strength: A strong personal financial statement, including evidence of liquidity (cash reserves), is essential. Lenders need to see that you can cover debt service during unexpected vacancies or repairs.

Entity Requirement: Loans are almost always made to a business entity, such as an LLC or corporation, rather than to an individual. This protects both the lender and the borrower.

Portfolio and Property Guidelines

Portfolio Size: Lenders have minimums and maximums for the number of properties in a single blanket loan, typically ranging from 2 to 25 properties.

Loan Amounts: There will be a minimum loan amount per property (e.g., $50k-$100k) and a maximum total loan amount for the portfolio (e.g., $2M to $6.25M+, with some lenders going much higher).

Eligible Properties: The most common eligible property types are 1-4 unit residential properties, condos, and townhomes. Some lenders, like RCN Capital, may also finance multifamily or mixed-use portfolios.

Financial Metrics: LTV and DSCR

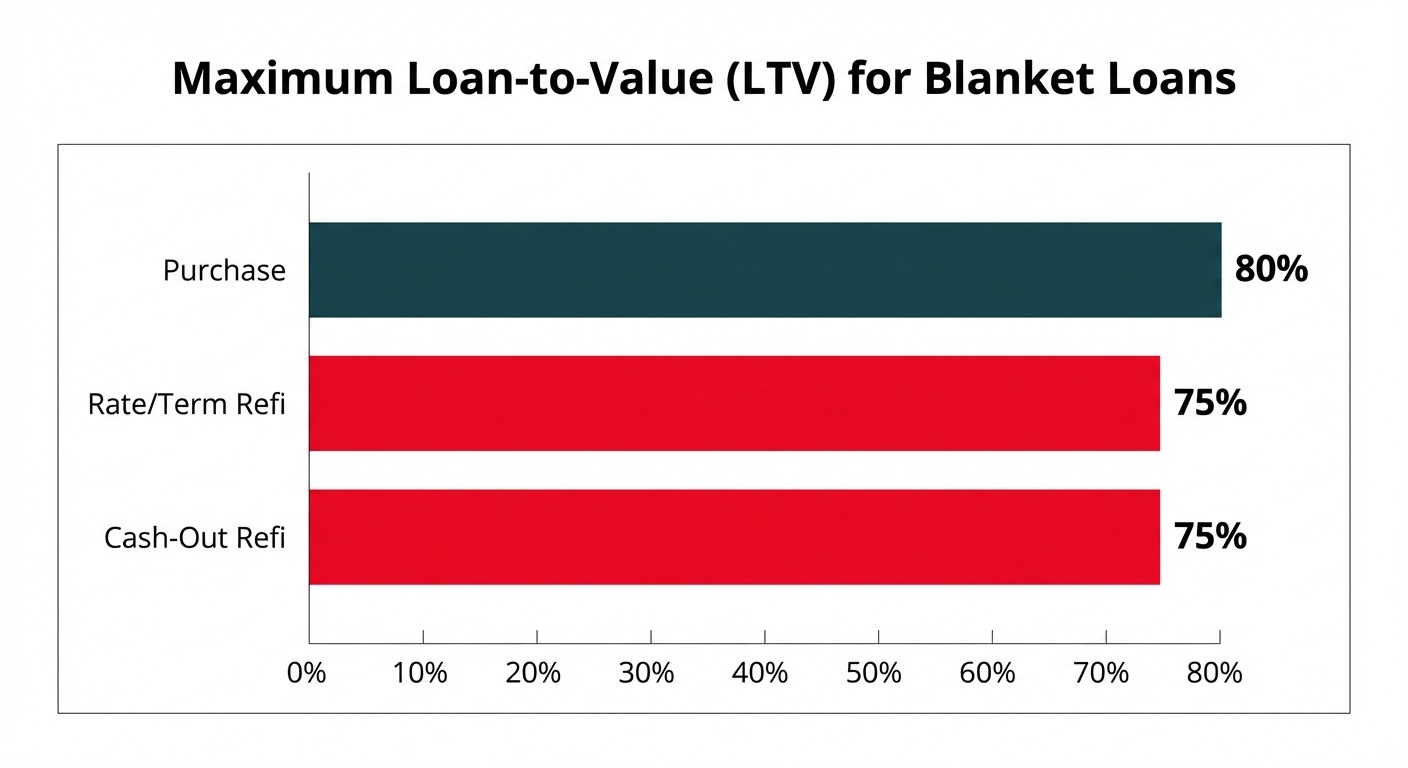

Loan-to-Value (LTV): The maximum LTV is a key metric. For a portfolio purchase, lenders may go up to 80% LTV. For a cash-out refinance, where the risk is perceived as higher, the maximum LTV is often capped at 75%.

Portfolio DSCR: Lenders require the portfolio's overall DSCR to be above a certain threshold, typically between 1.00x and 1.20x. A DSCR of 1.20x means the portfolio's income is 120% of its debt obligations.

Individual Property DSCR: While the portfolio's aggregate performance is most important, lenders often have a floor for individual properties. They may require that no single property in the portfolio has a DSCR below 0.75x to prevent one very poor-performing asset from dragging down the average.

Occupancy and Property Type Restrictions

Occupancy Rate: Lenders often require a minimum portfolio occupancy rate, typically 90% by unit, to ensure stable cash flow.

Geographic Concentration: Underwriters will review the geographic location of the properties. A high concentration in a single neighborhood or market can be seen as a risk, and the lender may reduce leverage to compensate.

Unique Properties: Non-warrantable condos, rural properties, or other unique assets may face lower LTV limits or be excluded from the portfolio altogether.

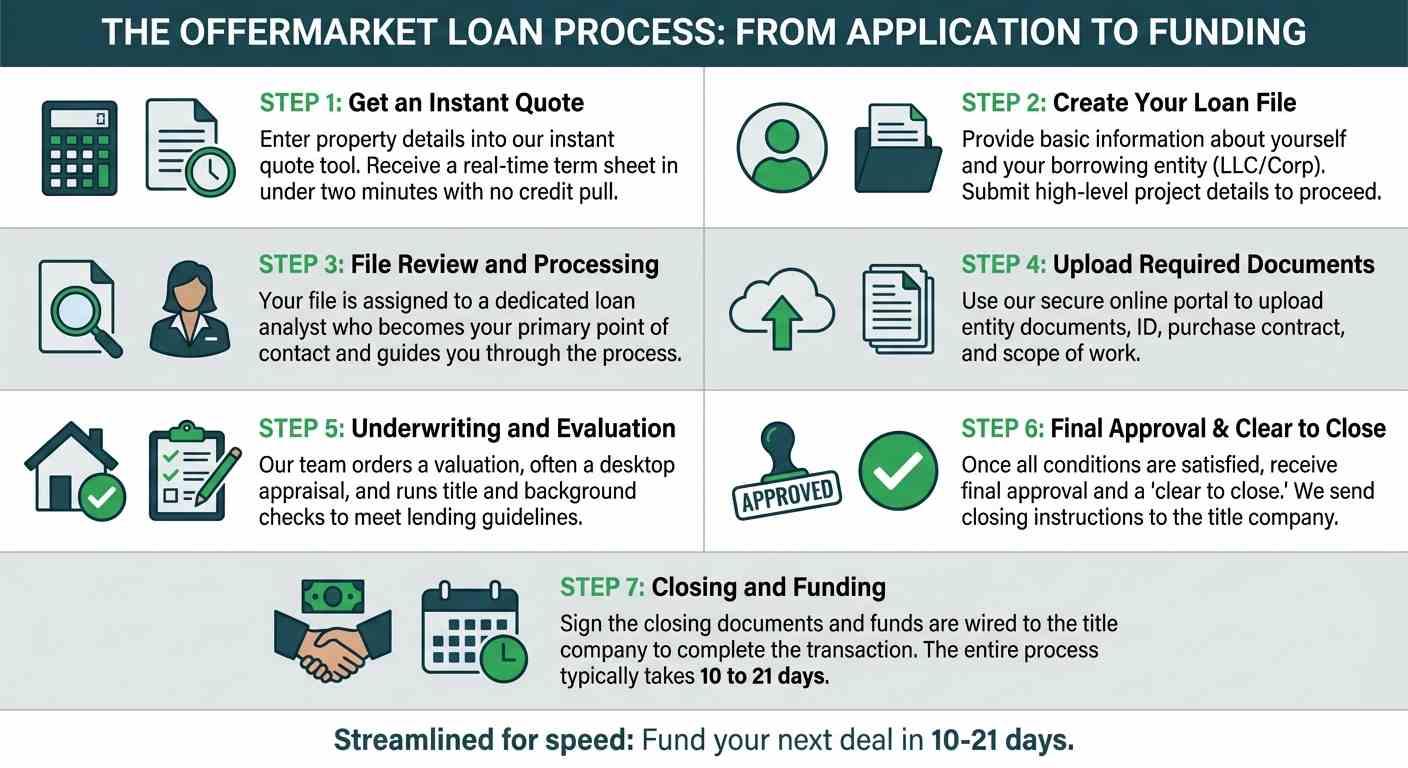

The OfferMarket Loan Process From Application to Funding

While specific steps vary by lender, the journey from application to funding for a blanket loan generally follows a clear path. Tech-forward lenders like OfferMarket have streamlined these steps to accelerate the timeline.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Take the Next Step with OfferMarket

Choosing the right financing is the key to unlocking your portfolio's true potential. While many lenders offer blanket mortgages, OfferMarket stands apart by combining speed, technology, and an unwavering focus on the investor's experience. Our process eliminates the friction points and delays that hold you back, allowing you to close in as few as 10-21 days. With modern tools like desktop appraisals and an app-based draw system, we put control back in your hands.

Don't let slow, outdated lending processes dictate the pace of your growth. Empower your real estate investment strategy with a financing partner built for the modern investor.

- Get your instant blanket mortgage quote today and see the customized rates and terms you qualify for in minutes.

Analyze your numbers with our free DSCR Calculator and Rental Portfolio tools to make data-driven decisions.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull