Hard Money Loan South Dakota

OfferMarket Loans

Check your rate

60 seconds · no credit pull

Last updated: May 19, 2025

At OfferMarket, our mission is to empower you to build wealth through South Dakota real estate. To support your investing journey across the Mount Rushmore State, we provide a comprehensive platform:

💰 Private lending tailored for South Dakota properties

☂️ Insurance rate shopping designed for South Dakota market risks

🏚️ Off market properties in South Dakota neighborhoods and cities

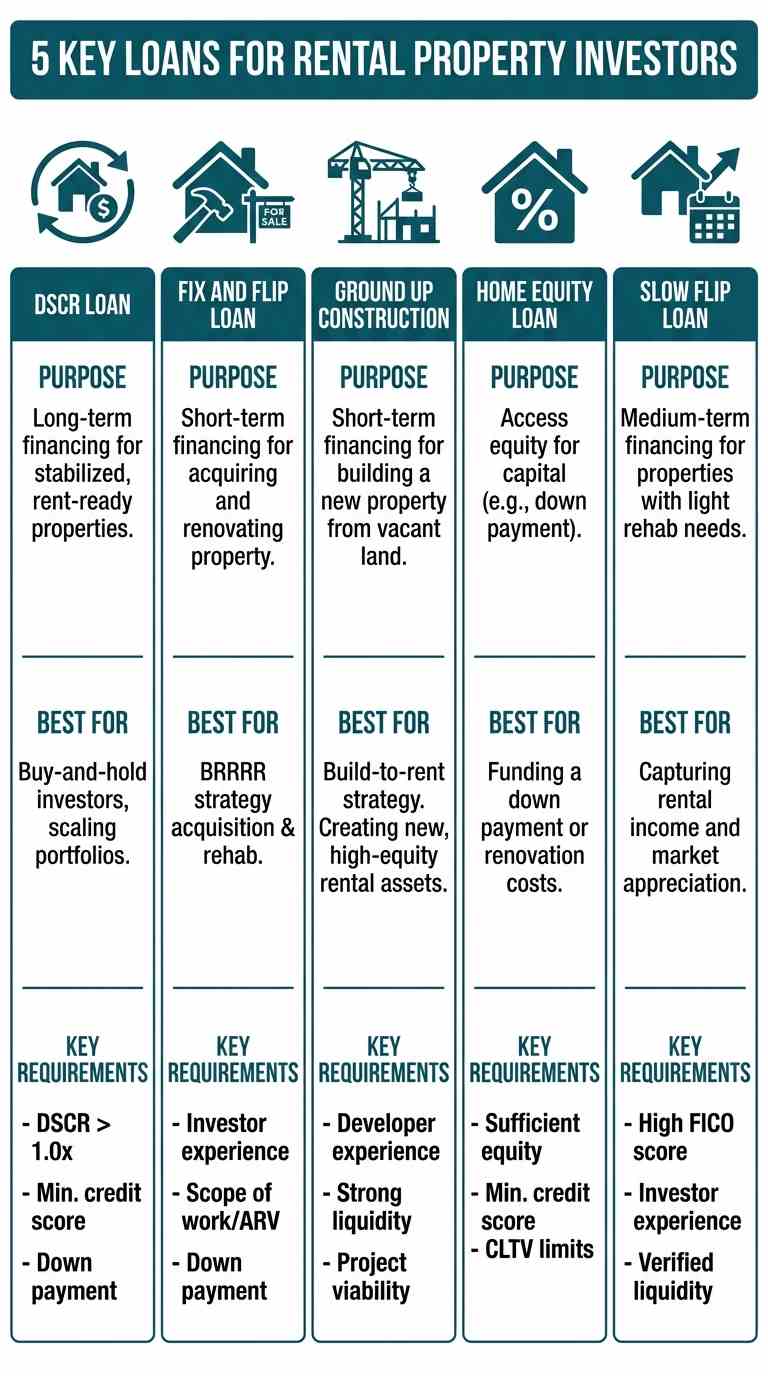

Our Hard Money Loan South Dakota program delivers quick, reliable, and competitive financing to purchase, refinance, and renovate 1-4 unit residential investment properties throughout the state.

Whether your plan is to flip a property for profit in Sioux Falls or Rapid City, or rent and refinance into a DSCR loan, we are eager to help you succeed in South Dakota’s real estate market.

Let’s explore the OfferMarket Hard Money Loan South Dakota Program!

What is a hard money loan South Dakota?

A hard money loan in South Dakota is a short-term, asset-backed loan using 1-4 unit residential real estate as collateral. It provides the capital to buy, refinance, and rehab properties in South Dakota to either flip for profit or hold as rentals in your investment portfolio.

In the South Dakota real estate community, hard money loans are often called “bridge loans” or “fix and flip loans.” These terms are widely used among local investors and private lenders alike.

Hard money loan South Dakota scenarios

South Dakota real estate investors typically use hard money loans for:

Buying and renovating older homes in neighborhoods like Pierre or Aberdeen to modernize and increase property value without tying up their own cash

Refinancing properties bought with cash in fast-paced markets like Brookings and then funding rehab projects

Refinancing existing loans on properties needing updates, allowing time and funds to finish renovations before selling or refinancing into long-term rental loans

Acquiring below-market off market properties across South Dakota’s small towns to sell “as-is” for profit

Tapping equity on cash purchases without plans to rehab, preparing to sell or reinvest elsewhere in the South Dakota market

Refinancing properties where rehab is complete but needing time to sell or refinance without rehab funds

How it works in South Dakota

A hard money loan South Dakota has two parts:

- Initial Advance – The loan amount wired to the title company at closing to cover the property purchase price.

- Construction Holdback – The portion of the loan reserved for property rehab, paid out to you as draws during construction.

These loans are flexible to fit your South Dakota project needs. You may only want an initial advance or only a construction holdback, or both combined to maximize leverage and minimize cash outlay.

For example, if you’re purchasing a fixer-upper in Sioux Falls, you might use both components to cover buying and rehab costs. Or if you bought a property outright in Rapid City and want funds just for renovation, a construction holdback alone may suffice.

Your exit strategy in South Dakota will usually be to flip for profit or rent and refinance with a DSCR loan. Market fluctuations in cities like Sioux Falls may lead you to change your exit plan, and that flexibility helps mitigate risk in the South Dakota market.

You might start a project planning to buy, rehab, rent, refinance, and repeat (BRRRR method) but find that rental demand in smaller South Dakota towns is softer than expected, making a profitable resale the better option.

Or you might intend to flip a property in Rapid City, but if the market slows, you could rent it out and refinance with a DSCR loan, giving you time to sell when the market rebounds.

These dual strategies are critical for South Dakota investors seeking to navigate local market cycles safely.

Who uses hard money loans in South Dakota?

Fix and flip investors active in South Dakota’s residential markets

Rental property investors using the BRRRR strategy in cities like Sioux Falls, Rapid City, and beyond

Many South Dakota investors employ hybrid strategies, flipping some homes while renting others based on current market conditions — a proven best practice we support.

Hard Money Loan Program Guidelines

| Criteria | Guideline |

|---|---|

| Loan amount (minimum) | $25,000 |

| Loan amount (maximum) | $2,000,000 |

| ARV (minimum) | $100,000 |

| Experience | Not required |

| Credit score (minimum) | 680 |

| Borrowing entity | LLC or Corporation |

| Initial advance | Up to 90% |

| Construction holdback | Up to 100% |

| LTARV (maximum) | 75% |

| Interest rate | Get instant quote |

| Origination fee | 1.5 to 2 points |

| Term | 12 to 24 months |

| Points out | None |

| Prepayment penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full (51% of borrowing entity must guarantee) |

| Exit strategy: Sale | Minimum 30% ROI |

| Exit strategy: Refinance | Minimum 1.1 DSCR after repairs |

| Valuation | Appraisal or In-house valuation |

| SqFt (minimum) | Single family: 700+ |

| 2-4 unit: 500+ per unit | |

| Condo: 500+ | |

| Acreage (maximum) | 5 acres |

| Interest accrual | Under $100K loan: full boat |

| $100K+ loan: as disbursed | |

| Advanced draws | Lender discretion |

| Down payment (minimum) | $10,000 |

Project Eligibility in South Dakota

Our mission is to help you build wealth through South Dakota real estate, and managing risk is a top priority. Across our lending portfolio in the Mount Rushmore State, less than 0.5% of loans have ever defaulted and gone into foreclosure. Your success is our pride, and we strive to maintain the lowest default rates in South Dakota’s private lending market.

Borrowers with limited experience who take on highly complex rehab projects in South Dakota’s smaller cities or rural areas face the greatest financial risks. Heavy rehab projects often encounter delays, cost overruns, and shifting market conditions which can challenge even seasoned South Dakota investors—especially during uncertain economic times.

As your hard money lender in South Dakota, we act as your partner, advisor, and risk manager. Clear expectations are crucial to help you safely grow your real estate business across South Dakota’s diverse markets. Below you’ll find our rehab scope classifications and eligibility criteria customized for South Dakota investments.

Initial Advance for South Dakota Hard Money Loans

The initial advance is determined by your experience, deal specifics, and local South Dakota market conditions. We consider your portfolio of South Dakota investment properties in the last 24 months and verified rehab projects over five years.

Minimum credit score is 680, with a strong preference for guarantors scoring 720+. Licensed Realtors, General Contractors, and Professional Engineers in South Dakota receive increased leverage.

If the purchase price exceeds the appraised “As Is” value in South Dakota, the initial advance is based on the lower appraised value, not the contract price.

Your exit strategy affects initial advance eligibility. Selling projects require at least a 30% gross margin and $15,000 profit projection. Renting and refinancing projects must demonstrate a minimum 1.1 DSCR after repairs. Use our South Dakota Fix and Flip Calculator and DSCR Calculator to analyze your options.

Properties designated as rural by CFPB or USDA in South Dakota have limited initial advances and require minimum experience tier 3.

Experience-based Tiers for South Dakota Investors

| Tier | Verifiable Experience in South Dakota |

|---|---|

| 1 | 0 projects |

| 2 | 1 to 2 projects |

| 3 | 3 to 4 projects |

| 4 | 5 to 9 projects |

| 5 | 10+ projects |

Initial Advance by Tier for South Dakota

| Tier | Initial Advance (% of Purchase Price) |

|---|---|

| 1 | 80%* |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

85% may be available as an exception for borrowers with excellent credit and liquidity in South Dakota.

Adjustments to Initial Advance in South Dakota

| Scenario | Adjustment |

|---|---|

| Credit score less than 720 | -5% |

| Full gut rehab | -5% |

| New South Dakota market | -5% |

| Licensed South Dakota Realtor | +5% |

| Licensed South Dakota General Contractor | +10% |

| Licensed South Dakota Professional Engineer | +10% |

| Rural South Dakota property | -20% (experience 3+) |

Rehab Scope Classification for South Dakota

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget less than 25% of purchase price |

| Moderate | Rehab budget 25% to 49.99% of purchase price |

| Heavy | Rehab budget 50% to 99.99% of purchase price |

| Extensive | Rehab budget 100%+ of purchase price – includes additions, expansions, or ADUs; low purchase price “lopsided” deals* |

In South Dakota, “lopsided deals” occur when rehab costs exceed the purchase or As Is value, common in some rural or smaller markets.

Rehab Scope Eligibility in South Dakota

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | Eligible | Eligible | Eligible | Eligible | Eligible |

| Moderate | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Heavy | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Extensive | Ineligible | Ineligible | Eligible | Eligible | Eligible |

LTARV Limits in South Dakota

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | 70% | 70% | 75% | 75% | 75% |

| Moderate | Ineligible | 70% | 75% | 75% | 75% |

| Heavy | Ineligible | 70% | 75% | 75% | 75% |

| Extensive | Ineligible | Ineligible | 70% | 70% | 70% |

LTFC Limits in South Dakota

LTFC (Loan-to-Full-Cost) applies to extensive rehab scopes in South Dakota, ensuring borrowers retain equity in higher risk projects.

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | N/A | N/A | N/A | N/A | N/A |

| Moderate | Ineligible | N/A | N/A | N/A | N/A |

| Heavy | Ineligible | N/A | N/A | N/A | N/A |

| Extensive | Ineligible | Ineligible | 85% | 90% | 90% |

Example: No Experience, South Dakota Property

Purchase price: $100,000

Tier: 1 (0 similar verified projects)

Credit score: 695

Rehab budget: $24,000

ARV: $150,000

Initial advance: $75,000 (75%)

Construction holdback: $24,000

Total loan amount: $99,000

LTARV: 66%

LTFC: 79.8%

Interest accrual: Full boat

Example: No Experience, Excellent Credit, South Dakota

Purchase price: $100,000

Tier: 1 (0 projects)

Credit score: 750

Rehab budget: $24,000

ARV: $150,000

Initial advance: $80,000 (80%)

Construction holdback: $24,000

Total loan amount: $104,000

LTARV: 69.33%

LTFC: 83.9%

Interest accrual: As disbursed

Example: 5 Experience, South Dakota Investor

Purchase price: $100,000

Tier: 4 (5 projects)

Credit score: 750

Rehab budget: $20,000

ARV: $150,000

Initial advance: $90,000 (90%)

Construction holdback: $20,000

Total loan amount: $110,000

LTARV: 73.33%

LTFC: 91.67%

Interest accrual: As disbursed

Refinance Using As Is Value Instead of Cost Basis in South Dakota

Our standard underwriting approach in South Dakota involves lending within your cost basis — the total of purchase price plus sunk costs — to ensure you maintain equity ("skin in the game"). However, if you have a seasoned South Dakota property valued higher As Is than your cost basis and want to leverage that for renovations, OfferMarket carefully evaluates these requests with the following conditions:

The property must be habitable (condition rating C4 or better) and not in disrepair according to South Dakota appraisers

The property must be seasoned for at least 3 years in the South Dakota market

Payoff statements from previous lenders must be clean of default interest, extension fees, or late fees

Borrower credit score minimum of 680

Experience Tier 3 or higher with at least 4 verifiable South Dakota rehab projects

Strong market support with comparable sales validating the higher As Is value in South Dakota neighborhoods

Supportive transaction scenarios (e.g., property rented for 3+ years, tenants vacated, now ready for renovation and resale)

Transactions Involving Wholesalers in South Dakota

For wholesaler transactions in South Dakota, the entire assignment fee or double-close price run-up may be included in your cost basis for initial advance calculations, up to 20% above the original purchase price from the owner of record. Any amount beyond that is the borrower’s responsibility.

Example:

A-B Contract (owner to wholesaler): $100,000

B-C Contract (assignment fee): $25,000

As Is Value: $125,000

Value basis for initial advance: $120,000

South Dakota wholesaler transaction rules:

OfferMarket includes assignment fees or double-close run-ups up to 20% of A-B price

Financing may be denied for assignment fees if the property was listed on the MLS in South Dakota

Full chain of contracts (A-B, B-C) and wholesaler operating agreements are required

Finder’s fees and referral fees are not financed

Transactions must be arm’s length and at fair market value

Construction Holdback in South Dakota

The construction holdback funds are disbursed via draw requests for verified progress against your South Dakota rehab scope. If you have sufficient liquidity to cover rehab yourself, you may opt out of the construction holdback.

For loans above $100,000 in South Dakota, interest accrues only on funds disbursed under construction holdback (“as disbursed” interest).

| Criteria | Details |

|---|---|

| Minimum draw amount | None |

| Maximum draw amount | 100% of remaining holdback |

| Minimum number of draws | 0 |

| Maximum number of draws | None |

| Materials delivered but not installed | 50% (receipt required) |

| Draw inspection | App-based, self-serve |

| Draw turnaround | 0 to 2 business days |

| Draw fee | $270 |

| Wire fee | $30 |

Appraisal and In-House Valuation for South Dakota

All South Dakota hard money loans require a valuation via 3rd party appraisal or in-house valuation based on your project and loan parameters.

In-house valuation eligibility in South Dakota

| Criteria | Requirement |

|---|---|

| Property type | Single family, Duplex, Triplex, Quadplex |

| Experience Tier | 4 or higher |

| Credit score | 720+ |

| Rural property | No |

| New market | No |

| LTARV | Max 70% |

OfferMarket reserves the right to require an interior or exterior appraisal even if you meet in-house criteria.

Exterior appraisal South Dakota scenarios

REO sales

Foreclosure auctions

Sheriff sales

Online auctions

Bankruptcy sales

Exterior appraisals must be dated within 120 days of settlement (re-certification needed if 120-179 days).

Interior appraisal requirements

Properties not qualifying for exterior appraisal require full interior appraisal using forms specific to South Dakota residential property types:

| Property Type | Appraisal Forms |

|---|---|

| Single family | 1004 + 1007 ARV with As Is value |

| 2-4 Unit | 1025 + 216 ARV with As Is value |

| Condo | 1073 + 1007 ARV with As Is value |

OfferMarket orders appraisals through approved appraisal management companies (AMC). You will be responsible for paying appraisal invoices.

Scenario: Stabilized Hard Money Loan South Dakota

If your South Dakota property is in good condition with no deferred maintenance (appraisal rating C4 or better), OfferMarket funds up to 75% of the As Is value. This “stabilized” loan is suitable for properties ready for rent or sale.

| Criteria | Guideline |

|---|---|

| LTV (maximum) | Tier 1: 70% |

| Tier 2: 70% | |

| Tier 3: 75% | |

| Tier 4: 75% | |

| Tier 5: 75% | |

| LTFC (maximum) | Tier 1: 80% |

| Tier 2: 80% | |

| Tier 3: 90% | |

| Tier 4: 90% | |

| Tier 5: 90% | |

| Appraisal condition | C1, C2, C3 or C4 |

| Loan Term (maximum) | 12 months |

Key Loan Details for South Dakota Hard Money Loans

| Criteria | Details |

|---|---|

| Loan Amount | $25,000 to $2,000,000* |

| Units per Property | 1 to 4 units |

| Eligible Property Types | Non-owner occupied 1-4 unit residential including: single family, 2-4 unit multifamily, condos, townhomes, planned unit developments in South Dakota |

| Property Minimum Size | Single Family: 700+ sq ft; Condo and 2-4 unit: 500+ sq ft per unit; Max acreage: 5 acres |

| Loan to Cost (LTC) | Up to 90% purchase, 100% rehab |

| Loan to ARV (LTARV) | Up to 75% |

| Down Payment | Minimum $10,000 for purchase under $100K |

| Loan Term | Standard 12 months; 18-24 months available for specific South Dakota projects |

| Extensions | Up to 50% of original term (fees apply) |

| Points | 1.5 to 2 points ($2,000 minimum) |

| Prepayment Penalty | None |

| Occupancy | Non-owner occupied, business purpose only |

| Transaction Types | Arms-length purchase or refinance |

| Geographic Region | All South Dakota locations eligible for hard money loans |

| Amortization | Interest-only with balloon payment at maturity |

| Interest Accrual Method | Loans < $100K: full boat; Loans ≥ $100K: as disbursed |

Extensions for South Dakota Hard Money Loans

Hard money loans in South Dakota are designed to be short-term—typically 12 to 24 months, with most loans paid off within a year. Extensions should be avoided when possible since they incur extra fees, interest, and increase the risk of foreclosure if repayment isn’t completed by the extension limit.

To minimize the need for extensions in South Dakota projects, focus on avoiding:

Contractors with limited experience or references within the South Dakota construction market

Overly aggressive rehab scopes relative to your experience and liquidity in South Dakota

South Dakota markets with slow zoning or permitting processes

Situations where you don’t have immediate access to the property (e.g., tenant holdovers or leases requiring eviction)

Projects without a clear dual exit strategy of selling or refinancing

Extension Limits in South Dakota

| Initial Loan Term | Maximum Extension Allowed |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Extension Terms and Fees for South Dakota Loans

| Extension Term | Fee (% of total loan amount) |

|---|---|

| 3 months (1st request) | 1% |

| 3 months (2nd request) | 1.5% |

| 6 months (1st request) | 2.5% |

Extension Prerequisites

For South Dakota loans, you must confirm your builder’s risk insurance policy is active for the entire extension period to qualify.

Ineligible Property Types in South Dakota

The following property types are not eligible for funding under the South Dakota hard money loan program:

Mixed use buildings

Multifamily properties with 5+ units

Condotels and co-ops

Mobile or manufactured homes

Commercial properties such as retail, office, or industrial

Cabins or log homes common in South Dakota recreational areas

Properties with oil/gas leases or operating farms, ranches, or orchards

Vacation or seasonal rentals

Unique, exotic, or luxury properties

Properties accessed only by unpaved or dirt roads

Exception Scenarios in South Dakota

Certain exceptions are available with specific conditions for South Dakota loans:

Guarantor credit scores between 660-679

Leasehold (ground rent) arrangements

Single-family properties 500 to 699 sq ft

2-4 unit properties with one or more units between 400 to 499 sq ft

Initial advances based on As Is value exceeding cost basis

Non-arms length transactions

Borrower and Guarantor Requirements for South Dakota Loans

| Item | Requirement / Eligibility |

|---|---|

| Borrowing Entities | LLC or Corporation; nonprofits not eligible |

| Eligible Borrowers | US citizens, US permanent residents, qualified foreign nationals |

| Foreign Nationals | Valid passport, valid US visa (excludes travel/student visas unless on Visa Waiver Program) |

| Credit Requirements | Minimum 680 FICO (exceptions for 660-679) |

| Credit Report | Tri-merge report within 120 days |

| Liquidity | Minimum cash to close + 25% rehab budget held in liquid assets by guarantors |

| Eligible Liquid Assets | Personal/business bank accounts, brokerage, retirement accounts (50% haircut on retirement) |

| Guaranty Structure | Purchase: at least 51% of borrowing entity must guarantee; Cash-out refinance: 100% guarantee required |

| Recourse | Full recourse required |

| Guarantor Net Worth | Aggregate net worth at least 50% of loan amount |

Credit and Background Items for South Dakota Borrowers

If 3 credit scores reported, the middle score is used; if 2 scores, the lower is used

Six months of interest reserves required if no mortgage tradelines or fewer than 5 tradelines

Bankruptcy discharged at least 4 years prior to loan settlement date

Foreclosure completed at least 4 years prior

Between 4-7 years since bankruptcy or foreclosure: minimum 3 months interest reserves required

Late mortgage payments within 12 months require letter of explanation and possible loan committee review

Past due balances on mortgage/non-mortgage tradelines must be paid in full prior to funding

Involuntary liens or judgments must be resolved before funding

Pending civil lawsuits require LOE and loan committee approval

Pending criminal lawsuits or financial/serious/repeat crimes disqualify borrower from funding

Interest Reserves

Interest reserves are collected at settlement and held in escrow, drawn down against accrued interest before you begin monthly interest payments.

| Interest Reserve | Scenario |

|---|---|

| 0 months | At lender discretion |

| 1 month | Guarantor FICO 700+ |

| 3 months | Guarantor FICO 660-699 |

| 6 months | Guarantor FICO 660-699 and/or credit/background concerns |

Financed Interest Payments

To protect your liquidity and credit during rehab, South Dakota borrowers may finance interest payments—meaning interest accrues and is paid at loan payoff instead of monthly.

Example:

Loan amount: $100,000

Interest rate: 12%

Loan held for 9 months

Accrued interest: $9,000

Payoff statement includes unpaid principal $100,000 + unpaid interest $9,000

Property Sourcing Guidelines for South Dakota

New market transactions require a General Contractor agreement or Letter of Explanation for waiver

Properties with prior price run-ups, wholesale deals, or non-arms length transactions require additional documentation

Projects with condos, conversions, or significant renovations require architect/engineer letters or permits

Submit purchase contracts, settlement statements, payoff letters, track record, and formation documents with loan files

Insurance Guidelines for South Dakota Hard Money Loans

Protect your South Dakota investment with Builders Risk insurance—covering the dwelling, liability, and builder risk during construction or vacancy.

| Coverage Type | Limit | Required? |

|---|---|---|

| Dwelling | Replacement cost or loan amount | Yes |

| Liability | $1M per occurrence / $2M annual aggregate | Yes |

| Builders Risk | Included | Yes |

| Flood | $250,000 or loan balance if in FEMA flood zone | Yes |

Coverage Details for South Dakota

| Coverage Item | Requirement |

|---|---|

| AM Best Rating | A- VIII or higher |

| Policy Type | Special Form |

| Deductible | $1,000 to $5,000 |

| Lender’s Designation | Mortgagee and Additional Insured |

| Exclusions | No windstorm, hail, or named storm exclusion |

| Cancellation | 30-day notice |

💡 Pro tip for South Dakota investors: install smoke detectors, secure locks, and cameras as soon as you take ownership to meet insurance requirements and avoid denied claims.

Frequently Asked Questions

What states does OfferMarket fund hard money loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have more than one hard money loan at the same time?

Yes! It’s common for South Dakota and other OfferMarket clients to hold multiple hard money loans simultaneously. However, we prioritize your risk management. If your liquidity or project pace suggests risk, we will discuss how to best manage your loan portfolio safely.

Are hard money loans considered commercial loans?

Yes. Hard money loans are “business purpose” loans made to your borrowing entity (LLC or Corporation), and are thus classified as commercial loans.

What is the minimum loan amount?

The minimum loan amount for South Dakota hard money loans is $25,000.

Which property types are eligible?

We finance non-owner occupied 1-4 unit residential properties including single-family homes, townhomes, small multifamily (2-4 units), and warrantable condos across South Dakota.

Properties like 2-4 unit mixed use, 5-9 unit mixed use or multifamily, 10+ unit residential, and commercial properties are not eligible under this program but may be available through other OfferMarket loan programs.

How is Loan-to-Value (LTV) calculated?

For hard money loans, LTV usually refers to Loan-to-After-Repair-Value (LTARV). The initial advance is based on the lower of the As Is value and the purchase price or refinance price. LTARV is the total loan amount (initial advance + construction holdback) divided by the appraised after-repair value.

What credit score is required?

A minimum FICO of 680 is required, with exceptions possible for scores 660-679. We consider the credit scores of all members personally guaranteeing the loan.

Is experience required?

Experience is not mandatory but verified rehab experience in South Dakota or similar markets increases your loan leverage through our experience Tier system.

Does wholesaling count as experience?

No. Wholesaling does not count as experience since you are not financially responsible for completing rehab.

What documentation is required?

Purchase Transaction Requirements

| Loan File Section | Documents Required |

|---|---|

| Purchase Contract | Fully executed by buyer and seller |

| Credit Report | Soft tri-merge credit report for each borrowing entity guarantor |

| Background Report | Required for each borrowing entity guarantor |

| Track Record | Required for each borrowing entity guarantor |

| ID Verification | Government-issued ID (driver’s license, passport, Green Card) |

| Borrowing Entity | Articles of Organization/Incorporation, Operating Agreement/Bylaws, Certificate of Good Standing, W-9 |

| Scope of Work | Detailed rehab budget used to determine ARV |

| Appraisal Report | Link provided to pay appraisal invoice; appraisal uploaded to loan file |

| Bank Statements | Two most recent statements per guarantor (personal or business accounts) |

| Letter of Explanation | If requested by underwriting (e.g., large deposits, late payments, background items) |

Refinance Transaction Requirements

| Loan File Section | Documents Required |

|---|---|

| Settlement Statement | Fully executed by buyer and settlement agent |

| Credit Report | Soft tri-merge credit report for each borrowing entity guarantor |

| Background Report | Required for each borrowing entity guarantor |

| Track Record | Required for each borrowing entity guarantor |

| ID Verification | Government-issued ID (driver’s license, passport, Green Card) |

| Borrowing Entity | Articles of Organization/Incorporation, Operating Agreement/Bylaws, Certificate of Good Standing, W-9 |

| Sunk Costs | Line items and costs already incurred |

| Scope of Work | Detailed rehab budget used to determine ARV and guide rehab |

| Appraisal Report | Link provided to pay appraisal invoice; appraisal uploaded to loan file |

| Bank Statements | Two most recent statements per guarantor (personal or business accounts) |

| Letter of Explanation | If requested by underwriting (e.g., large deposits, late payments, background items) |

Are there Special Requirements for Loans Over $1 Million?

| Criteria | Explanation |

|---|---|

| Experience | Minimum of 3 similar or higher price point projects strongly preferred |

| Market Liquidity | Minimum of 3 comparable sales within a 2-mile radius sold on MLS in the last 6 months |

| Credit Score | Minimum 680 with at least 5 trade lines and 24-month history |

| Rural Designation | Not eligible if designated rural by CFPB, USDA, or appraisal report |

| Track Record | Required for each member of the borrowing entity |

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit on the same tax parcel |

| Arms-length | Transaction between unrelated parties at fair market value |

| Non Arms-length | Transactions involving related parties potentially affecting fairness |

| Initial Advance | Loan amount wired at closing for purchase price |

| Construction Holdback | Loan portion reserved for rehab, disbursed by draw |

| Interest Reserves | Interest funds held in escrow to cover accrued interest |

| LOE | Letter of Explanation addressing credit or background questions |

| LTC | Loan to Cost ratio: loan amount to purchase + rehab costs |

| LTFC | Loan to Full Cost ratio: loan amount to total project cost |

| LTV | Loan to Value based on As Is property value |

| LTARV | Loan to After Repair Value based on estimated post-rehab value |

| As Disbursed Interest | Interest charged only on disbursed loan funds |

| Full Boat Interest | Interest charged on the entire loan amount |

| Lopsided deal | Rehab budget exceeds purchase price or As Is value |

| GC Agreement | General Contractor contract for project management |

| DSCR | Debt Service Coverage Ratio measuring income vs debt |

Instant Hard Money Loan Quote for South Dakota

OfferMarket Capital LLC is a leading private lender specializing in 1-4 unit residential real estate hard money loans and DSCR loans, including in South Dakota. Our mission is to help you build wealth through South Dakota real estate, and we welcome the opportunity to partner with you on your next deal.

Thousands of real estate investors trust OfferMarket monthly. Membership is free and includes:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull