Hard Money Loan Michigan

OfferMarket Loans

Check your rate

60 seconds · no credit pull

Last updated: May 13, 2025

At OfferMarket, we’re committed to helping you grow your real estate investment portfolio right here in the Great Lakes State. Whether you’re flipping homes in Detroit, rehabbing duplexes in Grand Rapids, or refinancing rentals in Lansing, we provide a complete suite of services to simplify and supercharge your investment strategy:

💰 Michigan-focused private lending

☂️ Insurance rate comparison tailored to local properties

🏚️ Off-market opportunities in top Michigan cities

Our Michigan Hard Money Loan program delivers quick, reliable, and cost-effective financing for acquiring, rehabbing, or refinancing 1-4 unit residential investment properties.

Whether you’re in it for the quick flip or planning a long-term BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, our team is here to help you execute successful projects across Michigan’s dynamic housing markets.

Let’s dive into the details of OfferMarket’s Michigan Hard Money Loan Program.

What is a hard money loan?

A hard money loan is a short-term real estate investment loan secured by a tangible asset—in this case, 1-4 unit residential properties in Michigan. The primary goal is to purchase, refinance, and renovate these properties to either sell for a profit or retain them as income-generating rentals.

These loans go by many names in investor circles—“bridge loans,” “fix and flip loans,” and even “rehab loans.” Whatever term you prefer, they all serve the same purpose: fast, flexible funding for time-sensitive deals.

Hard money loan scenarios

Investors throughout Michigan—from Wayne County to Kent County—leverage hard money loans for a wide variety of strategic use cases:

Acquisition and rehab of distressed properties – Ideal when you need financing to both purchase and renovate a fixer-upper in neighborhoods like Flint or Saginaw without overextending your own funds.

Cash-out refinance after an all-cash purchase – Useful if you secured an off-market property in Ann Arbor with cash for speed, and now want to recover funds to begin renovations.

Refinance of an active rehab project – You’ve already started work in cities like Kalamazoo, but need new financing to finish the job.

Purchasing undervalued properties without renovation plans – Great for turning quick profits on properties acquired well below market value in places like Battle Creek or Bay City.

Refinancing cash purchases with no rehab intention – Extract equity from a solid deal you made in Jackson or Port Huron to fund your next move.

Refinancing an existing loan post-rehab – You’ve completed the work and want more breathing room to sell or refinance into long-term financing.

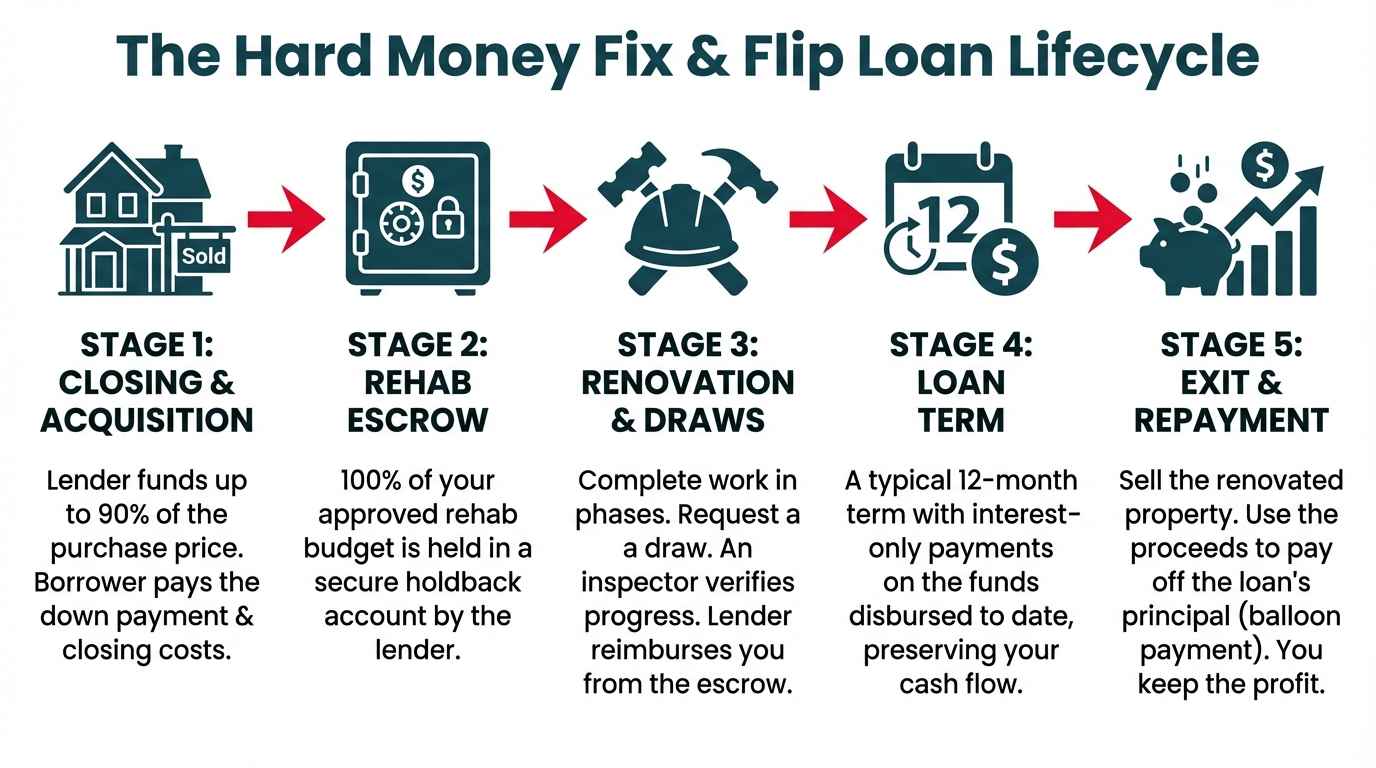

How it works

A Michigan hard money loan from OfferMarket consists of two main components:

Initial Advance – This portion is allocated toward the property purchase. It’s wired directly to the title company at closing.

Construction Holdback – This portion covers your rehab costs and is disbursed as you make progress on your renovation plan.

You’re in control. You can take just the purchase advance, just the rehab funds, or both—depending on your strategy and liquidity.

Most of our Michigan clients use both components to reduce the amount of personal capital tied up in projects. Some prefer to fund rehab work themselves to retain full control. Others pay cash for the property and only borrow against the renovation budget. We’re flexible so you can execute confidently.

The typical outcomes for your Michigan hard money project:

Fix and Flip: Sell the rehabbed property for a profit in growing cities like Ypsilanti or Royal Oak.

BRRRR Method: Hold onto the asset, refinance into a DSCR loan, and generate rental income from areas like East Lansing or Traverse City.

It’s perfectly acceptable to adjust your exit strategy along the way. For instance:

You may plan to BRRRR, but strong resale comps in your area nudge you toward selling for a quicker profit.

Alternatively, market shifts may push your flip into a rental hold while you wait for better conditions.

That’s why selecting properties with multiple viable outcomes is key to reducing risk in Michigan’s evolving real estate climate.

Who uses hard money loans in Michigan?

Hard money loans are a go-to strategy for two main types of investors in Michigan:

- Fix and Flip Investors (a.k.a. House Flippers)

These are entrepreneurs who buy properties in neighborhoods like Southfield or Pontiac, renovate them quickly, and sell for a profit. Speed, flexibility, and funding power make hard money loans ideal for these fast-paced projects. - Buy and Hold Investors (BRRRR Method)

Investors focused on long-term wealth use our Michigan hard money loans to purchase and rehab rental properties, then refinance into DSCR loans to build a stable portfolio. Whether you're targeting college towns like Ann Arbor or suburban areas around Grand Rapids, the BRRRR strategy is a proven path to passive income.

* Learn more about our Fix and Rent bundle, which combines a hard money loan for acquisition and rehab with a discounted DSCR loan for refinancing.

As noted above, many Michigan investors follow a hybrid approach—flipping some properties while renting others—depending on the property type, neighborhood dynamics, and broader economic conditions. We encourage this kind of flexibility as a best practice across our client base.

Michigan Hard Money Loan Program Guidelines

| Criteria | Guideline |

|---|---|

| Loan amount (minimum) | $25,000 |

| Loan amount (maximum) | $2,000,000 |

| ARV (minimum) | $100,000 |

| Experience | Not required |

| Credit score (minimum) | 680 |

| Borrowing entity | LLC or Corporation |

| Initial advance | up to 90% |

| Construction holdback | up to 100% |

| LTARV (maximum) | 75% |

| Interest rate | get instant quote |

| Origination fee | 1.5 to 2 points |

| Term | 12 to 24 months |

| Points out | None |

| Prepayment penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full (51% of borrowing entity must guarantee) |

| Exit strategy: Sale | minimum 30% ROI |

| Exit strategy: Refinance | minimum 1.1 DSCR after repairs |

| Valuation | Appraisal report or In-house valuation |

| SqFt (minimum) | Single family: 700+ 2-4 unit: 500+ per unit Condo: 500+ |

| Acreage (maximum) | 5 |

| Interest accrual | Under $100,000 loan: full boat $100,000+ loan: as disbursed |

| Advanced draws | Lender discretion |

| Down payment (minimum) | $10,000 |

Whether you’re funding a flip in West Michigan or improving a fourplex in Flint, these guidelines ensure transparency and help you plan your project financing with confidence.

Project Eligibility

At OfferMarket, our priority is to be your trusted partner in Michigan real estate investment—and that means prioritizing your financial safety above all else. That’s why every hard money loan we originate is vetted with disciplined underwriting criteria. Our overall loan default rate is below 0.5%, one of the lowest in the private lending industry, and we take pride in keeping our Michigan borrowers secure and successful.

In markets such as Detroit’s historic neighborhoods or the up-and-coming suburbs of Oakland County, it’s essential to avoid projects that exceed your skill level or financial cushion. Projects with major structural or system-wide rehabs—referred to as "heavy" or "extensive" rehabs—tend to carry higher risks. These projects often face longer timelines, unexpected costs, and complications like zoning red tape or permitting delays, especially in urban cores like Flint or older neighborhoods in Lansing.

We see time and time again that less experienced investors, especially those taking on complex rehabs in uncertain economic conditions, can fall into financial difficulty without proper guidance. That’s where we step in—not just as a lender, but as your strategic partner. From the start, we work to align expectations and help you understand what your deal needs to succeed in the Michigan market.

Let’s now break down how we assess project eligibility, starting with the Initial Advance and how it’s calculated.

Initial Advance

Your initial advance is tailored to both the specifics of your deal and your personal investing track record. Whether you’ve flipped ten homes in Macomb County or you’re just getting started with your first investment in Benton Harbor, we examine two major factors:

The number of investment properties you've owned in the last 24 months.

The number of successfully completed, verifiable rehab projects in the past five years.

We require a minimum credit score of 680, but for maximum leverage, we strongly prefer a credit score of 720+ from the personal guarantor of your Michigan-based borrowing entity. Increased leverage is also offered to licensed Realtors, General Contractors, and Professional Engineers—credentials that demonstrate hands-on expertise and enhance deal execution reliability.

If your contract purchase price is higher than the As Is value determined by our appraisal or internal valuation, the loan advance will be calculated based on the lower of the two, to protect both parties from over-leveraging.

Your exit strategy in Michigan matters too:

If your plan is to sell the property, we require a minimum projected gross margin of 30% and at least $15,000 in projected profit.

If your plan is to refinance and rent, or if your flip profit margin doesn’t meet requirements, the project must show a minimum post-repair DSCR of 1.1.

Rural properties—such as homes on the outskirts of Northern Michigan—may receive a lower advance and require an experience level of at least Tier 3 due to higher logistical and appraisal challenges.

Experience-based Tiers

To help us responsibly assess borrower readiness, we use an experience-tier framework. This ensures that our Michigan investors are matched with appropriate leverage levels based on verifiable experience:

| Tier | Verifiable experience |

|---|---|

| 1 | 0 |

| 2 | 1 to 2 |

| 3 | 3 to 4 |

| 4 | 5 to 9 |

| 5 | 10+ |

If you’ve completed just one or two flips in areas like Warren or Dearborn, you’d likely fall into Tier 2. Seasoned investors with dozens of successful projects across Wayne, Kent, or Ingham counties would qualify for Tier 5.

Initial Advance by Tier

Based on your experience tier, your allowable initial advance on the property purchase price is as follows:

| Tier | Initial advance (% of purchase price) |

|---|---|

| 1 | 80%* |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

* Borrowers in Tier 1 may be eligible for up to 85% on an exception basis if they demonstrate strong credit (720+) and robust liquidity.

Adjustments to Initial Advance

Several deal or borrower-specific variables may modify your initial advance. This is especially relevant in complex rehab projects in cities like Ypsilanti or emerging markets such as Muskegon:

| Scenario | Adjustments |

|---|---|

| Credit score less than 720 | -5% |

| Full gut rehab | -5% |

| New market | -5% |

| Licensed Realtor | up to +5% |

| Licensed General Contractor | up to +10% |

| Licensed Professional Engineer | up to +10% |

| Rural | -20% (Tier 3+) |

These adjustments help tailor the loan offer to your actual risk profile.

Rehab Scope Classification

We classify rehab projects based on the size of the renovation budget relative to the property’s purchase price. These classifications are particularly useful when comparing cosmetic rehabs in Grand Rapids to full-gut projects in Detroit:

| Rehab Scope | Definition |

|---|---|

| Light | Budget < 25% of purchase price |

| Moderate | Budget 25% to 49.99% of purchase price |

| Heavy | Budget 50% to 99.99% of purchase price |

| Extensive | Budget ≥ 100% of purchase price — includes additions, ADUs, or “lopsided” deals where rehab exceeds the As Is value |

Rehab Scope Eligibility

Based on your experience tier, here's what rehab scopes you're eligible to pursue with OfferMarket in Michigan:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | Eligible | Ineligible | Ineligible | Ineligible |

| 2 | 1–2 | Eligible | Eligible | Eligible | Ineligible |

| 3 | 3–4 | Eligible | Eligible | Eligible | Eligible |

| 4 | 5–9 | Eligible | Eligible | Eligible | Eligible |

| 5 | 10+ | Eligible | Eligible | Eligible | Eligible |

Less experienced Michigan investors are encouraged to focus on lighter cosmetic rehabs—often found in stable suburban neighborhoods like Livonia or Sterling Heights.

LTARV Limits

The loan-to-after-repair value (LTARV or ARLTV) determines how much financing you can receive relative to the projected post-rehab value of the property. Here are the limits by tier and rehab scope:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | 70% | Ineligible | Ineligible | Ineligible |

| 2 | 1–2 | 70% | 70% | 70% | Ineligible |

| 3 | 3–4 | 75% | 75% | 75% | 70% |

| 4 | 5–9 | 75% | 75% | 75% | 70% |

| 5 | 10+ | 75% | 75% | 75% | 70% |

These limits help you balance leverage with risk and ensure safe capital structures in every Michigan transaction.

LTFC Limits

LTFC—Loan to Full Cost—is specifically applied to “extensive” rehabs, where the project budget exceeds the property’s value or purchase price:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | N/A | Ineligible | Ineligible | Ineligible |

| 2 | 1–2 | N/A | N/A | N/A | Ineligible |

| 3 | 3–4 | N/A | N/A | N/A | 85% |

| 4 | 5–9 | N/A | N/A | N/A | 90% |

| 5 | 10+ | N/A | N/A | N/A | 90% |

This ensures that even in high-stakes, large-scale rehabs, the borrower maintains meaningful equity and financial commitment.

Example: No Experience

Let’s say you’re a first-time investor in Lansing, eyeing a budget-friendly distressed property.

Purchase price: $100,000

Experience Tier: 1 (no prior verifiable rehab projects)

Credit score: 695

Rehab budget: $24,000

ARV (After Repair Value): $150,000

Your initial advance would be 75% of the purchase price, equating to $75,000. You’d also receive a construction holdback of $24,000 to fund the rehab. Total loan: $99,000

LTARV: 66%

LTFC: 79.8%

Interest accrual: Full loan amount (aka “full boat” interest)

This is a common setup for beginners in markets like Kalamazoo or Jackson, where entry prices are accessible but profits can be substantial with the right execution.

Example: No Experience, Excellent Credit

Now picture a similar property in Saginaw, but you’ve got excellent credit:

Purchase price: $100,000

Experience Tier: 1

Credit score: 750

Rehab budget: $24,000

ARV: $150,000

With a strong credit score, you’re eligible for an 80% initial advance:

Initial advance: $80,000

Construction holdback: $24,000

Total loan: $104,000

LTARV: 69.33%

LTFC: 83.9%

Interest accrual: As disbursed (not on undrawn funds)

This approach benefits creditworthy borrowers who want to preserve cash flow early in their investment journey.

Example: 5 Experience

If you’ve already successfully completed at least five comparable rehab projects—perhaps across metro Detroit or in smaller towns like Adrian—you fall into Tier 4.

Purchase price: $100,000

Experience Tier: 4

Credit score: 750

Rehab budget: $20,000

ARV: $150,000

You’d receive the max 90% initial advance:

Initial advance: $90,000

Construction holdback: $20,000

Total loan: $110,000

LTARV: 73.33%

LTFC: 91.67%

Interest accrual: As disbursed

This tier gives seasoned Michigan investors the capital efficiency to tackle larger volume or multiple deals concurrently.

Refinance using As Is value instead of Cost Basis for Initial Advance

If you're holding a seasoned property—say a Duplex in Battle Creek that you've rented for years—and want to leverage its current value rather than the original cost, our refinance model supports that under strict criteria:

Property must be in habitable condition (C4 or better in appraisal terms)

Must have been owned (seasoned) for 3+ years

No delinquent interest or fees on current payoff

Guarantor credit score must be 680+

Minimum Experience Tier: 3

Clear market comparables must support your higher As Is value

Narrative must justify renovation need post-tenancy (e.g., long-time tenant vacated)

This model is often used by landlords in Flint or Wyandotte converting long-term rentals into value-add projects.

Transactions involving wholesalers, price run-ups

Wholesaling is active in Michigan markets like Inkster, River Rouge, and Bay City, where spread opportunities abound. If you're purchasing from a wholesaler, we allow part of their fee to be financed—up to 20% over the A-B contract price.

For example:

A-B contract: $100,000 (seller to wholesaler)

B-C assignment fee: $25,000

As Is value: $125,000

Max value basis for loan: $120,000 (20% above A-B price)

Conditions:

Assignment or double-close fees cannot exceed 20% of the A-B price

The property cannot be listed on the MLS

Documentation: A-B contract, B-C assignment, wholesaler’s operating agreement

No funding for finder’s fees or non-arm’s length markups

Appraisal must support total value (retail or wholesale)

We aim to support your strategy while guarding against inflated risk from excessive markups.

Construction Holdback

In Michigan, managing your draw schedule is key—especially with cold winters that can delay exterior work in cities like Traverse City or Alpena. Here’s how our draw process works:

| Draw Processing Guideline | Details |

|---|---|

| Minimum draw amount | None |

| Maximum draw amount | 100% of remaining construction holdback |

| Minimum number of draws | 0 |

| Maximum number of draws | Unlimited |

| Materials delivered but not installed | Eligible for up to 50% (invoice required) |

| Draw inspection | App-based (self-serve) |

| Draw turnaround | 0 to 2 business days |

| Draw fee | $270 |

| Wire fee | $30 |

This self-serve draw model is ideal for GC-led projects in counties like Washtenaw or Ottawa, where crews are ready and mobilized.

Appraisal and In-house valuation

We require a valuation for every Michigan hard money loan—either a third-party appraisal or an internal valuation, depending on your profile and deal location.

In-house valuation eligibility:

| Criteria | Requirement |

|---|---|

| Property type | SFR, duplex, triplex, quadplex |

| Tier | 4 or higher |

| Credit score | 720+ |

| Rural | Not allowed |

| New market | Not allowed |

| LTARV | 70% max |

If you're flipping a quadplex in Ypsilanti and meet these standards, you may be eligible for faster underwriting with an internal valuation.

Exterior appraisal

You may use a drive-by appraisal if:

The deal is a REO, auction, or bankruptcy sale

Appraisal is dated within 120 days of closing

If 120–179 days, we’ll need recertification

This is especially helpful for quick-turn acquisitions from sheriff’s auctions in places like Wayne County or Genesee County.

Interior appraisal

For most standard purchases in areas like Ann Arbor or Holland, we’ll require a full interior appraisal. Appraisal form requirements are as follows:

| Property Type | Required Forms |

|---|---|

| Single Family | 1004 + 1007 ARV (includes As Is value) |

| 2–4 Unit | 1025 + 216 ARV (includes As Is value) |

| Condo | 1073 + 1007 ARV (includes As Is value) |

We order all appraisals via licensed AMCs. Once you pay the appraisal invoice, we’ll coordinate everything directly with the appraiser to streamline the process.

Appraisal transfer

Already commissioned an appraisal for your Michigan property? You may be eligible to transfer it, provided:

Ordered through a compliant AMC

Report is <180 days old

If 120–179 days old, it must be re-certified

Transferring lender provides:

Signed AIR-compliant transfer letter

PDF and XML copies of appraisal

Proof of payment (invoice)

This is a popular option for investors doing multiple deals in the Metro Detroit area who want to avoid duplicate appraisal costs.

Scenario: Stabilized Hard Money Loan

Let’s say you’ve just acquired a solid single-family rental in Sterling Heights, and the property is in good condition—no deferred maintenance, no urgent repairs. With a C4 or better condition rating, this home qualifies for our Stabilized Hard Money Loan approach.

Instead of focusing on rehab, we underwrite the loan based on the As Is value and fund up to 75% of that figure. This scenario works beautifully for landlords and investors in places like Novi or Farmington Hills where the goal is to refinance, list for sale, or tap equity while keeping costs low.

| Guideline | Details |

|---|---|

| LTV (max) | Tier 1–2: 70% Tier 3–5: 75% |

| LTFC (max) | Tier 1–2: 80% Tier 3–5: 90% |

| Appraisal condition | C1, C2, C3, or C4 |

| Loan term | Up to 12 months |

This is a great fit if your Michigan rental property is nearly turnkey and you need short-term leverage without dealing with construction holdbacks.

Key Loan Details

We offer transparent, investor-friendly hard money loans across Michigan—backed by terms designed to help you scale sustainably.

| Criteria | Details |

|---|---|

| Loan Amount | $25,000 to $2,000,000* |

| Units Per Property | 1–4 |

| Eligible Property Types | Non-owner occupied residential Single family, 2–4 unit multifamily, condos, townhomes |

| Property Size | SFR: ≥700 SQFT 2–4 units: ≥500 SQFT per unit Condos: ≥500 SQFT |

| Max Acreage | 5 acres |

| Loan to Cost (LTC) | Up to 90% purchase, 100% rehab |

| LTARV | Up to 75% |

| Down Payment | Min. $10,000 (for purchases < $100K) |

| Loan Term | 12–24 months standard Extensions available (see below) |

| Points | 1.5 to 2 (minimum $2,000) |

| Prepayment Penalty | None |

| Occupancy | Non-owner occupied only |

| Transaction Types | Purchase, refinance |

| Coverage Area | All MI cities & counties—excluding states where lending isn’t authorized |

| Amortization | Interest-only with balloon payment |

| Interest Accrual | Under $100K: Full boat $100K+: As disbursed |

Our loans are structured to give you full control over exit strategy and timelines—no lock-ins, no hidden fees.

Extensions

Hard money loans are designed to be short-term financial bridges, not long-term crutches. In Michigan, we see most loans paid off well before the 12-month mark. However, if your flip in Dearborn hits a snag, or your refinance in Portage needs more time, we allow reasonable extensions.

That said, extensions aren’t ideal—they trigger fees, additional interest, and increase foreclosure risk if deadlines are missed. Avoiding extensions should always be the goal.

To do that, steer clear of:

GCs with weak references

Overly ambitious rehabs

Permit-heavy municipalities (e.g., Detroit historical zones)

Projects where you can’t access the property immediately (e.g., inherited tenants)

Exit strategies with only one viable outcome

Success comes from planning your project in a way that builds in buffer time and optionality.

Extension Limits

We cap extensions at 50% of your original term. You can request them in 3- or 6-month increments.

| Initial Term | Max Extension |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Each extension request triggers a fresh review of your insurance, timeline, and exit readiness.

Extension Terms and Fees

Fees are applied to your payoff statement based on the length and number of extensions:

| Extension Term | Fee |

|---|---|

| 3 months (1st request) | 1% of total loan amount |

| 3 months (2nd request) | 1.5% |

| 6 months (1st request) | 2.5% |

To proceed with an extension, your builder’s risk insurance policy must be active throughout the extension period. We’ll verify this before approving the request.

Ineligible Property Types

The following property types are not eligible for funding under our Michigan hard money program:

Mixed-use buildings

5+ unit multifamily

Condotels or co-ops

Mobile/manufactured homes

Commercial properties (e.g., office, retail)

Cabins, log homes

Properties with gas/oil leases

Working farms or orchards

Short-term or seasonal vacation rentals

Unique or ultra-luxury homes

Landlocked or dirt road parcels

We focus on conventional investment properties where resale or rental is backed by strong local demand—especially in stable Michigan metros.

Exception Scenarios

In certain cases, we may approve exceptions for deals that fall slightly outside standard guidelines. For example:

Credit score: 660–679

Leasehold land (with ground rent)

SFR between 500–699 SQFT

2–4 unit with any unit between 400–499 SQFT

Initial advance based on higher As Is value than cost basis

Non-arm’s length purchases

Financed interest payments (rolled into loan)

Each exception is evaluated case-by-case with a close look at liquidity, deal quality, and exit strategy strength. Exception-friendly areas include well-comped, lower-cost cities like Ecorse or Inkster, where creative deals are common.

Borrower and Guarantor Requirements

To be eligible for a Michigan hard money loan, you must meet the following qualifications:

| Item | Requirement |

|---|---|

| Borrowing Entities | LLC or Corporation (no nonprofits) |

| Eligible Borrowers | US Citizens, Permanent Residents, and approved Foreign Nationals |

| Foreign Nationals | Must have valid Passport + Visa (non-student/travel), and US FICO score if guaranteeing |

| Credit Score | Minimum 680 (660–679 exceptions possible) |

| Credit Report | Tri-Merge report, no older than 120 days |

| Liquidity | Enough to cover estimated cash to close + 25% of rehab budget |

| Eligible Liquid Assets | Checking/savings, brokerage, retirement (50% haircut), business accounts |

| Guaranty | Purchases: 51%+ of entity must guarantee Cash-out refis: 100% must guarantee |

| Recourse | Full personal guaranty required |

| Net Worth | Aggregate guarantor net worth must equal ≥50% of loan amount |

We evaluate the financial backing behind each project to ensure it’s safely structured from day one.

Liquidity Verification

Ensuring liquidity is crucial—especially in Michigan where rehab timelines can vary due to weather, labor availability, and local permitting. We require that all guarantors demonstrate a minimum amount of accessible cash or liquid assets to cover both the estimated cash to close and 25% of the projected rehab budget.

This requirement is designed to make sure you’re never strapped for funds mid-project—whether you’re restoring a craftsman bungalow in Ferndale or converting a duplex in Eastpointe into modern rentals.

Eligible Liquid Assets

Personal bank accounts – Checking or savings accounts in your name

Entity bank accounts – From your borrowing LLC or Corporation

Business bank accounts – From related entities (must provide operating agreement)

Brokerage accounts – Stocks, bonds, etc. in personal or entity name

Retirement accounts – 401(k), IRA, etc. (50% value applied due to withdrawal restrictions)

Verification Process

You’ll submit the two most recent monthly statements for each account

No seasoning period required (new accounts are acceptable)

Large deposits must be explained with a simple Letter of Explanation (LOE)

Funds do not need to be transferred or pooled—we only need to verify their availability

This verification step helps us—and you—ensure your Michigan real estate project can weather unexpected costs, delays, or shifts in scope without jeopardizing your credit or capital stack.

Credit and Background Items

We perform thorough credit and background reviews for all Michigan borrowers. Here's how we handle key flags:

Tri-merge scores: If 3 scores, we use the middle one. If 2, we use the lower.

No mortgage tradelines: Requires 6 months of interest reserves

<5 tradelines: Also requires 6 months of interest reserves

Bankruptcy/foreclosure: Must be ≥4 years old; if 4–7 years, 3 months reserves required

Late mortgage payments (past 12 months): LOE required, may be ineligible

Delinquent balances (mortgage or non-mortgage): Must be paid prior to funding

Liens/judgments: Must be cleared

Pending lawsuits (civil): LOE required

Pending criminal or financial crimes: Not eligible

Serious or repeat offenses: Reviewed individually

We value transparency and work with you to proactively resolve red flags.

Interest Reserves

In some cases, we collect interest reserves upfront at closing. This means a portion of your loan’s interest obligation is pre-funded and held in escrow, then used to cover future monthly interest payments.

This is especially useful for investors in markets like Midland or Ypsilanti, where cash flow planning is essential during slower seasons or phased renovations.

| Interest Reserve | Scenario |

|---|---|

| 0 month | Discretionary (standard loans) |

| 1 month | Guarantor FICO score 700+ |

| 3 months | FICO score 660–699 |

| 6 months | FICO score 660–699 and/or flagged credit/background items |

By front-loading interest payments, we protect your liquidity during the early stages of your Michigan project when capital tends to be most constrained.

Financed Interest Payments

If you’re tackling a heavy rehab in Pontiac or managing multiple flips across Wayne and Macomb counties, you might benefit from financed interest payments. This structure rolls your interest into the payoff, so you don’t have to make monthly payments during the loan term.

Example:

Loan amount: $100,000

Interest rate: 12%

Loan term: 9 months

Accrued interest: $9,000

Payoff Statement:

Unpaid principal: $100,000

Interest due: $9,000

Total payoff: $109,000

This structure is popular with high-volume Michigan investors who prioritize liquidity and project acceleration.

Property Sourcing Guidelines

Whether you’re sourcing deals in Washtenaw County, Kent County, or quiet corners of Shiawassee, the following documentation is required to process your loan:

Purchase transactions:

Purchase contract (signed by buyer/seller)

Credit/background reports

ID verification (driver's license, passport)

Entity docs (Articles, Operating Agreement, Good Standing cert, W-9)

Rehab scope and itemized budget

Appraisal or valuation

2 months of bank/brokerage/retirement statements

Letter of explanation (as needed)

Refinance transactions:

Settlement statement from original closing

All items listed above, plus sunk cost breakdown (already incurred costs)

In some cases, we may also request GC agreements, track record files, or additional comps if your market is less liquid (i.e., smaller towns like Owosso or Coldwater).

Insurance Guidelines for Hard Money Loans

Insuring your Michigan project is non-negotiable. Whether you’re flipping a lakefront home in Holland or gutting a duplex in Detroit, you’ll need a specialized Builders Risk policy that covers renovation-related risks.

We require a policy that includes:

| Coverage Type | Minimum Limit | Required? |

|---|---|---|

| Dwelling | Full replacement or total loan amount | Yes |

| Liability | $1M per occurrence / $2M aggregate | Yes |

| Builders Risk | Included | Yes |

| Flood | Greater of $250K or loan balance (if FEMA flood zone) | Conditional |

Insurance Details

| Requirement | Detail |

|---|---|

| Carrier rating | A- VIII or better (AM Best) |

| Policy type | Special Form |

| Deductible | $1,000–$5,000 |

| Lender clauses | Must list OfferMarket as mortgagee & additional insured |

| Exclusions | No named storm, hail, or windstorm exclusions |

| Cancellation notice | 30 days minimum |

| Loan File Sections | Documents Required |

|---|---|

| Purchase | Fully executed purchase contract |

| Credit Report | Soft tri-merge pull per guarantor |

| Background Report | One per guarantor |

| Track Record | Verifiable past project history |

| ID Verification | Driver’s license, passport, or green card |

| Borrowing Entity | Articles of Organization, Operating Agreement, Certificate of Good Standing, W-9 |

| Scope of Work | Line-item rehab budget |

| Appraisal Report | Ordered via AMC, uploaded to file |

| Bank Statements | 2 most recent per guarantor; personal or business |

| Letter of Explanation | Required if background/credit flags appear (i.e. large deposits, past-due debts) |

💡 Pro Tip for Michigan: Immediately upon taking ownership, install locks, smoke detectors, and basic security cameras. These actions may be required for coverage and help prevent claim disputes.

Frequently Asked Questions

What states does OfferMarket fund hard money loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have more than one hard money loan at a time?

Absolutely. Many of our Michigan-based clients carry multiple hard money loans simultaneously—particularly full-time real estate investors or developers working on staggered project timelines.

That said, we take capital risk seriously. If we determine that your liquidity, cash flow, or construction capacity won’t support the additional project responsibly, we’ll collaborate with you to adjust scope or timeline to avoid overextension.

Our goal is not to limit your growth—but to make sure that growth is sustainable, especially in high-velocity markets like Detroit, Grand Rapids, or Ann Arbor where multiple deals are common.

Are hard money loans considered commercial?

Yes. Hard money loans are business purpose loans, not personal financing. They’re originated to your business entity—usually a Michigan-registered LLC or Corporation—and are treated as commercial loans from a legal and underwriting perspective.

This distinction has important implications:

These loans are not subject to owner-occupancy regulations or consumer lending protections

You must have a properly structured borrowing entity

Proceeds must be used for legitimate investment activity—not personal or primary residence use

What is the minimum loan amount?

Our minimum loan size is $25,000, which makes us a great match for investors working in affordable Michigan markets like Flint, Saginaw, or Inkster. Even with smaller deals, you can still access professional-grade funding and investor support.

Which property types are eligible?

We finance non-owner occupied residential properties that meet the following criteria:

1–4 unit properties

Single-family residences

Duplexes, triplexes, and quadplexes

Warrantable condominiums

Townhomes and Planned Unit Developments (PUDs)

We do not fund properties that are:

5+ unit multifamily

Mixed-use with commercial space

Commercial buildings (office, retail, etc.)

This ensures we remain focused on traditional residential real estate projects that dominate Michigan’s investment landscape.

How do you calculate LTV and LTARV?

In Michigan, as elsewhere, LTV (Loan-To-Value) and LTARV (Loan-To-After-Repair-Value) determine your leverage ratio.

LTV is based on the lower of the purchase price or current As Is value

LTARV is based on the appraised or estimated After Repair Value

If you’re purchasing a rental in Wyoming, MI for $110,000 with an ARV of $160,000 and requesting $120,000 in total funding, your LTARV would be 75%.

We provide both initial advance and construction holdback components, giving you optimal flexibility based on these ratios.

What are the credit requirements?

We require a minimum credit score of 680 to qualify, though scores between 660–679 may be approved on an exception basis depending on liquidity, experience, and deal quality.

We look only at the scores of those members in the borrowing entity who will personally guarantee the loan

We do not consider the credit of non-guarantor members

In Michigan, where entry prices are relatively low, strong credit can also unlock higher leverage on lower-cost deals—perfect for first-time investors or repeat flippers building momentum.

What are the experience requirements?

Experience is not required to qualify for a Michigan hard money loan. That said, borrowers with prior experience may qualify for better leverage and more complex rehab scopes.

Our experience tiers are based on verifiable rehab projects

We’ll request documentation during the Track Record portion of your Loan File

Examples include settlement statements, operating agreements, and LLC ownership docs

Each tier increases your eligibility for higher advance percentages, heavier rehab scopes, and more favorable terms.

Does being a wholesaler count toward experience?

No. While wholesaling is a valid business model—and we do support wholesale transactions—wholesale deals do not count toward experience for tier purposes.

This is because as a wholesaler, you weren’t financially responsible for the renovation, risk management, or completion of the project.

However, if you’re transitioning from wholesaling to rehabbing in Michigan, we’re happy to help you bridge that gap and grow into the next phase of your investing career.

What documentation is required?

We’ve streamlined our Loan File system to make it easy for Michigan investors to complete their documentation and move quickly through underwriting.

Purchase Transactions

| Loan File Sections | Documents Required |

|---|---|

| Purchase | Fully executed purchase contract |

| Credit Report | Soft tri-merge pull per guarantor |

| Background Report | One per guarantor |

| Track Record | Verifiable past project history |

| ID Verification | Driver’s license, passport, or green card |

| Borrowing Entity | Articles of Organization, Operating Agreement, Certificate of Good Standing, W-9 |

| Scope of Work | Line-item rehab budget |

| Appraisal Report | Ordered via AMC, uploaded to file |

| Bank Statements | 2 most recent per guarantor; personal or business |

| Letter of Explanation | Required if background/credit flags appear (i.e. large deposits, past-due debts) |

Refinance Transactions

| Loan File Sections | Documents Required |

|---|---|

| Settlement Statement | From original acquisition |

| Credit Report | Soft tri-merge pull per guarantor |

| Background Report | One per guarantor |

| Track Record | Verifiable past project history |

| ID Verification | Driver’s license, passport, or green card |

| Borrowing Entity | Articles of Organization, Operating Agreement, Certificate of Good Standing, W-9 |

| Sunk Costs | Line-item breakdown of already incurred costs |

| Scope of Work | Post-refi rehab plan and ARV projection |

| Appraisal Report | Ordered via AMC or transferred (if eligible) |

| Bank Statements | 2 most recent per guarantor |

| Letter of Explanation | Only required if specific risks are flagged |

Our underwriting process is designed to be thorough, yet efficient—so you can spend less time chasing paperwork and more time securing your next investment property in Michigan.

Are there special requirements for loans over $1M?

Yes—if your project in Michigan requires over $1,000,000 in funding (up to our $2 million max), it will be reviewed with enhanced underwriting criteria. These high-value loans often involve properties in affluent suburbs like Bloomfield Hills, Birmingham, or Northville, where higher price points require greater diligence.

| Criteria | Explanation |

|---|---|

| Experience | Must have completed at least 3 similar projects; prior success at similar or higher price points strongly preferred |

| Market Liquidity | Minimum 3 comparable sales within 2 miles, closed in the past 6 months |

| Credit Score | Minimum 680 with at least 5 trade lines aged 24 months or more |

| Rural Designation | Not allowed if designated “rural” by CFPB, USDA, or appraisal report |

| Track Record | Complete track record required for each member of the borrowing entity |

These extra requirements help ensure that large-scale projects are appropriately resourced and structured for success.

Glossary of Key Terms

Here’s a breakdown of commonly used terms in our hard money lending program—essential for new and seasoned Michigan investors alike.

Michigan Instant Hard Money Loan Quote

OfferMarket Capital LLC is your trusted hard money lender for 1–4 unit investment properties across Michigan—from Detroit’s rebounding neighborhoods to rental-rich college towns like East Lansing and upscale communities in Oakland County.

Our goal is simple: empower you to build long-term wealth through real estate. With thousands of active investors using OfferMarket every month, we’re proud to be part of your investing journey.

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull