Hard Money Loan Oklahoma

OfferMarket Loans

Check your rate

60 seconds · no credit pull

Last updated: May 19, 2025

At OfferMarket, our purpose is to empower Oklahomans to build lasting wealth through real estate investments. To assist you on your investing journey, we provide a comprehensive, state-specific platform:

💰 Private lending in Oklahoma ☂️ Insurance rate comparison tailored for Oklahomans 🏚️ Exclusive off-market Oklahoma properties

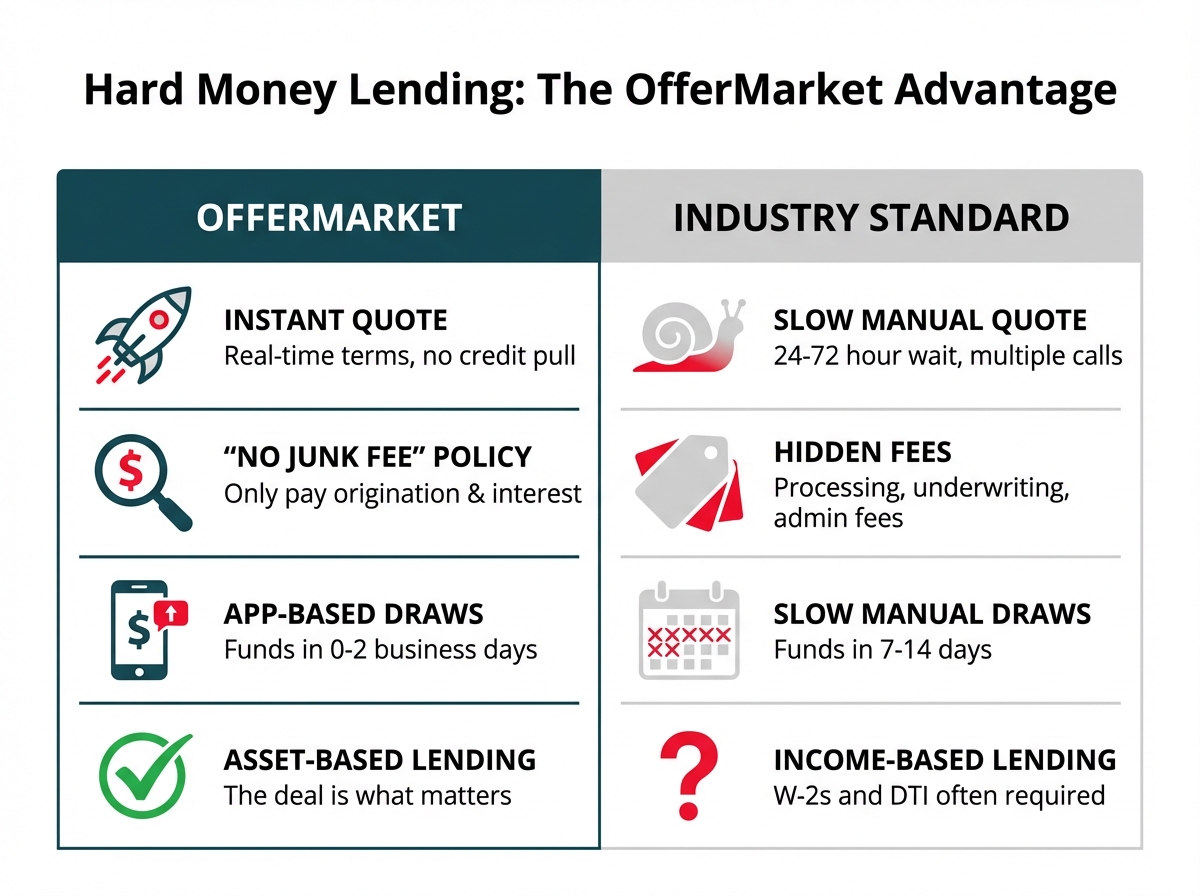

Our Hard Money Loan Oklahoma program offers rapid, reliable, and affordable funding designed specifically to acquire, refinance, and enhance 1-4 unit residential investment properties throughout Oklahoma.

Whether your aim is to renovate and flip homes in Oklahoma City's growing neighborhoods or invest in rental properties near Tulsa or Norman, we’re eager to earn your business and actively contribute to your investment success.

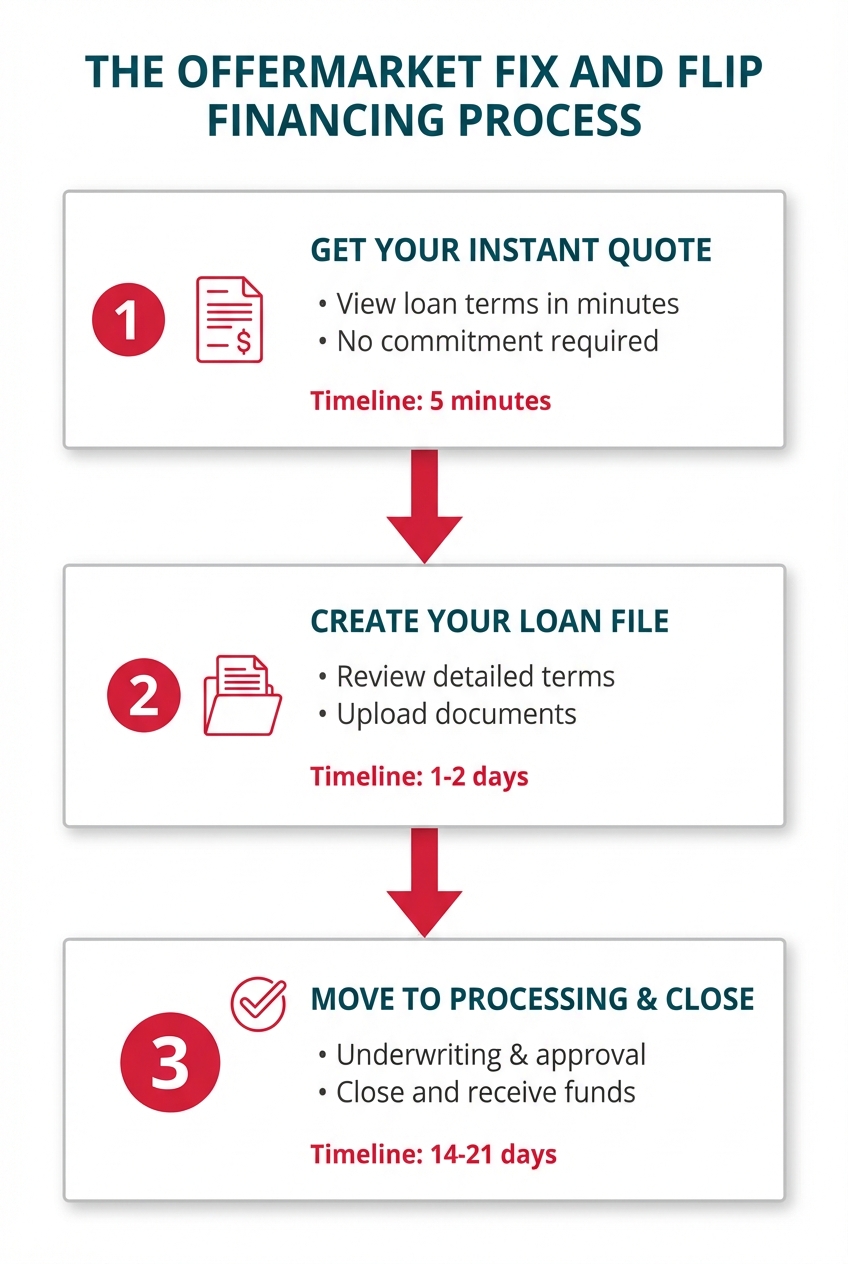

Let's dive into the details of OfferMarket’s Hard Money Loan Oklahoma Program!

What is a Hard Money Loan?

A hard money loan in Oklahoma is a short-term, asset-backed financing solution, specifically designed for 1-4 unit residential real estate. These loans help investors quickly purchase, refinance, and rehab properties for profit or to hold in their rental portfolios.

Hard money loans in Oklahoma are frequently termed as "bridge loans" or "fix and flip loans," widely recognized by Oklahoma-based real estate investors and private lenders alike.

Hard Money Loan Scenarios in Oklahoma

Investors across Oklahoma commonly use hard money loans for these specific scenarios:

- Purchasing and renovating distressed properties, like a dated single-family home in Edmond or Norman, without fully relying on personal cash.

- Refinancing a distressed home initially acquired with cash, perhaps a quick cash deal secured in Moore or Lawton, then tapping into equity for renovations.

- Refinancing existing loans on unfinished renovation projects in Oklahoma City, providing additional time and capital to finalize rehab efforts.

- Acquiring undervalued off-market Oklahoma properties intending immediate resale without renovation.

- Refinancing cash-bought properties to extract equity for other Oklahoma real estate opportunities.

- Refinancing completed renovations in markets like Tulsa to extend sale or refinance windows.

How it Works

Hard money loans in Oklahoma typically include two main components:

- Initial Advance: Funds toward the purchase price, wired to the Oklahoma title company at closing.

- Construction Holdback: Funds designated for renovation costs, released via draw reimbursements as renovation milestones in Oklahoma are completed.

Investors have flexibility: some utilize only the initial advance, others opt solely for a construction holdback, but most Oklahoman investors strategically employ both to optimize leverage and minimize out-of-pocket expenses.

Your exit strategy typically includes flipping for profit or refinancing into long-term financing, such as a DSCR loan, to hold as rental property in stable markets like Oklahoma City or Norman.

Who Uses Hard Money Loans in Oklahoma?

- Fix and flip investors ("flippers") targeting emerging Oklahoma neighborhoods.

- Rental investors employing the BRRRR Method (Buy, Rehab, Rent, Refinance, Repeat) prevalent in established rental markets such as Tulsa.

It is common for investors in Oklahoma to adopt a hybrid strategy, flipping select properties while retaining others based on local market conditions.

Hard Money Loan Program Guidelines

| Criteria | Guideline |

|---|---|

| Loan amount (min/max) | $25,000 – $2,000,000 |

| ARV (minimum) | $100,000 |

| Credit score (minimum) | 680 |

| Borrowing entity | LLC or Corporation |

| Initial advance | up to 90% |

| Construction holdback | up to 100% |

| LTARV (maximum) | 75% |

| Origination fee | 1.5 to 2 points |

| Term | 12 to 24 months |

| Interest Rate | Instant Quote Available |

| Exit Strategy: Sale | min 30% ROI |

| Exit Strategy: Refinance | min 1.1 DSCR after repairs |

Project Eligibility

Our mission is to help Oklahomans build wealth through real estate, and our top priority is helping you manage risk effectively. Across our Oklahoma lending portfolio, fewer than 0.5% of originated hard money loans have required foreclosure. We take pride in this track record, and we are deeply committed to supporting your success in the Sooner State.

First-time investors in Oklahoma who take on high-risk renovation projects face significant financial risk. Heavy and extensive rehabs often lead to delays, cost overruns, and exposure to market volatility, especially in areas with limited contractor availability or fluctuating home values like rural Oklahoma counties.

As your lending partner, we work with you as a deal advisor, risk manager, and capital provider. By establishing clear expectations and providing structured guidance, we empower you to grow your real estate business safely. Below, we detail how our rehab scope classification works and how your experience affects eligibility in Oklahoma.

Initial Advance

In Oklahoma, your initial advance depends on both your personal and deal-specific qualifications. We assess the number of investment properties you've owned in Oklahoma (or comparable markets) over the past 24 months and the number of similar rehab projects completed in the past five years. A minimum credit score of 680 is required, though we prefer scores of 720+.

Realtors, licensed general contractors, and professional engineers in Oklahoma may qualify for increased leverage.

If the purchase price exceeds the appraised As Is value for Oklahoma properties, we will use the appraised value—not the contract price—to determine the initial advance.

Your projected exit strategy also influences your initial advance. If you're planning to sell, you must project a minimum 30% gross margin and a profit of at least $15,000. For rental strategies, or if your sale projections fall short, your projected DSCR after renovations must be at least 1.1. Our Fix and Flip Calculator and DSCR Calculator can help you analyze your Oklahoma-specific deal.

If the property has a rural designation in Oklahoma, we require a minimum experience level of 3, and the initial advance will be reduced.

Experience-Based Tiers

| Tier | Verifiable Experience |

|---|---|

| 1 | 0 |

| 2 | 1 to 2 |

| 3 | 3 to 4 |

| 4 | 5 to 9 |

| 5 | 10+ |

Initial Advance by Tier

| Tier | Initial Advance (% of purchase price) |

|---|---|

| 1 | 80%* |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

(*) Exceptions up to 85% are considered for excellent credit and strong liquidity.

Adjustments to Initial Advance

| Scenario | Adjustment |

|---|---|

| Credit score less than 720 | -5% |

| Full gut rehab | -5% |

| New market (within Oklahoma) | -5% |

| Licensed Oklahoma Realtor | up to +5% |

| Licensed General Contractor (OK) | up to +10% |

| Licensed Professional Engineer (OK) | up to +10% |

| Rural Oklahoma location | -20% (Exp. 3+) |

Rehab Scope Classification

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget < 25% of purchase price |

| Moderate | Rehab budget 25% - 49.99% of purchase price |

| Heavy | Rehab budget 50% - 99.99% of purchase price |

| Extensive | Rehab budget >= 100% of purchase price or value |

Note: A "lopsided deal" in Oklahoma is one where the purchase price or As Is value is less than the renovation budget. These require strict LTFC limits.

Rehab Scope Eligibility

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | Yes | No | No | No |

| 2 | 1-2 | Yes | Yes | Yes | No |

| 3 | 3-4 | Yes | Yes | Yes | Yes |

| 4 | 5-9 | Yes | Yes | Yes | Yes |

| 5 | 10+ | Yes | Yes | Yes | Yes |

LTARV Limits

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | Eligible | Eligible | Eligible | Eligible | Eligible |

| Moderate | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Heavy | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Extensive | Ineligible | Ineligible | Eligible | Eligible | Eligible |

LTFC Limits

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | N/A | N/A | N/A | N/A | N/A |

| Moderate | Ineligible | N/A | N/A | N/A< | N/A |

| Heavy | Ineligible | N/A | N/A | N/A< | N/A |

| Extensive | Ineligible | Ineligible | 85% | 90% | 90% |

These limits ensure Oklahoma investors retain sufficient equity to mitigate execution risk on high-leverage, complex projects.

Example: No Experience

Property in Midwest City, OK

- Purchase Price: $100,000

- Tier: 1 (0 completed projects)

- Credit Score: 695

- Rehab Budget: $24,000

- ARV: $150,000

- Initial Advance: $75,000 (75%)

- Construction Holdback: $24,000

- Total Loan: $99,000

- LTARV: 66%

- LTFC: 79.8%

- Interest Accrual: Full boat

Example: No Experience, Excellent Credit

Property in Broken Arrow, OK

- Purchase Price: $100,000

- Tier: 1 (0 completed projects)

- Credit Score: 750

- Rehab Budget: $24,000

- ARV: $150,000

- Initial Advance: $80,000 (80%)

- Construction Holdback: $24,000

- Total Loan: $104,000

- LTARV: 69.33%

- LTFC: 83.9%

- Interest Accrual: As disbursed

Example: 5 Completed Projects

Property in Tulsa, OK

- Purchase Price: $100,000

- Tier: 4 (5 similar verified rehabs)

- Credit Score: 750

- Rehab Budget: $20,000

- ARV: $150,000

- Initial Advance: $90,000 (90%)

- Construction Holdback: $20,000

- Total Loan: $110,000

- LTARV: 73.33%

- LTFC: 91.67%

- Interest Accrual: As disbursed

Refinance Using As Is Value Instead of Cost Basis

When refinancing an Oklahoma property, we typically lend against the cost basis (purchase price + capital improvements). However, if your property has appreciated and qualifies, we can lend based on the higher As Is value.

To qualify for this in Oklahoma:

- Property must be habitable (C4 or better condition)

- Owned for at least 3 years

- Clean payoff statement (no late fees or penalties)

- Credit Score: 680+

- Experience Tier: 3 or higher

- Clear evidence that As Is value exceeds cost basis

- Supporting scenario (e.g., previously rented out in Norman, now vacant and ready for renovations)

Wholesale Transactions and Price Run-Ups in Oklahoma

If you’re purchasing a property in Oklahoma through a wholesaler or a double close, OfferMarket may include the wholesaler markup in the cost basis, up to 20% of the A-B contract price.

For example:

- A-B Contract: $100,000 (wholesaler purchases from original owner)

- B-C Assignment: $25,000

- As Is Value: $125,000

- Financed Value Basis: $120,000

Requirements:

- Assignment fee max: 20% of original purchase price

- Full chain of contracts (A-B and B-C)

- Wholesaler operating agreement

- No MLS listing permitted

- No finder/referral fees allowed

- Transaction must be arm’s length

Construction Holdback in Oklahoma

Construction holdback funds are released as reimbursements for completed work in Oklahoma. Reimbursement draws are processed quickly, often within 0–2 business days, ensuring local contractors and timelines stay on track.

| Draw Criteria | Oklahoma Guidelines |

|---|---|

| Minimum draw | None |

| Maximum draw | 100% of holdback |

| Materials delivered only | 50% with receipts |

| Inspection | App-based (self-serve) |

| Draw Fee | $270 |

| Wire Fee | $30 |

You can choose to forgo the construction holdback if you plan to fund the rehab with your own capital. For loans above $100K, you only accrue interest on funds actually disbursed ("As Disbursed" method).

Appraisal and In-House Valuation in Oklahoma

All hard money loans in Oklahoma require a property valuation. Depending on your scenario and project scope, this may be fulfilled through a third-party appraisal or our internal in-house valuation.

In-House Valuation

| Criteria | Requirement |

|---|---|

| Property Type | 1-4 unit residential |

| Experience Tier | 4 or higher |

| Credit Score | 720+ |

| Rural Designation | Not eligible |

| New Market | Not eligible |

| LTARV | Max 70% |

We reserve the right to require a full appraisal even when these conditions are met.

Exterior Appraisal

Eligible for properties acquired via:

- Foreclosure auction (common in counties like Pottawatomie or Garfield)

- Sheriff’s sale

- REO or bankruptcy sale

- Online real estate auctions

Exterior appraisals must be dated within 120 days of closing. If older than 120 days but under 180, a recertification is required.

Interior Appraisal

Used for all other transactions:

| Property Type | Appraisal Forms |

|---|---|

| Single Family | 1004 + 1007 ARV with As Is (non-gridded) |

| 2–4 Unit | 1025 + 216 ARV with As Is (non-gridded) |

| Condo | 1073 + 1007 ARV with As Is (non-gridded) |

We handle all orders via approved appraisal management companies (AMCs) in Oklahoma, and you will receive a link to pay the invoice. Unpaid appraisals will delay your loan file.

Appraisal Transfers

Appraisals ordered outside of OfferMarket can be transferred if:

- Ordered via an approved AMC

- Less than 180 days old

- Recertified if 120–179 days old

- Transfer letter from lender confirms compliance with Appraiser Independence Requirements (AIR)

- Original appraisal files and paid invoice are submitted

Stabilized Hard Money Loans in Oklahoma

If your Oklahoma property is rent-ready (C4 condition or better) with no deferred maintenance, we can offer a "stabilized" loan:

| Criteria | Guideline |

|---|---|

| LTV Max | Tier 1-2: 70%; Tier 3-5: 75% |

| LTFC Max | Tier 1-2: 80%; Tier 3-5: 90% |

| Condition | C1–C4 |

| Max Term | 12 months |

Key Loan Details for Oklahoma Investors

| Criteria | Details |

|---|---|

| Loan Amount | $25,000 – $2,000,000 |

| Units per Property | 1 – 4 |

| Eligible Property Types | Non-owner occupied SFRs, condos, 2–4 unit multi-family |

| Minimum SqFt | SFR: 700+; Multi-unit: 500+ per unit |

| Max Acreage | 5 acres |

| LTC | Up to 90% purchase; 100% rehab |

| LTARV | Up to 75% |

| Down Payment | Minimum $10,000 if purchase < $100K |

| Term | 12 months standard; up to 24 months available |

| Points | 1.5–2 points (minimum $2,000) |

| Prepayment Penalty | None |

| Occupancy | Non-owner occupied |

| Eligible Regions | Oklahoma and all qualifying U.S. states |

| Amortization | Interest-only with balloon payment |

| Interest Accrual | < $100K: full boat; ≥ $100K: as disbursed |

Extensions

Hard money loans in Oklahoma are structured for short-term use—typically between 12 and 24 months. Most Oklahoma investors pay off these loans within 12 months. While extensions are available, they are not ideal due to associated fees, increased interest, and potential foreclosure risk if not paid off by the end of the extension.

To avoid needing an extension on your Oklahoma hard money loan, steer clear of:

- Inexperienced or under-referenced general contractors

- Overly ambitious rehab scopes relative to your experience or cash reserves

- Projects in municipalities with slow permitting or inspection processes (e.g., rural counties)

- Delayed access to the property (e.g., inherited tenants or eviction situations)

- Properties lacking a clear dual exit strategy (e.g., resale or refinance)

Addressing these risks will significantly reduce the likelihood of delays that might require a loan extension.

Extension Limits

| Initial Loan Term | Max Extension |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Extension Terms and Fees

| Extension Term | Fee |

|---|---|

| 3 months (1st) | 1% of total loan amount |

| 3 months (2nd) | 1.5% of total loan amount |

| 6 months (1st) | 2.5% of total loan amount |

Extension Prerequisites

To be approved for a loan extension in Oklahoma, your builder's risk insurance policy must remain active and cover the new extension period.

Ineligible Property Types in Oklahoma

We do not provide hard money loans in Oklahoma for the following property types:

- Mixed use buildings

- Multifamily properties with 5+ units

- Condotels or co-ops

- Mobile or manufactured homes

- Commercial real estate

- Cabins or log homes

- Properties with oil or gas leases

- Operational farms, orchards, or ranches

- Vacation or seasonal rentals

- Unique, exotic, or ultra-luxury properties

- Properties accessed by unpaved/dirt roads

Exception Scenarios for Oklahoma

| Scenario | Notes |

|---|---|

| Guarantor credit score 660–679 | Case-by-case basis |

| Leasehold (ground rent) | Considered individually |

| Single family 500–699 sq ft | Eligible by exception |

| 2–4 unit property with unit <500 sq ft | Exception reviewed |

| Initial advance based on high As Is value | Requires thorough review |

| Non-arm’s length transactions | Detailed documentation required |

| Financed interest payments | May be offered to preserve liquidity |

Credit and Background Review for Oklahoma

| Item | Requirement |

|---|---|

| Tri-Merge Scores | Use middle score of 3; lowest of 2 |

| No Mortgage Tradelines | 6 months interest reserves required |

| Fewer than 5 Tradelines | 6 months interest reserves required |

| Bankruptcy | Must be discharged 4+ years ago |

| Foreclosure | Must be completed 4+ years ago |

| Bankruptcy/Foreclosure within 4–7 years | 3 months interest reserves |

| Recent Late Mortgage | LOE required; subject to review |

| Past Due Tradelines | Must be resolved before funding |

| Liens or Judgments | Must be paid before funding |

| Civil Lawsuits | LOE required; subject to review |

| Criminal Charges | Not eligible if current; serious/repeat offenses disqualify |

Interest Reserves in Oklahoma

These are funds collected at settlement and held in escrow to cover early interest payments.

| Guarantor Credit | Required Reserves |

|---|---|

| FICO 700+ | 1 month |

| FICO 660–699 | 3 months |

| FICO 660–699 with risk flags | 6 months |

| At Lender Discretion | 0–6 months |

Financed Interest Payments

To preserve liquidity and help investors avoid credit card overuse during rehab, OfferMarket may offer financed interest payments in Oklahoma. This allows accrued interest to be added to your final payoff statement instead of requiring monthly interest payments.

Example:

- Loan Amount: $100,000

- Interest Rate: 12%

- Hold Period: 9 months

- Accrued Interest: $9,000

Payoff Statement:

- Principal: $100,000

- Interest: $9,000

Property Sourcing Guidelines for Oklahoma Investors

To ensure smooth and secure transactions for Oklahoma investors, the following sourcing and documentation guidelines apply:

- New Market Transactions: If you are investing in an Oklahoma market for the first time, you must provide a General Contractor agreement or a Letter of Explanation (LOE) outlining why a GC is not needed.

- Wholesale Deals and Price Escalation: Transactions involving significant price increases (e.g., double closings or assignments common in Oklahoma City and Tulsa markets) require supporting documents. We review chain of title, assignments, and wholesale spreads carefully.

- Major Renovations and Conversions: For condo conversions, significant structural changes, or properties needing major permits, documentation from a licensed Oklahoma architect or engineer—or municipal permits—must be included.

Required Documents:

- Signed purchase contracts

- Settlement statements

- Payoff letters (if applicable)

- Track record of borrower

- Entity formation documents (Articles, Operating Agreement, etc.)

Insurance Guidelines for Oklahoma Hard Money Loans

It is essential to protect your Oklahoma real estate investments against damage, liability, and construction risks. Builders Risk or Fix and Flip Insurance is required on all loans, offering comprehensive coverage during the rehab or vacancy phase.

Required Coverages and Limits

| Coverage Type | Limit | Required |

|---|---|---|

| Dwelling | Replacement Cost or Loan Amount | Yes |

| Liability | $1M per occurrence / $2M aggregate | Yes |

| Builders Risk | Included | Yes |

| Flood | $250K or Loan Balance (if in FEMA flood zone) | Conditional |

Policy Details

| Item | Requirement |

|---|---|

| AM Best Rating | A- VIII or greater |

| Policy Type | Special Form |

| Deductible | $1,000 to $5,000 |

| Lender's Designation | Mortgagee and Additional Insured |

| Exclusions | No exclusions for windstorm, hail, or named storms |

| Cancellation | 30-day advance notice required |

Pro Tip for Oklahoma Investors: As soon as you take title, install smoke detectors, locks, and security cameras. These small steps not only help comply with insurance requirements but also prevent claims denials in case of incidents.

Frequently Asked Questions

What states does OfferMarket fund hard money loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I do more than one hard money loan at a time in Oklahoma?

Yes. Many Oklahoma investors carry multiple loans simultaneously. We prioritize your financial safety, so we'll help evaluate your liquidity and pace of execution before approving additional deals.

Are hard money loans considered commercial loans?

Yes. These are business-purpose loans issued to your LLC or corporation and are treated as commercial loans under Oklahoma lending laws.

What is the minimum loan amount?

The minimum hard money loan amount in Oklahoma is $25,000.

Which property types are eligible?

Eligible properties include non-owner occupied 1–4 unit residential properties such as:

- Single-family residences

- Townhomes

- Duplexes, triplexes, and fourplexes

- Warrantable condos

Note: Mixed-use, 5+ unit multifamily, and commercial properties are not eligible in this program.

How is Loan-to-Value (LTV) calculated?

LTV typically refers to Loan-to-As-Is-Value. For hard money loans in Oklahoma, we primarily use Loan-to-After-Repair-Value (LTARV) to assess your project’s leverage.

What are the credit requirements?

Minimum FICO score is 680. Exceptions between 660–679 are considered case-by-case. We look at scores for all guarantors in the borrowing entity.

What are the experience requirements?

None. New Oklahoma investors are welcome. More experience unlocks higher leverage and better terms. Each project is assessed against your verified track record.

Does wholesaling count toward experience?

No. Since you did not personally manage the rehab or financial aspects of the project, wholesale deals do not count toward experience tiering.

What documents are required for Oklahoma deals?

Purchase Transactions

| Required Document | Description |

|---|---|

| Purchase Contract | Fully executed by buyer and seller |

| Credit Report | Tri-merge soft credit report for each guarantor |

| Background Report | Required for each guarantor in the borrowing entity |

| Track Record | History of previous completed investment projects |

| ID Verification | Government-issued ID (driver’s license, passport, etc.) |

| Borrowing Entity Docs | Articles of Organization, Operating Agreement, Certificate of Good Standing, W-9 |

| Scope of Work | Detailed rehab budget to support ARV |

| Appraisal Report | Ordered through OfferMarket AMC, uploaded to file |

| Bank Statements | Two most recent personal/business statements per guarantor |

| Letter of Explanation | If required (e.g., large deposits, credit issues) |

Refinance Transactions

| Required Document | Description |

|---|---|

| Settlement Statement | From original purchase transaction |

| Sunk Costs | Receipts and breakdown of already incurred expenses |

| Scope of Work | Itemized rehab plan and budget |

| Appraisal Report | Current valuation ordered via AMC |

| Borrowing Entity Docs | Same as above: formation and tax documentation |

| Bank Statements | Two recent personal or business statements from guarantor(s) |

| Letter of Explanation | If requested by underwriting |

Are there special rules for loans over $1M?

Yes. For Oklahoma loans over $1M:

- Minimum of 3 completed projects

- Strong comp sales within 2 miles (last 6 months)

- FICO 680+ with 5 active tradelines

- Not eligible in rural designated zones

- Full borrower track record required

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit, an additional residence on the same lot |

| Arms-length | Transaction between unrelated parties acting in their own interest |

| Non-Arms-length | Deal involving related or connected parties |

| Initial Advance | Portion of loan used for purchase, wired at closing |

| Construction Holdback | Portion of loan used for renovation, disbursed via draws |

| Interest Reserves | Escrowed interest payments collected upfront |

| LOE | Letter of Explanation for unusual financial items |

| LTC | Loan-to-Cost (purchase + rehab) |

| LTFC | Loan-to-Full-Cost ratio for extensive rehabs |

| LTV | Loan-to-Value of current property condition |

| LTARV | Loan-to-After-Repair-Value (post-rehab value) |

| As Disbursed Interest | Interest charged only on funds released |

| Full Boat Interest | Interest charged on total approved loan amount |

| Lopsided Deal | When rehab costs exceed property value or price |

| GC Agreement | General contractor project agreement |

| DSCR | Debt Service Coverage Ratio (rent ÷ monthly debt) |

Instant Hard Money Loan Quote

OfferMarket Capital LLC is proud to be a leading private lender for Oklahoma real estate investors. Whether you're flipping in OKC or scaling rentals in Tulsa, we’re ready to support your vision.

Join thousands of real estate investors who trust OfferMarket. Membership is free and gives you access to:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull