Hard Money Loan Hawaii

OfferMarket Loans

Check your rate

60 seconds · no credit pull

Last updated: May 9, 2025

At OfferMarket, we’re on a mission to help you build long-term wealth through smart real estate investing — and Hawaii is no exception. Whether you’re scouting fixer-uppers on Oʻahu, flipping bungalows on the Big Island, or renting duplexes on Maui, we offer a comprehensive all-in-one platform built for local investors:

💰 Private Lending

☂️ Insurance Rate Shopping

🏚️ Off-Market Properties

Our Hawaii Hard Money Loan program is crafted to deliver fast, reliable, and cost-effective financing options for 1-4 unit residential investment properties statewide.

Whether you plan to flip your property or stabilize and refinance into a DSCR loan, we’d be honored to play a role in your real estate journey and help you thrive in the Aloha State.

Let’s dive into the OfferMarket Hard Money Loan Program.

What is a hard money loan?

A hard money loan is a short-term real estate loan secured by a physical asset—typically a 1-4 unit residential property. This type of financing is widely used by real estate investors in Hawaii to purchase, renovate, refinance, and profit from properties.

You may hear the term used interchangeably with “bridge loan” or “fix and flip loan.” Regardless of the name, the core idea remains the same: these loans offer speed, flexibility, and funding that conventional loans often cannot match.

Hard money loan scenarios

Real estate investors in Hawaii tap into hard money loans for a variety of reasons:

Purchasing and renovating a dated or storm-damaged home on Kauaʻi, using loan funds instead of personal capital

Refinancing a property initially acquired with cash from a motivated seller, then using the loan to fund needed upgrades

Taking out a new loan to replace an existing high-interest or maturing loan while completing a renovation

Acquiring an investment property in AS IS condition below market value, with no plans for improvements

Releasing equity from a cash purchase to reinvest in a new deal, without making renovations

Refinancing after rehab completion to hold the property longer or sell when market conditions improve

How it works

Every hard money loan in Hawaii from OfferMarket consists of two main parts:

- Initial Advance: This covers a portion of the purchase price and is disbursed to the title company at settlement.

- Construction Holdback: This funds your renovation and is reimbursed through draw requests as work progresses.

You can opt for either component, or both, depending on your strategy. Many Hawaii investors choose both to maximize leverage and reduce personal cash outlay. Others use only the Initial Advance or only the Holdback based on their rehab plans and capital reserves.

Whether you’re flipping a plantation home on Molokaʻi or planning a BRRRR strategy for a Honolulu duplex, we’re flexible. The choice is yours.

Your exit strategy will ultimately guide your financing decisions. You might enter a project with a BRRRR plan—Buy, Rehab, Rent, Refinance, Repeat—but pivot to a flip if the resale market is favorable. Or perhaps you’ll shift from a planned flip to a rental hold if tourism-driven housing demand temporarily cools.

Flexibility is critical in Hawaii’s diverse and dynamic real estate market, where market shifts, seasonal cycles, and local regulations can influence your path. Having dual exit options helps you reduce risk and remain profitable.

Who uses hard money loans?

In Hawaii, real estate investors span a broad spectrum — from first-time flippers on Oʻahu to experienced rental investors expanding portfolios across the islands. Here’s who typically relies on hard money loans in the Aloha State:

- Fix and flip investors – Also known as "flippers," these investors seek to buy undervalued homes, renovate them, and quickly sell for a profit. Whether it's a beach cottage in Hilo or a 1960s walk-up in Honolulu, speed and funding flexibility are critical.

- Rental property investors – Especially those following the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). Our Hawaii-based clients use our Fix and Rent bundle to transition seamlessly from hard money to DSCR loans, especially in popular long-term rental zones like Kihei or Kailua.

Many investors pursue a hybrid model — flipping certain properties while holding others as rentals. This dual approach is particularly valuable in a market like Hawaii where housing trends and rental demand vary island by island.

Hard Money Loan Program Guidelines

| Criteria | Guideline |

|---|---|

| Loan amount (minimum) | $25,000 |

| Loan amount (maximum) | $2,000,000 |

| ARV (minimum) | $100,000 |

| Experience | Not required |

| Credit score (minimum) | 680 |

| Borrowing entity | LLC or Corporation |

| Initial advance | up to 90% |

| Construction holdback | up to 100% |

| LTARV (maximum) | 75% |

| Interest rate | get instant quote |

| Origination fee | 1.5 to 2 points |

| Term | 12 to 24 months |

| Points out | None |

| Prepayment penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full (51% of borrowing entity must guarantee) |

| Exit strategy: Sale | minimum 30% ROI |

| Exit strategy: Refinance | minimum 1.1 DSCR after repairs |

| Valuation | Appraisal report or In-house valuation |

| SqFt (minimum) | Single family: 700+ 2-4 unit: 500+ per unit Condo: 500+ |

| Acreage (maximum) | 5 |

| Interest accrual | Under $100K loan: full boat $100K+ loan: as disbursed |

| Advanced draws | Lender discretion |

| Down payment (minimum) | $10,000 |

Project Eligibility

At OfferMarket, your success is our priority. In Hawaii, where real estate investments often involve unique logistics and island-specific permitting, we prioritize conservative risk management to help you avoid common pitfalls.

Fewer than 0.5% of our nationwide loans ever go into foreclosure. We intend to keep that number low by guiding you into projects you’re equipped to manage. That’s especially critical when tackling properties with large-scale renovations or remote access in places like Lānaʻi or Kauaʻi.

We work closely with borrowers as a funding partner, risk manager, and deal advisor. Our structured rehab scope system ensures you’re approved for projects that match your experience and capacity.

Initial Advance

Your initial advance is calculated based on deal-specific and borrower-specific factors. Here's what we look at:

Number of rental or flip projects completed in the last 5 years

Credit score (minimum 680, preferably 720+)

Professional credentials (Realtors, General Contractors, Engineers are eligible for higher leverage)

If your contract purchase price is higher than the appraised As Is value, we base the loan on the appraised value.

If your plan is to flip the property, we require a projected gross margin of 30% or more and at least $15,000 in profit. If you’re planning to refinance and hold, we look for a DSCR of at least 1.1 post-repairs.

Properties in remote or rural areas of Hawaii may require more experience (Tier 3 or higher) and will receive limited leverage to protect against liquidity risks in those markets.

Experience-based Tiers

| Tier | Verifiable experience |

|---|---|

| 1 | 0 |

| 2 | 1 to 2 |

| 3 | 3 to 4 |

| 4 | 5 to 9 |

| 5 | 10+ |

Initial Advance by Tier

| Tier | Initial advance (% of purchase price) |

|---|---|

| 1 | 80%* |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

* Borrowers with excellent credit and liquidity may be eligible for 85% at Tier 1 on an exception basis.

Adjustments to Initial Advance

| Scenario | Adjustments |

|---|---|

| Credit score less than 720 | -5% |

| Full gut rehab | -5% |

| New market | -5% |

| Licensed Realtor | +5% |

| Licensed General Contractor | +10% |

| Licensed Professional Engineer | +10% |

| Rural | -20% (3+ experience required) |

Rehab Scope Classification

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget is less than 25% of purchase price |

| Moderate | Rehab budget is 25% to 49.99% of purchase price |

| Heavy | Rehab budget is 50% to 99.99% of purchase price |

| Extensive | Rehab budget is 100%+ of purchase price — includes additions, low-cost purchases, and high renovation ratios |

Rehab Scope Eligibility

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | Eligible | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | Eligible | Eligible | Eligible | Ineligible |

| 3 | 3-4 | Eligible | Eligible | Eligible | Eligible |

| 4 | 5-9 | Eligible | Eligible | Eligible | Eligible |

| 5 | 10+ | Eligible | Eligible | Eligible | Eligible |

LTARV Limits

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | 70% | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | 70% | 70% | 70% | Ineligible |

| 3 | 3-4 | 75% | 75% | 75% | 70% |

| 4 | 5-9 | 75% | 75% | 75% | 70% |

| 5 | 10+ | 75% | 75% | 75% | 70% |

LTFC Limits

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | N/A | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | N/A | N/A | N/A | Ineligible |

| 3 | 3-4 | N/A | N/A | N/A | 85% |

| 4 | 5-9 | N/A | N/A | N/A | 90% |

| 5 | 10+ | N/A | N/A | N/A | 90% |

Example: No Experience

Purchase price: $100,000

Tier: 1 (no verified experience)

Credit score: 695

Rehab budget: $24,000

ARV: $150,000

Initial advance: $75,000 (75%)

Construction holdback: $24,000

Total loan: $99,000

LTARV: 66%

LTFC: 79.8%

Interest: Full boat

Example: No Experience, Excellent Credit

Purchase price: $100,000

Tier: 1 (no verified experience)

Credit score: 750

Rehab budget: $24,000

ARV: $150,000

Initial advance: $80,000 (80%)

Construction holdback: $24,000

Total loan: $104,000

LTARV: 69.33%

LTFC: 83.9%

Interest: As disbursed

Example: 5 Experience

Purchase price: $100,000

Tier: 4 (5 similar verifiable experiences)

Credit score: 750

Rehab budget: $20,000

ARV: $150,000

Initial advance: $90,000 (90%)

Construction holdback: $20,000

Total loan: $110,000

LTARV: 73.33%

LTFC: 91.67%

Interest: As disbursed

Refinance using As Is value instead of Cost Basis for Initial Advance

In certain refinance scenarios, especially common in Hawaii where properties appreciate quickly, you may want to tap into equity based on current value rather than just your cost basis. Our standard lending model prioritizes equity by funding against your actual capital invested — that is, purchase price plus any already incurred renovation costs.

However, if you’re refinancing a seasoned property — say, a triplex in Kaimukī you’ve held for several years — and it’s now worth significantly more, OfferMarket may lend based on the As Is value under the following conditions:

Property is in livable condition (C4 or better)

Held for at least 3 years

Clean payoff statement from the previous lender

Borrower credit score of 680+

Experience Tier 3 or higher (minimum of 4 similar verified rehab projects)

Strong market comps supporting the valuation

Logical story (i.e., property was rented, tenants moved out, now ready for renovation and resale)

Transactions involving wholesalers, price run-ups

We understand the dynamics of Hawaii's tight-knit investing community where wholesaler deals are common. If your deal includes a markup from a wholesaler or double-close structure, we’ll include the increased cost in your value basis — within limits.

Example:

A-B Contract (seller to wholesaler): $100,000

B-C Contract (wholesaler to you): $125,000

As Is Value: $125,000

Allowable markup: $20,000 (20% max of original purchase price)

We’ll lend on the higher price as long as:

The markup doesn’t exceed 20%

The property wasn’t listed on the MLS

We receive full A-B and B-C contracts and wholesaler documentation

We do not finance referral fees or non-arm’s length premiums. These deals must be fully documented, legitimate transactions.

Construction Holdback

In Hawaii’s competitive and high-cost renovation landscape, preserving your liquidity is key. Our Construction Holdback helps you do just that. It covers your rehab costs and is disbursed through draw reimbursements as the work progresses.

If you already have the cash and prefer not to use a holdback, that’s fine — we can structure your loan without it. But if you do use it, here’s how it works:

| Criteria | Draw Processing Guideline |

|---|---|

| Minimum draw amount | None |

| Maximum draw amount | 100% of remaining holdback |

| Minimum number of draws | 0 |

| Maximum number of draws | None |

| Materials delivered but not installed | 50% (must show receipt/invoice) |

| Draw inspection | App-based (self-inspection) |

| Draw turnaround | 0–2 business days |

| Draw fee | $270 |

| Wire fee | $30 |

Hawaii investors love our rapid draw processing — often same-day — which helps keep your project on schedule without needing to float large upfront costs.

Appraisal and In-house valuation

A thorough valuation is essential to protect your deal and ours. For properties on the islands, where values vary block by block, we offer several appraisal routes depending on your scenario and experience.

In-house valuation

| Criteria | Eligibility requirement |

|---|---|

| Property type | Single family, Duplex, Triplex, Quadplex |

| Tier | 4 or higher |

| Credit score | 720+ |

| Rural | Not allowed |

| New market | Not allowed |

| LTARV | 70% max |

Even if you qualify, OfferMarket may still require an appraisal based on the risk profile of the property.

Exterior appraisal

An exterior-only appraisal is permitted if your Hawaii investment property is:

A REO sale

Foreclosure auction

Sheriff’s sale

Online auction

Bankruptcy sale

The report must be no older than 120 days from your settlement date. If it’s older than 120 but under 180 days, we’ll need recertification.

Interior Appraisal

Any other scenario not mentioned above will require a full interior appraisal.

| Property type | Appraisal forms |

|---|---|

| Single family | 1004 + 1007 ARV with As Is value included |

| 2-4 Unit | 1025 + 216 ARV with As Is value included |

| Condo | 1073 + 1007 ARV with As Is value included |

OfferMarket will order the appraisal through an approved AMC. You’ll simply complete the invoice, and we’ll upload the report directly to your Loan File.

Appraisal Transfer

Already paid for an appraisal with another lender? No problem — we can transfer it as long as:

It was ordered via AMC

It’s less than 180 days old at closing

The lender provides a signed transfer letter certifying AIR compliance

You share the full report (PDF + XML) and proof of payment

Scenario: Stabilized Hard Money Loan

If your Hawaii property is in great condition (no deferred maintenance, C4 or better), we can underwrite the loan based on its current As Is value and provide up to 75% LTV.

| Criteria | Guideline |

|---|---|

| LTV (max) | Tier 1–2: 70%, Tier 3–5: 75% |

| LTFC (max) | Tier 1–2: 80%, Tier 3–5: 90% |

| Appraisal condition | C1 to C4 |

| Loan Term (max) | 12 months |

This option is ideal if you're preparing the property for resale or listing it as a rental and don’t need extensive rehab.

Key Loan Details

| Criteria | Details |

|---|---|

| Loan Amount | $25,000 to $2,000,000 |

| Units per Property | 1–4 |

| Eligible Property Types | Single-family homes, 2–4 unit multifamily, condos, townhomes |

| Property Size | SFR: ≥700 sqft Condo/2–4 unit: ≥500 sqft/unit |

| Acreage limit | 5 acres |

| LTC | Up to 90% purchase, 100% rehab |

| LTARV | Up to 75% |

| Down Payment | Minimum $10K (under $100K price) |

| Term | 12 months standard; up to 24 months |

| Extensions | Up to 50% of original term |

| Points | 1.5 to 2 points |

| Prepay Penalty | None |

| Occupancy | Non-owner occupied only |

| Transaction Types | Purchase, Refinance |

| Regions | All U.S. states except those restricted |

| Amortization | Interest-only w/ balloon |

| Interest Accrual | Under $100K: Full Boat $100K+: As Disbursed |

Extensions

While hard money loans are short-term by design, sometimes you need more time — especially with Hawaii’s slower permitting cycles or unexpected island logistics. Extensions are available but should be used sparingly.

Avoid delays by planning for:

Contractor availability

Local permit timelines

Clean title access (i.e. no lingering tenants or liens)

Market shifts that impact exit strategy

Extension Limits

| Initial Loan Term | Max Extension |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Extension Terms and Fees

| Extension Term | Fee |

|---|---|

| 3 months (1st) | 1% of total loan amount |

| 3 months (2nd) | 1.5% |

| 6 months (1st) | 2.5% |

Before requesting an extension, make sure your insurance policy is current and active through the new maturity date.

Ineligible Property Types

To ensure quality underwriting and limit risk exposure, our Hawaii hard money loan program does not support certain property types. Regardless of the island — from Oʻahu to Molokaʻi — if the asset falls into any of the categories below, it is not eligible for financing through this program:

Mixed use (i.e., retail below, residential above)

Multifamily with 5+ units

Condotels (common in Waikīkī high-rises)

Co-ops

Mobile or manufactured homes

Commercial buildings

Cabins or log homes (often found in more rural areas like Volcano, HI)

Properties with oil/gas leases

Working farms, ranches, or orchards

Seasonal vacation rentals (i.e., short-term Airbnb-only listings)

Unpaved access roads

If your Hawaii property falls into one of these categories, reach out — we may still offer options through our alternative lending programs.

Exception Scenarios

We strive to be flexible where possible. If your Hawaii deal includes any of the following characteristics, it may be considered an exception — reviewed on a case-by-case basis:

Guarantor credit score between 660–679

Leasehold properties (common in parts of Honolulu and Maui)

Single-family homes sized 500–699 SQFT

2–4 unit properties with any unit below 500 SQFT

Loans based on As Is value exceeding cost basis

Non-arm’s length transactions (i.e., family members involved)

Financed interest payments

Unusual ownership or title scenarios

We evaluate each file holistically and work to provide options that align with your experience and the project’s potential.

Borrower and Guarantor Requirements

| Item | Requirements / Eligibility |

|---|---|

| Borrowing Entities | Must be an LLC or Corporation. No nonprofits. |

| Eligible Borrowers | U.S. Citizens, Permanent Residents, and qualified Foreign Nationals. |

| Foreign Nationals | Must have: - Valid Passport - Valid U.S. Visa (not student/tourist unless Visa Waiver Program) - U.S. FICO score if acting as Guarantor |

| Credit Requirements | - Minimum FICO: 680 - Tri-Merge report < 120 days old - If <5 tradelines: 6 months interest reserves required |

| Liquidity Requirements | Guarantors must verify sufficient liquidity to cover estimated cash to close + 25% of rehab budget |

| Guaranty Structure | - Purchases: at least 51% of entity must guarantee - Cash-out refinances: 100% must guarantee - Full Recourse required |

| Net Worth | Combined net worth of guarantors must equal at least 50% of loan amount |

Credit and Background Items

We use a full tri-merge credit report and background screening to ensure our Hawaii-based borrowers meet minimum standards. Here’s how we review your file:

Credit Scores:

3 scores: middle score

2 scores: lower score

Mortgage history:

No mortgage tradelines → 6 months reserves

Fewer than 5 tradelines → 6 months reserves

Bankruptcy or foreclosure:

Must be 4+ years old to be considered

If between 4–7 years → 3 months reserves

Late mortgage payments:

- Subject to review with Letter of Explanation (LOE)

Judgments, tax liens, or child support arrears:

- Must be resolved before funding

Pending legal actions:

Civil: reviewed case by case

Criminal: ineligible if financial or serious in nature

Interest Reserves

To keep your Hawaii rehab project moving smoothly and protect your liquidity, we sometimes apply interest reserves — especially for borrowers with limited credit history or experience.

| Interest Reserve | Scenario |

|---|---|

| 0 month | At lender’s discretion |

| 1 month | Guarantor FICO 700+ |

| 3 months | Guarantor FICO 660–699 |

| 6 months | FICO 660–699 and any concerning credit/background flag |

These reserves are escrowed and applied to your interest as it accrues. You don’t need to make monthly payments until reserves are depleted.

Financed Interest Payments

If you're undertaking a major renovation in Hilo or Līhue and want to keep more cash on hand, you may qualify to finance your interest. That means instead of making monthly payments, your accrued interest is rolled into the final payoff.

Example:

Loan amount: $100,000

Rate: 12%

Held: 9 months

Accrued interest: $9,000

Final payoff: $109,000 (principal + interest)

This option is ideal when you're focused on project execution and prefer to defer carrying costs.

Property Sourcing Guidelines

Hawaii’s market is unique, and so are our requirements when you bring us a deal. Here’s what we ask for depending on your situation:

New market: Must submit GC agreement or explain why one isn’t needed

Wholesale or price jumps: Provide A-B and B-C contracts

Major renovations or conversions: Architect/engineer letter or permit

Required docs:

Purchase contract

Settlement statement (if refinancing)

Payoff letters

Track record

Formation documents for your LLC

The clearer your file, the faster we can fund.

Insurance Guidelines for Hard Money Loans

Your Hawaii property — whether mid-rehab or awaiting resale — must be insured properly. That includes both the physical structure and liability protection. Builders Risk policies are required and must meet these thresholds:

| Coverage type | Limit | Required |

|---|---|---|

| Dwelling | Replacement Cost or Loan Amount | ✔ |

| Liability | $1M per occurrence / $2M aggregate | ✔ |

| Builders Risk | Included | ✔ |

| Flood | Greater of $250K or loan balance (if FEMA hazard zone) | Conditional ✔ |

Coverage Details

| Item | Requirement |

|---|---|

| AM Best Rating | A- VIII or higher |

| Policy Type | Special Form |

| Deductible | $1,000–$5,000 |

| Lender Designation | Mortgagee and Additional Insured |

| Exclusions | No named storm, hail, or windstorm exclusions |

| Cancellation | 30-day notice required |

💡 Pro tip: Install smoke detectors, locks, and cameras right after acquisition to comply with insurance terms — especially vital in vacant or remote Hawaii properties.

Frequently Asked Questions

What states does OfferMarket fund hard money loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have multiple hard money loans at once?

Absolutely. Many of our Hawaii investors juggle multiple flips or rentals. If we feel it stretches your liquidity, we’ll let you know and work together to manage risk.

Are hard money loans considered commercial loans?

Yes. Even if you're fixing up a single-family home in Honolulu, the loan is for business purposes — so it's classified as commercial.

What’s the minimum loan amount?

$25,000.

What property types are eligible?

Non-owner occupied residential: single-family, 2–4 unit multifamily, condos, and townhomes.

How is Loan-to-Value (LTV) calculated?

Most Hawaii investors use Loan-To-After-Repair Value (LTARV):

LTARV = (Initial Advance + Holdback) / ARV

What are the credit requirements?

Minimum 680 FICO. Exceptions 660–679 considered. Only guarantors are reviewed.

Is experience required?

No, but it helps. More experience = more leverage. Your tier is based on similar completed projects.

Does wholesaling count toward experience?

No — only actual ownership and project execution qualifies.

What documentation is needed?

Our streamlined Loan File system guides you through everything, and stores reusable docs for future applications.

Purchase Transaction Requirements

When purchasing a property in Hawaii — whether it’s a fixer-upper in Wahiawā or a duplex in Hilo — you'll complete the “Purchase” section of your Loan File. Here’s what you’ll need:

| Document | Requirement |

|---|---|

| Purchase Contract | Signed by both buyer and seller |

| Credit Report | Soft tri-merge report for each guarantor |

| Background Report | Required for each guarantor |

| Track Record | For all entity members involved in real estate |

| ID Verification | Government-issued ID (driver’s license, passport, or green card) |

| Borrowing Entity Docs | Articles of Organization/Incorporation, Operating Agreement/Bylaws, Certificate of Good Standing, and W-9 |

| Scope of Work | Detailed rehab budget for determining ARV |

| Appraisal Report | You’ll pay the AMC invoice; we’ll upload the appraisal |

| Bank Statements | Most recent 2 statements from each guarantor (personal, business, or retirement accounts) |

| Letter of Explanation | If requested (i.e., large deposits, late payments, or legal issues) |

Refinance Transaction Requirements

If you’re refinancing a property in Hawaii — say, cashing out a successful flip in Wailuku or taking equity from a seasoned rental in Kailua — the “Refinance” section of your Loan File is what you’ll complete. Here's what to include:

| Document | Requirement |

|---|---|

| Settlement Statement | From original purchase, signed by buyer and title agent |

| Credit Report | Soft tri-merge report for all guarantors |

| Background Report | Required for each member of the borrowing entity |

| Track Record | Needed for all guarantors |

| ID Verification | Valid government-issued photo ID |

| Borrowing Entity Docs | Operating agreement, articles, certificate of good standing, W-9 |

| Sunk Costs | All prior investments made into the property (purchase + rehab) |

| Scope of Work | Rehab budget to guide ARV and draw releases |

| Appraisal Report | Paid by you and uploaded into the Loan File |

| Bank Statements | Two most recent statements per guarantor |

| Letter of Explanation | If requested by underwriting (i.e., large deposits, prior legal history) |

Are there special requirements for loans over $1M?

Hawaii’s property values are among the highest in the nation, especially in areas like Honolulu, Lahaina, and Kakaʻako. For loans over $1 million (up to our $2M max), we apply enhanced guidelines to ensure stability and success:

| Criteria | Requirement |

|---|---|

| Experience | Minimum Tier 3 (at least 3 similar projects) |

| Market Liquidity | At least 3 comparable sales within a 2-mile radius within past 6 months |

| Credit Score | Minimum 680 with 5+ tradelines with 24-month histories |

| Rural Property | Not eligible if designated “rural” by CFPB and USDA or flagged in appraisal |

| Track Record | Detailed and verified for each entity member |

If your Maui or Big Island investment requires a jumbo hard money loan, we’ll work with you closely to ensure the deal structure supports long-term success.

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit – secondary, standalone unit on the same parcel |

| Arms-length | A deal between unrelated parties with no special relationship |

| Non-arms-length | Deal involving family or business ties; may affect pricing or fairness |

| Initial Advance | Loan portion allocated to property purchase; wired at closing |

| Construction Holdback | Funds allocated for rehab; released via draw reimbursements |

| Interest Reserves | Escrowed interest collected upfront to reduce monthly payments |

| LOE | Letter of Explanation — provides context for anomalies in credit or history |

| LTC | Loan-to-Cost — ratio of loan amount to combined purchase and rehab cost |

| LTFC | Loan-to-Full-Cost — includes all deal expenses including purchase and rehab |

| LTV | Loan-to-Value — ratio of loan amount to current “As Is” value |

| LTARV | Loan-to-After-Repair Value — ratio of total loan to estimated after-rehab value |

| As Disbursed Interest | Interest accrues only on funds released (not entire loan) |

| Full Boat Interest | Interest charged on total loan amount from day one |

| Lopsided Deal | Property where rehab cost exceeds As Is value or purchase price |

| GC Agreement | Contract with licensed General Contractor handling the rehab |

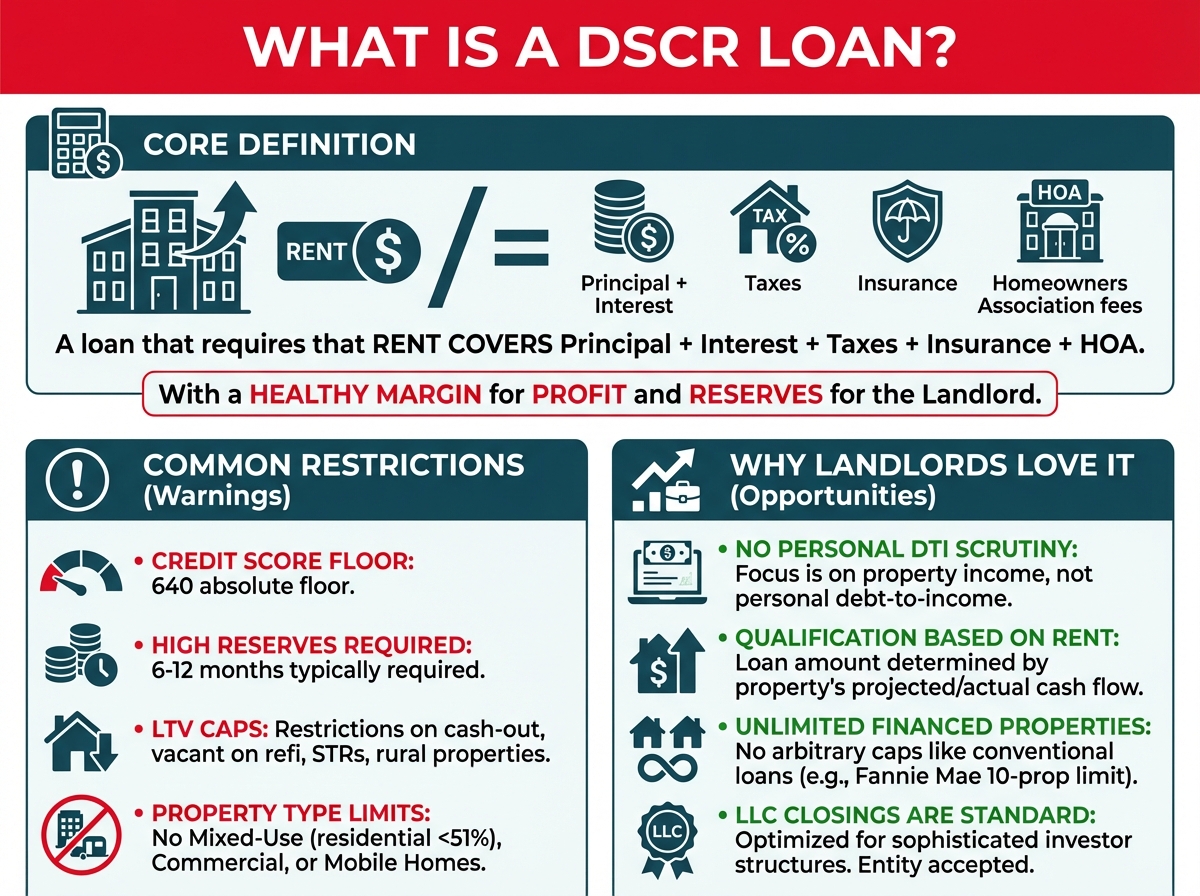

| DSCR | Debt Service Coverage Ratio — measures cash flow relative to loan obligations |

Get Your Instant Hawaii Hard Money Loan Quote

OfferMarket Capital LLC is your go-to source for private lending in Hawaii, specializing in hard money and DSCR loans for 1–4 unit residential properties. Whether you’re acquiring a triplex on Maui, refinancing a rental in Kaneohe, or flipping an estate in Kona — we’re ready to help.

Our platform supports thousands of real estate investors every month and membership is always free. Here’s what you get:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull