*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Fix and Flip Loans: The Complete Guide (Hard Money, HELOANs & More)

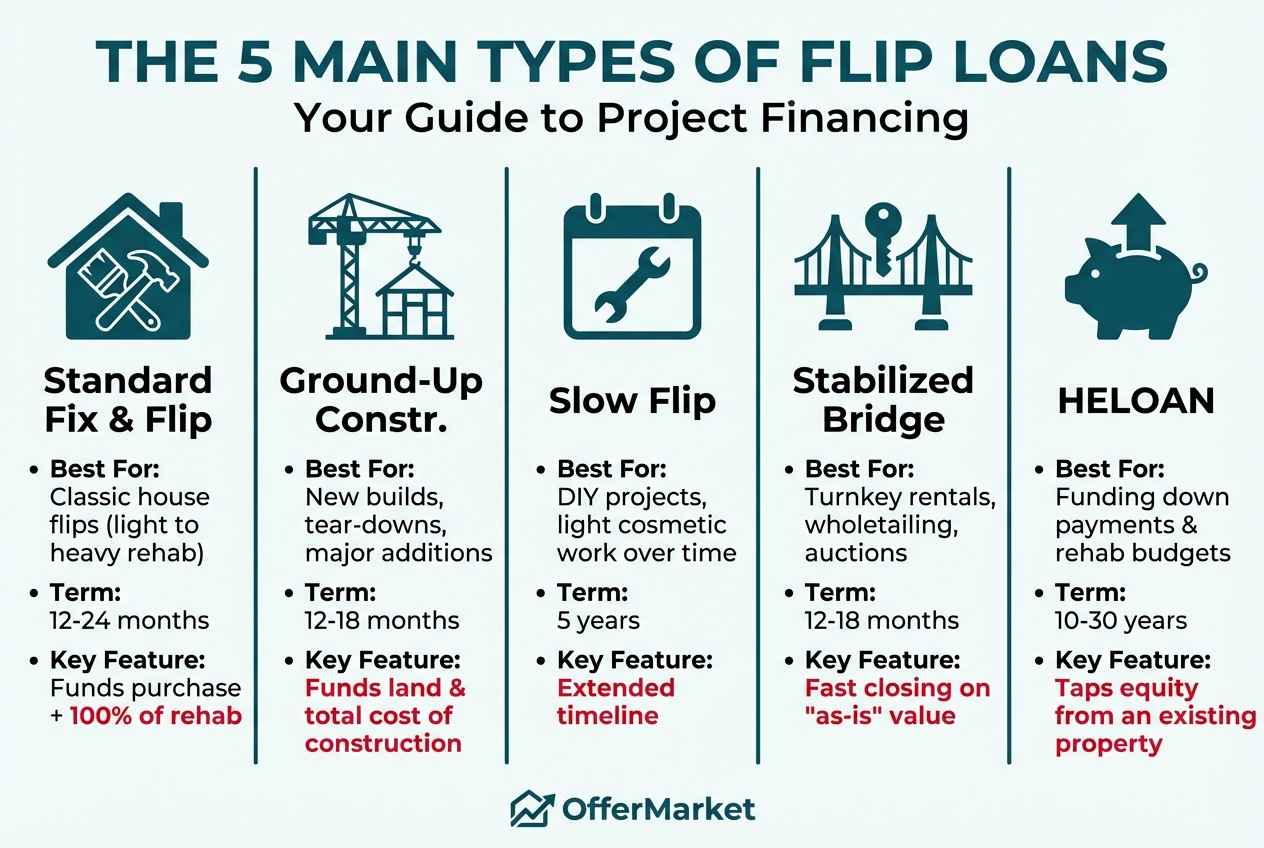

Fix and flip loans are short-term financing instruments used by real estate investors to purchase and renovate properties with the intent to sell for a profit. Unlike traditional mortgages, these loans are underwritten based on the property's After Repair Value (ARV) and the borrower's experience, allowing for high leverage on both the acquisition and renovation costs. The five primary types of financing investors use for flipping projects are Standard Fix & Flip Loans, Ground-Up Construction Loans, Slow Flip Loans, Stabilized Bridge Loans, and Home Equity Loans (HELOANs). Each is designed for a specific project scope, timeline, and investor profile.

Understanding the differences is crucial for maximizing profitability and ensuring a smooth project lifecycle. A standard fix and flip loan, often a form of hard money, is ideal for projects lasting 6-18 months involving cosmetic to significant interior renovations. For building a new property from the ground up, a Ground-Up Construction loan is required. Investors tackling smaller projects over several years might opt for a Slow Flip loan, while those acquiring nearly turnkey properties can use a Stabilized Bridge loan for a fast closing. Finally, a HELOAN allows an investor to tap into equity from an existing property to fund a new project's down payment or rehab budget. This guide will provide an in-depth analysis of each option, helping you match your specific deal to the most suitable financing.

Deep Dive 1: The Standard Fix & Flip Loan (Hard Money)

The Standard Fix & Flip loan is the quintessential financing tool for real estate investors. Often referred to as a hard money loan, it's a short-term, asset-based commercial loan designed specifically to cover the purchase and renovation of a property that will be sold within 12 months. Longer terms of 18 to 24 months are available, but they are exclusively reserved for specific, extensive project types such as expansions, additions, conversions, or building Accessory Dwelling Units (ADUs).

What It Is

This is an interest-only loan where the lender provides funds for both the acquisition of the property and the costs of its renovation. Unlike a conventional loan that focuses on the borrower's personal income, a fix and flip loan's approval hinges on the viability of the project itself—specifically, its After Repair Value (ARV). Lenders are primarily concerned with the property's potential profit, making it an ideal vehicle for investors who may not qualify for traditional financing on an investment property.

How It Works

The loan is structured in two parts: the acquisition funds and the construction holdback.

Acquisition Funds: At closing, the lender funds a percentage of the property's purchase price. This is typically up to 85-90% of the purchase price for experienced investors.

Construction Holdback: The lender approves a budget for 100% of the renovation costs. However, this money is not given to the borrower upfront. Instead, it's held in an escrow account by the lender.

The borrower is responsible for covering the down payment (the portion of the purchase price not covered by the loan) and any closing costs.

Example:

- Purchase Price: $200,000

- Rehab Budget: $50,000

- Total Project Cost: $250,000

- ARV: $350,000

A lender might offer 85% of the purchase price ($170,000) and 100% of the rehab budget ($50,000). The borrower would need to bring the remaining 15% of the purchase price ($30,000) plus closing costs to the table. The $50,000 for rehab is held back to be disbursed as work is completed.

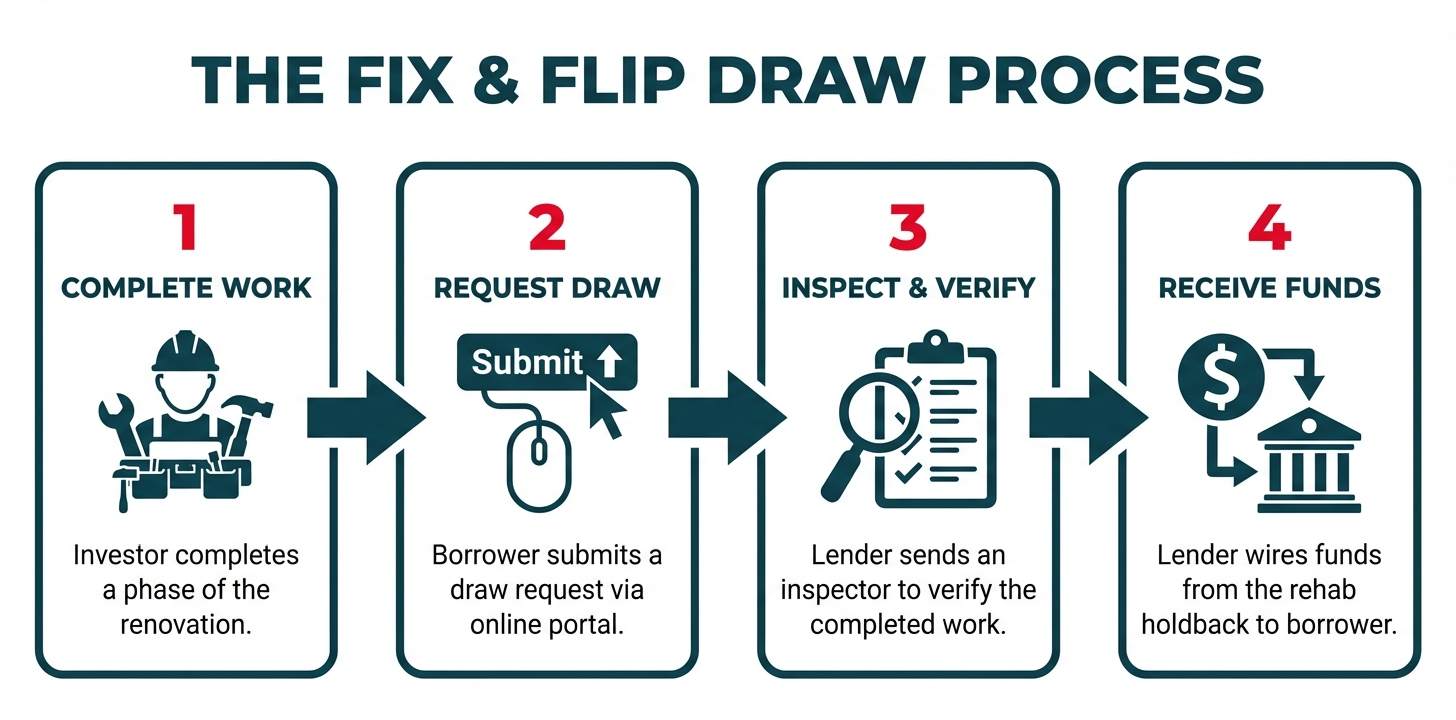

The Draw Process

To access the construction holdback, the borrower must submit a "draw request." This process ensures the lender's funds are being used as intended to increase the property's value.

Work Completion: The investor completes a portion of the renovation according to the agreed-upon Scope of Work (SOW). For instance, after completing the demolition and framing, they might be ready for their first draw.

Draw Request: The borrower submits a request to the lender, often through an online portal or app, detailing the work that has been completed.

Inspection: The lender sends an inspector to the property to verify that the work claimed in the draw request has been completed to a satisfactory standard. Modern lenders like OfferMarket uses app-based inspections or desktop valuation tools to expedite this step.

Disbursement: Once the inspection is approved, the lender releases the corresponding amount of funds from the construction holdback directly to the borrower's bank account. This cycle repeats until the renovation is complete and the entire holdback has been disbursed.

Lender Requirements

While asset-based lenders still have minimum requirements for the borrower. These are often tiered based on experience.

Credit Score: A minimum FICO score of 680 is a common benchmark, though some lenders may go slightly lower for a very experienced borrower with a strong deal.

Experience: Lenders classify investors into tiers. A new investor (0-2 flips in the last 36 months) will receive slightly less favorable terms (e.g., lower leverage, higher interest rate) than a seasoned pro (10+ flips).

Liquidity: Borrowers must demonstrate they have enough cash on hand (liquidity) to cover the down payment, closing costs, and several months of interest payments (known as reserves). A minimum overall net worth equal to at least 10% of the total loan amount.

Entity: Most lenders require the borrower to close in the name of a business entity, such as an LLC or S-Corp, not in their personal name. This protects both the borrower and the lender.

Pros

High Leverage: Lenders often finance up to 90% of the purchase and 100% of the renovation, minimizing the investor's out-of-pocket cash.

Speed to Close: Hard money lenders can close in as few as 10-21 days, a significant advantage in a competitive market compared to the 45-60 days for conventional loans.

Ideal for BRRRR: The loan is perfect for the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, providing the short-term capital needed for the first two steps.

Cons

Short Maturity: The typical 12 month term puts pressure on the investor to complete the project and sell or refinance before the loan's balloon payment is due.

Exit Strategy Pressure: If the market shifts or renovations are delayed, the looming maturity date can force an investor to sell for a lower price than anticipated.

The "Full Boat" Interest Rule: Many hard money loans calculate interest based on the full loan amount (purchase + total rehab) from day one if your loan amount is under $100,000. This increases the total cost of borrowing.

Best For

Standard Fix & Flip loans are best for the classic house flipping model: buying a distressed property, performing light to heavy cosmetic or interior renovations, and selling it within a year. It's the workhorse loan for full-time flippers and BRRRR investors.

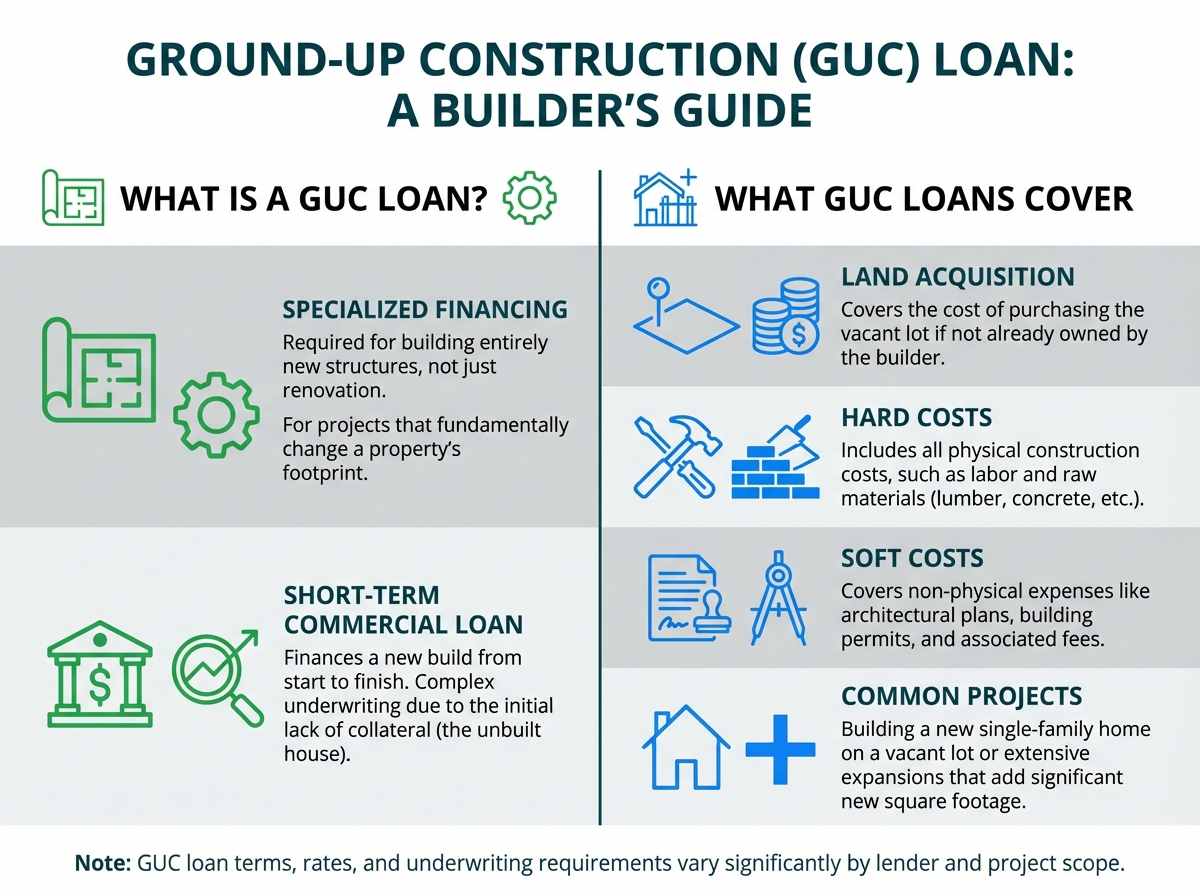

Deep Dive 2: Ground-Up Construction (GUC) & Extensive Expansion Loans

When a project goes beyond renovation and into the realm of new creation, a Ground-Up Construction (GUC) loan is required. This specialized financing is designed for building entirely new structures, such as a single-family home on a vacant lot, or for projects involving extensive expansions that fundamentally change a property's footprint.

What It Is

A GUC loan is a short-term commercial loan that covers the costs associated with a new build. This includes the land acquisition (if not already owned), hard costs (labor and materials), and soft costs (architectural plans, permits, fees). Because the collateral (the house) doesn't exist at the start of the loan, underwriting is significantly more complex and risk-averse.

Lender Requirements

The bar for GUC loans is the highest in real estate investment financing.

Strict Experience Verification: Lenders will not fund a GUC project for a first-time investor but for experience tiers from 3, 4, or 5. They typically require proof of multiple (often 5+) successful and comparable new construction projects or substantial rehabs within the last 2-3 years.

Detailed Plans & Permits: If building or construction permits are not yet issued, lenders will accept detailed architectural plans or an architect letter stamped by a licensed architect or structural engineer.

Strong Financials: Borrowers must verify significant financials, specifically a minimum net worth equal to at least 10% of the total loan amount. However, a vetted 3rd-party General Contractor (GC) is not universally mandatory; highly experienced investors can act as their own GC or provide a Letter of Explanation (LOE) detailing their execution plan, though a formal GC contract is strictly required if the borrower is building in a new market.

Appraisal and Feasibility Study: The loan relies on an "as-completed" appraisal, which estimates the property's value after the new construction is finished. Lenders will scrutinize this value heavily.

Key Metrics

GUC loans use a different primary metric than standard flips.

Loan-to-Total-Cost (LTFC): This is the main metric, sometimes just called Loan-to-Cost (LTC). It measures the loan amount as a percentage of the total project cost (land + hard costs + soft costs). Lenders typically cap LTFC specifically 85% for Tier 3 investors, and 90% for Tier 4 and Tier 5 investors.

"As-Completed" ARLTV: The loan amount will also be capped by a percentage of the After-Repair Value, which in this case is the "as-completed" value. This is usually around 70% of the projected future value. The lender will use the lower of the two calculations to determine the final loan amount.

Underwriting Scrutiny

GUC loans face the highest level of due diligence for several reasons:

No Initial Collateral: The lender is funding a concept. If the project fails midway, they are left with a partially built structure on a plot of land, which is difficult to value and liquidate.

Complexity and Variables: New construction is subject to numerous risks, including supply chain disruptions, labor shortages, weather delays, and municipal inspection hold-ups. Underwriters mitigate municipal and construction delays upfront by requiring detailed architectural plans stamped by a licensed architect or structural engineer, or by requiring approved building and construction permits to be in place

Budget Overruns: It is common for construction projects to go over budget. Lenders need to be confident the borrower has the experience to manage the budget effectively and the personal liquidity to cover any shortfalls.

Pros

Highest Profit Potential: Creating a new property from scratch offers the greatest opportunity for forced appreciation and, consequently, the highest potential profit margins.

Full Creative Control: The investor can build a modern, desirable product tailored to current market demands, avoiding the quirks and hidden problems of an older structure.

Cons

High Risk: The potential for significant delays and budget overruns is much higher than in a standard renovation.

Municipal Delays: The project's timeline is heavily dependent on the efficiency of the local permitting and inspection departments, which can be unpredictable.

Stringent Experience Prerequisites: This type of financing is inaccessible to new or inexperienced investors.

Best For

GUC loans are exclusively for experienced developers and builders undertaking projects like speculative new home construction, tear-downs of old properties to build new ones, or building major additions like an Accessory Dwelling Unit (ADU).

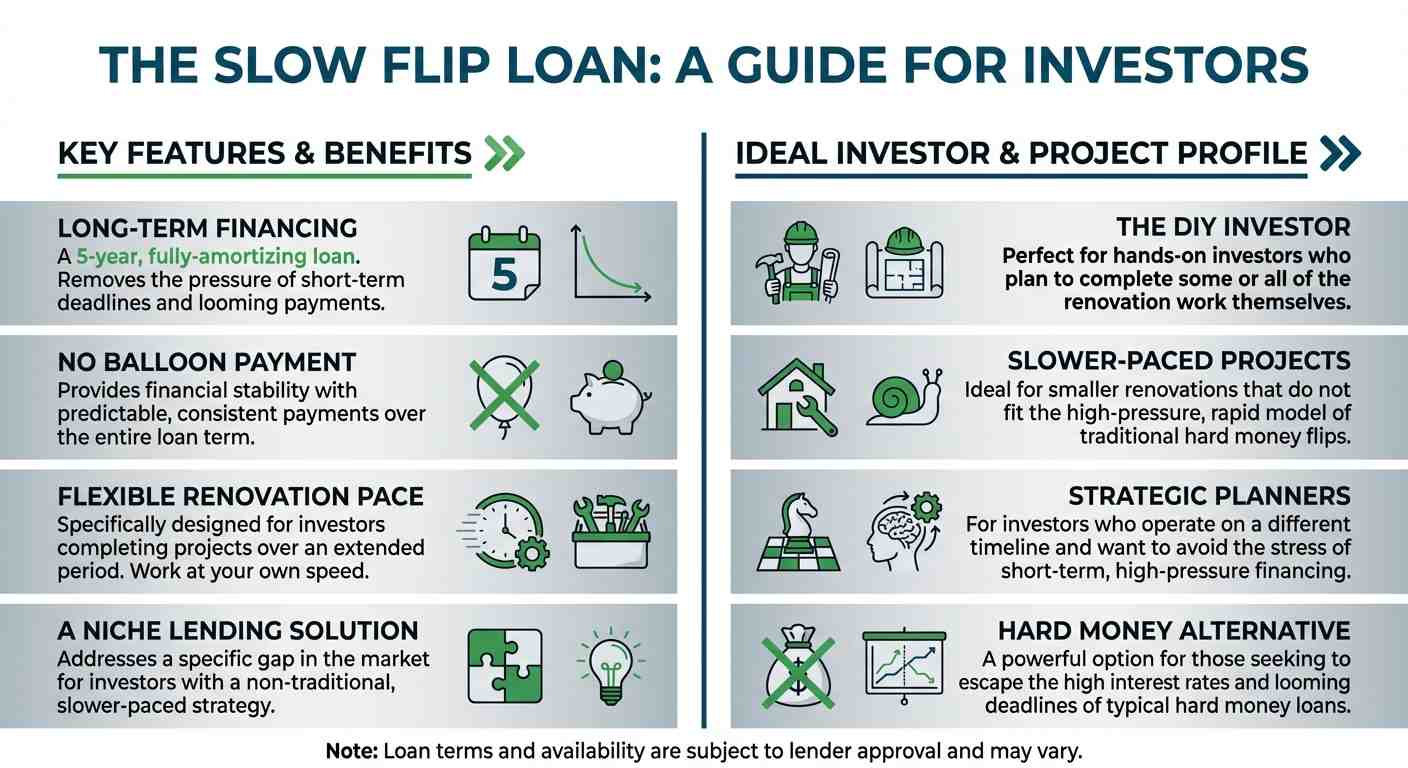

Deep Dive 3: The Slow Flip Loan

The Slow Flip loan is a niche but powerful product designed for investors who operate on a different timeline. It addresses a specific gap in the market: financing for smaller, slower renovation projects that don't fit the high-pressure, short-term model of traditional hard money.

What It Is

A Slow Flip loan is a long-term, fully-amortizing loan with a 5-year term. It's intended for investors who plan to complete a renovation over an extended period, often doing some of the work themselves (DIY). The loan structure allows for a more relaxed pace, removing the threat of a looming balloon payment.

Lender Requirements

While the timeline is more forgiving, the borrower requirements are still stringent, as the lender is taking on a longer-term risk.

- High FICO Scores: Lenders typically look for FICO scores of 720 or higher.

- Verified Liquidity: Lenders want to see that you have ample cash reserves to cover closing costs, interest payments during the renovation, and unforeseen project expenses.

- Past Experience: A track record of successfully completing similar value-add projects is often required. Lenders want to see you have a history of managing renovations and turning non-performing assets into cash-flowing rentals.

Unique Features

The Slow Flip loan stands out due to two key characteristics:

5-Year Term: The standard term is 5 years, providing significant flexibility compared to a traditional 12-month bridge loan. This term features a 5-4-3-2-1 prepayment penalty. For very low loan amounts, the term can sometimes be reduced to 3 years with management approval.

Potential for Over 100% Financing: While the program can lend greater than 100% of the purchase price on deeply discounted properties, this excess is strictly used to roll in closing costs, not renovation costs. To unlock financing over 100% of the purchase price, the borrower must meet strict hurdles: an 800+ FICO score, $50,000+ in verified liquidity, 5+ completed past projects, and the "As-Is" LTV must remain under 80%. Additionally, the absolute maximum loan amount for the entire Slow Flip program is strictly capped at $50,000.

Pros

Extended Timeline: The 5-year term eliminates the primary stressor of hard money lending—the need to finish and sell quickly. This is ideal for part-time or DIY investors.

Removes Balloon Payment Pressure: With a fully amortizing structure, the investor is steadily paying down principal and interest, avoiding a massive lump-sum payment at the end of the term.

Cons

Low Maximum Loan Amount: These loans are typically capped at a much lower amount than hard money loans, often around $50,000. This restricts their use to projects with a low purchase price and minimal renovation budget.

Prepayment Penalty: To compensate for the long-term nature of the loan, lenders often include a prepayment penalty structure (e.g., a 5/4/3/2/1 structure, where the penalty is 5% of the loan balance if paid off in year one, 4% in year two, and so on). This can eat into profits if the investor decides to sell early.

Best For

Slow Flip loans are perfect for DIY investors tackling light cosmetic flips on lower-priced homes, part-time investors who need a long runway to complete work on weekends, or for projects in markets where a longer holding period might be advantageous.

Deep Dive 4: The Stabilized Bridge Loan

A Stabilized Bridge loan is a short-term financing tool for acquiring properties that are already in good, lease-ready condition and require minimal to no renovation. It serves as a "bridge" to either a quick resale or long-term financing.

What It Is

This is a short-term, often interest-only, loan used to purchase a property quickly. Unlike a fix and flip loan, there is no construction holdback because the property is not expected to undergo significant repairs. The loan is secured by the "as-is" value of the property.

Lender Requirements

The focus of underwriting is almost entirely on the property's current condition and its ability to generate income.

Property Condition: The property must be in near lease-ready condition, typically rated C4 or better on a property condition scale. This means all major systems are functional, and the property is habitable. A Fannie Mae guide to property condition ratings provides a good external reference for these standards.

DSCR Underwriting: For rental properties, the loan is often underwritten using the Debt Service Coverage Ratio (DSCR). The property's expected rental income must be sufficient to cover the mortgage payment, taxes, insurance, and association fees (PITIA). A DSCR of 1.00x or higher is typically required. Furthermore, some programs allow the DSCR to fall as low as 0.75x if the borrower has a stronger credit profile and accepts lower maximum leverage.

Clear Exit Strategy: The borrower must have a clear plan to pay off the bridge loan within its 12 month term, whether through a sale (wholetailing) or a refinance into a long-term rental loan. Extended terms of 18 to 24 months are exclusively reserved for complex projects like ground-up construction or major structural additions.

Funding Structure

Leverage is not based purely on the "as-is" appraised value in all scenarios. For a new purchase, lenders calculate your maximum loan amount using the lesser of the purchase price or the "as-is" appraised value. If you are refinancing a property you have owned for less than 6 to 12 months (depending on the specific program), lenders calculate leverage using the lesser of your total Cost Basis or the "as-is" appraised value.

The "as-is" appraised value alone is generally only used on refinances for properties seasoned longer than 6 to 12 months. A lender might offer up to 75-80% Loan-to-Value (LTV). Any light cosmetic updates or repairs must be paid for entirely out-of-pocket by the borrower, as there is no renovation escrow.

Pros

Very Fast Closings: Because there is no rehab budget to underwrite or construction plan to approve, these loans can close extremely quickly, often in 10-21 days. This is a major advantage when competing against cash offers or buying at auction.

Less Paperwork: The application process is streamlined, requiring less documentation than a full fix and flip loan.

Ideal for Competitive Bids: The speed and simplicity make it a powerful tool for winning deals in a hot market.

Cons

All Renovation Costs Are Out-of-Pocket: Even for a "rent-ready" property, there are often minor costs for paint, cleaning, or small repairs. The borrower must have the cash on hand to cover 100% of these expenses.

Not for Value-Add Projects: This loan is unsuitable for properties that require significant work to reach their full market value.

Best For

Stabilized Bridge loans are ideal for several scenarios:

Acquiring Turnkey Rentals: An investor can use a bridge loan to quickly secure a rental property and then refinance into a permanent 30-year DSCR loan once a lease is in place.

Auction Properties: Many real estate auctions require a buyer to close within a very short timeframe, which a bridge loan can accommodate.

Wholetailing: An investor can use a bridge loan to purchase a property, do a quick clean-up, and then immediately list it on the MLS to sell to another buyer for a small profit, without doing a full renovation.

Deep Dive 5: The HELOAN (Standalone Second Mortgage)

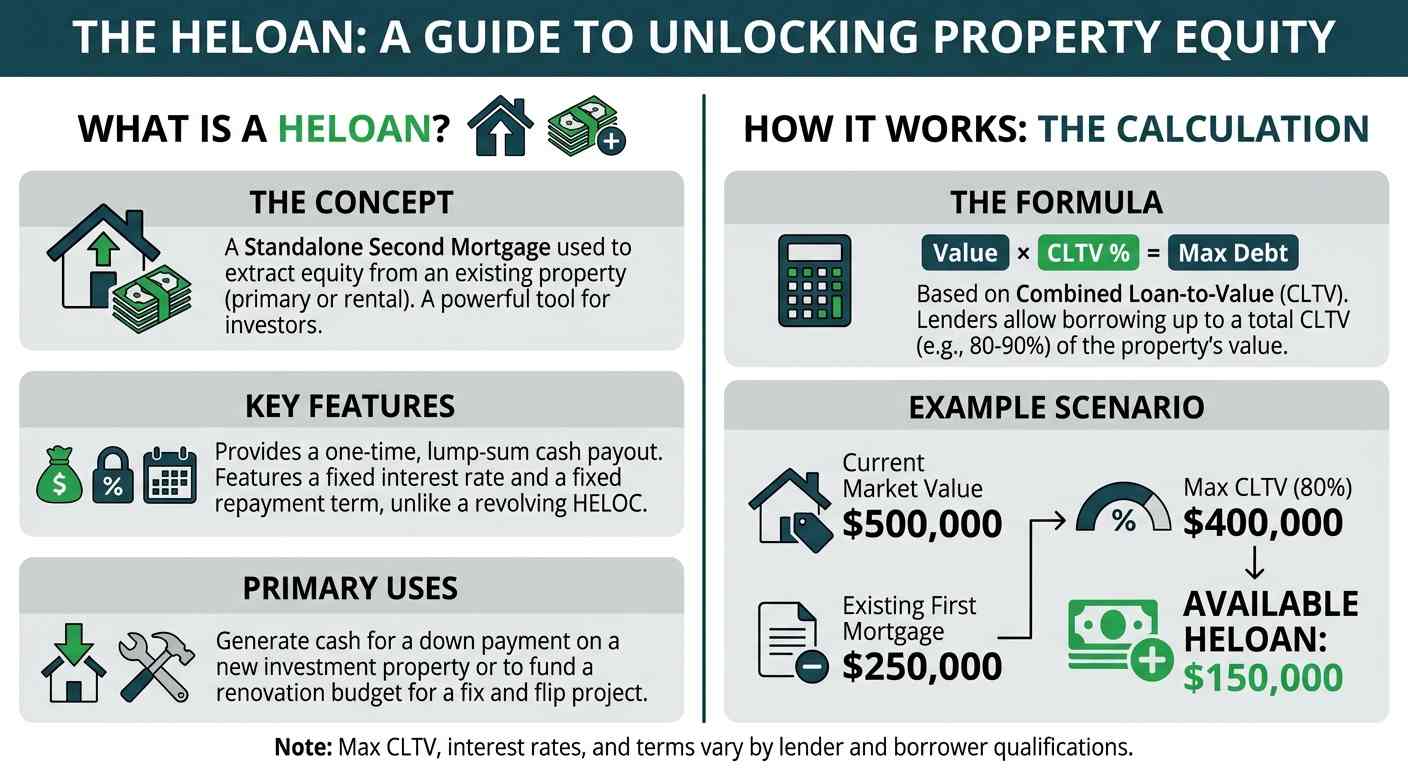

A Home Equity Loan, or HELOAN, is not a direct flip loan itself, but rather a powerful tool for funding one. It's a closed-end second mortgage that allows an investor to extract equity from an existing property (either a primary residence or another rental) to generate cash for a down payment or renovation budget on a new project.

What It Is

A HELOAN is a loan taken out against the equity in a property you already own. It's called a "second mortgage" because it sits in a subordinate lien position behind your primary (or "first") mortgage. Unlike a Home Equity Line of Credit (HELOC), which is a revolving line of credit, a HELOAN provides a lump-sum cash payout at closing and has a fixed interest rate and a fixed repayment term (typically 10-30 years).

How It Works

The core principle is tapping into the value you've built in an existing asset.

Example:

- Current Market Value of Your Rental Property: $500,000

- Existing First Mortgage Balance: $250,000

- Your Equity: $250,000

A lender might allow you to borrow up to a total Combined Loan-to-Value (CLTV) of 80-85%. But if you've built a strong portfolio and have excellent credit, you might qualify for up to 90%.

- 80% of $500,000 = $400,000 (Maximum total debt allowed)

- $400,000 (Max Debt) - $250,000 (Existing Mortgage) = $150,000

In this scenario, you could take out a HELOAN for up to $150,000 in cash. You could then use this cash as the 20% down payment and reserve requirement for a new $500,000 fix and flip project.

Qualification Methods

HELOANs on investment properties can be qualified in several ways:

Bank Statement (Alternative Income): Designed for self-employed investors, this method qualifies income based on 12 months of personal or business bank statements, or a 1-year Profit and Loss (P&L) statement.

DSCR-Based: Exclusively for investment properties, lenders evaluate the asset's cash flow rather than your personal income. The long-term gross rental income must generate a minimum 1.00x DSCR to cover the combined payments (PITIA) for both the existing first mortgage and the new second mortgage. Note that short-term rental income is strictly prohibited for DSCR qualification on second mortgages.

Lender Requirements

- Credit Score: A FICO score of 680 or higher is generally required.

- Debt-to-Income Ratio (DTI): Most lenders want to see a DTI of 43% or lower, including all your property-related debts.

- Property Type and Condition: Your investment property needs to be in good shape and meet lender guidelines.

- Equity Position: Plan on having at least 15-20% equity in the property.

- Rental Income History: Lenders like to see a solid track record of stable rental income.

- Cash Reserves: Be prepared to show you have enough cash on hand to cover 6-12 months of mortgage payments.

Pros

- Fast Access to Cash: HELOANs can close relatively quickly, providing a lump sum of cash that can be deployed for new investment opportunities.

- No Reserves Required for the Loan Itself: Since you are receiving cash, this cash can then be used to meet the reserve requirements for a separate fix and flip loan.

- Protects Low-Interest First Mortgages: This is a major benefit in a rising interest rate environment. Instead of doing a cash-out refinance of a first mortgage that has a 3% interest rate, an investor can leave that loan untouched and simply add a second mortgage, preserving their low-cost debt.

Cons

Adds a Lien to a Stabilized Asset: You are increasing the debt and risk on a performing asset in your portfolio to fund a speculative new project.

Adds Another Monthly Payment: This increases the overall debt service for your portfolio.

Best For

A HELOAN is best for established investors who have built up significant equity in their primary residence or rental portfolio and want to access that capital to scale their business. It's a strategic way to source the down payment, closing costs, or renovation budget for a new flip project without having to sell an existing asset or disturb a low-interest-rate first mortgage.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Key Metrics and Terminology for Flip Loans

Navigating the world of flip loans requires understanding a specific set of terms and metrics. These are the numbers and concepts that lenders use to evaluate the risk and potential of your project.

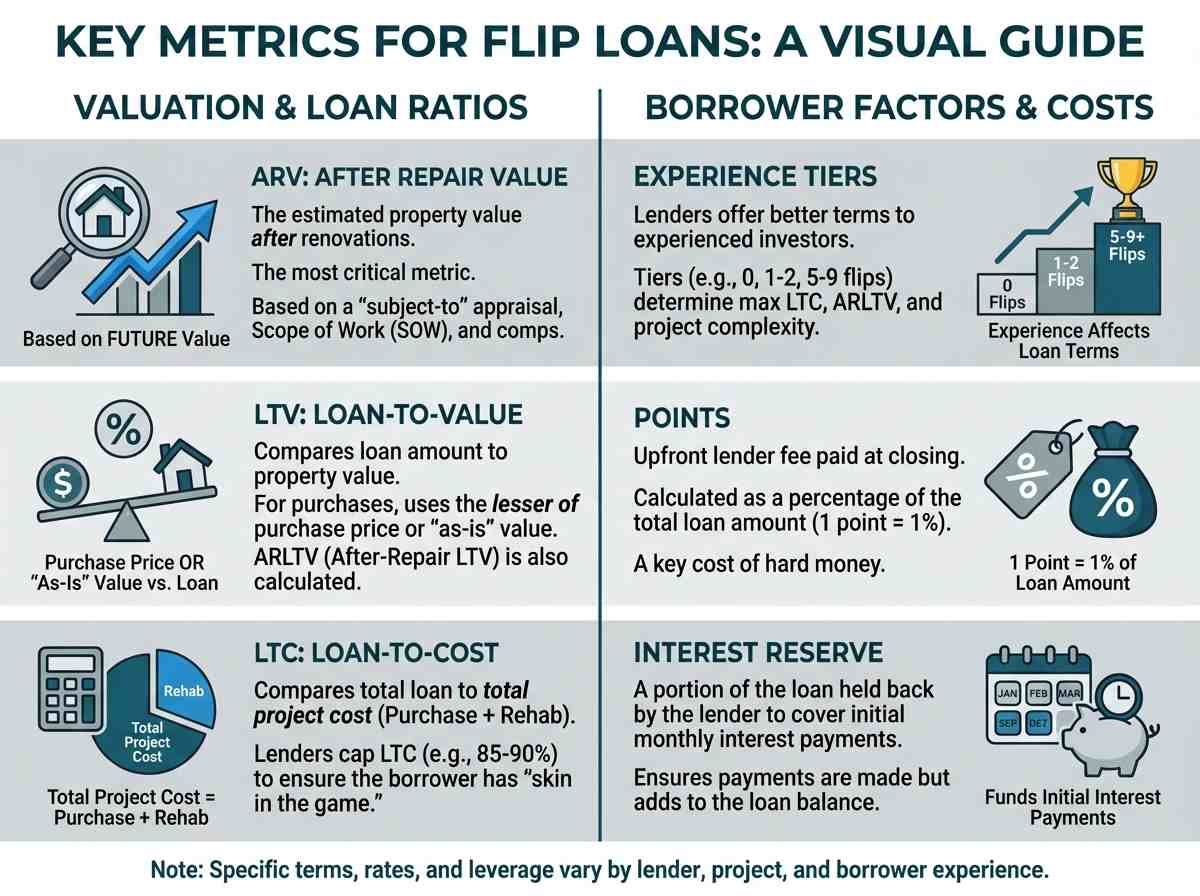

ARV: After Repair Value

ARV is the estimated value of a property after all planned renovations are completed. This is the single most important metric for a fix and flip loan. An independent appraiser determines the ARV by conducting a "subject-to" appraisal, where they analyze the property, your detailed Scope of Work (SOW), and recent sales of comparable, fully-renovated properties (known as "comps") in the area. The entire loan amount is based on the lender's confidence in the ARV.

LTV, LTC, and LTFC: Understanding the Ratios

These three acronyms are often used interchangeably, but they measure different things.

LTV (Loan-to-Value): This compares the loan amount to the value of the property. For a purchase, lenders do not simply use the purchase price; they strictly calculate LTV using the lesser of the purchase price or the "as-is" appraised value. For a refinance on a property owned for less than 6 to 12 months, LTV is based on the lesser of your total Cost Basis (purchase price plus documented improvements) or the current appraised value.

*LTC (Loan-to-Cost):* This compares the total loan amount to your total project cost (Purchase Price + Renovation Costs + Closing Costs). Lenders cap their total loan at a specific LTC—typically 85% to 90% for experienced investors—ensuring the borrower retains "skin in the game".

LTFC (Loan-to-Total-Cost): This is synonymous with LTC but is specifically used in Ground-Up Construction, where the "cost basis" includes the land acquisition, hard construction costs (labor and materials), and soft costs (architectural plans, permits, fees).

Example:

Purchase Price: $200,000

Rehab: $50,000

Total Cost: $250,000

ARV (After-Repair Value): $350,000

Total Loan Amount: $220,000 (comprised of $170,000 upfront for acquisition and a $50,000 construction holdback)

The LTV: Lenders calculate two separate LTV metrics: an Initial LTV of 85% ($170,000 upfront advance / $200,000 purchase price) and an ARLTV (After-Repair Loan-to-Value) of 62.8% ($220,000 total loan / $350,000 ARV).

The LTC: The LTC is 88% ($220,000 total loan / $250,000 total cost). This is the key metric the lender watches to limit their exposure relative to the project's actual cost.

Experience Tiers

Lenders mitigate risk by offering better terms to more experienced investors. A typical tier structure might look like this:

Tier 1 (0 Properties): Designed for inexperienced investors. The maximum renovation budget is capped at $100,000 (subject to a maximum of 25% of the purchase price). You are restricted to "light" renovations and can qualify for up to 80% Loan-to-Cost (LTC) and 70% After-Repair Value (ARLTV).

Tier 2 (1-2 Properties): The maximum renovation budget increases to 2x your highest verified past budget (up to a $500,000 cap). You can qualify for up to 85% LTC and 75% ARLTV.

Tier 3 (3-4 Properties): Allows for higher leverage up to 85% LTC and 75% ARLTV. At this tier, borrowers also gain more flexibility for heavier renovations or entering new markets.

Tier 4 (5-9 Properties): Unlocks the highest initial leverage, allowing you to borrow up to 90% LTC and 75% ARLTV.

Tier 5 (10+ Properties): Reserved for the most experienced investors. Allows up to 90% LTC and 75% ARLTV while permitting the most complex projects, including extensive renovations (exceeding 100% of the purchase price), additions, conversions, and ADUs.

DSCR: Debt Service Coverage Ratio

DSCR is primarily used for qualifying income-producing properties, like those financed with a Stabilized Bridge or a HELOAN on a rental. It measures the property's ability to pay its own bills.

Formula: Gross Monthly Rent / Monthly PITIA (Principal, Interest, Taxes, Insurance, Association Dues)

A DSCR of 1.0 means the income exactly covers the expenses. Lenders require a DSCR above 1.0, typically 1.1 to 1.25, to ensure the property has a positive cash flow buffer.

Points and Interest Reserves

These are key costs associated with hard money loans.

- Points: An upfront fee paid to the lender at closing, calculated as a percentage of the total loan amount. 1 point = 1% of the loan. A $300,000 loan with 2 points would have a $6,000 fee.

- Interest Reserve: Instead of making monthly interest payments out-of-pocket, some lenders will hold back a portion of the loan funds to cover the first several (e.g., 3-6) months of payments. This ensures the lender gets paid even if the project faces early delays, but it also means the borrower is paying interest on the interest being held.

How to Choose the Right Flip Loan for Your Project

Selecting the correct financing is as critical as choosing the right property. Using the wrong loan product can erode profits, create unnecessary stress, and even jeopardize the project. Here’s a framework for making the right choice.

Matching Loan Type to Renovation Scope

The nature and extent of your renovation is the first and most important factor.

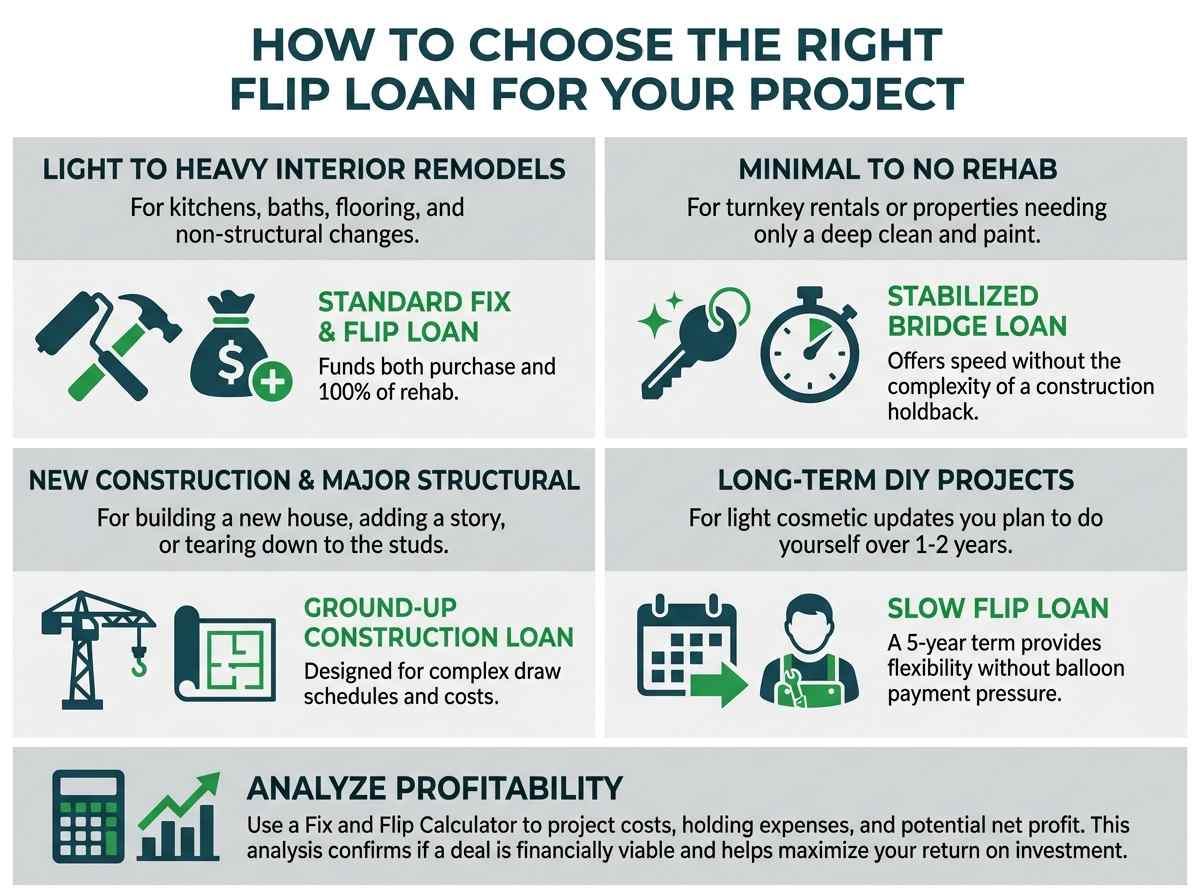

Light Cosmetic Updates to Heavy Interior Remodels: (e.g., kitchens, baths, flooring, paint, non-structural changes).

- Your Best Bet: Standard Fix & Flip Loan. It's designed specifically for this, funding both purchase and 100% of the rehab.

Minimal to No Rehab: (e.g., buying a turnkey rental or a property needing only a deep clean and paint).

- Your Best Bet: Stabilized Bridge Loan. It offers the speed you need to acquire the property without the complexity of a construction holdback you don't need.

New Construction or Major Structural Changes: (e.g., building a new house, adding a second story, tearing down to the studs).

- Your Best Bet: Ground-Up Construction Loan. This is the only product designed to handle the complexities, draw schedules, and cost structure of a new build.

Small, DIY Project Over a Long Period: (e.g., a light cosmetic update you plan to do yourself over 1-2 years).

- Your Best Bet: Slow Flip Loan. The 5-year term provides the flexibility you need without the pressure of a 12-month balloon payment.

Using a Fix and Flip Calculator to Analyze Profitability

Before you commit to a property, you must run the numbers. A comprehensive fix and flip calculator is an indispensable tool. It allows you to input your purchase price, estimated rehab costs, and financing terms (interest rate, points) to project your total costs, holding expenses, and potential net profit. This analysis will confirm if a deal is financially viable and help you compare different loan offers to see which one maximizes your return on investment.

The Application and Underwriting Process From Start to Finish

Modern lenders like OfferMarket have streamlined the loan application process, leveraging technology to make it faster and more transparent. Here is a typical step-by-step journey from inquiry to closing.

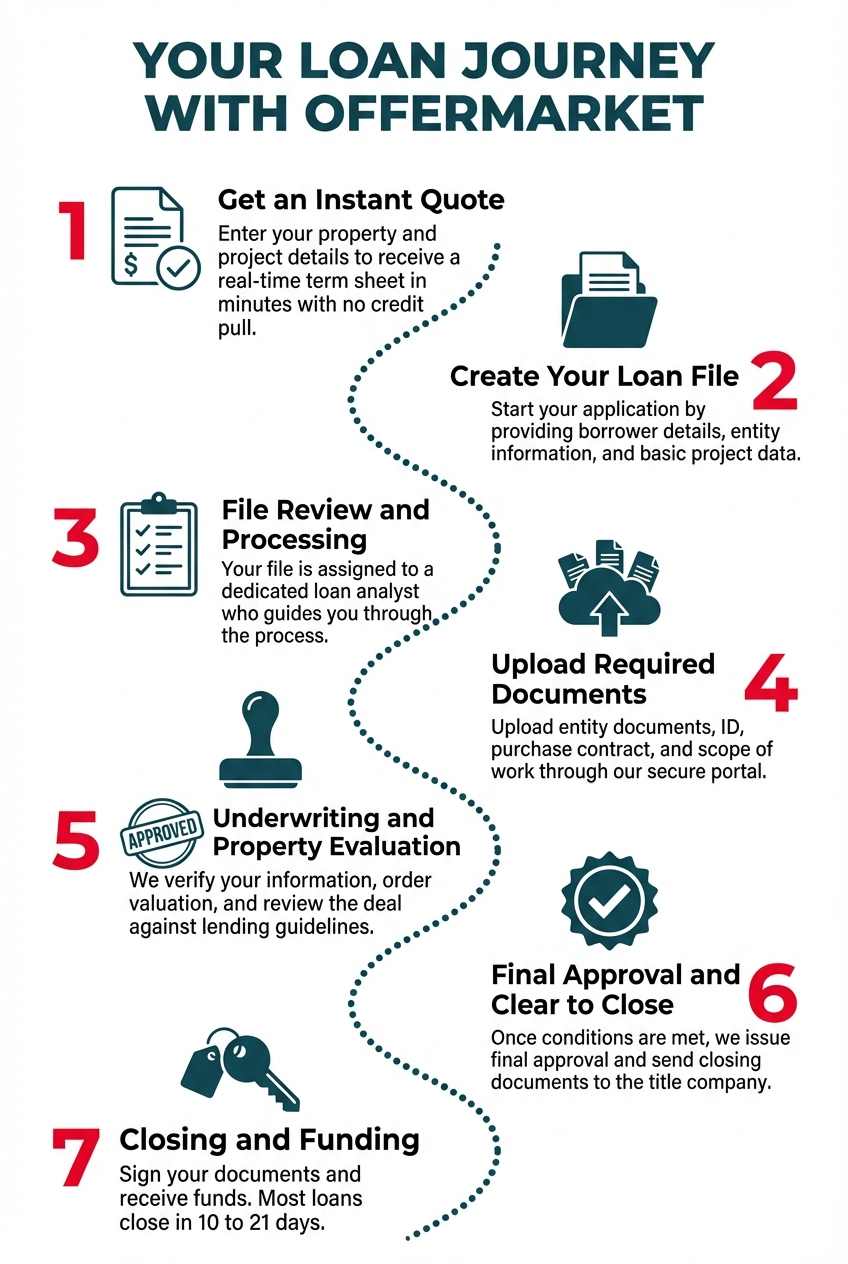

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Closing and Funding

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

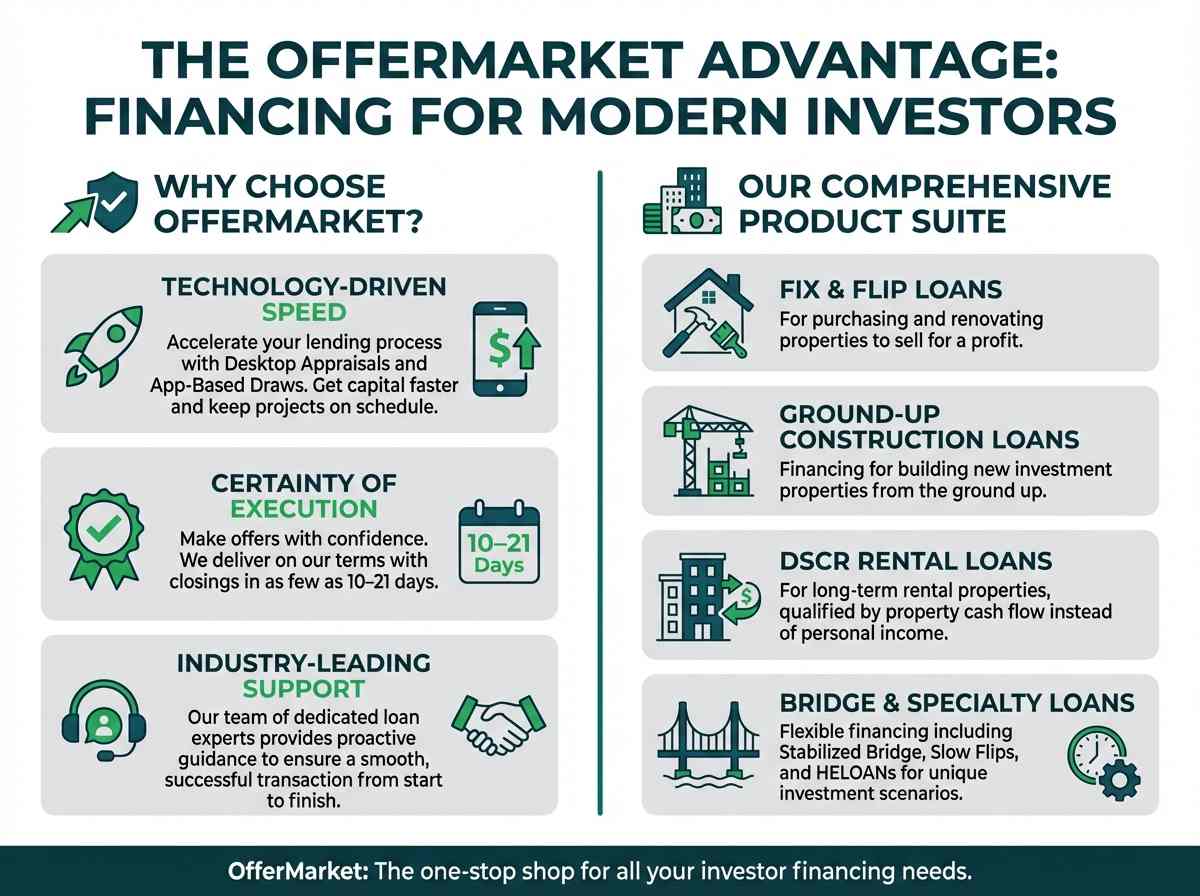

The OfferMarket Advantage: Financing for Modern Investors

In a market that demands speed, efficiency, and reliability, choosing the right lending partner is paramount. OfferMarket is built from the ground up to serve the needs of modern real estate investors, combining a comprehensive product suite with cutting-edge technology and unparalleled support.

A Comprehensive Product Suite

Why juggle multiple lenders for different projects? OfferMarket provides a one-stop shop for all your investor financing needs. We offer the full spectrum of products discussed in this guide:

- Standard Fix & Flip Loans

- Ground-Up Construction Loans

- Slow Flip Loans

- Stabilized Bridge Loans

- DSCR Rental Loans

- HELOANs

This comprehensive suite allows you to build a long-term relationship with a single lending partner who understands your business and can support your growth, from your first flip to a complex new construction project.

Technology-Driven Speed

Our proprietary technology platform is designed to eliminate friction and accelerate the lending process.

Desktop Appraisals: For many projects, we can use advanced valuation models and data analytics to perform a desktop appraisal, saving you the time and expense of a traditional field appraisal.

App-Based Draws: Requesting your renovation funds is as simple as using an app on your phone. Our streamlined draw process means you get your capital faster, keeping your project on schedule and your contractors paid on time.

Certainty of Execution

In real estate investing, a lender's promise needs to be bankable. Our streamlined process and experienced team provide certainty of execution, allowing you to make offers with confidence. We consistently deliver on our terms, with closings in as few as 10–21 days.

Industry-Leading Support

From your first inquiry to your final loan payoff, our team of dedicated loan experts is here to support you. We provide guidance, answer your questions, and work proactively to ensure a smooth and successful transaction, allowing you to focus on what you do best: finding and executing great deals.

Get Your Instant Fix and Flip Loan Quote

The first step to financing your next successful flip is knowing your numbers. An instant quote empowers you to analyze deals quickly and make strong, confident offers.

See Your Specific Rates, Leverage, and Terms in Minutes

Stop guessing what your financing will cost. By entering a few key details about your project into our free tool, you can receive a transparent, detailed term sheet in minutes. This quote will show you the specific interest rate, points, leverage (LTV/LTC), and total loan amount you qualify for based on your property and experience level.

Make Faster, More Confident Offers

With a reliable quote from OfferMarket in hand, you can walk into a negotiation knowing exactly what you can afford. This allows you to act decisively in a competitive market, structure your offers intelligently, and demonstrate to sellers that you are a serious, well-capitalized buyer.

The Next Steps

Receiving your quote is just the beginning. It's a no-obligation way to see how OfferMarket can help you fund your next project. If you like the terms, our platform makes it easy to move forward with your application and connect with one of our loan advisors who can guide you the rest of the way.

Ready to see your terms? Get your instant fix and flip loan quote today!

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull