DSCR Loan South Carolina

OfferMarket Loans

Check your rate

60 seconds · no credit pull

DSCR Loan South Carolina Example Deal

DSCR Loan South Carolina calculation

DSCR Loan Requirements

DSCR Loan South Carolina Common Questions

Last updated: November 21, 2024

Looking for a DSCR loan for your South Carolina investment property? Welcome and thank you for stopping by! We encourage you to stick around, get an instant quote, and take advantage of our market-leading insights and tools designed to help you build wealth through real estate:

We fund a lot of DSCR loans in South Carolina and we've built relationships with wonderful clients in the state. We're particularly active in Beaufort, Charleston, North Charleston and Summerville, and we can fund your next purchase or refi anywhere as long as it's not rural.

We love working with rental property investors in the Palmetto State, and we sure hope to have the opportunity to work with you.

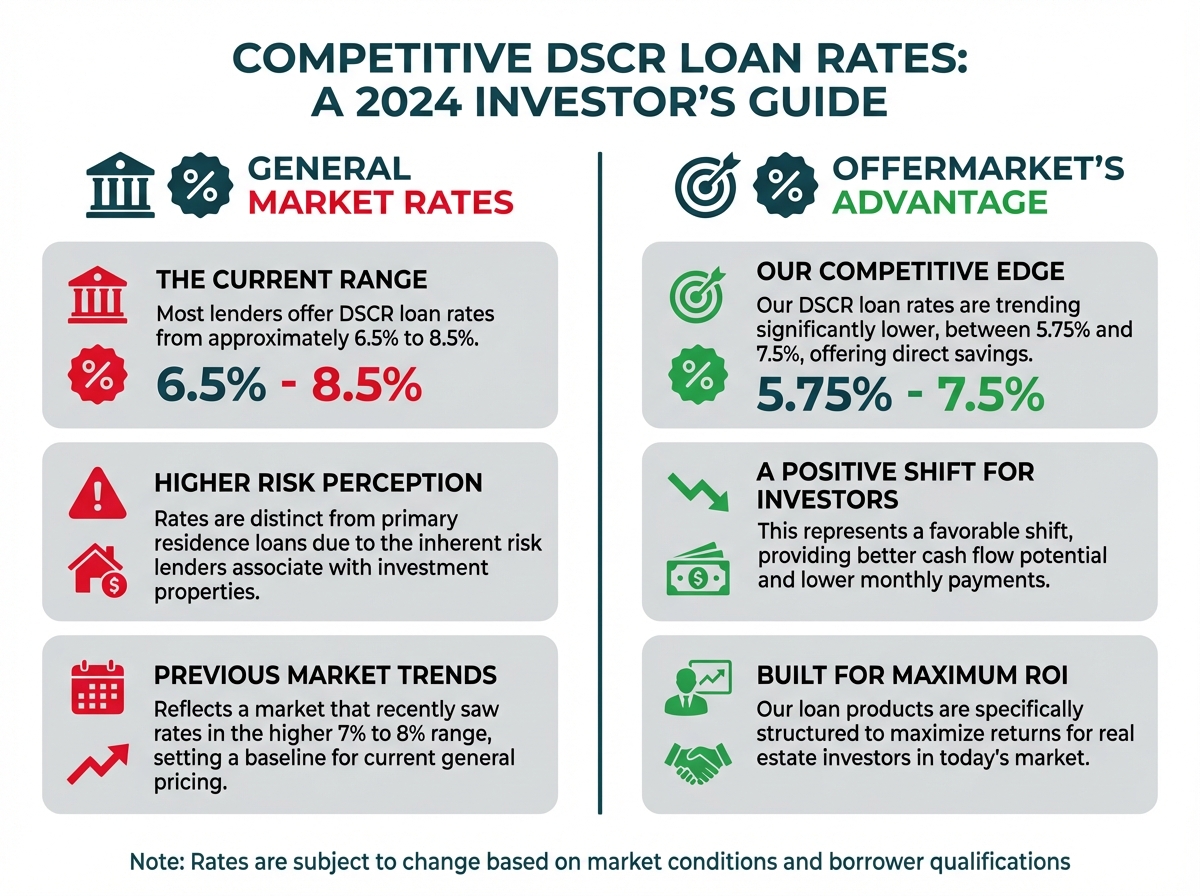

South Carolina DSCR loan interest rates

Source: DSCR Loan Interest Rates Index

Here are frequently asked questions from our South Carolina clients:

What is a DSCR loan?

DSCR stands for debt service coverage ratio, and it is a simple metric to determine if an investment property generates more or less income than the monthly mortgage payment. A DSCR loan is simply a mortgage specifically for a rental property where the maximum loan amount is determined by the DSCR of the property. As your loan amount increases, your monthly mortgage payment increases, and your DSCR decreases. 1.1 is currently the minimum DSCR to qualify for a given loan amount. Use our DSCR Calculator to help you run your numbers, understand DSCR, max loan amount, monthly cash flow, cash to close and cash out for your next deal.

Can I cash out refi with no seasoning?

Yes! OfferMarket is one of the only private lenders with a cash out refi no seasoning program. Instead of waiting for 6 months to refinance your rental property, you can refi as soon as your renovation is completed and the property is leased. Why should you have to wait to pull cash out of a property and reinvest it into growing your business?

Do I qualify for a DSCR loan?

Borrowing Entity: Because our loans are business purpose, we only fund loans to business entities. If title is currently held in your personal name, you would need to transfer it into an LLC or corporation before we can fund.

Credit Score: the minimum credit score is 660. If you have more than one borrower in your borrowing entity, the ownership of each member will determine which credit score we use. If you do not want to use one of the member's credit score, they will need to own less than 50% of the borrowing entity. We use a tri merge credit report, which is a hard credit pull that collects your credit report from Experian, Equifax and Transunion, and we take the middle score. So, if your tri merge report is 721, 697, 738, then we will use 721 to determine your loan terms.

Background Check: if you have a clean background report, then you're all set. If you have one or more bankruptcy, felony or misdemeanor on your background report, then we will need you to provide a letter of explanation to determine if you are eligible for funding.

Non-Rural: if your property is designated as rural or the appraiser indicates that your property is rural on their appraisal report, then we may not be able to fund your loan. DSCR loans are meant for properties in highly liquid markets where you can quickly sell the property for market price if need be.

Minimum As Is Value: currently, we require your property to appraise for at least $100,000, and we require your loan amount to be at least $75,000.

What is the maximum DSCR loan amount?

Purchase: we can fund up to 80% of the purchase price as long as the property does not appraise for below the purchase price, and the appraisal market rent supports that loan amount.

Rate and term refinance: if you have an existing loan on the property, we can refinance up to 80% LTV as long as you do not receive more than 2% of the loan amount as a cash out at settlement.

Cash out refinance: we can fund up to 75% LTV.

If you're looking for more higher leverage than the above terms (i.e. higher LTV, lower down payment), we urge you to use caution because legitimate DSCR lenders will rarely offer more leverage than what is offered by OfferMarket.

How long does it take to get a DSCR loan?

Our target for every DSCR loan is to fund in 20 to 25 days. Here are the most common reasons why funding can be delayed:

Appraisal delay: 3rd party appraisers provide a report due date but may miss that deadline. The appraiser's report may need to be revised and the appraiser may be delayed in providing their revised report.

Title work delay: title companies and closing attorneys may take more time to complete the title work, especially if they are waiting on a lien certificate from a the county or title is clouded.

Borrower delay: in your OfferMarket Loan File, we provide you with a checklist of items that we need in order for your file to be ready for final review and loan approval. Our processing team will follow up to remind you when there are items that we need you to take care of, and if you do not take action on these items in a timely manner, then your loan will be delayed.

Best cities to buy rental properties in South Carolina

| Rank | City | Population | Population Growth Rate | Median Household Income | Median Home Price | Market Rent |

|---|---|---|---|---|---|---|

| 1 | Charleston | 147,928 | 1.3% | $75,274 | $425,000 | $1,700 |

| 2 | Columbia | 137,276 | 0.6% | $61,791 | $350,000 | $1,400 |

| 3 | North Charleston | 114,542 | 1.9% | $60,422 | $325,000 | $1,300 |

| 4 | Mount Pleasant | 98,900 | 2.1% | $73,167 | $400,000 | $1,600 |

| 5 | Rock Hill | 71,548 | 0.9% | $57,350 | $275,000 | $1,200 |

| 6 | Greenville | 67,086 | 1.2% | $74,975 | $375,000 | $1,500 |

| 7 | Summerville | 48,331 | 1.6% | $67,900 | $300,000 | $1,250 |

| 8 | Goose Creek | 44,464 | 1.8% | $65,500 | $250,000 | $1,100 |

| 9 | Spartanburg | 39,619 | 1.1% | $55,150 | $225,000 | $1,000 |

How do I get started with a DSCR Loan?

⚡ get your instant DSCR loan quote and pre-approval -- takes less than a minute, be sure to submit so we can confirm the best possible terms (our instant quote is conservative and we commonly can actually provide a lower rate and higher loan amount)

📄 upload your purchase agreement or lease into your OfferMarket Loan File

🧑💻 schedule your relationship manager call from your Loan File -- speak with your dedicated relationship manager who will address your questions and concerns and make sure we are a good fit to be your lender.

OfferMarket Loans

Check your rate

60 seconds · no credit pull