DSCR Calculator

Last updated: June 16, 2025

Are you taking advantage of the most powerful and collaborative DSCR Calculator to analyze your rental property purchases and refinances? Our DSCR loan calculator will help you...

✅ calculate DSCR exactly how DSCR lenders do ✅ screen rental property investment opportunities ✅ understand how interest rate, rent, taxes, insurance and HOA fees affect DSCR ✅ confirm loan amount that your property qualifies for ✅ calculate net proceeds or cash to close ✅ access an instant DSCR loan quote with accurate offered interest rate and LTV ✅ save your calculation as you evaluate multiple deals ✅ share your calculation with colleagues

In this article we will cover multiple ways and approaches that can be used to calculate DSCR ratio to quantify the attractiveness of a transaction. We will start at learning about the calculation itself and then move on to different variations of the calculation or the inputs that could be used.

DSCR Formula

DSCR = Rent ÷ PITIA

Where:

Rent = the lower of the actual rent in the lease agreement or market rent opinion in the appraisal report

PITIA = Mortgage Payment = Principal + Interest + Taxes + Insurance + Association Dues

Interest Only DSCR Loan Calculation

DSCR loans can also be structured with an initial 5 or 10 year interest-only period as follows:

| Structure | 5 Yr IO | 10 Yr IO |

|---|---|---|

| Term | 30 Years | 30 Years |

| Amortization | Full, years 6 - 30 | Full, years 11 - 30 |

| Interest rate | Fixed | Fixed |

| Min DSCR | 1.0 | 1.0 |

DSCR = Rent ÷ ITIA

Where:

ITIA = Interest Only Mortgage Payment = Interest + Taxes + Insurance + Association Dues

DSCR Calculation

DSCR or Debt Service Coverage Ratio is a metric used by private lenders to assess the financial strength of a rental property and determine the maximum eligible loan amount or loan-to-value (LTV). When assessing the financial health and feasibility of a deal or investment, it's key to break down its capability to bring on sufficient cash flow to cover its debt liabilities. The Debt Service Coverage Ratio( DSCR) is a fundamental metric used by lenders, investors, and judges to assess the borrower's capacity to repay debt. In this blog post, we will dive into the concept of DSCR and provide a step-by-step companion on how to calculate it.

The Debt Service Coverage Ratio (DSCR) is a financial benchmark that measures the relationship between the cash flow available to service debt and the debt payments due within a specific period. It's normally expressed as a ratio, which indicates the number of times the cash flow covers the debt arrears.

Lenders frequently use DSCR as a crucial factor in determining the creditworthiness of a borrower, and investors count on it to estimate the risk associated with a deal. Below, you will learn how DSCR is calculated a few different ways that produce slightly different values. The standard DSCR calculation for 1-4 unit residential investment properties is Rent ÷ PITIA or Rent ÷ ITIA in the case of DSCR loans with an initial interest only period.

Interpreting DSCR

A DSCR of 1 means the property generates just enough operating income to "service the debt" on the property. That means a DSCR of 1 is breakeven, $0 free cash flow. A DSCR greater than 1 means the rental property generates more than enough income to service its debt. A DSCR less than 1 means the property does not generate enough income to service its debt and therefore the owners need to pay out of pocket every month to cover the shortfall.

| DSCR | Meaning |

|---|---|

| Less than 1 | Owner needs to pay out of pocket to cover monthly expenses |

| 1 | Owner breaks even, property covers its expenses exactly |

| Greater than 1 | Owner receives excess cash, property more than covers expenses |

DSCR Loan Calculation

In order to properly understand the concept of debt service coverage ratio, it's helpful to use an example:

Jenny is in contract to buy a rental property for $200,000. The property appraises for $200,000 with a $2,000 market rent opinion from the appraiser. Jenny's learns about a type of loan -- called a "DSCR loan" -- where the maximum loan amount is based on the cash flow of the property and she doesn't need to have a W2 or provide tax returns. The lender is able to provide up to 80% LTV ($160,000), as long as the debt service coverage ratio is at least 1.1 at 80% LTV. Jenny uses the calculator above to plug in the numbers and realizes that the property has a DSCR of 1.37 at 80% LTV, far more than the minimum required to qualify for 80% LTV.

Using the DSCR calculator not only helped Jenny understand what loan amount she qualified for, it gave her the confidence that she's buying a good deal, and it helped he understand the interplay between DSCR inputs including rent, taxes, insurance, and interest rates and how that affects cash to close and cash on cash return. If the market rent were $1,500, Jenny would only qualify for 70% LTV because DSCR would be too low at higher LTVs.

Here is an example of a DSCR loan funded by OfferMarket:

- Transaction type: cash out refinance

- Borrowing entity: LLC

- Guarantor credit score: 730

- Property type: single family (1 unit)

- As Is value: $158,000

- Loan amount: $118,500

- Interest rate: 6.87%

- Structure: 30 year term, full amortization, fixed rate

- Principal and Interest (monthly): $778.06

- Insurance (monthly): $117.54

- Taxes (monthly): $66.78

- HOA (monthly): $0.00

- PITIA: $962.39

- Rent: $1,400

- DSCR: 1.4547

For a cash out refinance (cash to borrower on the settlement statement is $2,000+), the maximum LTV is 75%. As you can see, from the actual example, the borrower is generating $437.61 in free cash flow ($1,400 - $962.39).

The minimum DSCR in our DSCR loan program is 1.0, so technically the borrower would have qualified for 75% LTV even if the subject property's monthly rent was $962.39. This being said, we strongly prefer a minimum DSCR of 1.1 (market rent of $1058.63) to ensure you have a buffer of free cash flow to be able to build up reserves to pay for inevitable items including maintenance, vacancy, insurance premium increases and tax increases. Over time, as you increase your monthly rent, your DSCR should increase as long as it more than offsets any increases in your taxes and insurance.

DSCR Loan Calculator

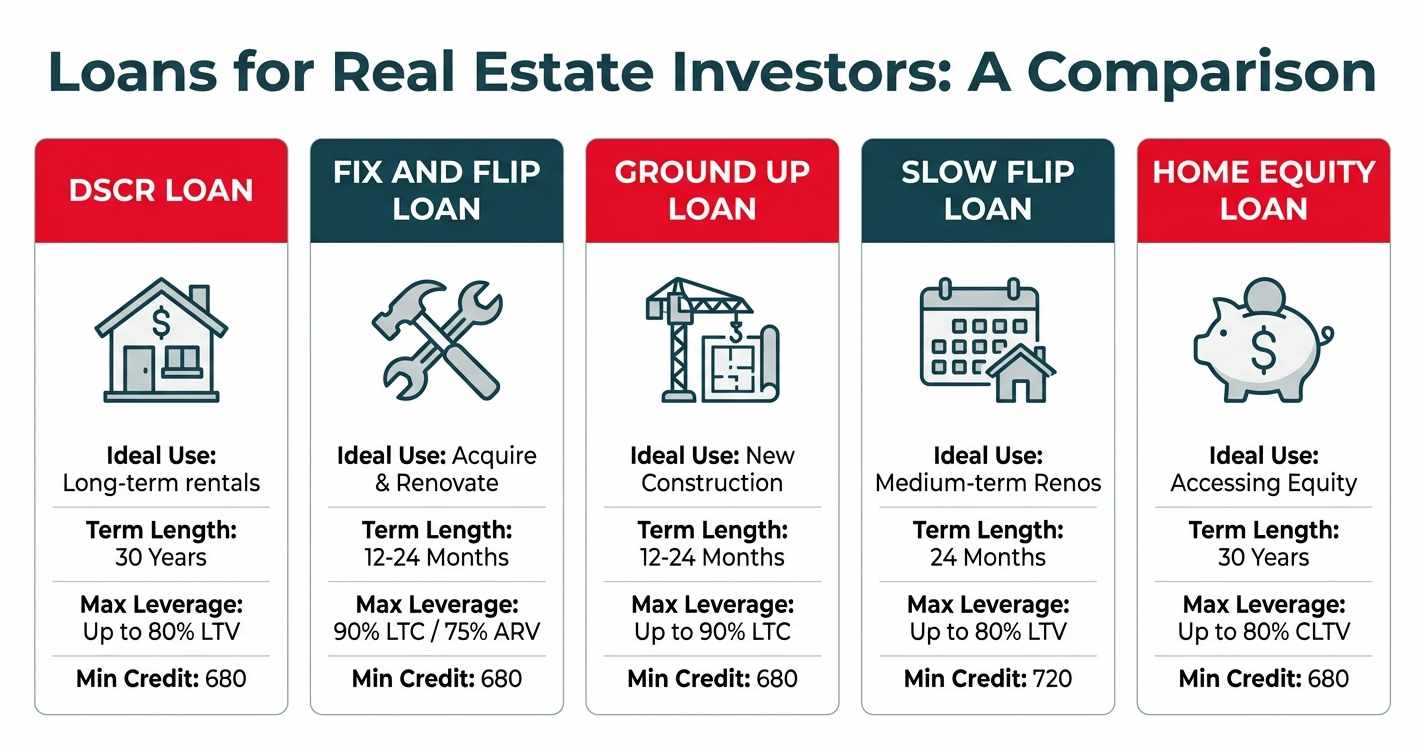

Lenders will have a minimum DSCR in their loan program guidelines, and if the DSCR is equal to or greater than that minimum, the property will qualify for DSCR loans are business purpose loans that use the rental property as collateral, and are most commonly 30 year fixed rate mortgages. DSCR loan programs -- also known as non-QM or non qualifying mortgages -- do not look at the borrowers income or tax returns.

DSCR loans are originated based on three core underwriting components:

- Deal economics (DSCR) -- does the rental property generate cash flow?

- Borrower credit score -- does the borrower have a history of paying their debts?

- Borrower experience -- does the borrower have other investment properties and know what they're doing?

Borrower experience is less important because the borrower can always hire a property management company. Deal economics and credit score are deal breakers. Most rental property investors don't realize just how important their credit score, so read on on how credit score affects your loan amount and interest rate for DSCR loans. Hint: 720 is the magic number!

See DSCR Loan Interest Rate Index.

DSCR Calculation

Private lenders use two different formulas to calculate DSCR. It's important to understand each method in order to avoid max LTV surprises for your next DSCR loan.

Max LTV for DSCR Loans

Many private lenders have a maximum LTV of 75% for cash out refinance, and 80% for purchase scenario.

DSCR for Vacant Rental Property

It is important to be aware that many lenders will utilize 90% of the appraised rent amount if your property is vacant at settlement. This will reduce your DSCR and may reduce the maximum LTV and loan amount.

How to Calculate Debt Service Coverage Ratio (DSCR) for a Rental Property

Calculating DSCR for a rental property follow exactly the same steps as we outlined above. First you need to gather necessary data regarding the property as inputs to the calculation. Once you have the inputs and you need verify their accuracy by leveraging public data sources and finally calculate the DSCR itself. Below we will tackle this task step by step.

Input property-specific data

The data inputs for the calculation that need to be sourced from property data include:

- Rent

- Taxes

- Insurance

- Utilities

- HOA

- Property Management

- Maintenance

Once you have this data, if its for a new purchase, to look at comparable properties and see if your data is in the ballpark value of comparable properties. This will increase your confidence over the numbers that you are using since these are just estimates that you have research because you haven't actually received any rent or paid any bills for this property yet.

Once you gained confidence into your input data we can proceed to the calculation step. Why is it important to verify your inputs versus comparable properties? Well, its important because if your inputs to the DSCR calculation are inaccurate, the conclusion of the calculation will also be inaccurate. In statistics there is a saying 'garbage in, garbage out', meaning, calculation is just a tool that depends on what information you provide it with. If you build a house on bad foundation, you will eventually have a bad house, same logic tracks for DSCR calculations and the input data they are based on.

Complete the DSCR calculation

We recommend using our DSCR calculator (above) though you can use the simple formula: Rent ÷ PITIA

Understanding DSCR

Once you have calculated the DSCR for your rental property, it's important to understand its implications

DSCR Value

A DSCR value greater than 1 indicates that the rental property's cash flow is sufficient to cover its mortgage payments. The advanced the proportion, the more comfortably the property can handle its debt.

DSCR Threshold

Lenders and investors may have different criteria for an acceptable DSCR. Generally, a DSCR of1.2 or advanced is considered favorable, as it provides a margin of safety. However, specific circumstances, such as the property's location or demand conditions, might need a advanced DSCR to mollify risks effectively.

Risk Assessment

A low DSCR, below 1, suggests that the rental property's cash flow may not be enough to cover its mortgage payments. This indicates advanced threat for lenders and investors, as it increases the liability of financial difficulties in repaying the debt.

As you can see, DSCR calculation for a rental property is almost identical to DSCR calculations for any other type of properties since inputs to the calculation remain the same.

How to Calculate Debt Service Coverage Ratio (DSCR) from Cash Flow Using a DSCR Calculator

While DSCR is typically calculated using Net Operating Income (NOI), it’s also possible to calculate it directly from cash flow. In this blog post, we will guide you through the process of calculating the Debt Service Coverage Ratio (DSCR) using cash flow as a starting point, with the help of a DSCR Calculator.

- Determine Cash Flow Available for Debt Service (Gross Rent) – Identify the cash flow available to service debt within a specific period. This includes all available cash that can be allocated towards debt payments. Cash flow can be derived from sources such as operating income, non-operating income, and any other relevant inflows. Using a DSCR Calculator can simplify this step and ensure you’re accurately calculating available cash.

- Determine Total Debt Service (PITIA) – Identify the total debt service, which includes all principal and interest payments due within the same period. This information can be obtained from loan documents or by contacting your lender. A DSCR Calculator can help you input this data and get an accurate debt service figure.

- Apply the DSCR Formula – Divide the cash flow available for debt service by the total debt service to calculate the Debt Service Coverage Ratio (DSCR). A DSCR Calculator will instantly provide the DSCR value once these inputs are made, making the process faster and more accurate. ice by the total debt service to calculate the Debt Service Coverage Ratio( DSCR).

How to Calculate Debt Service Coverage Ratio (DSCR) in Excel

Knowing DSCR calculation and be able to use it is the first step to using it for your analysis of deals. Financially savvy real estate investors and DSCR lenders, by virtue of needing to use this formula several times a day, have come up with easier ways to apply it to quickly gain insight into the characteristics of a deal. We are of course talking about implementing the DSCR calculation in Excel. Request access to our DSCR Loan Calculator Excel Formula Google Sheet

Let's explore the step-by-step process of calculating the Debt Service Coverage Ratio (DSCR) in Excel

Step 1: Determine DSCR loan interest rates

Here we track the prevailing market rate from the best DSCR lenders and compare it to OfferMarket's DSCR loan interest rate which is generally more competitive.

Step 2: Enter values for DCSCR loan calculation inputs

- Interest Rate -- refer to our DSCR Loan Interest Rate Index

- Value Basis -- If purchase transaction, use the lower of As Is value or Purchase Price. If refinance transaction, use the actual or estimated As Is value.

- Annual Taxes

- Annual Insurance

- Annual Flood Insurance

- Annual HOA

- Monthly Payment -- use the PMT function for PITIA or ITIA (for interest only period structure)

- DSCR -- If fully amortizing (no interest only period) use Rent ÷ PITIA, if interest only use Rent ÷ ITIA

Step 3: Analyze the outputs

Make necessary adjustments to ensure you arrive as close as possible to your target loan amount based on your target DSCR and minimum DSCR constraints.

How to Calculate Maximum Loan Amount Using Debt Service Coverage Ratio (DSCR)

If you know your DSCR as well as a ballpark interest rate your lender will charge you, you will be able to calculate the maximum DSCR loan you potentially qualify for. We say potentially because every lender is different and they might have internal rules that will limit loan amounts in certain situations depending on other factors that aren't captured in our calculation below. Given that, let's delve into the step- by- step process of calculating the maximum loan amount using the Debt Service Coverage Ratio (DSCR).

Step 1: Determine the rent that will be used

This is the lower of the actual lease or the market rent opinion in the appraisal report.

Step 2: Determine your desired DSCR and loan program minimum

At OfferMarket the minimum DSCR is 1.0 though most rental property investors target 1.1 or 1.2 to ensure a safe amount of free cash flow to build reserves to pay for maintenance and property management expenses.

Step 3: Determine your target loan amount

If this is a purchase, the maximum is 80% LTV where the value basis ("V") is the lower of the purchase price or As Is value in the appraisal report. This implies a minimum down payment of 20%. If this is a refinance, the maximum LTV is 80% where the value basis ("V") is the As Is value in the appraisal report.

Step 4: Determine your PITIA or ITIA based on your target loan amount

We recommend using our DSCR calculator (above) to determine what your monthly payment will be. Monthly payment is Principal + Interest + Taxes + Insurance + Association dues or Interest + Taxes + Insurance + Association dues for interest-only DSCR loans. Use public record to confirm taxes and get a landlord insurance quote to confirm your insurance premium.

###**Step 5: Confirm the loan amount you qualify for based on DSCR As with the previous step, we recommend using our DSCR calculator (above) to determine if your DSCR is at or above the minimum or your target DSCR at the given loan amount. Keep in mind that your maximum LTV depends on credit score! Learn how credit score affects LTV for DSCR loans.

Once we have the value in step 4, we need to interpreting it for the benefit of our analysis. Generally, the maximum DSCR loan amount has implication on three distinct but intra-related factors, loan affordability, risk and lender requirements.

Loan Affordability -- The maximum loan amount represents the estimated borrowing capacity based on the project's cash flow and the desired DSCR threshold. It provides an indication of the loan size that can be supported while maintaining a satisfactory DSCR.

Risk Assessment -- It's advisable to consider a lower loan amount to maintain a comfortable DSCR, If the calculated maximum loan amount exceeds the scheme's financing needs. This mitigates the threat of financial strain in case of unexpected changes in the scheme's cash flow.

Lender Requirements -- Keep in mind that lenders may have specific criteria regarding DSCR and loan- to- value ratios. They may impose additional requirements based on the scheme's characteristics, such as its location, market conditions, and industry risks.

Calculating the maximum loan amount using the Debt Service Coverage Ratio( DSCR) is a critical step in assessing the borrowing capacity of a deal. By considering the deal's cash flow, desired DSCR threshold, and estimated annual interest rate, you can determine the maximum loan amount that can be reasonably supported. Remember to factor in threat considerations and lender requirements when determining the optimal loan amount for your specific deal.

Grow and optimize your rental portfolio with OfferMarket

OfferMarket is a real estate investing platform. Our mission is to help you build wealth through real estate. We focus on 1-4 unit residential investment properties. OfferMarket membership is free, and comes with the following benefits:

🏠 Off market properties -- access off market deal flow posted on our marketplace by distressed sellers, tired landlords and wholesalers. 💰 Private lending -- access discounted loan terms for DSCR loans, Fix and Flip loans and low balance loans. ☂️ Insurance rate shopping -- shop 40+ carriers, access coverage that meets lender guidelines, save hundreds on your premiums.

If you are not already an OfferMarket member, we hope you will accept our invitation to join us!

OfferMarket Loans

Check your rate

60 seconds · no credit pull