*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

What is a Tri Merge Credit Report?

Last updated: November 26, 2025

Tri Merge credit report is used by mortgage lenders to collect FICO credit reports from all three consumer credit bureaus: Equifax, Transunion, Experian. Trimerge credit reports can either be hard inquiries ("hard pull") which can negatively impact your credit score or soft inquiries ("soft pull") which does not negatively impact your credit score. At OfferMarket, we are dedicated to protecting your credit score and that is why we only utilize soft trimerge credit reports.

If you are a real estate investor shopping for a DSCR loan or fix and flip loan, understanding the tri merge credit report can help you get a lower interest rate and higher loan amount.

Credit Report Mid Score

Private lenders that use tri merge reports will take the "mid score" when determining your credit score for underwriting and loan pricing purposes. This means the highest and lowest score will be ignored, and the middle or second highest score will be used.

If the report returns only 2 scores (i.e. one of your credit bureau accounts is frozen), then the lender will take the lowest score.

DSCR Loan Credit Score

DSCR loan programs have varying minimum credit score requirements. OfferMarket's DSCR loan program has a minimum credit score of 660, while many other private lenders have a minimum credit score of 680.

It's important to understand that, as your credit score approaches the minimum, your DSCR loan interest rate will be progressively higher, and your LTV will be progressively lower.

DSCR loan programs are hyper sensitive to credit score for the following reasons:

Securitization guidelines: there is robust and growing demand for DSCR loan mortgage backed securities, and the sponsors who aggregate DSCR loans and have them rated by credit rating agencies want the highest possible credit score, a conservative amount of leverage (LTV), and an attractive interest rate. A "compensating factor" for low credit score is to require a lower LTV and a higher interest rate.

Credit risk: credit score is highly correlated with a borrower's ability to consistently and successfully make mortgage payments, if your credit score is on the lower end of the acceptable range, then the lender will require a higher interest rate in order to be compensated for accepting higher credit risk in their loan portfolio.

How does credit score affect LTV?

While credit score is not the only factor in determining LTV (DSCR is also highly important), it is known to be a sticking point where private lenders give few if any exceptions to their guidelines:

| Credit Score | LTV (purchase) | LTV (cash out refi) |

|---|---|---|

| 720+ | 80% | 75% |

| 700 - 719 | 80% | 75% |

| 680 - 699 | 70% | 65% |

| 660 - 679 | 65% | 65% |

How does credit score affect interest rate?

As a rule of thumb, you can count on higher credit scores to qualify for lower interest rates. Conversely, you can count on lower credit scores to qualify for higher interest rates:

| Credit Score | Interest Rate |

|---|---|

| 760+ | +0.00% |

| 740 - 759 | +0.05% |

| 720 - 739 | +0.1% |

| 700 - 719 | +0.15% |

| 680 - 699 | +0.25% |

| 660 - 679 | +0.50% |

DSCR Loan Minimum Credit Score

As you can see from the tables above, a middle credit score of 720 or higher will generally qualify you for the highest LTV and close to the best interest rate.

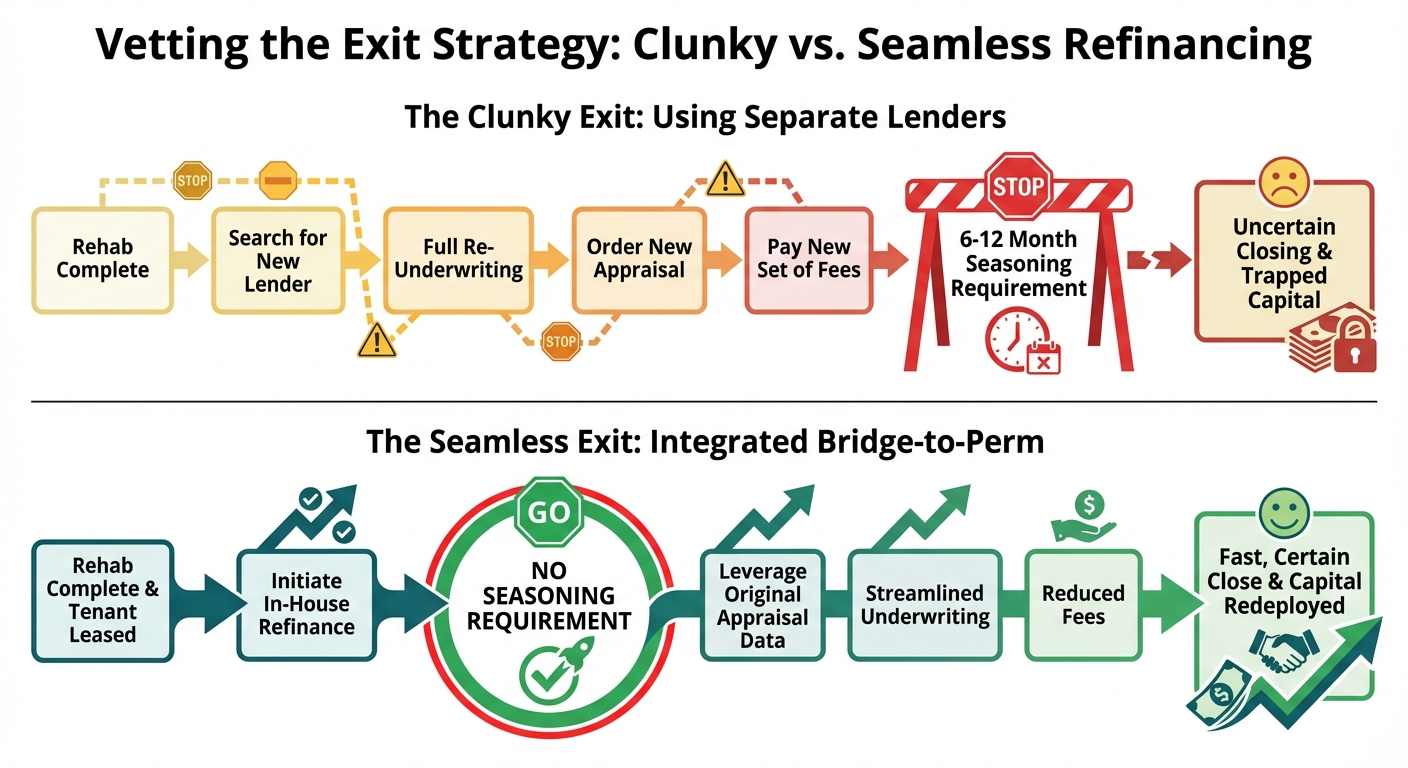

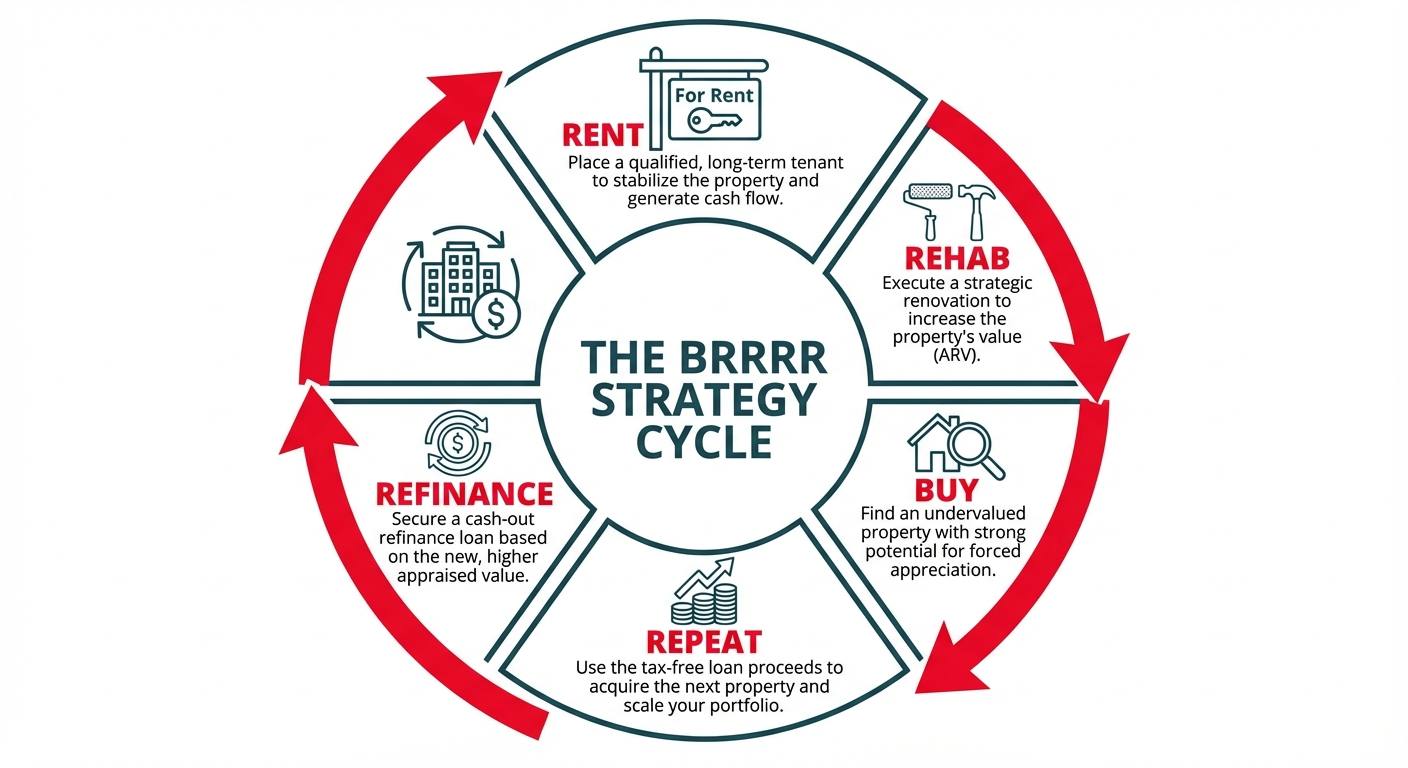

It is all too common to see BRRR investors get through their rehab using credit cards. High credit utilization results in a lower credit scores. So when it comes time for your cash out refi, your score may prevent you from qualifying for the highest LTV and lowest interest rate.

This common scenario leaves cash trapped in your deal, lowering your cash on cash return and increasing your financing costs due to higher interest rate.

In the worst case scenario, we see BRRR investors forced to either bring cash to closing in order to pay off their fix and flip loan, or forced to sell because their credit score is too low to qualify for a DSCR loan. While we specialize in deal structuring and can help you avoid these issues, as the saying goes "an ounce of prevention is worth a pound of cure", and it is absolutely imperative that rental property investors diligently protect their credit score.

For this reason, we continually remind our rental property investor clients that a 720 credit score is the magic number.

Fix and Flip Loan Minimum Credit Score

Fix and flip loan programs generally have a much lower minimum credit score. Some private lenders and hard money lenders will approve credit scores in the 580 - 620 range depending on experience, deal strength, and the reason for the low credit score.

When your credit score is under 620, lenders may require 6 to 12 months of interest reserves to be funded into escrow at settlement. Instead of making monthly interest payments, your payments will be disbursed from your interest reserve. Any unused funds in your interest reserve will be applied towards your payoff when the property is sold.

If your exit strategy is to refinance from our fix and flip loan into a DSCR loan, most DSCR loan programs will require a minimum credit score of 680.

Tri Merge Vendors

At OfferMarket Capital, we will use one of the following trimerge vendors for your credit report:

CIC Credit Tri Merge Report

- EQUIFAX/FICO CLASSIC V8

- TRANSUNION/FICO CLASSIC (04)

- EXPERIAN/FAIR, ISAAC (VER. 2)

Xactus (formerly Credit Plus) Tri Merge Report

- EQUIFAX/FICO CLASSIC V5

- TRANSUNION/FICO CLASSIC (04)

- EXPERIAN/FAIR, ISAAC (VER. 2)

Free Credit Report FICO 8

Your free credit report will likely use the FICO 8 scoring model which tends to have a lower sensitivity to one-time late payments and therefore a higher score compared to the other, older scoring models that are used in tri merge credit reports.

FICO 8

While FICO Score 8 or FICO CLASSIC V8 is the most commonly used credit report, it is actually the least commonly used scoring model for mortgage inquiries.

This unfortunate truth is the cause of a lot of frustration among borrowers who are surprised to find that their tri merge report mid score is significantly lower than the FICO 8 free credit report score they just checked before proceeding with the loan.

FICO CLASSIC V5

The FICO 5 scoring model is commonly used in tri merge reports.

FICO CLASSIC (04)

The FICO 4 scoring model is commonly used in tri merge reports.

FAIR, ISAAC (VER. 2)

The FICO 2 scoring model is commonly used in tri merge reports, and this version is commonly the lowest of the three scores.

How much does a Tri Merge Credit Report cost?

While most lenders do not charge for tri merge reports, it can cost anywhere from $20 to $40 for a trimerge report.

How does a lender run a tri merge report?

In order for a lender to run a tri merge credit report, they must first receive your express written consent. This is typically obtained through a simple one to two page "Credit Release Authorization" or "Borrower Signature Authorization" that you e-sign. Most credit release authorizations will also include authorization to run your background report.

Is a Tri Merge a hard credit pull?

Yes, a trimerge report is a hard inquiry across all three credit bureaus. For this reason it is important to avoid excessive or unecessary tri merge reports because one of the factors in the FICO scoring model is the "number of inquiries". A high number of inquiries is looked at as a credit risk by FICO and the credit bureaus and will result in a reduction to your credit score.

How do I access my tri merge credit report?

The Fair Credit Reporting Act (FCRA) and Equal Credit Opportunity Act (ECOA) are important laws that provide consumer protections concerning access to your credit report. Technically, your lender is not required to provide you with the tri merge report that you authorized (and possibly paid for).

At OfferMarket, we believe it's important that you have total transparency into your credit report and we make the tri merge report available immediately in your Loan File. Your OfferMarket relationship manager is always happy to review your tri merge report with you, so you understand the items on your report that you can resolve in order to increase your credit score and access better loan terms.

How many days is a tri merge report valid?

It depends on lender guidelines. Many lenders will not fund a loan if the tri merge report is older than 90 days. Other lenders will allow the report to be up to 120 days old. Few lenders will allow the report to be up to 365 days old.

Can I transfer my tri merge report?

Many lenders require the tri merge report to be run through their vendor account and will therefore not accept a tri merge report from another lender. One reason for this common policy is because of forged reports, though tri merge vendors have a secure verification URL that the lender can use to confirm that the PDF report has not been tampered with.

At OfferMarket Capital, we want to avoid unnecessary inquiries on your credit. We will allow you to transfer your tri merge report whenever possible as long as:

- the report is from an approved tri merge vendor

- the report is not older than 90 days as of the closing date

- our institutional investor that will be purchasing the loan does not have a strict policy against tri merge report transfer

Join OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders and flippers. We focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull