*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Cash Out Refi No Seasoning

Last update: July 24, 2025

Most DSCR lenders require a period of 6 months before allowing a Cash Out Refi No Seasoning of a newly acquired rental property. This policy, called “seasoning,” is at odds with your best interests as a rental property investor because you want to be able to recycle your cash into your next deal. How many more deals can you do if you don’t need to wait months for your Cash Out Refi No Seasoning?

Stop wasting time and money waiting for your lender's seasoning requirements to cash out refi into a DSCR loan.

| OfferMarket | Other Lenders | |

|---|---|---|

| Seasoning requirement | None or 90 days | 6 months |

| Origination fee | 1% | 2% |

| Time to close | 15 - 25 days | 30 - 60 days |

| Interest Rate | Get Instant Quote | Current DSCR loan Rates |

Cash Out Refi No Seasoning Explained

A cash out refi no seasoning is when you implement a new loan on a property that you already own, and you receive cash proceeds at closing. Regardless of whether the property is owned free and clear (no existing debt), or has an existing loan in place, your DSCR lender may require you to wait until you’ve owned the property for 6 months in order to complete your refinance. However, with a Cash Out Refi No Seasoning, you can avoid this waiting period and

Seasoning is frustrating for real estate investors because it slows you down by trapping cash in your property that you could otherwise be using to buy more properties. During periods of market volatility, seasoning can be even more stressful because DSCR loan interest rates may rise and home values may decline while you're waiting for "title to season" so you can complete your cash out refi.

No Seasoning DSCR Loan Program

| No Seasoning Terms | Guidelines |

|---|---|

| Interest rate | Get Instant Quote |

| Minimum loan amount | $55,000 |

| Minimum As Is value | $100,000 |

| Unit count | 1 to 4 |

| Lease | Required |

| Security deposit | Receipt required |

| 1st month's rent | Receipt required |

| Property condition | C4 or better |

| Rental ownership/management experience | Not required |

| Minimum credit score | 680 |

| Max LTV | 75% |

| Max LTC | 100% (less than 90 days seasoning), 140% (90 to 179 days seasoning) |

| Minimum verified rehab | 20% of purchase price (less than 90 days seasoning), n/a (90+ days seasoning) |

| Origination fee | 1 to 2 points (depends on loan amount) |

| Lender fee | $1,495 to $1,995 |

| Appraisal | AMC market price |

| Time to close | 20 - 25 days |

Cash out refi LTV

| Credit Score (Trimerge) | Max LTV |

|---|---|

| 680 - 699 | 70% |

| 700+ | 75% |

Why do lenders have seasoning requirements?

DSCR lenders require seasoning for a handful of reasons:

- want to see a track record of paying your current loan

- want to discourage a type of fraud where borrowers cash out a property with a serious hidden defect that renders the property to be worth a lot less than its appraised value

- want to see that work has been done to improve the value of the property

Lenders with Cash Out Refi No Seasoning requirements

Lenders with no seasoning requirements are few and far between. Rest assured, we have you covered. Working closely with experienced rental property investors, specifically those that use the BRRR method, we've come to the conclusion that a no seasoning option needs to exist. Take advantage of our DSCR loan program to cash out refi up to 75% LTV with no seasoning!

In order to qualify for a Cash Out Refi No Seasoning, you need to have a minimum credit score of 680, and we will want to see before and after photos as proof that you have added value to the property. Technically, you don’t need to have a lease in place, though it is preferred. With a Cash Out Refi No Seasoning, you can access the cash value of your property without the typical waiting period required by other lenders.

Cash our refi with existing debt

Having existing debt (i.e. a hard money fix and flip loan) is an advantage for no and low seasoning cash out refi because it allows you higher loan-to-cost ("LTC"). If you have a lien on your property for a loan you used to purchase and rehab the property, here's what you can expect:

| Option 1 | Option 2 | |

|---|---|---|

| Existing debt | Yes | Yes |

| Seasoning | None | 90 days |

| Max LTV | 75% | 75% |

| No seasoning throttle | Max LTC: 100% | Max LTC: 140% |

Cash out refi no debt

If you're refinancing a rental property owned free and clear (with no existing debt, bought with cash), no and low seasoning guidelines are as follows:

| Option 1 | Option 2 | |

|---|---|---|

| Existing debt | $0 | $0 |

| Seasoning | None | None |

| Max LTV | 75% | 80% |

| No seasoning throttle | Max LTC: 100% | Max cash to borrower on settlement statement: 100% of cost basis (purchase price + closing costs + verified rehab) |

Buying rental property with cash offers a significant advantage, particularly in a competitive market. Sellers often prefer cash buyers because they can close quickly without the risk of financing falling through. However, once the property is purchased, the next step for most rental property investors is to complete a Cash Out Refi No Seasoning to access the equity in the property.

When working with lenders that impose seasoning requirements, investors are forced to wait a specific period—often six months—before refinancing. This waiting period can limit the investor's ability to move quickly on new opportunities. With a Cash Out Refi No Seasoning, however, you can avoid this delay and refinance your property as soon as you are ready, ensuring that your timeline is not dictated by the lender's seasoning requirements. This approach allows you to access your funds and reinvest in new properties without unnecessary delays.

Buy in cash, rehab the property, tenant the property, and get your cash out at the best possible terms as quickly as possible so you can have your cash for your next deal. If the BRRRR method works to plan, you'll have more cash out than what you invested.

With our no seasoning DSCR loan guidelines, we can fund your cash out refi as soon as you're ready.

Fix and Flip to DSCR with Cash Out Refi No Seasoning

If you currently have a fix and flip loan and you're ready to refi into a DSCR loan, you may have thought that seasoning was required. While many clients who use our fix and flip loan take 6–12 months to refi into a DSCR loan, we also work with an elite group of clients who move fast. These clients are able to complete their rehabs significantly faster than the average BRRR investor, and they want to work with a lender who can offer a Cash Out Refi No Seasoning, allowing them to access their equity without unnecessary delays. With a Cash Out Refi No Seasoning, you can refinance quickly and continue scaling your investments without being held back by traditional seasoning requirements.

Your cash out refinance doesn't need to be delayed by frustrating seasoning requirements. BRRR investors should not be penalized for efficiently rehabbing and renting properties. If you buy a property today, complete your rehab by week 2 and leased by week 3, that's quite impressive and we want to be your lender.

| Option 1 | Option 2 | |

|---|---|---|

| Existing debt | Yes | Yes |

| Seasoning requirement | None | 90 days |

| Max LTV | 75% | 75% |

| Max LTC | 100% | 140% |

| Verified rehab | required | required |

| Verified rehab amount | 20%+ of original purchase price | no limit |

How long does a cash out refinance take?

A cash out refinance typically takes 30 - 45 days, unless you're working with OfferMarket. We streamline your cash out refi by making it easy to complete processing items in your Loan File, and making sure your appraisal and title order are completed in days instead of weeks. We've closed no seasoning cash out refis in under 3 weeks and our target for every cash out refi is to close in 15 - 30 days.

No Seasoning Refinance for Faster Access to Cash

Most DSCR lenders require 6 months. OfferMarket does not have a seasoning requirement as long as the property has been improved through verifiable rehab.

No seasoning refinance

If you're a BRRR investor, a no seasoning refinance is the way to go. Accelerate the turnover of your capital, recycle it into your next deal faster, build your portfolio faster. Let's take a look at a scenario where you have Rental Investor A and Rental Investor B, both incredibly consistent BRRR method investors.

Rental Investor A works with a lender that offers a No Seasoning Refinance requirement. Rental Investor B works with a lender that requires 6 months of seasoning. Both investors cash out 100% of their invested capital, utilize 100% of their capital on each deal, and have their next deal ready to close as soon as they cash out. Like clockwork, Rental Investor A completes and starts new projects every 3 months thanks to the No Seasoning Refinance option. In contrast, Rental Investor B completes and starts projects every 6 months, constrained by the seasoning requirement.

Starting from 0 properties, after 5 years, Rental Investor A will have a portfolio of 20 properties, while Rental Investor B will have a portfolio of 10 properties. Seasoning is costing Rental Investor B millions of dollars of equity and a lot of rental income!

| No Seasoning | 6 Month Seasoning | |

|---|---|---|

| Year 1 | 4 properties | 2 properties |

| Year 2 | 8 properties | 4 properties |

| Year 3 | 12 properties | 6 properties |

| Year 4 | 16 properties | 8 properties |

| Year 5 | 20 properties | 10 properties |

DSCR loan cash out refi

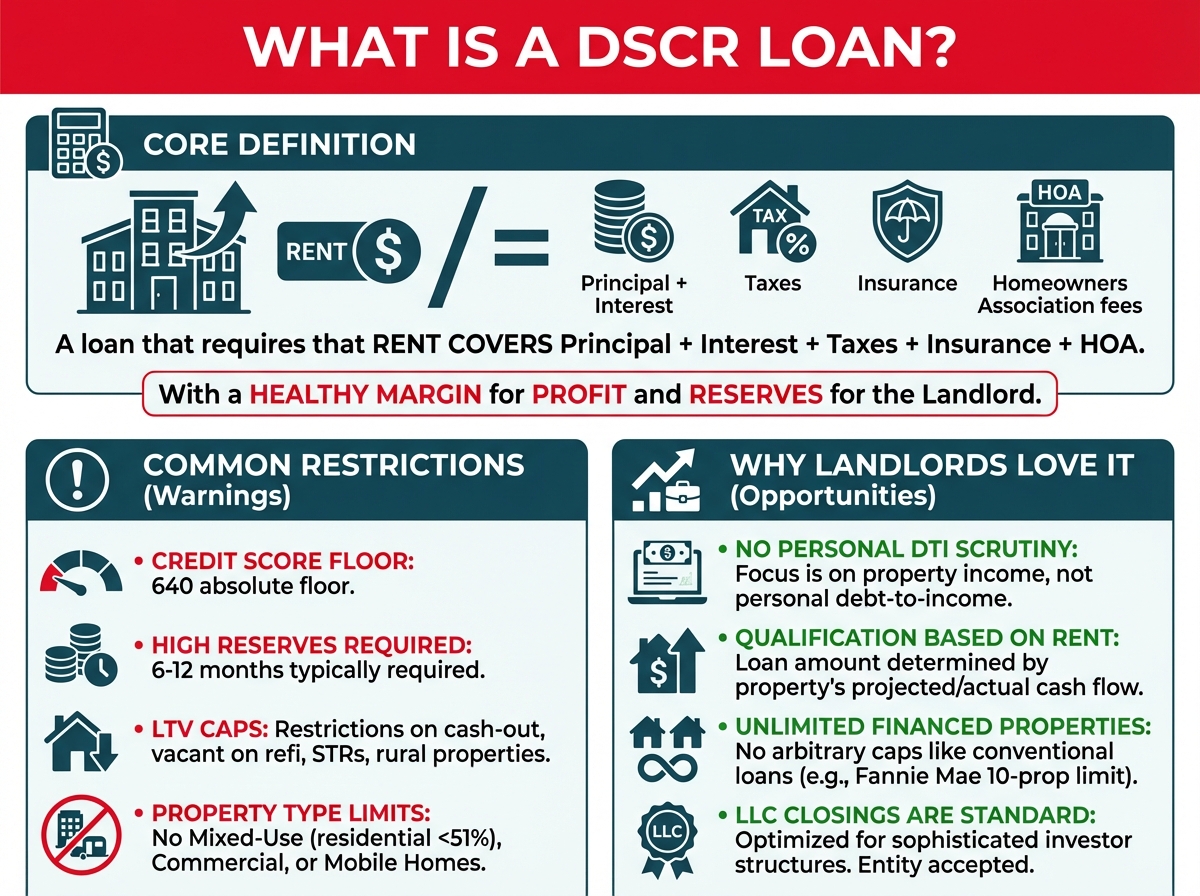

Most rental property investors use 30 year fixed rate DSCR loans because they are based on the cash flow of the rental property and therefore do not require extensive underwriting, income verification or tax returns. Compared to conventional loans and bank loans, DSCR loans are significantly faster, with interest rates and fees that are generally competitive. We make it easy to get a DSCR loan, and we would love to be your lender. Submit your loan today and get your cash out refi done!

Grow and optimize your rental property portfolio with OfferMarket

OfferMarket is a rental property investing platform. Membership is entirely free and includes access to the following:

🏠 Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Community & insights

Our mission is to help you build wealth through real estate. If you are not already a member, we hope you will accept our invitation to join us!

OfferMarket Loans

Check your rate

60 seconds · no credit pull