*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loan Florida Requirements: Key Steps for Real Estate Investors

Last Update: June 24, 2025

This article is about DSCR loan requirements specific to rental properties in Florida. For an interactive DSCR loan review for your Florida property, we recommend visiting our DSCR Loan Florida landing page.

Navigating the world of real estate investment can be a daunting task, especially when it comes to securing the right financing. In Florida, DSCR loans have emerged as a popular option for investors looking to leverage their properties' income potential. These loans, based on the Debt Service Coverage Ratio (DSCR), offer a unique approach by focusing on the property's cash flow rather than the borrower's personal income.

DSCR stands for Debt Service Coverage Ratio, a key metric used by lenders to evaluate whether a rental property generates enough income to cover its debt obligations. It is calculated as:

DSCR = Gross Rental Income ÷ PITIA (Principal, Interest, Taxes, Insurance, and any HOA fees).

A DSCR of 1.0 means the income equals debt payments; higher values indicate positive cash flow.

Understanding the requirements for a DSCR loan in Florida is crucial for investors aiming to maximize their portfolio's growth. Lenders typically evaluate the property's ability to generate sufficient income to cover its debt obligations. Lenders generally require a minimum DSCR of 1.0 to 1.2, depending on borrower credit. For example, a borrower with a credit score under 720 might need a DSCR of 1.2 to qualify.

By exploring the specific criteria and benefits of DSCR loans in Florida, investors can make informed decisions that align with their financial goals and real estate strategies.

Understanding DSCR Loans

DSCR loans evaluate property cash flow to determine loan eligibility. Lenders assess the Debt Service Coverage Ratio (DSCR) to ensure the rental income can cover debt obligations. A DSCR above 1.0 indicates that income exceeds debt payments, strengthening the borrower's position. This approach differs from traditional loans focusing on personal income. Investors benefit from flexibility, as DSCR loans offer purchasing and refinancing opportunities without stringent income documentation.

DSCR loans do not require personal income verification—no W-2s, pay stubs, or tax returns. This makes them highly accessible for investors with self-employment income, complex financials, or multiple properties.

Commercial and residential properties in Florida often leverage DSCR loans, accommodating varied investment strategies. Borrowers should understand specific lender criteria, as requirements may vary. Each lender sets a minimum DSCR; typically, this ranges from 1.1 to 1.5. Loan terms and interest rates reflect the calculated DSCR, affecting overall financing costs.

Prepayment flexibility often accompanies DSCR loans, appealing to investors seeking long-term strategies. Borrowers may avoid penalties associated with early repayment, enhancing financial planning. Understanding these aspects allows investors to maximize property profitability while meeting debt obligations.

Key Requirements for DSCR Loans in Florida

| Underwriting item | Required |

|---|---|

| Loan application | Yes |

| Credit report (soft) | Yes |

| Background report | Yes |

| Bank statements (2 most recent) | Yes |

| Ownership verification or purchase contract | Yes |

| Appraisal | Yes |

| Appraisal risk review | Yes |

| Landlord insurance | Yes |

| Wind mitigation inspection | Recommended |

| 4-point inspection | Recommended |

| W-2 | No |

| Tax return | No |

DSCR loans in Florida offer unique financing options, emphasizing property cash flow over personal income. Understanding key requirements is essential for potential borrowers.

Loan Structure Options

Interest-Only Payments: Available for 5 or 10 years, ideal for investors maximizing cash flow.

Amortized Payments: Full amortization over a 30-year term is also available.

Balloon Payment: Some interest-only loans have a balloon payment at maturity, which is a lump sum due at the end of the loan term.

Credit Score Expectations

Most DSCR loans require a minimum credit score of 660, though some products or scenarios may allow lower scores with stricter terms. A higher score (680+) often qualifies for better rates and higher leverage.

Loan-to-Value Ratio

The loan-to-value (LTV) ratio for DSCR loans typically ranges from 70% to 80%. Borrowers must ensure adequate down payment or equity, as this ratio directly impacts loan approval and conditions.

Debt Service Coverage Ratio

A minimum DSCR of 1.1 to 1.5 is common among lenders in Florida. This ratio measures property income against debt payments, crucial for loan qualification.

Proof of Income and Financial Records

Although personal income documentation is less rigid than traditional loans, lenders assess financial stability. Borrowers might need to present bank statements, rental agreements, and other relevant financial records to support loan approval.

Application Process for DSCR Loans

Securing a DSCR loan in Florida involves multiple steps to evaluate the borrower's potential and the property's financial viability. Ensuring thorough preparation can streamline the process.

Pre-qualification Steps

Lenders conduct an initial assessment to gauge eligibility before proceeding with a full application. This often includes reviewing the property’s rental history and projected income to ensure it meets the minimum DSCR requirements, usually between 1.1 and 1.5. Borrowers should prepare a summary of financial goals and investment strategies, helping lenders understand their overall plans. A preliminary credit check may also occur, where a minimum score of around 620 is considered a positive indicator.

Documentation Needed

Applicants for a DSCR loan must provide comprehensive documentation to support their request. Essential documents include current bank statements, existing rental agreements, and a detailed report of the property's financial performance. Proof of property ownership and insurance coverage is also necessary. If refinancing, copies of the existing mortgage and payment history are required. Although personal income documentation is not the focus, displaying overall financial stability strengthens the application.

Benefits and Challenges of DSCR Loans in Florida

DSCR loans offer unique advantages and challenges for real estate investors in Florida. Investors can benefit from these loans' specific features while weighing potential drawbacks.

Potential Drawbacks and Considerations

Interest Rates and Fees:

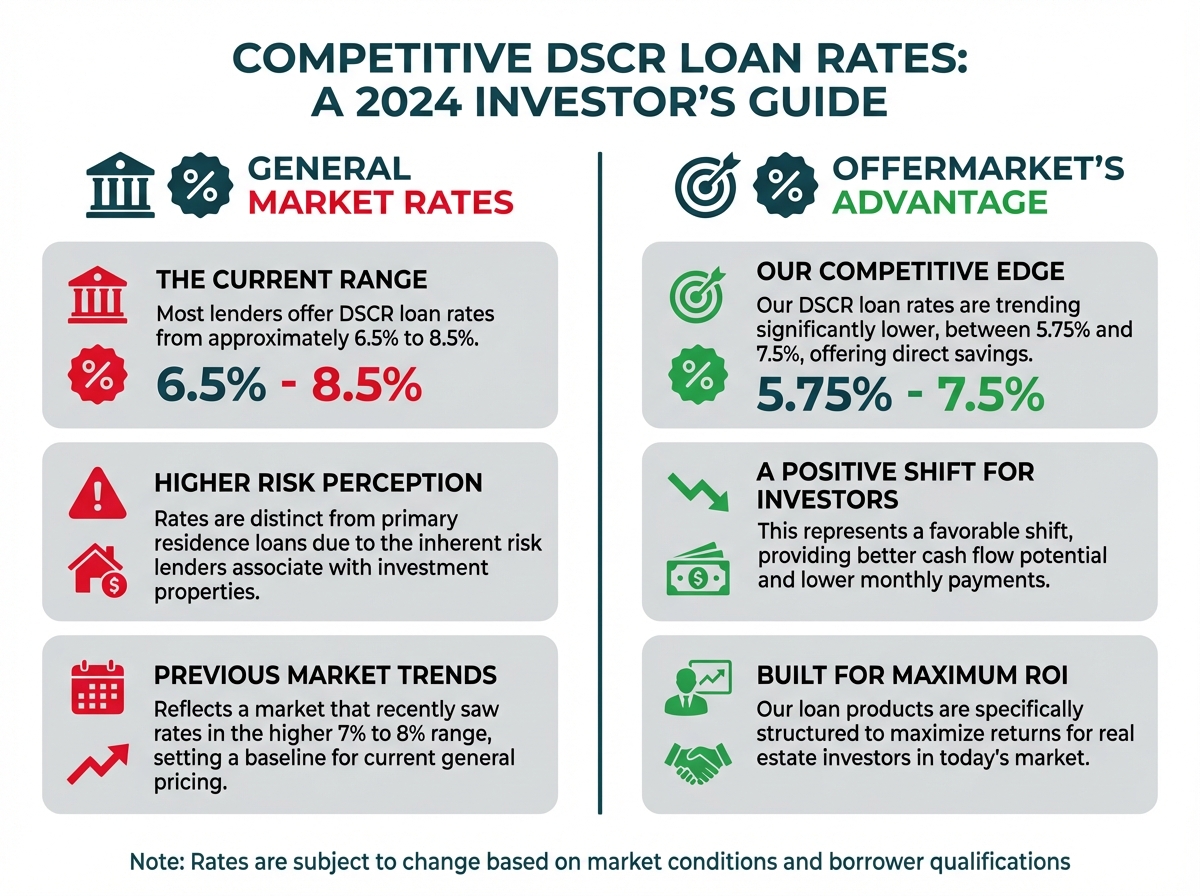

DSCR loan rates are typically higher than conventional loans and influenced by the 5-Year Treasury rate + credit spread. Factors affecting your rate include:

- Credit Score

- Loan-to-Value (LTV)

- DSCR

- Property Type & Location

Common Fees Include:

- Origination Fee: 1.5–2 points

- Underwriting & Processing Fees

- Draw Fees: $270–$300 (for rehab loans)

- Closing Costs: Typically 3–6% of the loan amount

*Prepayment Penalties:

DSCR loans may include a prepayment penalty, depending on the lender. OfferMarket’s prepayment penalty options range from no prepayment penalty ("no PPP") to 5-4-3-2-1. Note that short-term interest only bridge, fix and flip, and hard money loans generally do not have prepayment penalties.

Advantages for Florida Investors

DSCR loans prioritize property income over personal income, offering flexibility. Many investors, especially those with non-traditional income, find this appealing. These loans support various investment strategies, including the acquisition and refinancing of both commercial and residential properties. Lenders usually offer high loan amounts based on property cash flow, helping investors leverage more properties. Prepayment options are flexible, allowing investors to adjust repayment schedules without incurring penalties.

Potential Drawbacks and Considerations

Despite DSCR loans' benefits, some drawbacks exist. Borrowers must ensure property income consistently meets minimum DSCR thresholds, ranging from 1.1 to 1.5, to secure favorable terms. Economic fluctuations might impact rental income, thereby affecting loan eligibility. Investors should also consider interest rates, which can be higher than those of traditional loans due to the focus on property income. Lenders still require comprehensive documentation, including bank statements and rental agreements, to assess financial stability. Additionally, a minimum credit score of 620 is needed, impacting loan terms and interest rates if not met.

Conclusion

Navigating the DSCR loan landscape in Florida requires a strategic approach to real estate investment. By focusing on property cash flow rather than personal income, these loans offer a flexible financing solution for both seasoned and new investors. Understanding lender criteria, such as minimum DSCR and credit score requirements, is crucial for securing favorable terms. While DSCR loans provide opportunities for leveraging property income, maintaining consistent rental revenue is essential to mitigate potential risks. Thorough preparation and documentation can enhance the likelihood of loan approval, allowing investors to capitalize on the dynamic Florida real estate market. Florida is one of the top-performing states for DSCR loan demand and rental yield, making it an excellent market for this type of financing. OfferMarket offers DSCR loans across the state of Florida.

Frequently Asked Questions

What are DSCR loans, and why are they popular in Florida?

DSCR (Debt Service Coverage Ratio) loans are popular in Florida because they focus on a property's cash flow rather than the borrower's personal income. This makes them ideal for investors who have non-traditional income sources. By assessing the property's rental income to cover debt obligations, DSCR loans provide flexibility for purchasing and refinancing opportunities without requiring extensive personal income documentation.

How is DSCR calculated, and why is it important?

DSCR is calculated by dividing the property's net operating income by its debt obligations. A DSCR above 1.0 indicates that the property generates more income than needed to cover its debt payments, which strengthens the lender's confidence in the borrower's ability to repay the loan. This ratio is crucial for determining loan eligibility and terms.

What are the typical requirements for obtaining a DSCR loan in Florida?

To obtain a DSCR loan in Florida, borrowers typically need a minimum credit score of 620 and must meet lender-specific DSCR requirements, usually between 1.1 and 1.5. The loan-to-value (LTV) ratio ranges from 70% to 80%, requiring a sufficient down payment or equity. Applicants must also provide financial records like bank statements and rental agreements to demonstrate financial stability.

How can DSCR loans benefit real estate investors in Florida?

DSCR loans benefit Florida real estate investors by prioritizing property income over personal income. This is advantageous for those with varying income sources. These loans also allow for leveraging higher loan amounts based on property cash flow and offer prepayment flexibility, enabling investors to avoid penalties for early repayment, which supports long-term investment strategies.

What challenges do Florida investors face with DSCR loans?

Florida investors may face challenges such as meeting minimum DSCR thresholds amid economic fluctuations impacting rental income. Interest rates for DSCR loans can be higher than those for traditional loans. Comprehensive documentation to assess financial stability is still necessary, requiring detailed preparation to strengthen the loan application.

What documentation is required for the DSCR loan application process?

For a DSCR loan application, borrowers need to provide comprehensive documentation, including bank statements, rental agreements, proof of property ownership, and insurance. If refinancing, existing mortgage documents and payment history are required. Although personal income documentation is less emphasized, demonstrating financial stability enhances the application’s success.

Are there any prepayment penalties associated with DSCR loans?

DSCR loans often offer prepayment flexibility, allowing investors to repay loans early without facing penalties. This feature is appealing to those with long-term investment strategies, as it facilitates management of debt obligations and maximizes property profitability by adjusting financing based on market conditions and financial goals.

Grow and optimize your portfolio with OfferMarket

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull