*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Top Lenders: Who Offers DSCR Loans for Real Estate Investors?

Last Update: November 28, 2024

Navigating the world of real estate financing can be a daunting task, especially when looking for specialized loan products like DSCR loans. Debt Service Coverage Ratio (DSCR) loans are crucial for investors seeking to finance income-generating properties, as they focus on the property's cash flow rather than the borrower's personal income. These loans are particularly appealing to real estate investors who want to expand their portfolios without the traditional income verification hurdles.

A variety of lenders offer DSCR loans, each with unique terms and qualifications. From traditional banks to private lenders and credit unions, understanding who provides these loans can help investors make informed decisions. By identifying the right lender, investors can unlock opportunities to grow their investments efficiently. The right DSCR loan provider can make all the difference in securing the financial backing needed to succeed in the competitive real estate market.

Understanding DSCR Loans

DSCR loans focus on the cash flow generated by the property to determine loan eligibility. By using the Debt Service Coverage Ratio, lenders assess whether a property's income can cover its loan payments. DSCR calculates this ratio by dividing the net operating income by the total debt service. For instance, a DSCR of 1.25 indicates that the property generates 25% more income than required to cover debt payments.

These loans suit investors who lack traditional income verification but own properties with strong revenue streams. They allow borrowers to expand their portfolios with greater ease since approval relies on property performance rather than personal financials. DSCR loans are primarily offered by private lenders who specialize in real estate investment financing. Some platforms like OfferMarket operate as both direct lenders and referral sources, depending on the state and licensing requirements.

The DSCR formula is: Gross Rental Income ÷ PITIA (Principal, Interest, Taxes, Insurance, HOA). A DSCR above 1.0 means the property earns more than it costs to finance monthly. Lenders typically require a minimum DSCR of 1.0 to 1.25 for approval.

DSCR Loan Qualification: Property-First, Not Personal Income

DSCR loans do not rely on personal income, W-2s, tax returns, or DTI ratios. Instead, lenders evaluate:

Gross Rental Income

Monthly PITIA costs

Resulting DSCR ratio (must usually be ≥1.0–1.25)

This makes DSCR loans ideal for investors who are self-employed, have complex financials, or simply want to avoid full-document underwriting.

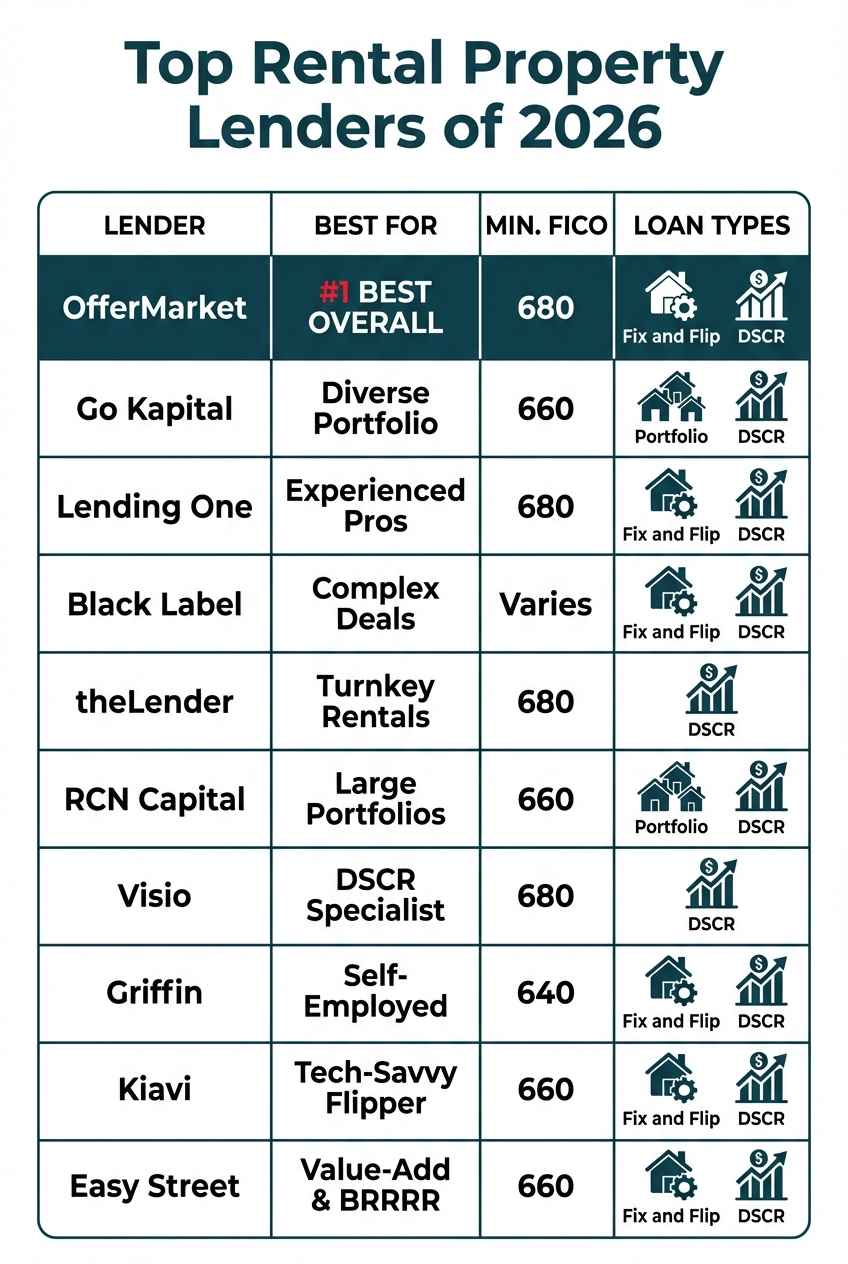

Key Players in the DSCR Loan Market

The DSCR loan market is dominated by private lenders with specialized underwriting expertise in investment property financing. While some banks or credit unions may offer products labeled as DSCR loans, they often involve traditional underwriting and higher documentation requirements. Specialized lenders like OfferMarket Capital LLC focus on streamlined approval processes, fast closings, and property-based qualification.

Major Banks

Major banks act as pivotal sources for DSCR loans. They benefit from established trust factors and provide competitive interest rates. Banks like JPMorgan Chase and Bank of America extend DSCR loans due to their ability to leverage extensive financial resources and standardized lending processes. Investors often prefer banks because they offer a comprehensive suite of financial services that can simplify portfolio management.

Credit Unions

Credit unions serve as important contributors to the DSCR loan market. They focus on member-centric services and often present more flexible terms compared to traditional banks. Investors might choose credit unions like Navy Federal Credit Union for their personalized customer service and community-focused approach. Despite smaller scale operations, credit unions might offer favorable interest rates and lower fees, appealing to many property investors.

Online Lenders

Online lenders play a dynamic role in providing DSCR loans. They utilize technology to streamline the application process, minimizing paperwork and expediting loan approvals. Companies such as OfferMarket and Kiavi stand out for their innovative platforms and competitive pricing structures. Investors are attracted to online lenders for their convenience and speed, making them a popular choice for tech-savvy individuals seeking efficient financing solutions.

Comparing Loan Terms

Debt Service Coverage Ratio (DSCR) loans offer diverse terms for real estate investors. Understanding these differences helps in choosing the right financial partner.

Interest Rates

DSCR loan interest rates vary based on the lender and the property's risk profile. DSCR loan interest rates generally range from 7% to 9%, depending on credit score, LTV, DSCR, and property type. These rates are higher than conventional mortgages due to the investment focus and reduced documentation requirements.

Loan Amounts

Private DSCR lenders typically offer loans from $55,000 to $2,000,000, with some offering higher limits for experienced investors or portfolios. Minimums are often lower than conventional lenders, making DSCR loans accessible for small-to-mid-size investors. In contrast, some private lenders and online platforms, like Kiavi, might approve smaller loans, appealing to newer investors or those with modest property portfolios. Identifying a lender that aligns with the investor's financial goals is essential.

Repayment Options

Repayment terms for DSCR loans often range from 5 to 30 years, depending on the lender's policies and the investor's preference. Banks might offer more traditional 15- or 30-year solutions to match standard mortgage structures. However, private lenders could propose shorter terms, like 5- or 10-year plans, for investors seeking quicker equity build-up. Tailoring repayment terms to investment strategies is vital for maximizing financial outcomes.

Application Process for DSCR Loans

Securing a DSCR loan requires understanding the specific steps involved in the application process. Prospective borrowers should first assess the property's cash flow to determine eligibility. They must gather necessary financial documents, such as rent rolls and operating income statements, to demonstrate the property's ability to service debt.

Once documentation is prepared, applicants should research and select a lender offering DSCR loans. Options include major banks, credit unions, and private lenders. The choice depends on competitive interest rates, loan terms, and lender-specific requirements.

Submitting a loan application involves providing detailed property information and financial documentation. Lenders evaluate these to calculate the DSCR and decide on loan approval. Applicants may undergo further assessment if the property risk profile requires additional scrutiny, impacting interest rates and terms.

Upon approval, borrowers receive loan terms outlining the interest rate, repayment period, and any conditions set by the lender. It's crucial to review these terms carefully to ensure alignment with investment goals. Effective communication with the lender throughout the process enhances the likelihood of securing favorable loan conditions.

Tips for Choosing a DSCR Loan Provider

Evaluating Reputation and Experience

When selecting a DSCR loan provider, assess the provider's reputation and experience. Established providers, like major banks and reputable credit unions, typically offer a track record of reliability. Check customer reviews and industry awards for additional insight.

Comparing Interest Rates

Analyze interest rates across different providers for the best financial terms. Banks often provide competitive rates around 3%, whereas private lenders may exceed 8%, depending on property risk. A comprehensive comparison ensures better loan choices.

Assessing Loan Terms

Review loan terms thoroughly. Terms can vary significantly, with repayment periods from 5 to 30 years. Consider how these terms align with your investment strategy to ensure feasible repayment plans and optimal financial outcomes.

Evaluating Flexibility

Assess the flexibility offered by lenders. Some online platforms, such as OfferMarket and Kiavi, are known for streamlined application processes. Evaluate if the lender offers adaptable solutions that meet unique investment needs.

Examining Customer Service

Prioritize lenders known for exceptional customer service. Credit unions are often highlighted for personalized attention, which can simplify complex loan processes. Investigating communication efficiency can lead to smoother transactions.

Investigating Specialization

Identify if the lender specializes in investment properties. Tailored expertise can benefit investors who rely on property cash flow rather than personal income for loan approval. Specialized knowledge often leads to better assessment and loan terms.

DSCR Loans vs. Fix & Flip and Bridge Loans

DSCR loans are typically used for long-term rental financing. They are distinct from Fix and Flip or Bridge Loans, which are short-term loans used for acquisition and renovation.

OfferMarket offers a bundled approach called Fix and Rent, where investors use a short-term rehab loan and then refinance into a DSCR loan once the property is stabilized and rented. This is ideal for investors who want both renovation financing and long-term rental cash flow.

Conclusion

Navigating the landscape of DSCR loans requires investors to thoroughly evaluate their options among various lenders, each offering unique advantages. Whether opting for the competitive rates of major banks, the personalized service of credit unions, or the streamlined processes of online platforms, choosing the right lender is crucial. By understanding the nuances of loan terms, interest rates, and the application process, investors can align their financing strategies with their investment goals. This ensures not only the successful acquisition of income-generating properties but also sustainable growth in their real estate portfolios.

Frequently Asked Questions

What is a Debt Service Coverage Ratio (DSCR) loan?

A DSCR loan is a type of real estate financing that focuses on the cash flow generated by a property rather than the borrower's personal income. It's intended for investors in income-generating properties, using the Debt Service Coverage Ratio (DSCR) to determine if the property's income can cover loan payments. The DSCR indicates how much more income is produced than needed for debt obligations, making it ideal for investors who might lack traditional income verification but have strong property revenue.

Why are DSCR loans beneficial for real estate investors?

DSCR loans benefit real estate investors by prioritizing property cash flow over personal income, simplifying the financing process for those with robust property earnings. Without needing extensive income documentation, investors can expand their portfolios more easily. These loans allow for a more accurate assessment of property performance, thus facilitating investment growth even for those without traditional income proof.

Which lenders offer DSCR loans?

DSCR loans are offered by a range of lenders including major banks like JPMorgan Chase and Bank of America, credit unions such as Navy Federal Credit Union, and online lenders like OfferMarket and Kiavi. Each lender has distinct terms and interest rates, making it crucial to select one that aligns with the investor's financial goals and preferences.

How do interest rates vary for DSCR loans?

Interest rates on DSCR loans vary based on the lender and the property's risk profile. Major banks typically offer competitive rates starting around 3%, while private lenders may impose higher rates, often exceeding 8%. The specific rate will depend on the property's income potential and associated risks, requiring careful consideration to ensure favorable financial terms.

What are typical loan amounts and repayment terms for DSCR loans?

DSCR loan amounts generally start at $250,000 with banks and credit unions, but some private lenders and online platforms may approve smaller amounts for newer investors. Repayment terms range from 5 to 30 years, depending on lender policies and investor preferences. It's essential for investors to choose terms that align with their investment strategy for optimal outcomes.

What is the application process for securing a DSCR loan?

Securing a DSCR loan involves assessing the property's cash flow and gathering financial documents, such as rent rolls and income statements. Prospective borrowers should research lenders for competitive rates and terms, then submit detailed property information and documentation. Lenders evaluate these to calculate DSCR and determine loan approval. Upon approval, borrowers receive loan terms specifying interest rates and repayment periods.

What should investors consider when choosing a DSCR loan provider?

Investors should consider the lender's reputation and experience, compare interest rates, and thoroughly assess loan terms, including flexibility and customer service quality. It's vital to choose a lender specializing in investment properties to ensure better assessment and tailored loan terms, contributing to successful investment growth and financial outcomes.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull