*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Hard Money Refinance for Real Estate Investors

Last Updated: November 26, 2025

In the fast-paced world of real estate investing, timing is everything. For fix and flip investors and those pursuing the Buy, Rehab, Rent, Refinance, Repeat "BRRRR method", hard money loans serve as a powerful tool to keep projects moving forward. But what happens when you need to pivot your financing?

Enter hard money refinance: a strategic move that allows you to pull equity out of a property, extend timelines, or transition to more stable long-term financing. This approach is especially valuable for investors focused on 1-4 unit residential properties, where quick access to capital can mean the difference between capitalizing on a hot deal or watching it slip away.

Hard money refinance involves using a short-term, asset-based loan to replace or supplement an existing financing structure. Unlike traditional bank loans, which emphasize borrower credit and income, hard money lenders prioritize the property's potential value after repairs, known as the After Repair Value (ARV). This makes it ideal for investors who buy distressed properties, rehab them, and either flip for profit or hold for rental income. By refinancing into another hard money loan or cashing out equity, you can replenish your cash reserves, fund additional rehabs, or bridge gaps until a permanent loan is in place.

For fix and flip investors, hard money refinance helps maintain momentum during rehabs, allowing you to seize new opportunities without halting progress. BRRRR enthusiasts benefit by recycling capital after the "rehab" phase, enabling the "repeat" step sooner. The key is understanding how these refinances work in real-world scenarios. In this article, we will explore three common situations: cashing out after a cash purchase, handling a maturing loan with incomplete rehab, and transitioning to a Debt Service Coverage Ratio (DSCR) loan post-rehab. We will draw on proven guidelines to provide clear examples, benefits, and steps to success. Whether you are a seasoned investor or just starting with your first flip, these insights will empower you to use hard money refinance as a lever for growth.

The beauty of hard money lies in its flexibility. Loans typically range from $25,000 to $2,000,000, with advances up to 90% of the purchase price and 100% of rehab costs, based on your experience level. Interest rates are competitive, interest-only during the term, and there are no prepayment penalties, giving you room to exit on your terms. With terms of 12 to 24 months and easy extensions, you can adapt to delays without derailing your business plan. As we dive deeper into hard money loans, you will see how these features make hard money refinance not just a backup plan, but a proactive strategy for scaling your portfolio.

Understanding Hard Money Loans: The Foundation of Smart Refinancing

Before jumping into specific scenarios, it is essential to grasp the basics of hard money loans. These are private lender products designed for real estate investors who need speed and flexibility over rigid qualifications. Traditional mortgages can take weeks or months to approve, but hard money funding often closes in days, making it perfect for competitive markets where off-market deals vanish quickly.

At their core, hard money loans are secured by the property itself, with lending decisions driven by the loan-to-value (LTV) ratio and loan-to-cost (LTC) metrics. For 1-4 unit residential properties, including single-family homes, townhomes, condos, and small multifamily units, lenders evaluate the as-is value, purchase price, rehab budget, and projected ARV. A minimum ARV of $100,000 ensures the deal has enough upside potential. This ARV focus rewards investors who can identify value-add opportunities, such as cosmetic updates or structural fixes that boost marketability.

Loan terms are straightforward and investor-friendly. The standard duration is 12 months, with options for 18 or 24 months on larger or more complex projects. Payments are interest-only, meaning you pay monthly interest on the drawn amount (for loans over $100,000) or the full loan balance (for smaller ones), with the principal due as a balloon payment at maturity. This structure preserves cash flow during the rehab phase, when expenses like materials and labor are front-loaded.

Interest rates vary based on market conditions and borrower profile, but they are typically lower than credit card rates or personal loans, often in the single digits when quoted. Origination fees range from 1 to 2 points (1-2% of the loan amount, with a $2,000 minimum), and there are no points paid out of pocket upfront. Additional costs include a $270 draw fee per rehab disbursement and a $30 wire fee, keeping overall expenses predictable. Best of all, no prepayment penalties mean you can refinance or sell without extra costs if the market shifts favorably.

Eligibility is accessible, even for newer investors. No prior experience is required for entry-level (Tier 1) borrowers, though higher tiers (based on completed flips: 1-2 for Tier 2, more for Tiers 3 and 4) unlock better terms like higher advances (up to 90% of purchase price) and loan-to-ARV ratios (up to 75%). A minimum credit score of 680 is standard, with exceptions down to 660, and lenders pull a recent tri-merge report. Debt-to-income ratios are not a barrier, but you will need liquidity: enough cash to close plus 25% of your rehab budget in verifiable assets, like bank or brokerage statements.

The entity structure must be an LLC or corporation, with full recourse and a personal guarantee from at least 51% of the owners (100% for cash-out refinances). Properties must be non-owner-occupied, at least 700 square feet for single-family or 500 per unit for multifamily, and on no more than 5 acres. Exit strategies are key: for flips, aim for a 30% ROI and $15,000 minimum profit; for rentals, ensure a 1.1 DSCR post-repairs.

The funding process is efficient. For purchases, you submit the contract, credit reports, entity documents, scope of work, and bank statements. An appraisal (or in-house valuation for qualified borrowers) confirms values. Initial funds wire to title at closing, while rehab draws reimburse costs via an app-based system, with inspections ensuring progress. Turnaround for draws is often 0-2 business days, minimizing downtime.

What makes hard money shine for refinancing? Its adaptability. Extensions add up to 50% more time (e.g., 6 months on a 12-month loan) for 1-2.5% fees, and cash-out options are available for seasoned properties. Risks are low, with default rates under 0.5%, thanks to conservative underwriting like rehab scope adjustments (e.g., lower advances for full gut jobs). By building on this foundation, hard money refinance becomes a bridge to bigger wins, turning potential roadblocks into opportunities for expansion.

Scenario 1: Cashing Out After a Cash Purchase to Fuel New Deals

Imagine this: you spot a diamond-in-the-rough single-family home in a desirable neighborhood. With $100,000 in cash from a prior flip, you buy it outright to move fast and avoid bidding wars. Now, as rehab begins, another off-market deal pops up, but your liquidity is tied up. This is the perfect moment for a hard money cash-out refinance. By pulling equity from your cash-purchased property, you replenish funds to grab the new opportunity while your crew works on the first one.

As long as you're not stuck in "mid-construction", hard money lenders generally love this scenario because the property is already in your control and the rehab component of your project is not off schedule or over budget. For cash-out refinances from a free and clear property into a hard money loan, your initial advance will be up to 90% of your purchase price and then you will have access to up to 100% of your rehab budget via draw processing reimbursements.

Let's walk through a real-world example based on standard guidelines. Suppose you bought a single family property for $100,000 cash last week. You were planning on knocking out this project without a hard money loan but you found a wholesale real estate deal you would be crazy to pass up. So you find a hard money lender and get a fix and flip loan:

- Initial advance: $90,000 (90% based on your verifiable experience)

- Construction holdback: $50,000

- Total loan: $140,000

- ARV: $200,000

- LTARV: 70%

- Interest rate: 10.25% (get your instant quote)

- Term: 12 months

- Structure: fixed rate, interest only

- Origination fee: $2,800 (2%)

- Time to close: 10 days

- Note: interest is only charged on the funds that are advanced, so you are not charged interest on the construction holdback component of your loan until those funds are drawn.

Net of closing costs, you cash out roughly $84,000 which you use to purchase the wholesale real estate deal in cash -- but don't forget, you could have also purchased it with a hard money loan. Many hard money lenders are happy to finance multiple projects at the same time and prefer purchase scenarios above refinance scenarios.

The hard money refinance process starts with submitting your original settlement statement, sunk costs (simple list of rehab completed so far), updated scope of work. The lender will either conduct an internal valuation or order an appraisal of the property. Funding wires quickly, often within days, so you can close on that second property without delay, stress or financial strain.

Now you have 2 rehab projects going at the same time, keeping your contractors busy, getting better economies of scale (lower rehab costs). One of the projects will be a $50,000+ fix and flip profit, the other will be a perfect BRRRR into a DSCR loan refinance for your long term rental portfolio. This is how we build wealth through real estate.

In this scenario, you avoid opportunity costs of tying up cash in your rehab project, leveraging the first property's equity to scale faster while enhancing your cash liquidity for proper risk management. For BRRRR investors, this cash-out sets up the "refinance" step early, recycling capital without waiting for full rehab.

Risk management is critical. Always ensure your cash liquidity meets or exceeds 25% of your ongoing rehab budgets, and focus on deals that have dual exit strategy potential -- flip or rent -- in case market conditions shift.

To execute smoothly, document everything: photos of progress, contractor bids, and market comps. Partner with lenders offering no prepayment penalties, so you can pivot to sale or DSCR later. Investors report closing up to 80% faster than banks, preserving deal momentum.

This strategy turns single-project thinking into portfolio building. By refinancing early, you create a flywheel: each property funds the next, compounding your returns. For fix and flip investors and BRRRR investors, it means better capital efficiency. Approach with a clear ARV justification, and you will find hard money refinance opens doors you did not know existed.

Scenario 2: Refinancing a Maturing Hard Money Loan Mid-Construction

Rehabs rarely go perfectly. Contractor issues, permitting delays, supply chain issues, or scope creep can push timelines, leaving you facing a maturing hard money loan with unfinished work. Rather than scrambling for a forced sale, you may be able to refinance into a new hard money loan or extend your existing one. This keeps your project alive, protects your investment, and positions you for a strong exit.

Extensions are the first line of defense: add 3-6 months (up to 50% of the term) for 1-2.5% of the loan balance, this is as simple as providing proof of active fix and flip insurance and signing a 1-page extension agreement. But if more time is needed or terms have changed, a full "mid-construction" refinance resets the clock with fresh capital.

The problem with mid-construction hard money refinances is that most lenders hate them. It's a huge red flag, and the lender does not want to be the "market fool" to pay off another lender that may have been unwilling to extend a hard money loan. Hard money loans mature quickly. It doesn't take much to go into maturity default -- where even though you're paying your monthly interest, your loan is technically in default because it has not been paid off and the maturity date is in the past.

In order to successfully refinance a hard money loan mid-construction, you need to prove to the lender that you are organized, that you are not in financial distress (protect your credit score above all else!), and that an extenuating circumstance outside of your control (i.e. permitting delays affecting all rehab projects in the market) caused the delay.

Consider this mid-construction hard money refinance example

You secured a 12-month hard money loan for a $100,000 single-family purchase and $20,000 rehab, ARV $150,000. As a Tier 4 investor with five prior flips and 750 credit, you got 90% purchase advance ($90,000) and full rehab holdback, totaling $110,000 at 73% LTARV. Nine months in, electrical surprises add $5,000 and two months, pushing maturity with 40% rehab complete.

Your current lender is over-extended and wants their money back, so you opt for refinance with a different hard money lender. You submit updated docs like progress photos, revised scope of work ($25,000 total rehab), and your new lender orders a new appraisal confirming a higher ARV at $165,000. The lender approves a new 12-month loan for $115,000 (70% LTARV) where you are not being cashed out, you're effectively getting a rate and term refinance to finish your rehab project. Even though the term is 12 months, you'll likely payoff the loan in 3-4 months which is the time it will take to complete the rehab and sell or refinance into a 30 year rental property mortgage.

Communication is key when facing delays

Don't be silent, be proactive and transparent. Notify your lender as soon as you run into issues -- there's a very good chance they can help you navigate whatever problem you're facing. If you think you'll need to extend your hard money loan, notify your lender at least 60 days prior to maturity to make sure you have enough time to extend in a stress free manner without rushing insurance review and any other extension formality.

Budget for extension fees (i.e. up to 2.5 points added to the loan's eventual payoff statement). Maintain cash liquidity to carry the project to the next draw reimbursement. Protect your credit score by not running up your credit cards -- this is a classic mistake that can eliminate DSCR loan refi as an exit strategy option. When you are facing a mid-construction hard money refinance or extension, you are in the danger zone and you need to double down on discipline to get your project to the finish line.

This scenario highlights hard money's risk and its resilience. Don't panic, instead view maturity as a checkpoint. Refinance strategically, and you emerge stronger, with a completed asset ready to generate returns. Many investors chain two-three loans per property, turning delays into diversified income streams.

Scenario 3: Transitioning from Hard Money to DSCR Loans After Rehab Completion

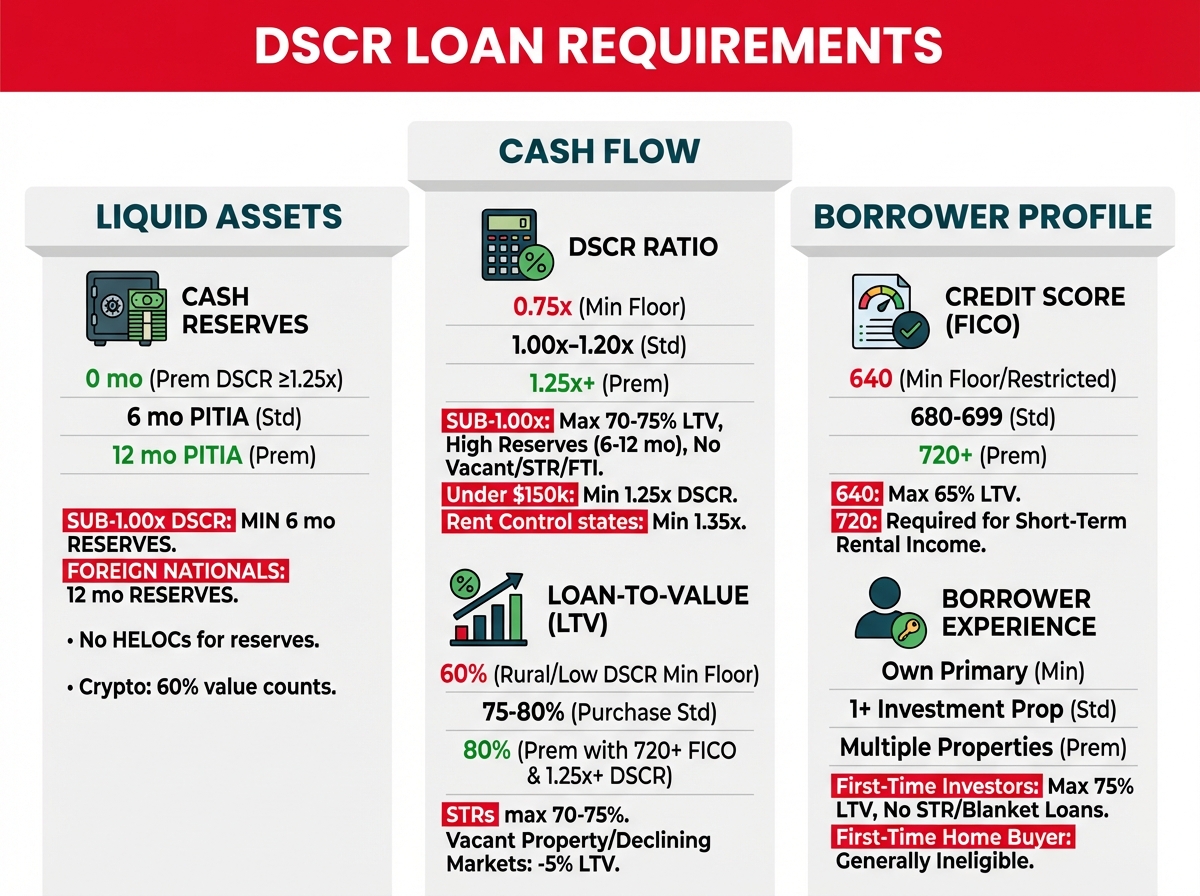

Congratulations! Your rehab is completed, and the property shines. The hard money loan that fueled it is maturing soon, but flipping now feels risky in a softening market. Time to refinance into a DSCR loan, a long-term rental product that qualifies based on property income, not personal income or W-2 employment. To maximize approval odds, rent the property unfurnished on a 12-month lease before closing, providing proof of cash flow.

DSCR loans are the go-to financing tool for BRRRR investors, offering 30-year terms at fixed rates, with LTV up to 80%, no personal DTI checks, no tax returns and no W-2 employment verification. Post-rehab, your hard money exit requires a minimum DSCR of 1.0, and a property that is not rural making this seamless.

DSCR Refi Example

A fix and rent investor used a $109,000 hard money loan ($85,000 initial advance, $24,000 construction holdback) on a $100,000 purchase for a duplex that required $24,000 rehab to achieve an ARV of $170,000 to $185,000. The investor (Tier 1, 0 verifiable experience) protected their credit score throughout and their soft trimerge credit report was 725 when it came time to refi into a DSCR loan:

- As Is appraisal: $180,000

- Hard money payoff statement: $109,000

- DSCR loan: $135,000 (75% LTV, 30 year term, fixed rate)

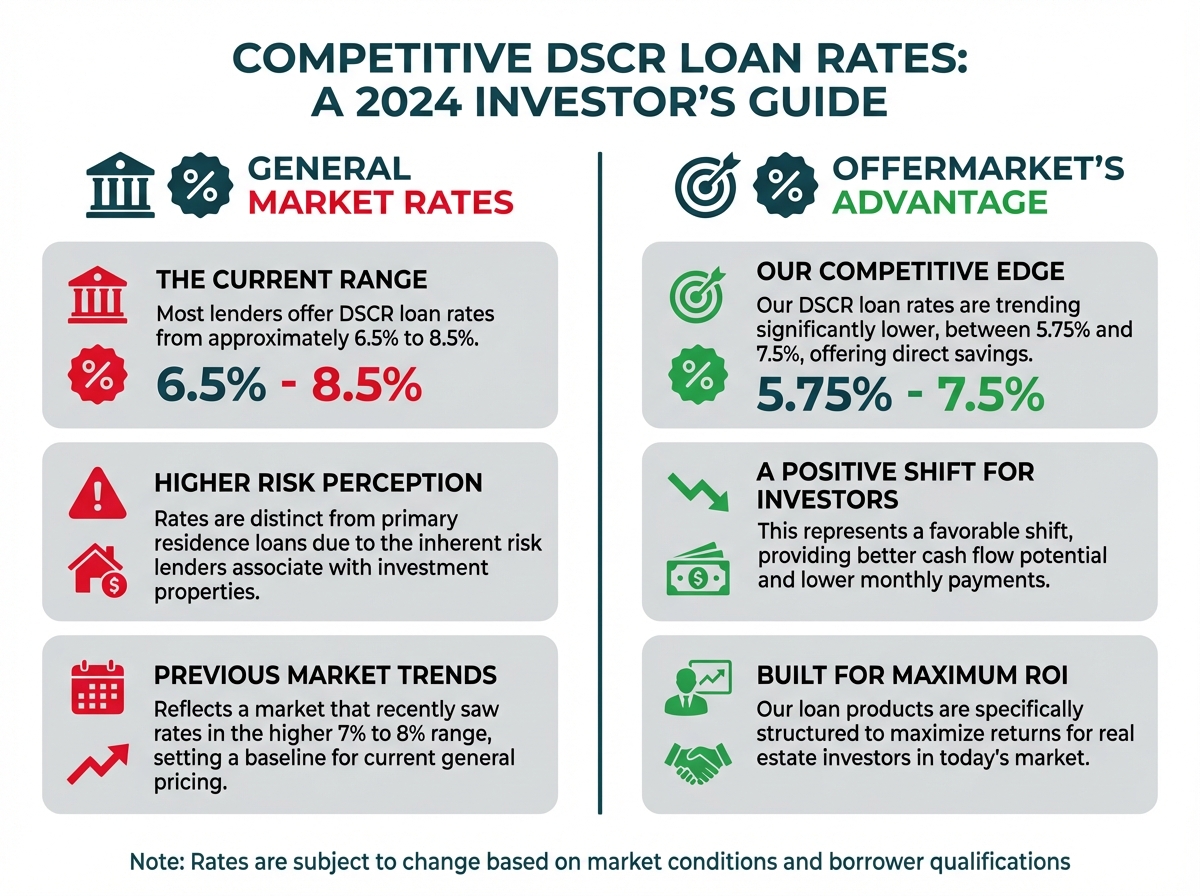

- DSCR loan rate: 6.5% -- see DSCR loan rates

- Refinance closing costs (title fees, lender fees, pre-paids): $8,000

- Cash out proceeds: $18,000

- Time to close: 10 - 30 calendar days

For fix and flippers pivoting to hold, this creates passive income, avoids short term capital gains, qualifies for an eventual 1031 exchange, and allows you to wait for better market conditions to sell the property.

💡 Tips: Secure pre-approval before purchasing and rehabbing to make sure the property type is eligible for DSCR loan at attractive terms. Run your numbers conservatively: ARV, LTV, rehab costs, project timeline, cash reserves. Stay on top of your contractors, hold them accountable to budgets and timelines.

In one case, a flipper faced deteriorating market conditions for a sale and decided to rent and refi into a DSCR loan. The property appraised for higher than they could have sold it and they cashed out over $20,000 more than they invested into the project. Their free cash flow was over $600 per month from their tenant, and this was the start of what is now approaching a 100 property rental portfolio that generates over $50,000 per month in free cash flow.

Hard money, in partnership with a lender focused on serving as your risk-management advisor, is a powerful launchpad for building long-term wealth.

Conclusion: Empower Your Investing Journey

Hard money refinance is more than a tool, it is a catalyst for innovation. From cash-outs that spark growth to bridges over delays and pathways to stable rentals, it equips you to navigate real estate's twists with confidence. Embrace these strategies, and watch your 1-4 unit portfolio flourish. The next deal awaits, are you ready to refinance your way to it?

Join OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders and flippers. We focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull