*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How to Get Fix and Flip Loans with OfferMarket

Getting financing for your next flip doesn't have to slow down your investment plans. At OfferMarket, we've built a straightforward process that cuts the typical 45-60 day timeline with traditional lenders down to just 1-3 weeks. That means you can move as fast as cash buyers while keeping your capital free for more deals.

The OfferMarket Advantage: Quote to Close in Record Time

It all starts with our instant quote system. We can quote and qualify you for fix and flip loans in under 2 minutes right on our online platform. This isn't a ballpark figure or a soft pre-qualification—it's a real quote based on your specific deal, your experience, and the property's potential After Repair Value (ARV).

While traditional lenders take 30-45 days to make their decision, our technology gives you immediate answers about your borrowing power. As soon as you get your quote, we automatically create your Loan File, and our processing team gets to work moving your deal toward the finish line.

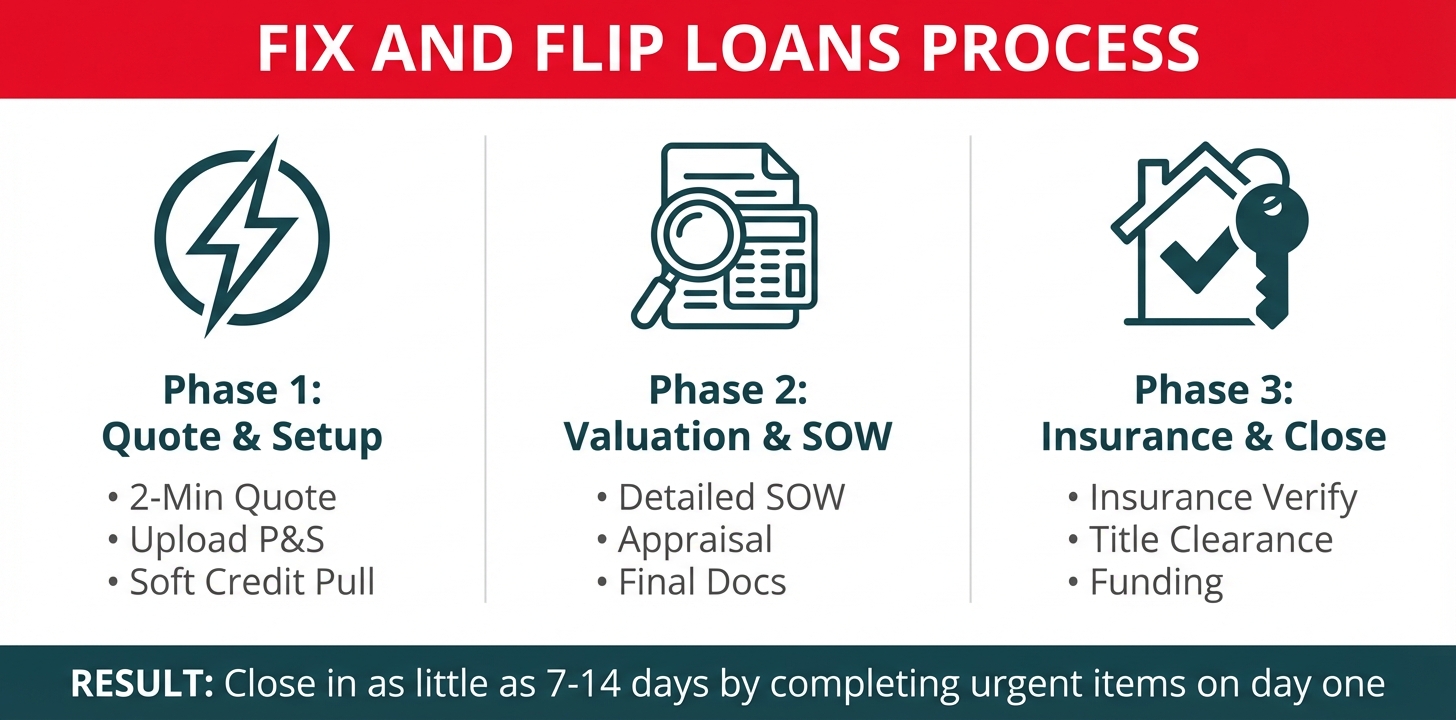

Step-by-Step: From Quote to Closing

Step 1: Get Your Instant Quote (2 Minutes)

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

You'll instantly see your maximum loan amount, interest rate, and required down payment based on your Experience Tier. You'll know exactly how much leverage you qualify for—whether that's 80%, 85%, or 90% of the purchase price—before you ever talk to a loan officer.

Step 2: Upload Purchase contract and complete sections marked URGENT

Once you move forward, our streamlined system walks you through the full underwriting checklist inside your dashboard.

First you will need to complete Processing section that are marked URGENT. We like to kick off our process by having you upload a Purchase Contract, authorize a soft credit pull through our website as well as complete a loan application where you enter some additional information.

If your property requires an appraisal we also like you to complete appraisal authorization on the first day so we can order the appraisal on the next business day which should accelerate all the timelines. In some cases for fix and flip loans we allow a desktop appraisal which make things a lot more streamlined.

Step 3: Submit Your Scope of Work

Upload a detailed Scope of Work (SOW) broken down by trade or building system—demolition, framing, plumbing, electrical, HVAC, finish work. This trade-based structure matters for two key reasons:

Accurate ARV Determination: The appraiser uses your SOW to calculate the property's After Repair Value, which directly impacts your maximum loan amount.

Faster Draw Reimbursements: By separating trades into "rough" and "finish" phases, you can request draws immediately after rough work is completed, rather than waiting for entire rooms to be marketable. This approach can put cash back in your pocket 30-45 days faster compared to room-by-room SOWs.

Step 4: Upload remaining documents

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

This digital-first approach cuts out the endless back-and-forth you get with traditional lenders. No faxing documents, no redundant form-filling, no waiting days for a loan officer to return your call.

Step 5: Appraisal and Title (3-7 Days)

Good news for experienced investors: OfferMarket can often approve loans using app-based inspection process for properties in excellent condition or when you have a strong track record. This cuts out the 5-7 day wait for an interior inspection, saving you time and money.

That said, for maximum leverage deals where you're pushing 90% LTC and 75% ARV, a full interior appraisal ensures you get the highest possible loan amount.

Here's a pro tip: if you complete the appraisal payment the same day you submit your application, we can usually close your loan within 2 weeks. The appraisal establishes both the As-Is value and the ARV—the two numbers that drive your underwriting.

Once appraisal is complete, the closing process moves to the title company. OfferMarket's integrated platform connects directly with title companies across the country, giving everyone involved real-time access to closing documents, wire instructions, and settlement statements.

Step 6: Secure Your Landlord Insurance (OfferMarket will help with this)

Before closing, complete the Insurance Verification section in your dashboard. You can choose OfferMarket’s preferred insurance partner—who shops multiple carriers for you—or bring your own policy.

You’ll enter:

- Subject property address

- Insured entity name (your LLC)

- Dwelling coverage amount

- Effective date

- Claims history

- Mailing address

- Date of birth

OfferMarket provides Landlord Insurance for 1–4 unit residential properties, allowing you to:

- Get an accurate quote inside the platform

- Ensure coverage meets lender requirements

- Avoid last-minute closing delays

This eliminates the scramble to find compliant insurance at the last minute.

Step 7: Clear to Close (7-14 Days from Application)

Once all items show 100% complete in your Processing dashboard:

- Title is cleared

- Insurance is completed

- Settlement statement is finalized

Your file moves to closing.

Result:

Some of the best real estate investors we have worked with have completed URGENT processing items on day one of their application which allowed OfferMarket to close in as little as 7–14 days.

Real-World Example Timeline: From Quote to Funded

Day 1 (Monday): You submit an online instant quote at 10:00 AM and receive approval for a $320,000 loan (85% of $350,000 purchase + $100,000 renovation budget, capped at 75% of $560,000 ARV). By 2:00 PM, you complete your full application inside the dashboard—credit authorization, bank statements, LLC docs, track record, purchase contract, and personal financial statement. By 4:00 PM, you upload your detailed trade-based Scope of Work and pay the appraisal fee. Appraisal and title are ordered same day.

Day 2 (Tuesday): OfferMarket processor begins to review uploaded files and with appraisal authorization in hand, they schedule an appraisal with the client.

Day 3-8: The appraiser inspects the property. Title work begins. Processing verifies liquidity, experience, and entity documents. You complete the Insurance Verification section in your dashboard and bind landlord coverage effective at closing.

Day 8-13: The appraisal returns (As-Is: $280,000, ARV: $560,000). Underwriting confirms the ARV supports the renovation budget, validates projected 22% ROI, and issues conditional approval. Title continues clearing.

Day 13-15: All conditions are cleared. Title is clean. Insurance is verified. Settlement statement is finalized. File is issued Clear to Close.

Day 15-17: Closing documents are prepared. You sign. Funds are wired to the title company.

Day 17-19: Closing completed. You take ownership and renovation begins immediately.

Total Timeline: 17-19 Business Days from Application to Funded

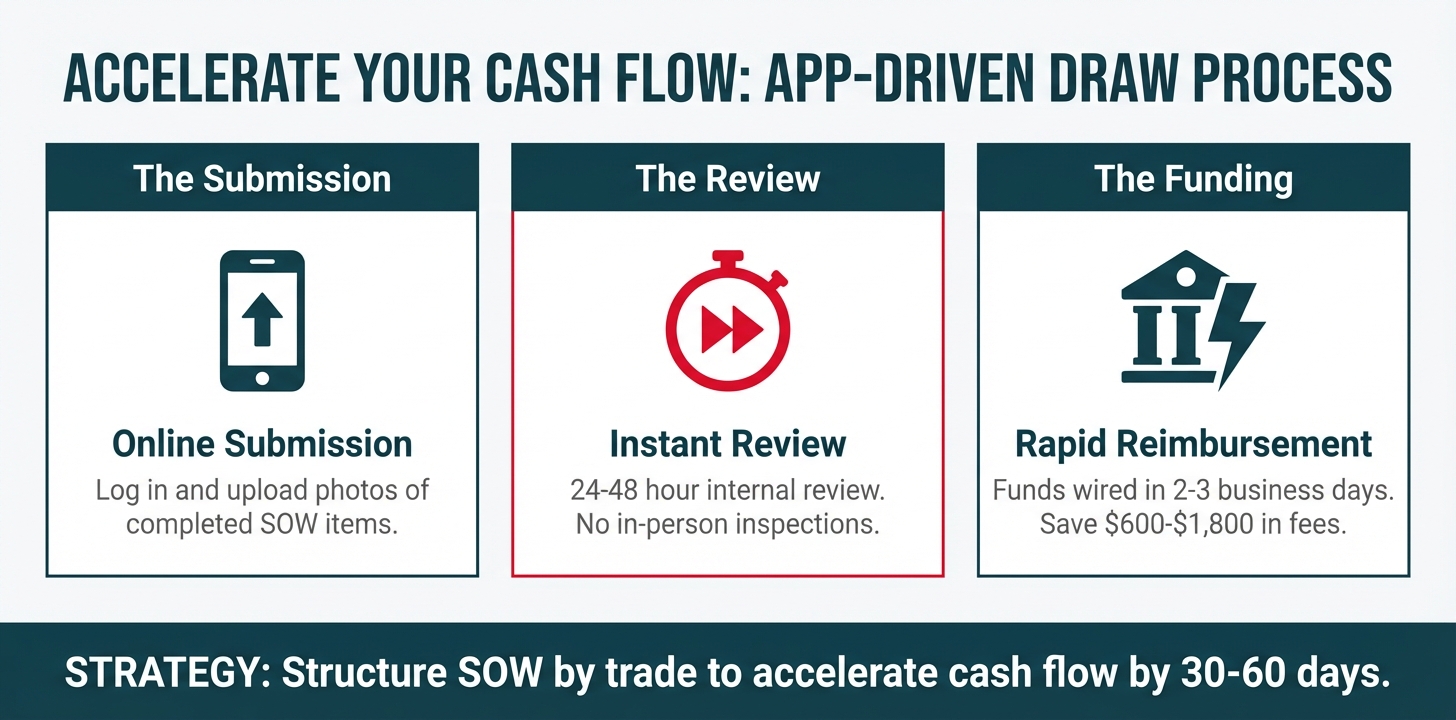

The Online App-Driven Draw Process: Saving Thousands on Re-Inspections

Some lender still require in person inspections for draw processing, I am sure you are familiar with costly re-inspections on every draw request—often $150-$300 per visit. With 4-6 inspections over the life of your project, that's $600-$1,800 added to your costs. Even worse, scheduling these inspections creates 5-10 days of delay between completing work and getting reimbursed. Not to mention the value of your time spent arranging all the inspections and baby sitting the appraiser while he is at the site. Time is money!

OfferMarket's app-driven draw process eliminates this friction entirely:

Submit Draw Requests Online: Log into your loan portal, select the completed work items from your approved SOW, and upload photos documenting the finished work.

Instant Review: OfferMarket's draw coordinators review submissions within 24-48 hours—no scheduling, no waiting for inspectors to drive to the property.

Rapid Reimbursement: Once approved, funds are wired directly to your account within 2-3 business days.

Here's a smart strategy: structure your SOW by trade rather than by room. This way, you can submit draw requests as soon as rough plumbing, rough electrical, or framing is complete—even if the kitchen or bathrooms aren't yet marketable. The result? You accelerate your cash flow by 30-60 days compared to traditional draw structures, keeping more capital working across multiple projects.

Our Fix and Flip Loans are your Competitive Advantage That Maximize Your ROI

App based Appraisals for Speed: When property condition and borrower experience allow, OfferMarket can approve loans using exterior-only or desktop appraisals. That's 5-7 days shaved off your timeline and $100-$200 saved in appraisal costs.

No Re-Inspection Fees: Our app-driven draw process puts $600-$1,800 back in your pocket per project—savings that go straight to your bottom line instead of paying for redundant inspections.

Interest Calculated "As Disbursed": For loans ≥$100,000, you only pay interest on what you've actually drawn, not the full loan amount. Translation? You're not paying interest on renovation funds sitting idle in escrow. That's $2,000-$5,000 in potential savings over a 12-month term.

No Prepayment Penalty: Sold the property? Great—exit your loan immediately. No minimum interest requirements or prepayment fees chipping away at your hard-earned profit.

Experience-Based Leverage: Here's where it gets exciting. As you complete projects and climb our Experience Tiers, OfferMarket automatically boosts your borrowing power from 80% to 90% of purchase price. Less cash needed at closing means you can scale from 1-2 flips per year to running 5-10+ projects simultaneously.

Next Step: Get Your Instant Quote For Fix and Flip Loans

The best way to see OfferMarket's competitive advantages in action is to run a quote on a real deal—whether it's a property you're under contract on or a hypothetical scenario to understand your borrowing power.

Apply here to get your instant quote in under 2 minutes. Simply input your deal parameters and see exactly what interest rate, loan amount, and down payment we can offer. There's no obligation, no credit pull at the quote stage, and no reason to wait.

Once you see the numbers, you'll understand why savvy investors are choosing OfferMarket as their go-to platform for fast, competitive, and scalable fix and flip financing.

How to Qualify for a Fix and Flip Loan

Getting approved for a fix and flip loan means meeting specific borrower qualifications and showing that your investment project passes key financial tests. Unlike traditional mortgages that zero in on your personal income and debt-to-income ratios, fix and flip loans look at the bigger picture—your business structure, investment track record, and whether the deal makes financial sense. Getting familiar with these qualification criteria puts you in the driver's seat when it comes to securing competitive financing and growing your flipping business.

Establish a Business Entity

Here's the deal: fix and flip loans are designed for business-purpose, non-owner-occupied properties, so you can't apply as an individual. You'll need to set up a formal business entity—either a Limited Liability Company (LLC) or Corporation—before you submit your loan application. This isn't just red tape; it creates a smart legal barrier between your personal and business assets, protecting both you and the lender.

Here's what you should know: at least one LLC member (or members holding at least 51% ownership together) must sign a full recourse personal guaranty. What does this mean for you? If the project doesn't pan out or the loan defaults, the lender has recourse beyond just the property. So while your business entity owns the property, you're personally standing behind the loan with your credit and assets.

If you're just getting started, don't sweat it—forming an LLC is pretty straightforward and takes anywhere from a few days to a few weeks in most states. Beyond checking the lender's box, your entity structure gives you liability protection and opens the door to potential tax benefits as you grow your real estate investment portfolio.

Credit Verification and Background Checks

Lenders will pull a tri-merge credit report, which gathers data from all three major credit bureaus—Experian, Equifax, and TransUnion. This gives them the full story on your credit history, how you handle payments, and any red flags that could impact your approval. At OfferMarket, we want to protect our borrower's credit scores, so we always only use soft credit pulls so our inquiries don't reduce our client's credit scores.

Beyond the credit report, expect lenders to run background checks looking for serious financial crimes, recent bankruptcies, or foreclosures. While past credit events don't automatically disqualify you, they do require adequate seasoning periods. Here's the deal: bankruptcies and foreclosures typically need to be at least four years behind you for standard approval. That said, some lenders may work with you if you're in that four-to-seven-year window—you'll just need additional interest reserves.

Minimum FICO Score Requirements

Let's talk numbers. The absolute floor for most fix and flip lenders is a 600 FICO score, but honestly, that comes with some serious restrictions and higher costs. For the best experience, aim for 680 or higher—you'll dodge the heavy underwriting scrutiny and unlock better terms. According to industry standards, if you're just starting out (0-2 completed projects), you'll typically need a 680 minimum. Got a solid track record? You might qualify with scores as low as 660.

Higher FICO means less capital is required

Here's something important to understand: your FICO score directly determines how much you'll need in interest reserves at closing:

- 600-620 FICO: 12 months of interest reserves required

- 620-640 FICO: 9 months of interest reserves required

- 640-660 FICO: 6 months of interest reserves required

- 660-680 FICO: 3 months of interest reserves required

- 680+ FICO: 1 month of interest reserves required

Think of these reserves as your safety net—they ensure you can keep making payments if your project hits delays or runs longer than expected. The better your credit score, the less cash you need upfront, which means more capital to spread across multiple deals.

Proof of Liquidity and Net Worth

Credit scores aren't the whole picture. Lenders also want to see documented proof that you have enough liquidity to handle surprises during renovation. The standard rule of thumb: your net worth (or the combined net worth of all guarantors) should equal at least 10% of your requested loan amount.

For example, if you're seeking a $300,000 fix and flip loan, you'll need to show a minimum net worth of $30,000. The good news? You can meet this requirement through several types of liquid assets:

- Cash in bank accounts

- Stocks, bonds, and investment accounts

- Retirement accounts (though some lenders may discount these)

- Equity in other real estate holdings

- Business assets and accounts receivable

Lenders will verify your liquidity through bank statements (typically the most recent two months), brokerage statements, and other financial documentation. This step ensures you have enough reserves to handle cost overruns, permit delays, or market shifts that could affect your project timeline or bottom line.

Document Your Investment Experience

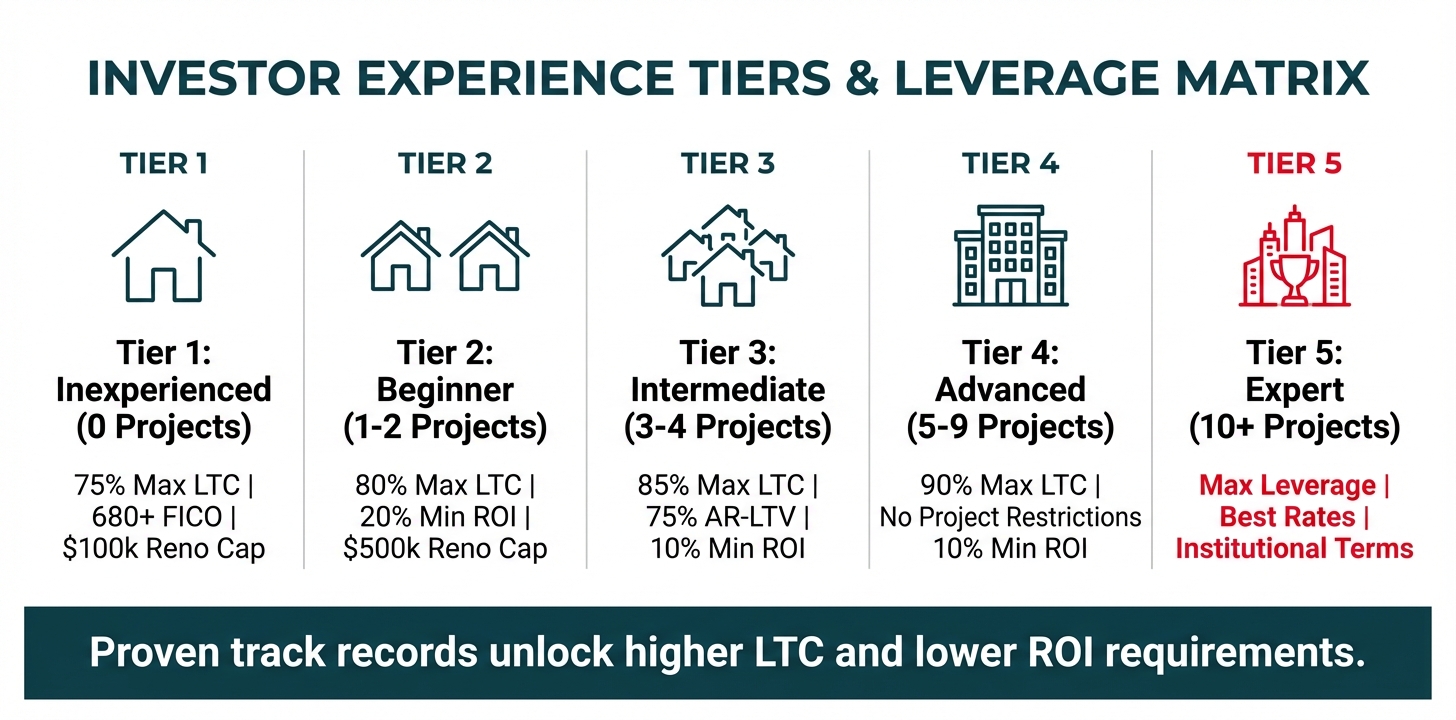

Here's where your track record really pays off. Your borrowing power and leverage depend on your "Experience Tier," which lenders determine by counting the investment properties you've successfully bought, sold, or held within the last 36 months. The logic is straightforward: experienced investors pose less risk and can tackle more complex projects with bigger renovation budgets.

Experience Tier Breakdown:

Tier 1 - Inexperienced (0 Projects)

- No completed fix and flip or rental property deals in the last three years

- Requires minimum FICO score of 680

- Maximum 75% loan-to-cost (80% with FICO ≥ 720)

- Renovation budget capped at $100,000 or 25% of purchase price

- No additions, extensions, or ADU conversions allowed

- Must demonstrate 20% minimum ROI or 1.10x debt service coverage ratio

Tier 2 - Beginner (1-2 Projects)

- One or two completed deals in the last three years

- Maximum 80% loan-to-cost

- Renovation budget capped at 2x your highest past project budget (max $500,000)

- No additions, extensions, or ADU conversions allowed

- Must demonstrate 20% minimum ROI

Tier 3 - Intermediate (3-4 Projects)

- Three or four completed deals in the last three years

- Maximum 85% loan-to-cost

- Maximum 75% after-repair loan-to-value (ARLTV)

- Renovation budget capped at 2x your highest past project budget (max $500,000)

- No ADU conversions or condo conversions allowed

- Must demonstrate 10% minimum ROI

Tier 4 - Advanced (5-9 Projects)

- Five to nine completed deals in the last three years

- Maximum 90% loan-to-cost

- Maximum 75% after-repair loan-to-value

- Renovation budget capped at 2x your highest past project budget (max $500,000)

- No project type restrictions

- Must demonstrate 10% minimum ROI

Tier 5 - Expert (10+ Projects)

- Ten or more completed deals in the last three years

- Maximum 90% loan-to-cost

- Maximum 75% after-repair loan-to-value

- Renovation budget capped at 2x your highest past project budget (max $500,000)

- No project type restrictions

- Must demonstrate 10% minimum ROI

To document your experience, gather detailed information about each qualifying project, including:

- Property addresses and acquisition dates

- Purchase prices and sale prices (or current rental income for hold properties)

- Renovation budgets and timelines

- Proof of ownership and disposition (HUD-1 settlement statements, deeds, tax returns)

This documentation helps lenders verify your track record and place you in the right experience tier—which directly impacts the financing terms you'll qualify for. As you can see, moving up through these tiers puts more borrowing power in your hands while lowering your minimum ROI requirements. That's a winning combination that makes it easier to spot profitable deals and grow your portfolio.

Submit a Detailed Scope of Work (SOW)

Your Scope of Work is one of the most important pieces of your loan application. Think of it as your renovation roadmap—a comprehensive document that spells out every detail of your project. And here's a pro tip: organize it by trade or building system, not room-by-room.

Why Trade-Based Organization Matters:

When you structure your SOW by trade (demolition, plumbing, electrical, HVAC, drywall, flooring, painting), you set yourself up for success in several key ways:

Faster Draw Reimbursements: Finish all the electrical rough-in throughout the house? Request a draw for that entire trade right away—no waiting for individual rooms to be 100% complete.

Better Cash Flow Management: Separating trades into "rough" and "finish" phases means you get reimbursed for rough work (framing, plumbing rough-in, electrical rough-in) before you need to shell out for finish materials and labor.

Clearer Progress Tracking: Lenders and inspectors can verify completion percentages much more easily when work is organized by trade. The result? Faster draw approvals.

More Accurate Budgeting: This approach matches how contractors actually bid and complete work, which means fewer surprises and budget headaches down the road.

Essential SOW Components:

Your Scope of Work should cover these key areas with detailed line items:

- Demolition and Disposal: What's coming out, dumpster costs, any hazardous material removal

- Foundation and Structural: Foundation repairs, beam replacements, structural reinforcements

- Plumbing: Rough-in and finish work, fixture specs, water heater details

- Electrical: Panel upgrades, rough-in wiring, fixtures, lighting specs

- HVAC: System replacement or repair, ductwork changes, thermostat upgrades

- Framing and Drywall: Wall modifications, ceiling repairs, drywall installation and finishing

- Insulation: Type and R-value specs for walls, attics, and crawl spaces

- Exterior Work: Roofing, siding, windows, doors, landscaping, hardscaping

- Interior Finishes: Flooring types and square footage, paint specs, trim work

- Kitchen and Bathrooms: Cabinets, countertops, appliances, fixtures—get specific here

- Permits and Inspections: Required permits, inspection fees, compliance costs

Keep in mind: the appraiser uses your SOW to determine the After Repair Value (ARV) of the property. Being thorough and accurate here directly impacts your loan amount and overall deal success. An incomplete or poorly organized SOW can result in a lower ARV appraisal, which directly reduces your maximum loan amount. Additionally, your SOW dictates exactly how renovation funds will be released through the draw process, so any work not included in the original SOW may not be eligible for reimbursement.

Pass the Deal Economics Test

Here's where the rubber meets the road: proving your project pencils out and delivers enough return to justify the lender's risk. This step involves a thorough appraisal and profitability analysis that looks at both where your property stands today and where it's headed after renovations.

The Appraisal Process:

Lenders will order a professional appraisal that establishes two critical values:

As-Is Value: What the property is worth right now, in its current condition—warts and all, including any damage, deferred maintenance, or outdated features.

After Repair Value(ARV): What the property will be worth once you've completed all your planned renovations, based on comparable sales of similar updated properties in the neighborhood.

The appraiser reviews your Scope of Work carefully to confirm your planned improvements make sense for the area and will actually deliver the value bump you're projecting. Appraisals must be completed within 120 days of closing and typically include interior and exterior inspections, though exterior-only appraisals may be accepted for REO properties, foreclosure auctions, or sheriff sales.

To double-check accuracy, lenders require a secondary review through a Collateral Desktop Appraisal (CDA) or Appraisal Risk Report (ARR). If the secondary review differs from the original appraisal by more than 10%, the lower value is used, or a second full appraisal may be ordered.

Minimum ROI Requirements:

Once the appraisal establishes the As-Is value and ARV, underwriters calculate your projected Return on Investment (ROI) using this formula:

ROI = (ARV - Total Project Cost) / Total Project Cost × 100

Where Total Project Cost includes:

- Purchase price

- Renovation budget

- Closing costs and fees

- Interest reserves

- Holding costs (insurance, utilities, property taxes)

The minimum required ROI varies based on your experience tier:

- Tier 1 (Inexperienced): Minimum 20% ROI required, or 1.10x debt service coverage ratio if planning to refinance into a rental loan

- Tier 2 (Beginner): Minimum 20% ROI required

- Tier 3-5 (Intermediate to Expert): Minimum 10% ROI required

These ROI thresholds are your safety net. They give you enough breathing room to handle surprise expenses, market shifts, or project delays—and still walk away with a solid profit. If your deal doesn't hit the minimum ROI for your tier, we'll have to pass, no matter how strong your credit or track record looks.

Additional Deal Economics Considerations:

ROI is just the starting point. Here's what else we look at when evaluating your deal:

Maximum Loan-to-Cost (LTC): Your loan can't exceed your tier's maximum percentage of total project cost (that's purchase price plus your renovation budget).

Maximum After-Repair Loan-to-Value (ARLTV): Your loan also can't exceed your tier's maximum percentage of the ARV—usually capped at 70-75%.

Minimum Down Payment: Buying a property under $100,000? You'll need to bring at least $10,000 to the table, regardless of your LTC percentage.

Seller Credits: These are fine and get factored into your net purchase price, but if they seem excessive, expect us to take a closer look.

Wholesaler Fees: We allow up to 20% of the original purchase price. Go higher, and you'll need to explain why—big fees can signal inflated pricing.

Structure your deal with these guidelines in mind from day one, and you'll boost your approval chances while chasing projects with real profit potential. Use OfferMarket's Fix and flip loan calculator system to run different scenarios quickly—dial in the right mix of purchase price, renovation budget, and projected ARV before you even make an offer.

Qualifying Properties: What Can You Finance with Fix and Flip Loans?

Here's the thing: not every property is a fit for fix and flip financing. Knowing what qualifies before you start hunting saves you time and headaches. Fix and flip loans are specifically designed for non-owner-occupied investment properties that meet certain criteria around property type, size, condition, and intended use. Let's break down what qualifies.

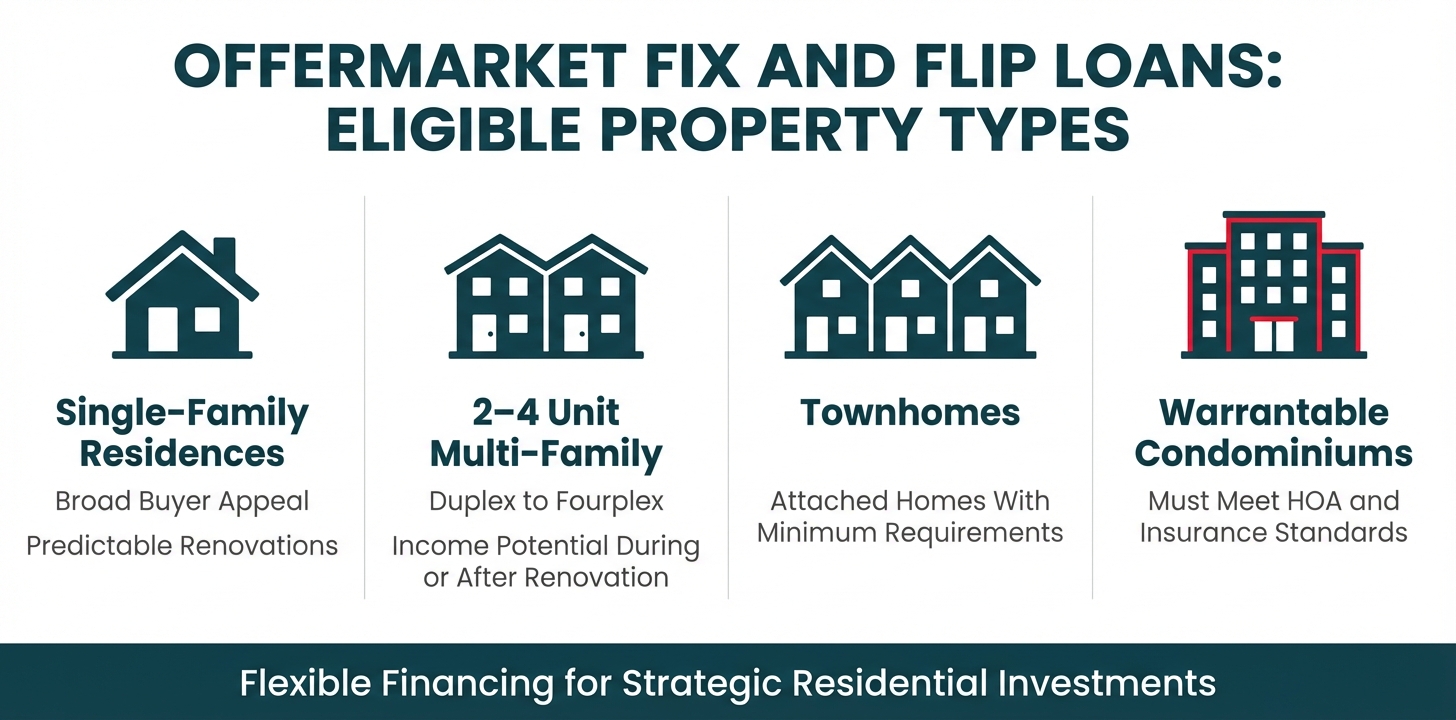

Eligible Property Types

OfferMarket's fix and flip loans can finance a wide variety of residential investment properties, including:

Single-Family Residences (SFR): These detached homes are the bread and butter of fix and flip projects—they appeal to a broad buyer pool and typically offer predictable renovation timelines.

2-4 Unit Multi-Family Properties: Duplexes, triplexes, and fourplexes are fair game here. These smaller multi-family buildings can boost your profit potential since you can generate rental income during or after your renovation.

Townhomes: Attached single-family homes in planned communities qualify, as long as they meet minimum square footage requirements and aren't tied to non-warrantable HOA structures.

Warrantable Condominiums: Condos need to meet specific warrantability standards—think adequate owner-occupancy ratios, proper insurance coverage, and a financially stable HOA. Non-warrantable condos (those caught up in litigation, with too many investors, or still under construction) typically won't make the cut.

Size and Acreage Requirements

Beyond property type, OfferMarket has specific size parameters to ensure your property fits within the residential investment sweet spot:

| Requirement | Specification |

|---|---|

| Minimum Square Footage (SFR) | 700 sq ft |

| Minimum Square Footage (Condo/Multi-Unit) | 500 sq ft per unit |

| Maximum Acreage | 5 acres |

Properties that fall below these minimum square footage thresholds are generally considered too small to generate the market value or rental income needed to make the investment worthwhile. Conversely, properties exceeding 5 acres often cross into rural or agricultural classifications, which are explicitly excluded from the program.

Ineligible Property Types

Fix and flip loans are flexible, but certain property types simply don't qualify. Here's what's off the table—and why:

5+ Unit Apartment Buildings: Once you hit five units, you're in commercial real estate territory. These properties need specialized multifamily financing.

Mixed-Use Commercial Spaces: Buildings that blend residential and commercial uses (think apartments above a retail storefront) don't fit within residential lending guidelines.

Manufactured Housing and Mobile Homes: Depreciation concerns and appraisal challenges make these properties ineligible.

Raw Land and 100% Vacant Land: No existing structure means nothing to rehabilitate—so these parcels can't be financed under fix and flip programs.

Co-ops: With co-ops, you own shares rather than real property. That structure doesn't work with traditional real estate lending.

Rural Properties: Properties in sparsely populated areas or outside metropolitan statistical areas (MSAs) typically don't qualify due to limited market liquidity and fewer appraisal comparables. Look up if your property is rural here.

Log Homes: These specialty builds come with unique appraisal and insurance hurdles that fall outside standard underwriting.

Property Condition and Renovation Scope Categories

Here's where fix and flip loans really shine: they can finance properties in rough shape—even ones traditional banks won't touch. That said, the scope of your renovation directly affects your eligibility tier, budget caps, and leverage.

We break renovation projects into four scope levels based on how your renovation budget compares to the purchase price:

| Renovation Scope | Budget as % of Purchase Price | Typical Work Included | Experience Required |

|---|---|---|---|

| Light | Less than 25% | Cosmetic updates: paint, flooring, fixtures, landscaping | All tiers eligible |

| Moderate | 25% - 50% | Kitchen/bath remodels, HVAC replacement, roof repair, window upgrades | All tiers eligible |

| Heavy | 50% - 100% | Structural repairs, foundation work, complete system replacements, major layout changes | Tier 2+ (1+ completed projects) |

| Extensive | Greater than 100% | Additions, ADUs, condo conversions, ground-up construction components | Tier 3+ (3+ completed projects) |

Planning an extensive renovation with additions, accessory dwelling units (ADUs), or conversions? You'll need to provide either valid building permits or an architect's letter confirming your proposed work is feasible and compliant. These projects are only available to experienced investors (Tier 3 and above) due to their complexity, extended timelines, and higher risk profiles.

Fire-Damaged and Distressed Properties

Our fix and flip loans are built for distressed properties that need serious work. We're talking fire damage, flood damage, neglected homes, and foreclosures. Here's the deal with fire-damaged properties: you'll need a Structural Engineer Report confirming the bones of the building are solid and safe to renovate. If the foundation or structure is beyond saving, we can't finance it—but don't worry, we'll help you spot these issues early.

How the Draw Process Works: Maximizing Cash Flow During Renovation

When you close on a fix and flip loan, the lender doesn't hand you a lump sum of cash to cover the entire renovation budget. Instead, the renovation funds are held in escrow as a "construction holdback" and released in stages as you complete specific construction milestones. Understanding this draw process is key to keeping your cash flow healthy and steering clear of costly delays during your flip.

Understanding Construction Holdbacks and Reimbursement Draws

The construction holdback model works in your favor—it protects both you and the lender by ensuring renovation funds are only released when real progress has been made on the property. Here's the straightforward breakdown: you pay your contractors and suppliers upfront, then submit a draw request to the lender with documentation showing the work is done. The lender verifies everything (usually through an inspection or photo documentation), then reimburses you for that completed milestone.

Keep in mind: this is a reimbursement system, not an advance. You'll need enough cash on hand to cover initial costs until the lender releases the funds. Smart investors plan ahead by keeping a cash reserve equal to at least one or two draw cycles—typically around 20-30% of your renovation budget in working capital.

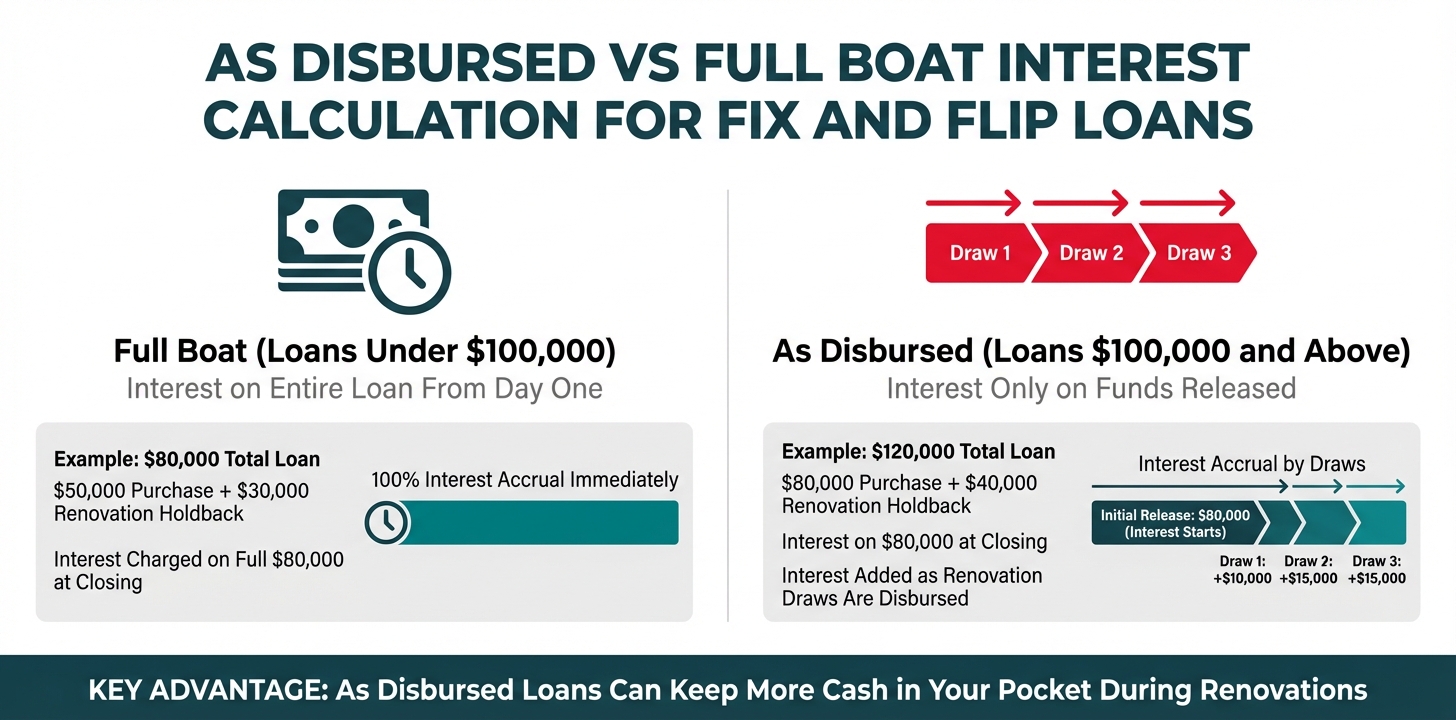

'As Disbursed' vs 'Full Boat' Interest Calculation

How interest accrues on your fix and flip loan depends on the total loan amount:

Loans Under $100,000 ('Full Boat'): Interest is calculated on the entire loan amount from day one, regardless of whether renovation funds have been disbursed. For example, if you borrow $80,000 ($50,000 purchase + $30,000 renovation holdback), you pay interest on the full $80,000 starting at closing—even though that $30,000 in renovation funds is still sitting in escrow.

Loans $100,000 and Above ('As Disbursed'): Here's where things get interesting for larger projects. You only pay interest on the money that's actually hit your account. Let's say you're working with a $120,000 loan ($80,000 purchase + $40,000 renovation holdback). At closing, you're only paying interest on that $80,000. As you complete work and request draws, interest kicks in on those additional funds. The bottom line? This structure can keep thousands of dollars in your pocket, particularly on bigger renovations where you're pulling draws over several months.

Strategic Scope of Work Structuring for Faster Reimbursement

Here's a game-changer most new investors miss: how you structure your Scope of Work (SOW) directly impacts your cash flow. The common mistake? Organizing everything room-by-room (think "Complete Kitchen" or "Complete Master Bathroom"). The problem is you're stuck waiting until every last detail in that room is finished before you can get reimbursed.

Here's the smarter play—structure your SOW by trade or building system:

- Demolition

- Framing/Structural

- Plumbing (Rough-In)

- Electrical (Rough-In)

- HVAC (Rough-In)

- Insulation

- Drywall

- Plumbing (Finish)

- Electrical (Finish)

- Flooring

- Cabinets and Countertops

- Paint

- Fixtures and Trim

The magic here is splitting trades into "rough" and "finish" phases. This means you can get paid right after rough work passes inspection—no waiting around for the finished product. Picture this: your plumber wraps up all the rough plumbing, it passes inspection, and boom—you submit your draw request for "Plumbing Rough-In" and have money back in your account within days. No more twiddling your thumbs for weeks while you wait on faucets and toilets.

The payoff? This trade-based approach can get money back in your hands 30-60 days faster than the room-by-room method. That means less cash tied up and more flexibility throughout your project.

OfferMarket's Streamlined Draw Process

Here's the good news: OfferMarket has built an online, app-driven draw process that cuts through the traditional headaches and costs of construction holdback management. Forget scheduling in-person re-inspections for every draw request—those can run you $150-$300 per visit and eat up 3-5 days just coordinating schedules. With OfferMarket's platform, you simply submit draw requests digitally with photo documentation and contractor invoices.

Here's what the system puts in your hands:

- Instant draw request submission through the online portal, 24/7

- Photo-based verification for most draw milestones, eliminating costly re-inspection fees

- Automated tracking of your renovation budget and remaining holdback balance

- Faster approval timelines, typically 24-48 hours for straightforward requests

For larger or more complex milestones, OfferMarket may still require a physical inspection, but the platform's efficiency means you're spending less time playing phone tag and more time running your flip like a pro.

Timeline Expectations for Draw Approvals

Knowing what to expect with draw approval timelines puts you in control of your construction schedule and cash flow:

| Draw Request Stage | Typical Timeline |

|---|---|

| Submit draw request with documentation | Same day (instant via online portal) |

| Lender review and verification | 1-2 business days |

| Physical inspection (if required) | 2-3 business days to schedule, 1 day to complete |

| Draw approval and fund release | 1-2 business days after verification |

| Total turnaround time (photo verification) | 3-5 business days |

| Total turnaround time (physical inspection) | 5-10 business days |

Most lenders, including OfferMarket, allow you to submit draw requests up to twice per month. Smart investors plan their construction schedule to hit major milestones right before their bi-weekly draw windows. This way, you're requesting reimbursement as often as possible and keeping less of your own cash tied up in the project.

Leverage Based on Experience: Max LTC and ARV Caps

Here's something powerful about fix and flip loans: your borrowing power grows as your track record does. Traditional mortgages focus mainly on your income and credit score. Fix and flip lenders? They reward your proven experience with significantly higher leverage limits. This tiered system helps you scale your operations while keeping risk in check for everyone involved.

The Five Experience Tiers Explained

Fix and flip lenders group borrowers into five experience tiers based on how many investment properties you've successfully bought, sold, or held in the last 36 months. Each tier opens the door to higher loan-to-cost (LTC) ratios, bigger renovation budgets, and more flexible underwriting.

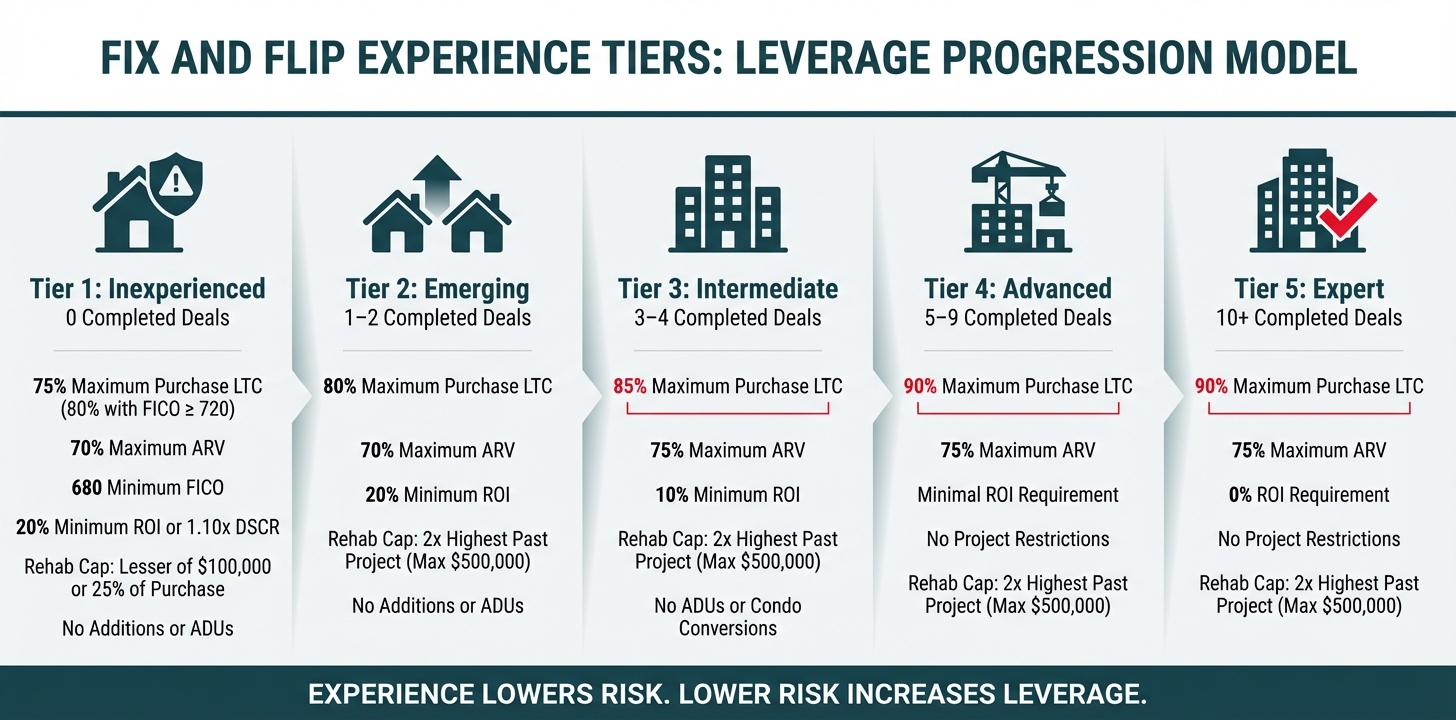

Tier 1: Inexperienced Investors (0 Completed Deals)

Tier 1 is where every investor starts—first-time flippers with no documented track record yet. Because lenders assume the highest risk with these borrowers, they impose the strictest limitations:

- Maximum Purchase LTC: 75% (can increase to 80% with FICO ≥ 720)

- Maximum ARV: 70%

- Renovation Holdback: 100% of approved budget

- Project Restrictions: No additions, extensions, or ADUs allowed. Rehab budget capped at the lesser of $100,000 or 25% of the purchase price

- Minimum FICO: 680 required

- ROI Requirement: Minimum 20% projected return or 1.10x Debt Service Coverage Ratio (DSCR) on exit

Here's what this means for you as a Tier 1 borrower: you'll need to bring 20-25% of the purchase price to the table and stick to straightforward cosmetic renovations. Think of this tier as your training ground—a place to build your track record while lenders get comfortable with your abilities. It's a smart starting point that keeps everyone protected.

Tier 2: Emerging Investors (1-2 Completed Deals)

Congratulations—you've closed your first deal or two! Now you're in Tier 2, and the doors start opening wider:

- Maximum Purchase LTC: 80%

- Maximum ARV: 70%

- Renovation Holdback: 100% of approved budget

- Project Restrictions: No additions, extensions, or ADUs. Rehab budget capped at 2x your highest past project (maximum $500,000)

- ROI Requirement: Minimum 20% projected return

Here's the exciting part: your down payment drops from 25% to 20%, and your renovation budget grows with your experience. Did your first flip have a $75,000 rehab budget? Your next project can now go up to $150,000. Your track record is literally paying off.

Tier 3: Intermediate Investors (3-4 Completed Deals)

This is where things get really interesting. Tier 3 unlocks institutional-level leverage that can supercharge your investing:

- Maximum Purchase LTC: 85%

- Maximum ARV: 75%

- Renovation Holdback: 100% of approved budget

- Project Restrictions: No ADUs or condo conversions. Rehab budget capped at 2x your highest past project (maximum $500,000)

- ROI Requirement: Minimum 10% projected return (reduced from 20%)

This tier is a game-changer for growing your portfolio. The increase to 85% LTC means you only need to bring 15% of the purchase price to the table, and the ARV cap rising to 75% opens the door to properties that need more extensive work. Plus, with the ROI requirement dropping from 20% to 10%, you'll find a much wider range of profitable opportunities within reach.

Tier 4: Advanced Investors (5-9 Completed Deals)

At Tier 4, you're stepping into maximum leverage territory, and nearly all project restrictions disappear:

- Maximum Purchase LTC: 90%

- Maximum ARV: 75%

- Renovation Holdback: 100% of approved budget

- Project Restrictions: None. You're cleared for additions and ground-up construction

- Rehab Budget: Capped at 2x your highest past project (maximum $500,000)

- ROI Requirement: Minimal to none, based on lender discretion

With just a 10% down payment, you can keep more capital free for multiple projects at once. No project restrictions? That means you're ready for complex additions, major structural work, and even building from scratch.

Tier 5: Expert Investors (10+ Completed Deals)

Tier 5 gives you the same powerful leverage as Tier 4, plus the smoothest underwriting experience available:

- Maximum Purchase LTC: 90%

- Maximum ARV: 75%

- Renovation Holdback: 100% of approved budget

- Project Restrictions: None

- Rehab Budget: Capped at 2x your highest past project (maximum $500,000)

- ROI Requirement: 0% (no minimum profitability needed)

Without ROI requirements holding you back, you can go after deals other investors simply can't—think slower markets or longer-timeline projects that build long-term portfolio value rather than quick returns.

How Experience Unlocks Higher Leverage

The tier system is built to reward your track record with greater borrowing power. According to industry analysis, most lenders loan up to 75% of ARV for standard borrowers, though experienced investors can access up to 90% for purchase financing. This tiered approach helps lenders manage risk while giving you—the proven investor—the leverage you need to grow your portfolio.

The renovation budget cap of "2x your highest past project" is there to protect you from biting off more than you can chew. If your largest renovation to date cost $200,000, your next project can have up to a $400,000 budget. It's a smart way to stretch your skills without overextending.

Strategic Scaling: The Capital Preservation Advantage

Here's where the experience tier system really shines: it keeps more cash in your pocket as you grow. Let's break it down:

Scenario A: Tier 1 Investor (0 Deals)

- Purchase Price: $200,000

- Required Down Payment: 25% = $50,000

- Renovation Budget: $75,000 (100% financed)

- Total Cash Required: $50,000 + closing costs

Scenario B: Tier 3 Investor (3-4 Deals)

- Purchase Price: $200,000

- Required Down Payment: 15% = $30,000

- Renovation Budget: $150,000 (100% financed)

- Total Cash Required: $30,000 + closing costs

See the difference? Moving from Tier 1 to Tier 3 saves you $20,000 per project while doubling your renovation budget. That extra $20,000? It can fund a down payment on a second property. Now you're running two deals with the same capital that used to cover just one.

The Path to Multiple Simultaneous Projects

This is where smart scaling really pays off. Here's a roadmap from one project a year to five or more:

Year 1 (Tier 1): Complete 1-2 projects using 25% down payments. Focus on building your track record and learning the ropes.

Year 2 (Tier 2-3): With 2-3 completed deals under your belt, you now qualify for 80-85% LTC. Your down payment requirement drops to 15-20%, freeing up 5-10% of each purchase price to fund additional acquisitions.

Year 3 (Tier 4-5): Once you've closed 5+ deals, you qualify for 90% LTC with just a 10% down payment. That means you can now run three projects at once using the same capital that covered one Tier 1 deal.

Here's the bottom line: this kind of scaling happens because lenders reward your track record. As you prove you can execute, they reduce your cash requirement per deal. Higher leverage plus lower ROI thresholds equals more deals, more markets, and smarter use of your starting capital.

How to Move Up the Tiers Faster

Want to accelerate your progress? Here's your game plan:

Document Everything: Keep thorough records of every acquisition, renovation, and sale. Lenders want to see HUD-1 settlement statements, deeds, and sale records to verify your experience.

Complete Projects Cleanly: A successful flip means you bought it, fixed it, and sold it (or refinanced into a rental). Abandoned or foreclosed projects won't count toward your tier.

Time Your Applications Strategically: Got 2 deals done and a third about to close? Wait for that sale to finalize before applying for your next loan. Moving from Tier 2 to Tier 3 can save you tens of thousands in down payment costs.

Build Your Renovation Budget Gradually: Your next project's budget cap is 2x your highest past project. So increase your renovation scope with each flip to expand what you can tackle next.

Review Your Activity Annually: We recommend sitting down once a year to review your last 36 months of real estate activity. You might spot an opportunity to wrap up an active project and unlock the next tier for your upcoming deals.

The experience tier system turns fix and flip financing into a powerful tool for scaling your portfolio strategically. By understanding how to leverage these tiers, you can systematically reduce your capital requirements, expand your project scope, and ultimately build a portfolio that generates sustainable, repeating profits.

Strategic Scaling: Leveraging Experience Tiers to Maximize Capital Efficiency

Here's what seasoned fix and flip investors know: these loans aren't just financing tools—they're strategic leverage instruments that unlock exponential scaling potential as you build your track record. The key to rapid portfolio growth lies in systematically advancing through the lender's experience tiers, which dramatically reduces your per-project cash requirements while simultaneously expanding the universe of properties you can purchase.

Capital Preservation Through Experience Advancement

The financial impact of moving from Tier 1 (inexperienced) to Tier 3+ (intermediate/advanced) is substantial. At Tier 1, you're limited to 75-80% Loan-to-Cost on the purchase price, meaning you need to bring 20-25% of the purchase price as a down payment. However, once you complete your third or fourth project and advance to Tier 3, your maximum leverage jumps to 85% LTC, cutting your required down payment to just 15%. By Tier 4 (5+ completed projects), you unlock 90% LTC, reducing your cash requirement to only 10% of the purchase price.

Let's break down the capital efficiency difference with a realistic scenario. Say you're purchasing properties at $200,000 each:

Tier 1 Investor (0-2 Deals):

- Purchase Price: $200,000

- Maximum LTC: 80%

- Required Down Payment: $40,000

- Number of Simultaneous Acquisitions with $200,000 Capital: 5 properties

Tier 3 Investor (3-4 Deals):

- Purchase Price: $200,000

- Maximum LTC: 85%

- Required Down Payment: $30,000

- Number of Simultaneous Acquisitions with $200,000 Capital: 6-7 properties

Tier 4+ Investor (5+ Deals):

- Purchase Price: $200,000

- Maximum LTC: 90%

- Required Down Payment: $20,000

- Number of Simultaneous Acquisitions with $200,000 Capital: 10 properties

This progression shows you exactly how advancing from Tier 1 to Tier 4 allows you to double your acquisition capacity with the same amount of liquid capital. Rather than tying up $40,000 per property, you're only committing $20,000, freeing up substantial reserves for unexpected repairs, permit delays, or market opportunities.

Expanding Your Deal Pipeline: The ROI Minimum Advantage

Beyond capital efficiency, experience tier advancement dramatically widens the pool of properties you can pursue with fix and flip financing. Here's the deal: at Tier 1 and Tier 2, lenders require strict profitability thresholds—typically a minimum 20-30% projected Return on Investment—to protect newer investors from overextending on thin-margin deals. But as you climb to Tier 3 and beyond, those ROI minimums drop significantly, often to 10% or even 0% for seasoned flippers.

This opens up a whole new world for your deal sourcing. Picture a property projecting only a 15% ROI after all costs. At Tier 1, that deal gets rejected—no exceptions, no matter how promising the property looks. But at Tier 4? That same property gets the green light, and you can move forward with confidence.

What does this mean for you in practical terms? Experienced investors unlock access to:

- Properties in slower-appreciation markets that still deliver solid dollar profits

- Higher-priced homes where percentage returns compress but absolute gains stay strong

- Quick-turn cosmetic flips with lower risk but modest ROI percentages

- Strategic buys in emerging neighborhoods before appreciation kicks into gear

According to recent industry surveys, 89% of home flippers plan to complete at least one fix and flip in 2025, with experienced investors targeting multiple projects at once. The average real estate investor flips between 2 to 7 homes per year, with top performers leveraging their experience tier status to maximize deal flow while keeping capital flexible.

Strategic Recommendation: Audit Your Last 36 Months

Here's a smart move that can accelerate your growth: take a close look at your real estate activity over the past 36 months. This simple audit does two important things for you:

Confirm Where You Stand: Lenders determine your experience tier based on verified deals—properties you've purchased, renovated, and sold (or held as rentals) in the last three years. Pull together your closing statements, HUD-1 forms, and sale records to get an accurate count of your qualifying projects.

Spot Easy Wins: Got projects that are nearly across the finish line but haven't closed yet? Pushing these to completion can move you up a tier right away. Say you've done 2 flips and have a third property just waiting on final inspections and listing—wrap that up, and you've unlocked Tier 3 status with 85% LTC on your next deal.

Practical Scaling Scenario: From 2 Flips to 6 Flips Annually

Let's map out what a realistic 24-month growth plan looks like for an investor at Tier 2 (2 completed projects) with $150,000 in available capital:

Months 1-6 (Tier 2 Status):

- Finish 1 project already in the works → You're now Tier 3

- Purchase Price: $180,000 at 80% LTC = $36,000 down payment

- Renovation Budget: $50,000 (100% financed)

- Total Cash Needed: ~$36,000 + closing costs

- Projects Running Simultaneously: 1

Months 7-12 (Tier 3 Status Unlocked):

- Now at Tier 3 (3 completed projects), your LTC jumps to 85%

- Purchase Price: $180,000 at 85% LTC = $27,000 down payment

- Renovation Budget: $50,000 (100% financed)

- You're Saving per Deal: $9,000 compared to Tier 2

- Projects Running Simultaneously: 2 (those savings free up cash for another project)

Months 13-18 (Tier 4 Status Unlocked):

- At Tier 4 (5 completed projects), LTC climbs to 90%

- Purchase Price: $180,000 at 90% LTC = $18,000 down payment

- Renovation Budget: $50,000 (100% financed)

- You're Saving per Deal: $18,000 compared to Tier 2

- Projects Running Simultaneously: 3-4 (better leverage means you can overlap projects)

Months 19-24 (Scaling Phase):

- Keep your Tier 4+ status by completing projects consistently

- Lower ROI requirements open doors to 12-15% return properties you couldn't touch before

- Annual Flip Target: 6-8 properties (up from 2-3 at Tier 2)

Here's the bottom line: by working your way up through experience tiers, you can transform a 2-flip-per-year operation into a 6-8-flip-per-year business without putting in more of your own money. It's all about smarter leverage and making your capital work harder for you.

Next Step: Experience Tier Consultation

Ready to fast-track your growth? Book a consultation with OfferMarket's loan advisory team, and we'll dig into your last 36 months of real estate activity together. Here's what we'll tackle:

- Pin down your current experience tier with precision

- Spot any projects you can wrap up quickly to bump up your tier status

- Structure your next deal to squeeze maximum leverage from your updated tier

- Map out a 12-24 month scaling plan that fits your capital situation

Get your instant quote here and see exactly how your track record translates into better borrowing power and smarter capital use.

Get Your Instant Quote for Fix and Flip Loans Today

Here's the truth: waiting weeks for financing answers is one of the biggest roadblocks to scaling your real estate investment business. That's why we built a fix and flip loan process that cuts through the traditional red tape—because when you're competing for properties in today's market, every day counts.

Why OfferMarket's Process Changes the Game

2-Minute Quote and Qualification: Forget the days of endless back-and-forth with lenders. With OfferMarket, you can get quoted and qualified for a fix and flip loan in under 2 minutes. Apply here and see for yourself. The moment you submit, we create your dedicated Loan File and our processing team gets to work immediately—no guessing games, no radio silence.

Lightning-Fast Closings: Pay your appraisal fee the same day you apply, and we can typically get you to the closing table within 1-3 weeks. What does that mean for you? You can go head-to-head with cash buyers instead of watching deals disappear during a 45-day bank approval marathon. As LendSure points out, speed isn't a luxury for investors—it's a necessity when opportunities are time-sensitive.

Desktop Appraisals Where Applicable: When your property and profile qualify, we use desktop appraisals to speed things up and save you money upfront. And when a full appraisal is needed, we make sure you're getting the maximum Loan-to-Value (LTV) your experience level qualifies for—so you keep more capital working for you.

Online App-Driven Draw Process: Say goodbye to scheduling headaches and waiting around for reimbursements. Our digital draw system lets you submit your documentation online, get faster approvals, and receive funds for completed work without the delays and inspection fees that chip away at your renovation budget. This feature alone can save you thousands of dollars per project while keeping your cash flow healthy throughout the construction phase.

Integrated Ecosystem: OfferMarket doesn't just provide loans—we've built a complete platform that connects loans, property listings, and insurance services in one place. This means you can source your next deal, secure financing, and protect your investment without juggling multiple vendors and platforms. It's everything you need under one roof.

OfferMarket Loans

Check your rate

60 seconds · no credit pull