*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The Potential of a DSCR Loan for Single Family Homes

Last Updated: January 15, 2025

A DSCR (Debt Service Coverage Ratio) loan is a type of real estate financing where loan eligibility is based on the property's rental income—not the borrower's personal income. It's designed specifically for non-owner-occupied investment properties, like single-family rentals. If you’re investing in a single-family home to rent out, a DSCR loan can help you qualify based on the property's cash flow alone, without requiring W-2s or tax returns.

What is a DSCR Loan for Single Family Homes?

A DSCR loan for single family homes is a specialized financing option that assesses your ability to cover debt obligations based on the income generated by the property itself. Unlike traditional loans that primarily consider your personal income and credit history, a DSCR loan for single family homes focuses on the property's financial performance. This means that if you're investing in a single family home to rent out, the rental income becomes a key factor in securing your loan.

Investment Property Use Only

It’s important to note that DSCR loans for single-family homes are strictly for investment properties only. You cannot use a DSCR loan to purchase a primary residence, second home, or vacation home. The property must be rented to generate income, and lenders will not approve these loans for personal use occupancy.

Investment Property Use Only

It’s important to note that DSCR loans for single-family homes are strictly for investment properties only. You cannot use a DSCR loan to purchase a primary residence, second home, or vacation home. The property must be rented to generate income, and lenders will not approve these loans for personal use occupancy.

Why Choose a DSCR Loan for Single Family Homes?

Choosing a DSCR loan for single family homes offers several advantages that cater specifically to real estate investors:

- Simplified Qualification: Since the loan is based on the property's income, you might qualify even if your personal income is limited.

- Flexible Terms: DSCR loans often come with more flexible terms compared to conventional loans, allowing for better cash flow management.

- Investment Focused: These loans are tailored for investment properties, making them ideal for those looking to build a real estate portfolio.

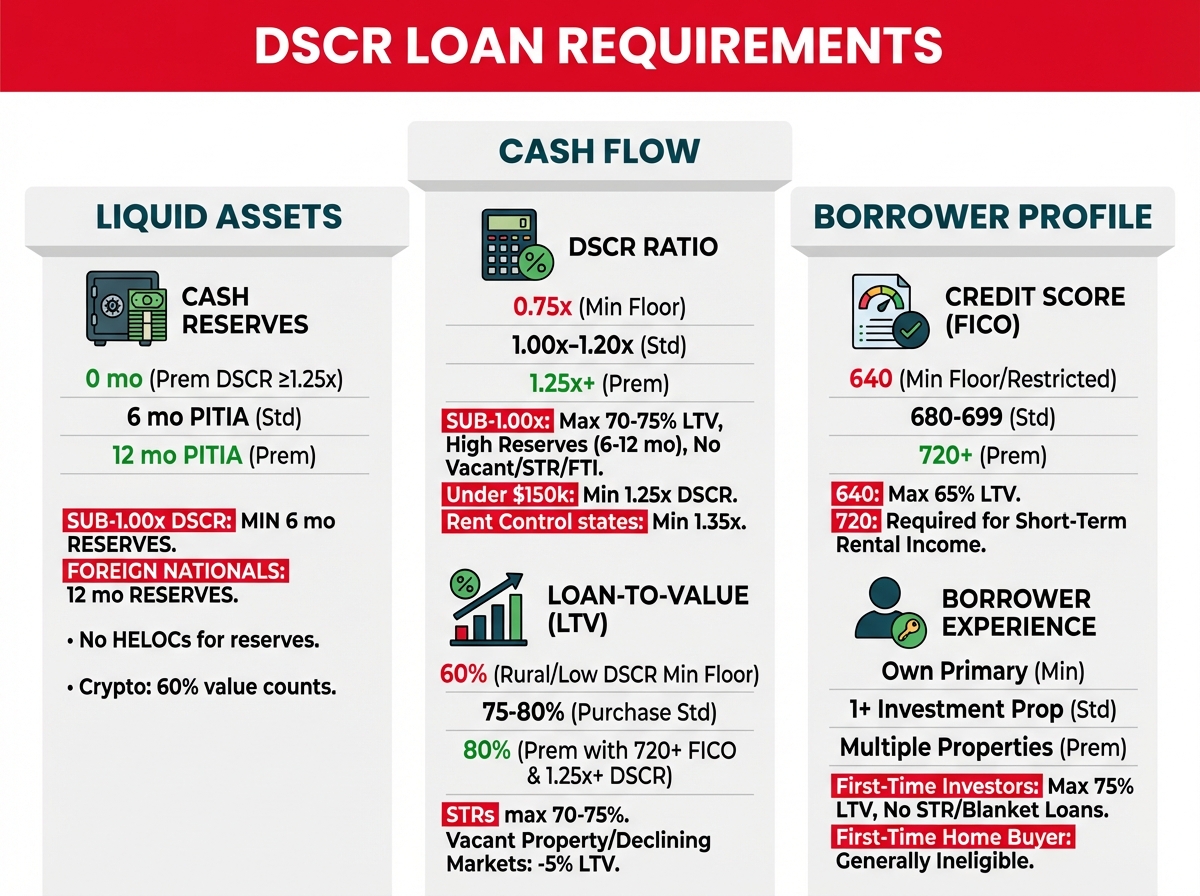

Eligibility Criteria for a DSCR Loan for Single Family Homes

Understanding the eligibility requirements is essential when considering a DSCR loan for single family homes. By thoroughly comprehending these criteria, you can better prepare your application and increase your chances of approval. Here are the key factors lenders typically evaluate:

1. Property Income

The rental income generated by the single family home is a cornerstone of your eligibility for a DSCR loan for single family homes. Lenders will meticulously assess whether this income is sufficient to cover the loan payments and any associated expenses. Here's how you can ensure your property income meets the necessary standards:

- Current Rental Income: Provide detailed documentation of the current rental income. This includes lease agreements, rental payment history, and any additional income streams associated with the property, such as parking fees or laundry services.

- Market Rent Analysis: Lenders may conduct a market rent analysis to determine if the current rental income aligns with the prevailing market rates. Demonstrating that your property is rented at or above market rates can strengthen your application.

- Occupancy Rates: High occupancy rates are favorable indicators of steady rental income. Ensure you have a history of low vacancy rates, which reassures lenders of the property's income stability.

- Future Rental Potential: If the property is newly acquired or recently renovated, outline the potential for increased rental income. This could include planned upgrades, improved amenities, or positioning the property in a high-demand area.

- Market Rent Appraisal: For vacant or newly acquired properties, lenders often rely on a market rent schedule as part of the property appraisal to estimate rental income. If the property already has tenants, lenders may use the current lease agreement, but it must reflect market rates.

2. Debt Service Coverage Ratio (DSCR)

The Debt Service Coverage Ratio (DSCR) is a critical metric in securing a DSCR loan for single family homes. It measures the property's ability to generate enough income to cover its debt obligations. Here's a deeper dive into understanding and optimizing your DSCR:

- Target DSCR: Most lenders prefer a DSCR of at least 1.20 to 1.25 for DSCR loans for single family homes. This ensures a safety cushion, accounting for potential fluctuations in rental income or unexpected expenses.

- Improving DSCR: If your DSCR is below the preferred threshold, consider strategies to enhance it. This could involve increasing rental income through property upgrades, reducing operating expenses by optimizing management practices, or refinancing existing debts to lower interest rates.

- Impact of DSCR on Loan Terms: A higher DSCR not only improves your chances of loan approval but can also lead to more favorable loan terms, such as lower interest rates and higher loan amounts. Lenders view a robust DSCR as a sign of lower risk.

3. Property Condition

The condition of the single family home plays a significant role in your eligibility for a DSCR loan for single family homes. Lenders want to ensure that the property maintains its value and continues to generate rental income. Here's what to focus on regarding property condition:

- Property Inspection: A thorough property inspection is typically required. The inspection assesses the structural integrity, electrical systems, plumbing, roofing, and overall maintenance of the property. Addressing any identified issues beforehand can prevent delays in the loan process.

- Appraisal Value: An independent appraisal will determine the current market value of the property. Ensuring that your property is in good condition can positively influence its appraisal value, which in turn affects the loan amount you may qualify for.

- Maintenance Records: Providing comprehensive maintenance records demonstrates that the property is well-cared for. Regular upkeep reduces the risk of significant repairs in the future, assuring lenders of the property's long-term viability.

- Renovations and Upgrades: If you've recently renovated or upgraded the property, highlight these improvements. Enhancements such as modern kitchens, updated bathrooms, energy-efficient windows, and new appliances can increase rental desirability and justify higher rental rates.

- Compliance with Local Regulations: Ensure that the property complies with all local building codes and regulations. Non-compliance can pose risks and potentially hinder your loan approval.

4. Investment Experience

While not always mandatory, having experience in real estate investment can be advantageous when applying for a DSCR loan for single family homes. Lenders may view experienced investors as lower-risk borrowers due to their proven track record. Here's how investment experience can influence your eligibility:

- Track Record: Demonstrating a history of successful real estate investments can bolster your application. Provide evidence of past property acquisitions, rental income stability, and effective property management.

- Property Management Skills: Effective management of rental properties is crucial for maintaining consistent income and minimizing vacancies. If you manage your properties efficiently or have a professional property manager in place, highlight this in your application.

- Understanding of Market Dynamics: Showcasing your knowledge of the local real estate market, including trends, demand, and property values, can reassure lenders of your ability to make informed investment decisions.

- Financial Management: Experience in handling property finances, such as budgeting for maintenance, managing cash flow, and optimizing expenses, demonstrates your capability to maintain a healthy DSCR.

- References and Testimonials: Providing references from previous lenders, property managers, or tenants can add credibility to your investment experience. Positive testimonials can strengthen your application by showcasing your reliability and professionalism.

5. Personal Financial Health

In addition to the primary eligibility criteria, lenders may also consider your overall financial health when evaluating a DSCR loan for single family homes. While the focus is on the property's income, your personal financial situation can still influence the decision. Here's what to consider:

- Credit Score: While DSCR loans don’t require income verification like W-2s or tax returns, your credit score is a critical qualifying factor. Lenders typically require a minimum score of 620, but scores of 680 or higher generally receive the most competitive rates and higher LTV allowances. A strong credit score reflects lower risk and leads to better loan terms.

- Debt-to-Income Ratio (DTI): Although DSCR loans prioritize property income, lenders may still assess your personal DTI to ensure you aren't overleveraged. Maintaining a healthy DTI demonstrates your ability to handle additional debt.

- Cash Reserves: Having sufficient cash reserves can provide a safety net for unexpected expenses or temporary rental income gaps. It signals to lenders that you are prepared to manage potential financial challenges.

- Legal and Tax Considerations: Ensure that there are no outstanding legal issues or significant tax liabilities that could affect your ability to secure and repay the loan.

6. Down Payment and Property Limitations

DSCR loans for single-family homes typically require a down payment of 20% to 35%. There are no zero-down options for these investment-focused loans. In addition, not all properties qualify: homes located in rural or low-density areas may be ineligible based on the appraisal and lender guidelines. Most DSCR lenders, including OfferMarket, also require the borrower to use a business entity (LLC or Corporation) to hold title to the property.

6. Down Payment and Property Limitations

DSCR loans for single-family homes typically require a down payment of 20% to 35%. There are no zero-down options for these investment-focused loans. In addition, not all properties qualify: homes located in rural or low-density areas may be ineligible based on the appraisal and lender guidelines. Most DSCR lenders, including OfferMarket, also require the borrower to use a business entity (LLC or Corporation) to hold title to the property.

Calculating the Debt Service Coverage Ratio (DSCR)

Understanding how to calculate the DSCR is fundamental when applying for a DSCR loan for single family homes. Here’s a simple formula to help you:

DSCR = Rent / PITIA

PITIA: Principal + Interest + Taxes + Insurance + Association Dues.

A DSCR of 1.0 means the property generates just enough income to cover the debt service. Typically, lenders prefer a DSCR of 1.25 or higher to ensure a cushion.

Example Calculation

| Metric | Amount |

|---|---|

| Monthly Rent | $2,500 |

| Principal | $800 |

| Interest | $600 |

| Taxes | $200 |

| Insurance | $150 |

| Association Dues | $50 |

| Total PITIA | $1,800 |

| DSCR (Rent / PITIA) | 1.39 |

In this example, the DSCR is 1.39, meaning the property generates 39% more income than is needed to cover its debt service—well above the minimum threshold many lenders require.

Benefits of a DSCR Loan for Single Family Homes

Delving deeper into the advantages, a DSCR loan for single family homes can significantly enhance your investment strategy:

1. Enhanced Purchasing Power

With a DSCR loan for single family homes, you can potentially qualify for larger loan amounts since the property's income is a primary consideration. This means you can invest in higher-value properties, increasing your rental income and overall return on investment.

2. Improved Cash Flow Management

DSCR loans often come with terms that are more favorable for cash flow management. Lower interest rates and longer repayment periods can help ensure that your rental income comfortably covers loan payments, reducing financial stress.

3. Diversification of Investment Portfolio

Investing in single family homes using DSCR loans allows you to diversify your real estate portfolio. Diversification helps mitigate risks associated with market fluctuations and economic downturns, providing a more stable investment landscape.

4. Potential Tax Benefits

Real estate investments come with various tax benefits, such as deductions for mortgage interest, property taxes, and depreciation. A DSCR loan for single family homes can maximize these benefits, enhancing your overall financial position.

The Application Process for a DSCR Loan for Single Family Homes

Navigating the application process for a DSCR loan for single family homes involves several steps. Here’s a comprehensive guide to help you through:

Step 1: Prepare Your Financial Documents

Gather all necessary financial documents, including:

- Property income statements (rental income, vacancy rates)

- Operating expenses (maintenance, property management fees)

- Personal financial statements (if required)

- Credit history and score

Step 2: Calculate Your DSCR

Use the DSCR formula to ensure your property meets the minimum requirements. A higher DSCR increases your chances of loan approval and favorable terms.

Step 3: Select a Suitable Lender

While you shouldn’t compare lenders in your content, it's important to choose one that specializes in DSCR loans for single family homes. Look for lenders with experience in investment property financing.

Step 4: Complete the Application

Fill out the loan application form, providing all required information about the property and your financial status. Be thorough and accurate to avoid delays.

Step 5: Underwriting and Approval

The lender will review your application, assess the property's income potential, and verify all provided information. This stage may involve property appraisals and inspections.

At OfferMarket, you can receive an instant quote for your DSCR loan without a credit pull, making it easy to explore your options risk-free. We specialize in DSCR loans for single-family rentals and other 1–4 unit residential properties, and we support investors looking to finance multiple properties or use a Fix and Rent strategy for rehab projects.

Step 6: Closing the Loan

Once approved, you'll move to the closing process, where you'll sign the loan agreement and finalize the purchase or refinancing of your single family home.

At OfferMarket, you can receive an instant quote for your DSCR loan without a credit pull, making it easy to explore your options risk-free. We specialize in DSCR loans for single-family rentals and other 1–4 unit residential properties, and we support investors looking to finance multiple properties or use a Fix and Rent strategy for rehab projects.

Managing Your DSCR Loan for Single Family Homes

Successfully managing a DSCR loan for single family homes requires diligent financial oversight and proactive property management. Here are some tips to help you stay on track:

Monitor Property Performance

Regularly review the rental income and operating expenses to ensure your property remains profitable. Address any issues promptly to maintain a healthy DSCR.

Maintain a Reserve Fund

Having a reserve fund can help you cover unexpected expenses, such as repairs or vacancies, ensuring that your debt service remains covered even during challenging times.

Optimize Property Management

Effective property management can enhance tenant satisfaction, reduce vacancy rates, and control operating expenses, all of which positively impact your DSCR.

Reevaluate Loan Terms Periodically

As your property appreciates and your DSCR improves, consider refinancing options to secure better loan terms, reduce interest rates, or access additional funds for further investments.

Common Challenges and How to Overcome Them

While a DSCR loan for single family homes offers numerous benefits, it's essential to be aware of potential challenges and strategies to overcome them:

1. Fluctuating Rental Income

Rental income can vary due to market conditions or tenant turnover. To mitigate this, conduct thorough market research before investing and maintain a robust tenant screening process to ensure consistent occupancy.

2. Managing Operating Expenses

Unexpected expenses can impact your DSCR. Keep a detailed budget, prioritize maintenance to prevent costly repairs, and consider hiring a professional property manager to control costs effectively.

3. Maintaining a Strong DSCR

A declining DSCR can jeopardize your loan status. Regularly monitor your financial metrics, adjust rental rates as needed, and explore ways to increase property income without significantly raising expenses.

Maximizing the Benefits of a DSCR Loan for Single Family Homes

To fully leverage a DSCR loan for single family homes, consider the following strategies:

Invest in High-Growth Areas

Choose locations with strong rental demand, economic growth, and potential for property value appreciation. This ensures your investment remains profitable and your DSCR remains healthy.

Enhance Property Value

Invest in property improvements that can justify higher rental rates. Upgrades such as modern kitchens, updated bathrooms, and energy-efficient features can attract higher-paying tenants.

Diversify Your Investments

Use the capital from your DSCR loan to invest in multiple single family homes. Diversifying across different locations and property types can spread risk and increase overall returns.

Stay Informed About Market Trends

Keep abreast of real estate market trends, interest rate changes, and economic indicators. This knowledge allows you to make proactive decisions to optimize your investment strategy.

Final Thoughts

Embarking on the journey of real estate investment with a DSCR loan for single family homes can be a game-changer. It empowers you to leverage the income potential of your properties, offers flexible financing options, and sets the stage for long-term financial success. By understanding the intricacies of DSCR loans, preparing diligently, and managing your investments wisely, you can unlock unparalleled opportunities in the real estate market.

Take control of your investment future today with a DSCR loan for single family homes and watch your real estate dreams become a reality.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull