*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

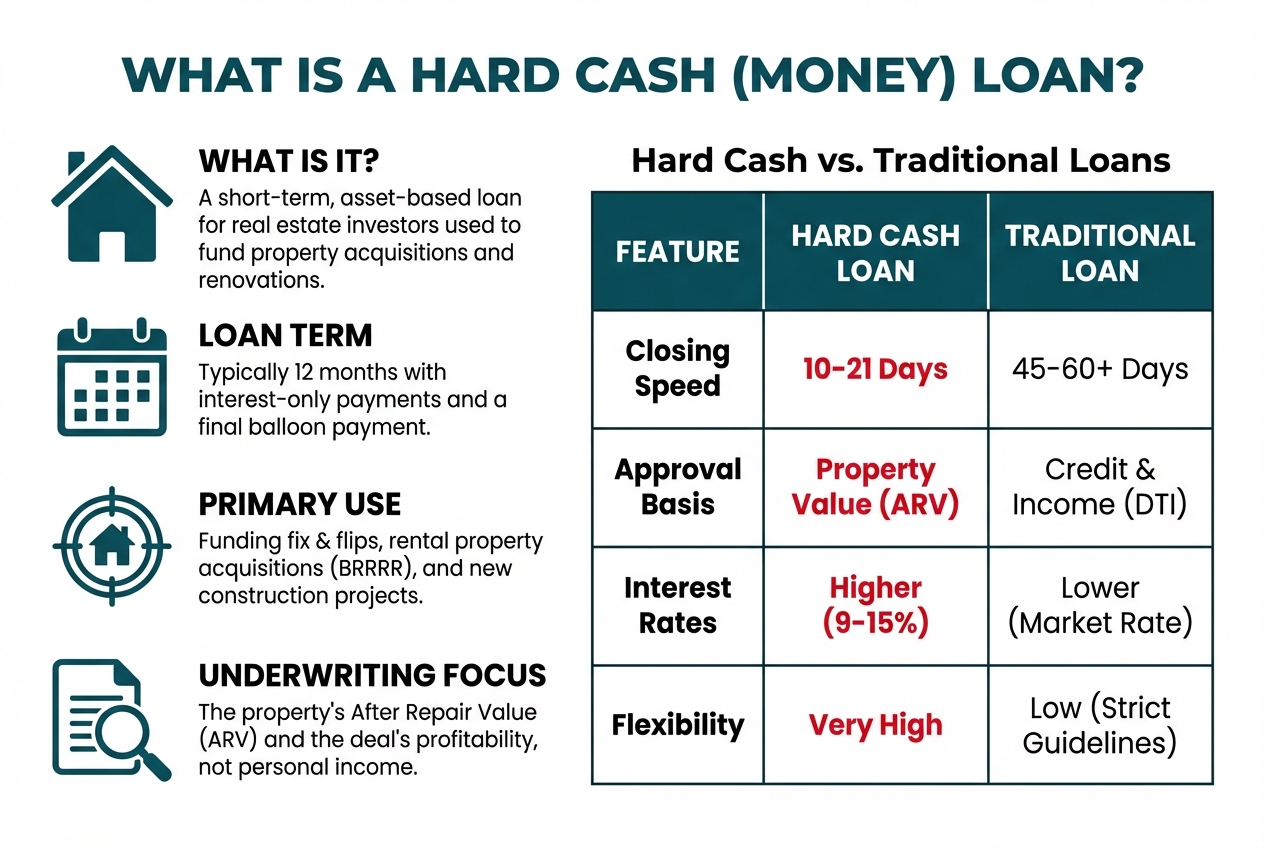

DSCR Loan Pros and Cons

Last updated: July 10, 2024

Instant Quote With No Credit Pull (OfferMarket-Specific)

OfferMarket offers an instant DSCR loan quote in under 2 minutes with no credit pull. This is a unique benefit of OfferMarket and not standard across all DSCR lenders. Other lenders may require full applications and hard credit pulls upfront.

DSCR Loan Pros

No personal income verification -- you will never be asked for W2 or tax returns. DSCR loans are based on the cash flow potential of the rental property. If the appraised or actual income applicable to the property can cover debt payments (as well as taxes, insurance and HOA) with some additional margin then it will most likely qualify. Most common approach to evaluating this, is using what is called debt service coverage ration (DSCR) and hence why these loans are referred to as DSCR loans. This points is paramount for full time real estate investors that no longer have W-2 income and thus derive all of their earning from their real estate portfolios.

Fast close -- OfferMarket's target is 20 - 25 days and we frequently close in under 20 days. Many bank based commercial loans could take multiple months to close which exposes the borrower to the changing guideline risk, where during the process, bank's management changes their lending guidelines creating a 'moving-goalpost' problem for borrowers where certainty of a close diminishes the longer the loan is outstanding.

Certainty of closing -- if you and the property meet DSCR loan program guidelines, it is nearly certain that your loan will be funded. As mentioned in the previous bullet point, the speed of finishing the loan is related to certainty of getting to the finish line. The faster loan processing and underwriting takes place the higher is the chance that loan will be funded. Changing credit environment that is influenced by economic conditions, credit market conditions and housing market conditions makes loan underwriting from large financial institutions susceptible to changing guidelines that trickle from upper management and influence borrower qualifications for ultimately securing the funding. For example, if a borrower has a credit score that is on a border of different interest rate terms, and credit market condition deteriorate, the loan terms could be updated to a higher interest rate to compensate the bank for higher perceived borrower credit risk, which in turn can cause the loan number no longer to 'pencil' and provider adequate profit margin for the borrower, thus the borrower has less incentive to finish the loan they have started. At non-bank institutions, credit standards are often less dynamic and the reputational risk of the firm is much higher thus they are more inclined to honor initial deal terms compared to large bank insitutions where borrowers are seen as dime-a-dozen rather then valuable clients with whom establishing long term relationships at a sacrifice of few basis points is seen as a worth trade-off.

No seasoning cash out refi -- if you're buying in cash or with hard money, you can cash out refi at up to 75% LTV. Other loan products have much stricter time and LTV requirements when it comes to refinances, which will slow down investors timelines to grow their portfolio. For example, if other loans, such as a bank loans, are used for refinance purposes to pull money out of existing portfolio to power the growth and acquire more properties, if seasoning requirements are 3 to 6 months, after four cycles of refinances the borrower that uses bank loans vs DSCR loans will be 1 to 2 years behind the borrower that exclusively using DSCR loans.

Higher LTVs -- In the same way as above example, bank loans refinances are often at a lower LTVs then DSCR loans, which ultimately compounds into slower growth for the borrower/investor where after several cycles of acquisitions and refinances borrower that uses bank loans falls significantly behind the borrower/investors that uses DSCR loans because the refinance LTVs allow them to pull out less cash from each property, thus limiting their ability to acquire new properties.

No limits on portfolio size -- Conventional bank loans ofter have clearly defined tiers of portfolio size of the borrowers. For example, we encounter investors that were able to secure attractive bank loans for first one to two properties in their portfolio using bank loans and their W-2s. This is absolutely a great approach if you are just starting out as a real estate investor and you still have a W-2 job (an approach we recommend to some of our would-be borrowers). However, as these real estate investors start to grow their portfolios beyond 2 or 3 properties, their bank point of contacts start to deny their loan requests because banks impose hard limits on the size of portfolios applicable to "conventional rental loans" they can extend. On the other hand, DSCR loans qualifications only focus on a single property at a time and its ability to cover debt service. We do ask our borrowers to share figures regarding the rest of their portfolio and debt obligations they have on those properties but its very rarely a limiting factor, quite the opposite, large portfolio ownership shows us that the client is organized, savvy and experienced and thus presents a lower credits risk from lender perspective. Additionally, our credit standards allow us to provide attractive discounts to experienced borrowers with large portfolios because of larger collateral base they present as well as opportunity to power their continued growth into the future.

OfferMarket requires borrowers to hold title in a business entity such as an LLC or Corporation, which is a standard for business-purpose loans. Individual borrower name/title is typically not eligible.

Hard money lender competitiveness - Banks, conventional real estate loan providers, often aren't very sensitive to competition in the rental loan niche because large percentage of their loans and profit are derived from more main stream loan products such as retail mortgage loans (owner-occupied), car loans and commercial real estate loans, while rental and landlords loans are just a tiny part of their book. Due to this arrangement, banks have a low incentive to compete with other banks provide attractive terms to their borrowers in this specific niche. In contrast, hard money lenders that exclusively specialize in DSCR loans and have DSCR loans as their 'bread-and-butter' product, have a huge incentive to provide the best possible loan terms to their borrowers and win over any additional borrowers with incentive deals to kick off long term relationships with each additional client.

DSCR Loan Cons

Higher fees -- Since DSCR loans are often offered at a smaller scale (total issuance volume) and by smaller providers, they usually command higher closing and underwriting fees compared to the fees charged on conventional loans from larger providers at larger scales. As in many other places in the economy, 'economies of scale' of a product are beneficial to the end consumers. In the case of DSCR loans, its a product that is considered a niche product because total volume issuance of the loans is relatively small in dollar size amount and number of loans issued. Due to this, providers have less profit to reinvest in automation and systemization of underwriting of the loan product and have to endure a more manual process which translates into higher fees for the borrowers to cover fixed costs. Additionally, since many providers are not bank sized institutions, with additional revenue lines, there aren't additional revenue inflows that can be used to scale these loan products thus causing higher comparative fees due to the level of manual, human driven work required to collect borrower's information, underwrite and cross verify the information and ultimately issue the loan. Many brokers and private lenders charge higher interest rates and higher fees than the best DSCR lenders. OfferMarket is buckling this trend by heavily automating many of the underwriting flows in order to deliver the lowest fees across the industry for the benefit of it borrowers. We invite any borrower, to get a get an instant quote from us (no sign up necessary) and compare our transparently stated fees against any other quote they may have

Down payment percentage -- While many retail real estate loans may have attractively low requirements for down payments, DSCR loans typically have stricter requirements. Some retail loans may have downpayment requirements as low as 0%-3% down to enter into a loan, since most DSCR loans are business purpose loans, 20%-30% down payments are more typical (75-80 LTV). This is due to the business purpose (and thus more speculative) nature of these loans where lender is seeking to protect their investment and requiring borrower to have more 'skin-in-the-game' to show commitment to the deal. While this requirement might seem draconian in nature, in our lending experience, its been a great barrier to prevent bad outcomes. Higher down payment requirements, as well as, liquidity requirements (cash or cash-equivalent balances) shown by borrowers served as defense mechanisms to help these borrowers avoid back outcomes such as defaults if their deal assumptions weren't met, such as deal profitability or issues with securing tenants. At OfferMarket we try hard to disspell the myth of no down payment DSCR loans because such a loans, if existed would put borrowers into dangerous situation where they would be highly levered with debt with no room for any volatility in the environment they operate in. For example, if a borrower got a no down payment DSCR loan, they would most likely have to find the tenant to pay the highest possible rent for their target area, if they failed to do so, the property would produce a negative cashflow each month putting strain on borrower's finances and reduce their ability to hold the property until the time when rents could increase to provide a positive margin for the borrower. Having an 80 LTV or 75 LTV loan would require borrower to find a tenant with more appropriate (lower) market rent paying ability to cover the debt payments, making it more likely for the borrower to hold on to the property for the long term, at which point rents and property values could increase.

Higher minimum credit scores -- Conventional and retail lending products often have lower credit score requirements than business purpose DSCR loans. This is once again a protective feature of these loans to prevent bad outcomes. Since these loans are not used to fund owner occupied properties and the borrower must be able to secure a tenant to generate rent to cover debt service, higher minimum credit score (while not a perfect metric by any means) is an indicator or a proxy of borrower's organizational skills and business savvy. Conventional wisdom in the DSCR lending industry goes something like "if a borrower can't manage something as simple as a credit score, how will they be able to successfully juggle all the tasks necessary to manage their real estate portfolio" (getting loans, securing tenants, dealing with maintenance requests, prospecting new deals, etc.). At OfferMarket, we prefer to work with clients that have a credit score above 680, while clients that have a credit score above 720 get our best terms based on the credit score metric, such as lower interest rate and lower required DSCR for their deal to be eligible. We often get asked, why does my credit score matter if DSCR loan is supposed to look at the profitability of the property? Borrower's credit score matters because properties are not profitable automatically, they are only profitable if the borrower can execute on their plan to turn that property into a cash flowing rental. Credit score is a great proxy to be able to judge how 'serious' and 'competent' a borrower is when it comes to business dealings because it is often the simplest thing to manage out of all the other issues that may arise when engaging in the business of landlording. Accordingly, credit score is an accurate proxy for the guarantor's ability to avoid late payments, default and foreclosure. While OfferMarket's minimum credit score is 660, there may be other DSCR lenders with guidelines that allow credit score as low as 620. Given the importance of credit score, there is generally a substantial reduction of LTV and may even be an increase in interest rate for borrowers with credit scores below 720.

➤ *Note: Credit score requirements vary by lender. While OfferMarket requires a minimum score of 660 for DSCR loans, some lenders may allow scores as low as 620. Higher credit scores typically yield better terms such as lower rates and higher LTV.*

Minimum DSCR metric - Arguably the most important metric for qualifying for DSCR loans is the debt service coverage ratio (DSCR). It usually ranges from 1.5 to 1 among all lenders in our network. For OfferMarket, our guideline DSCR cut off is 1.2 for lower credit score borrowers (below 720) and 1.1 for borrowers that have a credit score above 720 (subject to future changes in our underwriting guidelines and getting an instant quote will be a better source of information then this article since it might not be updated for changing guidelines as fast as our quoting engine). Lower debt service coverage ratio is more permissive then higher one. A good way to think about it is, if DSCR is 1, that means income from the property will completely cover debt service with no room to spare. 1.2 DSCR will have a 20% profit margin after covering all the debt service. The higher the ratio the better it is for the investor. If you want to quickly calculate a DSCR ratio on any deal that you are considering, you can try our DSCR calculator.

Higher interest rates - Once again, due to higher risk of DSCR loans and their more speculative, business purpose vs owner occupied (conventional, retails) loans, they usually carry a higher interest rate to compensate lenders for higher risk. The down side of higher interest rates is that more deals won't 'pencil' in and provide the borrower with enough profit margin to take them on. As mentioned in the previous bullet point above, DSCR is a great way to calculate a potential profit margin on a deal as well as debt obligation which factors in the interest rate on the loan. At OfferMarket we understand how important low interest rate is to our borrowers, so we don't charge an additional spread on top of the interest rate that we offer, a common practice employed in the industry by other lenders. We maintain an interest rate index so our borrowers can always stay up to date on the interest rate trends in the industry and have a better transparency into the rates that we offer.

OfferMarket calculates DSCR interest rates using the 5-Year US Treasury yield + credit spread, which varies based on borrower credit score, LTV, and DSCR. Other lenders may use different pricing models and add undisclosed markups.

At OfferMarket, typical origination fees range from 0.5 to 2 points with no added underwriting or processing fees. However, fees vary widely between DSCR lenders.

Prepayment penalties - Retail and conventional loans typically don't have a prepayment penalty feature. Prepayment penalty is a loan covenant that mandates an extra payment if the loan is paid of early, before the expected maturity. Prepayment penalties are meant to compensate lenders (and ultimately loan investors that provide capital for the loan) in case borrower want to pay them off early and lenders face what is called a 'reinvestment' risk where the capital allocated to this loan must be re-deployed else where and usually at a lower interest rate, since early prepayments are usually triggered by decrease in interest rates and borrower finding alternative sources of capital at a lower rate that makes it attractive to prepay an existing loan. At OfferMarket we have a range of prepayment penalty options to provide our borrowers with flexibility they need, however, the lower the prepayment penalty chosen, the higher the initial interest rate assigned to a loan to compensate our capital providers for the aforementioned 're-investment' risk.

Low consumer protection - The factors mentioned above such as higher down payments, higher interest rates, prepayment penalties are all features that reduce borrower's protection in a DSCR transaction in favor of lender protection. This is in contrast with retail mortgages where U.S. government plays an active role to protect lenders from borrower defaults and in exchange mandates certain consumer protection features such as lower down payments, lower rates and no prepayment penalties. This is because DSCR loans are 'business-purpose' loans where government won't step in to protect lenders and borrowers are assumed to be sophisticated business professionals that have deeper understanding of the loan terms they are committing to then retail individuals that are signing a personal mortgage for an owner occupied dwelling (non-business purpose loan). Due to perceived sophistication of the DSCR borrowers, there are less consumer protections, because by definition this type of loan is more speculative and carries a higher risk of loss for the borrower and requires more business savvy for successful execution and completion.

Mortgage experience requirement - while DSCR loan guidelines vary depending on the institutional investor that purchases the DSCR loan from the originating DSCR lender, it is generally required that among the members of the borrowing entity, there is a guarantor that has at least one (1) mortgage with at least 24 months of history and no late payments within the past 12 months. This "trade line" requirement is usually verified via trimerge credit report, however, it is fairly common for the borrower to have a business purpose mortgage (i.e. another DSCR loan) that does not report to personal credit. In this scenario, a verification of mortgage signed by the business purpose lender or servicer can serve as evidence of mortgage experience. The mortgage experience does not need to be active, it can be a mortgage that has since been paid off. The reason for this requirement is that institutional DSCR loan investors want the borrower to have demonstrated experience making on-time mortgage payments. If there is no verifiable mortgage experience, it is up to the DSCR lender's loan committee and their institutional investor to allow an exception. Successful exceptions to this requirement often require "compensating factors" such as high credit score, high liquidity, real estate investing experience, LTV that is 5-10% below maximum (i.e. 70% instead of 75% on a cash out refinance).

Property Location Restrictions (OfferMarket-Specific) - DSCR loans are a powerful financing tool for real estate investors, but one important limitation—especially with lenders like OfferMarket—is that properties designated as “rural” on the appraisal report are generally ineligible. This designation is based on the property's geographic location and market characteristics, and if marked rural, the loan application may be declined regardless of the borrower’s qualifications. The reason lies in capital markets: DSCR loans are typically packaged into mortgage-backed securities and sold to institutional investors like pension funds, insurance companies, and credit funds. These investors do not permit rural properties in their portfolios due to perceived higher risk, limited liquidity, weaker rental demand, and appraisal challenges. As a result, lenders like OfferMarket must follow these restrictions to maintain loan salability. If you're considering an investment in a less populated area, it’s essential to check the property’s eligibility early, preferably before ordering an appraisal, and speak with your lender to avoid delays or disqualification. For such rural assets, local banks or credit unions—who retain loans on their balance sheets—may be more flexible. In short, while DSCR loans offer great benefits, property location is a critical eligibility factor, and understanding this early in the financing process can save investors time, money, and frustration.

Documentation Required by OfferMarket (May Vary By Lender):

Soft Tri-Merge Credit Report

Track Record

Background Report

Appraisal

Purchase Contract

Bank Statements, etc.

DSCR Loans vs Bank Loans

Many banks aren't lending right now -- specifically commercial loans for 1-4 unit rental properties. if you find a bank that says it's open for business, there's a good chance they are not in a hurry to fund your loan, and they're asking for tax returns and income verification.

In competitive real estate markets, speed matters. Whether you're putting in an offer on a rent ready investment property, or you're refinancing out of a fix and flip loan or cash purchase, you need speed and you need certainty. Banks are no longer a reliable source of capital for rental property investors.

DSCR Loans vs Conventional Loans

If you haven't already exceeded the maximum number of conventional loans (10), you may be considering going the conventional route. As with bank loans, you're subjecting yourself to strict income verification by way of W2 and tax returns. For many real estate investors who are self employed or who don't show income on their tax returns, this isn't a viable option.

If you're working with a competitive DSCR lender, it will be hard to find reasons to not use DSCR loans to finance your rental properties and grow your portfolio.

The market for DSCR loans for single family (1-4 unit) rental properties is relatively young, already over $100B of annual origination volume, and growing fast with an insatiable level of demand from institutional credit investors that buy DSCR loans (life insurance companies, credit funds, pension funds). As the market for DSCR loans continues to mature, and real estate investors become educated about DSCR loans, we will see DSCR loans become the go-to option for rental property investors.

OfferMarket is a leading DSCR lender (low cost, online) founded by rental property investors who experienced first-hand just how powerful DSCR loans can be to finance and grow your rental portfolio yet how common it is to encounter brokers and private lenders who add negative value.

OfferMarket Loans

Check your rate

60 seconds · no credit pull