Bridge Loan Oregon

OfferMarket Loans

Check your rate

60 seconds · no credit pull

Last Updated: April 30, 2025

At OfferMarket, we are driven by a passion for powering real estate success across the beautiful state of Oregon. Our mission is crystal clear: to help Oregonian investors like you expand your portfolios, amplify returns, and navigate the dynamic investment landscape with certainty.

With our fully integrated platform, you’ll gain access to:

💰 Tailored private lending options

☂️ Investor-focused insurance rate comparisons

🏚️ Exclusive off-market Oregon property opportunities

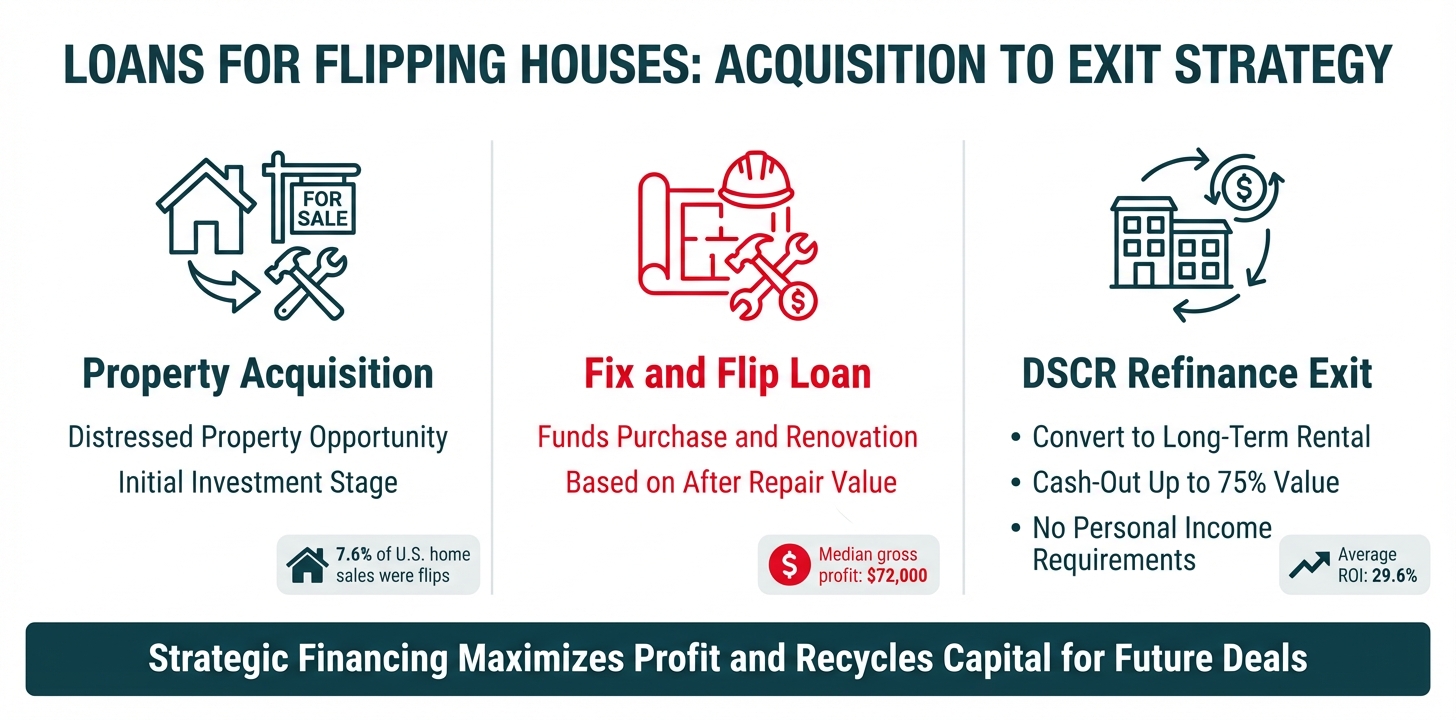

Our Oregon Bridge Loan program is built to deliver fast, dependable, and cost-effective funding—giving you the confidence to purchase, renovate, and scale your residential real estate projects across the Beaver State.

Whether you're aiming to flip homes for immediate gains or build lasting rental wealth through a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, OfferMarket is your committed partner at every turn.

What Is an Oregon Bridge Loan?

An Oregon bridge loan is a short-term financing tool thoughtfully designed for real estate investors who need quick access to capital—helping to "bridge" the gap until a longer-term loan or exit plan is achieved.

Common Use Cases for Oregon Bridge Loans

Investors across Oregon turn to bridge loans for a range of needs, such as:

- Purchase and renovation of distressed properties: Unlock the funding you need to buy and breathe new life into homes—without tying up your own cash reserves.

- Refinance and renovate: If you scooped up a fixer-upper with cash, a bridge loan lets you tap that equity to finance the rehab work.

- Pay off an existing loan and complete the project: Need to settle up with your first lender but still have work to do? A bridge loan keeps your project moving.

- Purchase without renovation: Snag underpriced Oregon properties without renovation plans, aiming for a profitable AS-IS resale.

- Refinance a cash purchase (no rehab): Extract equity from a property you bought outright, even if no construction is involved.

- Refinance after rehab completion: Wrapped up your renovation but need breathing room to sell or refinance? A bridge loan buys you that critical time.

In the world of real estate investing, bridge loans often go by names like "hard money loans" or "fix-and-flip loans." Savvy investors and private lenders use these terms interchangeably.

How Our Oregon Bridge Loan Works

Each OfferMarket Oregon bridge loan has two main parts:

Initial Advance: This funds your property purchase and is wired directly to your title company at closing.

Construction Holdback: Reserved for your rehab budget, these funds are released in stages as you complete the work.

What sets us apart? Flexibility.

You can utilize both the initial advance and construction holdback—or just one, depending on what your project demands.

Many Oregon investors take advantage of both to maximize leverage while preserving cash. But if you're self-funding the rehab—or skipping renovations altogether—that’s perfectly fine. Our Oregon bridge loans are built to fit your investment game plan.

In Oregon's dynamic real estate market, flexibility is your biggest asset. Our bridge loan program evolves with your strategy—even when that strategy changes mid-project.

1. Sell for Profit (Fix and Flip)

If your plan is to renovate and sell for a solid return, our loan terms are designed to keep you nimble, letting you move quickly and capitalize on profits without being boxed in by rigid loan structures.

2. Rent and Refinance (BRRRR Method)

Building wealth through rentals instead? Acquire, renovate, rent out, and refinance with a DSCR (Debt Service Coverage Ratio) loan—all while keeping your cash flow healthy and resilient.

Who Benefits from Oregon Bridge Loans?

From first-time investors to seasoned pros, our Oregon bridge loans are tailored to meet you wherever you are:

Fix and Flip Investors ("Flippers")

Need fast capital to move on investment opportunities? We've got you covered.

BRRRR Method Investors (Buy, Rehab, Rent, Refinance, Repeat)

Growing a rental empire across Oregon? Our Fix and Rent bundle combines a bridge loan for acquisition and rehab with a discounted DSCR loan for refinancing.

A lot of successful Oregon investors flip some properties and hold others. We encourage this balanced approach—it’s smart risk management and maximizes your opportunities in a constantly shifting market.

Oregon Bridge Loan Program Guidelines

Here’s a snapshot of the lending parameters for Oregon investors:

| Criteria | Guideline |

|---|---|

| Loan Amount (Min-Max) | $25,000 – $2,000,000 |

| After Repair Value (ARV) | Minimum $100,000 |

| Experience Requirement | None |

| Minimum Credit Score | 680 |

| Borrowing Entity | LLC or Corporation |

| Initial Advance | Up to 90% of purchase price |

| Construction Holdback | Up to 100% of rehab budget |

| Loan-To-ARV (LTARV) | Maximum 75% |

| Interest Rate | Instant quote available |

| Origination Fee | 1.5 to 2 points |

| Loan Term | 12 to 24 months |

| Prepayment Penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full recourse (51% guarantor requirement) |

| Exit Strategy (Sale) | Minimum 30% projected ROI |

| Exit Strategy (Refinance) | Minimum 1.1 DSCR post-repair |

| Valuation Method | Appraisal report or in-house valuation |

| Minimum Property Size | Single family: 700+ SQFT, 2-4 unit: 500+ SQFT/unit, Condo: 500+ SQFT |

| Max Acreage | 5 acres |

| Interest Accrual | Under $100K: Full Boat; $100K+: As Disbursed |

| Advanced Draws | Lender discretion |

| Minimum Down Payment | $10,000 |

Project Eligibility

At OfferMarket, our vision is simple: empower Oregon investors to build sustainable wealth safely and smartly.

We’re proud that fewer than 0.5% of our loans end up in foreclosure—a testament to our focus on responsible lending and proactive support.

Complex projects with heavy rehabs naturally come with more risks—delays, unexpected costs, or market shifts can all impact outcomes. That's true even for experienced investors. During uncertain economic cycles, those risks grow.

We act not just as your lender, but as your project advisor and risk management partner. Ensuring project feasibility upfront is one of the keys to helping you succeed in Oregon’s real estate market.

Initial Advance

The amount we advance upfront toward your purchase depends on your experience, credit standing, and specifics of the deal.

Key factors include:

Number of investment properties you’ve owned in the past 24 months

Number of similar rehab projects completed in the last 5 years

Minimum credit score of 680 (720+ preferred for best terms)

Licensed professionals (Realtors, General Contractors, Engineers) may qualify for better leverage

If your purchase price is higher than the appraised "As-Is" value, the advance is based on that lower appraised value.

Your exit strategy impacts it too:

Flips: Need minimum 30% gross margin and $15,000 projected profit

Rent and refinance: Post-repair DSCR must be 1.1+

Oregon rural property deals might have slightly lower leverage requirements and need higher experience levels (Tier 3+).

Experience-Based Tiers

We group experience into tiers to tailor lending accordingly:

| Tier | Verifiable Experience |

|---|---|

| 1 | 0 completed projects |

| 2 | 1–2 completed projects |

| 3 | 3–4 completed projects |

| 4 | 5–9 completed projects |

| 5 | 10+ completed projects |

Initial Advance by Experience Tier

The higher your verified experience, the stronger your initial funding. Here’s how your experience level affects the percentage we can lend toward your Oregon property purchase:

| Tier | Initial Advance (% of Purchase Price) |

|---|---|

| 1 | 80% (up to 85% with outstanding credit/liquidity) |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

Adjustments to Initial Advance

Depending on the specifics of your project, we might adjust your initial funding percentage slightly:

| Scenario | Adjustment |

|---|---|

| Credit score under 720 | -5% |

| Full gut rehab needed | -5% |

| First deal in a new market | -5% |

| Licensed Realtor | +5% (up to) |

| Licensed General Contractor | +10% (up to) |

| Licensed Professional Engineer | +10% (up to) |

| Rural Oregon property | -20% (and requires Tier 3 experience minimum) |

Rehab Scope Classification

Your project’s rehab scope impacts loan eligibility:

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget under 25% of the purchase price |

| Moderate | Rehab budget between 25% and 49.99% of purchase price |

| Heavy | Rehab budget between 50% and 99.99% of purchase price |

| Extensive | Rehab budget exceeds purchase price, or major expansions like ADUs |

Note: When your rehab budget outweighs the purchase price, it’s called a "lopsided deal"—special LTFC limits apply here.

Rehab Scope Eligibility

Your experience level also determines the rehab scope you’re eligible for:

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1–2 | 3–4 | 5–9 | 10+ |

| Light | Eligible | Eligible | Eligible | Eligible | Eligible |

| Moderate | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Heavy | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Extensive | Ineligible | Ineligible | Eligible | Eligible | Eligible |

Newer Oregon investors should prioritize light to moderate rehab projects—they finish faster and come with fewer surprises!

LTARV Limits

Your maximum Loan-To-After-Repair Value (LTARV) is based on both your experience and the complexity of your project:

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1–2 | 3–4 | 5–9 | 10+ |

| Light | 70% | 70% | 75% | 75% | 75% |

| Moderate | Ineligible | 70% | 75% | 75% | 75% |

| Heavy | Ineligible | 70% | 75% | 75% | 75% |

| Extensive | Ineligible | Ineligible | 70% | 70% | 70% |

LTFC Limits

For "extensive" rehabs, we cap the Loan-To-Full-Cost (LTFC) to ensure you maintain strong skin in the game:

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1–2 | 3–4 | 5–9 | 10+ |

| Light | N/A | N/A | N/A | N/A | N/A |

| Moderate | Ineligible | N/A | N/A | N/A | N/A |

| Heavy | Ineligible | N/A | N/A | N/A | N/A |

| Extensive | Ineligible | Ineligible | 85% | 90% | 90% |

Example: No Experience

| Criteria | Details |

|---|---|

| Purchase Price | $100,000 |

| Experience Tier | 1 (0 verifiable projects) |

| Credit Score | 695 |

| Rehab Budget | $24,000 |

| ARV | $150,000 |

| Initial Advance | $75,000 (75% of purchase price) |

| Construction Holdback | $24,000 |

| Total Loan Amount | $99,000 |

| LTARV | 66% |

| LTFC | 79.8% |

| Interest Accrual | Full Boat |

Example: No Experience, Excellent Credit

| Criteria | Details |

|---|---|

| Purchase Price | $100,000 |

| Experience Tier | 1 (0 verifiable projects) |

| Credit Score | 750 |

| Rehab Budget | $24,000 |

| ARV | $150,000 |

| Initial Advance | $80,000 (80% of purchase price) |

| Construction Holdback | $24,000 |

| Total Loan Amount | $104,000 |

| LTARV | 69.33% |

| LTFC | 83.9% |

| Interest Accrual | As Disbursed |

Example: 5 Completed Projects

| Criteria | Details |

|---|---|

| Purchase Price | $100,000 |

| Experience Tier | 4 (5 completed projects) |

| Credit Score | 750 |

| Rehab Budget | $20,000 |

| ARV | $150,000 |

| Initial Advance | $90,000 (90% of purchase price) |

| Construction Holdback | $20,000 |

| Total Loan Amount | $110,000 |

| LTARV | 73.33% |

| LTFC | 91.67% |

| Interest Accrual | As Disbursed |

Refinance Using As Is Value Instead of Cost Basis for Initial Advance

While our standard approach bases initial funding on your cost basis (purchase price plus rehab completed to date), there are scenarios where we may consider using the As Is appraised value—especially when that value is higher.

To qualify for this alternate method in Oregon:

The property must be habitable (C4 condition or better)

It must have been held for at least 3 years

The existing lender cannot be a bridge or construction lender (no default interest, fees, or penalties)

Your credit score must be 680+

You must be at least Tier 3 (3+ verified completed projects)

Strong market comps must support the As Is value

Context matters (e.g., long-term rental being repositioned or prepped for resale)

Transactions Involving Wholesalers, Price Run-Ups

In Oregon’s fast-moving real estate landscape, investors often buy from wholesalers or encounter deals with assignment fees and double closes. We understand the model and offer flexibility within clear limits.

If your Oregon deal includes an assignment fee or markup, we allow that fee to count toward your loan basis—up to 20% of the A-B contract price (the price paid by the wholesaler).

Example:

| Item | Amount |

|---|---|

| A-B Contract (Seller to Wholesaler) | $100,000 |

| B-C Contract (Wholesaler to You) | $125,000 |

| As Is Value | $125,000 |

| Eligible Value Basis | $120,000 (capped at 20% markup) |

If the markup exceeds 20%, the excess must be covered out of pocket.

Wholesaler Transaction Guidelines

To protect all parties and ensure compliance, we require:

Both the A-B and B-C contracts

The wholesaler’s operating agreement

Confirmation that this is an arm’s-length transaction

Proof the property is not listed on the MLS at the time of assignment (if you want to count the fee in your loan basis)

OfferMarket does not finance finder’s fees or referral payments. Deals with markups over 20% may be reviewed case by case—but the borrower must cover anything above the cap.

Construction Holdback

Your construction holdback is the part of the bridge loan reserved specifically for your Oregon renovation work. These funds are reimbursed to you through a draw process as your project progresses.

If you prefer to self-fund the rehab—or if no rehab is required—you can opt not to include a construction holdback.

For loans $100K or higher, interest is only charged on the portion you've drawn. For loans under $100K, interest accrues on the entire loan ("Full Boat").

| Criteria | Guideline |

|---|---|

| Minimum Draw Amount | None |

| Maximum Draw Amount | Up to 100% of available holdback |

| Minimum Number of Draws | 0 |

| Maximum Number of Draws | No cap |

| Delivered Materials (Uninstalled) | Up to 50% reimbursed with receipt |

| Draw Inspection | App-based, self-serve (photo submission) |

| Turnaround Time | 0–2 business days |

| Draw Fee | $270 per draw |

| Wire Fee | $30 per wire |

Pro tip: Our app-based draw process makes funding fast and painless, so you can keep your Oregon rehab project on schedule.

Appraisal and In-House Valuation

Every Oregon bridge loan through OfferMarket requires a valuation—either an external appraisal or our in-house valuation (for qualified scenarios).

In-House Valuation Eligibility

You may qualify for in-house valuation if:

| Criteria | Requirement |

|---|---|

| Property Type | 1–4 unit residential (SFR, Duplex, Triplex, Quadplex) |

| Experience Tier | 4 or higher |

| Credit Score | 720+ |

| Rural Property | Not eligible |

| New Market (First Deal in Oregon) | Not eligible |

| LTARV | Max 70% |

Even if eligible, OfferMarket may still require an appraisal based on underwriting review.

Exterior Appraisal Guidelines

Exterior-only appraisals are allowed for certain transaction types:

REO sales

Foreclosure auctions

Sheriff’s sales

Online auctions

Bankruptcy sales

The report must be:

Dated within 120 days of loan settlement

If 120–179 days old, a recertification is required

Interior Appraisal Guidelines

For most Oregon transactions, a full interior appraisal is required. Here’s what’s needed:

| Property Type | Appraisal Forms |

|---|---|

| Single Family | 1004 + 1007 (include ARV and As Is value) |

| 2–4 Units | 1025 + 216 (include ARV and As Is value) |

| Condominium | 1073 + 1007 (include ARV and As Is value) |

Appraisals are ordered via our AMC partners. Borrowers are responsible for paying the invoice before we can proceed with funding.

Appraisal Transfer

Already have an appraisal? It might be transferrable if:

Ordered through an approved AMC

Completed within 180 days

Recertified if 120–179 days old

Transfer package must include:

Signed transfer letter (AIR-compliant)

PDF + XML copies of the report

Paid invoice

Scenario: Stabilized Bridge Loan

For Oregon investment properties that are already in good shape—rent-ready, or market-ready for sale—you might qualify for our Stabilized Bridge Loan. This option allows you to borrow based on the As Is value, with no renovation budget required.

It’s ideal for seasoned investors who just need short-term capital to bridge into their next move.

| Criteria | Guideline |

|---|---|

| LTV (Maximum) | Tier 1: 70% Tier 2: 70% Tier 3: 75% Tier 4: 75% Tier 5: 75% |

| LTFC (Maximum) | Tier 1: 80% Tier 2: 80% Tier 3: 90% Tier 4: 90% Tier 5: 90% |

| Appraisal Condition Rating | C1–C4 only (property must be habitable and stable) |

| Loan Term (Maximum) | 12 months |

Note: This program is designed for investment properties that don’t need any rehab work.

Key Loan Details

| Criteria | Details |

|---|---|

| Loan Amount Range | $25,000 to $2,000,000* |

| Units per Property | 1–4 units |

| Eligible Property Types | Non-owner occupied 1–4 unit residential (SFRs, duplexes, triplexes, quads, condos, townhomes, PUDs) |

| Minimum Property Size | Single Family: ≥700 SQFT 2–4 Units and Condos: ≥500 SQFT per unit |

| Maximum Acreage | 5 acres |

| Loan to Cost (LTC) | Up to 90% purchase, 100% rehab |

| Loan to ARV (LTARV) | Up to 75% |

| Minimum Down Payment | $10,000 (for purchases under $100K) |

| Loan Term | 12 months standard; up to 24 months for certain projects |

| Extensions | Up to 50% of the original term |

| Points (Origination Fee) | 1.5 to 2 points ($2,000 minimum) |

| Prepayment Penalty | None |

| Occupancy | Business-purpose only, non-owner occupied |

| Transaction Types | Purchase, Refinance (arms-length only) |

| Geographic Coverage | All states except: AK, AZ, HI, MN, ND, NV, OR, SD, UT, VT |

| Amortization Structure | Interest-only with balloon payment |

| Interest Accrual Method | Under $100K: Full Boat $100K and above: As Disbursed |

Extensions

While Oregon bridge loans are meant to be short-term (12–24 months), we understand that delays happen. You can extend your loan term by up to 50% of the original duration—giving you extra time to complete your exit.

| Initial Loan Term | Max Extension |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Extension Terms and Fees

| Extension Term | Fee |

|---|---|

| 3 months (1st extension) | 1% of loan amount |

| 3 months (2nd extension) | 1.5% of loan amount |

| 6 months (1st extension) | 2.5% of loan amount |

These fees are included in your payoff statement.

Extension Prerequisites

Before we approve an extension, you’ll need to:

Confirm that your builder’s risk insurance covers the extended term

Satisfy any additional conditions requested by OfferMarket

Ineligible Property Types

Our Oregon Bridge Loan Program focuses on 1–4 unit residential investment properties. Certain types of real estate are outside our lending scope due to their risk profiles or specialized nature.

Not eligible:

Mixed-use buildings

Multifamily with 5+ units

Condotels or co-ops

Mobile/manufactured homes

Commercial spaces (retail, office, industrial)

Cabins, log homes, or ultra-luxury properties

Oil/gas lease properties

Working farms, ranches, or orchards

Vacation rentals or seasonal homes

Homes accessed only by dirt/unpaved roads

Exception Scenarios

Some situations fall into a gray area. We may review these Oregon deals case by case:

| Scenario | Consideration |

|---|---|

| Credit score 660–679 | May qualify with strong compensating factors |

| Leasehold interest | Case-by-case |

| Small SFR (500–699 SQFT) | Exception basis only |

| Small 2–4 unit (400–499 SQFT per unit) | Exception basis only |

| Initial advance based on As Is value | Allowed if all refinance conditions are met |

| Non-arm’s-length deals | Must be disclosed and reviewed |

| Financed interest payments | Available if you meet underwriting criteria |

Borrower and Guarantor Requirements

We take responsible lending seriously. To qualify for an Oregon bridge loan, your entity and guarantors must meet these criteria:

| Item | Requirement |

|---|---|

| Borrowing Entities | LLC or Corporation (no nonprofits) |

| Eligible Borrowers | U.S. Citizens, Permanent Residents, or qualifying Foreign Nationals |

| Foreign Nationals | Must have valid passport and U.S. visa (no travel/student visas); U.S. credit score required |

| Credit Score | Minimum 680 (case-by-case at 660–679) |

| Credit Report | Tri-merge, not older than 120 days |

| Liquidity | Enough for cash to close + 25% of rehab budget |

| Liquid Assets Accepted | Bank, brokerage, retirement (50% haircut on retirement accounts) |

| Verification | Two recent statements, no seasoning required |

| Guaranty | 51% of entity must personally guarantee for purchases; 100% for cash-out refinances |

| Recourse | Full recourse required |

| Guarantor Net Worth | At least 50% of loan amount |

Liquidity Verification

To ensure you're financially ready for your Oregon project, we’ll verify that guarantors control enough liquid assets to cover:

The down payment

At least 25% of your rehab budget

Accepted sources include:

Personal or business bank accounts

Brokerage accounts (individual or business)

Retirement funds (50% value considered due to limited accessibility)

A dedicated business account isn’t mandatory—but it’s a great move for organization and risk control.

Credit and Background Items

During underwriting, we take a comprehensive look at your credit and background to ensure a responsible lending partnership. Here’s what we review:

| Scenario | Requirement |

|---|---|

| Middle Credit Score | Middle of 3 scores used; lowest of 2 used |

| No Mortgage Tradelines | Requires 6 months of interest reserves |

| Fewer Than 5 Tradelines | Requires 6 months of interest reserves |

| Bankruptcy on Record | Must be discharged at least 4 years ago |

| Foreclosure on Record | Must be completed at least 4 years ago |

| Bankruptcy/Foreclosure (4–7 Years Ago) | At least 3 months of interest reserves required |

| Recent Late Mortgage Payments | Letter of Explanation (LOE) required |

| Past-Due Balances | Must be paid before loan closing |

| Involuntary Liens or Judgments | Must be cleared pre-funding |

| Pending Civil Lawsuits | Reviewed with LOE |

| Pending Criminal Cases | Not eligible |

| Financial Crimes | Not eligible |

| Other Criminal History | Requires LOE; subject to review by loan committee |

Interest Reserves

Depending on your credit profile and background, OfferMarket may collect interest reserves to ensure your Oregon project remains on stable financial footing.

| Guarantor FICO / Scenario | Reserve Requirement |

|---|---|

| Lender Discretion | 0 months |

| 700+ FICO | 1 month |

| 660–699 FICO | 3 months |

| 660–699 FICO + concerns | 6 months |

Financed Interest Payments

To help you conserve liquidity during construction or renovation, we offer financed interest. Instead of monthly payments, your interest simply accrues and is added to your loan payoff amount.

Example:

| Term | Amount |

|---|---|

| Loan Amount | $100,000 |

| Interest Rate | 12% annually |

| Term | 9 months |

| Accrued Interest | $9,000 |

| Payoff | Principal: $100,000 Interest: $9,000 |

Property Sourcing Guidelines

We’re committed to helping Oregon investors pursue high-quality projects. To support your success, we set clear property sourcing expectations.

If this is your first project in a market, provide:

A signed General Contractor (GC) agreement, or

A Letter of Explanation (LOE) explaining why a GC is not required

For deals involving wholesalers, prior sales with price markups, or non-arm’s-length transactions, extra documentation may be required.

If your project is complex (e.g. structural changes, additions), we may ask for:

Architectural plans

Engineer letters

Local permits and approvals

Bridge Loan Insurance Guidelines

Your Oregon investment property needs strong protection during its lifecycle. OfferMarket requires builder’s risk insurance (aka fix-and-flip insurance) for all bridge loan deals.

| Coverage Type | Requirement |

|---|---|

| Dwelling | Replacement cost or full loan amount (no coinsurance) |

| Liability | $1M per occurrence / $2M aggregate |

| Builder’s Risk | Included |

| Flood | If in FEMA Special Flood Hazard Area, coverage must exceed loan or $250,000 |

Additional Coverage Details

| Requirement | Standard |

|---|---|

| AM Best Rating | A- VIII or higher |

| Policy Type | Special Form |

| Deductible | $1,000 – $5,000 |

| Designations | OfferMarket listed as Mortgagee and Additional Insured |

| Cancellation | 30-day written notice required |

| Exclusions | No exclusions for wind, hail, or named storms |

💡 Pro tip for Oregon investors: Secure your property by installing locks, smoke detectors, and cameras immediately. This ensures compliance with insurance terms and helps protect your project.

Frequently Asked Questions

What states does OfferMarket fund bridge loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have multiple bridge loans at the same time?

Absolutely. Many OfferMarket clients manage several projects concurrently. We monitor liquidity and deal flow to help ensure you stay within a healthy risk profile.

Are bridge loans considered commercial loans?

Yes. All bridge loans through OfferMarket are business-purpose loans. They are issued to your legal entity (LLC or Corporation) and not personally to you.

What is the minimum loan amount?

| Minimum Loan Amount |

|---|

| $25,000 |

What types of properties qualify?

We lend on non-owner occupied 1–4 unit residential investment properties in Oregon and other supported states.

| Eligible Property Types |

|---|

| Single-family homes |

| Townhomes |

| 2–4 unit multifamily |

| Warrantable condominiums |

| Planned Unit Developments (PUDs) |

How is Loan-To-Value (LTV) calculated?

We typically use Loan-To-After-Repair Value (LTARV), based on the lesser of the purchase price or the As Is appraised value.

LTARV = (Initial Advance + Construction Holdback) ÷ ARV

What are the credit score requirements?

| Credit Criteria | Details |

|---|---|

| Minimum Score | 680 |

| Exception Range | 660–679 (case-by-case) |

| Guarantors Evaluated | All members providing a personal guarantee |

Do I need prior experience to qualify?

| Experience Requirement | Details |

|---|---|

| Required Experience | Not mandatory |

| Benefits of Experience | Better leverage and terms |

| Evaluation Method | Based on verified past rehab projects |

Does wholesaling experience count?

| Wholesaling Toward Experience | Eligibility |

|---|---|

| Acting only as a wholesaler | Not counted as direct project experience |

What documentation is required?

We’ve streamlined our process for both purchase and refinance transactions using our digital Loan File system.

Purchase Transaction Requirements

| Required Documents |

|---|

| Executed purchase contract |

| Soft-pull tri-merge credit report |

| Background check |

| Guarantor ID |

| Entity formation documents |

| Scope of Work (rehab budget) |

| Two recent bank/brokerage statements |

| Appraisal ordered through OfferMarket |

| Track record of completed projects |

| LOE (if requested by underwriting) |

Refinance Transaction Requirements

| Required Documents |

|---|

| Signed settlement statement |

| Payoff letters (if applicable) |

| Credit and background reports |

| Entity documents |

| Scope of Work (if applicable) |

| Sunk cost documentation |

| Appraisal ordered through OfferMarket |

| Bank/brokerage statements |

| Track record and ID for each guarantor |

| LOE (if needed) |

Are there special requirements for bridge loans over $1 million?

| Criteria | Requirement |

|---|---|

| Experience | Minimum Tier 3 (3+ similar projects) |

| Market Liquidity | 3+ comps within 2 miles in last 6 months |

| Credit Score | 680+, 5 tradelines with 24-month history |

| Rural Properties | Not eligible |

| Track Record | Required for all entity members |

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit. This is a secondary, self-contained, housing unit located on the same tax parcel as a main single family home. |

| Arms-length | An arms-length transaction is a deal between independent parties with no special relationship, ensuring fair market value. |

| Non Arms-length | A transaction where a personal, financial, or business connection between the parties may affect fairness, pricing, or terms. |

| Initial Advance | The component of the total loan that will go towards the purchase price. This amount is wired to the title company at closing. |

| Construction Holdback | The component of the total loan that will go towards the purchase price. This amount is wired to the title company at closing. |

| Interest Reserves | Reserves collected on the settlement statement and held in servicing escrow to be drawn down as payment for interest accrued as determined during underwriting based on credit score and late payment history. |

| LOE | Letter of explanation. A document that offers further details or clarification on particular issues, like a borrower's financial status, credit history, or background. |

| LTC | Loan to Cost. Ratio of the loan amount to the purchase price and rehab costs. |

| LTFC | Loan to Full Cost. Ratio of the total loan amount to the total cost, which includes both the purchase price and the construction budget. |

| LTV | Loan-To-Value. This is the ratio of loan amount to property’s As-Is value. |

| LTARV | Loan-To-After-Repair Value. Also referred to as "ARLTV". This is the ratio of loan amount to property’s estimated value after rehab is completed. |

| As Disbursed Interest | Interest is accrued only on the amount of the loan that has been funded (initial advance + drawn construction holdback). |

| Full Boat Interest | Also known as "Dutch Interest". Interest is accrued on the entire loan amount (initial advance + total construction holdback). |

| Lopsided deal | When the As Is value or purchase price is less than the rehab amount. In these scenarios, LTFC is limited to a maximum of 85%. |

| GC Agreement | A contract with a general contractor outlining project management and execution responsibilities. |

| DSCR | [Debt Service Coverage Ratio](https://www.offermarket.us/blog/debt-service-coverage-ratio). A measure of property income relative to debt obligations. The formula is Rent ÷ [PITIA](https://www.offermarket.us/blog/pitia) |

Get Your Instant Bridge Loan Quote

At OfferMarket Capital LLC, we proudly support real estate investors throughout Oregon and beyond. Specializing in bridge and DSCR loans for 1–4 unit residential investments, our goal is to help you:

Grow your Oregon real estate portfolio

Maximize ROI

Build generational wealth with confidence

We make financing fast, simple, and dependable, so you can stay laser-focused on what you do best: finding deals and executing successful projects.

Join thousands of real estate investors who use OfferMarket every month. With your free membership, you’ll gain access to:

💰 Private lending solutions tailored to your goals

☂️ Investor-focused insurance comparisons

🏚️ Off-market property leads

💡 Oregon market trends and data tools

Thousands of real estate investors get value from OfferMarket every month. Membership is entirely free and includes the following benefits:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull