Montana Bridge Loan Program

Last Updated: April 30, 2025

At OfferMarket, we are passionate about helping you expand your wealth through strategic real estate investments. To make your path to success smoother, we provide an all-in-one, hassle-free platform that includes:

💰 Direct access to private capital

☂️ The ability to compare competitive insurance rates

🏚️ Exclusive opportunities for off-market property deals

Our Bridge Loan Montana program is thoughtfully designed to deliver quick, dependable, and cost-efficient financing, making it easier for you to purchase and enhance 1-4 unit residential investment properties throughout Montana.

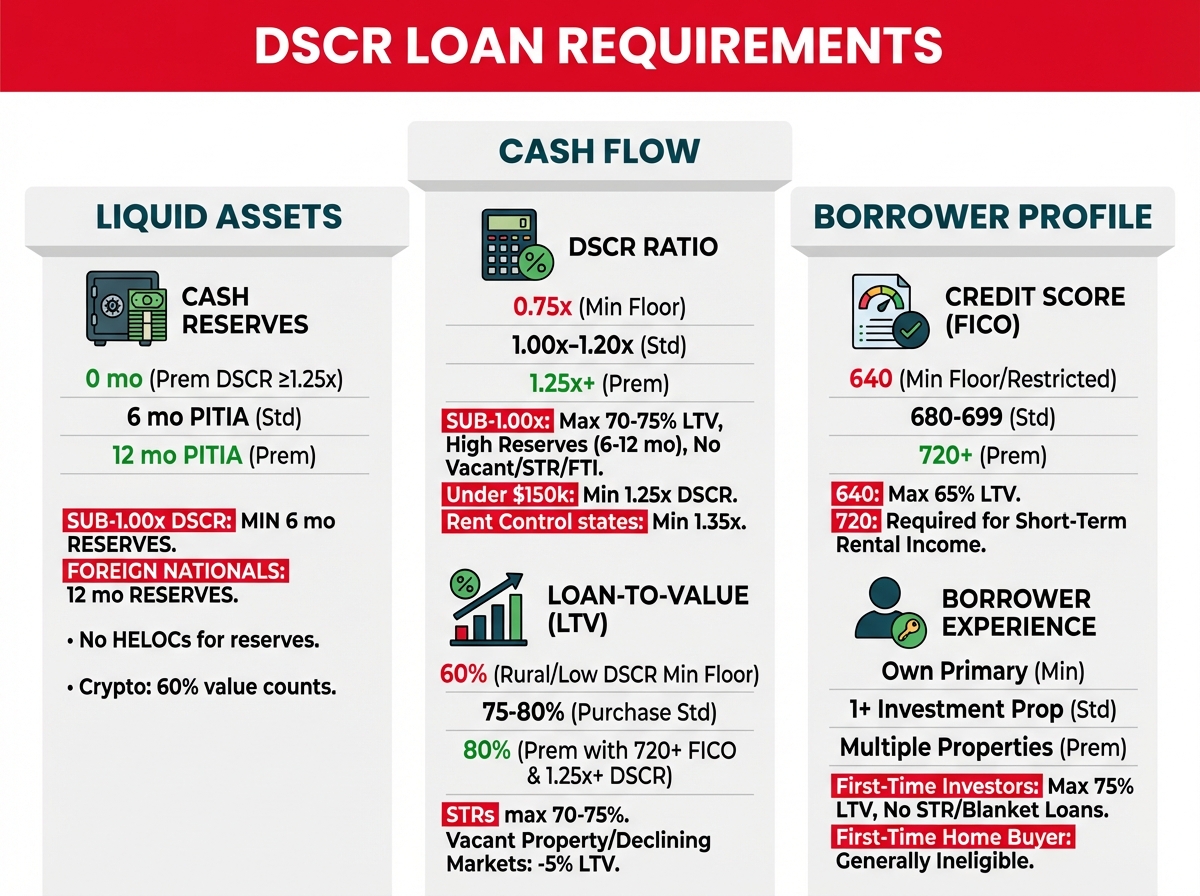

Whether your investment plan involves renovating and selling for a solid return or holding the property as a rental while refinancing with a DSCR loan, we’re here to back your strategy and help bring your goals to life.

Let’s dive into the details of the OfferMarket Montana Bridge Loan Program.

What is a Bridge Loan?

A bridge loan acts as short-term financing, giving you the flexibility to move forward with your investment while you work on securing longer-term funding options.

Common Bridge Loan Scenarios

For property investors in Montana, a bridge loan often serves as the ideal financial tool in scenarios like these:

- Purchasing a fixer-upper or distressed home — perfect for acquiring and rehabbing properties without tying up your own cash reserves.

- Refinancing a property purchased with cash and covering the renovation costs — perhaps you secured a property with a quick cash close and now need capital to complete the rehab work.

- Refinancing an existing loan to finish your renovations — maybe your current lender is asking for repayment, but the project still requires funding and time before you can refinance or sell.

- Acquiring properties without renovation plans — picking up undervalued properties, often off-market, with the intent to sell them as-is for profit.

- Refinancing a cash purchase with no rehab required — tapping into the equity from a below-market acquisition to fund your next investment.

- Refinancing an existing loan with renovations already completed — the rehab work is done, but you need more time before exiting through sale or refinance.

In the world of real estate investing, the terms bridge loan, hard money loan, and fix and flip loan are often used interchangeably, all referring to this flexible form of short-term financing.

How Does a Montana Bridge Loan Work?

Our Montana bridge loan program is built around two primary funding components that offer flexibility for your investment strategy:

Initial Advance — This is the upfront portion of the loan that covers part of your property’s purchase price. These funds are wired directly to the title company at closing.

Construction Holdback — This segment of the loan is reserved for your renovation work. Funds are released to you through reimbursement draws as you complete phases of your rehab project.

One of the standout benefits of a bridge loan is its adaptability. You have the option to secure just the initial advance without tapping into the construction holdback, or you can utilize the construction holdback without needing the initial advance — whichever combination works best for your project.

Many real estate investors in Montana choose to leverage both options, helping them maximize financing and reduce the amount of personal capital required. Some prefer to use their own funds for renovation, while others purchase properties with cash and use the construction holdback to cover up to 100% of their rehab costs.

When it comes to bridge loan Montana solutions, the program flexes to meet your investment needs.

Your exit strategy will typically fall into one of two categories:

Flip — Complete the renovations and sell the property for a profit.

Rent and Refinance — Hold onto the property as a rental and refinance into longer-term financing, such as a DSCR loan.

It’s common for investors across Montana to adjust their exit plans as the market evolves. There’s no need to lock yourself into one option upfront — flexibility is key.

Here are a couple of real-world examples:

You may start out following the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), but discover that the resale market is particularly strong in your area, leading you to sell instead of holding.

You might plan to flip, but if the Montana housing market slows, you could shift gears and hold the property as a rental, refinancing into a DSCR loan until conditions improve.

The key takeaway? Focus on properties that allow for multiple exit strategies so you can stay nimble and manage risk effectively.

Who Typically Uses Bridge Loans in Montana?

Our bridge loan Montana program is designed for a wide range of real estate investors. Here’s who benefits most from this flexible funding solution:

Fix and Flip Investors (Flippers) — Buyers who acquire properties at a discount, improve them through renovation, and then sell for a gain.

Rental Property Investors (BRRRR Method) — Investors who purchase, rehab, rent out, refinance, and repeat the process to grow long-term rental portfolios.

If you’re pursuing the BRRRR strategy, be sure to explore our Fix and Rent bundle, which combines a bridge loan for acquisition and rehab with a discounted DSCR loan for refinancing — a powerful combo for Montana investors.

Many of our clients choose a hybrid approach, flipping certain properties while holding others as rentals based on how each deal unfolds. This flexibility is often what separates successful investors from the rest.

Montana Bridge Loan Program Guidelines

| Criteria | Guideline |

|---|---|

| Loan amount (minimum) | $25,000 |

| Loan amount (maximum) | $2,000,000 |

| ARV (minimum) | $100,000 |

| Experience | Not required |

| Credit score (minimum) | 680 |

| Borrowing entity | LLC or Corporation |

| Initial advance | Up to 90% |

| Construction holdback | Up to 100% |

| LTARV (maximum) | 75% |

| Interest rate | Get instant quote |

| Origination fee | 1.5 to 2 points |

| Term | 12 to 24 months |

| Points out | None |

| Prepayment penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full (51% of borrowing entity must guarantee) |

| Exit strategy: Sale | Minimum 30% ROI |

| Exit strategy: Refinance | Minimum 1.1 DSCR after repairs |

| Valuation | Appraisal report or in-house valuation |

| SqFt (minimum) | Single family: 700+; 2-4 unit: 500+ per unit; Condo: 500+ |

| Acreage (maximum) | 5 |

| Interest accrual | Under $100,000 loan: full boat; $100,000+ loan: as disbursed |

| Advanced draws | Lender discretion |

| Down payment (minimum) | $10,000 |

Project Eligibility for Montana Bridge Loans

At OfferMarket, we’re dedicated to helping Montana-based investors grow their real estate portfolios while keeping their exposure to risk in check. One way we uphold this commitment is by focusing on lending strategies that prioritize your long-term success.

Our lending track record speaks volumes — less than 0.5% of the loans we’ve funded have ended in default requiring foreclosure. This puts us among the most reliable lenders in the private financing sector and reflects our focus on safeguarding your investment.

We’ve found that novice investors who jump into large, complicated rehab projects often face the steepest hurdles — whether it’s delays, unexpected expenses, or shifting market dynamics. Even experienced investors can run into trouble with these more complex deals, especially during uncertain economic periods.

Our approach to lending is more than just providing capital. We serve as your financing partner, risk advisor, and sounding board, helping you approach each project with clarity and confidence.

To further support this mission, we’ve developed a structured rehab classification system that determines your eligibility based on the project scope and your level of experience.

Initial Advance

The initial advance — the upfront funding portion of your Montana bridge loan — is based on several factors tied to both your project and your background. Here’s what we look at:

Number of investment properties you’ve owned in the past 24 months

How many similar rehab projects you’ve completed successfully over the last five years

Your minimum credit score (680 required, though we prefer 720+ for the guarantor within the borrowing entity)

Professional licensing — additional leverage is available to Realtors, General Contractors, and Professional Engineers

If your purchase price is higher than the As-Is property value (according to our appraisal or valuation), we’ll base your initial advance on the As-Is value — not your purchase contract price.

Your chosen exit strategy also plays a significant role. If your plan is to flip the property, we require at least a 30% gross margin and $15,000 in projected profit.

If your plan is to rent and refinance — or if your flip scenario falls short of these minimum thresholds — the project must achieve a minimum Debt Service Coverage Ratio (DSCR) of 1.1 after repairs.

To help you crunch these numbers with confidence, use our Fix and Flip Calculator and DSCR Calculator — designed to make evaluating your exit strategy straightforward.

If the property is located in a rural area, your initial advance will be capped, and a minimum of three completed projects is required to qualify.

Experience-Based Tiers

| Tier | Verifiable Experience |

|---|---|

| 1 | 0 projects completed |

| 2 | 1 to 2 projects completed |

| 3 | 3 to 4 projects completed |

| 4 | 5 to 9 projects completed |

| 5 | 10+ projects completed |

Initial Advance by Experience Tier

| Tier | Initial Advance (% of Purchase Price) |

|---|---|

| 1 | 80%* |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

Borrowers in Tier 1 may qualify for 85% advance on an exception basis if they maintain excellent credit and strong liquidity.

Adjustments to Your Initial Advance

Within our Montana bridge loan program, your initial advance percentage may be adjusted depending on certain borrower and project-specific factors. Below are the scenarios that could either increase or reduce the initial advance percentage for your deal:

| Scenario | Adjustment |

|---|---|

| Credit score below 720 | -5% |

| Full gut rehab project | -5% |

| Investing in a market where you have no prior experience | -5% |

| Licensed Realtor | Up to +5% |

| Licensed General Contractor | Up to +10% |

| Licensed Professional Engineer | Up to +10% |

| Rural property designation (requires 3+ completed projects) | -20% |

These adjustments help ensure the right balance of risk and reward for your Montana investment project, tailoring the loan structure to your specific situation.

Rehab Scope Classification

The renovation scope for your Montana investment property is determined by the size of your rehab budget relative to the purchase price. Understanding your rehab classification ensures that the project aligns well with your experience and financial strength.

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget is less than 25% of the purchase price |

| Moderate | Rehab budget is 25% to 49.99% of the purchase price |

| Heavy | Rehab budget is 50% to 99.99% of the purchase price |

| Extensive | Rehab budget exceeds 100% of the purchase price — includes additions, expansions, ADUs, or “lopsided deals” where the purchase price is low compared to the rehab budget |

A “lopsided deal” refers to scenarios where the property’s purchase price or As-Is value is significantly lower than the total rehab budget, requiring careful evaluation and responsible funding.

Rehab Scope Eligibility for Montana Bridge Loans

Our focus is on responsible lending practices that match your project’s scope with your level of experience. Here’s how your experience tier determines your eligibility for various levels of rehab projects under the bridge loan Montana program:

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | Eligible | Eligible | Eligible | Eligible | Eligible |

| Moderate | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Heavy | Ineligible | Eligible | Eligible | Eligible | Eligible |

| Extensive | Ineligible | Ineligible | Eligible | Eligible | Eligible |

For many Montana investors, focusing on lighter or moderate rehab projects helps reduce the likelihood of delays, budget overruns, and execution risk — especially if you’re newer to the market.

LTARV (Loan-to-After-Repair Value) Limits for Montana Investors

The maximum Loan-to-After-Repair Value (LTARV) depends on both your experience level and the rehab scope classification of your project. This structure supports safe lending practices and helps protect both the investor and the lender from over-leveraging.

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | 70% | 70% | 75% | 75% | 75% |

| Moderate | Ineligible | 70% | 75% | 75% | 75% |

| Heavy | Ineligible | 70% | 75% | 75% | 75% |

| Extensive | Ineligible | Ineligible | 70% | 70% | 70% |

By applying these leverage limits, the Montana bridge loan program promotes financial discipline, reducing exposure to unexpected risks that may arise during the project lifecycle.

LTFC (Loan-to-Full-Cost) Limits for Montana Bridge Loans

For projects classified as Extensive rehab — where the renovation budget exceeds the purchase price or As-Is value — we apply Loan-to-Full-Cost (LTFC) caps. LTFC refers to the portion of your total project cost (purchase price plus rehab budget) that the lender will fund.

This safeguard is designed to ensure that Montana investors maintain adequate equity in higher-risk scenarios.

| Tier | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Experience | 0 | 1-2 | 3-4 | 5-9 | 10+ |

| Light | N/A | N/A | N/A | N/A | N/A |

| Moderate | Ineligible | N/A | N/A | N/A | N/A |

| Heavy | Ineligible | N/A | N/A | N/A | N/A |

| Extensive | Ineligible | Ineligible | 85% | 90% | 90% |

For example, if your project qualifies for an 85% LTFC, we would fund 85% of your total project cost, and you would cover the remaining 15%. This ensures proper alignment between borrower and lender interests, particularly for projects that demand significant rehab execution.

Example 1: New Investor, Limited Experience

| Purchase Price | $100,000 |

|---|---|

| Experience Tier | 1 (0 verified projects) |

| Credit Score | 695 |

| Rehab Budget | $24,000 |

| ARV (After-Repair Value) | $150,000 |

| Initial Advance | $75,000 (75%) |

| Construction Holdback | $24,000 |

| Total Loan Amount | $99,000 |

| LTARV | 66% |

| LTFC | 79.8% |

| Interest Accrual | Full boat (accrues on total loan amount) |

Example 2: New Investor With Strong Credit

| Purchase Price | $100,000 |

|---|---|

| Experience Tier | 1 (0 verified projects) |

| Credit Score | 750 |

| Rehab Budget | $24,000 |

| ARV (After-Repair Value) | $150,000 |

| Initial Advance | $80,000 (80%) |

| Construction Holdback | $24,000 |

| Total Loan Amount | $104,000 |

| LTARV | 69.33% |

| LTFC | 83.9% |

| Interest Accrual | As disbursed |

Example 3: Experienced Montana Investor (5 Completed Projects)

| Purchase Price | $100,000 |

|---|---|

| Experience Tier | 4 (5 verified projects) |

| Credit Score | 750 |

| Rehab Budget | $20,000 |

| ARV (After-Repair Value) | $150,000 |

| Initial Advance | $90,000 (90%) |

| Construction Holdback | $20,000 |

| Total Loan Amount | $110,000 |

| LTARV | 73.33% |

| LTFC | 91.67% |

| Interest Accrual | As disbursed |

These examples illustrate how experience, credit score, and project scope influence the funding structure of your Montana bridge loan.

Refinancing Based on As-Is Value Instead of Cost Basis

For most Montana bridge loan scenarios, our underwriting is based on your cost basis, which includes your purchase price plus any sunk renovation costs. This ensures that you maintain real equity in the deal.

However, there are situations where we may offer financing based on the As-Is value of the property — especially if the property has appreciated over time. Here are the conditions that must be met to qualify for this option:

The property must be habitable, with an appraisal condition rating of C4 or better (no major disrepair).

Ownership seasoning of at least three years is required.

If refinancing an existing loan, the current loan must not be from a bridge or construction lender, and the account must be free of default interest, late fees, or extension penalties.

A minimum credit score of 680 is required, along with an experience tier of 3 or higher (at least 4 completed projects).

Strong support for the higher As-Is value must be validated through neighborhood sales comparables.

The refinance scenario must be reasonable — for example, the property may have been rented for several years, and now you’re seeking funding for upgrades before listing it for sale.

This approach provides added flexibility for experienced Montana investors whose properties have increased in value over time and are ready for repositioning.

Wholesaler Transactions and Price Run-Up Guidelines

In Montana real estate transactions where a wholesaler is involved, we allow assignment fees or double-close price increases to be factored into your value basis — but with clear limits to maintain fair lending practices.

Here’s how it works:

| Scenario | Guideline |

|---|---|

| Assignment fee / price markup allowed | Up to 20% of the original purchase price (A-B contract) |

| Any price increase beyond 20% | Must be covered by the borrower (not financed) |

Example of a Wholesaler Transaction:

| Party | Amount |

|---|---|

| A-B Contract (seller to wholesaler) | $100,000 |

| B-C Contract (wholesaler to investor) | $125,000 |

| As-Is Value | $125,000 |

| Value Basis for Initial Advance | $120,000 (capped at 20% markup) |

Important Wholesaling Guidelines:

Properties listed on the MLS are not eligible for financing of the assignment fee.

Full documentation is required, including A-B and B-C contracts, the wholesaler's operating agreement, and a clear chain of title.

Finder’s fees and referral fees are not eligible for financing.

All transactions must be arm’s length — meaning there should be no personal or financial relationship between the buyer and seller.

Construction Holdback

The construction holdback portion of your Montana bridge loan provides funding for your rehab work through a structured draw process. As you complete stages of your renovation, funds are disbursed to reimburse you for those completed phases.

| Criteria | Draw Processing Guideline |

|---|---|

| Minimum draw amount | None |

| Maximum draw amount | Up to 100% of remaining construction holdback |

| Minimum number of draws | 0 |

| Maximum number of draws | No limit |

| Materials delivered but not installed | Up to 50% reimbursed (with receipt or invoice) |

| Draw inspection | App-based (self-service inspections) |

| Draw turnaround | 0 to 2 business days |

| Draw fee | $270 per draw |

| Wire fee | $30 |

If you prefer to handle your rehab costs out of pocket, you’re welcome to forgo the construction holdback entirely and self-fund the renovation phase.

For loan amounts of $100,000 or more, interest accrues only on disbursed funds (known as “As Disbursed” interest). For loans under $100,000, interest accrues on the full loan amount from day one — commonly referred to as “full boat” interest.

Appraisal and Valuation Process for Montana Bridge Loans

Every Montana bridge loan begins with a property valuation to confirm eligibility and determine funding amounts. Depending on the type of deal and your experience level, we offer different valuation approaches:

In-House Valuation (for Select Scenarios)

Available when:

The property is a single-family home, duplex, triplex, or quadplex

You are a Tier 4 investor or higher

Credit score of 720+ (for the guarantor)

Property is not located in a rural area

You are not entering a new market

LTARV is limited to 70%

Note: Even with in-house valuation, OfferMarket reserves the right to request a formal appraisal when necessary.

Exterior Appraisal

Required for situations such as:

REO sales

Foreclosures or sheriff's sales

Online property auctions

Bankruptcy-related sales

The appraisal must be dated within 120 days of the loan settlement. If the appraisal is between 120 and 179 days old, a recertification is required.

Interior Appraisal

Used for all other property evaluations outside the criteria listed above. Required appraisal forms include:

| Property Type | Appraisal Forms Needed |

|---|---|

| Single family | 1004 + 1007 ARV with As-Is value (non-gridded) |

| 2-4 unit properties | 1025 + 216 ARV with As-Is value (non-gridded) |

| Condominiums | 1073 + 1007 ARV with As-Is value (non-gridded) |

We handle the appraisal process through our approved Appraisal Management Company (AMC), and borrowers are responsible for paying the AMC’s invoice before funding.

Appraisal Transfer

Already have an appraisal on hand? You may be able to transfer it for use with your Montana bridge loan, provided these conditions are met:

The appraisal was ordered through an approved AMC.

The report is less than 180 days old at the time of loan closing.

If the report is between 120 and 179 days old, recertification is required.

The transferring lender must provide a signed transfer letter confirming compliance with Appraiser Independence Requirements (AIR).

Required documentation includes:

Full appraisal report in PDF format

Appraisal report in XML format

Proof of appraisal invoice payment

This ensures a smooth process while remaining compliant with valuation guidelines.

Stabilized Bridge Loan Scenario for Montana Properties

If your Montana property is already stabilized — meaning it has no deferred maintenance and qualifies with an appraisal condition rating of C4 or better — you may be eligible for financing based on its current As-Is value rather than relying on after-repair projections.

This is known as a stabilized bridge loan, and it’s a great fit for properties that are already rent-ready or positioned for resale without the need for further rehab.

Guidelines for Stabilized Bridge Loans:

| Criteria | Guideline |

|---|---|

| LTV (maximum) | Tier 1: 70% Tier 2: 70% Tier 3: 75% Tier 4: 75% Tier 5: 75% |

| LTFC (maximum) | Tier 1: 80% Tier 2: 80% Tier 3: 90% Tier 4: 90% Tier 5: 90% |

| Appraisal condition rating | C1, C2, C3 or C4 |

| Loan Term (maximum) | 12 months |

This structure allows Montana investors to capitalize on existing equity in stabilized properties without waiting on rehab timelines.

Key Loan Details for Montana Bridge Loans

Here’s a quick summary of the essential loan terms available through our bridge loan Montana program:

| Criteria | Details |

|---|---|

| Loan Amount | $25,000 to $2,000,000* |

| Units per Property | 1 – 4 |

| Eligible Property Types | Non-owner occupied residential (1-4 unit), including single-family homes, condos, duplexes, triplexes, quadplexes, and townhomes |

| Minimum Property Size | Single-family: 700+ SQFT; Condo/2-4 units: 500+ SQFT per unit |

| Maximum Acreage | 5 acres |

| Loan-to-Cost (LTC) | Up to 90% purchase, 100% rehab |

| Loan-to-ARV (LTARV) | Up to 75% |

| Down Payment (minimum) | $10,000 if purchase price is under $100,000 |

| Loan Term | 12 months standard; 18–24 months available for select projects |

| Extensions | Up to 50% of original loan term (fees apply) |

| Points | 1.5 to 2 points ($2,000 minimum fee) |

| Prepayment Penalty | None |

| Occupancy | Non-owner occupied — business use only |

| Transaction Types | Purchase or refinance (arms-length only) |

| Geographic Availability | All U.S. states except AK, AZ, HI, MN, ND, NV, OR, SD, UT, VT |

| Amortization | Interest-only with balloon payment at maturity |

| Interest Accrual Method | Under $100K: full boat; $100K or more: as disbursed |

Extensions

While bridge loans are designed as short-term financing solutions (typically 12 to 24 months), we recognize that some projects may require additional time. Our Montana bridge loan program offers extension options — though we recommend viewing these as contingency plans rather than primary strategies.

Extending your bridge loan increases borrowing costs and carries the risk of foreclosure if the loan remains unpaid after the extension period.

Common Causes of Project Delays:

Inexperienced or unreliable contractors

Overly aggressive rehab plans beyond your capacity

Slow permitting processes in certain municipalities

Inherited tenants with active leases or eviction needs

Lack of a clear dual exit strategy (sell or refinance)

By identifying and controlling these risks upfront, you can keep your Montana real estate project on schedule and avoid the need for an extension.

Extension Limits for Montana Bridge Loans

If your Montana bridge loan isn’t fully paid off by the end of the original loan term, you have the option to extend the loan for up to 50% of the original loan term. Extensions are available in either 3-month or 6-month increments, depending on the needs of your project.

| Initial Loan Term | Maximum Extension Period |

|---|---|

| 12 months | Up to 6 months |

| 18 months | Up to 9 months |

| 24 months | Up to 12 months |

While extensions are available to offer flexibility, they should always be viewed as a backup plan — not a core part of your investment timeline. The strongest Montana investors focus on accurate project planning from the start to minimize the need for costly extensions.

Extension Terms and Fees for Montana Bridge Loans

If an extension becomes necessary on your Montana bridge loan, the following fee structure will apply. These fees will be added directly to your payoff statement when the loan is settled.

| Extension Term | Fee |

|---|---|

| 3 months (1st extension) | 1% of the total loan amount |

| 3 months (2nd extension) | 1.5% of the total loan amount |

| 6 months (1st extension) | 2.5% of the total loan amount |

Prerequisites for Extension Approval

Your builder’s risk insurance policy must remain active and valid for the entire duration of the extension period.

OfferMarket may request updated documentation depending on the progress and specifics of your Montana investment project.

Staying prepared and maintaining clear communication throughout your loan term helps ensure a smooth extension process if one becomes necessary.

Ineligible Property Types for Montana Bridge Loans

Certain types of properties fall outside the scope of our Montana bridge loan program due to their higher risk profile, unique use cases, or liquidity challenges. Here’s a list of property types that are not eligible for this program:

Mixed-use properties

Multifamily properties with 5 or more units

Condotels and co-ops

Mobile or manufactured homes

Commercial buildings (retail, office, industrial)

Cabins and log homes

Properties with active oil or gas leases

Working farms, ranches, or orchards

Seasonal or vacation rentals

Unusual, luxury, or exotic properties

Properties accessed by unpaved or dirt roads

These exclusions help maintain the financial integrity of the Montana bridge loan program and ensure responsible lending across all deals.

Exception Scenarios

In certain cases, exceptions to our standard guidelines may be considered on a case-by-case basis. Here are some of the situations where exceptions might apply for your Montana investment project:

| Exception Scenario | Details |

|---|---|

| Credit score between 660–679 | May be eligible depending on other strengths |

| Leasehold properties (ground rent) | Additional underwriting review required |

| Small property size | Single-family: 500–699 sq ft; 2–4 units: 400–499 sq ft per unit |

| Initial advance based on higher As-Is value | Requires solid supporting documentation |

| Non-arm’s-length transactions | Underwriting review required |

| Financed interest payments | May be available to preserve liquidity |

If you believe your deal qualifies for one of these exceptions, reach out to our team — we’re happy to evaluate the specifics of your Montana bridge loan scenario.

Borrower and Guarantor Eligibility for Montana Bridge Loans

| Item | Requirements / Eligibility |

|---|---|

| Borrowing Entities | Must be an LLC or Corporation (nonprofits not eligible) |

| Eligible Borrowers | U.S. Citizens, U.S. Permanent Residents, or approved Foreign Nationals |

| Foreign Nationals | Must provide a valid passport and U.S. Visa (travel/student visas not accepted unless under the Visa Waiver Program); U.S. FICO score required for guarantor role |

| Credit Requirements | Minimum FICO score of 680 (scores between 660–679 may be considered under exception review); Tri-Merge credit report required (no older than 120 days) |

| Liquidity Requirements | Guarantors must show enough liquidity to cover estimated cash to close plus 25% of the rehab budget |

| Guaranty Structure | At least 51% of the borrowing entity must personally guarantee the loan for purchases; 100% guarantor requirement for cash-out refinances |

| Aggregate Guarantor Net Worth | Combined net worth of guarantors must equal at least 50% of the total loan amount |

Liquidity Verification for Montana Bridge Loan Eligibility

To reduce risk and promote sound investing, we require verification that all guarantors hold sufficient liquid assets to cover their financial obligations. This process helps confirm that you’re well-positioned to handle unexpected expenses.

The required liquidity amount is calculated as:

Estimated cash to close + 25% of your rehab budget.

Approved Liquid Asset Types:

Personal bank accounts

Business bank accounts under the borrowing entity

Bank accounts under other business entities (if applicable)

Personal brokerage accounts

Brokerage accounts owned by the borrowing entity or other business entities

Retirement accounts in personal name (subject to a 50% reduction for calculation purposes)

Note:

Business accounts are not required but recommended for good financial organization.

Funds don’t need to be transferred into the borrowing entity’s account — we simply verify that the funds exist and are accessible.

Cash to close is confirmed via your settlement statement, showing your borrower contribution wired to the title company.

This liquidity verification approach protects your Montana bridge loan investment by ensuring you’re financially equipped for the entire project lifecycle.

Credit and Background Evaluation for Montana Bridge Loans

Every Montana bridge loan application undergoes a thorough credit and background screening to ensure responsible lending and reduce project risk. Here’s what you can expect from our review process:

| Scenario | Requirement / Result |

|---|---|

| Three credit scores available | The middle score (2nd highest) will be used |

| Two credit scores available | The lower of the two scores will be used |

| No mortgage tradelines on credit report | Must maintain 6 months of interest reserves |

| Fewer than 5 tradelines | 6 months of interest reserves required |

| Bankruptcy history | Must be discharged at least 4 years prior to settlement |

| Foreclosure history | Must be completed at least 4 years prior to settlement |

| Bankruptcy or foreclosure within 4–7 years | Requires at least 3 months of interest reserves |

| Late mortgage payments within the past 12 months | Letter of Explanation (LOE) required; subject to loan committee review |

| Past due balances (mortgage or non-mortgage) | All past due amounts must be cleared before funding |

| Involuntary liens or judgments | Must be fully paid off prior to loan funding |

| Pending civil lawsuits | LOE required; subject to loan committee discretion |

| Pending criminal cases | Not eligible for funding |

| History of financial crimes | Not eligible for funding |

| Serious criminal offenses | Not eligible for funding |

| Repeat criminal offenses | LOE required; subject to loan committee review |

Our goal is to work with Montana investors who are positioned for success and demonstrate strong financial responsibility.

Interest Reserve Requirements

Depending on your credit score and background, we may require interest reserves to be held at closing. These reserves help ensure that interest payments are covered during the initial stages of your loan period, providing a buffer before monthly payments begin.

| Interest Reserve Scenario | Reserve Requirement |

|---|---|

| 0 months | At lender’s discretion |

| 1 month | Required if guarantor’s FICO score is 700 or higher |

| 3 months | Required if guarantor’s FICO score is between 660–699 |

| 6 months | Required if FICO score is between 660–699 and/or if other credit or background factors raise concern |

This structure allows us to support Montana investors while maintaining a focus on financial safety for all parties involved.

Financed Interest Payments

To support your liquidity during the rehab phase, you may qualify for financed interest payments under the Montana bridge loan program. This option allows accrued interest to be added to your loan payoff balance instead of requiring monthly payments, giving you more flexibility to focus on the project.

Example of Financed Interest Calculation:

| Calculation Item | Amount |

|---|---|

| Total loan amount | $100,000 |

| Interest rate | 12% |

| Loan term until payoff | 9 months |

| Total accrued interest | $9,000 ($100,000 × 12% ÷ 12 months × 9 months) |

| Payoff statement | $100,000 principal + $9,000 accrued interest |

This structure allows Montana investors to preserve cash flow during renovations, helping to avoid liquidity strain while work is underway.

Property Sourcing Guidelines

When sourcing properties for your Montana bridge loan, our focus is on transparency, deal quality, and responsible underwriting. Here are key sourcing requirements:

If you are entering a new market, you must provide either a signed agreement with a General Contractor (GC) or submit a Letter of Explanation (LOE) stating why a GC is not needed for your project.

Deals involving prior sale price increases, wholesale transactions, or non-arm’s-length relationships require additional documentation and will undergo detailed review.

For condominiums, conversion projects, or major rehab efforts, we may require supporting documents from licensed architects, engineers, or relevant permits to verify the scope of work.

Each loan submission must include:

Purchase contracts

Settlement statements

Payoff letters (if applicable)

Your investor track record

LLC or Corporation formation documents

These guidelines help ensure that every Montana bridge loan we fund is backed by a solid, well-structured deal.

Bridge Loan Insurance Guidelines

Protecting both your property and your liability is a crucial part of a successful Montana bridge loan project. Builder’s Risk Insurance (also known as Fix and Flip insurance) is required throughout the life of your loan. This policy is specifically designed for properties under renovation, vacant homes, or distressed real estate.

Required Coverages and Limits

| Coverage Type | Limit | Required |

|---|---|---|

| Dwelling | Replacement Cost or Loan Amount (zero coinsurance) | Yes |

| Liability | $1M per occurrence / $2M annual aggregate | Yes |

| Builder’s Risk | Included | Yes |

| Flood | Greater of $250,000 or the loan balance (only if in FEMA flood zone) | Only if applicable |

Coverage Details

| Requirement Item | Requirement |

|---|---|

| AM Best Rating | A- VIII or higher |

| Policy Type | Special Form |

| Deductible | Between $1,000 and $5,000 |

| Lender’s Designation | OfferMarket listed as Mortgagee and Additional Insured |

| Policy Exclusions | Must not exclude windstorm, hail, or named storm coverage |

| Cancellation | Policy must provide a 30-day cancellation notice |

💡 Pro Tip:

Once you take possession of the property, we strongly recommend installing smoke detectors, door locks, and security cameras immediately. These basic safety measures help ensure that your insurance remains valid and protect against potential claims issues.

Frequently Asked Questions

What states does OfferMarket fund bridge loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have more than one bridge loan at the same time?

Absolutely. Many investors working with OfferMarket have multiple Montana bridge loans active at the same time. However, our team will always prioritize your financial safety. If we believe that taking on additional projects could stretch your liquidity too thin or put your execution ability at risk, we will raise this concern and work with you on a safer game plan.

Are bridge loans considered commercial loans?

Yes. All Montana bridge loans offered through OfferMarket are classified as business-purpose commercial loans. These loans are issued to your business entity (LLC or Corporation) and are not considered consumer-purpose or personal loans.

What is the minimum loan amount available?

The minimum loan size for our Montana bridge loan program is $25,000.

Which types of properties qualify for funding?

We fund non-owner occupied 1-4 unit residential properties across Montana. Eligible property types include:

Single-family homes

Townhomes

Duplexes, triplexes, and quadplexes (2-4 unit multifamily)

Warrantable condominiums

Note:

Mixed-use properties with 2-4 units, larger multifamily (5+ units), and commercial buildings such as retail or office spaces are not eligible for this program but may qualify for financing through other OfferMarket products.

How is Loan-to-Value (LTV) calculated for Montana bridge loans?

In the context of our Montana bridge loan program, LTV typically refers to Loan-to-After-Repair Value (LTARV) — though in some scenarios, it may refer to Loan-to-As-Is Value, depending on your project.

For purchase transactions, the initial advance is calculated using the lesser of:

The As-Is value (from an appraisal or valuation report), or

The purchase price (listed in your contract or shown on your settlement statement if it’s a refinance).

LTARV is determined by dividing your total loan amount (initial advance plus construction holdback) by the projected after-repair value of the property.

What credit score do I need to qualify?

A minimum FICO score of 680 is required to qualify for our Montana bridge loan program. If your score falls between 660 and 679, your application may still be considered under an exception review process.

We focus on the credit scores of the individuals within your business entity who will personally guarantee the loan. Scores from members who are not guarantors are not factored into the decision.

Do I need previous real estate investing experience to qualify?

No prior experience is required to be eligible for a Montana bridge loan through OfferMarket. However, the more real estate projects you’ve successfully completed, the better your potential loan terms and leverage.

Our experience-based tier system rewards investors who have a proven track record, allowing for higher initial advances and greater flexibility. When you complete the Track Record section in your Loan File, we verify your experience by reviewing settlement statements or other supporting documents.

Does wholesaling count toward experience?

No, wholesaling does not count toward your experience score in our system. Our experience tiers are based on deals where the investor took direct financial responsibility for completing the rehab work — not simply acting as an intermediary.

We believe that managing renovations, overseeing contractors, and successfully completing projects is what demonstrates true experience.

What documentation is required for a Montana bridge loan?

Our Loan File system makes documentation easy and efficient. The documents we require will depend on whether your Montana bridge loan is for a purchase or refinance.

Purchase Transaction Documentation:

| Loan File Section | Required Documentation |

|---|---|

| Loan File | Completed Loan File |

| Purchase Contract | Fully executed agreement between buyer and seller |

| Credit Report | Soft Tri-Merge credit report for each guarantor |

| Background Report | Required for every member of the borrowing entity |

| Track Record | Completed for each guarantor |

| ID Verification | Government-issued ID (driver’s license, passport, or Green Card) |

| Borrowing Entity | Articles of Organization/Incorporation, Operating Agreement/Bylaws, Certificate of Good Standing, W-9 |

| Scope of Work | Detailed rehab budget for determining ARV |

| Appraisal Report | Ordered through OfferMarket (invoice must be paid before closing) |

| Bank Statements | Two most recent statements for each guarantor (personal, business, or retirement accounts) |

| Letter of Explanation (LOE) | Required if requested by underwriting (e.g., large deposits, late payments, background items) |

Refinance Transaction Documentation:

| Loan File Section | Required Documentation |

|---|---|

| Loan File | Completed Loan File |

| Settlement Statement | From your original purchase closing |

| Credit Report | Soft Tri-Merge credit report for each guarantor |

| Background Report | Required for each member of the borrowing entity |

| Track Record | Completed for each guarantor |

| ID Verification | Government-issued ID (driver’s license, passport, or Green Card) |

| Borrowing Entity | Articles of Organization/Incorporation, Operating Agreement/Bylaws, Certificate of Good Standing, W-9 |

| Sunk Costs | List of all costs incurred to date (purchase plus rehab expenses) |

| Scope of Work | Detailed rehab budget if applicable |

| Appraisal Report | Ordered via OfferMarket (must be paid prior to closing) |

| Bank Statements | Two most recent statements for each guarantor (personal, business, or retirement accounts) |

| Letter of Explanation (LOE) | Required if requested by underwriting |

Are there special requirements for loans over $1 million?

Yes. For Montana bridge loans over $1 million (up to the program maximum of $2 million), additional underwriting applies:

| Criteria | Requirements |

|---|---|

| Experience | Minimum of 3 completed projects, preferably at similar or higher price points |

| Market Liquidity | At least 3 comparable sales within a 2-mile radius, closed on the MLS in the past 6 months |

| Credit Score | Minimum 680 FICO, with at least 5 tradelines showing a 24-month history |

| Rural Designation | Properties classified as rural are not eligible for loans over $1 million |

| Track Record | Required for each guarantor involved in the deal |

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit — a separate, self-contained living space on the same property as the primary home. |

| Arms-length | A deal where buyer and seller have no personal, financial, or business relationship, ensuring fair market terms. |

| Non Arms-length | A transaction where the buyer and seller are related or connected, potentially influencing pricing or terms. |

| Initial Advance | The upfront portion of your Montana bridge loan used to fund the property purchase. Funds are wired directly to the title company at closing. |

| Construction Holdback | The part of your loan reserved for rehab costs, released to you through draw reimbursements as renovation work is completed. |

| Interest Reserves | Funds held at closing to cover interest payments during the early loan period before monthly payments begin (if required). |

| LOE (Letter of Explanation) | A document providing details to explain credit issues, large deposits, or other underwriting questions. |

| LTC (Loan-to-Cost) | The ratio of your loan amount to the total cost of your project (purchase price plus rehab budget). |

| LTFC (Loan-to-Full-Cost) | The ratio of your loan amount to the full project cost, used for projects where rehab exceeds the purchase price or As-Is value. |

| LTV (Loan-to-Value) | The ratio of your loan amount to the property’s current As-Is value before rehab. |

| LTARV (Loan-to-After-Repair Value) | The ratio of your loan amount to the property’s projected value after the renovations are completed. |

| As Disbursed Interest | Interest that accrues only on the portion of the loan that has been funded (initial advance plus disbursed holdback). |

| Full Boat Interest | Interest that accrues on the full loan amount, including undrawn construction holdback, from day one. |

| Lopsided Deal | A project where the rehab budget is higher than the purchase price or As-Is value, triggering specific leverage limits (LTFC). |

| GC Agreement | A signed contract with a General Contractor outlining the scope of work, roles, and rehab plan for your investment property. |

| DSCR (Debt Service Coverage Ratio) | A calculation of rental income divided by debt obligations (Principal, Interest, Taxes, Insurance, and HOA dues), used to evaluate refinance scenarios. |

Instant Montana Bridge Loan Quote

At OfferMarket Capital LLC, our mission is to help Montana real estate investors succeed through fast, flexible, and reliable financing. Our private lending division specializes in bridge loans and DSCR loans designed specifically for 1-4 unit residential investment properties across Montana.

Thousands of real estate investors trust OfferMarket each month to fuel their next investment project. Our membership is completely free and gives you access to:

💰 Direct private lending solutions

☂️ Easy insurance rate shopping for optimal coverage

🏚️ Exclusive off-market investment opportunities

💡 Access to insightful market data and investing tools

If you're ready to take the next step toward securing your Montana bridge loan, click below to get your instant quote today and see how we can support your success.

Thousands of real estate investors get value from OfferMarket every month. Membership is entirely free and includes the following benefits:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights