*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Investment property loans - What options are out there?

Investing in real estate can be an excellent way to build wealth, but it requires careful consideration and planning. When it comes to financing an investment property, there are many options available. From traditional loans to alternative financing, it's essential to understand the pros and cons of each option to make an informed decision.

In this blog post, we'll explore the different types of financing available for investment properties and answer some of the most common questions on the topic. We'll discuss the benefits and risks of each type of financing, so you can determine which option is best for your investment goals.

Whether you're a seasoned real estate investor or just starting out, understanding the financing options available can make all the difference in the success of your investment. By the end of this post, you'll have a comprehensive understanding of the range of financing available, and be able to make an informed decision on how to fund your investment property. Lets dive in with a 30,000 ft overview of how to get an investment property loan to give us broad context for the rest of the article when we discuss each individual option.

How to get a loan for investment property?

A high-level overview of the steps involved in getting a loan for an investment property, assuming a generic loan product such as a debt-service-coverage-ratio DSCR loan:

Determine your investment property key performance indicators (KPIs). Before you start looking for a loan, you need to have a clear understanding of your investment parameters. After learning the target market, perfectly understanding what property type you want to pursue and why, you need to create an excel spreadsheet with all the information regarding your target parameters and how properties you are focusing on fit those criteria. Its vital to have written down estimates of expected rent, expected expenses and reserves that should be accumulated to protect your investment.

Optimize your financial situation for the moment of underwriting

In this step you pay off as much of your short term debt (credit card debt) as possible. There is a common misconception that outside of banking credit score doesn't matter. This is absolutely not the case and while credit scores are not perfect, they are used by every single lender in the ecosystem. Having a score above 720+ will provide you with the best terms on any funding you seek, which will add up to thousands of dollars over the life of a loan, thus it makes sense to pay off a couple of grand of credit card debt to enable long term wealth building. Apart from raising your score, making sure your any bankruptcies are far in the past and any issues with criminal background are expunged. Its vital that any expungements take effect well before any checks because even if they expungements were ordered but not executed and there are still blemishes on the background report (everyone deserves a 2nd chance, but not 3rd), and lenders sees them on the credit report, their hands might be tied since that report becomes part of the loan file. Finally, increasing your bank account cash cushion could be the final and best way to improve your chances to get a loan on great terms. If lender reviews your bank account or brokerage accounts and sees 50%-100% of the loan value in fairly liquid assets they will view you almost completely de-risked, giving you better negotiating leverage when it comes to loan terms.

Prepare your financial documents

Lenders will require financial documents such as tax returns (depending on the loan product, only banks and credit unions require income verification for investment properties), bank statements, appraisal report (potentially with addendums such as As Is 1004 and 1007 Rent Schedule, or As Is 1025, lender will most likely order this), LLC documents if applicable, such as certificate of good standing or certificate of existence depending on the state, formation documents, operating agreement, information about any of your partners, your credit and background reports (lender will most likely order these), track record about houses you've owned, rented or rehabbed, state issued ID, tax bills, leases, insurance, settlement statements from previous closing, proof of rent or security deposit receipt. These are just some of the documents that could come up and depending on loan product you decide to use might not be required at all.

Research lenders

Now that you are armed with all this information, you are well prepared to start researching lenders that might extend the type of financing you ultimately choose for your investment property. The best place to research lenders is online and through personal references. Apart from building your own list of lenders in excel after running a few search engine searches for keywords such as "investment property loans" or more specific terms related to the product you decide to pick "DSCR loans" or "Fix and flip loans" for example. Finding specialized shops that deal with fewer loan product types might result in better rates or experience and it isn't true across all loan products so its definitely worth your time to build a list of potential lenders in excel and compare their loan product offerings across many dimensions such as rates, fees, reputation, experience, online experience and others.

Apply for the investment property loan

Once you pick the best lender according to the criteria you have established its time to apply. Each lender will have slightly different process for how they accumulate documents for a loan file so you should ask some questions about what they require. You should be well prepared for this from previous steps. Usually, to get the best results and ensure the smoothest lending process, provide as many and all documents you can to the lender on day 1. This will allow the lender to review the documents and give you feedback that you can correct quickly. The most common thing we see is certificate of good standing is expired and you need to order a new one from the state which can take a few business days if your state doesn't have online access for this service. Lender Underwriting and appraisal takes place next. After you submit your loan file with all the lender required documents, the lender will conduct underwriting to evaluate the deal. They will also calculate the debt-service-coverage-ratio (DSCR) to determine if the deal meets their requirements for loan approval. Keep in mind, the deal is underwritten to standards that are predetermined with investors into this type of debt so often these standards are not flexible such as credit score cut offs. If your lender allowed an exception, its often would be the case is that your loan would not be re-sellable, which is one of the main reasons for lower interest rates (since re-sale allows intermediaries to lower their own risk profile). If the secondary market for these loans didn't exist, 20-30% interest rates would be the standard.

Underwriter approval, closing and funding can commence.

At this point, title company or a real estate attorney (depending on the state requirements of the transaction) should have been in contact and initiated processing of your title order to start inching closer to closing. The rest of the closing process involves signing loan documents and paying any closing costs. Once all the documents are in order title gives the go ahead to release the funds from escrow and you should see funding hit your bank account.

What type of loan is best for investment property?

This is a very open ended questions. Its depends. What type of investment property is it? Is it a condo? Single family rental? Quadplex!? What condition is the property in? Are you planning on renovating it at all? What about increasing livable square footage? Without knowing answers to these and many more questions its impossible to prescribe a single definitive answer. What we can do is present a huge variety of options and detail their benefits and risk so the reader may make their own decision in regards to which financial instrument, tool of their investment trade, they should employ to achieve their financial goals.

- Bank investment property loans These loans are extended to individuals from banks to fund their investment properties. Usually these loans are at premium to retail mortgage loans since they are not owner occupied. These are ideal loans for someone just starting out with their investment property career. These loans are seldom used by experience real estate investors due to a major eligibility requirement presented by banks, a W-2 income. While someone just starting out might still have their W-2 job and a higher credit score, they may easily qualify for this loan from the bank to get started. However after a few properties with this type of funding, banks will start to consider you an elevated risk and may stop lending to you for you 5th and on property. Another reason experienced real estate investors seldom use this loan is because they are self-employed and receive distributions from their businesses that own and rent out properties, thus they don't have any W-2 income that they can show to the bank to qualify for the loan.

- FHA loans Only in rare circumstanced such is when you are house hacking can FHA loans can be used for investment properties. FHA loans are designed to enable low income families to afford their homes. One provision of the FHA programs allows for 1-4 unit multifamily properties where you are living and occupying one of the units and renting the others out is allowed.

- VA loans Same as FHA loan. The only time you can use this type of funding for an investment property is when you are house hacking.

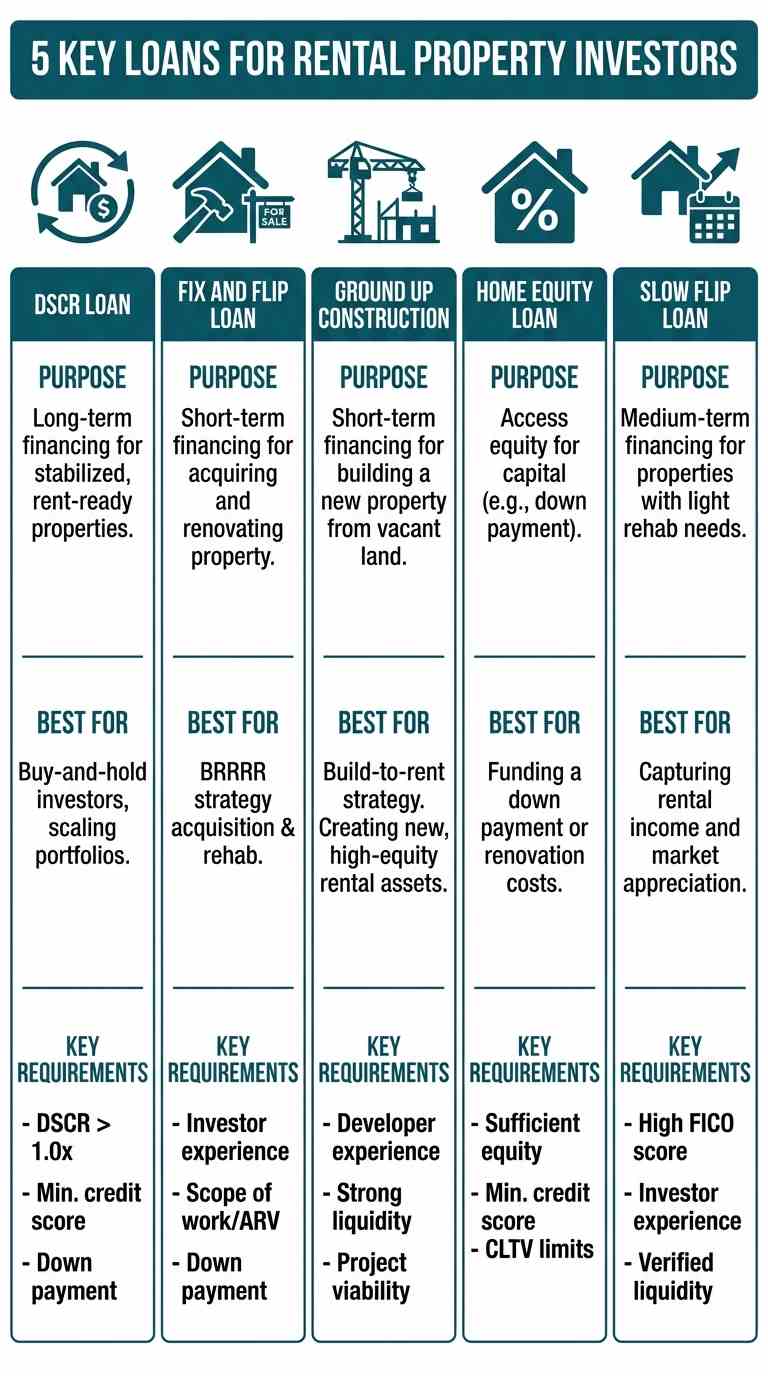

- Hard money loans These are short-term loans that are secured by the property itself, rather than the borrower's income. Hard money loans often have higher interest rates and fees, but a great option compared to methods that have higher interest rates and don't require W-2 verification, making it an ideal tool for experience real estate investors. Since hard money loans are based on the quality of the deal, the investor can keep getting as many loan as good deals they can find and have enough of the skin-in-the-game in terms of down payment. Hard money loans are essential for the BRRR method's repeatability, because you can get a hard money "Fix and Flip loan" or "Bridge loan" to have funds to Buy, and Rehab, then Rent and use a hard money "DSCR loan" to Refinance and complete the cycle of BRRR Method.

- Portfolio loans Portfolio loans are offered by private lenders and are not sold to investors. These loans may offer more flexible terms and underwriting requirements than traditional loans, but obviously a pre-requisite is that there are multiple properties that are being used for the purpose of this loan and its just provides a slight discount to doing similar type of funding but for each property individually.

- Bridge loans Bridge loans are short-term loans that are used to bridge the gap between buying a new property and selling an existing one. These loans may have higher interest rates and fees but offer quick funding and flexible repayment terms. These are typically used for BRRR Method and provide funding for the first 2 steps of the method, Buy and Rehab. These loans have a usual term of between 6 and 18 months and have a 2 components, one for the purchase price and another for the rehab budget thus making it an ideal tool to use when investment property needs to be rehabed.

- Home equity loans Home equity loans allow homeowners to borrow against the equity in their primary residence to finance an investment property. These loans may have lower interest rates than other types of loans but may put your primary residence at risk if you default on the loan. This type of financing exposes your primary residence and is probably not ideal way to start your real estate investment career. If you already have a home and a mortgage, its a better options to accumulate cash then increasing leverage. Keep this option in your back pocket for the future if necessary in the worst of the scenarios, kind of like in the game of Monopoly, you only mortgage your properties when you are in a jam for cash.

- Cash-out refinance A cash-out refinance allows you to refinance your existing mortgage for more than you owe and use the difference to finance an investment property. This option may offer lower interest rates than other types of loans but will increase your mortgage payment and may have higher closing costs. However, this is the tool that closes the loop of the BRRR Method. When you cash-out refinance out of your property you complete the last step of BRRR Method, the Refinance step. Hard money DSCR loans are the ideal product to refinance your repaired, tenant occupied rental into a 30-year fixed product and allow you to pull out all of your invested cash so you can repeat the BRRR Method from the start on another property.

- Seller financing Seller financing is when the seller of the property provides financing for the buyer. This option may offer more flexible terms and lower closing costs but may require a larger down payment and higher interest rates. Seller financing is all about relationships. If you have established understanding with the seller and you both agreed to the fair terms then it might be the right options. However, things change and its still advisable to seal the deal with at least a 1 page contract so you have some kind of paper trail. For every 100 successful cases of seller financing we have seen, there was always one disaster that wasn't good for anyone and contracts help reach mutual understanding.

- Crowdfunding Crowdfunding allows investors to pool their money to finance a real estate project. This option may offer lower minimum investments and higher potential returns, but may also be riskier than traditional loans. This method will require some elbow grease and a certain set of skills. If you have a dynamic personal network that is looking for opportunities and you have good personal reputation in this space, this might be a great way to raise some capital for your next investment opportunity. Other then networking, calling and shaking every corner of your network you will also have to become educated on the LLC partnerships and ways to fund your next investment and appropriate legal structures to surround yourself and limited partners with. Any time you collect investors money you run the risk of being considered an investment adviser which has its own compliance burdens, however for the purpose of real estate investing there are many other vehicles that can be employed to stay clear of that classification, such as a normal limited liability company (LLC) for example.

- Mezzanine loans Mezzanine loans are a type of financing that sits between debt and equity. These loans may have higher interest rates than other types of loans, but also offer more flexible repayment terms and may allow for a smaller down payment. Exotic loans types such as mezzanine loans, while a powerful tool if employed correctly, are full with pitfalls in the form of loan covenants. Having a competent and tested lawyer that specialized in real estate law review all your loan documents is essential when it comes to this product to stay safe.

- 1031 exchanges A 1031 exchange allows real estate investors to sell a property and reinvest the proceeds in a similar property without paying capital gains taxes known as depreciation recapture. This option requires strict adherence to IRS guidelines and may require the assistance of a qualified intermediary. One advantage of owning real estate is the annual depreciation that can be used against rental income, thus significantly reducing the tax liability. However, IRS made a provision to 'recapture' this depreciation reduction through what is known depreciation recapture process during the sale of an investment property. So if you ever sell and investment property outside of 1031 exchange you will have to pay depreciation recapture taxes, thus perpetually locking your capital in rental business (which is arguably a great thing from the perspective of growing you net worth).

- Private money loans Private money loans are loans provided by individual investors rather than traditional lenders. These loans may offer more flexible terms and faster funding than other types of loans, but may also come with higher interest rates and fees. These loans are similar in nature to hard money loans described above in terms of pricing, duration and collateral type. The only distinction is that it comes from an individual rather then an organization. Sometimes due to this personal relationship, your reputation and track record play a huge part in securing the loan versus document submissions required for extensive verification in the case of hard money lending businesses.

- Equity financing Equity financing involves selling ownership shares in a property to investors. This option may offer the potential for high returns and may not require regular payments, but may also require giving up some control over the property and sharing profits with other investors. This is viewed similarly to getting a home equity loan from the risk profile. Why increase leverage on something that you depend on unless you are absolutely locked into a corner. This is not an appropriate method of funding for an growth project such as acquisition of an investment property.

Can you use a VA loan for an investment property?

Its allowed for house hacking. There are some limited circumstances where a VA loan may be used for a multi-unit property if the borrower lives in one of the units as their primary residence. VA (Department of Veterans Affairs) loans are designed to help active-duty military personnel, veterans, and their eligible spouses purchase homes to live in as their primary residence and are not typically used for investment properties or second homes. In fact, using a VA loan for an investment property that is not owner-occupied or second home would be considered mortgage fraud and could result in serious legal consequences unless the criteria listed above is met.

Can you use FHA loan for investment property?

Only time you can use FHA loan for an investment property purposes is when you are house hacking. FHA loans are designed for owner-occupied properties, which means that they are not typically used for non-owner occupied properties such as investment properties. The primary purpose of FHA loans is to help individuals and families purchase homes to live in as their primary residence. However, there are some limited circumstances where an FHA loan may be used for a non-owner occupied property, such as a multi-unit property where the owner lives in one of the units and rents out the others. In these cases, the borrower must meet strict FHA guidelines and requirements, and the loan may have higher interest rates and more restrictive terms than loans designed specifically for investment properties. It's important to consult with a lender who is experienced in FHA loans to determine whether this type of financing is a viable option for your non-owner occupied property.

Can you use SBA loan for investment property?

No, SBA loans cannot be used for investment non-owner occupied properties. SBA loans are intended to help small businesses with their financing needs, and they have specific guidelines for how the funds can be used. SBA loans can be used for things like working capital, equipment purchases, inventory, and real estate purchases for the business owner's primary place of business.

What loan document says the property is an investment property?

There is not one specific loan document that declares a property to be an investment property. The main distinction if its an investment property, is it owner occupied. The classification of a property as an investment property is determined based on its use and the intention of the owner. In general, an investment property is a property that is purchased with the intention of generating income or profits from rental income, appreciation, or other means while not being occupied by its rightful owner. If you are applying for a loan to purchase an investment property, the lender may ask for documentation that supports the property's classification as an investment property.

Here are the documents that can be used to prove that the property is an investment property:

- Current lease agreement (signed with dates)

- Bank statements showing receipt of deposit and rent payment from tenant

- Tax documents such as IRS schedule E (1040-Schedule E, "Supplemental Income and Loss ") Part 1, showing you file for taxes for your rentals

Can you use USDA loan for investment property?

Yes, it is possible to use a USDA loan to purchase a 1-4 unit multifamily property, as long as you will be occupying one of the units as your primary residence. USDA loans have specific guidelines for multifamily properties, and they can be a great option for low- to moderate-income borrowers who are looking to purchase a property in an eligible rural area.

To qualify for a USDA loan for a multifamily property, you must meet the income and credit requirements, and the property must be located in an eligible rural area as defined by the USDA. In addition, you must occupy one of the units as your primary residence, and the property must meet certain property requirements, such as being structurally sound and meeting local building codes.

It's important to note that if you are purchasing a multifamily property with a USDA loan, the rental income from the other units cannot be used to qualify for the loan. The loan amount will be based on your income and ability to repay the loan, not on the potential rental income from the other units.

If you are considering using a USDA loan to purchase a multifamily property, it's a good idea to speak with a USDA-approved lender to discuss your options and determine if you meet the eligibility requirements.

Can I buy investment property with home equity loan?

Yes, but its a bad idea. A home equity loan, also known as a second mortgage, allows you to borrow against the equity you have built up in your primary residence. The funds can be used for a variety of purposes, including home improvements, debt consolidation, and in some cases, purchasing an investment property.

However, using a home equity loan to purchase an investment property can be risky, as you are using your primary residence as collateral for the loan. If you are unable to repay the loan, you could be at risk of losing your home. Additionally, interest rates on home equity loans can be higher than other types of loans, and you will need to factor in the cost of interest and fees when determining if this is a viable financing option for your investment property.

If you already own your residence and want to embark on the 'growth' project with risks such as real estate investing, your best option is waiting and saving a cash pile for the downpayment and even for the majority of the money required for your first investment property. This way you won't be starting your real estate career leveraged to the teeth, where one bad tenant can cascade to you living on the street. Experienced real estate investors take great lengths to establish separate LLCs for each property to insulate themselves and other rentals from this exact cascading effect that can make you bankrupt if you don't have appropriate reserves or legal protections.

Can I get an investment property loan without a job?

Job (W-2) isn't necessary but a source of income is. Self-employment income is the most common form of income seen in professional real estate investors since they use their businesses to pay themselves. It is vital to have a dependable source of income not only for the initial down payment but also for the unexpected costs that may arise during the course of the investment. Additionally, a stable income can help demonstrate to lenders your financial responsibility and your ability to repay their loans, which can increase your chances of obtaining favorable loan terms. Thus, it is crucial to ensure that you have a verifiable source of income and maintain a cash reserve to prepare for unforeseen circumstances while attempting to obtain an investment property loan.

Can you get a 203k loan on an investment property?

Yes, it is possible to obtain a 203k loan for a 1-4 multifamily property as long as you plan to live in one of the units as your primary residence. The FHA 203k loan program allows owner-occupants to finance the purchase or refinance of a property and the cost of renovation or rehabilitation in a single loan.

In the case of a 1-4 multifamily property, the owner-occupant must live in one of the units as their primary residence, and the other units must be rented out. The owner-occupant can use the 203k loan to make necessary repairs and renovations to the property, such as updating kitchens and bathrooms, repairing roofs and foundations, or adding new HVAC systems.

It's important to note that the 203k loan program has certain requirements and limitations, such as a minimum loan amount and specific eligibility criteria. Additionally, the property must meet certain standards for safety, livability, and energy efficiency. It's important to carefully research the program requirements.

Can you get a construction loan for an investment property?

Yes, it is possible to obtain a construction loan for an investment property. Construction loans are typically used to finance the construction of new homes or the renovation of existing properties. These loans provide funding for the construction or renovation phase of a project and are typically short-term, with repayment due once the project is completed.

Rehab, fix and flip, and bridge loans are all types of construction loans that are commonly used for investment properties. Rehab loans are used to finance the rehabilitation of an existing property that is in need of repair or renovation. Fix and flip loans are designed to finance the purchase and renovation of a property that will be sold quickly for a profit. Bridge loans are used to provide short-term financing for a property purchase until a more permanent source of financing can be obtained.

It's important to note that construction loans can be riskier than traditional mortgages, as there may be unforeseen complications or delays during the construction or renovation process. Additionally, interest rates and fees for construction loans may be higher than for traditional mortgages. It's important to carefully consider your financial situation and to consult with a financial advisor or mortgage professional before pursuing a construction loan for an investment property.

OfferMarket Loans

Check your rate

60 seconds · no credit pull