*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Hard Money Loans Explained: The 5-Step Guide to Get Funded

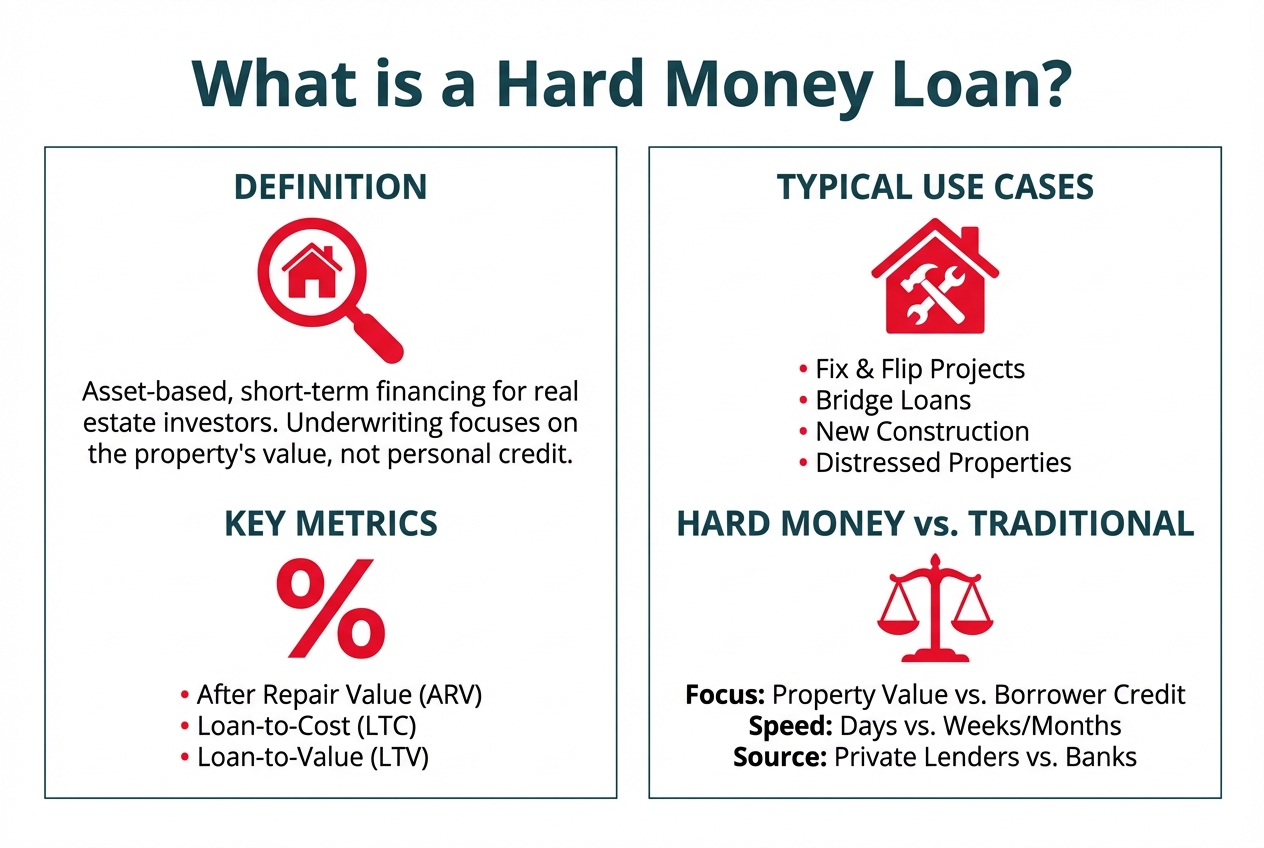

A hard money loan is a short-term, asset-based loan used by real estate investors to finance the purchase and renovation of a property. Unlike traditional mortgages that focus heavily on a borrower's credit score and income, hard money lending is primarily underwritten based on the value of the real estate collateral itself. The central metric is the property's After Repair Value (ARV)—its estimated market value once all proposed renovations are complete. Lenders also focus on the Loan-to-Cost (LTC), which is the loan amount as a percentage of the total project cost (purchase price plus renovation budget).

This focus on the property's potential value makes hard money loans an ideal financing tool for fix-and-flip projects, bridge loans to cover financing gaps, and new construction. Because the underwriting is streamlined and asset-focused, funding can occur in a matter of days rather than the weeks or months required for conventional bank loans. This speed allows investors to act quickly on time-sensitive opportunities, such as distressed properties or auction purchases, that traditional financing cannot accommodate.

The Hard Money Loan Process Step-by-Step

Understanding the hard money loan process demystifies how investors can secure financing so quickly. While specific steps can vary slightly between lenders, the core progression from application to funding is standardized across the industry. The entire process is designed for speed and efficiency, focusing on the economic viability of the project rather than the borrower's personal financial history. Here is a chronological breakdown of what to expect.

Step 1: Instant Quote and Experience Tiering

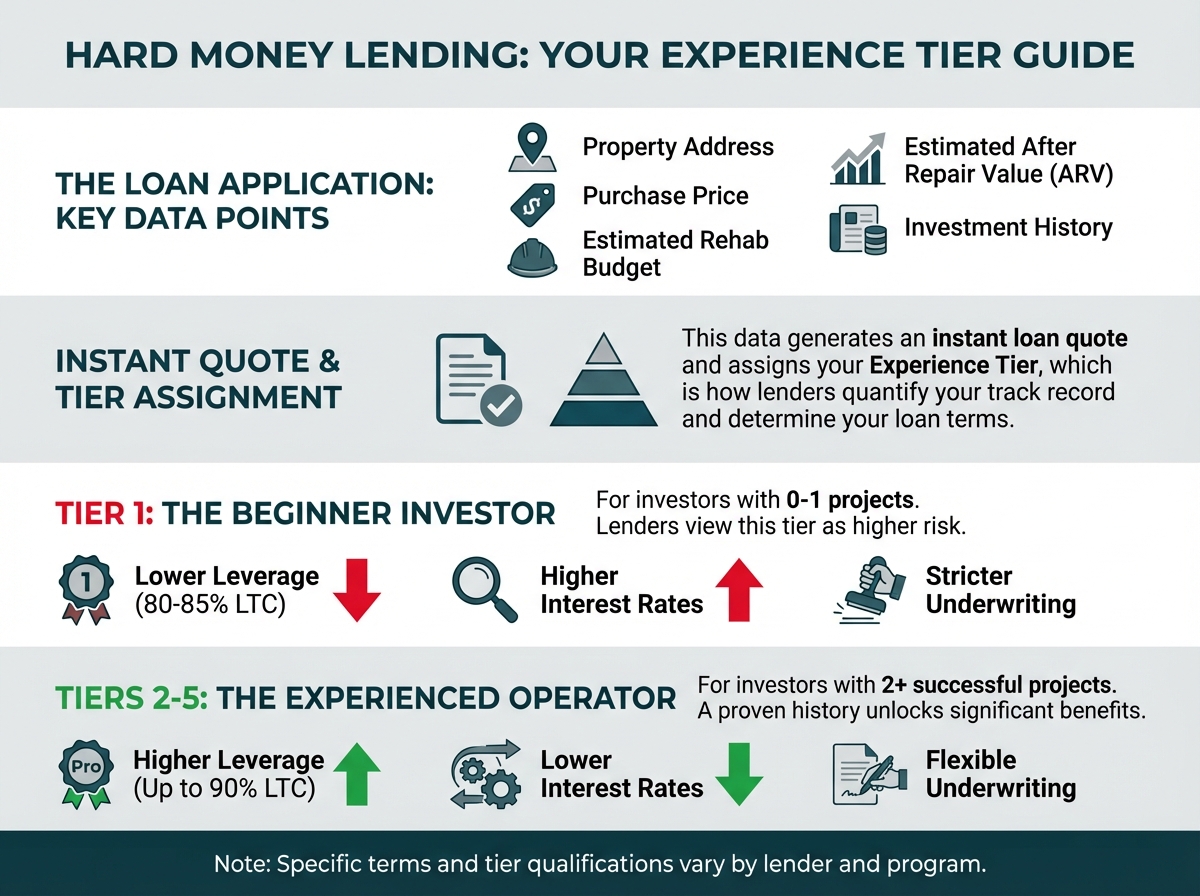

The journey begins with the initial loan application, which in modern lending platforms like OfferMarket is a streamlined digital process. You will provide high-level details about your project, including:

- Property Address: The location of the investment property.

- Purchase Price: The agreed-upon price in your purchase contract.

- Estimated Rehab Budget: A preliminary estimate of your construction costs.

- Estimated After Repair Value (ARV): Your projection of the property's market value after renovations.

- Investment History: A summary of your real estate investment experience, typically the number of similar projects completed in the last 12-36 months.

Based on this information, the lender’s system provides an instant loan quote. This preliminary offer outlines potential terms, including the interest rate, loan amount, leverage (LTC/LTV), and estimated fees. Crucially, this is also when the lender assigns you an Experience Tier.

Experience tiering is how hard money lenders quantify and reward a borrower's track record. It directly impacts the loan terms you receive.

- Tier 1 (0-1 projects): Inexperienced or first-time investors. Lenders view these borrowers as higher risk. As a result, Tier 1 borrowers typically face lower leverage (e.g., 80-85% LTC), higher interest rates, and stricter underwriting scrutiny. They may also be required to have more cash reserves.

- Tiers 2-5 (2+ projects): Experienced investors with a proven history of successful projects. As you move up the tiers, you unlock significant benefits: higher leverage (up to 90% LTC or more), lower interest rates, and a more flexible underwriting process. Lenders are more confident in the ability of an experienced operator to execute the business plan, manage the budget, and successfully exit the project.

Step 2: Document Submission for Formal Processing

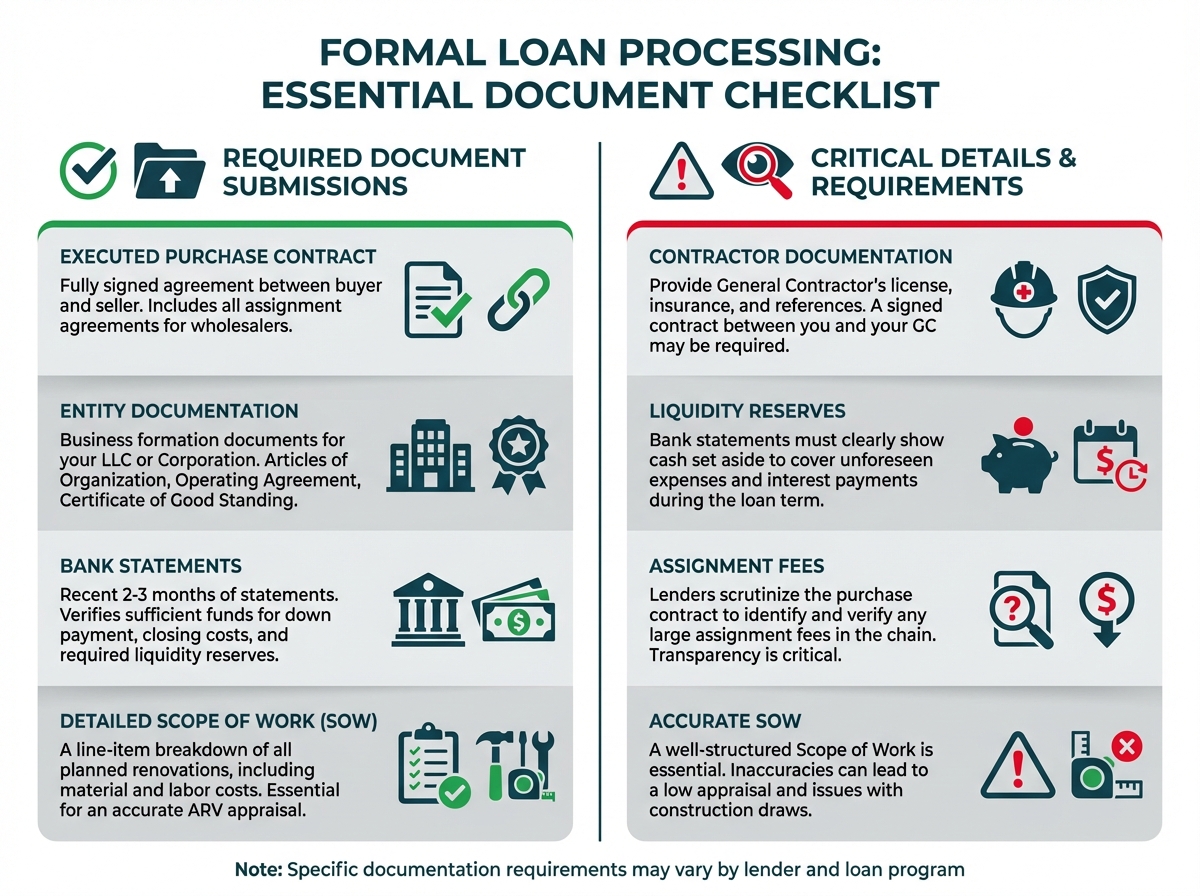

Once you accept the initial quote, the loan moves into formal processing. This is where you submit the detailed documentation that allows the underwriter to verify the project's details and your ability to execute it. The required package typically includes:

- Executed Purchase Contract: The fully signed agreement between you and the seller. If you are a wholesaler, this includes the original contract and all assignment agreements in the chain. Lenders scrutinize this to verify the purchase price and identify any large assignment fees.

- Entity Documentation: Hard money loans are commercial loans made to a business entity, not an individual. You will need to provide formation documents for your LLC or Corporation, such as the Articles of Organization, Operating Agreement, and a Certificate of Good Standing from the state.

- Bank Statements: You'll need to submit recent bank or brokerage statements (typically 2-3 months) to verify you have sufficient funds for the down payment, closing costs, and any required liquidity reserves. These reserves are cash set aside to cover unforeseen expenses and interest payments during the loan term.

- Detailed Scope of Work (SOW): This is one of the most critical documents. The SOW is a line-item breakdown of every planned renovation, including material and labor costs. A well-structured SOW is essential for an accurate ARV appraisal and for managing construction draws post-closing.

- Contractor Documentation: If you're using a General Contractor (GC), you may need to provide their license, insurance, and a list of references. Some lenders may also require a signed contract between you and your GC.

Step 3: Lender Underwriting and Property Valuation

With your documents submitted, the lender's underwriting team takes over. Their job is to validate the deal's viability and determine the final, approved loan amount. This involves several parallel processes:

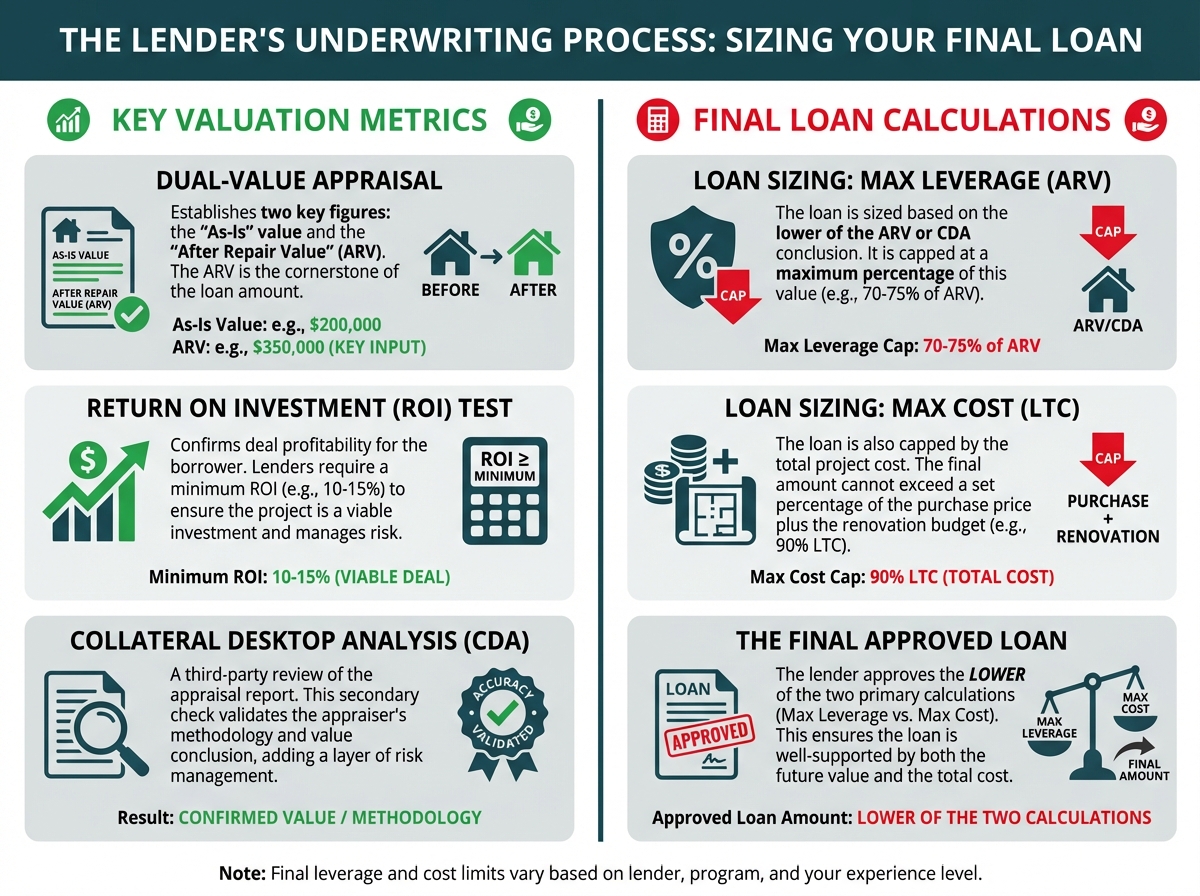

- The Dual-Value Appraisal: The lender will order an appraisal specifically for an investment loan. Unlike a standard appraisal, this report establishes two key values: the "As-Is" value of the property in its current condition and the "After Repair Value" (ARV) based on your detailed SOW. The appraiser will review your renovation plan, research comparable renovated properties (comps) in the area, and provide an expert opinion on what the property will be worth upon completion. The ARV is the cornerstone of the loan amount.

- The ROI Test: Lenders need to see that the project is profitable for you. They perform a Return on Investment (ROI) calculation to ensure there is a sufficient profit margin. A typical minimum requirement is a 10-15% ROI. This test confirms that after accounting for all costs (purchase, rehab, financing, closing, carrying, and selling costs), you will still make a healthy profit. If the numbers are too tight, the lender may see the deal as too risky.

- Collateral Desktop Analysis (CDA): Many lenders use a CDA as a secondary check on the appraisal. A CDA is a third-party review of the appraisal report, conducted by another valuation expert. They analyze the appraiser's methodology, the selected comps, and the final value conclusion to ensure it is well-supported and accurate. This adds a layer of risk management for the lender.

Based on the lower of the appraiser's ARV or the CDA's conclusion, the lender will "size" the final loan. They apply their maximum leverage for your experience tier (e.g., 70-75% of ARV) to determine the maximum loan amount. This is then cross-referenced with the Loan-to-Cost (LTC) limit (e.g., 90% of purchase price + rehab). The final loan amount will not exceed the lower of these two calculations.

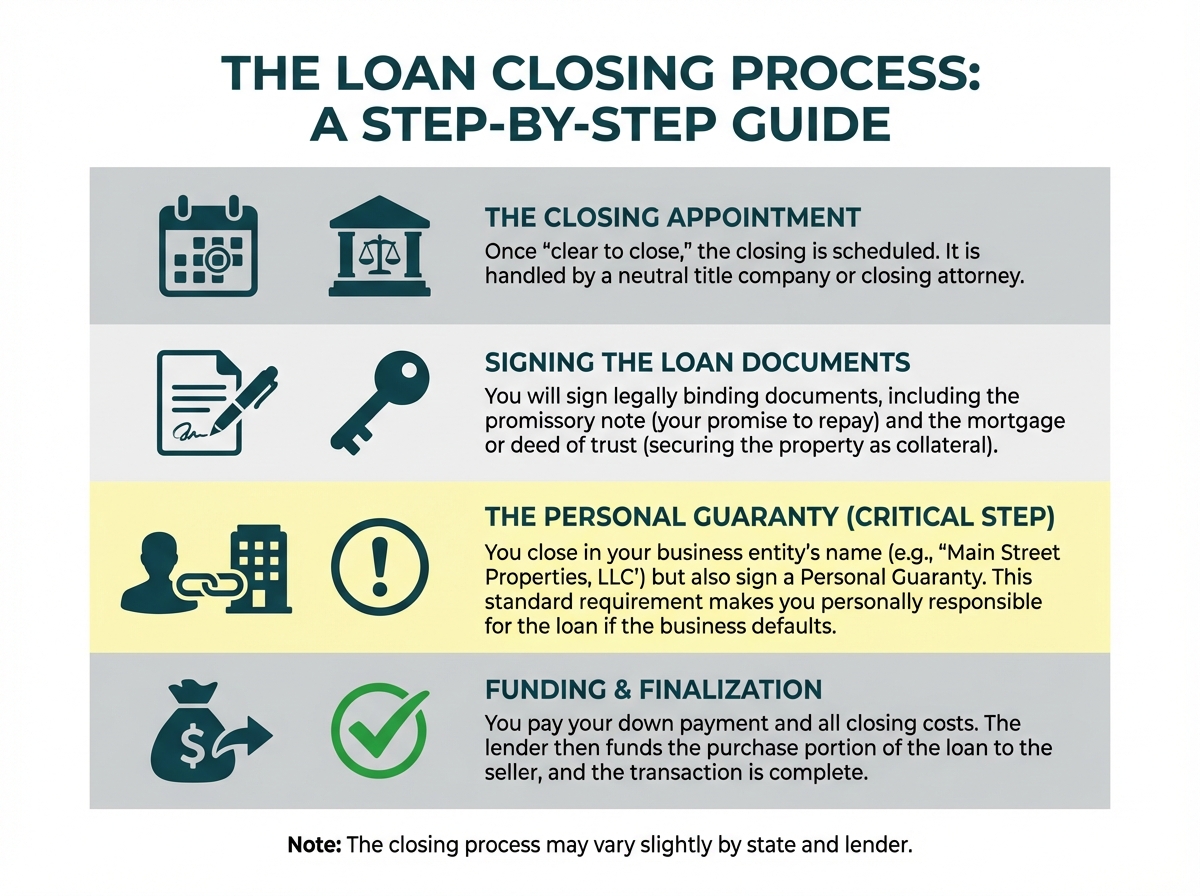

Step 4: Closing

Once underwriting is complete and you've received a "clear to close," you move to the final steps.

- Closing: The closing is handled by a title company or closing attorney. You will sign the loan documents, including the promissory note and mortgage/deed of trust. Critically, you will close in the name of your business entity (e.g., "Main Street Properties, LLC"), but you will also sign a Personal Guaranty. This is a standard requirement in hard money lending, making you personally responsible for repaying the loan if the business entity defaults. At closing, you will pay your down payment and closing costs, and the lender will fund the loan's purchase portion to the seller.

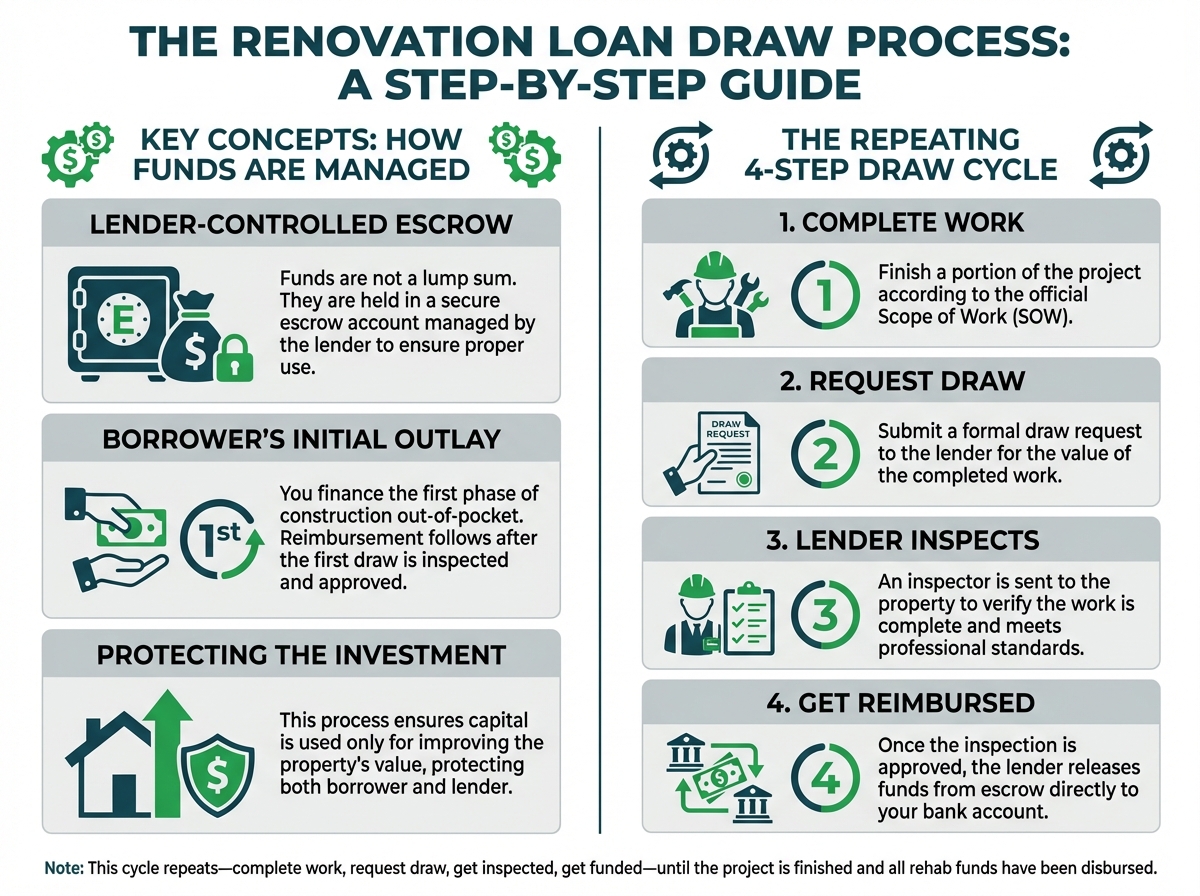

Step 5: Construction Draws

- Construction Draws: The funds allocated for your renovation are not given to you in a lump sum at closing. Instead, they are held in a lender-controlled escrow account. You will finance the first phase of construction out of pocket. Once a portion of the work outlined in your SOW is complete, you submit a draw request to the lender.

- The Draw Process: The lender sends an inspector to the property to verify that the work you've claimed is complete and done to a professional standard. Once the inspection report is approved, the lender releases the funds for that portion of the work directly to your bank account, reimbursing you for the expenses. This process repeats—complete work, request draw, get inspected, get funded—until the project is finished and all rehab funds have been disbursed. This ensures that the lender's capital is only used for its intended purpose of improving the property's value.

Navigating Common Pitfalls: The SOW Valuation Trap

The Scope of Work (SOW) is more than just a to-do list; it's a financial document that directly impacts your loan. Lenders have strict rules about what can be included in the rehab budget they finance, and misunderstanding these rules can lead to a "valuation trap" where significant portions of your budget are deemed ineligible for financing. This results in the lender withholding funds, forcing you to cover unexpected costs out of pocket.

Lender Rules for Soft Costs, Demolition, and Contingencies

Hard money lenders finance "hard costs"—tangible improvements that directly increase the property's value, like new kitchens, bathrooms, flooring, and roofing. They are far more restrictive about "soft costs" and other non-construction items.

- Soft Costs: These are expenses not directly related to physical construction. Lenders typically cap or entirely disallow financing for items like architectural plans, engineering fees, permit fees, and utility connection costs. A common cap is 5-10% of the total rehab budget. If your soft costs exceed this, you'll pay the difference.

- Demolition: While necessary, demolition does not add value; it prepares the property for value-add work. Lenders often cap demolition costs, for example, at no more than 10% of the total budget. Extensive demolition may be seen as a sign of a riskier, more complex project.

- Contingencies: A contingency line item (e.g., "10% for unforeseen issues") is standard practice in construction budgeting. However, lenders will almost never finance it. They expect you to have your own cash reserves to handle unexpected problems. Their loan is based on a defined, itemized plan, not a potential "what if."

How Improper SOW Structure Leads to Withheld Funds

When an appraiser or underwriter reviews your SOW, they will re-categorize or disallow any line items that violate the lender's guidelines.

Example: Imagine your total submitted SOW is $100,000.

- $10,000 for architectural plans and permits (Soft Costs)

- $15,000 for interior demolition (Demolition)

- $10,000 for a contingency fund (Contingency)

- $65,000 for kitchens, baths, flooring, etc. (Hard Costs)

The lender's rules might be: max 5% for soft costs and 10% for demolition, and 0% for contingency. The underwriter would adjust your "financeable" rehab budget as follows:

- Soft Costs: Capped at 5% of the new total, not the original $10k.

- Demolition: Capped at 10%.

- Contingency: $10,000 is disallowed entirely.

The result is that your financeable rehab budget is reduced to only the $65,000 in hard costs plus a small allowance for the other items. The lender might only approve a rehab loan of $75,000, leaving you with a $25,000 gap you must fund yourself.

Best Practices for Creating a Lender-Approved SOW

To avoid the valuation trap, structure your SOW with the lender's perspective in mind.

- Separate Budgets: Create two budgets. One is your internal, master budget with all costs, including contingencies. The second is the SOW you submit to the lender, focusing exclusively on financeable hard costs.

- Itemize Everything: Avoid vague line items like "Kitchen Remodel - $20,000." Instead, break it down: "Kitchen Cabinets - $7,000," "Granite Countertops - $4,000," "Appliance Package - $5,000," "Labor for Kitchen - $4,000." This detail gives the appraiser confidence in your plan and costs.

- Get a SOW Review: Before submitting your loan, have an expert or your loan officer review your SOW. They can spot red flags and help you restructure it to meet lender guidelines, ensuring you maximize your leverage and avoid surprises in underwriting.

Navigating Common Pitfalls: The Experience Step-Up Penalty

For investors looking to scale their operations, the "Experience Step-Up Penalty" can be a frustrating roadblock. Hard money lenders are inherently risk-averse when it comes to project size. They want to see a gradual, proven progression in the complexity and budget of your projects. Attempting to jump from a small, simple renovation to a massive, gut-rehab project can trigger underwriting exceptions that reduce your leverage or even lead to a loan denial.

The 2x Rule for Scaling Your Renovation Budget

While not a formal, written rule at every institution, a common guideline in underwriting is the "2x Rule." This informal principle suggests that a lender is most comfortable financing a new project where the rehab budget is no more than double the budget of your largest completed project.

- Example: If your most expensive completed flip had a rehab budget of $50,000, lenders will be very comfortable with a new project budgeted at $75,000 or even $100,000. However, if you suddenly apply for a loan with a $250,000 rehab budget, you have far exceeded the 2x guideline.

This isn't just about the dollar amount; it's about the implied complexity. A larger budget often means structural changes, significant additions, or high-end finishes—all of which require a more sophisticated level of project management. Lenders need to see you've successfully managed projects of increasing difficulty before they will fund a major leap.

Triggering Exception Reviews and Leverage Reductions

When you submit a loan application that dramatically exceeds your proven experience level, it gets flagged for an "exception review." This means a senior underwriter or credit committee must manually review the file. The potential outcomes are often unfavorable:

- Leverage Reduction: The most common outcome. The lender might say, "We can do this loan, but not at 90% LTC. We will reduce the leverage to 80% LTC." This forces you to bring significantly more cash to the table, potentially killing the deal's profitability.

- Increased Reserves: They may require you to hold a larger liquidity reserve, sometimes equal to 6-9 months of interest payments, to provide an extra cushion against potential delays or cost overruns.

- Outright Denial: In extreme cases, if the leap in project size is too great and you cannot provide compelling mitigating factors, the lender may simply decline the loan.

Proving Experience to Qualify for Larger, More Complex Projects

If you are planning a significant step up in project size, you must be proactive in proving your capability. Don't just submit the application and hope for the best. Build a case for yourself.

- Document Your Entire Track Record: Create a portfolio of all past projects, not just the most recent ones. Include before-and-after photos, final budgets vs. actual costs, and settlement statements showing the profitable sale.

- Highlight Relevant Professional Experience: If you have a background in construction management, architecture, or a related field, emphasize it. Provide a resume or a detailed summary of your professional history to show you have the skills to manage a larger project, even if it's your first time as the lead investor.

- Partner with Experience: If you are making a significant leap, consider bringing in an experienced partner or a highly credentialed General Contractor. Providing the lender with the resume and track record of your GC can give them the confidence that the project is in capable hands.

- Have a "Why": Be prepared to explain to the loan officer and underwriter why this project makes sense as your next step. A well-reasoned business plan that outlines the market opportunity and your specific strategy can be very persuasive.

By strategically building your track record and proactively documenting your capabilities, you can overcome the step-up penalty and successfully scale your real estate investment business.

Navigating Common Pitfalls: The FICO and Interest Reserve Shock

While hard money is asset-based, a borrower's credit score is not irrelevant. It's a key indicator of financial responsibility, and a low FICO score can trigger unexpected and costly requirements, primarily in the form of increased interest reserves. This can lead to a "shock" at the closing table when you discover you need to bring thousands of dollars more in cash than you originally planned.

Minimum Credit Score Requirements vs. Practical Implications

Most hard money lenders advertise a minimum FICO score, often around 620 or 640. However, simply meeting the minimum does not guarantee the best terms. Lenders use a tiered approach to credit risk, and there is often a significant difference in requirements for borrowers above and below a certain threshold, typically 660 FICO.

- Above 660 FICO: Borrowers in this range are generally considered lower risk. They often qualify for the lender's standard interest reserve requirement, which might be 3-6 months of interest payments held in reserve at closing.

- Below 660 FICO: When a borrower's score dips below this line, underwriters see elevated risk. They worry about the borrower's ability to handle financial stress if the project faces delays. To mitigate this risk, they impose stricter requirements.

How FICO Scores Below 660 Trigger Higher Reserve Requirements

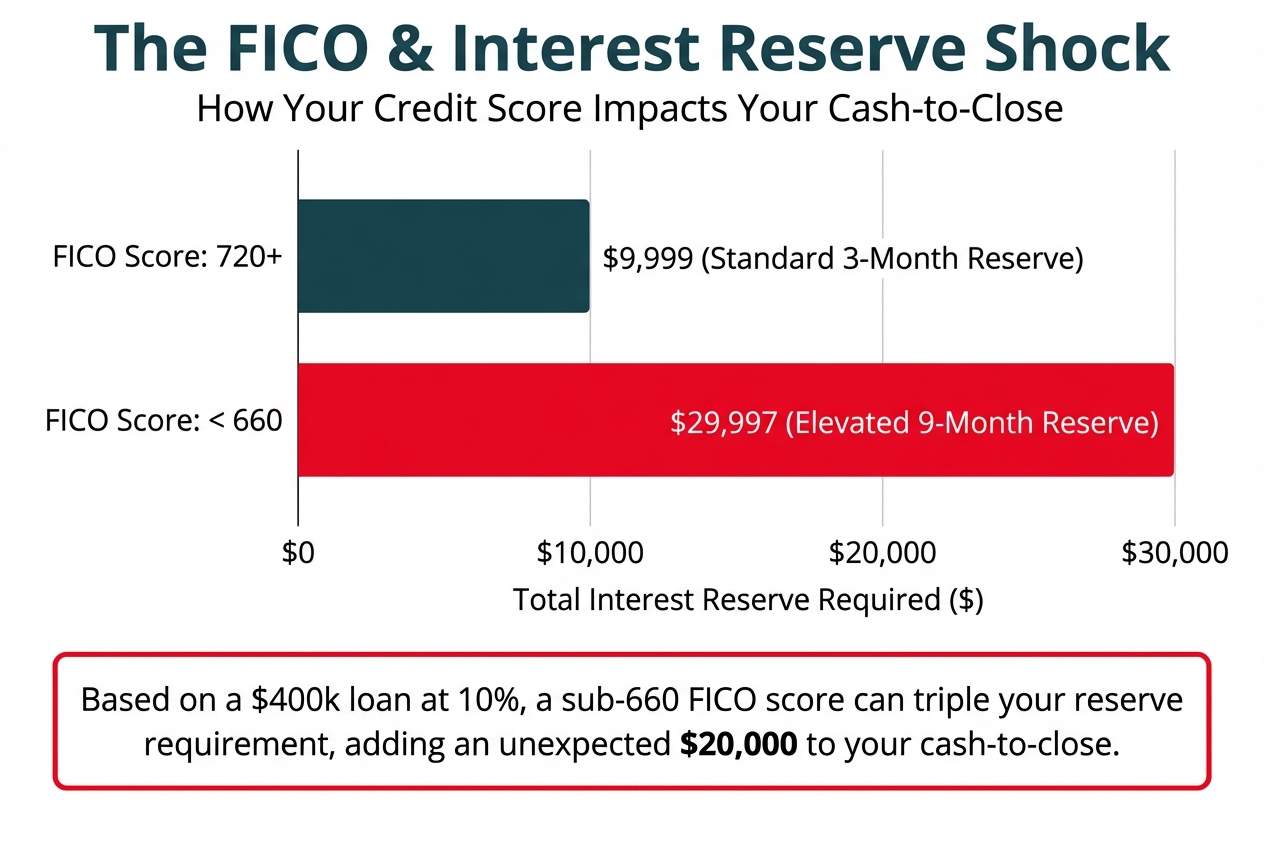

The most common penalty for a sub-660 FICO score is a substantial increase in the interest reserve requirement. The lender might double the standard requirement, demanding 9 or even 12 months of interest payments be held from the loan proceeds at closing.

This reserve is not an extra fee; it's a portion of your own loan funds that are set aside in an escrow account to cover the monthly interest payments. However, because it's withheld from the loan proceeds available to you, it directly increases your cash-to-close.

Calculating the Unexpected Cash-to-Close Impact

Let's walk through an example to see the real-world impact.

Scenario:

- Loan Amount: $400,000

- Interest Rate: 10% per annum

- Monthly Interest Payment: ($400,000 * 0.10) / 12 = $3,333

Case 1: Borrower with 720 FICO

- Standard Reserve Requirement: 3 months of interest payments

- Total Reserve: 3 * $3,333 = $9,999

- This amount is withheld from the loan at closing.

Case 2: Borrower with 650 FICO

- Elevated Reserve Requirement: 9 months of interest payments

- Total Reserve: 9 * $3,333 = $29,997

- This amount is withheld from the loan at closing.

The borrower with the lower FICO score needs to bring an additional $20,000 in cash to the closing table to cover the same down payment and closing costs. This is the "interest reserve shock," and it can easily jeopardize a deal if the investor hasn't planned for it.

Planning for Interest Reserves Based on Your Credit Profile

- Know Your Score: Before applying for a loan, pull your credit report from a source like Experian or Credit Karma. Understand where you stand and what an underwriter will see.

- Ask About Credit Tiers: When speaking with a loan officer, be direct. Ask, "What are your FICO tiers for interest reserves? What is the reserve requirement for a score like mine?" Don't rely on the advertised minimum.

- Model the Worst Case: When using a hard money loan calculator to estimate your cash-to-close, run a scenario with the highest potential interest reserve. It's better to be over-prepared with liquidity than to be caught short.

- Improve Your Score: If you are on the cusp of a credit threshold (e.g., a 655 FICO), it may be worth delaying your project for a month or two to implement credit-boosting strategies, such as paying down credit card balances or correcting errors on your report. The savings on reserve requirements could be substantial.

Navigating Common Pitfalls: Wholesale and Assignment Deals

Wholesaling is a popular strategy for finding off-market properties, but it adds a layer of complexity to hard money financing. Lenders are particularly cautious about deals involving large assignment fees, as they can inflate the purchase price and create valuation issues. Understanding how lenders view these transactions is key to structuring a wholesale deal that can be successfully financed.

Lender Scrutiny of Assignment Fees and Wholesaler Profit

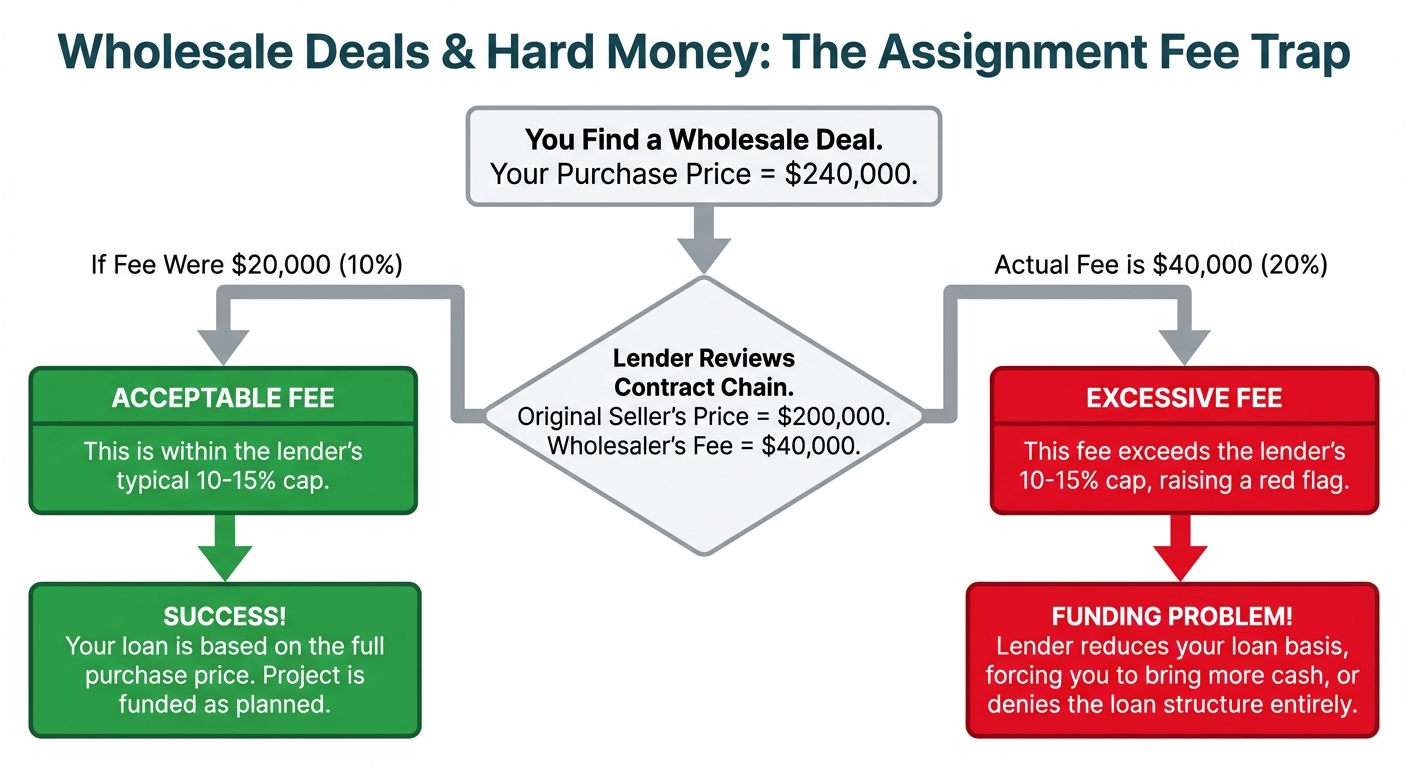

When you bring a wholesale deal to a lender, you submit the original purchase contract between the seller and the wholesaler, along with the assignment contract that transfers the rights to you, the end buyer. The lender's underwriter will immediately compare the original purchase price to your final purchase price. The difference is the wholesaler's assignment fee.

Lenders become concerned when this fee is excessively large. From their perspective, a huge assignment fee means you are paying significantly more than what the property was worth to the original seller just moments ago. This raises a red flag: is the true market value closer to the original contract price, or your higher price? This doubt can undermine the lender's confidence in the deal's valuation.

Maximum Allowable Assignment Fee

To manage this risk, most hard money lenders impose a cap on the allowable assignment fee. This cap is typically expressed as a percentage of the original purchase price. A common industry standard is a cap of 10% to 15%.

- Example:

- Original contract price (Seller to Wholesaler): $200,000

- Lender's maximum assignment fee cap: 10%

- Maximum allowable fee: $200,000 * 0.10 = $20,000

- Maximum purchase price the lender will recognize for your loan: $220,000

If the wholesaler in this scenario tries to charge you a $40,000 assignment fee (bringing your purchase price to $240,000), you have a serious financing problem.

How Excessive Fees Can Force a Loan Based on As-Is Value

When an assignment fee breaches the lender's cap, one of two things usually happens:

- Reduced Loan Basis: The lender will simply refuse to recognize the portion of the fee that exceeds their limit. In the example above, they would base your loan on a purchase price of $220,000, not your actual price of $240,000. This means you have to come up with the $20,000 difference in cash at closing.

- Reversion to As-Is Value: In cases of extremely high fees (e.g., 25% or more), the lender may lose all confidence in the After Repair Value model. They may decide the risk is too high and change the entire loan structure. Instead of lending based on future ARV, they will only lend a conservative percentage (e.g., 65-70%) of the property's current "As-Is" value. This drastically reduces the loan amount and almost always kills the deal for an investor who needs rehab funds.

Structuring Wholesale Deals for Successful Hard Money Financing

To avoid these pitfalls, savvy investors and wholesalers structure their deals with financing in mind from the very beginning.

- Negotiate with the Cap in Mind: As the buyer, know your lender's assignment fee cap before you negotiate with the wholesaler. Make it clear that any fee above the limit will need to be paid by you in cash, which may not be feasible.

- Use a Double Closing: For deals with very large wholesale spreads, a double closing (or simultaneous closing) can be a solution. In this scenario, the wholesaler first buys the property from the original seller (often using transactional funding). Moments later, they sell it to you in a separate transaction. Because this is now a traditional sale (A -> B, then B -> C), the lender only sees your purchase contract from the wholesaler (the B->C transaction). This eliminates the assignment fee issue, though it does involve slightly higher closing costs.

- Be Transparent with Your Lender: Don't try to hide a large assignment fee. Disclose the full contract chain upfront. A good loan officer can often help you find a creative solution, but only if they have all the information. Trying to conceal part of the transaction is a sure way to get your loan denied.

By understanding the lender's perspective on wholesaler profit, you can structure your deals to align with their risk tolerance, ensuring a smooth path to funding.

Hard Money Loans vs. DSCR Loans

While both are popular financing tools for real estate investors, hard money loans and DSCR loans serve fundamentally different purposes and are underwritten with completely different criteria. Choosing the right loan product is essential for aligning your financing with your investment strategy.

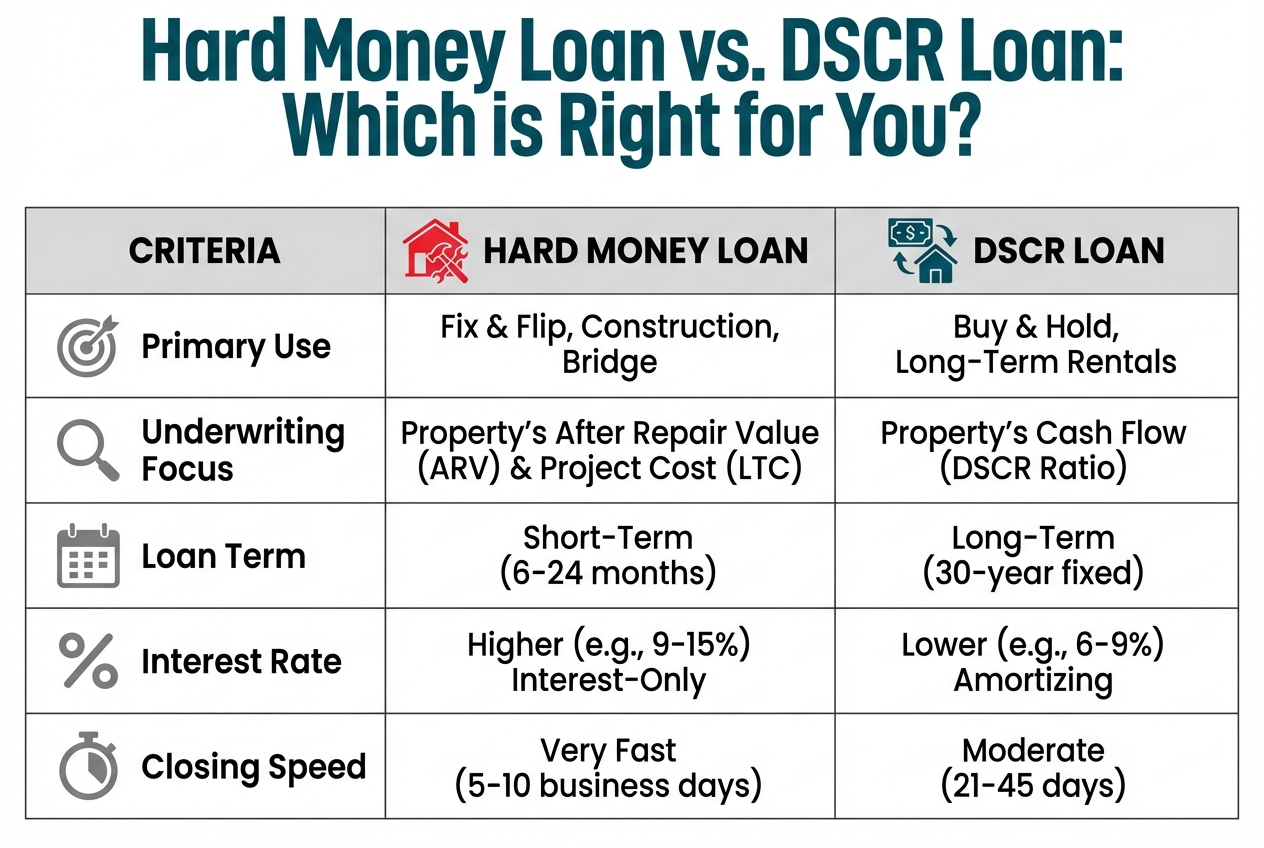

Core Difference in Underwriting Focus

- Hard Money Loan: The underwriting focus is entirely on the value of the asset, specifically its future value (ARV). The lender asks, "If this project is completed as planned, what will the property be worth, and is there enough value to cover our loan and provide the investor a profit?" The borrower's personal income is not a primary consideration.

- DSCR Loan: The underwriting focus is on the property's ability to generate income. The core metric is the Debt-Service Coverage Ratio (DSCR), which is calculated by dividing the property's Net Operating Income (NOI) by its total debt service (mortgage payment). Lenders typically require a DSCR of 1.20x or higher, meaning the property generates at least 20% more income than is needed to cover the mortgage. This loan is all about the asset's cash flow, not its one-time sale value.

Intended Use Case

- Hard Money Loan: This is a transitional loan. It's designed for short-term projects where the primary goal is to add value and then exit the project quickly. The classic use case is a fix-and-flip, where an investor buys, renovates, and sells a property within 6-12 months. It's also used for new construction or as a bridge loan to acquire a property quickly before refinancing into a long-term loan.

- DSCR Loan: This is a permanent or long-term financing solution. It's designed for investors who intend to buy and hold a property as a rental. The goal is not a quick sale but long-term cash flow and appreciation. It's the go-to product for building a portfolio of rental properties.

Typical Loan Terms, Speed, and Rates

| Feature | Hard Money Loan | DSCR Loan |

|---|---|---|

| Loan Term | 6-24 months | 30 years |

| Interest Rate | Higher (e.g., 9-15%) | Lower (e.g., 6-9%) |

| Payment Type | Interest-Only | Principal & Interest (Amortizing) |

| Closing Speed | Very Fast (5-10 days) | Slower (21-45 days) |

| Prepayment Penalty | Typically none or very short | Common (e.g., 3-5 years) |

Choosing the Right Loan Product

The choice between a hard money loan and a DSCR loan comes down to your investment strategy for that specific property.

- Choose a Hard Money Loan if:

- You are buying a property that needs significant renovation.

- Your primary goal is to sell the property for a profit in the near future (a flip).

- You need to close extremely quickly to beat competing offers.

- The property is currently vacant and cannot qualify for a loan based on income.

- Choose a DSCR Loan if:

- You are buying a rent-ready property or one that needs only minor cosmetic updates.

- Your primary goal is to hold the property as a long-term rental for cash flow.

- You are refinancing a completed fix-and-flip project to hold it as a rental (the "BRRRR" method).

- You have more time to close (3-6 weeks).

Many sophisticated investors use both products in sequence. They use a hard money loan to acquire and renovate a distressed property. Once the renovation is complete and a tenant is in place, they refinance the high-interest hard money loan into a lower-rate, 30-year fixed DSCR loan to hold the property for the long term.

The OfferMarket Advantage

Navigating the complexities of hard money lending requires a partner that prioritizes transparency, speed, and expertise. OfferMarket is built from the ground up to provide a modern, streamlined lending experience that empowers real estate investors to act decisively and maximize their returns. Our platform and process are designed to eliminate the common frustrations and pitfalls of traditional lending.

Instant Quotes with Sample Loan Files for Full Transparency

Uncertainty kills deals. That's why we provide more than just a rate—we provide clarity. When you get an instant quote from OfferMarket, you receive a detailed breakdown of your potential loan terms. More importantly, you get a sample Loan File. This is a comprehensive document that shows you exactly how we structure our loans, what our draw process looks like, and what documents will be required. You'll see the numbers and the process upfront, allowing you to make informed decisions without any hidden surprises down the road.

Streamlined Digital Process for Fast and Efficient Funding

In real estate investing, speed is a competitive advantage. Our proprietary technology platform digitizes the entire loan process, from application to closing. You can submit your project details, upload documents to a secure portal, and track your loan's progress in real-time. This efficiency eliminates unnecessary paperwork, endless email chains, and communication delays. The result is a faster, smoother path to the closing table, with the ability to fund loans in as few as 5-7 business days.

Competitive Terms with High Leverage

Our goal is to help you do more deals. We offer some of the most competitive terms in the industry, with leverage up to 90% of the purchase price and 100% of the renovation costs, not to exceed 75% of the After Repair Value. By providing high-leverage options, we enable you to preserve your capital, take on more projects simultaneously, and scale your investment portfolio more effectively. Our experience tiering system ensures that as your track record grows, your loan terms get even better.

Expertise in Navigating Complex Deals and Investor Needs

We are more than just a lender; we are a team of experienced real estate and finance professionals. We understand the nuances of complex transactions, from wholesale deals with large assignment fees to large-scale construction projects. Our loan specialists are trained to be consultative partners. We can review your Scope of Work for potential issues, help you structure your deal for financing success, and provide the expert guidance you need to navigate any challenges that arise. We've seen thousands of deals and can apply that knowledge to help make yours a success.

Your Strategic Next Steps

You now have a comprehensive understanding of what a hard money loan is, how the process works, and how to avoid common pitfalls. The next step is to apply this knowledge to your specific project. Taking decisive action with the right information is what separates successful investors from the rest.

- Get an Instant Quote: The most valuable next step is to see real numbers for your deal. Take five minutes to get an instant quote and receive your personalized terms and a sample Loan File. This will transform abstract concepts into a concrete financial model for your project.

- Use a Hard Money Loan Calculator: Model different scenarios. Use our hard money loan calculator to adjust the purchase price, rehab budget, and ARV. See how these changes impact your interest payments, down payment, and overall profitability.

- Schedule a Call to Review Your SOW and Experience: Don't go into underwriting blind. Schedule a call with an OfferMarket loan specialist. We can provide a complimentary review of your Scope of Work to ensure it's structured for maximum financing and help you accurately determine your Experience Tier to set clear expectations.

- Calculate Your Step-Up Budget Limit: If you're planning to take on a larger project than ever before, talk to us first. A specialist can help you understand the "2x rule" and how underwriters will view your experience, allowing you to target projects that you can confidently get financed.

OfferMarket Loans

Check your rate

60 seconds · no credit pull