*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The Illinois Land Trust Dilemma for Real Estate Investors

You've found the perfect investment property. The numbers work. Your exit strategy is solid. You submit your loan application with confidence—only to receive a denial letter citing an "ineligible entity structure." The culprit? Your property is held in an Illinois Land Trust.

This scenario plays out more frequently than most real estate investors realize. While land trusts have been a cornerstone of Illinois real estate planning for decades, offering privacy and estate planning benefits, they've become a significant roadblock in today's lending environment. The very features that make these trusts attractive to investors—anonymity, the classification of beneficial interest as personal property, and the separation of legal title from control—are precisely what make lenders uncomfortable in 2026.

At OfferMarket, we understand the frustration of having a viable investment opportunity slip away due to entity structure issues. That's why we've created this comprehensive guide: to demystify the Illinois Land Trust, explain exactly why it creates financing challenges, and most importantly, provide you with a clear, actionable path forward.

Our Policy and Commitment to Transparency

OfferMarket's policy is straightforward: properties held in Illinois Land Trusts are ineligible for financing through our loan programs. This isn't an arbitrary decision—it's rooted in federal compliance requirements, legal complexities unique to these trusts, and the operational realities of modern mortgage lending. However, we believe that a policy without education leaves investors in the dark. Our commitment is to explain not just the "what" but the "why" behind our lending guidelines, empowering you to make informed decisions about your investment strategy.

Unlike lenders who simply deny applications without explanation, we're dedicated to helping you understand the specific legal and regulatory issues that make land trusts incompatible with standard mortgage financing. More importantly, we'll show you exactly how to restructure your property ownership to qualify for financing while still protecting your investment interests.

Whether you're currently facing a loan denial, considering a land trust for a new acquisition, or simply trying to understand your options, this guide will equip you with the knowledge to navigate the intersection of Illinois land trust law and modern mortgage lending. By the end, you'll understand not only why your current structure may be preventing you from accessing capital, but exactly what steps to take to position your investment for financing success.

Let's begin by examining what an Illinois Land Trust actually is and how its unique legal structure sets it apart from every other form of property ownership.

What is an Illinois Land Trust?

An Illinois Land Trust is a distinctive legal arrangement that has its roots in 19th-century common law, first recognized in the Chicagoland area as a tool to provide individuals with greater control and privacy over their real estate holdings. While less common today than in decades past, it remains a legally valid ownership structure governed by both Illinois common law and several state statutes.

At its core, an Illinois Land Trust is defined as an arrangement under which a trustee holds legal and equitable title to real property, while the beneficiary retains all beneficial interest and control over that property. This creates a fundamental separation between who appears on public records as the owner (the trustee) and who actually controls and benefits from the property (the beneficiary).

The Three Key Parties

Every Illinois Land Trust involves three distinct roles, each with specific rights and responsibilities:

The Trustee is the entity that holds both legal and equitative title to the real estate. This is typically a bank, trust company, or other qualified financial institution—such as Chicago Title or a similar corporate trustee. The trustee's name appears on all public records, including the deed recorded with the county. However, the trustee's role is largely passive; they hold title but do not manage, control, or make decisions about the property. The trustee can only act when they receive formal written instructions from the beneficiary.

The Beneficiary is the individual or entity that holds all beneficial interest in the property. While their name does not appear on public records, the beneficiary retains complete control over the property, including the right to possess it, manage it, collect rent, make improvements, and ultimately direct its sale. The beneficiary receives all "proceeds and avails" from the property—meaning all income generated and all proceeds from any sale. This is the party that real estate investors typically think of as the "true owner," even though they do not hold legal title.

The Holder of the Power of Direction is the party authorized to issue binding instructions to the trustee. In most cases, this is the same person or entity as the beneficiary, but the trust agreement can designate a separate holder of this power. This individual has the exclusive authority to direct the trustee to execute deeds, sign mortgage documents, or take any other action affecting the legal title. The power of direction is exercised through formal written documents called "Letters of Direction."

The Core Concept: Separation of Title and Interest

The defining characteristic of an Illinois Land Trust is the legal separation it creates between title and beneficial interest. Under Illinois law, the trustee holds the legal and equitable title to the real estate, but the beneficiary holds an interest that is legally classified as personal property, not real property.

This classification is not merely a technicality—it has profound legal consequences. Because the beneficiary's interest is considered "personalty" (personal property), it can be transferred, assigned, or pledged as collateral with the same ease as corporate stock or other intangible assets. Judgments against a beneficiary do not automatically attach as liens against the real estate itself, because the beneficiary does not legally "own" the real property—they own a personal property interest in the trust.

This separation means that while the trustee's name appears on the deed and all public records, the trustee has no authority to act independently. The beneficiary, whose name is not on public records, retains complete control over all decisions affecting the property through their power of direction.

Establishing the Structure: Trust Agreement and Deed in Trust

Creating an Illinois Land Trust requires two essential legal documents:

The Trust Agreement is the foundational contract between the beneficiary and the trustee. This private document (which is not recorded publicly) establishes the terms of the trust, including:

- The identity of the beneficiary or beneficiaries

- The designation of who holds the power of direction

- The duties and limitations of the trustee

- The rights of the beneficiary to possess, manage, and control the property

- The beneficiary's right to receive all income and proceeds

- Provisions for successor beneficiaries in the event of death

- The duration of the trust (often 20 years, with renewal options)

The Deed in Trust is the legal instrument that transfers title to the property from the current owner to the trustee. This document is recorded with the County Recorder of Deeds in the Illinois county where the property is located, making the transfer a matter of public record. The deed identifies the trustee as the grantee (the party receiving title) and typically includes a trust number or designation, but it does not disclose the identity of the beneficiary. This recorded deed is what creates the privacy benefit—the public record shows only that the property is held by "XYZ Trust Company, as Trustee under Trust Agreement dated [date] and known as Trust No. [number]."

Once these documents are executed and the deed is recorded, the legal structure is complete. The trustee holds title, the beneficiary controls the property, and the separation between public record and actual ownership is established.

The Personal Property Classification: A Legal Quirk with Major Consequences

The most legally significant aspect of an Illinois Land Trust is that the beneficiary's interest is classified as personal property rather than real property. This classification is a product of Illinois common law and distinguishes the Illinois Land Trust from many other forms of property ownership.

In practical terms, this means:

- The beneficiary does not own "real estate"—they own a personal property interest in a trust that holds real estate

- Transfers of beneficial interest do not require a deed; they can be accomplished through simple assignment documents

- Judgments and liens against the beneficiary do not automatically attach to the real estate

- The interest can be pledged as collateral, but doing so requires a UCC filing rather than a mortgage

This personal property classification is the source of both the trust's primary benefits (privacy, ease of transfer, probate avoidance) and its primary drawbacks in the modern lending environment. As we will explore in later sections, this legal quirk is the fundamental reason why most mortgage lenders in 2026 classify Illinois Land Trusts as ineligible borrowers.

Understanding this foundational structure—the three parties, the separation of title and interest, and the personal property classification—is essential for any real estate investor considering or currently using an Illinois Land Trust. This legal framework creates unique advantages, but it also creates significant obstacles when seeking financing, as the structure conflicts with standard mortgage lending practices and federal transparency requirements.

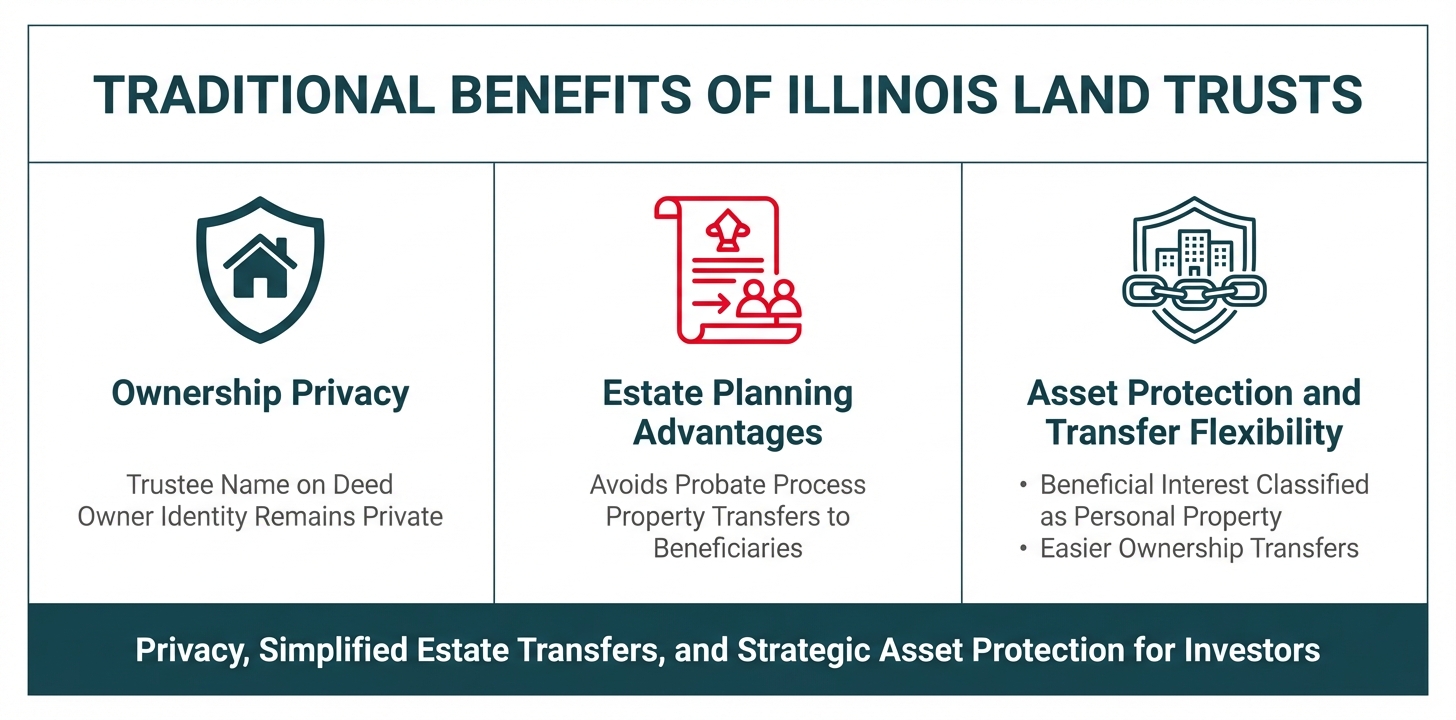

The Traditional Benefits: Why Investors Use Illinois Land Trusts

Despite the modern lending challenges they present, Illinois Land Trusts have remained a popular estate planning and asset protection tool for decades. Understanding why investors have historically favored this structure helps explain its continued use, even as financing options have become more restricted. The land trust offers four primary advantages that have made it an attractive option for real estate owners in Illinois.

Benefit 1: Anonymity and Privacy of Ownership

The most compelling reason investors choose an Illinois Land Trust is the privacy it provides. When you hold property in a land trust, the trustee's name—not yours—appears on the deed recorded with the county. This means your identity as the true owner remains off public records, shielding you from unwanted attention.

For real estate investors, this anonymity serves multiple practical purposes. It prevents solicitors, marketers, and potential litigants from easily identifying your property holdings. It also provides a layer of separation between you and the property, which can be valuable when negotiating deals or managing tenant relationships. According to estate planning experts, the trust agreement doesn't get filed anywhere and isn't part of the public record, meaning the details of ownership and beneficial interest remain completely private unless legally compelled to be disclosed.

This privacy feature has made land trusts particularly popular among investors who own multiple properties and prefer to keep their portfolio details confidential. However, it's worth noting that this same privacy feature is precisely what creates friction with modern lenders who are required to verify the identity of borrowers under KYC and AML regulations.

Benefit 2: Probate Avoidance and Simplified Estate Planning

One of the most significant practical advantages of an Illinois Land Trust is its ability to bypass the probate process entirely. When real estate is held in your individual name, it must typically pass through probate court upon your death—a process that can be time-consuming, expensive, and public.

A land trust elegantly sidesteps this issue. Because the beneficiary's interest is classified as personal property rather than real property, it can transfer automatically to successor beneficiaries named in the trust agreement. The trustee continues to hold legal title, so there's no "death" of the title that would trigger probate proceedings.

Land trusts allow property to pass directly to beneficiaries, eliminating the time and expense of probate administration. This automatic transfer mechanism means your heirs can take control of the property immediately upon your death, without waiting months or years for court proceedings to conclude. The transfer also remains private, avoiding the public disclosure that comes with probate.

For investors with multiple properties, this benefit becomes even more pronounced. Rather than each property requiring separate probate proceedings, all properties held in land trusts can transfer seamlessly according to the terms you've established in the trust agreements.

Benefit 3: Ease of Transferring Beneficial Interest

Traditional real estate transfers involve a complex process of deeds, title searches, recording fees, and potential transfer taxes. An Illinois Land Trust simplifies this considerably because the beneficial interest is personal property, not real property.

Transferring your beneficial interest in a land trust can be as straightforward as assigning personal property—similar to transferring shares of stock. This doesn't require recording a new deed or conducting a full title search. You simply execute an assignment of beneficial interest, and the transfer is complete. The trustee continues to hold legal title, so from a public records perspective, nothing has changed.

This ease of transfer makes land trusts particularly useful for estate planning purposes, allowing you to gift fractional interests to family members or adjust ownership percentages without the administrative burden of traditional real estate conveyancing. It also facilitates business transactions where you might want to bring in partners or restructure ownership without alerting the public or triggering unnecessary scrutiny.

However, it's important to note that while this flexibility exists under Illinois law, modern lenders view this very feature with suspicion. The ability to transfer beneficial interest so easily, without public recording, creates uncertainty about who actually controls the property securing their loan.

Benefit 4: Protection from Certain Judgments and Liens Against the Beneficiary

Perhaps the most legally sophisticated benefit of an Illinois Land Trust is the protection it can provide against certain types of creditor claims. Because your beneficial interest is classified as personal property rather than real property, judgments against you as an individual do not automatically attach as liens against the real estate held in the trust.

In traditional property ownership, if a creditor obtains a judgment against you, that judgment typically becomes a lien on all real estate you own in that county. This can complicate sales, refinancing, or any transaction involving the property. With a land trust, this automatic lien attachment doesn't occur because the real estate itself isn't in your name—it's in the trustee's name.

This doesn't mean your beneficial interest is completely protected from creditors—they can still pursue that personal property interest through other legal means. However, it does create an additional layer of complexity for creditors and can protect the property from certain types of claims that would otherwise attach automatically.

For real estate investors, this protection can be valuable when managing the risks associated with property ownership, tenant disputes, or business liabilities. It provides a degree of separation between your personal liability and the real estate assets you control.

The Historical Appeal to Illinois Investors

These four benefits—privacy, probate avoidance, ease of transfer, and creditor protection—have made Illinois Land Trusts a staple of estate planning and asset protection strategies in the state for generations. Real estate investors, in particular, have found them to be powerful tools for managing portfolios while maintaining control and flexibility.

However, the same features that make land trusts attractive for privacy and asset protection are precisely what make them problematic in the modern lending environment. The anonymity conflicts with transparency requirements, the personal property classification creates legal complications for mortgages, and the ease of transfer raises red flags about fraud and foreclosure risks.

Understanding these traditional benefits is essential for investors who must now weigh them against the very real limitation that properties held in Illinois Land Trusts are ineligible for financing from most lenders, including OfferMarket. The question becomes: are the privacy and estate planning benefits worth the trade-off of severely limited financing options?

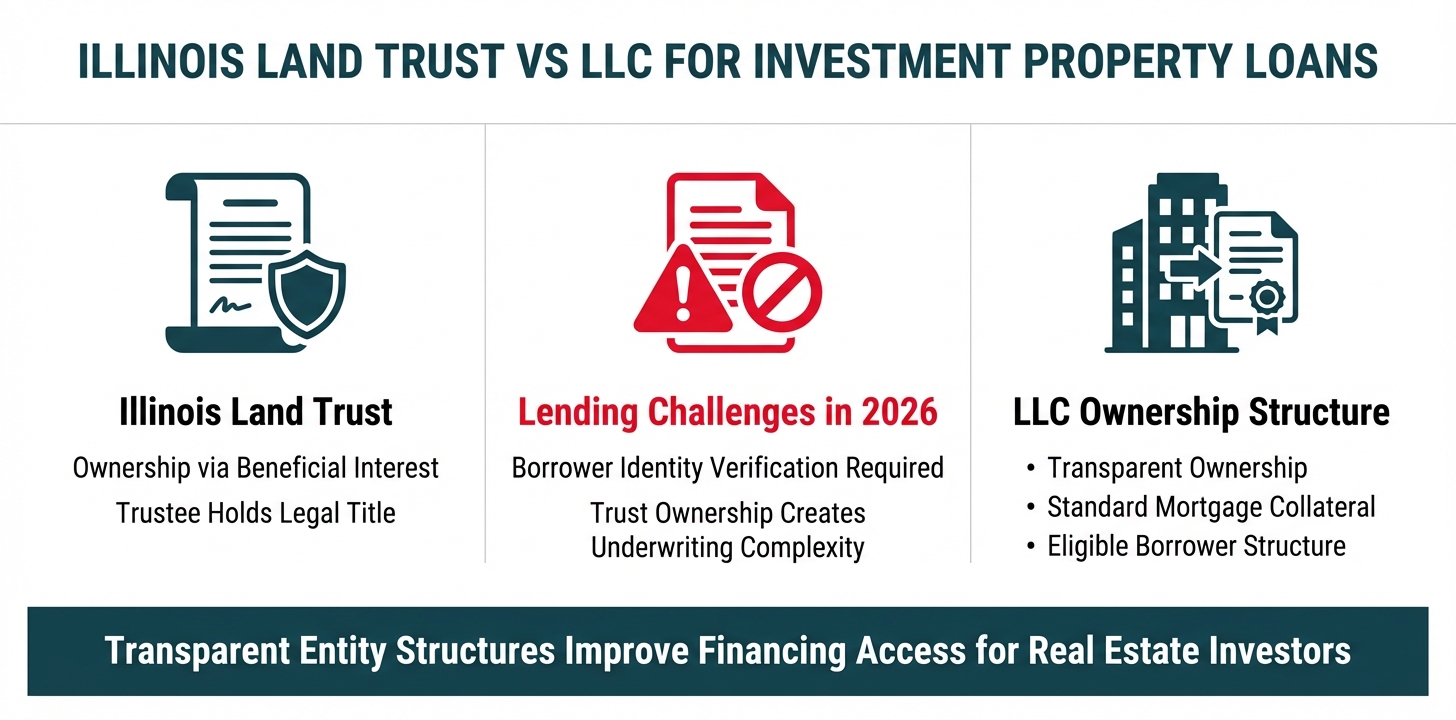

The Lender's Perspective: Why Illinois Land Trusts Are Ineligible for Financing

When real estate investors approach OfferMarket with a property held in an Illinois Land Trust, they encounter an immediate roadblock: properties held in Illinois Land Trusts are categorically ineligible for financing. This isn't an arbitrary policy decision or an outdated guideline that might change with a phone call to underwriting. It's a firm stance rooted in four interconnected risk factors that make these trusts fundamentally incompatible with modern mortgage lending practices.

Understanding why this policy exists is crucial for investors who need to pivot their ownership structure to secure financing. The reasons go far beyond simple paperwork preferences—they touch on federal compliance requirements, legal complexities that can derail foreclosure proceedings, and secondary market restrictions that determine whether a lender can profitably sell your loan after closing.

Reason 1: The Transparency Conflict with KYC and AML Regulations

The very feature that makes Illinois Land Trusts attractive to investors—anonymity—is precisely what makes them problematic for lenders operating under federal law. The USA Patriot Act and subsequent Anti-Money Laundering (AML) regulations impose strict "Know Your Customer" (KYC) requirements on all financial institutions. These laws mandate that lenders must identify and verify the identity of the ultimate beneficial owner of any entity they're lending to.

An Illinois Land Trust is specifically designed to keep the beneficiary's name off public records. The trustee's name appears on the deed, but the trustee is merely a passive title holder with no actual ownership interest. The beneficiary—the person who controls the property, receives all income, and makes all decisions—remains hidden from public view. This creates an immediate compliance problem for lenders.

Underwriters are required to document a clear chain of ownership and beneficial interest. When presented with a land trust, they face a structure that intentionally obscures this information. While the beneficiary can be disclosed through private trust documents, the verification process becomes significantly more complex than a standard transaction where the borrower's name appears directly on the title.

Federal regulators have intensified their scrutiny of lending practices that might facilitate money laundering or other financial crimes. Structures that provide anonymity—even when used for entirely legitimate privacy purposes—raise red flags in compliance departments. Underwriters know that approving loans to opaque ownership structures exposes their institution to regulatory risk, potential fines, and reputational damage if the beneficial owner later proves to be engaged in illegal activity.

For OfferMarket and other lenders, the risk-reward calculation is straightforward: the compliance burden and regulatory exposure of lending to a land trust far outweighs any potential benefit from closing the loan.

Reason 2: The "Personal Property" Quirk and UCC vs. Standard Mortgages

The second major obstacle stems from a unique feature of Illinois common law that most out-of-state lenders find baffling: the beneficiary's interest in an Illinois Land Trust is legally classified as personal property (personalty), not real property. This seemingly technical distinction has profound practical implications for how a loan must be secured.

In a standard real estate transaction, a lender secures their loan with a mortgage or deed of trust that creates a lien against the real property itself. The legal framework for these instruments is well-established, standardized across all 50 states, and deeply integrated into every lender's operational systems, legal templates, and underwriting software.

When the collateral is personal property rather than real property, everything changes. Securing a loan against the beneficiary's interest in a land trust requires a collateral assignment of beneficial interest governed by the Uniform Commercial Code (UCC) rather than traditional real estate law. This is the same legal framework used for securing loans against inventory, equipment, or accounts receivable—not real estate.

Most mortgage lenders' systems are simply not built to handle UCC-based collateral assignments for what is ostensibly a real estate loan. Their loan origination software, document preparation systems, title insurance requirements, and closing procedures are all designed around standard mortgages. Retooling these systems for a UCC filing would require custom legal work, specialized title insurance endorsements, and manual underwriting processes that fall outside the lender's normal workflow.

Even if a lender were willing to undertake this complexity, the legal risks multiply. Foreclosing on a UCC collateral assignment is a fundamentally different process than foreclosing on a mortgage. The procedures, timelines, and potential defenses available to the borrower all differ significantly. Most lenders lack in-house expertise in UCC foreclosure proceedings for real estate collateral, and the legal costs of hiring outside counsel to navigate this unfamiliar territory can quickly exceed the value of pursuing the foreclosure at all.

For OfferMarket, maintaining operational efficiency and legal clarity requires sticking to standard real estate mortgages. The "personal property" classification of land trust interests makes them incompatible with our lending infrastructure.

Reason 3: Heightened Foreclosure and Fraud Risks

The third reason Illinois Land Trusts are ineligible relates to the mechanics of how trustees are authorized to act on behalf of the trust—and the fraud risks this creates. Under Illinois law, a trustee can only execute legal documents (such as mortgage agreements, deeds, or refinancing papers) when they receive a formal written instruction called a Letter of Direction from the beneficiary.

This requirement introduces a significant vulnerability into the lending process. The lender is not directly contracting with the beneficial owner; they're contracting with a trustee who claims to be acting under the authority of a letter that the lender has no independent way to verify. The lender must trust that the Letter of Direction is authentic, that it was actually signed by the true beneficiary, and that the person claiming to be the beneficiary actually holds that legal status.

The industry has learned this lesson the hard way. There have been documented cases where fraudsters have created fake Letters of Direction, impersonated beneficiaries, and successfully obtained mortgage loans against properties they didn't actually control. By the time the fraud was discovered—often when the real property owner became aware of an unexpected foreclosure notice—the loan proceeds had long since disappeared, and the lender was left holding a mortgage that was void from the beginning due to the trustee's lack of actual authority.

Even in non-fraudulent scenarios, disputes over the validity of Letters of Direction create legal quagmires. If a beneficiary later claims they never authorized the trustee to sign a mortgage, or if there are multiple beneficiaries with conflicting instructions, the lender can find themselves in protracted litigation just to establish whether they have a valid lien at all.

These "liability traps" have made lenders extremely cautious about any transaction that requires reliance on third-party authorization documents. When a borrower holds title in their own name or through a transparent LLC structure, the lender can verify authority through standard corporate resolutions and personal guarantees. With a land trust, they're always one forged letter away from a loan that may be legally unenforceable.

Reason 4: Secondary Market Incompatibility with Fannie Mae and Freddie Mac

The final reason—and perhaps the most decisive from a business perspective—is that loans secured by Illinois Land Trusts are extremely difficult, if not impossible, to sell on the secondary market to Fannie Mae and Freddie Mac, the government-sponsored enterprises that purchase the vast majority of residential mortgages in the United States.

Fannie Mae and Freddie Mac have extensive guidelines governing what types of loans they will purchase, and these guidelines strongly prefer lending to **"natural persons"**—individual human beings—rather than trusts or other legal entities. While their guidelines do contain provisions that theoretically allow for loans to certain types of trusts, the requirements are extraordinarily specific and the documentation burden is substantial.

For a land trust loan to be eligible for sale to Fannie Mae or Freddie Mac, the lender would need to obtain and verify extensive documentation about the trust structure, confirm that the trust meets specific legal requirements, ensure that the beneficiaries are properly identified and creditworthy, and navigate a maze of special underwriting conditions that most loan officers have never encountered in their careers. Even a small error in this documentation can result in the loan being rejected for purchase, leaving the lender stuck holding the debt on their own balance sheet.

Most lenders operate on a business model where they originate loans with the intention of selling them to Fannie Mae or Freddie Mac within days or weeks of closing. This "originate-to-distribute" model allows lenders to recycle their capital quickly and minimize their exposure to long-term interest rate risk and borrower default. When a loan cannot be sold to the secondary market, it ties up the lender's capital for the entire term of the loan—potentially 15 to 30 years.

For OfferMarket, ensuring that every loan we originate meets secondary market standards is essential to our business model and our ability to offer competitive rates to investors. Loans that cannot be sold to private institutional investors require significantly higher interest rates to compensate for the additional risk and capital requirements. Rather than creating a separate, more expensive product tier for land trust properties, we've made the strategic decision to focus exclusively on ownership structures that align with secondary market preferences.

The combination of these four factors—KYC/AML compliance conflicts, the personal property classification requiring UCC collateral assignments, heightened fraud and foreclosure risks, and secondary market incompatibility—creates an insurmountable barrier for Illinois Land Trust financing. For investors who currently hold property in this structure, the path forward is clear: restructuring ownership into an eligible entity is not optional if you want to secure financing from OfferMarket or virtually any other institutional lender in 2026.

A Deeper Dive into the Risks for Lenders

When a mortgage lender evaluates a loan application for property held in an Illinois Land Trust, they aren't simply being overly cautious—they're responding to a complex web of federal compliance mandates, legal ambiguities, and operational risks that make these structures fundamentally incompatible with modern lending standards. Understanding these specific concerns provides clarity on why even well-established trusts face systematic denial in today's mortgage market.

KYC/AML Compliance: The Underwriter's Duty to Identify the Ultimate Beneficial Owner

At the heart of the land trust problem lies a direct conflict between the structure's core purpose—anonymity—and the lender's legal obligation to know exactly who they're doing business with. Under the USA PATRIOT Act and subsequent regulations, financial institutions must establish robust Customer Identification Programs (CIPs) and Customer Due Diligence (CDD) procedures that go beyond surface-level documentation.

The Customer Due Diligence Rule, which took effect in 2018, explicitly requires covered financial institutions to identify and verify the beneficial owners of legal entity customers. According to federal regulations, a beneficial owner is any individual who owns 25% or more of the equity interests in a legal entity or exercises significant control over it. Lenders must collect identifying information—including name, date of birth, address, and a government-issued identification number—for each beneficial owner and verify this information through documents, non-documentary methods, or both.

For an Illinois Land Trust, this creates an immediate compliance dilemma. The trustee appears on public records as the titleholder, while the true beneficial owner remains intentionally obscured. The trust agreement—a private document not filed with any public office—contains the actual ownership information, but obtaining and verifying this document introduces friction into what lenders need to be a streamlined, auditable process.

Underwriters are trained to view structures designed to obscure ownership as potential red flags for money laundering, terrorist financing, or other financial crimes. When a loan file contains a land trust, the underwriter must conduct additional due diligence to "pierce the veil" of the trust and identify the individuals who ultimately control and benefit from the property. This requires obtaining the trust agreement, verifying the beneficiaries' identities, confirming that no beneficial owners appear on sanctions lists (such as OFAC's Specially Designated Nationals list), and documenting all of this research in the loan file.

This level of scrutiny isn't merely a best practice—it's a regulatory requirement with serious consequences for non-compliance. Financial institutions that fail to maintain adequate AML/KYC programs face substantial civil and criminal penalties, including fines that can reach millions of dollars and potential criminal prosecution of responsible individuals. Given these stakes, most lenders adopt a risk-averse approach: when faced with an ownership structure that complicates beneficial ownership identification, they simply decline the application rather than assume the compliance risk.

The irony is profound: the very feature that makes Illinois Land Trusts attractive to investors—privacy—is precisely what makes them toxic to lenders operating under federal anti-money laundering mandates.

Legal Complexities in Lending: Why a UCC Collateral Assignment is Undesirable for Real Estate Lenders

Beyond compliance concerns, Illinois Land Trusts introduce a fundamental legal complexity that disrupts the standard mortgage lending process: the classification of the beneficiary's interest as personal property rather than real property.

In a conventional real estate transaction, the lender secures their loan with a mortgage (or deed of trust in some states) that creates a lien against the real property itself. This mortgage is recorded in the county land records, providing public notice of the lender's interest and establishing priority over subsequent claims. If the borrower defaults, the lender can foreclose on the property through well-established judicial or non-judicial procedures, ultimately taking possession of and selling the real estate to recover their investment.

With an Illinois Land Trust, this straightforward process becomes legally convoluted. Because the beneficiary's interest is personal property under Illinois common law, a standard real estate mortgage cannot properly secure the lender's interest. Instead, the lender must take a collateral assignment of the beneficial interest, which is governed by Article 9 of the Uniform Commercial Code (UCC) rather than real estate law.

This distinction creates multiple practical problems for lenders:

Perfection Requirements Differ: To perfect a security interest in personal property, the lender must file a UCC-1 financing statement with the Illinois Secretary of State, not a mortgage with the county recorder. This creates confusion about where to search for liens and how to establish priority among competing creditors.

Foreclosure Procedures Are Unclear: The UCC provides remedies for secured parties to take possession of collateral and sell it to satisfy a debt, but these procedures were designed for equipment, inventory, and accounts receivable—not real estate. Applying UCC foreclosure remedies to an interest in real property creates legal ambiguity that most lenders prefer to avoid entirely.

Title Insurance Complications: Title insurance companies, which protect lenders against defects in title, are generally reluctant to insure loans secured by beneficial interests in land trusts. The personal property classification creates uncertainty about whether standard title insurance policies adequately cover the lender's collateral position.

System Incompatibility: Most mortgage lenders operate with loan origination systems, underwriting software, and servicing platforms built exclusively around real estate mortgages. These systems contain templates for standard mortgage documents, automated workflows for recording mortgages in county land records, and foreclosure procedures aligned with state real estate law. Introducing a UCC collateral assignment requires manual workarounds, custom documentation, and specialized legal review—all of which increase costs and introduce operational risk.

Secondary Market Rejection: Perhaps most critically, loans secured by beneficial interests in land trusts face systematic rejection in the secondary mortgage market. Fannie Mae and Freddie Mac, which purchase the vast majority of conforming residential mortgages, have strict guidelines that strongly prefer loans secured by traditional mortgages on real property. While their guidelines technically allow for land trust financing under certain narrow circumstances, the requirements are so burdensome that most lenders avoid them entirely rather than risk being stuck holding a non-saleable loan.

The net result is that even if a lender wanted to accommodate an Illinois Land Trust, their operational infrastructure and secondary market constraints make it practically impossible to do so efficiently.

The "Letter of Direction" Problem: The Risk of Forged Documents and Legal Liability

A unique feature of Illinois Land Trusts introduces yet another layer of risk that has left lenders burned in the past: the trustee's reliance on "Letters of Direction" from the beneficiary to execute any action affecting the property.

Under the standard Illinois Land Trust structure, the trustee holds legal title but has no independent authority to manage or dispose of the property. Instead, the beneficiary (or designated holder of the power of direction) must provide written instructions—a Letter of Direction—authorizing the trustee to take specific actions such as executing a mortgage, selling the property, or entering into a lease.

This creates a vulnerability that has resulted in significant losses for lenders: the risk of forged or fraudulent Letters of Direction.

Consider the mechanics of a typical mortgage transaction involving a land trust. The borrower approaches a lender seeking a loan secured by property held in trust. The lender prepares mortgage documents and sends them to the trustee for execution. The trustee, before signing, requires a Letter of Direction from the beneficiary authorizing them to execute the mortgage. The trustee verifies that the letter bears the beneficiary's signature, then signs the mortgage documents on behalf of the trust.

The problem arises when the Letter of Direction is forged or issued by someone without actual authority. Because the trustee typically has limited contact with the beneficiary and may not have robust procedures for verifying signatures or confirming authority, fraudulent letters can slip through. When this happens, the mortgage executed by the trustee may be void or voidable, leaving the lender with no valid security interest despite having already disbursed the loan funds.

Historical cases have demonstrated this exact scenario playing out with devastating consequences. In some instances, individuals have forged Letters of Direction to mortgage properties they didn't actually control, pocketing the loan proceeds and leaving lenders holding worthless paper. In other cases, disputes among multiple beneficiaries have resulted in competing Letters of Direction, creating title defects that rendered the lender's mortgage unenforceable.

The legal liability extends beyond the immediate fraud. Lenders who accept mortgages executed based on fraudulent Letters of Direction may find themselves entangled in litigation with the true beneficial owners, who argue that the mortgage is invalid because the trustee acted without proper authorization. Even if the lender ultimately prevails, the legal costs and delays associated with resolving these disputes can far exceed the value of the underlying loan.

This "liability trap" has made lenders extremely wary of land trusts. The risk-reward calculation simply doesn't make sense: the potential for fraud and the complexity of verifying Letters of Direction far outweigh any benefit from making the loan. As a result, most institutional lenders have adopted blanket policies excluding land trusts rather than attempting to manage these document verification risks on a case-by-case basis.

National Lender Unfamiliarity: Why Out-of-State Underwriters Default to Denial

The final piece of the puzzle is perhaps the simplest yet most insurmountable: Illinois Land Trusts are a creature of Illinois common law, and most national mortgage lenders are based outside of Illinois.

Unlike statutory law, which is codified in clear legislative text, common law develops through court decisions over time. While Illinois has supplemented land trust common law with statutes such as the Land Trust Fiduciary Duties Act and the Land Trust Recordation and Transfer Tax Act, the fundamental legal principles governing these trusts remain rooted in judicial precedent that developed over more than a century.

For an underwriter sitting in Charlotte, Phoenix, or New York reviewing a loan application, an Illinois Land Trust appears as an unfamiliar and potentially risky legal structure. The underwriter may have never encountered one before, and their standard reference materials—underwriting guidelines, legal checklists, and approval matrices—likely don't address them. The trust agreement may contain legal terminology and provisions that differ from the real estate documents the underwriter reviews daily.

Faced with this uncertainty, the underwriter has two choices: invest significant time researching Illinois land trust law, consulting with legal counsel, and seeking approval from senior management for an exception to standard guidelines, or simply decline the application and move on to the next loan in the queue.

The economic incentives heavily favor denial. Underwriters are typically measured on efficiency metrics—how many loans they can process per day—and compensated based on loan volume, not on successfully navigating complex legal structures. Spending hours researching an unfamiliar ownership structure for a single loan doesn't make business sense when dozens of straightforward applications are waiting for review.

Moreover, underwriters operate in a risk-averse environment where approving a loan that later defaults reflects poorly on their judgment and can affect their employment. Declining a loan due to an unfamiliar ownership structure carries no professional penalty—it's simply a prudent exercise of caution. Approving that same loan and having it later result in foreclosure complications or losses opens the underwriter to criticism and potential disciplinary action.

This dynamic creates a systematic bias against Illinois Land Trusts at national lenders. Even if the legal structure is sound and the borrower is creditworthy, the simple fact that the underwriter is unfamiliar with Illinois common law creates an insurmountable barrier to approval.

The result is a lending environment where Illinois Land Trusts face near-universal rejection, not because of any specific defect in the borrower's creditworthiness, but because the ownership structure itself introduces compliance risks, legal complexities, fraud vulnerabilities, and unfamiliarity that lenders are unwilling to accept. For real estate investors seeking financing, this means that holding property in a land trust—regardless of its other benefits—effectively disqualifies the property from conventional mortgage financing in the modern lending market.

Your Path to Financing: How to Restructure Property Ownership for a Loan

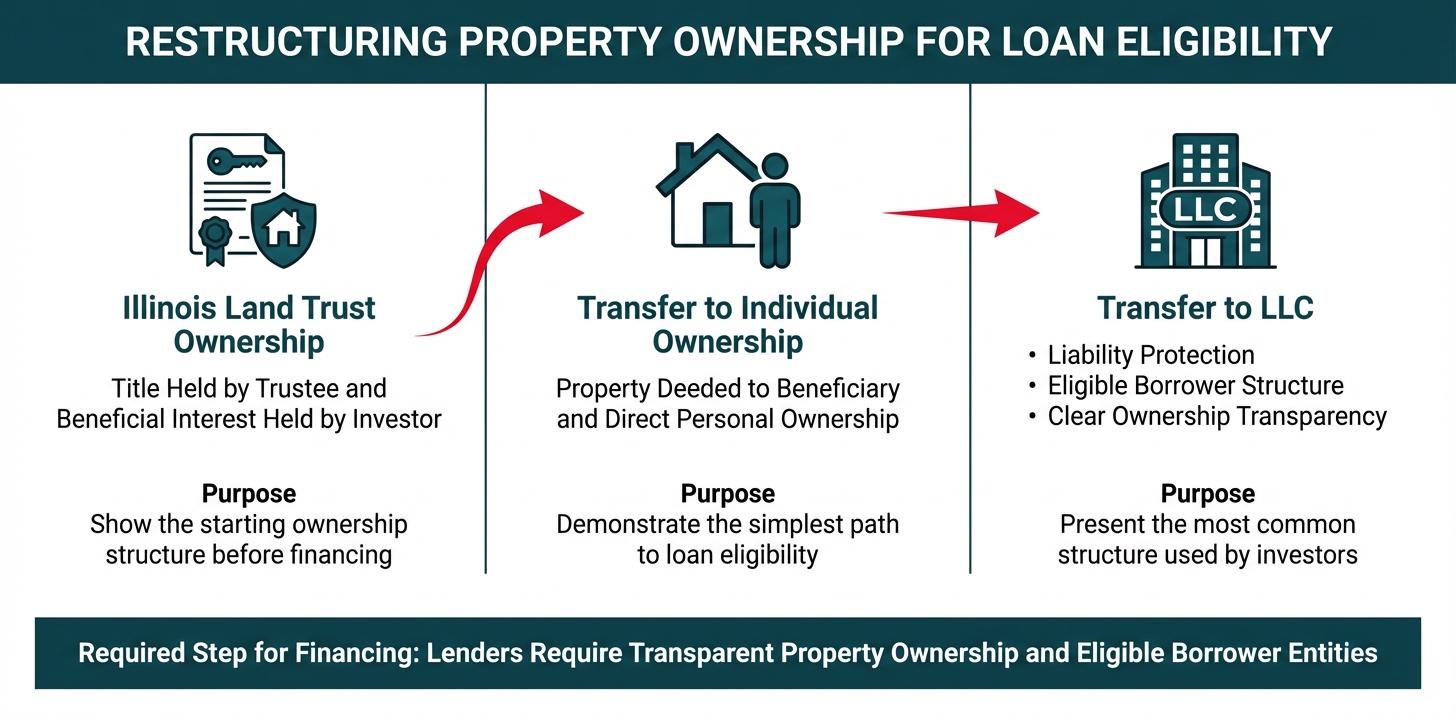

If you're a real estate investor who currently holds property in an Illinois Land Trust and you're seeking financing from OfferMarket, the essential first step is clear: you must move the property out of the land trust before applying for a loan. This restructuring is not optional—it's a prerequisite for eligibility. The good news is that the process, while requiring attention to legal detail, is straightforward when you understand the mechanics.

The beneficiary of an Illinois Land Trust retains the fundamental right to end the trust at any time and transfer the property out of the trust structure. This flexibility is one of the trust's inherent features, making the transition to a lender-eligible ownership structure a manageable task for most investors.

Why This Step Is Non-Negotiable

Before we dive into the mechanics, it's worth reiterating why this step is mandatory. OfferMarket's underwriting standards—like those of most institutional lenders—require transparency in ownership, clear legal pathways for foreclosure if necessary, and compliance with federal KYC and AML regulations. An Illinois Land Trust, by design, obscures beneficial ownership and classifies the beneficiary's interest as personal property rather than real property. This structure creates legal and operational friction that makes it incompatible with standard mortgage lending practices.

By moving your property into either your individual name or an eligible entity like an LLC, you eliminate these barriers and create a clean, transparent ownership structure that lenders can confidently underwrite.

Option 1: Deeding the Property to an Individual Name (The Beneficiary)

The most straightforward path is to transfer the property from the land trust directly into your own name as an individual. This approach works well if you plan to hold the property personally or if you're seeking a loan product that allows individual ownership.

Step 1: Obtain a Quit Claim Deed or Warranty Deed Form

The first step in this process is to prepare the appropriate deed document. In Illinois, you'll typically use either a Quit Claim Deed or a Warranty Deed to transfer property out of a land trust. The deed will show the trustee (the entity currently holding legal title) as the grantor and you (the beneficiary) as the grantee.

Many county recorder offices and title companies provide standard deed forms that you can download and complete. You'll need to ensure the deed includes all required information: the legal description of the property, the permanent real estate index number, the property address, and the names and addresses of both the grantor (trustee) and grantee (you).

Step 2: Execute the Deed with the Trustee's Signature

Because the trustee holds the legal and equitable title to the property, the trustee must sign the deed to effectuate the transfer. However, remember that under Illinois land trust law, the trustee can only act upon receiving a formal Letter of Direction from you, the beneficiary.

You'll need to provide your trustee with a written Letter of Direction instructing them to execute the deed transferring the property to you. This letter should reference the trust agreement, identify the property by legal description, and clearly state your direction for the trustee to convey the property to you individually.

Once the trustee receives this letter, they will sign the deed on behalf of the trust. The deed must be notarized to be valid for recording.

Step 3: Complete the Illinois Real Estate Transfer Declaration (Form PTAX-203)

Illinois law requires that you file Form PTAX-203, the Illinois Real Estate Transfer Declaration, with the deed or trust document when recording a property transfer. This form collects information about the transaction, including the sale price or fair market value, and is used to calculate transfer taxes.

In the case of transferring property out of a land trust to the beneficiary, you may qualify for an exemption from transfer taxes. According to the Illinois Department of Revenue's instructions for Form PTAX-203, you must file either the completed form with any required documents or an exemption notation on the original deed.

Common exemptions for land trust transfers include transfers between a grantor and their revocable trust, or transfers that don't involve a sale or valuable consideration. Consult with your attorney or title company to determine which exemption applies to your situation and how to properly document it.

Step 4: Record the Deed with the County Recorder

The final step is to record the deed with the County Recorder's office in the Illinois county where the property is located. You'll submit the signed and notarized deed along with the completed Form PTAX-203 (or exemption notation) and pay the required filing fees.

Recording the deed makes the transfer a matter of public record and officially moves the property from the land trust into your individual name. Once recorded, you'll receive a stamped copy of the deed showing the recording date and document number, which serves as proof of your ownership.

At this point, the property is no longer held in the land trust, and you can proceed with applying for financing from OfferMarket with the property titled in your individual name.

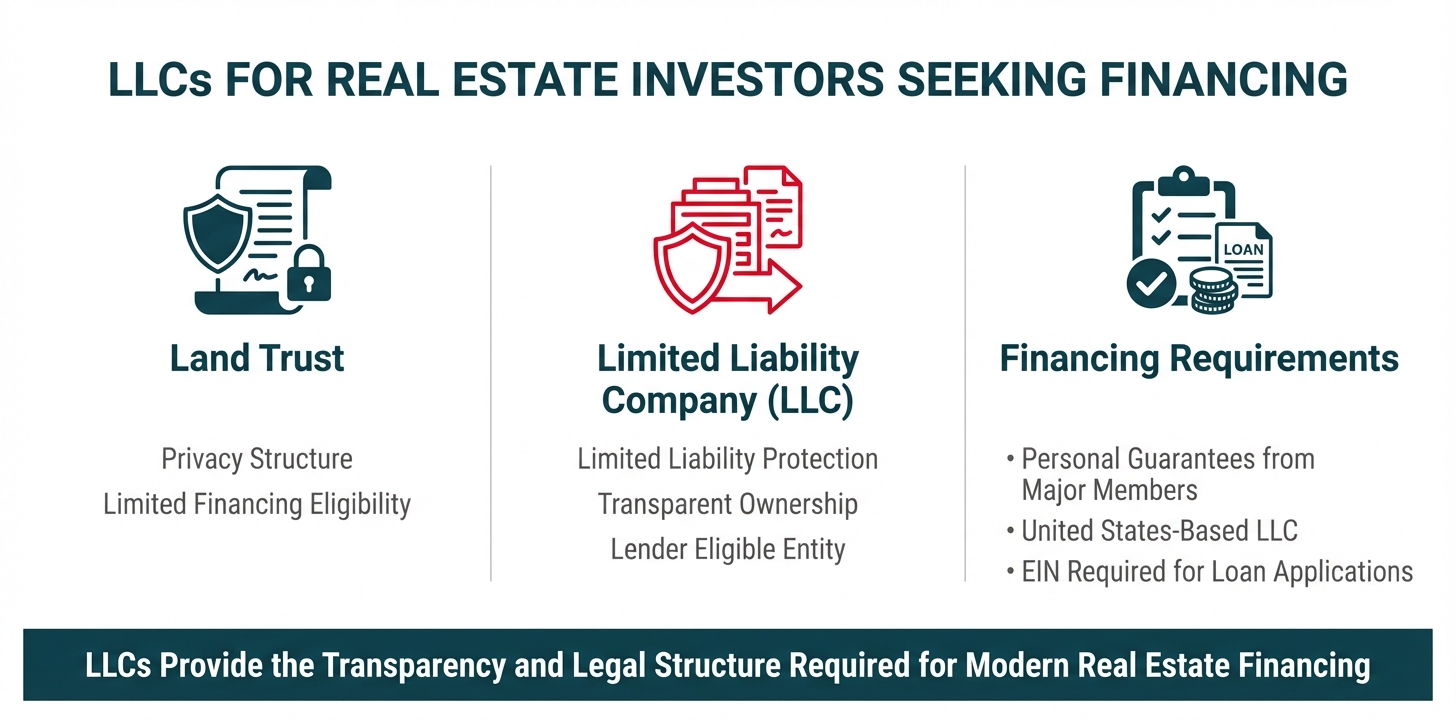

Option 2: Deeding the Property to an Eligible Entity, Such as an LLC

While transferring the property to your individual name is the simplest approach, many real estate investors prefer to hold investment properties in a Limited Liability Company (LLC). This strategy offers several advantages and is fully compatible with OfferMarket's lending guidelines, provided the LLC meets certain requirements.

Why an LLC Is Often the Preferred Structure

An LLC provides a balance of liability protection, operational flexibility, and lender acceptability that makes it an attractive alternative to both individual ownership and land trusts.

First, an LLC offers liability protection by creating a legal separation between your personal assets and the investment property. If a tenant is injured on the property or if the property faces a lawsuit, the claimant's recourse is generally limited to the assets held within the LLC, protecting your personal wealth.

Second, an LLC provides operational and tax flexibility. You can structure the LLC with multiple members, allocate profits and losses according to your operating agreement, and choose how the entity is taxed (as a disregarded entity, partnership, S-corporation, or C-corporation).

Third, and most importantly for financing purposes, a properly structured U.S.-based LLC is an eligible borrower for OfferMarket loans. Unlike an Illinois Land Trust, an LLC provides the transparency and legal clarity that lenders require. The LLC's operating agreement and articles of organization clearly identify the members (owners), and the entity can hold title to real property in a straightforward manner that fits within standard mortgage lending frameworks.

LLC Requirements for OfferMarket Financing

While LLCs are eligible entities, there are specific requirements you must meet:

- The LLC must be formed and registered in the United States

- Any member with a 20% to 25% or greater ownership interest (depending on the specific program) must act as a personal guarantor on the loan, and the guarantors combined must represent at least 51% of the entity's total ownership

- The LLC must provide its Tax Identification Number (EIN) and formation documents as part of the loan application

- The LLC's operating agreement must not contain provisions that restrict the lender's ability to foreclose or take title to the property in the event of default

These requirements ensure that the lender has full transparency into who controls the entity and has recourse to the personal assets of the guarantors if the loan defaults.

The Step-by-Step Process for Transferring to an LLC

The process for transferring property from a land trust to an LLC is similar to transferring to an individual, with a few additional steps:

Step 1: Form the LLC (If You Haven't Already)

If you don't already have an LLC established, you'll need to form one before you can transfer the property. This involves filing Articles of Organization with the Illinois Secretary of State, obtaining an Employer Identification Number (EIN) from the IRS, and drafting an operating agreement that governs how the LLC will be managed.

Many investors work with an attorney to ensure their LLC is properly structured for both asset protection and lender eligibility. The cost and complexity of forming an LLC are minimal compared to the benefits it provides.

Step 2: Prepare the Deed from the Trust to the LLC

Just as with an individual transfer, you'll need to prepare a deed showing the trustee as the grantor and your LLC as the grantee. The deed must include the LLC's full legal name exactly as it appears in the Articles of Organization.

Step 3: Provide a Letter of Direction to the Trustee

You'll provide your trustee with a Letter of Direction instructing them to execute the deed transferring the property to your LLC. The trustee will then sign the deed, which must be notarized.

Step 4: Complete Form PTAX-203 and Address Transfer Taxes

As with an individual transfer, you must complete and file Form PTAX-203 with the deed. Depending on the structure of your LLC and the nature of the transfer, you may qualify for an exemption from transfer taxes. If the LLC's members are identical to the beneficiaries of the land trust and no sale is occurring, an exemption may apply.

Step 5: Record the Deed with the County Recorder

The final step is to record the deed with the County Recorder's office in the county where the property is located, along with Form PTAX-203 and payment of any required fees. According to guidance from title companies that handle land trust transfers, the deed must be completed and recorded with the appropriate County Recorder to effectuate the transfer.

Once recorded, the property is officially titled in the name of your LLC, and you can proceed with your loan application to OfferMarket.

LLCs as the Preferred Entity for Real Estate Investors

For real estate investors seeking financing in 2026, a United States-based Limited Liability Company (LLC) has emerged as the gold standard for property ownership—particularly when an Illinois Land Trust is off the table. Unlike the opacity of a land trust, an LLC provides the transparency and legal clarity that modern lenders require while still offering robust asset protection.

Why LLCs Are Eligible for OfferMarket Financing

OfferMarket explicitly accepts U.S.-based LLCs as eligible borrowers for investment property loans. The reason is straightforward: LLCs operate within a well-established legal framework that provides lenders with the visibility and security they need to underwrite a loan confidently.

When you hold property in an LLC, the ownership structure is transparent. The LLC's formation documents, operating agreement, and member information are all accessible to the lender during the application process. This transparency directly addresses the "Know Your Customer" (KYC) and Anti-Money Laundering (AML) concerns that make land trusts problematic. Underwriters can clearly identify who owns the property, who controls it, and who will be responsible if the loan defaults.

From a legal standpoint, an LLC holds title to real property as real property—not as the personal property quirk that defines an Illinois Land Trust. This means lenders can use standard mortgage instruments and foreclosure procedures, which are built into every automated underwriting system in the industry. There are no UCC collateral assignments, no Letters of Direction, and no ambiguity about how the lender will recover their investment if things go wrong.

Requirements for LLC Financing

While LLCs are eligible, Most lenders does impose specific requirements to mitigate risk:

Personal Guarantees from All Members: Every member of the LLC must sign a personal guarantee on the loan. This means that if the LLC defaults, each member is personally liable for the debt. The guarantee pierces the corporate veil in a controlled, contractual way, giving the lender recourse beyond just the property itself. OfferMarket do not necessarily need every member of the LLC to sign a guarantee. We typically require personal guarantees only from members holding a 20% to 25% or greater ownership interest in the entity, provided those signing collectively represent at least 51% of the LLC's total ownership.

Tax Identification Number: The LLC must provide its federal Employer Identification Number (EIN) as part of the loan application. This allows the lender to verify the entity's legal existence, run background checks, and ensure compliance with federal lending regulations.

These requirements are non-negotiable, but they are also standard across the industry. For investors who have operated in land trusts specifically to avoid personal liability or public disclosure, this represents a significant shift in strategy.

Comparing Liability Protection: LLC vs. Land Trust

Both LLCs and land trusts offer forms of asset protection, but they achieve it through fundamentally different mechanisms—and each comes with trade-offs.

Liability Protection in an LLC: An LLC provides what is known as "limited liability," meaning that the personal assets of the members are generally shielded from lawsuits or judgments against the LLC. If a tenant sues the LLC for a slip-and-fall accident, the lawsuit targets the LLC's assets (the property and any business bank accounts), not the member's personal home, car, or savings. According to Gateville Law Firm, this liability protection is the key advantage of using an LLC structure, particularly when managing multiple properties through a Series LLC arrangement.

However, this protection is not absolute. Courts can "pierce the corporate veil" if the LLC is not properly maintained (e.g., commingling personal and business funds, failing to hold annual meetings, or undercapitalizing the entity). Additionally, as noted, lenders will require personal guarantees, which means members are still personally liable for the debt—even if they are protected from other types of liability.

Privacy and Judgment Protection in a Land Trust: An Illinois Land Trust does not provide direct liability protection in the way an LLC does. If someone sues you personally and wins a judgment, that judgment attaches to your personal property—and in an Illinois Land Trust, your beneficial interest is classified as personal property. However, because the trust keeps your name off public records, it makes you a harder target to find in the first place. As Aspire Legal explains, "A land trust is primarily used for privacy, while an LLC offers liability protection."

The land trust's true strength lies in its ability to avoid probate and simplify estate planning, not in shielding you from lawsuits. For investors who prioritize anonymity over liability protection, the land trust has historically been the preferred tool—but that privacy comes at the cost of financing eligibility in 2026.

The Hybrid Strategy: Combining Both Structures

Some sophisticated investors use a hybrid approach: they hold the beneficial interest of a land trust inside an LLC. This structure theoretically provides both the privacy of the trust and the liability protection of the LLC. However, this arrangement adds layers of complexity that many lenders—including OfferMarket—are unwilling to navigate. For financing purposes, the property must be held in a straightforward, single-entity LLC or in the investor's personal name.

Pros and Cons for Investors

LLC Pros:

- Eligible for financing with OfferMarket

- Clear liability protection for members (with proper maintenance)

- Transparent ownership structure that satisfies KYC/AML requirements

- Standard mortgage instruments and foreclosure procedures

LLC Cons:

- Requires personal guarantees, which expose members to debt liability

- Ownership is a matter of public record (less privacy than a land trust)

- Requires ongoing maintenance (annual filings, separate bank accounts, etc.)

Land Trust Pros:

- Maximum privacy—your name stays off public records

- Simplified estate planning and probate avoidance

- Easy transfer of beneficial interest without recording a new deed

Land Trust Cons:

- Ineligible for financing with OfferMarket and most lenders as of 2026

- Minimal liability protection compared to an LLC

- Requires trustee cooperation and Letters of Direction for all transactions

- Beneficial interest is personal property, subject to judgments

Making the Right Choice for Your Investment Strategy

For investors who need financing, the decision is clear: an LLC is the path forward. The transparency and legal clarity it provides are non-negotiable requirements in the current lending environment. While you sacrifice some privacy, you gain access to capital, liability protection, and a structure that works seamlessly with modern underwriting systems.

If privacy is your absolute priority and you do not need financing, a land trust may still serve a role in your portfolio—but it cannot be the entity holding title when you apply for a loan.

A Practical Guide: How to Set Up an Illinois Land Trust

Setting up an Illinois Land Trust is a straightforward legal process that requires careful attention to documentation and the selection of qualified professionals. While the structure offers privacy benefits, it's essential to understand each step to ensure your trust is properly established and legally compliant.

Step 1: Selecting a Qualified Trustee

The foundation of any Illinois Land Trust is choosing the right trustee to hold legal and equitable title to your property. Chicago Title Land Trust Company is one of the most established institutional trustees in Illinois, offering specialized land trust services with built-in protections against title fraud.

Your trustee can be a bank, trust company, attorney, or another qualified entity. The critical requirement is that they must be willing and able to carry out the fiduciary responsibilities of the role. Unlike other states where individuals commonly serve as trustees, Illinois investors typically prefer institutional trustees because they provide continuity, professional administration, and reduced personal liability.

When selecting a trustee, consider their experience with land trusts, their fee structure, and their willingness to execute documents promptly when you provide Letters of Direction. Chicago Title and other institutional trustees have standardized processes that make property transactions more efficient, though they charge annual fees for their services.

Step 2: Drafting the Land Trust Agreement

The Land Trust Agreement is the foundational contract between you (the beneficiary) and your chosen trustee. This private document establishes the terms under which the trustee will hold title and defines your rights as the beneficial owner.

Key provisions that must be included in your trust agreement:

Identification of Parties: The agreement must clearly name the trustee and all beneficiaries, along with their respective ownership percentages if there are multiple beneficial owners.

Power of Direction: This critical clause establishes who has the authority to direct the trustee's actions. Typically, this power rests with the beneficiary, but it can be assigned to a third party if desired.

Duration of the Trust: Illinois law allows land trusts to exist for up to 20 years, after which the trustee has a statutory duty to sell the property unless the trust is renewed or terminated earlier.

Distribution of Proceeds and Avails: The agreement must specify how rental income, sale proceeds, and other financial benefits from the property will be distributed among beneficiaries.

Successor Beneficiaries: To avoid probate, the agreement should designate who will inherit your beneficial interest upon your death, allowing for seamless transfer of ownership outside the court system.

Fiduciary Duties: Under the Land Trust Fiduciary Duties Act, holders of the power of direction are presumed to act in a fiduciary capacity unless the trust agreement explicitly states otherwise.

Most institutional trustees provide standardized trust agreement templates that comply with Illinois law, though you should have an attorney review any agreement before signing to ensure it meets your specific investment goals.

Step 3: Executing and Recording the Deed in Trust

Once your trust agreement is finalized, you must execute a formal Deed in Trust to transfer the property from your personal name into the trustee's name. This deed is the public-facing document that will be recorded with the County Recorder of Deeds in the Illinois county where your property is located.

The Deed in Trust typically includes:

- The legal description of the property being transferred

- The name of the trustee who will hold title

- A trust identification number or name (often a generic designation like "Land Trust No. 12345")

- Your signature as the grantor (the person transferring the property)

- Notarization and any required witnesses

The process requires drafting the deed and recording it with the appropriate county office, which makes the transfer a matter of public record. However, the actual trust agreement remains private and is not recorded, preserving the anonymity that makes land trusts attractive to many investors.

Recording fees vary by county but are generally modest compared to the potential privacy benefits. Once recorded, the public record will show the trustee as the titleholder, effectively removing your name from the property's ownership chain.

Step 4: Understanding the Power of Direction and Letters of Direction

The Power of Direction is what separates an Illinois Land Trust from other ownership structures. While the trustee holds legal title, they can only act upon written authorization from the beneficiary through a formal Letter of Direction.

When Letters of Direction Are Required:

- Executing mortgage documents or refinancing the property

- Selling or transferring the property to a new owner

- Entering into lease agreements or modifying existing leases

- Making capital improvements or major repairs

- Filing insurance claims or litigation related to the property

How to Execute a Letter of Direction:

Each letter must be in writing, signed by the beneficiary (or the designated holder of the power of direction), and typically notarized to prevent fraud. The letter should clearly state the specific action the trustee is authorized to take and any limitations on that authority.

For example, if you want to refinance your property, you would provide the trustee with a Letter of Direction authorizing them to sign the new mortgage documents on a specific date with a specific lender. The trustee cannot act without this written authorization, which protects you from unauthorized transactions but also means you must be proactive in providing direction whenever action is needed.

The Fraud Risk: Historically, forged Letters of Direction have created significant legal liability for trustees and lenders. This is one reason why many mortgage lenders now avoid financing properties held in land trusts—they fear being caught in disputes over whether a letter was genuine or fraudulent.

Step 5: Obtaining a TIN/EIN If Required

Whether your Illinois Land Trust needs a Tax Identification Number (TIN) or Employer Identification Number (EIN) from the IRS depends on how the trust is structured and whether you plan to seek financing.

For Simple Trusts: Most Illinois Land Trusts are treated by the IRS as "grantor trusts," meaning the tax liability passes through directly to the beneficiary's personal Social Security Number. In these cases, the trust itself does not file a separate tax return, and an EIN may not be required.

For Lender Compliance: However, if you plan to apply for mortgage financing, many lenders now require an EIN as part of their Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance procedures. Even though Illinois Land Trusts are currently classified as ineligible borrowers by most institutional lenders, having an EIN on file can help if lending guidelines change or if you're working with a private lender.

How to Obtain an EIN: You can apply for an EIN online through the IRS website at no cost. The application process is straightforward and typically takes only a few minutes. You'll need to provide basic information about the trust, including the trustee's name and the beneficiary's Social Security Number.

Important Note for 2026: As of early 2026, the lending environment has shifted dramatically against Illinois Land Trusts. Even with an EIN, most conventional and portfolio lenders categorize these trusts as ineligible borrowers due to transparency concerns and legal complexities. If financing is a priority for your investment strategy, you may need to hold title in your own name or transfer the property to an LLC before applying for a loan.

We recommend consulting a legal professional to discuss the implications of entity structuring. An experienced real estate attorney can help you determine whether an Illinois Land Trust aligns with your investment goals or whether an alternative structure, such as an LLC, would better serve your financing and liability protection needs.

Conclusion: Making an Informed Decision for Your Investment Strategy

The Illinois Land Trust has served real estate investors for decades as a powerful tool for privacy and estate planning. Its ability to keep ownership off public records, avoid probate, and simplify the transfer of beneficial interests made it an attractive choice for investors who valued discretion above all else. However, the modern lending environment of 2026 has fundamentally shifted the calculus for investors who need financing to grow their portfolios.

The Historical Appeal vs. Current Reality

Traditional benefits like anonymity and probate avoidance remain intact from a legal standpoint. If you own property free and clear and have no intention of refinancing or leveraging that equity, an Illinois Land Trust can still serve its original purpose. The trustee continues to hold legal and equitable title, your beneficial interest remains classified as personal property, and your name stays off the deed recorded at the county recorder's office.

But the moment you need a loan, everything changes. The very features that made land trusts appealing—privacy, the separation of legal title from beneficial interest, and the classification of your ownership as personal property—now trigger red flags for underwriters. Federal KYC and AML regulations require lenders to identify the ultimate beneficial owner with certainty. The legal quirk that transforms your interest into "personalty" forces lenders into unfamiliar UCC collateral assignment territory instead of standard mortgage procedures. Secondary market giants like Fannie Mae and Freddie Mac have made it clear they prefer lending to natural persons or transparent entities, not structures designed to obscure ownership.

The result is unambiguous: Illinois Land Trusts are ineligible borrowers under current OfferMarket loan programs, and this policy reflects a broader industry trend. Lenders have concluded that the foreclosure risks, legal complexities, and compliance burdens outweigh any potential benefit of working with these trusts.

Why Transparency and Structure Matter in 2026

The lending industry has moved decisively toward transparency and standardization. Underwriters are under intense regulatory pressure to verify the identity of borrowers and ensure that loan structures can be efficiently sold on the secondary market. This isn't a temporary trend—it reflects permanent changes in how financial institutions assess and manage risk.

A United States-based LLC offers everything a lender needs: a clear legal structure, transparent ownership through operating agreements, and a straightforward path to foreclosure if necessary. When you hold property in an LLC, the lender can record a standard mortgage against real property, not a UCC collateral assignment against personal property. Your LLC's members can provide personal guarantees, giving the lender recourse beyond just the property itself. Most importantly, the LLC doesn't obscure your identity—it documents it in a way that satisfies federal compliance requirements while still providing meaningful liability protection.

This is why entity structuring has become a critical consideration for real estate investors. The right structure doesn't just protect your assets; it positions you to access the capital you need to scale your portfolio. An LLC strikes the optimal balance between legal protection and financing eligibility, which is why it has become the preferred entity type for investment property ownership.

Structuring Your Deals for Success

Knowledge is power in real estate investing. Understanding the legal and financial implications of different ownership structures allows you to make strategic decisions that align with your long-term goals. If you currently hold property in an Illinois Land Trust and need financing, you now understand why restructuring is necessary and how to execute that transition.

The path forward is clear:

For existing land trust properties: Work with a qualified real estate attorney to deed the property out of the trust and into either your individual name or a U.S.-based LLC. This process typically involves executing a new deed from the trustee to the new owner and recording that deed with your county recorder. Once the property is held in an eligible entity structure, you can proceed with your loan application.

For future acquisitions: Consider establishing an LLC before purchasing your next property. This allows you to take title in an eligible entity from day one, avoiding the need for restructuring later. Your LLC's operating agreement should clearly identify all members, and those members should be prepared to act as personal guarantors on any financing.

For portfolio planning: If you own multiple properties, think strategically about how to structure your holdings. Different entity structures offer varying levels of tax efficiency and asset protection, and the optimal approach may involve multiple LLCs or a more sophisticated structure depending on your portfolio size and investment strategy.

The investors who succeed in 2026 and beyond will be those who understand that financing eligibility is just as important as legal protection. An ownership structure that blocks you from accessing capital ultimately limits your ability to grow. By choosing transparent, lender-friendly entities like LLCs, you position yourself to take advantage of opportunities as they arise.

Your Next Steps

You've now gained a comprehensive understanding of Illinois Land Trusts, why they're ineligible for financing, and how to restructure your property ownership to qualify for a loan. You know that the beneficiary's interest being classified as personal property creates legal complexities that lenders won't accept. You understand that federal compliance requirements demand transparency that land trusts were specifically designed to avoid. And you've learned that a U.S.-based LLC provides both the asset protection you need and the financing eligibility you require.

If you've already restructured your property out of a land trust—or if you hold title in your individual name or an eligible LLC—you're ready to move forward with financing.

Ready to finance your next investment property? Get your instant quote from OfferMarket now and discover how quickly you can access the capital you need to grow your portfolio. Our loan specialists understand the complexities of entity structuring and are here to help you navigate the process.

Have questions about whether your current entity structure qualifies? Contact our team to speak with a loan specialist who can review your specific situation and guide you toward the right solution. We're committed to transparency, education, and empowering investors with the knowledge they need to make informed decisions.

Your next deal is waiting. Let's make it happen.

OfferMarket Loans

Check your rate

60 seconds · no credit pull