*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

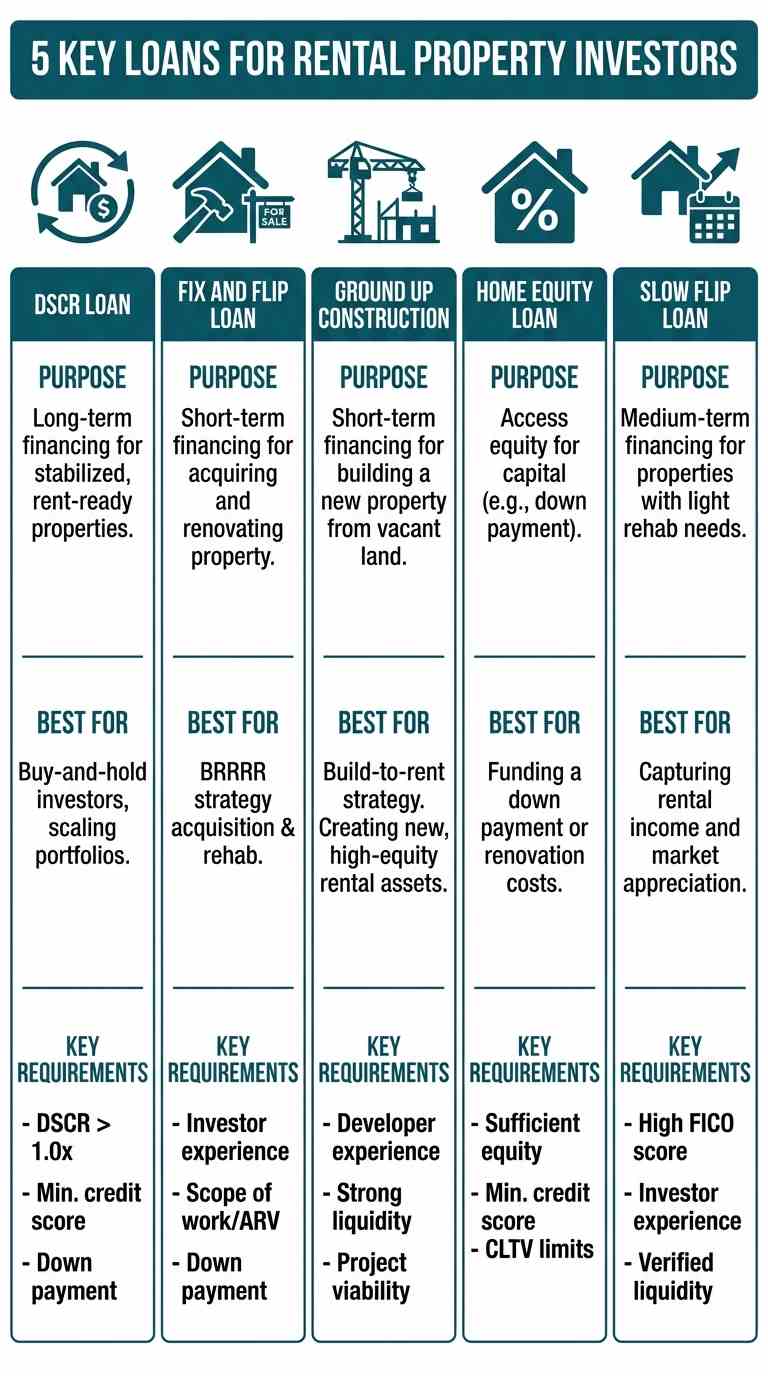

5 Types of Rental Property Loans for Investors

Financing a rental property requires a different approach than securing a mortgage for a primary residence. Investor loans are underwritten based on the property's potential to generate income, not just the borrower's personal financial picture. Understanding the five primary financing vehicles is the first step to scaling a real estate portfolio. These loans are specifically designed to meet different investment strategies, from long-term buy-and-hold to short-term construction projects.

The most common long-term financing solution is the DSCR (Debt Service Coverage Ratio) loan, which qualifies a borrower based on the property's cash flow. For investors focused on acquiring and renovating properties, a Fix and Flip loan provides the short-term capital needed for purchase and repairs. Those looking to create a rental from scratch can use a Ground-Up Construction loan. To fund a down payment, an investor might leverage a Home Equity Loan (HELOAN) on an existing property. Finally, for a strategy that blends light renovation with a medium-term hold, the Slow Flip loan offers a unique hybrid solution.

1. DSCR (Debt Service Coverage Ratio) Loan

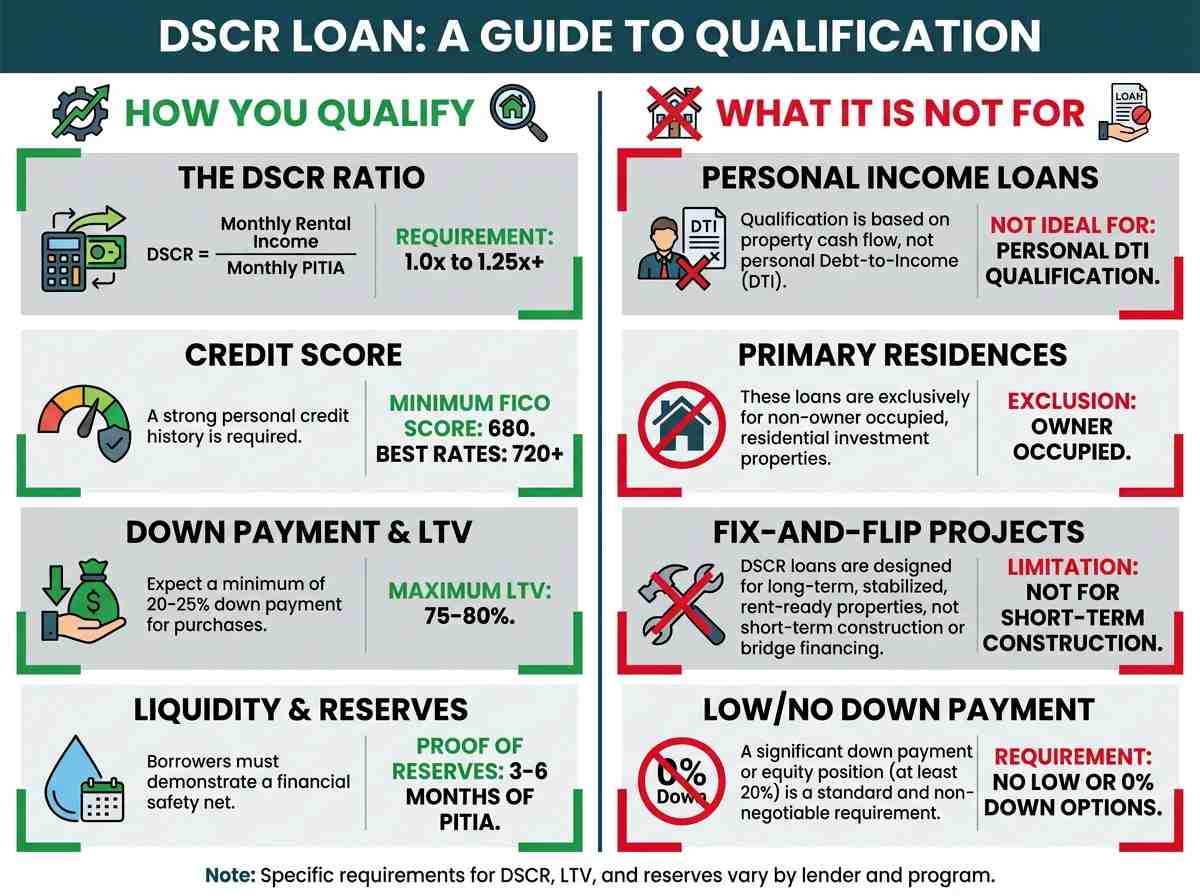

A DSCR loan is a type of non-qualified mortgage (Non-QM) designed specifically for real estate investors. Unlike conventional loans that heavily scrutinize a borrower's personal income and debt-to-income ratio (DTI), a DSCR loan focuses on the investment property's cash flow.

Purpose

The primary purpose of a DSCR loan is to provide long-term financing for income-generating, stabilized rental properties. It's the go-to product for investors looking to purchase a rent-ready property or refinance an existing one, including cash-out refinances.

Mechanics

Qualification hinges on the Debt Service Coverage Ratio, which measures the property's ability to cover its mortgage and related expenses. The formula is simple: Monthly Rental Income / Monthly PITIA (Principal, Interest, Taxes, Insurance, and any Association dues). If the resulting ratio is 1.0x or greater, the property generates enough income to cover its debt service. Lenders typically look for a DSCR of 1.25x or higher for the best terms, but many programs allow for ratios as low as 1.0x, and some even dip below for well-qualified borrowers.

Key Requirements

- Minimum DSCR: Typically 1.0x to 1.25x. A higher DSCR often leads to better pricing.

- Credit Score: A minimum FICO score is required, often starting at 680, with the best rates reserved for scores of 720+.

- Down Payment/Equity: Expect a down payment of at least 20-25% (or equivalent equity for a refinance). This translates to a maximum Loan-to-Value (LTV) of 75-80%.

- Liquidity: Borrowers must often show proof of reserves, typically 3-6 months of PITIA payments, to demonstrate they can cover vacancies or unexpected repairs.

Best For

DSCR loans are ideal for buy-and-hold investors who want to scale their portfolios without their personal DTI becoming a roadblock. They are also perfect for self-employed individuals or those with complex income structures that are difficult to document for conventional loans. If the property's cash flow is strong, the loan works.

2. Fix and Flip Loan

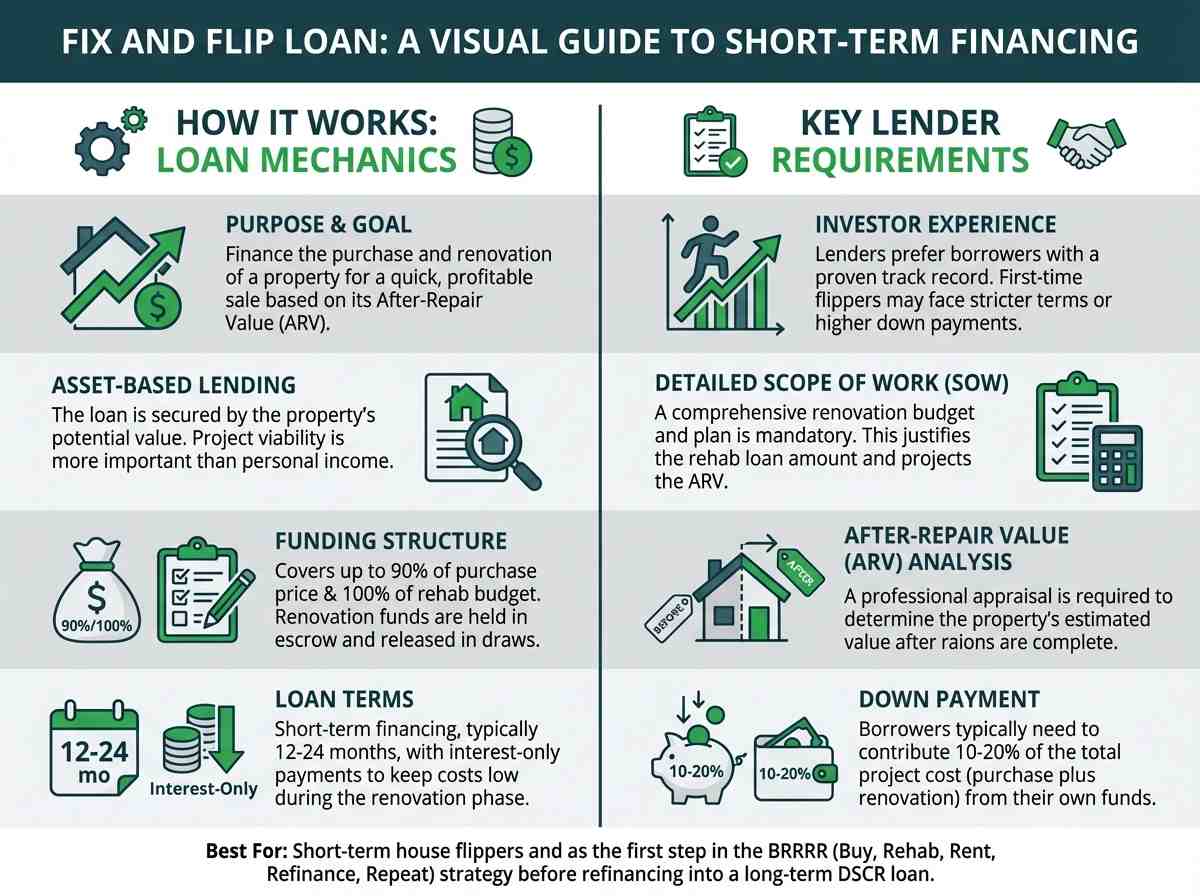

A fix and flip loan, often called a hard money loan or bridge loan, is a short-term financing tool used to acquire and renovate a property with the intent of selling it quickly for a profit.

Purpose

This loan provides the capital needed to both purchase a distressed property and fund the necessary renovations to bring it to its After-Repair Value (ARV).

Mechanics

These loans are asset-based, meaning the lender is more concerned with the viability of the project than the borrower's personal finances. The loan typically covers up to 90% of the purchase price and 100% of the renovation budget. The renovation funds are held in escrow and released in draws as construction milestones are completed and verified by an inspector. The loan term is short, usually 12-24 months, with interest-only payments.

Key Requirements

- Investor Experience: Lenders prefer borrowers with a track record of successful flips. First-time flippers may face higher rates or require larger down payments.

- Detailed Scope of Work (SOW): A comprehensive budget and renovation plan is mandatory. This document justifies the renovation loan amount and is used to project the ARV.

- ARV Analysis: The lender will conduct an appraisal to determine the property's estimated value after all renovations are complete. The loan amount is largely based on this future value.

- Down Payment: Typically 10-20% of the total project cost (purchase + rehab).

Best For

While designed for house flippers, this loan is the essential first step in the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy. An investor uses a fix and flip loan to acquire and rehab a property before stabilizing it with a tenant and refinancing into a long-term DSCR loan.

3. Ground Up Construction Loan

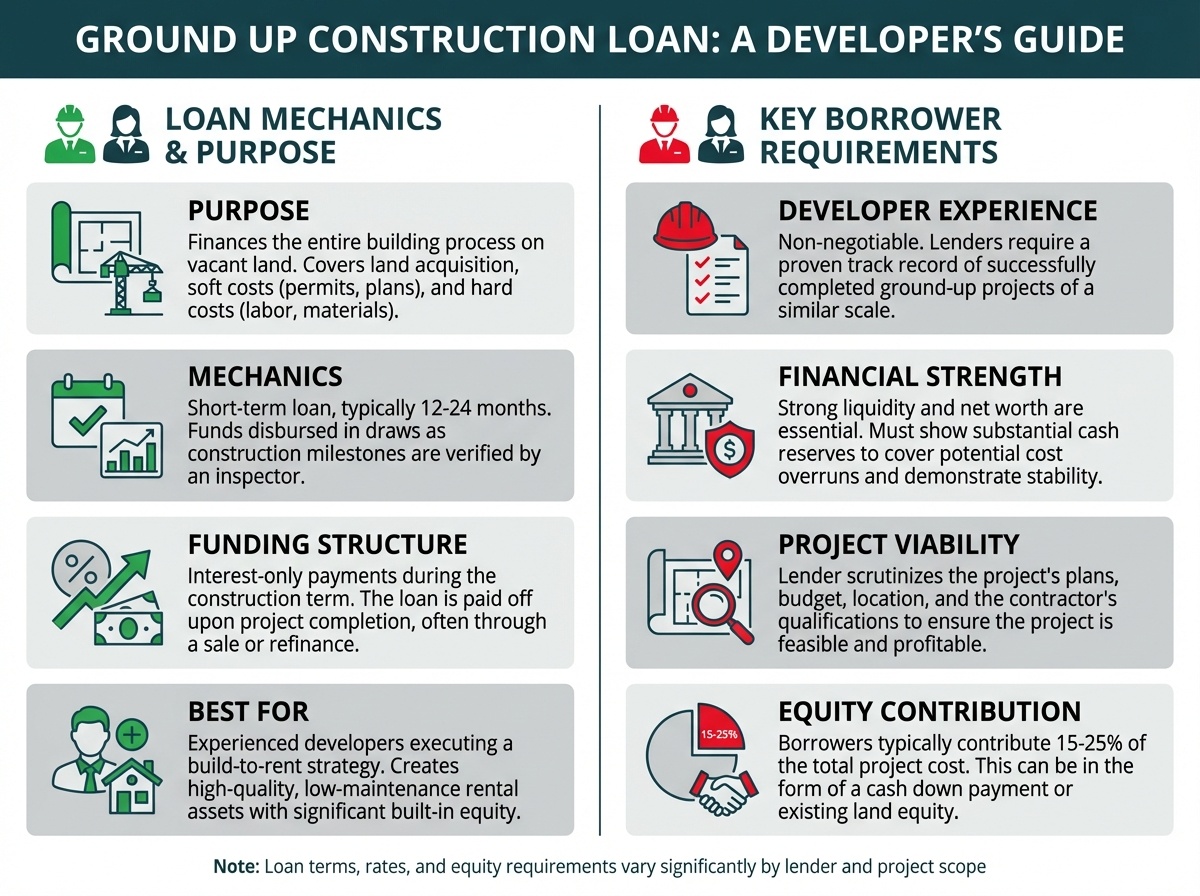

A ground up construction loan is a short-term loan that finances the entire process of building a new property on vacant land.

Purpose

This loan covers all associated costs, from land acquisition (if not already owned) and soft costs (permits, architectural plans) to the hard costs of labor and materials for construction.

Mechanics

Similar to a fix and flip loan, a construction loan is disbursed in draws based on a pre-approved construction schedule. As phases of the project are completed (e.g., foundation poured, framing complete), an inspector verifies the work, and the lender releases the next tranche of funds to the builder. These are interest-only loans with terms typically ranging from 12 to 24 months.

Key Requirements

- Significant Developer Experience: This is non-negotiable. Lenders require borrowers to have a proven track record of successfully completed ground-up projects of similar scale.

- Strong Liquidity and Net Worth: Borrowers must have substantial cash reserves and a strong financial statement to cover potential cost overruns and demonstrate financial stability.

- Project Viability: The lender will scrutinize the project's plans, budget, location, and the contractor's qualifications to ensure the project is feasible and likely to be profitable.

- Land Equity/Down Payment: The borrower typically needs to contribute 15-25% of the total project cost.

Best For

This loan is tailored for experienced investors and developers executing a build-to-rent strategy. By building a new rental property (such as a duplex or small multi-family building), they can create a high-quality, low-maintenance asset with significant built-in equity from day one.

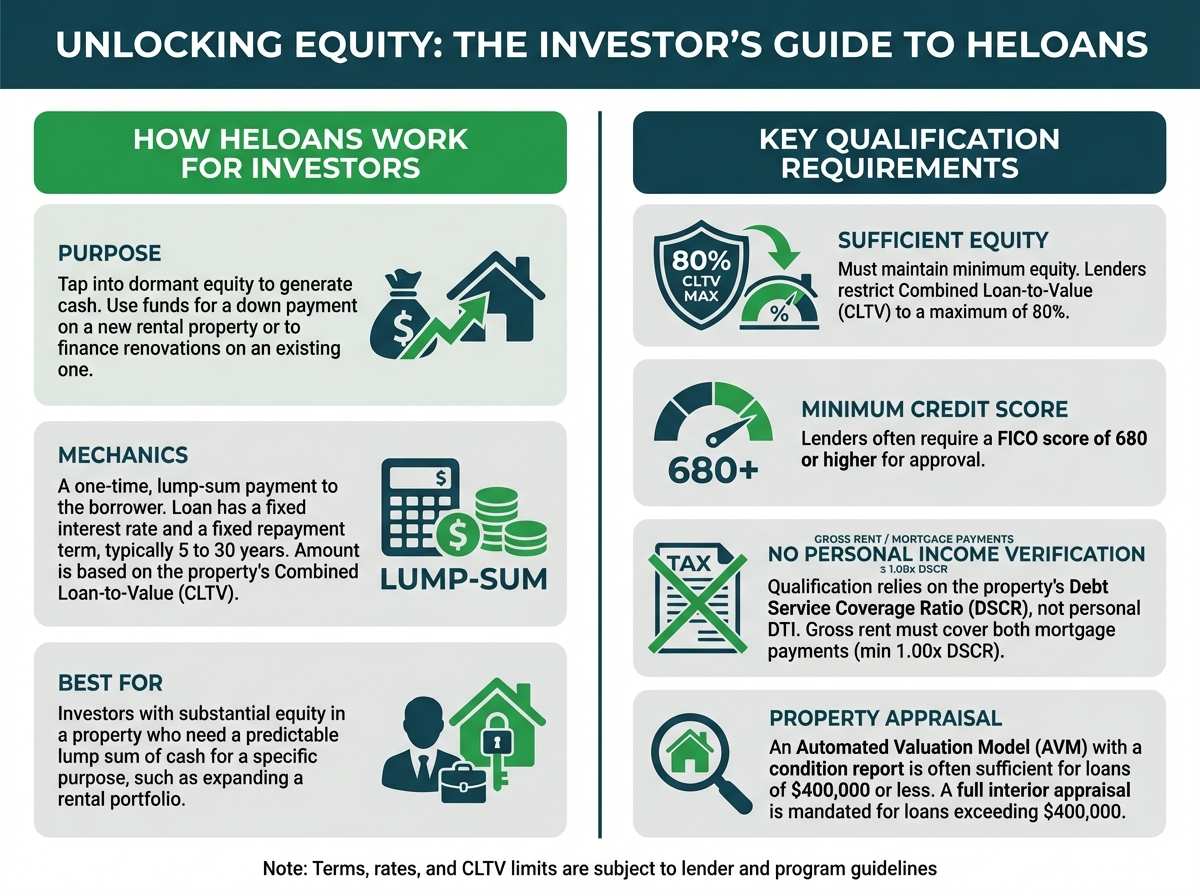

4. Home Equity Loan (HELOAN)

A Home Equity Loan, or HELOAN, is a type of second mortgage that allows a property owner to borrow against the equity they have built in an existing property.

Purpose

For real estate investors, the primary purpose of a HELOAN is to tap into dormant equity in their primary residence or another rental property to generate cash. This cash is most commonly used for the down payment on a new rental property purchase or to fund renovations on an existing one.

Mechanics

A HELOAN provides a one-time, lump-sum payment to the borrower. The loan amount is determined by the property's Combined Loan-to-Value (CLTV), which is the sum of the primary mortgage balance and the new home equity loan, divided by the property's current appraised value. Lenders typically cap the CLTV at 80-90%. The loan has a fixed interest rate and a fixed repayment term, usually 5 to 30 years.

Key Requirements

Sufficient Equity: The borrower must maintain a minimum amount of equity in the property, as lenders restrict your Combined Loan-to-Value (CLTV) to a maximum of 80%. For example, if your rental is worth $500,000 and your first mortgage balance is $250,000, you can secure up to $150,000 in a second lien (bringing your total combined debt to $400,000).

Minimum Credit Score: Lenders often require a FICO score of 680 or higher.

No Personal Income Verification (DSCR Underwriting): Because this is a business-purpose rental loan, lenders do not evaluate your personal income, tax returns, or Debt-to-Income (DTI) ratio. Instead, qualification relies entirely on the property's Debt Service Coverage Ratio (DSCR), meaning the monthly gross rent must cover both the existing first mortgage payment and the proposed second mortgage payment (requiring a minimum 1.00x DSCR)

Property Appraisal: While the lender must establish the property's current market value, a traditional full-interior appraisal is not always required. For loan amounts of $400,000 or less, lenders generally accept an Automated Valuation Model (AVM) paired with a property condition report. A full interior appraisal is only strictly mandated for loan amounts exceeding $400,000

Best For

A HELOAN is best for an investor who has built substantial equity in a property and needs a predictable lump sum of cash for a specific purpose, like a down payment. It's a powerful tool for leveraging an existing asset to expand a rental portfolio.

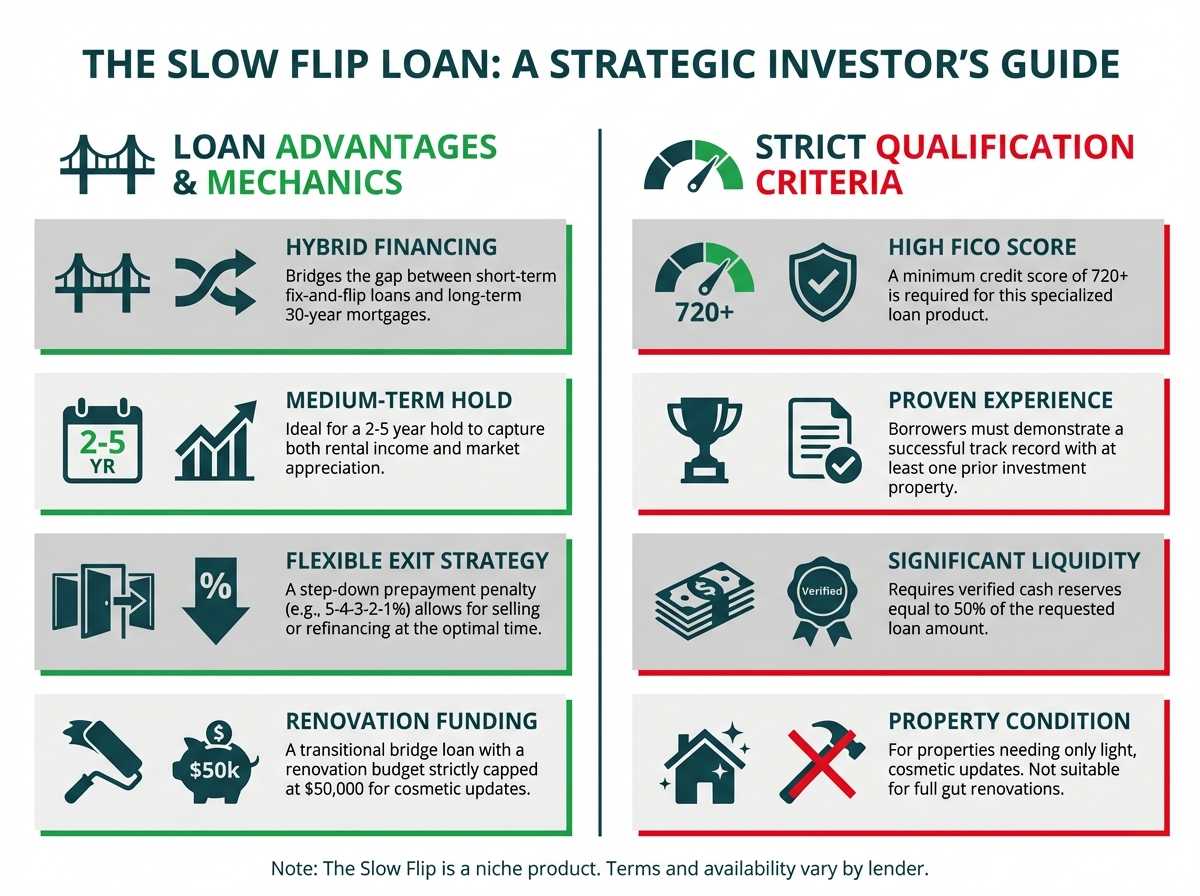

5. Slow Flip Loan

A Slow Flip loan is a hybrid financing product that bridges the gap between a short-term fix and flip loan and a long-term 30-year mortgage.

Purpose

This loan is designed for investors who acquire a property that needs light renovations and plan to hold it for a few years to capture market appreciation before selling or refinancing. It allows them to benefit from both rental income and potential value growth.

This is a transitional bridge loan strictly capped at a $50,000 maximum for small-balance renovations. Because it is designed to facilitate a renovation or medium-term hold before a sale or refinance.

Mechanics

The Slow Flip loan typically has a term of up to 5 years with a step-down prepayment penalty (e.g., 5% in year one, 4% in year two, etc.). This structure provides more flexibility than a hard money loan's 12-month term but avoids the long-term commitment of a 30-year mortgage. It allows the investor to hold the property through a market cycle without the pressure of an imminent balloon payment.

Key Requirements

- High FICO Score: Lenders often require a credit score of 720+ for this niche product.

- Prior Investment Experience: Borrowers usually need to demonstrate a history of successful real estate investments, a track record of at least one prior investment property.

- Verified Liquidity: Strong cash reserves are essential to qualify typically verified cash reserves equal to 50% of the requested loan amount.

- Property Condition: The property should be in relatively good condition, requiring only cosmetic updates rather than a full gut renovation.

Best For

This loan is perfect for the investor with a medium-term horizon. It's for someone who wants to make minor improvements, rent the property out for 2-3 years, and then sell or refinance after capturing both cash flow and appreciation. It's a less frantic version of a flip, offering multiple exit strategies.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

A Deep Dive into DSCR Loan Underwriting

While the DSCR formula is straightforward, lenders look at several interconnected factors during the underwriting process. Understanding these components will help you prepare your loan application and secure the best possible terms.

The DSCR Calculation Explained

As noted, the core of the underwriting is the DSCR calculation. Let's break down the two components:

Gross Rental Income: Lenders must verify the property's income. For a purchase, they will use the lesser of the appraiser's market rent opinion (from a Form 1007) or the actual rent from an executed lease. For a refinance of a seasoned property, they will typically use the current lease agreement, provided it's in line with market rates.

PITIA (Debt Service): This is the total housing payment. It includes the full Principal, Interest, Taxes, and Insurance payment for the new loan, plus any Homeowners' Association (HOA) or condo association dues. Lenders calculate this using the proposed loan amount, interest rate, and verified figures for property taxes and insurance premiums.

Example:

- Gross Monthly Rent: $3,000 ($36,000/year)

- Proposed Monthly PITIA: $2,400 ($28,800/year)

- DSCR Calculation: $36,000 / $28,800 = 1.25x

In this scenario, the property generates 25% more income than is needed to cover its debt service, making it a strong candidate for a DSCR loan. You can use a DSCR calculator to run this analysis on potential deals.

Credit, LTV, and Reserve Requirements

Beyond the property's cash flow, the borrower's financial strength plays a significant role in determining the loan terms.

Credit Score: This is a primary driver of your interest rate and maximum LTV. Lenders use a tiered system. For example, a borrower with a 720+ FICO score might qualify for 80% LTV, while a borrower with a 680 FICO might be limited to 70% LTV and receive a slightly higher interest rate.

Loan-to-Value (LTV): This represents the loan amount as a percentage of the property's allowable value. For a purchase transaction, lenders calculate your LTV using the lesser of the purchase price or the current appraised value. For a refinance, the calculation is heavily dictated by how long you have owned the asset (seasoning). If the property is fully seasoned (typically owned for more than 6 to 12 months), the LTV is based on the new appraised value. However, if it is unseasoned (owned for less than 6 to 12 months), lenders will generally restrict your valuation to the lesser of the current appraised value or your total Cost Basis (the original purchase price plus documented improvements). Lower LTVs represent less risk to the lender and will result in better interest rates and terms.

Reserve Requirements: Lenders need to see that you have the liquidity to withstand potential vacancies or unexpected maintenance. Most require 3-6 months of PITIA payments in a verifiable account (e.g., checking, savings, or brokerage account). For investors with large portfolios, the reserve requirement may be calculated as a percentage of the total unpaid balance of all their mortgages.

Property and Borrower Eligibility

DSCR loans are flexible but have specific guidelines for both the property and the borrower entity.

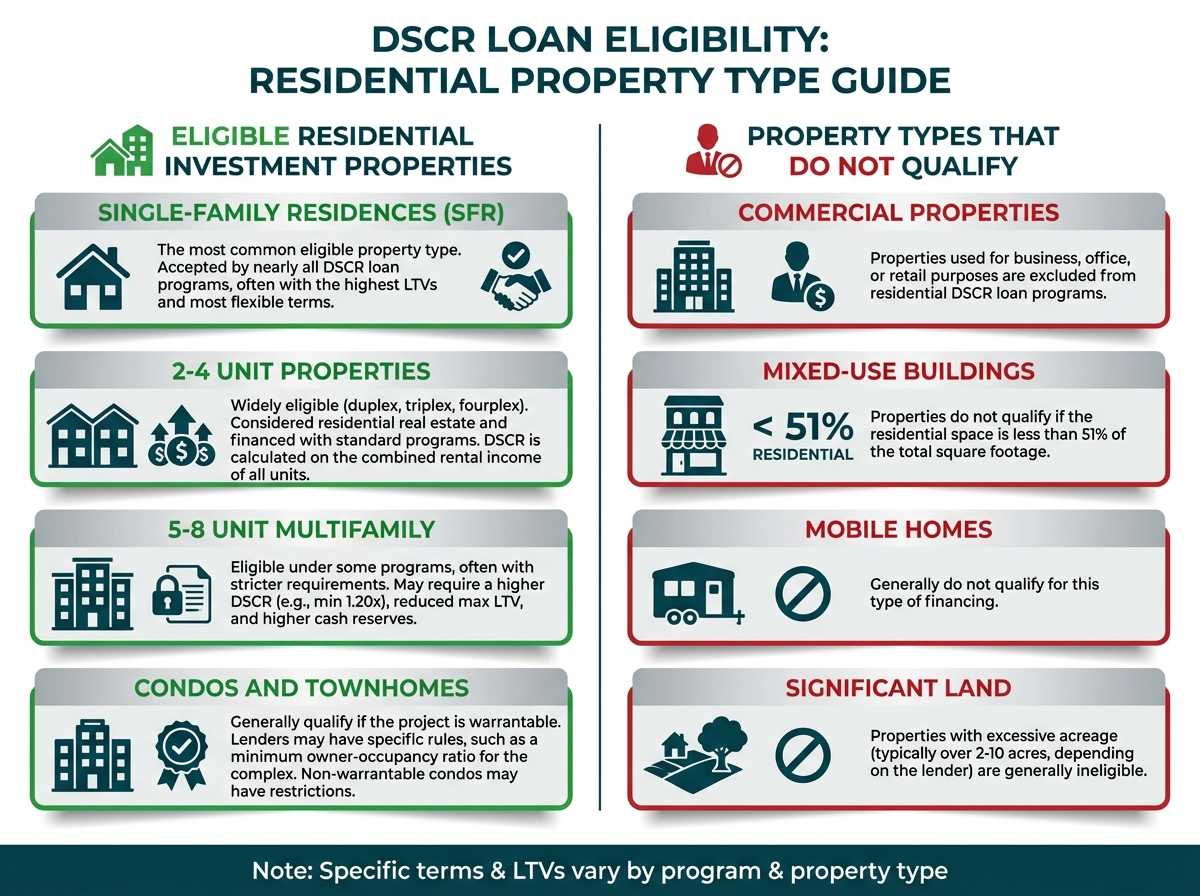

Eligible Property Types: These loans are available for residential properties, including single-family residences (SFRs), 2-4 unit properties, condos, townhomes, and sometimes even 5-8 unit multi-family buildings. Some lenders may have restrictions on condos, particularly non-warrantable condos.

Financing in an LLC: One of the major advantages of DSCR loans is the ability to close in the name of a Limited Liability Company (LLC) or other business entity. This is crucial for investors who want to protect their personal assets and maintain a professional business structure. Traditional lenders like Fannie Mae and Freddie Mac generally do not lend to LLCs.

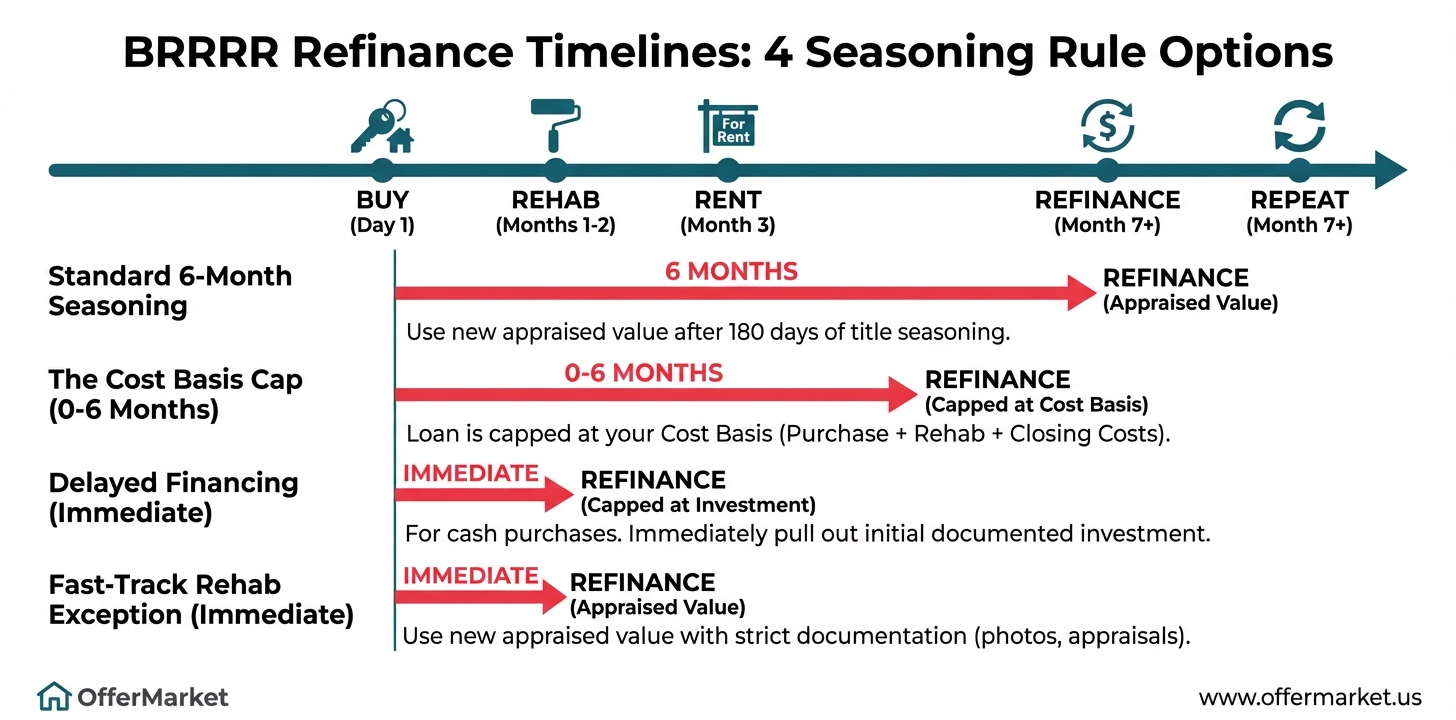

Seasoning Requirements

"Seasoning" refers to the period an investor must own a property before a lender will use its new, higher appraised value for a cash-out refinance. This is a critical concept for the BRRRR strategy.

The 6-Month Rule: Most lenders require a minimum of six months of seasoning. If you buy a property, renovate it, and try to refinance it after only three months, the lender will likely base the new loan on your original total cost (purchase price + documented rehab costs), not the new, higher ARV.

Purpose: This rule prevents predatory flipping and ensures the new value is stable and not just a temporary spike. Once you have held the property for six months, the lender will confidently use the current appraised value, allowing you to pull out your initial capital and the equity you've created.

Bypassing the 6-month seasoning requirement to accelerate capital velocity

The cornerstone of the Fast-Track method is leveraging the Delayed Financing Exception, a provision within conventional lending guidelines established by Fannie Mae. While many lenders are either unaware of this rule or unwilling to implement it, specialized lenders have built processes around it. This exception allows a borrower to execute a cash-out refinance immediately after purchasing a property with cash or a short-term loan (like a hard money loan), provided certain conditions are met. The key is proving that substantial renovations were completed, which justifies the new, higher appraised value. This turns a six-month cycle into a two- or three-month cycle, potentially tripling the number of deals an investor can complete in a year with the same pool of capital.

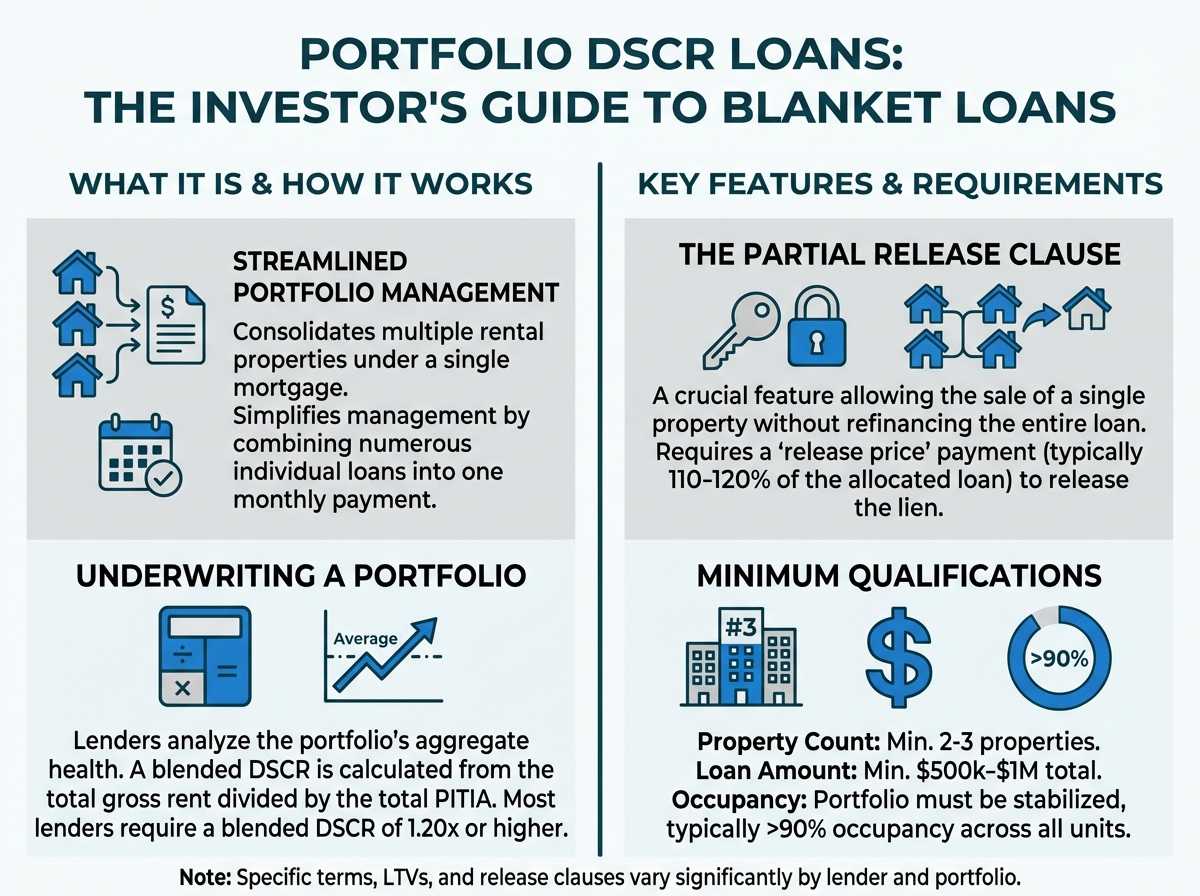

Scaling Your Portfolio with Blanket Loans

For seasoned investors managing multiple properties, a portfolio DSCR loan, often called a blanket loan, is a powerful tool for simplification and growth.

What is a Portfolio DSCR Loan?

A portfolio loan consolidates multiple rental properties under a single mortgage. Instead of juggling five, ten, or twenty individual loans with different payments and due dates, the investor has one loan and one monthly payment. This streamlines portfolio management and can unlock more favorable financing terms.

Underwriting a Portfolio

The underwriting process for a blanket loan is similar to a single DSCR loan but is performed on an aggregate basis.

Calculating a Blended DSCR: The lender calculates the total gross rent for all properties in the portfolio and divides it by the total PITIA for all properties. This results in a blended DSCR. For example, if some properties have a very high DSCR (e.g., 1.8x) and others are lower (e.g., 1.1x), the lender will look at the weighted average. Most portfolio lenders require a blended DSCR of 1.20x or higher.

Portfolio Metrics: Lenders will also analyze the portfolio's overall health, looking at factors like geographic diversification, average occupancy rate, and property types.

The Partial Release Clause

This is arguably the most important feature of a blanket loan. A partial release clause is a provision in the mortgage that allows the borrower to sell one of the properties in the portfolio without having to pay off the entire loan. The clause specifies a "release price" (typically 110-120% of the loan amount allocated to that specific property) that must be paid to the lender to release their lien on that single asset. This provides crucial flexibility for an investor who wants to strategically sell off an underperforming asset or capitalize on a hot market.

Key Requirements

- Minimum Property Count: Lenders often require a minimum of 2 to 3 properties to qualify for a blanket loan.

- Minimum Portfolio Loan Amount: The total loan amount typically needs to exceed a certain threshold, such as $500,000 or $1 million.

- Occupancy Rates: The portfolio must be stabilized, with a high occupancy rate (e.g., 90% or more) across all units.

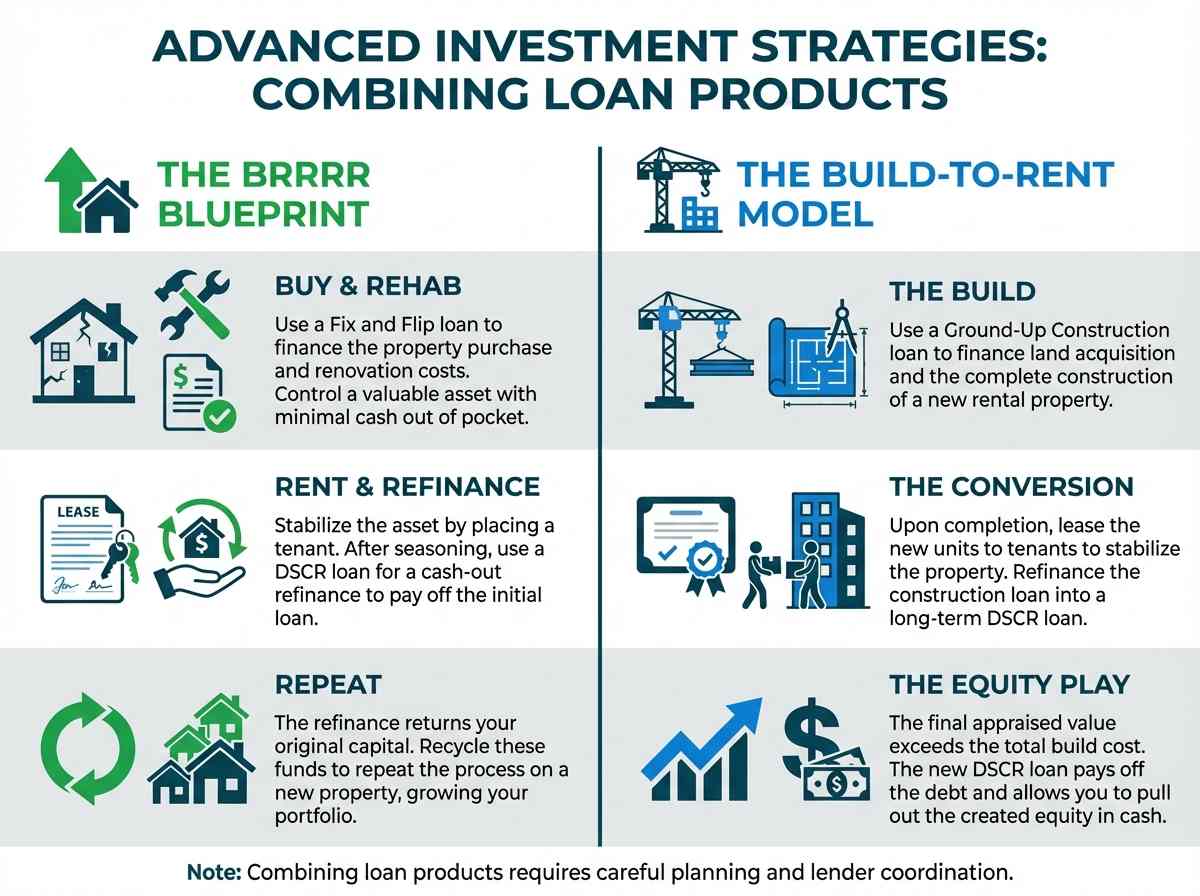

Advanced Investment Strategies: Combining Loan Products

The true power of these specialized loan products is realized when you combine them to execute sophisticated investment strategies. By pairing short-term acquisition loans with long-term rental financing, you can create a powerful engine for portfolio growth.

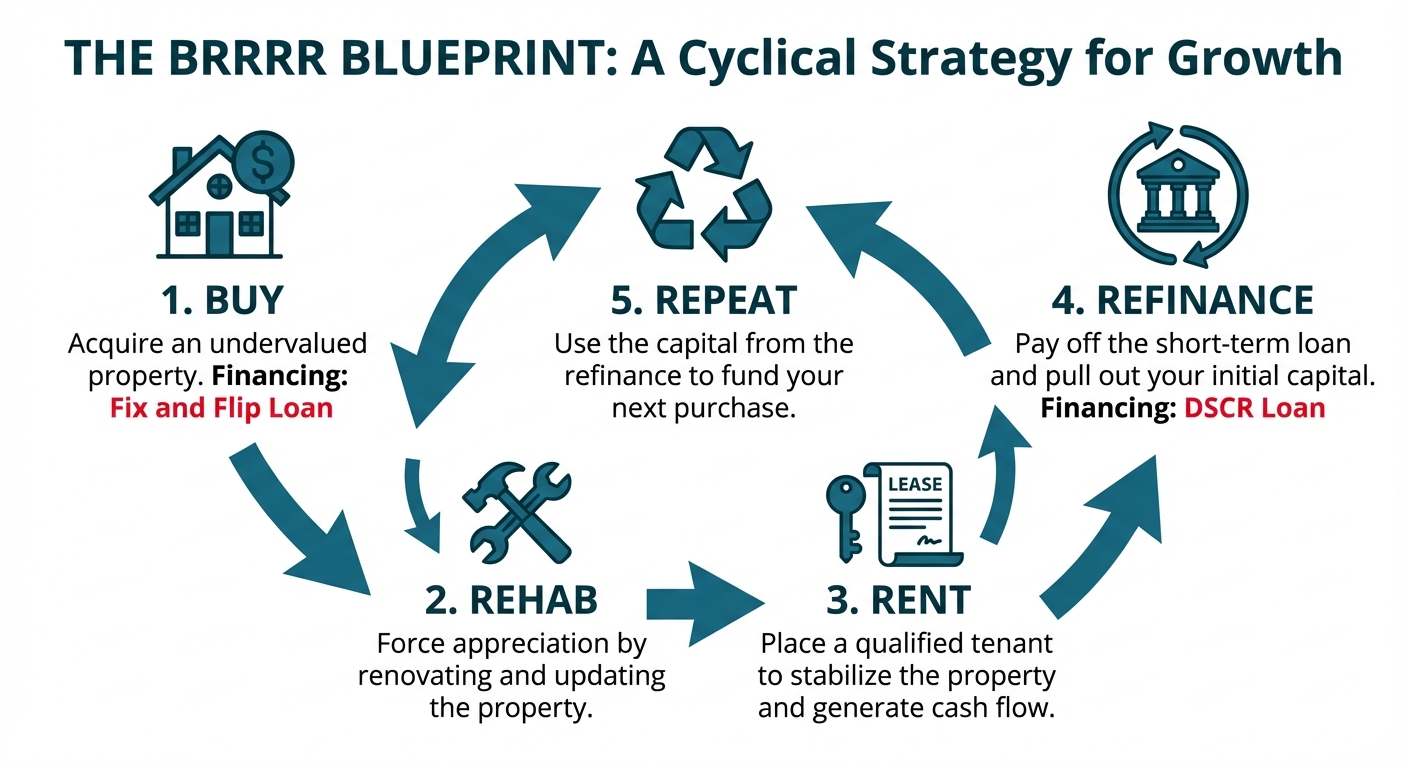

The BRRRR Blueprint: Fix and Flip Loan + DSCR Loan

The BRRRR method is a popular strategy for building a rental portfolio with a relatively small amount of initial capital. It revolves around buying distressed properties and forcing appreciation through renovation.

Buy and Rehab: An investor identifies an undervalued property that needs work. They use a Fix and Flip loan to finance both the purchase and the renovation costs. This allows them to control a valuable asset with minimal cash out of pocket.

Rent and Refinance: Once the renovations are complete, the investor places a tenant in the property, signing a lease. This "stabilizes" the asset by establishing a verifiable income stream. After the seasoning period (typically 6 months or no seasoning if you are leveraging the Delayed Financing Exception), apply for a cash-out refinance using a long-term DSCR loan. Because the property is now worth significantly more (the ARV), the new loan is large enough to completely pay off the original fix and flip loan.

Repeat: The best part of the strategy is that the DSCR loan often provides enough cash to not only pay off the first loan but also return the investor's original down payment and closing costs. This allows the investor to "recycle" their initial capital and use it to repeat the process on a new property, all while retaining the first cash-flowing rental.

The Build-to-Rent Model: Ground-Up Construction Loan + DSCR Loan

For more experienced developers, the build-to-rent model offers a way to create brand-new, high-performing rental assets from scratch, manufacturing equity in the process.

The Build: An investor or developer uses a Ground-Up Construction loan to finance the land acquisition and construction of a new rental property, such as a duplex or a row of townhomes. This short-term loan covers the project costs through completion.

The Conversion: Upon receiving the Certificate of Occupancy, the developer leases the units to tenants. Once stabilized, they refinance the construction loan into a long-term DSCR loan. According to market data from sources like the National Association of Home Builders (NAHB), the build-to-rent sector has seen significant growth, indicating strong tenant demand for new-construction rental products.

The Equity Play: The final appraised value of the newly constructed, stabilized property is almost always significantly higher than the total cost to build it. The new DSCR loan pays off the construction debt, and the developer can pull out the equity they created in cash. They are left with a brand-new, low-maintenance, cash-flowing rental property and have their capital back to start the next project.

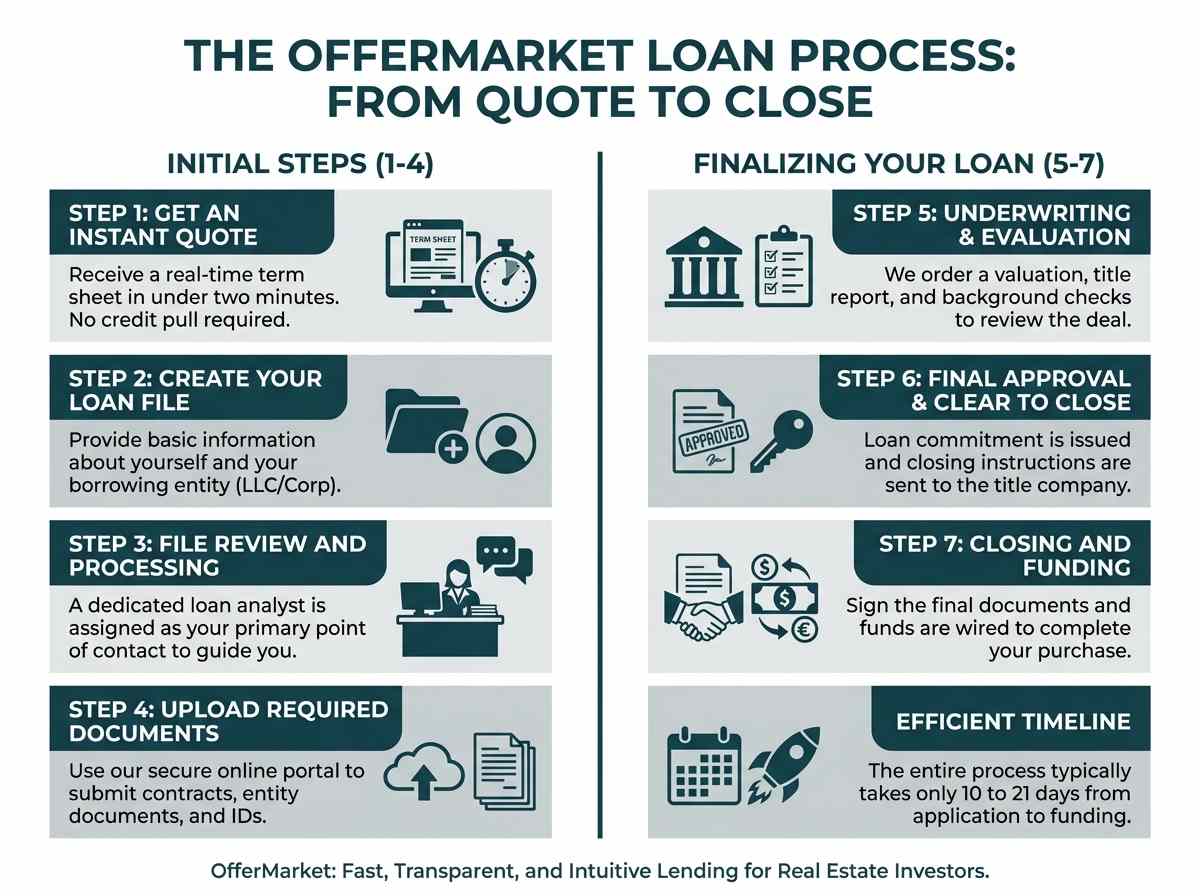

The OfferMarket Loan Process Step-by-Step

We've designed our lending platform to be fast, transparent, and intuitive for real estate investors. Our goal is to get you from application to closing as efficiently as possible.

Step 1: Get an Instant Quote: Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File: If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing: Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents: Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation: While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close: Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding: You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Get Your Instant Loan Quote

Understanding the theory behind rental property loans is the first step. The next is to see how it applies to your specific investment scenario. Asset-based lending is designed for speed and efficiency, removing the barriers that traditional banks put in front of real estate investors. By focusing on the property's income potential, we provide a streamlined path to financing that allows you to close deals faster and scale your portfolio with confidence.

Ready to see your terms? Get an instant loan quote and receive a customized rate and term sheet for your next rental property in under two minutes.

Want to analyze a deal's profitability first? Use our free DSCR & Fix and Flip Calculator to stress-test the cash flow and see how different financing scenarios impact your returns.

Run Your Numbers in 60 Seconds

Get a transparent breakdown of rates, terms, and max LTV for your next deal. No hard credit pull, no commitment.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull