*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Pros and Cons of Home Equity Loans for Real Estate Investors

Thinking about tapping into your property's equity to grow your real estate portfolio? You're not alone. Home equity loans have become a go-to financing tool for landlords and investors looking to unlock capital without selling their properties or refinancing their first mortgages.

![**Task**: Create a clean, professional infographic that explains the basic concept of a home equity loan for real estate investors, showing the relationship between property value, existing mortgage, and available equity.

**Visual Structure**: A vertical infographic layout with a house icon at the top, followed by a stacked bar representation showing the equity breakdown, and three key benefit callouts at the bottom.

**ASCII Layout Reference**:

```

+------------------------------------------+

| [HOUSE ICON - SIMPLE OUTLINE] |

| HOME EQUITY LOAN FUNDAMENTALS |

+------------------------------------------+

| |

| Property Value: $500,000 |

| +------------------------------------+ |

| | Available Equity | |

| | $200,000 | |

| | (Can Borrow Up To) | |

| +------------------------------------+ |

| | Existing Mortgage Balance | |

| | $300,000 | |

| +------------------------------------+ |

| |

| [ICON] Fixed Rates [ICON] Lump Sum |

| Predictable Immediate |

| Payments Capital |

| |

| [ICON] Tax Benefits |

| Potential Interest |

| Deductions |

+------------------------------------------+

```

**Image Section Breakdown**:

- Header section: House icon in deep teal (#1b444a) with text](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771971282907_n67ds5.jpg?alt=media&token=065210c5-af0e-4dd7-bc89-53cb9fb06d96)

Summary: Home Equity Loan Pros and Cons at a Glance

| Factor | Pros | Cons |

|---|---|---|

| Interest Rates | Fixed rates mean you'll know exactly what you're paying each month; average rates hovering around 7.59% as of February 2026—way better than credit cards or personal loans; rates have dropped to three-year lows | Still higher than your first mortgage rate; your actual rate depends on your credit score, LTV ratio, and lender; expect slightly higher rates on investment properties compared to your primary home |

| Qualification Options | Plenty of ways to prove your income: traditional W-2s, bank statements (12 months personal or business), DSCR for investors (minimum 1.00x ratio), 1099s, or P&L statements; great flexibility if you're self-employed | Credit score minimums are firm (typically 660-680 FICO); DTI maxes out at 50%; you'll need a clean payment history (no late payments in the last 12 months); first lien restrictions apply |

| Loan Amount & Leverage | Solid CLTV options: up to 90% for primary residences (720+ FICO), up to 80% for investment/second homes; unlimited cash-out when CLTV stays at 65% or below; loans under $400k may qualify for AVM instead of full appraisal | Cash-out tops out at $500k when CLTV exceeds 65%; rural properties face heavy restrictions or may not qualify; maximum 2 acres allowed; condotels are ineligible; property can't have been listed for sale in the past 6 months |

| Tax Benefits | Interest could be tax-deductible when you use funds for property improvements or business purposes (investment properties); always check with your tax advisor for your specific situation | Tax deduction doesn't apply to every use; personal debt consolidation likely won't qualify; investment property loans need a business purpose affidavit; tax implications can get tricky—professional guidance is worth it |

| Loan Structure | Lump sum gives you immediate capital for big projects; fixed repayment terms (10, 15, 20, or 30 years) make budgeting straightforward; no prepayment penalty on primary residences in most states | You're borrowing the full amount upfront—even if you don't need it all right away; investment properties often come with 1-5 year prepayment penalties; interest-only payments typically aren't an option (except Elite programs); fully amortizing structure is required |

| Reserve Requirements | Most programs require zero cash reserves (just cash to close); keeps your money free for other investments; gift funds are allowed for down payment on primary residences | No reserve cushion could put you at risk if rental income dips; gift funds can't count toward reserves (though reserves typically aren't required anyway); you'll still need to show sufficient cash to close |

| Closing Process & Fees | Streamlined process for loans under $400k: AVM with Property Condition Report works; O&E Report instead of full title policy cuts costs; faster closing timeline for smaller loans | Standard closing costs apply, including origination fees (0. 5-1%), appraisal fees ($300-$500), credit report fees, title fees; full appraisal required for loans >$400k; longer closing period than DSCR loans or other investor products (typically 30-45 days) |

| Property Eligibility | Works for primary residences, second homes, and investment properties; DSCR qualification option built specifically for investors; no seasoning requirement on your existing mortgage | Won't work if your first lien is a private mortgage opened within the last 12 months; first lien can't have negative amortization, balloon payment, or be a reverse mortgage; solar panel liens need to be subordinated or paid off; ADU rental income can't count toward qualification |

| Risk & Security | Lower risk than unsecured debt; your built-up equity gives you borrowing power; fixed payments shield you from rate increases; credit score impact usually minimal when you pay on time | Your property is collateral - missing payments puts you at foreclosure risk; adds to your total debt load; affects your debt-to-income ratio for future borrowing; flood insurance escrow required if property sits in a flood zone and first lien doesn't escrow |

| Market Trends (2024-2026) | Home equity originations climbed in 2024, with average originations hitting $844 million per company, up from $788 million in 2023; rates sitting at three-year lows; average FICO score for home equity loans landed at 749 in 2024 | Credit standards tighter than historical averages; more competition for borrowers; rate environment still elevated compared to pre-2022 levels; lenders pickier on investment properties |

| Use of Funds Flexibility | Put the money toward property renovations, purchasing additional investment properties, capital improvements, essential home equipment upgrades (HVAC, roofing), or business purposes | Investment property proceeds typically can't go toward personal consumer debt consolidation if you want to keep the business purpose exemption; restrictions on use may impact tax deductibility; lender may ask for documentation showing how you used the funds |

This table gives you a clear picture of the key factors to weigh when considering a home equity loan for your real estate portfolio. Each factor presents trade-offs that you'll need to weigh against your specific investment strategy, financial profile, and property portfolio goals.

Pros of Home Equity Loans for Real Estate Investors

Home equity loans pack some serious advantages for landlords and investors ready to put their existing property equity to work. Let's break down the benefits so you can see if this financing tool fits your game plan.

Fixed Interest Rates with Predictable Payments

Here's one of the biggest wins with home equity loans: your interest rate stays locked in for the entire loan term—whether that's 10, 15, 20, or 30 years. No surprises. Your monthly payment stays the same from start to finish, which makes budgeting and cash flow forecasting straightforward. And when you're juggling multiple properties and income streams, that kind of predictability is gold.

For landlords, this is a game-changer. You'll know exactly what your debt service looks like, so you can make sure your rental income covers your expenses without sweating over rate hikes. This stability gives you the confidence to plan your long-term investment moves without second-guessing.

Lower Interest Rates Compared to Unsecured Loans

Home equity loans typically come with significantly lower interest rates than unsecured options like personal loans or credit cards. Why? Because your property backs the loan, lenders see less risk—and they reward you with better rates. According to the Mortgage Bankers Association, home equity loan originations averaged $844 million per company in 2024, showing just how many savvy borrowers are tapping into this smart financing strategy.

For real estate investors like you, this rate advantage can put real money back in your pocket over the life of your loan. Let's say you're planning a $100,000 property renovation. The difference between a 7% home equity loan and a 12% personal loan could save you tens of thousands of dollars in interest over a 15-year period. That's money you can reinvest in your next deal.

High Leverage Options

Home equity loans give you serious leverage potential, especially if you've built strong credit. For your primary residence, you can tap up to 90% Combined Loan-to-Value (CLTV) with a FICO score of 720 or higher. For investment properties and second homes, you're looking at up to 80% CLTV.

Here's what that means in real numbers: Say you own an investment property worth $500,000 with a $200,000 first mortgage still on it. You could potentially unlock up to $200,000 in additional capital through a home equity loan (80% of $500,000 = $400,000 total debt capacity, minus your existing $200,000 mortgage). That's significant firepower for your next investment move.

Diverse Income Qualification Options

Here's where things get interesting for investors. Unlike traditional bank home equity loans that want to see W-2 income, today's home equity loan programs offer flexible qualification paths built specifically for real estate investors and self-employed borrowers like you:

DSCR (Debt Service Coverage Ratio) Qualification: For investment properties, you can qualify based on what the property earns—not what you earn personally. Lenders look at the property's gross rental income divided by PITIA (Principal, Interest, Taxes, Insurance, and Association dues), with a minimum DSCR of 1. 00x typically required. This means if your property generates $3,000 in monthly rent and has $2,700 in monthly PITIA, your DSCR is 1.11x, which qualifies you for the loan without needing to provide personal income documentation.

Bank Statement Qualification: Self-employed borrowers can qualify using 12 months of personal or business bank statements. Lenders analyze deposits to determine your income, making this a smart choice for investors who have strong cash flow but complex tax returns that might not reflect their true earning power.

1099 and P&L Statements: Independent contractors and business owners can use 1099 forms or profit and loss statements to demonstrate income, giving you more ways to show what you're really making beyond traditional W-2 documentation.

These flexible qualification paths open doors for investors who might hit roadblocks with conventional lenders, especially if you're strategically minimizing taxable income through depreciation and other savvy real estate tax strategies.

No Reserve Requirements

Many home equity loan programs require zero cash reserves beyond what's needed to close the transaction. This is a game-changer for real estate investors who want their capital working hard in income-generating assets rather than sitting on the sidelines in savings accounts.

Traditional mortgage products often require 3-6 months of reserves (enough liquid assets to cover your mortgage payments), which can lock up significant capital. By eliminating this requirement, home equity loans let you maximize your leverage and keep your money actively building wealth in your real estate portfolio.

Simplified Valuation Process Under $400,000

For loan amounts of $400,000 or less, many lenders accept an Automated Valuation Model (AVM) combined with a Property Condition Report instead of requiring a full interior appraisal. This streamlined approach delivers real benefits:

Cost Savings: Full appraisals typically run $400-$600 or more, while AVMs and property condition reports cost significantly less.

Time Efficiency: Traditional appraisals can take 2-4 weeks to schedule and complete, especially in competitive markets. AVMs can be generated within days, getting your loan across the finish line faster.

Less Intrusive: Property condition reports are exterior-only inspections, so you won't need to coordinate tenant access or disrupt occupancy for an interior appraisal.

The AVM gets the green light when the confidence score is high (≥90%) and the Forecast Standard Deviation (FSD) is low (≤0.13). This ensures you get accuracy without sacrificing speed.

Simplified Title Requirements

Here's another time-saver: for loans under $400,000, many programs accept an Owner and Encumbrance Property Report (O&E) instead of a full title insurance policy. This streamlined title product confirms ownership and flags any liens or encumbrances on the property—without the lengthy underwriting process of traditional title insurance.

The bottom line? Lower closing costs and faster processing, making it simpler and more affordable to tap into your home equity for your next investment move.

Unlimited Cash-in-Hand at Lower LTVs

Here's where things get exciting. If you maintain a CLTV of 65% or below, there's often no cap on your cash-out proceeds. This is a game-changer for investors sitting on substantial equity who want to pull out significant capital for portfolio growth or major projects.

Let's break it down: Say you own a property worth $1 million with a $200,000 first mortgage. You could potentially secure a home equity loan of up to $450,000 (bringing your CLTV to 65%) with no restrictions on your cash proceeds. For CLTVs above 65%, cash-out typically caps at $500,000—still plenty of firepower for most investment strategies.

Large Loan Potential

Home equity loans can unlock serious capital—often ranging from $50,000 to $500,000 or more, depending on your property value and equity position. This kind of borrowing power opens doors to significant real estate investment opportunities, such as:

- Acquiring additional rental properties

- Funding major renovations that boost property value

- Consolidating multiple high-interest debts to improve cash flow

- Building an accessory dwelling unit (ADU) to generate more rental income

- Making a down payment on a multifamily property

Access to large sums at fixed, competitive interest rates gives you powerful leverage to grow your portfolio strategically and efficiently.

Potential Tax Deductions

Here's some good news for your bottom line: interest paid on home equity loans may be tax-deductible if you use the funds to "buy, build, or substantially improve" the property securing the loan, according to IRS guidelines. For real estate investors like you, this can translate into meaningful tax advantages when using home equity loan proceeds for:

- Property renovations and improvements

- Major repairs that extend the property's useful life

- Adding square footage or additional units

- Purchasing the property itself

Keep in mind that tax laws are complex and evolve over time. The Tax Cuts and Jobs Act of 2017 changed the rules around home equity loan interest deductions, so we strongly recommend sitting down with a qualified tax professional who can help you understand how these deductions apply to your specific situation and investment goals.

Flexibility for Property Improvements and Portfolio Expansion

One of the biggest advantages of home equity loans? The flexibility to put your funds to work wherever they'll generate the best returns. Real estate investors commonly use home equity financing for property improvements, portfolio expansion, and strategic acquisitions—and you can do the same.

Property Improvements: Put those funds toward renovating your rental properties to boost their market value and rental income potential. Think kitchen and bathroom upgrades, adding bedrooms, or enhancing curb appeal—all moves that can increase your cash flow and long-term appreciation.

Portfolio Expansion: Use the equity in one property to make down payments on additional investment properties. This lets you grow your portfolio without draining your liquid savings.

Strategic Acquisitions: Need to move fast on a great deal? Home equity gives you quick access to capital for time-sensitive opportunities like off-market properties or distressed assets requiring cash offers.

Business Operations: Support your real estate business by funding property management upgrades, marketing efforts, or other operational expenses that help you run a tighter ship.

Unlike some financing products with restrictive use requirements, home equity loans provide a lump sum that you control, giving you the freedom to put your capital exactly where it will work hardest for your investment goals.

Occupancy Flexibility

Home equity loans are available for primary residences, second homes, and investment properties, so you have financing options no matter how you use your property. This flexibility is a real game-changer for real estate investors building a diverse portfolio, including:

- Your primary residence (which often qualifies for the highest LTV options)

- Vacation or second homes that you occasionally rent out

- Dedicated investment properties generating rental income

Bottom line? You can tap into equity from any property in your portfolio, not just your primary residence. That gives you multiple sources of capital as you grow your real estate holdings.

When you add it all up, these advantages make home equity loans a powerful tool in your financing toolkit. With predictable payments, competitive rates, high leverage, flexible qualification methods, and streamlined processes, you get efficient access to the capital you need to grow and optimize your investment portfolio.

Cons of Home Equity Loans

Home equity loans offer some compelling advantages for real estate investors, but let's be real—they also come with significant drawbacks and restrictions that you need to carefully weigh before moving forward. Understanding these limitations helps you make smart financing decisions that fit your investment strategy and risk tolerance.

Risk of Foreclosure

Here's the most serious consideration with a home equity loan: the risk of losing your property. Because the loan is secured by your home or investment property, falling behind on payments can lead to foreclosure. As lenders point out, "If you can't keep up with the home equity loan payments, the lender may foreclose on your property. "](https://www.chase.com/personal/mortgage/education/financing-a-home/second-mortgage-vs-home-equity-loan) This risk hits real estate investors especially hard. Think about it: vacancy periods, surprise repairs, or a dip in the rental market can all throw off your cash flow when you least expect it.

Here's what happens in a foreclosure: the first mortgage lender gets paid first from the property sale. Your home equity loan lender? They're second in line and only get paid after the primary mortgage is covered. Being in this subordinate position means you could lose everything you've put into the property—and still owe money if the sale doesn't cover both loans.

Another Monthly Payment to Manage

Let's be real: a home equity loan means one more fixed payment landing on your doorstep every month, right alongside your existing mortgage. This extra debt can squeeze your cash flow, especially when rental income dips or unexpected costs pop up across your properties.

If you're juggling multiple investment properties, these additional payments add up fast. That can limit your flexibility to jump on new opportunities or handle emergencies. And unlike some revolving credit options, you can't dial back your payments during slower months—they stay fixed no matter what.

You'll Need Solid Credit

Getting a home equity loan on an investment property means meeting some pretty strict credit standards. Most lenders want to see a FICO score of at least 660 to 680, and if your loan-to-value ratio is higher, you might need a 700 or above. Scores below 660? That's usually a dealbreaker for second lien financing.

Your mortgage payment history matters too—a lot. Lenders typically require a perfect record: zero late payments in the past 12 months (0x30x12). Even one late payment in the last year can knock you out of the running, no matter how strong the rest of your credit looks.

Debt-to-Income Ratio Cap

Here's something important to know: your debt-to-income (DTI) ratio is capped at 50% for income-based qualification on home equity loans. If you're a real estate investor juggling multiple mortgage payments, this can feel like a tight squeeze. The math is straightforward—all your monthly debt payments divided by your gross monthly income. The catch? Even if your rental properties are generating solid cash flow, those debt obligations on paper might still hold you back from qualifying.

![**Task**: Create a warning-style infographic highlighting the key risks and restrictions of home equity loans for real estate investors, designed to grab attention while maintaining professionalism.

**Visual Structure**: A vertical layout with a bold header, followed by six risk categories arranged in a grid format with warning icons, and a bottom cautionary note.

**ASCII Layout Reference**:

```

+---------------------------------------------------------------+

| ⚠ CRITICAL CONSIDERATIONS BEFORE BORROWING ⚠ |

+---------------------------------------------------------------+

| |

| [!] Foreclosure Risk [!] Credit Requirements |

| Property serves as FICO 660-680 minimum |

| collateral - payment 0x30x12 payment history |

| default = potential loss Higher scores for leverage |

| |

| [!] Additional Payment [!] DTI Cap at 50% |

| Fixed monthly obligation All debts count |

| No flexibility in Rental income may not |

| slower periods offset on paper |

| |

| [!] Closing Costs [!] Prepayment Penalties |

| 2-5% of loan amount 1-5 years on investment |

| Origination, appraisal, properties |

| title fees apply Limits exit strategy |

| |

+---------------------------------------------------------------+

| RECOMMENDATION: Maintain 6-12 months cash reserves |

| despite no formal requirement to protect against |

| rental income disruptions and market volatility. |

+---------------------------------------------------------------+

```

**Image Section Breakdown**:

- Header: Warning triangle icons (⚠) in vivid red (#ED072A) on both sides of](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771979823320_wjnwfm.jpg?alt=media&token=81df5993-3ea0-409f-aaeb-246dd3279b3d)

Upfront Costs and Closing Fees

Let's talk dollars and cents. Home equity loans come with upfront costs that chip away at your net proceeds. Here's what you're typically looking at:

- Origination fees: Usually 1-2% of the loan amount

- Appraisal fees: $400-$800 for a full appraisal (good news—loans under $400,000 may qualify for simplified AVM valuations)

- Credit report fees: $50-$100

- Title fees: Anywhere from a few hundred to over $1,000 for full title insurance (simplified O&E reports may be available for loans under $400,000)

- Recording fees and transfer taxes: These vary by jurisdiction

These expenses can stack up to several thousand dollars, so factor them into your ROI calculations. And those "no closing cost" options? They usually mean higher interest rates—which costs you more over the life of the loan.

Longer Closing Periods Than DSCR Loans

If you've worked with DSCR (Debt Service Coverage Ratio) loans before, you know they can move fast. Home equity loans? Not so much. The extra steps—subordinate lien positioning, title work, coordinating with your first mortgage holder—all add time to the process.

What does this mean for you? When a great investment opportunity pops up or you need funds quickly for a property issue, that 30-45+ day closing period can feel painfully slow. If you're used to the speed of cash deals or bridge financing, this timeline requires some patience and planning ahead.

No Interest-Only Payment Options

Here's something to keep in mind: unlike some investment property financing products, standard home equity loans typically don't offer interest-only payment options. These are fully amortizing loans with terms of 10, 15, 20, or 30 years, meaning every payment includes both principal and interest.

If you're a real estate investor who likes to maximize cash flow by keeping monthly payments low, this could be a sticking point. Interest-only payments are generally reserved only for "Elite" borrowers on primary residences with credit scores above 700, putting them out of reach for most investment property scenarios.

Prepayment Penalties on Investment Properties

Investment property home equity loans often come with prepayment penalties ranging from one to five years, depending on state law. Simply put, "you pay a fee if you pay off the loan early," which can put a real dent in your exit strategy flexibility.

Planning to refinance, sell the property, or pay off the loan ahead of schedule? These are common moves for active real estate investors, and these penalties can cost you thousands of dollars. The good news is the penalty structure typically decreases over time (e.g., 5% in year one, 4% in year two, etc.), but it's still a meaningful constraint on your financial flexibility worth factoring into your plans.

First Lien Restrictions

Here's an important rule to know: you cannot obtain a home equity loan if your existing first mortgage has certain "risky" features. Your loan application will be denied if the first lien:

- Is a private mortgage (hard money loan) opened within the last 12 months

- Has negative amortization features

- Has a balloon payment due during the amortization period of the new second lien

- Is a reverse mortgage

These restrictions can throw a wrench in your plans if you frequently use creative financing strategies or bridge loans. If you recently used private money to acquire a property, you'll need to wait at least 12 months before you can tap into equity through a traditional home equity loan.

Rural Property and Acreage Limitations

Here's something many investors don't realize: rural properties typically don't qualify for most home equity loan programs. There's also an acreage cap to keep in mind—usually no more than 2 acres for eligible properties. If you own property in a less populated area or have a larger lot, this could throw a wrench in your financing plans.

Properties that fall under USDA rural classifications or sit outside metropolitan statistical areas often face limited or zero financing options. That means you might need to explore alternative funding routes or be prepared for lower loan-to-value ratios. Check here to see if your property is rural.

Recently Listed Property Ineligibility

Here's a rule that catches many investors off guard: if your property was on the market within six months of applying for a home equity loan, you won't qualify. This "listing lockout" exists because lenders want to see that you're committed to holding the property long-term—not using the loan as a quick cash grab before selling.

If you've recently tested the waters or pivoted your investment strategy, this six-month waiting period could put your capital access on hold. You may need to look at other financing options in the meantime.

Flood Insurance Escrow Requirements

Even if you prefer handling your own property taxes and hazard insurance payments, flood insurance plays by different rules. When your property sits in a flood zone and your primary mortgage doesn't escrow for flood coverage, you'll need to set up a flood insurance escrow account for your second lien.

This can catch you off guard with extra monthly costs and added complexity—especially if you've deliberately avoided escrow accounts to keep direct control over your insurance and tax payments.

Solar Panel and PACE Lien Issues

Got solar panels with UCC filings or liens attached—like HERO or PACE financing? Your property won't qualify for a home equity loan unless those liens get paid off or formally subordinated to your new loan. Here's the catch: solar financing companies rarely agree to take a back seat. That means many properties with financed solar systems simply won't make the cut.

This restriction has become increasingly problematic as solar installations have grown more common on investment properties. You may need to pay off solar financing entirely before accessing home equity, which can require significant upfront capital.

ADU Rental Income Cannot Be Used

If your property includes an Accessory Dwelling Unit (ADU) that generates rental income, here's something important to know: that income cannot be used for qualification purposes on a home equity loan. This limitation can significantly reduce your qualifying income, particularly in markets where ADUs represent a substantial portion of a property's income potential.

For investors who have added ADUs specifically to increase property cash flow and value, this restriction means the additional income won't help you qualify for larger loan amounts, despite your property's improved financial performance.

Impact on Credit Score and Future Borrowing Capacity

Taking on a home equity loan will impact your credit score in several ways. The hard inquiry during application will cause a temporary dip, and the new debt will increase your credit utilization ratio and overall debt load. The good news? Responsible payment behavior will ultimately benefit your credit. Just keep in mind that the initial impact can affect your ability to obtain other financing in the short term.

Additionally, the loan will appear on your credit report and be factored into debt-to-income calculations for future financing. This could potentially limit your ability to acquire additional investment properties or access other credit products until you've paid down the balance or increased your income.

Business Purpose Affidavit Requirements

For investment properties, you'll need to sign an affidavit stating the loan is for business purposes. This requirement comes with restrictions—cash-out proceeds generally cannot be used for personal consumer debt consolidation if you're qualifying under investor guidelines.

In practical terms, this means you cannot use the funds to pay off personal credit cards, auto loans, or other consumer debts while maintaining the business purpose classification. Violating this restriction could jeopardize the loan's business purpose status and potentially affect its tax treatment and regulatory classification.

When is a Home Equity Loan a Good Fit for Real Estate Investors?

Home equity loans on investment properties can be powerful tools in your real estate toolkit when you use them strategically. Knowing when this financing option makes sense—and having a solid exit strategy—helps you maximize returns while keeping risk in check.

![**Task**: Create an illustrative conceptual image showing a real estate investor reviewing financial documents with a calculator, property photos, and renovation plans spread across a desk, representing strategic planning for using home equity loans.

**Visual Structure**: A professional desk scene photographed from above (bird's eye view) showing organized financial planning materials, with deep teal and vivid red accents incorporated into the scene through folders, charts, and highlighting.

**ASCII Layout Reference**:

```

+---------------------------------------------------------------+

| [DESK SURFACE - TOP VIEW] |

| |

| [Property Photo 1] [Calculator] [Property Photo 2] |

| |

| [Renovation Plans [Financial [Laptop showing |

| with red markup] Documents] property data] |

| |

| [Coffee Cup] [Pen & Notes] [Folder labeled |

|](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771981056641_kd843e.jpg?alt=media&token=e8e6434a-c0ef-4a58-b1e9-d17f21624494)

Optimal Scenarios for Using Home Equity Loans

Funding Major Property Renovations to Increase Rental Income

One of the smartest uses for a home equity loan is financing substantial property improvements that directly boost your rental income. Real estate investors often tap into equity to fund new opportunities, leveraging the value in current properties to generate capital. Whether you're adding an extra bedroom, updating kitchens and bathrooms, or opening up living spaces, these renovations can justify higher rents and attract quality tenants.

The fixed interest rate and predictable monthly payments of a home equity loan make it straightforward to calculate your return on investment. For example, if a $50,000 renovation lets you increase monthly rent by $500, you can figure out exactly how long it will take to recoup your investment while covering the loan payment. That kind of clarity is invaluable when you're planning your portfolio's growth.

Purchasing Additional Investment Properties

Using equity from one property to acquire another is a tried-and-true wealth-building strategy among real estate investors. A home equity loan gives you the lump sum you need for down payments on new investment properties, letting you expand your portfolio without draining your cash reserves. This approach works especially well when you've spotted a strong acquisition opportunity but don't want to sell other investments or wait to save up.

With OfferMarket's home equity loans offering up to 80% CLTV on investment properties, you can tap into significant capital while keeping ownership of your existing asset. This approach lets you control more real estate with less of your own money, potentially boosting returns across your entire portfolio.

Upgrading Essential Systems

Major system replacements—HVAC units, roofing, electrical panels, plumbing infrastructure—are big-ticket items, but they're essential for protecting property value and keeping tenants happy. These upgrades won't make headlines, but they're the backbone of steady cash flow and help you sidestep costly emergency repairs that can throw your budget off track.

A home equity loan works well for these capital expenses because the fixed payment structure lets you spread the cost over many years, aligning with how long the equipment will actually last. Instead of draining your emergency fund or racking up high-interest credit card debt, you can finance these improvements at competitive rates and keep cash on hand for your next opportunity.

Consolidating High-Interest Business Debt

If you're juggling multiple high-interest obligations—hard money loans, business credit cards, or personal loans used for real estate purposes—a home equity loan can offer real debt consolidation advantages. Swapping out variable, high-rate debt for a fixed-rate home equity loan can lower your overall interest costs and streamline your finances into one manageable monthly payment.

One important note: for investment properties that qualify under OfferMarket's investor guidelines, you'll need to sign a business purpose affidavit, and cash-out proceeds typically can't go toward personal consumer debt consolidation. This consolidation strategy shines brightest when you're replacing other business-purpose debt tied to your real estate activities.

Portfolio Diversification

[Using home equity to buy a second home or investment property can be a smart, strategic way to build wealth through real estate](https://www. firstsavingsmortgage.com/mortgage-blog/how-to-use-your-home-equity-to-buy-a-second-home-or-investment-property/). Tapping into the equity you've already built lets you spread your investments across different markets, property types, or strategies—all without selling what you already own. This kind of diversification can help lower your overall risk while boosting your returns.

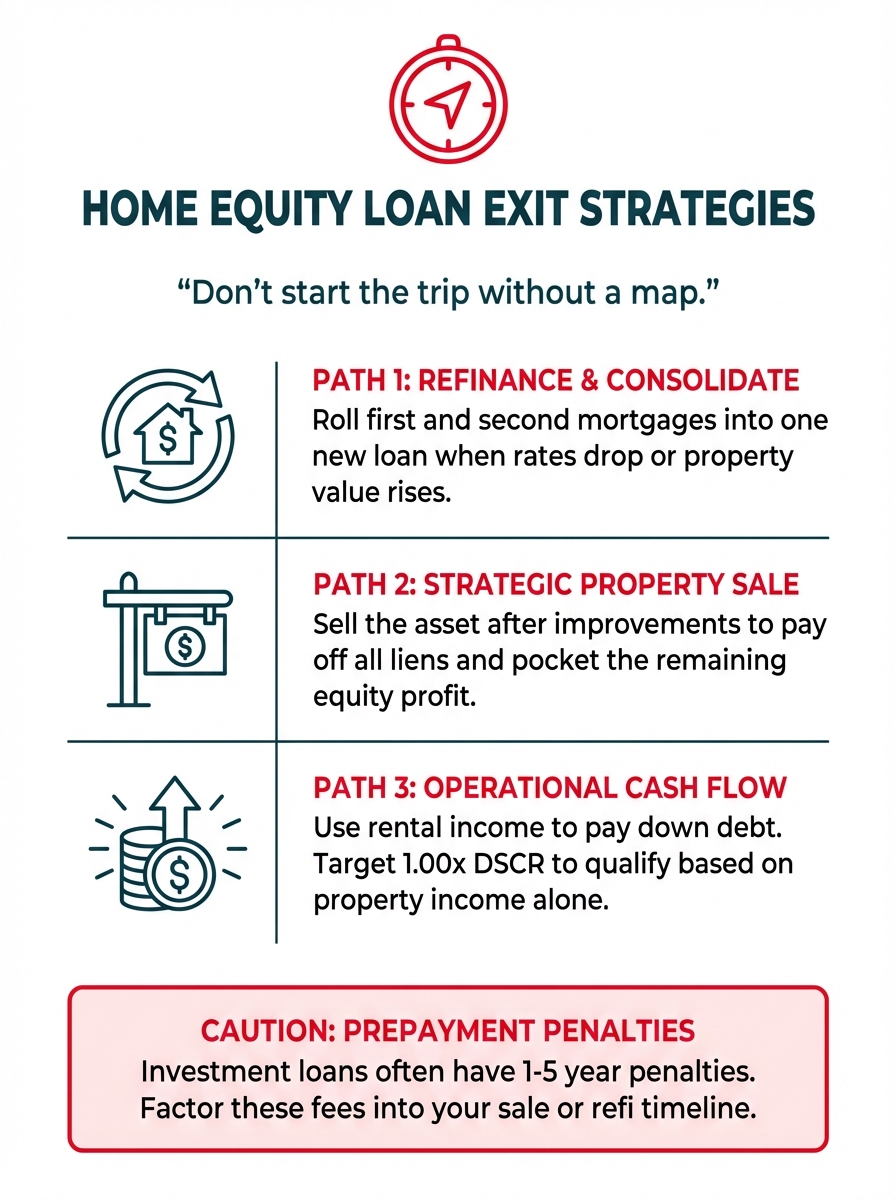

The Importance of Clear Repayment Plans and Exit Strategies

Taking on a home equity loan without a solid repayment plan is like setting out on a road trip without GPS—you might get there eventually, but expect some wrong turns and unnecessary stress along the way. Smart investors always have multiple exit strategies mapped out before signing on the dotted line.

Refinancing as an Exit Strategy

As your property gains value and you build more equity, rolling both your first and second mortgages into a single new loan can be a smart move. This works especially well when interest rates drop or when you've boosted your property's worth through upgrades. Refinancing can wipe out that second payment altogether, potentially cutting your monthly costs while giving you fresh loan terms to work with.

Property Sale

Selling is the most straightforward way to close out a home equity loan. When the market's hot or you've squeezed all the value you can from a property, a sale lets you pay off both loans and pocket your profits. This strategy really shines when you've used your loan funds for improvements that significantly bumped up what the property is worth.

Cash-Out from Operations

For many investors, the sweet spot is generating enough rental income to chip away at—or completely pay off—the home equity loan over time. This approach takes careful planning and realistic expectations about what you'll actually collect in rent, how often units might sit empty, and what it costs to keep things running. By building the loan payment into your property's pro forma, you can keep your investment cash-flow positive while chipping away at that debt over time.

For investment properties, OfferMarket's DSCR qualification option is a game-changer here. If your property brings in solid rental income with a Debt Service Coverage Ratio of at least 1.00x (meaning gross rents cover PITIA), you can qualify based on the property's cash flow alone—no personal income documentation needed. This approach fits hand-in-glove with a cash-flow-focused exit strategy.

Prepayment Considerations

Here's something important to keep in mind: investment property home equity loans often come with prepayment penalties lasting one to five years, depending on state law. So if you pay off the loan early—through refinancing, selling the property, or saving up cash—you might face a penalty fee. Build this into your exit strategy planning, and weigh whether paying off early is worth the extra cost.

Strategic Timing: Keeping Loans Under $400,000

Here's where OfferMarket really shines: loans under $400,000 come with a streamlined process that can save you time and money. Stay below this threshold, and you can often skip the full interior appraisal. Instead, we use an Automated Valuation Model (AVM) paired with a Property Condition Report—as long as the confidence score hits 90% or higher and the FSD stays at 0.13 or below.

What's more, loans under $400,000 may qualify for a simplified Owner and Encumbrance (O&E) Report instead of full title insurance. The bottom line? Faster closings and lower costs, so you can jump on time-sensitive deals without the usual financing delays.

If you're an investor who needs to move fast on renovations or acquisitions, keeping your financing under $400,000 gives you a real edge. Need more capital? Think about whether splitting financing across multiple properties or phasing your project could let you take advantage of this faster track.

DSCR Qualification: Leveraging Cash-Flowing Properties

If you've got a property that's pulling its weight in rental income, OfferMarket's DSCR qualification option could be your ticket to smarter financing. Here's the deal: instead of digging through your personal income documents like traditional lenders do, we focus on one thing—can your property cover its own debt?

To qualify using DSCR, your rental income needs to cover your total housing expenses (that's Principal, Interest, Taxes, Insurance, and Association fees) at a minimum ratio of 1.00x. In plain terms? If your monthly PITIA runs $2,000, your gross monthly rents need to hit at least $2,000. And here's a bonus: stronger DSCR ratios can open doors to better loan terms or higher loan-to-value ratios.

This approach is a real win if you're self-employed, have a complicated tax situation, or your W-2 doesn't tell the full story of your financial strength. Even better—you can qualify based on projected income for a property you're upgrading, using market rent schedules instead of what it's currently bringing in.

How OfferMarket Helps You Make Strategic Decisions

Here's where OfferMarket stands apart. We're not just a lender—we're a full-service real estate platform that brings together lending, marketplace insights, and insurance services. That means you get the complete picture of your financing options, not just a yes or no on your application. Our team partners with you to structure financing that fits your investment strategy and exit plan.

Wondering about the ROI on a big renovation? Trying to figure out the sweet spot for your loan amount to stay under that $400,000 threshold for faster processing? Not sure if DSCR qualification is right for you? We've got your back. Our instant quote feature lets you run different scenarios in minutes—compare loan amounts, terms, and payment structures to find what works best for your goals.

Because we understand property values, rental markets, and insurance costs across your portfolio, we offer guidance that cookie-cutter lenders simply can't provide.

This integrated approach ensures your home equity loan works as a strategic tool for portfolio growth—not just another debt on your books.

Home Equity Loan vs. HELOC: Understanding Your Second Mortgage Options

Choosing between a home equity loan (HELOAN) and a home equity line of credit (HELOC) is a big decision for real estate investors and landlords. The right choice can make a real difference in how you manage cash flow and grow your portfolio. Both options let you tap into your property's equity, but they work in very different ways—each with its own advantages and trade-offs worth understanding.

Interest Rate Structure: Fixed vs. Variable

Here's the biggest difference between these two products: how interest rates work. Home equity loans come with fixed interest rates that stay the same for the entire loan term, typically 10 to 30 years. Your monthly payment stays predictable, which makes budgeting and cash flow planning much easier—especially when you're juggling multiple rental properties.

HELOCs, on the other hand, almost always have variable interest rates tied to a benchmark like the prime rate. When the Federal Reserve moves rates up or down, your HELOC rate—and your monthly payment—moves with it. For investors, this can make financial planning tricky. Recent market trends show that HELOCs feel the impact of rate changes almost immediately, so they're especially sensitive to shifts in monetary policy.

Payment Structure: Lump Sum vs. Revolving Credit

With a home equity loan, you get a single lump sum at closing. The full amount lands in your account right away, and you start making fixed monthly payments that cover both principal and interest. This setup is ideal when you have a specific, one-time need—like funding a down payment on your next investment property, tackling a full renovation, or replacing major systems like an HVAC unit.

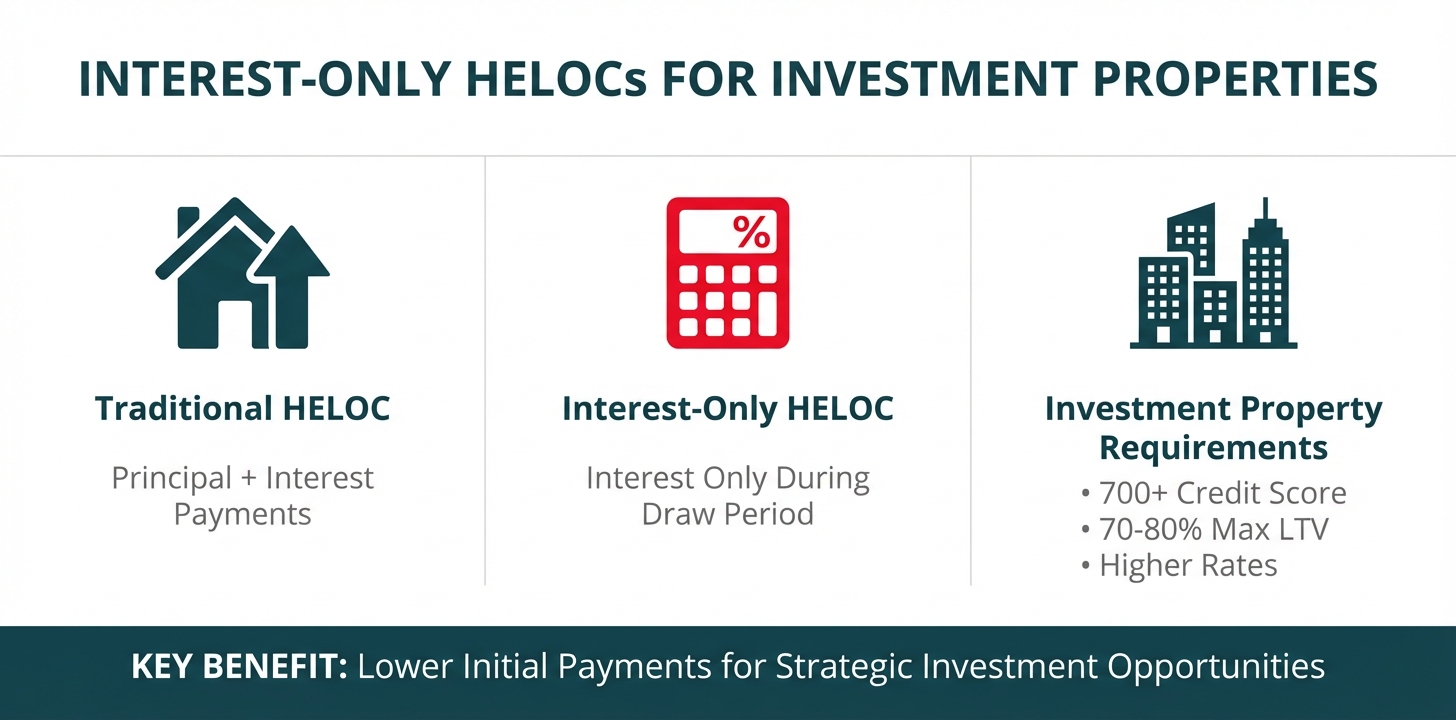

HELOCs work a lot like a credit card that's backed by your property. You get approved for a maximum credit limit, but you only borrow what you need, when you need it, during the draw period (typically 5-10 years). You can borrow, pay it back, and borrow again—all up to your limit. During the draw period, most HELOCs only require interest payments, though you're free to chip away at the principal if you'd like. Once the draw period wraps up, the repayment period kicks in (typically 10-20 years), where you can no longer access funds and must pay back both principal and interest.

Flexibility in Accessing Funds

HELOCs shine when it comes to short-term flexibility for investors who need ready access to capital. If you're actively flipping houses, handling surprise repairs across several properties, or jumping on deals as they pop up, a HELOC's revolving credit gives you a financial safety net—no need to apply for a new loan every time.

But here's the thing: this flexibility demands discipline. It's easy to keep dipping into that available credit, which can lead to overleveraging—a real risk in real estate, where market dips can eat into your equity fast. Plus, lenders can freeze or slash your HELOC limit if property values drop or your finances shift, potentially cutting off your funds right when you need them most.

Home equity loans may not offer the same ease of accessing more funds, but they deliver certainty and structure. You know exactly what you're borrowing, what your monthly payment looks like, and when you'll be debt-free. For investors with a clear plan for growing or improving their portfolio, that predictability often beats the convenience of revolving credit.

Repayment Terms and Schedules

Home equity loans come with simple, fully amortizing repayment schedules. From your very first payment, you're knocking down principal while covering interest. You'll get a clear amortization schedule that shows exactly how much equity you're rebuilding each month and when you'll own your property outright.

HELOC repayment works differently than a standard loan and happens in two separate phases:

Draw Period (typically 5-10 years): You can borrow funds up to your credit limit and usually make interest-only payments, though paying down principal is allowed and smart to do when possible.

Repayment Period (typically 10-20 years): The line closes to new borrowing, and you start repaying the outstanding balance through principal and interest payments.

Here's the catch: this two-phase structure can create payment shock if you're not prepared. An investor who has been making $300/month interest-only payments during the draw period might suddenly face $1,200/month principal-and-interest payments when the repayment period kicks in—a cash flow hit that could squeeze your rental income margins tight.

![**Task**: Create a comprehensive comparison chart showing Home Equity Loan (HELOAN) versus Home Equity Line of Credit (HELOC) with key features, benefits, and drawbacks for real estate investors.

**Visual Structure**: A side-by-side comparison table with a header, two main columns (HELOAN and HELOC), and rows for different comparison categories with icons.

**ASCII Layout Reference**:

```

+---------------------------------------------------------------+

| HOME EQUITY LOAN vs HELOC COMPARISON |

+---------------------------------------------------------------+

| FEATURE | HELOAN | HELOC |

+-------------------+----------------------+--------------------+

| [Icon] Interest | Fixed Rate | Variable Rate |

| Rate | Predictable | Fluctuates |

+-------------------+----------------------+--------------------+

| [Icon] Fund | Lump Sum | Revolving Credit |

| Access | At Closing | Draw as Needed |

+-------------------+----------------------+--------------------+

| [Icon] Payment | Fixed P&I | Interest-Only |

| Structure | From Day 1 | Then P&I |

+-------------------+----------------------+--------------------+

| [Icon] Payment | Fully Predictable | Can Increase |

| Predictability | ✓ Stable | ⚠ Variable |

+-------------------+----------------------+--------------------+

| [Icon] Best For | Specific Projects | Ongoing Needs |

| | One-Time Capital | Flexible Access |

+-------------------+----------------------+--------------------+

| [Icon] Risk | Lower | Higher |

| Level | No Rate Risk | Rate Exposure |

+-------------------+----------------------+--------------------+

| |

| INVESTOR RECOMMENDATION: |

| HELOANs provide superior stability for portfolio planning |

| and long-term investment strategies with predictable DSCR. |

+---------------------------------------------------------------+

```

**Image Section Breakdown**:

- Header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771981230249_sewkqk.jpg?alt=media&token=b424efec-b3a8-4cbc-a48b-00ac988e18a0)

Risk Factors: Rate Fluctuations and Market Volatility

Because HELOCs come with variable rates, you're taking on interest rate risk that fixed-rate home equity loans simply don't have. Picture a real estate investor who opened a HELOC when rates were at historic lows. As rates climbed, their monthly payment could have doubled or even tripled, eating directly into the cash flow from their rental properties.

If you're a landlord running on tight margins—where rental income needs to cover mortgage payments, property taxes, insurance, maintenance, and still leave you with positive cash flow—unpredictable payment increases can quickly turn a profitable property into a money pit.

Fixed-rate home equity loans take this guesswork off the table. Whether interest rates rise or fall, your payment stays the same, making it easier to forecast returns and keep stable debt service coverage ratios across your portfolio.

Market Trends: Issuance Volume and Investor Preferences

Recent market data shows some interesting patterns in how investors are choosing between these products. Total originations of HELOCs and home equity loans increased by 7.2% in 2024, reflecting growing investor interest in tapping home equity as property values have climbed significantly.

HELOCs have historically dominated the home equity market, with approximately 40% of mortgage consumers maintaining a HELOC in 2025. However, home equity loans are gaining traction among real estate investors who prioritize payment stability and structured debt management over revolving credit flexibility.

Here's what we're seeing in the market: retail homeowners tend to gravitate toward HELOCs for their flexibility—think home improvements, education costs, or managing life's curveballs. Real estate investors and landlords, on the other hand, are increasingly choosing fixed-rate home equity loans when making strategic portfolio moves—whether that's acquiring another property, funding value-add renovations, or consolidating higher-interest investment debt.

Comparison Table: HELOAN vs. HELOC for Real Estate Investors

| Feature | Home Equity Loan (HELOAN) | Home Equity Line of Credit (HELOC) |

|---|---|---|

| Interest Rate | Fixed for entire term | Variable, adjusts with market rates |

| Rate Predictability | Complete certainty | Uncertain; subject to rate fluctuations |

| Fund Disbursement | Lump sum at closing | Draw as needed up to credit limit |

| Payment Structure | Fixed monthly principal + interest | Interest-only during draw period, then P&I |

| Payment Predictability | Highly predictable | Variable; can increase significantly |

| Access to Additional Funds | None without new loan | Ongoing during draw period |

| Repayment Period | Begins immediately | Begins after draw period ends |

| Typical Term | 10-30 years (fully amortizing) | 5-10 year draw + 10-20 year repayment |

| Best For Investors | Specific, planned capital needs | Ongoing, flexible funding requirements |

| Cash Flow Impact | Consistent, predictable | Variable; potential for payment shock |

| Risk Profile | Lower; no rate risk | Higher; rate and payment uncertainty |

| Portfolio Planning | Easier to model and forecast | Requires conservative assumptions |

| Closing Costs | Typically higher upfront | Often lower or waived |

| Prepayment Penalties | May apply (especially investment properties) | Less common |

| Credit Limit Changes | Not applicable | Lender can reduce or freeze line |

Why Fixed-Rate HELOANs Make Sense for Portfolio Growth

If you're serious about building and managing a rental property portfolio, here's the bottom line: fixed-rate home equity loans give you the structured, predictable financing you need to plan with confidence and execute your long-term investment strategy. Here's why:

Debt Service Coverage Ratio (DSCR) Stability: When you're qualifying for additional investment property financing using DSCR methodology, lenders look at whether your rental income can cover your debt payments. Fixed HELOAN payments make this math clean and predictable, while variable HELOC payments create uncertainty that could trip you up when you're ready to acquire your next property.

Proforma Accuracy: Smart investment decisions start with solid financial projections. With fixed payments, you can build reliable proformas that show exactly how a property improvement will boost your net operating income and cash-on-cash returns—no need to pad your numbers with rate increase buffers.

Refinancing Strategy: As a savvy investor, you're probably already thinking about your exit strategy—refinancing when rates drop or your property value climbs. A fixed-rate HELOAN gives you a known payoff amount to work with, while HELOC balances that shift with draws and payments can muddy your refinancing plans.

Portfolio Stress Testing: Smart investors prepare for the unexpected—vacancies, surprise repairs, market dips. Fixed HELOAN payments stay constant in your stress-test models, while variable HELOC payments force you to run multiple scenarios, adding complexity when you need clarity.

OfferMarket's Fixed-Rate HELOANs for Investment Properties

OfferMarket is built for real estate investors and landlords who want fixed-rate home equity loans that work as hard as they do. Instead of exposing your portfolio to the ups and downs of rate volatility with a traditional HELOC, OfferMarket's HELOAN products give you:

- Predictable fixed rates so you can forecast cash flow across your entire portfolio with confidence

- Alternative qualification methods including DSCR (based purely on property cash flow) and bank statement programs perfect for self-employed investors

- High leverage options up to 90% CLTV on primary residences and 80% CLTV on investment properties

- Streamlined processes with AVM valuations and simplified title work for loans under $400,000, saving you time and money at closing

If you want the peace of mind that comes from knowing exactly what you'll pay each month—regardless of where interest rates head—OfferMarket's fixed-rate home equity loans deliver the stability your portfolio deserves.

Why Fixed-Rate HELOANs Give You an Edge

If you're a real estate investor who values predictable payments and structured financing, a fixed-rate HELOAN is often a smarter choice than revolving or variable-rate options. When you're juggling multiple properties, mapping out long-term renovations, or executing a specific investment play, knowing your exact monthly payment for the entire loan term takes a major unknown off your plate.

This predictability really pays off when interest rates are climbing. While HELOC borrowers see their payments tick up with every Federal Reserve rate hike, you'll keep the same payment no matter what the market does. For investors building portfolios with calculated risk in mind, that stability can mean the difference between steady growth and stretching yourself too thin.

Here's another way to look at it: the lump-sum structure of a home equity loan—sometimes seen as a drawback—can actually work in your favor. When you receive a set amount of capital, you're naturally pushed to plan how you'll use it rather than pulling funds bit by bit without a clear game plan. This encourages smarter capital allocation and sharper project planning.

Bottom Line: If you need ongoing, flexible access to smaller amounts of capital and can handle payment swings, a HELOC might work for you. But if you're executing a specific strategy—buying another property, tackling a major renovation, or consolidating higher-interest debt—a fixed-rate home equity loan through an investor-focused lender like OfferMarket typically delivers better stability, predictability, and alignment with how professional real estate investors actually operate.

Real-World Success: How OfferMarket Helped a Landlord Expand Their Portfolio

Let's look at Marcus, a real estate investor in Atlanta with three single-family rentals under his belt. He spotted a great opportunity—a fourth property that was undervalued due to cosmetic issues but sat in an appreciating neighborhood with solid rental potential. The purchase price? $185,000. His renovation budget to get it market-ready? About $25,000.

Marcus had approximately $150,000 in equity across his existing properties but didn't want to deal with the drawn-out process of a traditional bank refinance or HELOC application. He also wanted to keep his cash reserves intact for ongoing property management needs and potential vacancies.

Using OfferMarket's platform, Marcus received an instant quote for a home equity loan on his primary residence within minutes. Because his loan amount was under $400,000, he qualified for the simplified valuation process using an AVM and Property Condition Report, skipping the typical 2-3 week wait for an appraiser. He completed the entire loan file online, uploading his documentation through OfferMarket's secure portal during his lunch breaks over two days.

Marcus chose to qualify using the DSCR program on one of his investment properties instead of providing personal tax returns, which made his paperwork much lighter. With a DSCR of 1.15x on the property (the rental income comfortably covered the monthly mortgage payment, taxes, insurance, and association fees), he locked in a $60,000 home equity loan at a competitive fixed rate.

The completely digital closing process meant Marcus never had to take time off work or juggle schedules with a notary. From initial quote to funded loan, the entire process wrapped up in just 18 days—roughly half the time of a traditional bank HELOAN. Marcus put the funds toward purchasing and renovating his fourth property, which he brought to market as a rental within six weeks. That property now brings in $1,850 in monthly rent against a $1,200 mortgage payment, adding solid positive cash flow to his portfolio.

Within 18 months, Marcus came back to OfferMarket for another home equity loan to fund his fifth acquisition. His reason? The speed, transparency, and investor-focused approach kept him coming back.

Why OfferMarket's Integrated Approach Matters

OfferMarket's combination of lending expertise with insights from its real estate marketplace and insurance services creates a feedback loop that works in your favor as an investor. The marketplace data helps OfferMarket understand current property values, rental rates, and market trends across different regions, which informs more accurate and competitive lending decisions. The insurance division's knowledge of risk factors and property conditions contributes to more realistic property valuations and risk assessments.

This integrated perspective allows OfferMarket to offer competitive pricing that reflects the actual risk profile of real estate investors, rather than applying generic consumer lending criteria. Because the platform truly understands rental property economics, underwriters can confidently approve DSCR loans and investment property financing that traditional lenders might pass on.

For landlords and real estate investors who value speed, transparency, and products built specifically for their needs, OfferMarket represents a smarter approach to real estate financing—one that recognizes investment properties deserve investment-focused solutions, not retrofitted consumer products. According to industry analysis, finding lenders that truly understand investment property financing remains a challenge for many landlords, making OfferMarket's specialized approach a real advantage in today's market.

Conclusion

Home equity loans are a powerful tool in your financing toolkit when you're ready to leverage property equity for portfolio growth and strategic improvements. Throughout this guide, we've walked through the compelling advantages and important considerations every investor should weigh before moving forward.

Key Benefits Recap

Here's what makes home equity loans attractive for investment properties:

Fixed Interest Rates and Predictable Payments: Unlike variable-rate products, home equity loans give you the stability of fixed interest rates with consistent monthly payments over 10, 15, 20, or 30-year terms. This predictability makes budgeting and cash flow management significantly easier for investors managing multiple properties.

Lower Interest Rates: Because your property backs the loan, home equity loans typically come with much lower interest rates than unsecured options like personal loans or credit cards. That difference can add up to thousands of dollars in savings over the life of your loan.

High Leverage Opportunities: With combined loan-to-value (CLTV) ratios reaching up to 90% for primary residences and 80% for investment properties, you can tap into significant capital while still holding onto meaningful equity in your properties.

Diverse Qualification Options: Today's home equity loan programs meet you where you are. Whether you qualify through DSCR-based approval (ideal for investors), bank statement programs (perfect for self-employed borrowers), or traditional documentation, there's likely a pathway that works for your situation—even if conventional banks have turned you away.

Strategic Flexibility: The lump-sum payout gives you immediate capital to make high-impact moves: renovate a property to boost rental income, secure a down payment on your next investment, or tackle essential upgrades that protect your property's value.

Critical Risks to Remember

Of course, every smart investor weighs the benefits against the risks:

Foreclosure Risk: Your property is on the line. If you can't make payments, you could lose your investment to foreclosure. That's why maintaining solid cash reserves and having a clear repayment plan isn't optional—it's essential.

Credit and Financial Requirements: Most programs look for minimum FICO scores of 660-680, a clean mortgage payment history (0x30x12), and debt-to-income ratios no higher than 50%. If your financial picture is complicated, these hurdles may require some planning to clear.

Closing Costs and Fees: Don't forget to factor in origination fees, appraisal costs, title fees, and credit report charges—they add up faster than you might expect. While loans under $400,000 may qualify for simplified valuation and title processes, it's smart to set aside 2-5% of your loan amount for closing costs—that way, there are no surprises at the finish line.

Prepayment Penalties: Here's something to keep on your radar: investment property loans often come with prepayment penalties lasting 1-5 years. This can affect your options if you decide to refinance or sell sooner than planned, so factor this into your strategy.

OfferMarket Loans

Check your rate

60 seconds · no credit pull