*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How to Get an LLC Loan for Investment Property (2026 Guide)

Securing a loan for an investment property under a Limited Liability Company (LLC) is a standard practice for savvy real estate investors. The best loan types for this purpose are commercial or private money loans specifically designed for business entities. The most common and effective options include DSCR loans for long-term rentals, hard money or bridge loans for short-term needs, fix and flip loans for renovation projects, portfolio loans for multiple properties, and ground up construction loans for new builds. These financial products are underwritten based on the property's investment potential and the strength of the personal guarantor, rather than the strict personal income requirements of conventional mortgages.

Lenders like OfferMarket specialize in these types of loans, offering a streamlined process tailored to real estate investors operating through an LLC. The key is to partner with a lender who understands the nuances of entity-based lending and can provide financing that aligns with your investment strategy, whether it's acquiring a cash-flowing rental or funding a quick flip.

Best Loan Types for an LLC Investment Property

When financing an investment property through an LLC, you move away from conventional residential mortgages and into the realm of commercial and private lending. These loans are specifically designed for business entities and are underwritten based on the property's performance and the investor's experience. Understanding the different types available is the first step to securing the right financing for your deal.

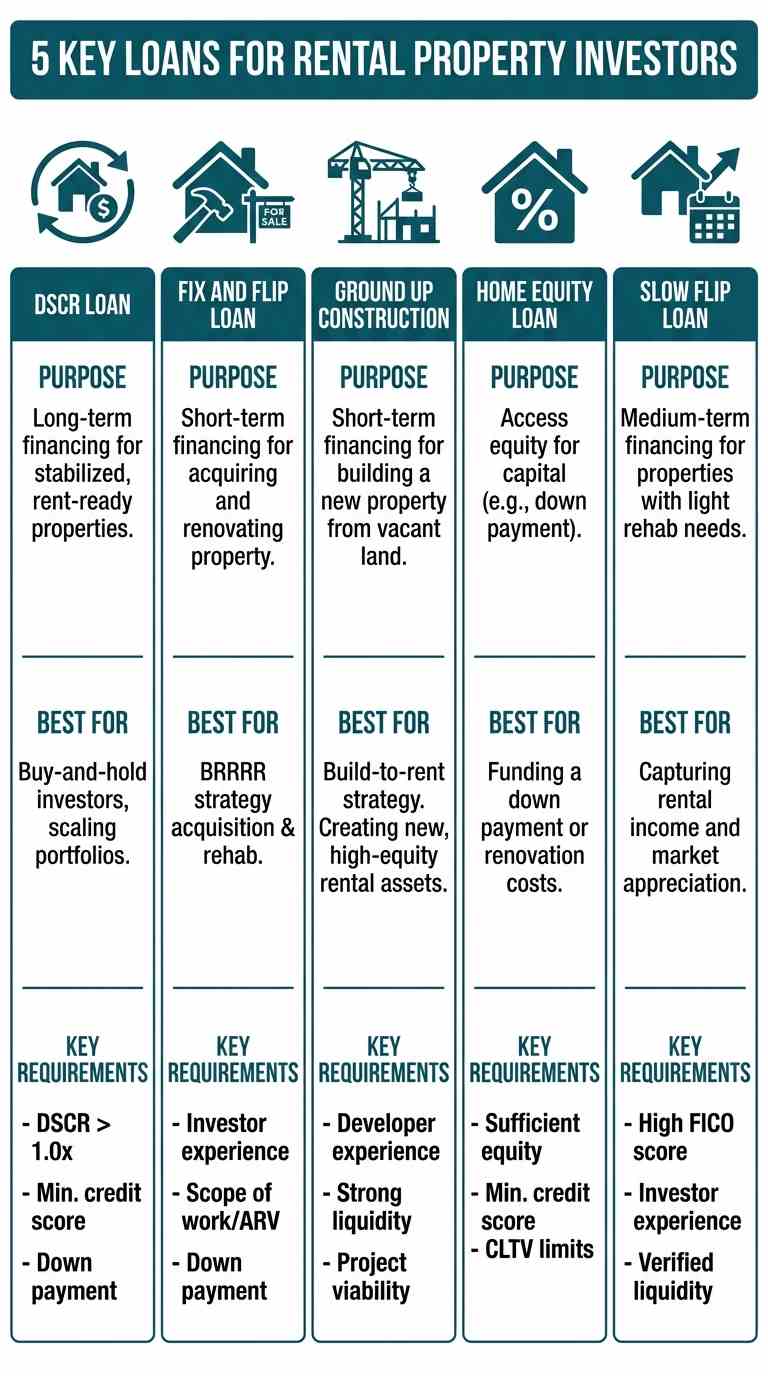

DSCR Loans for Cash-Flowing Rentals

A Debt Service Coverage Ratio (DSCR) loan is the go-to financing solution for acquiring or refinancing long-term rental properties held in an LLC. Unlike conventional loans that heavily scrutinize your personal debt-to-income ratio (DTI), a DSCR loan focuses on the property's ability to generate enough income to cover its mortgage payments and expenses.

The core of a DSCR loan is the ratio itself:

DSCR = Gross Rental Income / PITIA (Principal, Interest, Taxes, Insurance, and any Association fees)

- A DSCR of 1.25x is a common lender benchmark, meaning the property's income is 125% of its total housing expense.

- A ratio of 1.0x means the income exactly covers the expenses (breakeven).

- A ratio below 1.0x indicates negative cash flow.

Who it's for: Real estate investors (both new and experienced) who are purchasing or refinancing buy-and-hold rental properties that are either currently cash-flowing or have the clear potential to do so. It's ideal for those who want to scale their portfolio without their personal income being a limiting factor.

Key Features:

- No Personal Income Verification: Lenders typically do not require tax returns or W-2s.

- Unlimited Properties: Investors can use DSCR loans to finance a large number of properties, unlike conventional loans which have limits (typically 10).

- LLC-Centric: These loans are designed to be made directly to an LLC.

- Interest Rates: Rates are typically 1-3% higher than conventional mortgages but are competitive for investment properties.

Actionable Advice: Before applying, use a DSCR calculator to analyze your potential deal. Ensure your projected rental income, based on a professional appraisal's fair market rent analysis, will meet the lender's minimum DSCR requirement, which is usually between 1.10x and 1.25x.

Hard Money and Bridge Loans for Short-Term Financing

Hard money loans and bridge loans are short-term financing tools used by investors to acquire property quickly, fund renovations, or "bridge" the gap until long-term financing can be secured. They are offered by private lenders and are underwritten based almost entirely on the subject property's value, specifically its After Repair Value (ARV).

Who it's for: Investors who need to close a deal faster than a traditional lender can (e.g., in an auction or a competitive market), or investors buying a distressed property that wouldn't qualify for traditional financing. They are also used for value-add projects where the goal is to renovate, stabilize (get a tenant), and then refinance into a long-term DSCR loan—a strategy known as BRRRR (Buy, Rehab, Rent, Refinance, Repeat).

Key Features:

- Speed: Can often close in 10-21 days.

- Asset-Based: The loan is secured by the property itself; borrower credit is a secondary consideration.

- Flexible Underwriting: Fewer hoops to jump through compared to conventional or even DSCR loans.

- Higher Cost: Interest rates (often 9.75-12%) and origination points (1-2%) are significantly higher to compensate for the lender's increased risk and the short-term nature of the loan.

- Short Term: Typically have terms of 12 to 24 months with interest-only payments.

Actionable Advice: When using a hard money loan, your exit strategy is paramount. Before you even take the loan, you must have a clear and realistic plan for how you will pay it back, whether through selling the property or refinancing into a permanent loan.

Fix and Flip Loans for Renovation Projects

A fix and flip loan is a specific type of hard money loan tailored for investors who intend to purchase, renovate, and sell a property for a profit. The key feature of these loans is that they can finance both the purchase of the property and a significant portion (often 100%) of the renovation budget.

The loan amount is based on the ARV. For example, a lender might offer up to 75% of the ARV. If a property is purchased for $200,000, needs $50,000 in repairs, and has an ARV of $350,000, a lender might loan up to $262,500 (75% of $350k). This covers the entire purchase and renovation cost.

Who it's for: House flippers and real estate investors who specialize in value-add projects. It's designed for short-term holds where the primary goal is resale.

Key Features:

- Purchase + Rehab Funding: Covers both major costs of a flip.

- Draw Schedule: Renovation funds are not given as a lump sum. They are disbursed in "draws" after specific project milestones are completed and inspected.

- Interest-Only Payments: Borrowers only pay interest during the loan term, which keeps holding costs low.

- ARV-Based: Leverage is determined by the future value of the property, allowing investors to finance a larger portion of the total project cost.

Actionable Advice: Create a detailed Scope of Work (SOW) and budget before applying. Lenders will scrutinize your renovation plan and budget to ensure it's realistic and aligns with the projected ARV. Use a Fix and Flip Calculator to model your potential profit, costs, and timeline.

Portfolio Loans for Financing Multiple Properties

A portfolio loan is a single loan that covers multiple investment properties. Instead of having individual mortgages for each property in your LLC, you can consolidate them under one blanket mortgage. This is an excellent tool for experienced investors looking to scale and simplify their operations.

Who it's for: Established investors who own several (typically 5 or more) rental properties and want to streamline their debt, free up equity for new acquisitions, or simplify their bookkeeping.

Key Features:

- One Loan, One Payment: Simplifies debt management significantly.

- Cash-Out Refinancing: Investors can often pull equity out from their portfolio's combined value to fund new deals.

- Cross-Collateralization: All properties in the portfolio serve as collateral for the single loan.

- Customized Terms: Terms are often more negotiable than with single-asset loans.

Actionable Advice: To qualify, lenders will want to see a well-organized and profitable portfolio. Prepare a detailed schedule of real estate owned (SREO) that lists each property's address, value, current debt (if any), and rental income. Lenders will analyze the portfolio's aggregate DSCR.

Ground Up Construction Loans for New Builds

For investors looking to build an investment property from scratch—whether a single-family rental, a duplex, or a small multi-family building—a ground up construction loan is the necessary financing vehicle. These are short-term loans, similar to fix and flip loans, but for new construction.

The loan funds the land acquisition (if not already owned) and the entire construction budget. Like a rehab loan, funds are disbursed on a draw schedule as the project hits key milestones (e.g., foundation poured, framing complete, etc.).

Who it's for: Experienced investors, developers, and builders who are constructing new residential properties to be held as rentals or sold for a profit.

Key Features:

- Land and Construction Costs: Can cover a high percentage of the total project cost.

- Draw-Based Disbursement: Protects both the lender and the borrower by ensuring funds are used as intended and work is progressing.

- Interest-Only on Drawn Funds: You only pay interest on the portion of the loan that has been disbursed, which helps manage costs during the construction phase.

- Requires Experienced Team: Lenders will heavily vet the borrower's and the general contractor's experience and track record.

Actionable Advice: Your application package for a ground up loan is extensive. It must include architectural plans, a line-item budget (hard and soft costs), permits, and a detailed resume of your general contractor. The lender needs to be confident that your team can complete the project on time and on budget.

Get Your 2026 Term Sheet

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Can You Use a Conventional Loan for an LLC?

This is one of the most common questions from investors new to using an LLC. The short answer is generally no; you cannot originate a conventional loan (one backed by Fannie Mae or Freddie Mac) in the name of an LLC. However, the topic is nuanced, particularly when it comes to transferring a property into an LLC after closing.

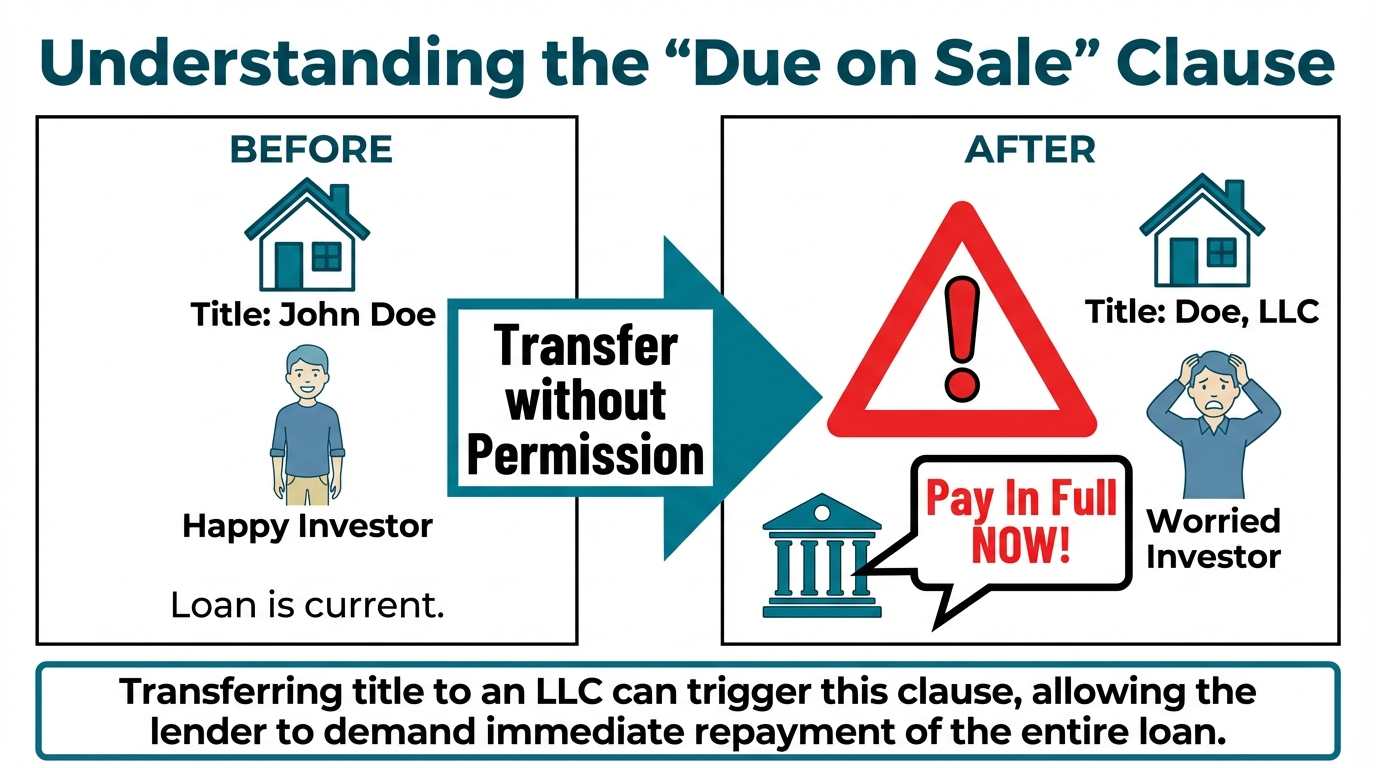

The "Due on Sale" Clause Explained

At the heart of this issue is the "due on sale" clause (or acceleration clause) found in virtually every conventional mortgage agreement. This clause gives the lender the right to demand full repayment of the loan balance if the property is sold or transferred without the lender's permission.

When you transfer the title of a property from your personal name to an LLC, you are technically changing the ownership. This action can trigger the due on sale clause. For many years, investors debated whether lenders would actually enforce this. In practice, as long as payments were being made, most lenders didn't bother. However, relying on a lender to not enforce a contractual right is a risky strategy.

Transferring Title vs. Originating the Loan in an LLC

There's a critical distinction between two scenarios:

Originating a Loan in an LLC: This involves applying for and closing on the loan with the LLC as the borrower from day one. Conventional lenders like major banks and credit unions will not do this for residential mortgages. Their underwriting systems are designed for individual borrowers, not business entities.

Transferring Title to an LLC Post-Closing: This involves securing a conventional loan in your personal name and then, after closing, transferring the title to your LLC via a quitclaim deed.

The second scenario was made slightly less risky by the Garn-St. Germain Depository Institutions Act of 1982. This federal law prohibits lenders from exercising the due on sale clause for certain types of transfers, including a transfer into an inter vivos trust (living trust) in which the borrower is and remains a beneficiary. Some attorneys have argued this protection can extend to single-member LLCs where the borrower is the sole member, but this is a legal gray area and not universally accepted. The safest route is to get the lender's permission, which they may or may not grant.

Why Commercial or Private Lending is Preferred

Given the risks and gray areas associated with conventional loans, the overwhelming best practice is to use a loan product designed for LLCs from the start.

No "Due on Sale" Risk: Commercial and private loans (like DSCR or Hard Money) are made directly to the LLC. The title is vested in the LLC's name at closing, so there is no transfer and no risk of triggering the clause.

Designed for Business: These lenders understand real estate as a business. Their underwriting is focused on the asset and the business plan, not your personal financial picture.

Scalability: Commercial lenders don't have the 10-property limit that Fannie Mae imposes. They want to see you grow your portfolio.

Asset Protection from Day One: Your personal name is never on the title, ensuring the liability shield of the LLC is in place from the moment you take ownership.

Lender-Specific Rules and Seasoning Requirements

Unlike conventional lenders that heavily scrutinize title changes, private money lenders are specifically designed for real estate investors and actively encourage you to hold title in an LLC. If you currently own a property in your personal name, you can typically refinance it into an LLC using a DSCR loan directly at the closing table without a specific "title transfer" waiting period.

However, private lenders do enforce ownership seasoning rules to determine your maximum leverage, rather than to prevent owner-occupant fraud. If you have owned the property for less than 6 to 12 months (depending on the specific program and whether you are executing a cash-out or rate/term refinance), the lender will restrict your leverage by calculating your Loan-to-Value (LTV) using the lesser of your total Cost Basis (original purchase price plus documented improvements) or the current appraised value.

This seasoning policy ensures the investor maintains sufficient equity in the deal and protects the lender against artificially inflated appraisals shortly after an acquisition. The risk of owner-occupant fraud is eliminated entirely upfront, as all DSCR borrowers must sign a strict Business Purpose Affidavit legally certifying that the property will be used exclusively for investment purposes and neither the borrower nor their family will live there.

Step-by-Step Guide to Getting an LLC Loan

The process of getting an investment property loan for your LLC is more straightforward than many investors think, especially when working with an investor-focused lender. It involves preparing your entity, gathering documents, and following a clear application and underwriting process.

Step 1: Pre-qualification and Getting Your Instant Quote

At OfferMarket, we've streamlined this with our Instant Quote tool. Instead of filling out pages of paperwork and waiting days for a response, you can get real, transparent terms in minutes. You'll need to provide:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

OfferMarket Advantage: Our instant quote system lets you run the numbers on potential deals before you even submit a formal application. You can run multiple property scenarios through our calculator to identify which investments offer the best cash flow potential, ensuring you only submit applications for properties that make financial sense.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

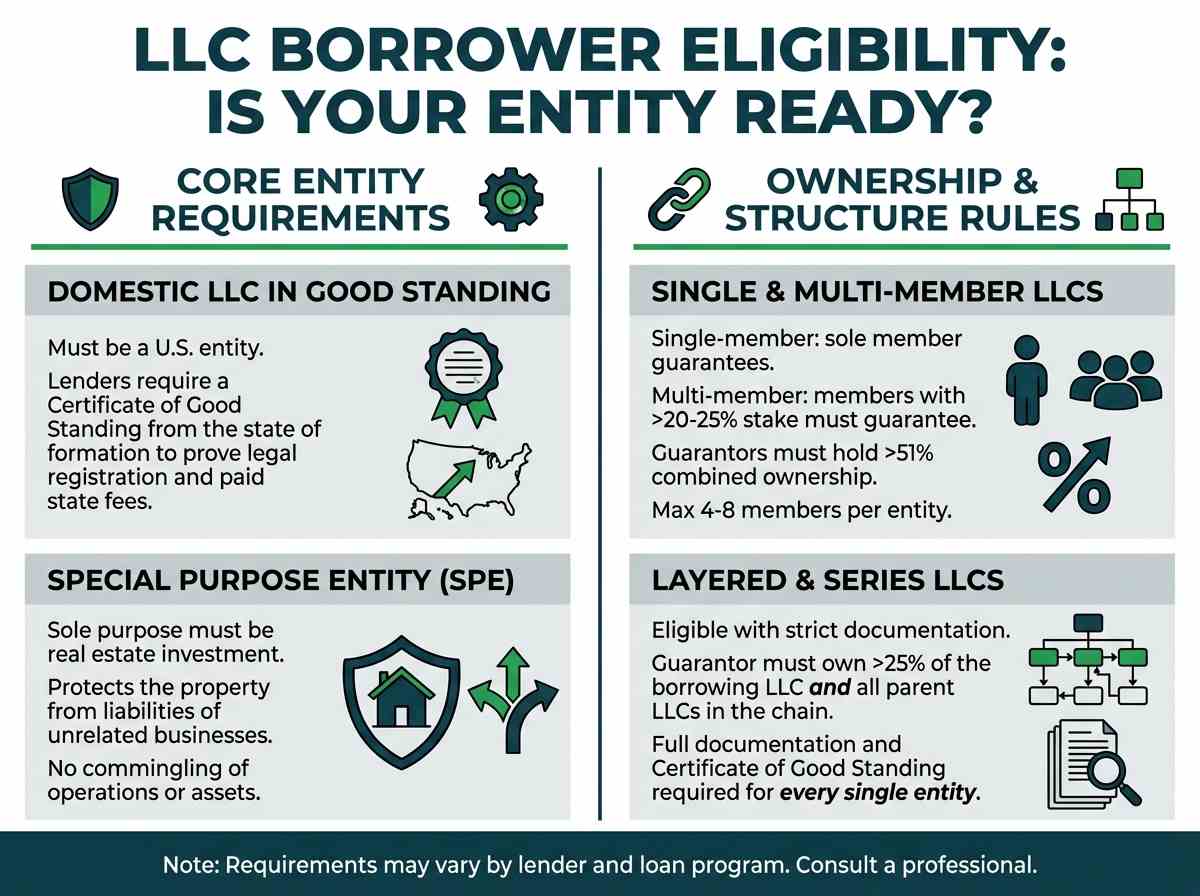

LLC Borrower Eligibility: Is Your Entity Ready?

Not every LLC is automatically eligible for an investment property loan. Lenders have specific requirements for the borrowing entity to ensure it's a legitimate, properly structured vehicle for real estate investment.

Requirement for a Domestic LLC in Good Standing

The LLC must be a domestic entity, meaning it was formed in one of the 50 U.S. states or the District of Columbia. Lenders will verify this by requesting a Certificate of Good Standing (sometimes called a Certificate of Existence or Certificate of Status) from the Secretary of State where the LLC was formed. This certificate proves that your LLC is legally registered and has paid all its state fees and filed all necessary reports. If your LLC is not in good standing, you will need to resolve any issues with the state before a lender will proceed.

Business Purpose Limited to Real Estate Investment

The LLC must be a "special purpose entity" (SPE). This means its sole purpose is to hold, manage, and conduct activities related to real estate investment. The lender wants to ensure the LLC's assets (the investment properties) are not at risk from liabilities arising from another, unrelated business. For example, if you also run a catering business, you should not run it out of the same LLC that holds your rental properties. This separation is crucial for both liability protection and financing eligibility.

Rules on the Number of Members or Owners

Lenders have specific rules regarding LLC structures and personal guarantees:

Single-Member LLCs (SMLLC): Very common and straightforward to finance. The sole member acts as the individual personal guarantor.

Multi-Member LLCs: Also very common, but subject to strict guarantor thresholds. Any member with a 20% to 25% or greater ownership stake is considered a material owner and must provide a full recourse personal guarantee. Additionally, the individuals providing the personal guarantees must hold a combined ownership stake equal to at least 51% of the borrowing entity.

Maximum Number of Members: To avoid overly complex ownership structures, lenders strictly cap the allowable number of members. Depending on the specific loan program, an entity is generally limited to a maximum of 4 to 8 total owners.

Eligibility for Layered or Series LLC Structures

More sophisticated investors may use advanced entity structures, such as Layered LLCs (where a holding company owns operating LLCs) or Series LLCs. Both structures are explicitly eligible for financing, provided they meet strict guarantor and documentation hurdles:

The 25% Ownership and Signing Rule: It is not enough to simply map the flow of ownership to the ultimate guarantor. The Personal Guarantor for the transaction must own at least 25% of the specific Borrowing Entity LLC and own at least a 25% stake in all subsequent ascending LLCs that make up the overall holding structure. Furthermore, the Personal Guarantor must possess legal signing rights for the Borrowing Entity and every single ascending LLC in that chain.

Comprehensive Documentation Requirements: Providing an organizational chart is insufficient to clear underwriting. The borrower must provide the full suite of entity documentation (Articles of Organization, Operating Agreement, EIN, etc.) for the borrowing LLC and every ascending parent LLC in the structure. Additionally, a valid Certificate of Good Standing is required from the state of formation for every single LLC in the layered or series structure.

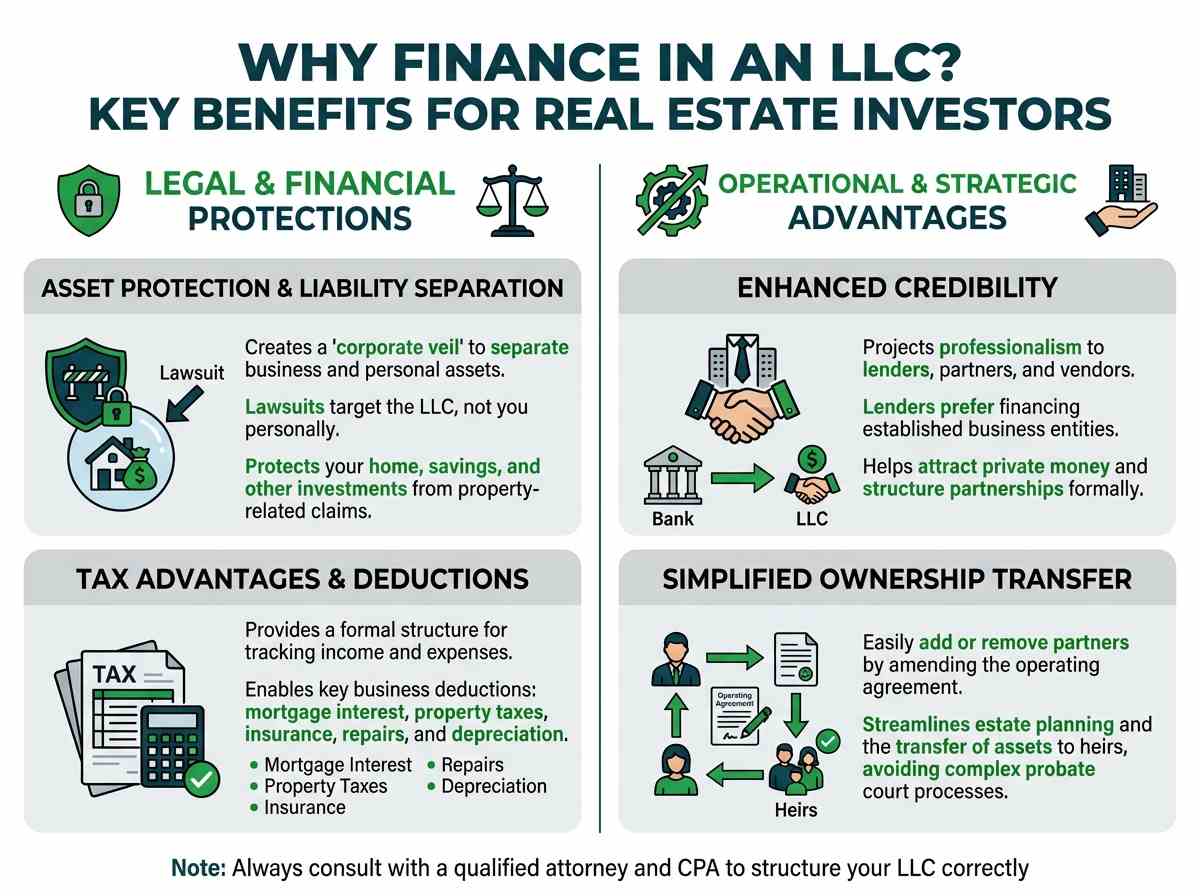

Why Finance an Investment Property in an LLC?

Holding investment property in an LLC is a foundational strategy for serious real estate investors. The benefits go far beyond just a name on a title; they provide crucial legal and financial protections that are unavailable when holding property in a personal name.

Asset Protection and Liability Separation

This is the single most important reason to use an LLC. When you hold a rental property in your personal name, all of your personal assets—your primary home, your car, your savings, your investments—are potentially at risk in a lawsuit related to that property. If a tenant, contractor, or visitor is injured on the property and sues, a judgment against you could be satisfied from your personal wealth.

An LLC creates a "corporate veil," a legal barrier between your business and personal affairs.

- LLC as the Owner: The LLC owns the property.

- LLC as the Defendant: If a lawsuit arises, the plaintiff sues the LLC, not you personally.

- Limited Liability: Any judgment is generally limited to the assets owned by the LLC (i.e., the equity in the property itself). Your personal assets are protected.

This protection is not absolute—it can be "pierced" if you fail to maintain the LLC properly (e.g., by commingling funds)—but when managed correctly, it is a powerful shield.

Enhanced Credibility with Lenders and Partners

Operating as a formal business entity like an LLC projects a higher level of professionalism and seriousness.

- With Lenders: Lenders who specialize in investment property loans prefer to lend to LLCs. It shows them you are treating your real estate activities as a business, which gives them more confidence in you as a borrower.

- With Partners: If you plan to bring in partners or raise private money for deals, operating through an LLC is non-negotiable. It provides a formal structure for ownership percentages, profit distribution, and management roles, all documented in the operating agreement.

- With Service Providers: Contractors, property managers, and other vendors will see you as a more established business, which can lead to better service and terms.

Tax Advantages and Business Expense Deductions

While a standard LLC is a "pass-through" entity for tax purposes (meaning profits and losses are passed through to the members' personal tax returns), it provides a formal structure for tracking income and expenses. This simplifies accounting and makes it easier to claim legitimate business deductions.

You can deduct expenses such as:

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Property management fees

- Depreciation

Consult with a qualified CPA, but using an LLC can also open the door to more advanced tax strategies, such as electing to be taxed as an S-Corporation in certain situations to potentially reduce self-employment taxes.

Simplified Transfer of Ownership and Estate Planning

An LLC simplifies the process of changing ownership, both during your lifetime and as part of your estate plan.

- Bringing on a Partner: To add a partner, you simply amend the operating agreement and issue new membership units. You don't need to change the title of the property itself, which would be a complex and costly process.

- Estate Planning: You can transfer ownership of your LLC membership interests to a living trust or to your heirs. This can be a much simpler and more private process than transferring direct ownership of multiple properties through probate court. The LLC and its properties continue to operate seamlessly without being tied up in probate.

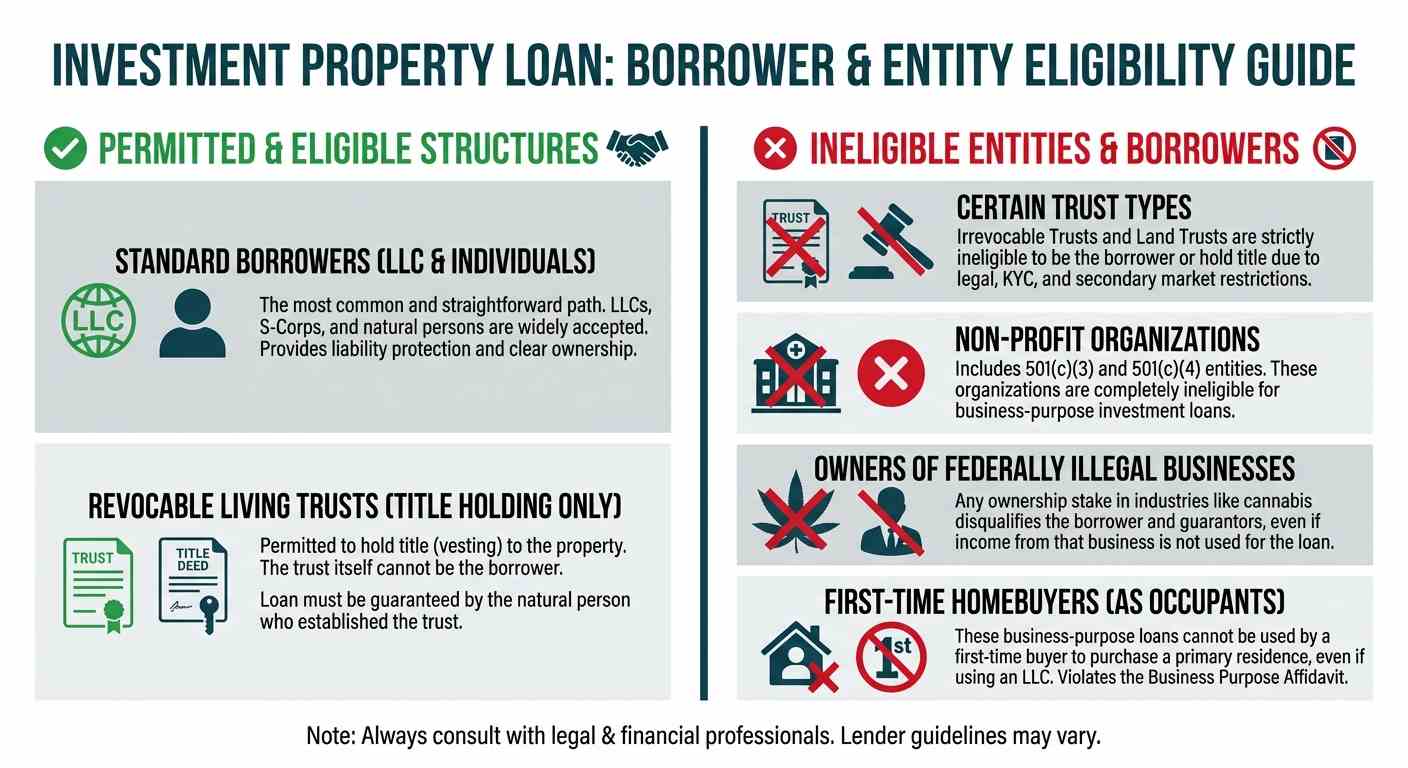

Ineligible Entities and Structures to Avoid

While investor-focused lenders are flexible, there are certain types of entities and borrowers that are generally ineligible for standard LLC investment property loans. Understanding these exclusions can save you time and prevent application rejections.

Certain Types of Trusts

Irrevocable Trusts: These are strictly ineligible to be borrowers or hold title across standard programs.

Land Trusts: A land trust itself cannot be the borrower on a loan,. Furthermore, lenders generally avoid funding properties held in structures like Illinois Land Trusts due to secondary market restrictions, Know Your Customer (KYC) anonymity rules, and the legal quirk that the beneficial interest is classified as personal property rather than real property.

Revocable Living Trusts (Inter Vivos Trusts): While a revocable trust cannot be the actual borrower on the loan, it is explicitly permitted to hold the title (vesting) of the subject property,,. This requires that the trust was established by a natural person who is the primary beneficiary and uses their personal income or assets to qualify,.

Non-Profit Organizations

Non-profit organizations, explicitly including 501(c)(3) and 501(c)(4) entities, are completely ineligible for these business-purpose loans,.

Entities with Ownership in Federally Illegal Businesses

Borrowers, guarantors, or business entities with any ownership stake in a federally illegal business (such as the cannabis or hemp industry) are strictly ineligible,. This applies even if the income from that federally illegal business is not being used to qualify for the loan.

First-Time Homebuyers

First-time homebuyers are completely ineligible for these investment property programs,,. These loans are strictly for business-purpose investment properties,. A first-time homebuyer cannot use an LLC to purchase a primary residence they intend to live in, as this violates the mandatory Business Purpose Affidavit signed at closing,.

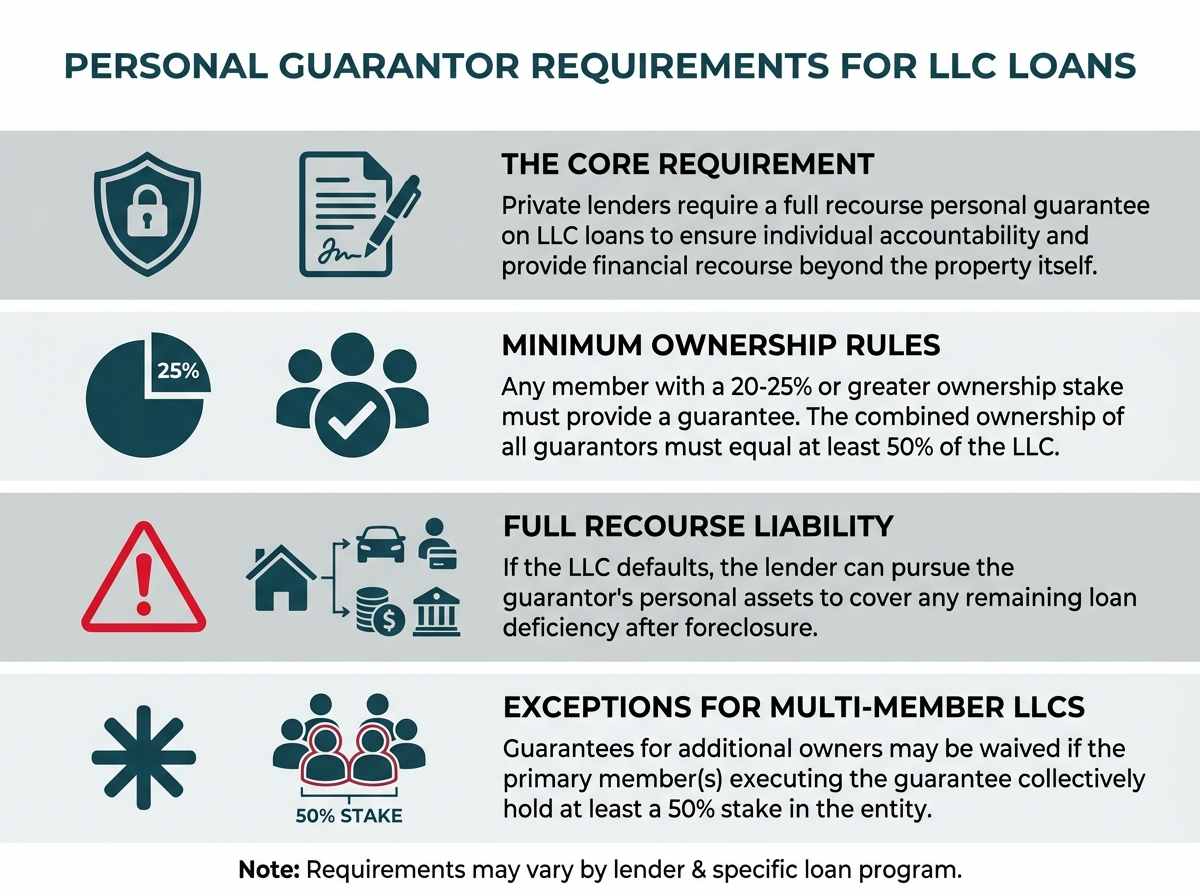

Personal Guarantor Requirements for LLC Loans

One of the most important concepts when financing a property in an LLC is the personal guarantee. Private lenders strictly require a full recourse personal guarantee on LLC loans to ensure individual accountability and provide financial recourse beyond the property itself if the entity defaults.

Minimum Ownership Stake

Any member holding a 20% to 25% or greater ownership interest in the LLC is considered a material owner and is generally required to provide a personal guarantee. Additionally, the combined ownership stake of all personal guarantors must equal at least 50% of the borrowing entity. If no single owner holds the minimum threshold, the majority owner must step in as the guarantor to fulfill this requirement.

Responsibilities and Liabilities

Signing a personal guarantee creates a full recourse obligation. If the LLC defaults and the property is foreclosed, the lender retains the right to pursue the guarantor's personal assets to cover any remaining loan deficiency.

Exceptions for Multi-Member LLCs

While standard rules typically require all material owners to guarantee the loan, some private lender programs allow the guarantee for additional owners to be waived. This is permitted provided that the highest majority member(s) executing the full recourse guarantee collectively make up at least a 50% stake in the entity.

Who Can Be a Personal Guarantor?

Lenders have specific eligibility criteria for the individuals who can serve as personal guarantors on an LLC loan. These requirements are based on residency status, as this affects the lender's legal ability to enforce the guarantee if necessary.

U.S. Citizens and Permanent Residents

This is the most straightforward category.

- U.S. Citizens: Individuals born in the U.S. or who have become naturalized citizens are fully eligible.

- Permanent Residents: Also known as "Green Card" holders, these individuals are legally permitted to live and work in the U.S. on a permanent basis and are eligible to be guarantors.

Proof of status is typically verified through standard identification documents.

ITIN Borrowers Residing in the U.S.

An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the IRS to individuals who are required to have a U.S. taxpayer identification number but who do not have, and are not eligible to obtain, a Social Security Number (SSN).

Many modern lenders, including OfferMarket, have programs that allow U.S.-residing ITIN holders to be personal guarantors. This opens up investment opportunities for many foreign nationals who live and invest in the United States but are not permanent residents. The key requirement is that they must physically reside in the U.S.

Non-Permanent Resident Aliens with Specific Visa Types

Individuals legally residing in the U.S. on a temporary basis are eligible if they hold specific valid visas (such as the E, G, H, L, NATO, O, P, and TN series). They must provide copies of their unexpired visa and/or a valid Employment Authorization Document (EAD) if not sponsored by their current employer.

Foreign Nationals

Many DSCR programs explicitly allow Foreign Nationals living abroad to guarantee an LLC loan. However, they face stricter terms: leverage is typically capped at 65% to 70% LTV (requiring a 30% to 35% down payment), and they must verify 6 to 12 months of PITIA reserves. Furthermore, these funds typically must be seasoned in a U.S. FDIC-insured institution for 30 to 60 days prior to closing. Borrowers from OFAC-sanctioned countries or specific restricted nations (such as Venezuela) are strictly ineligible.

Why Choose OfferMarket for Your LLC Loan?

When you're ready to finance your LLC's next investment, choosing the right lender is as important as choosing the right property. OfferMarket is a modern lending platform built from the ground up to serve the specific needs of real estate investors. We combine technology, speed, and expertise to provide a superior borrowing experience.

Streamlined Process Designed for Real Estate Investors

We speak your language. Our entire process, from application to closing, is designed with the investor in mind. We don't ask for unnecessary paperwork or waste your time with processes meant for primary homebuyers. Our online platform makes it easy to submit your LLC and property information, upload documents, and track your loan's progress 24/7.

Fast Closings in 10-21 Days to Secure Deals Quickly

In a competitive real estate market, speed is a critical advantage. While traditional lenders can take 45-60 days to close a loan, OfferMarket's efficient process allows us to close most loans in 10 to 21 days. This speed gives you the power to compete with cash buyers, negotiate better terms with sellers, and lock down deals before your competition.

Modern Technology Like Desktop Appraisals and App-Based Draws

We leverage technology to make your life easier and your deals more profitable.

Desktop Appraisals: For many loan scenarios, we can use a desktop appraisal, which is faster and more cost-effective than a traditional in-person appraisal, saving you time and money.

App-Based Draws: For fix and flip or new construction projects, our mobile app simplifies the draw process. You can request funds, upload progress photos, and get your renovation money disbursed quickly, keeping your project on schedule without the hassle of paper forms and multiple site visits.

Competitive Rates and Lower Fees for Scaling Portfolios

Our goal is to be your long-term financial partner. We offer highly competitive interest rates and transparent, fair fees. By eliminating the overhead of traditional brick-and-mortar lenders, we pass the savings on to you. Lower borrowing costs mean better cash flow on your rentals and higher profit margins on your flips, allowing you to scale your investment portfolio more effectively.

Get Your Instant LLC Loan Quote

Navigating the world of LLC financing doesn't have to be complicated. With the right knowledge and the right lending partner, you can leverage your business entity to protect your assets and scale your real estate portfolio effectively. The key is to choose a loan product that matches your strategy and work with a lender who is built to serve investors.

Ready to see what terms your LLC can qualify for? The next step is simple.

Submit Property and LLC Details Online in Minutes

Use OfferMarket's free and easy-to-use tool to get a transparent loan quote. There's no impact on your credit score to see your options. Simply provide some basic information about your LLC and the investment property you're looking to finance.

Receive a Transparent Term Sheet with Rates and Fees

Within minutes, you'll receive a detailed term sheet outlining the interest rate, loan amount, and all associated fees for various loan options. We believe in 100% transparency, so you'll see all the numbers upfront with no hidden costs.

Connect with a Dedicated Loan Officer

Once you receive your quote, you'll be connected with a dedicated loan officer who specializes in working with real estate investors. They can answer your specific questions, guide you through the next steps, and help you close your loan quickly and efficiently.

Don't let financing be the bottleneck in your investment journey. Get an instant quote from OfferMarket today and fund your LLC's next deal with confidence.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull