*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

2026's Top Hard Money Lenders: Who Offers 90% LTC & 100% Rehab?

The hard money lending world has changed a lot, with plenty of lenders now competing to meet real estate investors' varied needs. Whether you're tackling your first flip or juggling multiple projects as an experienced investor, choosing the right lender can make or break your deal. Below, we've put together a detailed list of 23+ trusted hard money lenders, each bringing something different to the table for various investment approaches.

OfferMarket – The Integrated Real Estate Investment Platform

OfferMarket isn't your typical hard money lender. We've built an integrated ecosystem that brings together financing, property listings, and insurance solutions under one roof. What does that mean for you? Better market insights, a smoother process, and more money staying in your pocket.

Here's What Sets Us Apart:

- Industry-Leading Leverage: Get up to 90% Loan-to-Cost (LTC) and 100% of your renovation budget covered—so you can stretch your capital further

- Transparent Terms: No surprise junk fees like application charges, processing fees, or document prep costs. What you see is what you get

- Marketplace: Our property marketplace gives us eyes on extensive deal flow, which means we understand market conditions and property values at a deeper level

- Comprehensive Insurance Solutions: Get integrated insurance quotes that ensure you're properly covered without overpaying

- Diverse Product Suite: We work with multiple capital providers to offer fix and flip, DSCR, slow flip, low balance DSCR, HELOANs—whatever fits your strategy

- In-House Underwriting: Fast, consistent decisions with dedicated relationship managers who know your goals

- Experience-Based Rewards: The more projects you complete, the better your leverage and terms become

Other Leading Hard Money Lenders

Kiavi

Lima One Capital

Griffin Funding

RCN Capital

New Silver

CoreVest Finance

LendingOne

Easy Street Capital

Groundfloor

Asset Based Lending (ABL)

We Lend

Fund That Flip

Flip Funding

Gauntlet Funding

Residential Capital Partners

MoFin Lending

Socotra Capital

BridgeWell Capital

Rehab Financial Group

Sherman Bridge Lending

Patch of Land

Wilshire Quinn Capital

Choosing the Right Lender for Your Strategy

With so many options out there, picking the right hard money lender comes down to a few key factors: how much experience you have, what kind of project you're tackling, where you're investing, and what your specific financing needs look like. Larger national lenders like Kiavi and Lima One bring consistency and scale to the table, while regional specialists often deliver more hands-on service and deeper knowledge of your local market. Platform-integrated lenders like OfferMarket stand out by taking a holistic approach—combining financing with marketplace insights and insurance solutions for a smoother investment experience.

The bottom line? Evaluate each lender based on their terms, leverage options, geographic coverage, closing speed, and how upfront they are with you. In the sections ahead, we'll walk you through exactly how to compare these lenders so you can make the smartest choice for your investment strategy.

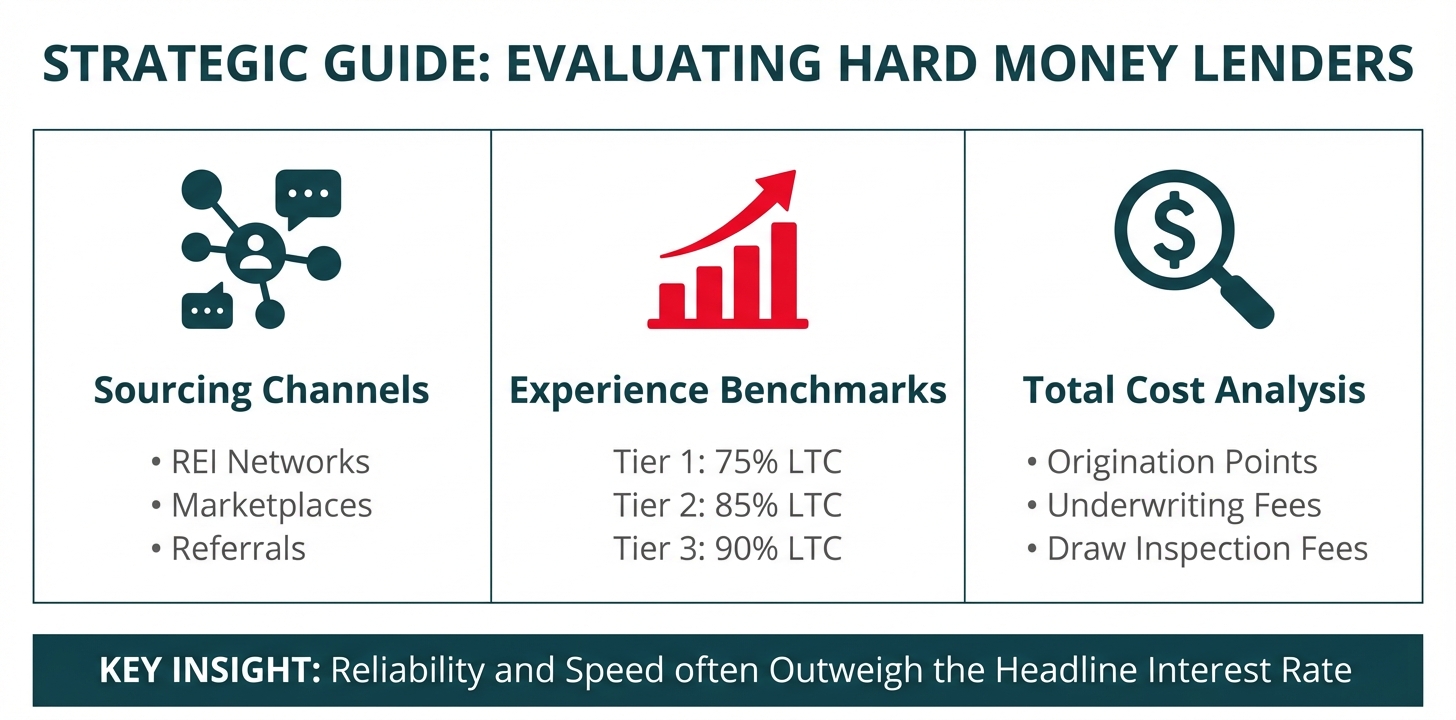

How to Find and Evaluate Hard Money Lenders

Finding the right hard money lender can make or break your real estate deal. This isn't like getting a traditional mortgage where you stroll into your neighborhood bank. Hard money lending takes a more strategic approach when it comes to sourcing and vetting potential partners. Here's the deal: you need to know where to look, what questions to ask, and how to size up lenders beyond just their advertised interest rates.

Finding Hard Money Lenders: Where to Start Your Search

Real Estate Investor Networks and Meetups

Local real estate investor associations (REIAs) and meetup groups are goldmines for finding reputable hard money lenders. These gatherings connect you with active investors who've worked with various lenders in your market. The real talk you'll get at these events is invaluable—you'll hear which lenders actually follow through on their promises and which ones turn closing day into a nightmare.

Attending these meetings regularly also helps you build relationships with lenders who often attend to network with potential borrowers. This face-to-face interaction gives you a real sense of how they communicate, how quickly they respond, and whether they're genuinely invested in helping you succeed. Some of the strongest lending partnerships begin with a simple handshake at a local investor meetup.

Specialized Online Investment Marketplaces

Platforms like OfferMarket introduce integrated ecosystems bring buyers, sellers, and financing together in one place. The big advantage over standalone lender websites? You can compare multiple financing options right alongside property listings, making your journey from finding a deal to closing it much smoother.

What does that mean for you? Smarter underwriting, more competitive terms, and lenders who truly understand what makes deals work in your specific area. When you partner with a platform that sees everything—from property search to insurance to financing—you tap into their complete picture of the market.

Online Directories and Lender Databases

You'll find several online directories that organize hard money lenders by state and loan type. These can be helpful jumping-off points, but here's a word of caution: not every directory carefully screens their listings, and some lenders simply pay for top placement regardless of their actual performance. Use these resources to build your initial list, then roll up your sleeves and do your homework before committing to anyone.

Referrals from Successful Investors and Real Estate Professionals

In the hard money lending world, a recommendation from an experienced investor is worth its weight in gold. When a seasoned flipper or rental property investor points you toward their lender, they're putting their reputation on the line—vouching for that lender's dependability, speed, and honest dealings. Similarly, real estate agents, title companies, and contractors who work regularly with investors often have insights into which lenders consistently perform well.

Don't be shy about asking fellow investors what they've experienced—the good and the bad. Try questions like "Who did you use for your last three deals?" and "Have you ever had a deal fall through because of your lender?" These conversations uncover the real story that glossy marketing materials won't tell you.

Critical Questions to Ask When Evaluating Lenders

Once you've got a list of potential lenders, it's time to roll up your sleeves and dig in. The questions you ask during initial conversations will help you figure out whether a lender truly fits your investment strategy and where you are in your journey.

Loan Amount Parameters

Start with the basics: "What are your minimum and maximum loan amounts?" This straightforward question confirms the lender can actually handle your deal size. Some lenders focus on smaller loans ($50,000-$150,000) while others prefer bigger projects ($500,000+). If your typical deal falls outside their wheelhouse, expect higher rates or tougher terms—they're compensating for added risk or extra paperwork on their end.

Underwriting Process and Speed

Here's a key one: "Is your underwriting handled in-house, and what's your typical timeline from application to approval?" In-house underwriting means faster, more predictable results. Lenders who farm out underwriting to third parties? That's where delays and surprises creep in. When you're sizing up lenders, understanding their approval process tells you whether they can move fast enough to help you land competitive deals.

Then ask: "How many deals do you close per month, and what percentage of applications get approved?" These numbers show you both their bandwidth and how picky they are. A lender closing 50+ deals monthly has solid systems running smoothly. An approval rate between 60-80% suggests they're selective but reasonable—too high might indicate loose underwriting, too low suggests overly conservative criteria.

Relationship Management

Here's a question that really matters: "Will I be assigned a dedicated relationship manager or point of contact throughout the loan process?" Having someone in your corner makes a huge difference when you're racing to close a deal or need quick answers about a draw request. Lenders who pass you around between different reps create frustrating communication gaps and costly delays.

A dedicated relationship manager who gets your business strategy, knows your track record, and can go to bat for you internally is worth their weight in gold. This person becomes your partner in building your real estate portfolio, not just someone processing paperwork.

Draw Structures and Renovation Funding

Ask: "How do you structure the draws for renovation funds, and do you fund 100% of the rehab budget?" Getting clear on the draw process is key for managing your cash flow. Some lenders make you pay contractors out of pocket first and reimburse you after inspections, while others pay contractors directly. How quickly inspections and approvals happen can make or break your project timeline.

Make sure you know whether they fund 100% of your approved rehab budget or only a portion (like 90%). If they hold back 10%, you'll need extra cash on hand to cover that gap. Also dig into their inspection process—do they use third-party inspectors, how fast can inspections get scheduled, and what's the typical turnaround for draw approval once the inspection is done?

Experience Tier Requirements

"What are your experience tier requirements, and how do they affect leverage and terms?" This question is crucial for mapping out your growth path. Most hard money lenders group their borrowers into tiers based on completed projects:

- Tier 1 (Beginner): 0-2 completed projects, typically 75-80% LTC, higher rates

- Tier 2 (Intermediate): 3-5 completed projects, typically 80-85% LTC, mid-range rates

- Tier 3 (Experienced): 6+ completed projects, typically 85-90% LTC, best rates

Knowing where you fall helps you set realistic expectations for your current deal and gives you a clear picture of the better terms waiting for you as you build your track record with the lender.

Fee Transparency

This question is non-negotiable: "What are all the fees associated with this loan, including any that aren't included in the interest rate?" Demand complete transparency about every fee—origination, application, processing, underwriting, document preparation, wire transfer, courier, and any other charges.

Be cautious of lenders who dance around fee questions or say they'll "work it out down the road." The good ones? They hand you a detailed fee breakdown right from the start. Here's a smart move: add up all those fees alongside your interest expense to get your true cost of capital. That lender advertising 10% interest with 3 points in fees? They might actually cost you more than one charging 11% with just 1 point.

Closing Timeline

Ask: "What's your average closing timeline from application to funding?" In real estate investing, time is money—literally. A lender dragging their feet for 45 days could mean watching deals slip away in hot markets. Top-tier hard money lenders get you to the finish line in 10-15 days, and some can even close in 7 days for experienced investors with clean deals.

Here's another good one: "What factors typically cause delays in your closing process?" Their answer tells you where the bottlenecks are. If third-party appraisals or title work slow things down, you can get ahead of it by starting those processes early.

Extension Options

"What are your policies on loan extensions, and what do they cost?" This one's essential for protecting yourself. Let's face it—projects rarely go exactly as planned. Contractor hiccups, permit headaches, or shifting market conditions might mean you need extra time. Knowing the extension terms upfront saves you from scrambling later.

Here's what you'll typically see: extensions run 3-6 months and cost 1-2 points plus ongoing interest. Some lenders draw a hard line at 18-24 months total, no matter what. Others ramp up the cost with each extension to encourage you to wrap things up on schedule.

Default Process

Now for the question nobody wants to ask: "What's your process if a borrower defaults or can't complete the project? While no one plans to default, understanding how a lender handles tough situations tells you a lot about who they really are. Good lenders roll up their sleeves and work with borrowers to find solutions—whether that means bringing in new contractors, extending terms, or helping facilitate a property sale. Predatory lenders? They jump straight to foreclosure at the first sign of trouble.

Ask about their historical default rate and how they've navigated past defaults. A lender who claims they've never had a default either has extremely conservative underwriting or simply hasn't been in the game long enough to face real challenges.

Additional Evaluation Criteria Beyond the Basics

Reputation and Reviews

In today's connected world, a lender's online reputation tells a powerful story. Search for reviews on Google, Better Business Bureau, Trustpilot, and real estate investor forums. Look for patterns in the feedback—one negative review might be an outlier, but multiple complaints about the same issue (hidden fees, slow draws, poor communication) point to systemic problems.

Pay close attention to how lenders respond to negative reviews. Do they own the issue and offer solutions, or do they get defensive and point fingers at borrowers? How they respond often reflects exactly how they'll treat you when challenges arise.

Transparency in Communication

Throughout your initial conversations, gauge how transparent the lender really is. Do they answer your questions directly and completely, or sidestep the specifics? Are they willing to share sample loan documents before you apply? Do they explain their underwriting criteria in plain terms?

Transparency shows up on their website and marketing materials too. Lenders who clearly display their rates, fees, and terms are confident in what they offer. Those who make you call for "customized quotes" might be less competitive or tack on fees based on how eager they think you are.

Technology Platform and Tools

Today's best hard money lenders provide user-friendly technology platforms for applications, document uploads, draw requests, and loan tracking. A user-friendly online portal tells you a lot about a lender—it shows they care about your experience and run a tight ship. Clunky systems where you're emailing documents back and forth or calling just to get updates? That's wasted time, and it usually means slower processing across the board.

Ask for a demo of their borrower portal. Can you check your loan status anytime, day or night? Submit draw requests online? Upload documents securely? Track your payment history? These features might seem like nice-to-haves until you're juggling multiple projects and need answers fast.

Geographic Coverage and Local Expertise

Make sure the lender actually works in your target markets. Some hard money lenders say they're national but don't really know the ins and outs of specific regions. Others zero in on particular states or metro areas where they've built solid relationships with appraisers, inspectors, and title companies.

Here's the thing: real estate is local. A lender who gets the neighborhood dynamics, knows what contractors charge in your area, and understands regional market trends can underwrite your deal faster and more accurately. They'll also give you better feedback on whether your renovation budget makes sense and if your ARV projections hold water.

The Importance of Comparing Multiple Lenders

Don't commit to the first lender you talk to, no matter how good their terms sound upfront. Talk to at least three to five lenders so you know what's really out there. This comparison shopping pays off in several ways:

First, it gives you negotiating power. When you can honestly say, "Lender X offered me these terms," Lender Y might just sweeten their deal. Second, you'll learn what's normal in the market—you'll spot competitive offers versus outliers pretty quickly. Third, you'll find the lender whose communication style and approach actually fit how you like to work.

Understanding Total Cost of Capital

Here's the biggest mistake new investors make: they zero in on interest rates and miss the bigger picture of what a loan actually costs. Your total cost of capital includes:

- Interest rate (monthly cost)

- Origination points (upfront cost, typically 1-3% of loan amount)

- Processing and underwriting fees (typically $500-$1,500)

- Appraisal costs (usually $400-$800, sometimes more for complex properties)

- Draw inspection fees (typically $100-$150 per inspection)

- Extension fees (if needed, typically 1-2 points per extension)

- Prepayment penalties (some lenders charge if you pay off early)

Here's the key: calculate your all-in cost for the expected loan duration. A 9% loan with 2 points might actually cost you more than a 10% loan with 0.5 points if you're planning a quick 6-month flip. Run the numbers for different scenarios—what happens if the project stretches to 12 months instead of 6? What if you need an extension?

The lender advertising the "lowest rate" often isn't your cheapest option once you factor in all fees and a realistic project timeline. This is where an integrated platform like OfferMarket gives you an edge—our holistic view of your deal, combined with relationships across multiple capital providers, helps ensure you're getting genuinely competitive total costs, not just eye-catching headline rates.

Finding and evaluating hard money lenders takes work, but that effort pays off throughout your investing career. The right lender becomes a true strategic partner who helps you grow your business. The wrong one? Stress, delays, and money out the window. Take time to ask the tough questions, compare your options, and choose a lender who shows you transparency, expertise, and a real commitment to your success.

What Are Hard Money Loans?

Think of hard money loans as your fast-track ticket to real estate investing. These asset-based, short-term financing solutions are built for investors who need to move quickly when opportunity knocks. Here's the key difference: while traditional lenders spend weeks scrutinizing your credit score, pay stubs, and debt-to-income ratios, hard money lenders zero in on what really matters—the property itself. This game-changing approach puts you in the driver's seat when you're competing for deals or chasing that diamond-in-the-rough property.

Simply put, a hard money loan uses real property as security, and your approval hinges on what that asset is worth today and what it could be worth tomorrow—not your personal financial history. This means you can jump on opportunities that banks would either turn down flat or drag out for weeks. The property backs the loan, and its value—not your W-2s or tax returns—determines how much you can borrow.

The Structural Framework of Hard Money Loans

Hard money loans follow a straightforward structure that sets them apart from conventional financing. Most loans run for 12 months, though you'll find lenders offering 18 to 24-month terms for bigger projects like major additions, conversions, or ground-up builds. Why so short? Because these loans are designed to carry you from purchase to either sale or refinancing into a long-term loan.

Here's how payments typically work: you pay interest only each month, then pay off the entire principal as a balloon payment when the loan matures. This setup keeps more cash in your pocket during renovations so you can focus on adding value to the property. Let's break it down: on a $200,000 loan at 10% annual interest, you're looking at roughly $1,667 per month in interest payments, with the full $200,000 principal due at the end of your term.

Interest charges can be structured in two primary ways depending on the loan size and lender preferences. For smaller loans (typically under $100,000), lenders often use a "full boat" structure where interest is charged on the total loan amount from day one, regardless of when funds are actually drawn. For larger loans, an "as disbursed" structure is more common, where interest accrues only on the unpaid principal balance as funds are drawn for renovation work. This second approach can result in significant interest savings for investors undertaking substantial rehab projects.

Understanding ARV and LTC: The Core Metrics

Two key concepts sit at the heart of hard money lending: After Repair Value (ARV) and Loan-to-Cost (LTC). These metrics are the building blocks lenders use to evaluate deals and determine how much funding you can access.

After Repair Value (ARV) is simply what your property will be worth once all your planned renovations are complete. Lenders bring in professional appraisers to assess both the current "as-is" value and the projected ARV based on your renovation plans. Here's a quick example: a distressed property might be worth $150,000 today but could hit $300,000 after a solid renovation. That ARV figure is what lenders look at when deciding how much capital to put behind your project.

Loan-to-Cost (LTC) tells you what percentage of your total project cost the loan covers—that includes both your purchase price and renovation budget. Let's say you're buying a property for $150,000 and putting $50,000 into renovations (total cost: $200,000). If a lender offers you $180,000, that's 90% LTC. The higher your LTC, the less cash you need upfront—freeing up capital for your next deal or those surprise expenses that pop up. Top-tier lenders like OfferMarket offer up to 90% LTC for experienced investors, which can dramatically reduce how much capital you need to tie up in each project.

Who Uses Hard Money Loans and Why

Hard money loans work for a wide range of real estate investors, from first-timers tackling their debut fix-and-flip to experienced pros juggling multiple properties in their portfolio. The private lending market has experienced substantial growth, with activity up 12.3% in 2024 compared to 2023. This tells us something important: hard money has moved from a niche product to a go-to financing strategy for savvy investors.

So why are more investors turning to hard money? Let's break it down:

Speed and Certainty of Execution: In hot real estate markets, closing fast can make or break a deal. Hard money lenders typically close in 7-14 days, while conventional financing drags on for 30-60 days. That speed lets you make cash-equivalent offers, go toe-to-toe with institutional buyers, and jump on time-sensitive opportunities like foreclosure auctions or off-market deals.

Access to Distressed Properties: Traditional banks shy away from properties in rough shape—they want minimum habitability standards met. Hard money lenders see things differently. They focus on what a property will be worth after renovation, not its current condition. That means foreclosures, estate sales, fire-damaged properties, and major fixer-uppers are all on the table for you.

Flexibility Beyond Credit Scores: Yes, hard money lenders look at credit scores (usually wanting a minimum FICO of 680), but they skip the rigid debt-to-income math that limits conventional borrowing. If you've got solid real estate experience and a strong deal, you can secure financing even if your personal income wouldn't cut it for a traditional mortgage. The question shifts from "Can you afford the payment?" to "Does this deal pencil out?"

Portfolio Scalability: Traditional mortgages often cap you at 4-10 financed properties thanks to Fannie Mae and Freddie Mac guidelines. Hard money loans don't count against those limits since private lenders hold them rather than selling to government-sponsored enterprises. This allows ambitious investors to scale their portfolios without hitting artificial ceilings, supporting strategies like the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) that require rapid capital recycling.

Strategic Capital Deployment: Smart investors use hard money loans as a powerful tool to stretch their dollars further. By leveraging up to 90% of project costs, you can spread your capital across multiple projects at once instead of locking it all into a single deal. This approach helps you diversify your risk while potentially boosting your overall returns. Here's a simple example: with $200,000 in capital, you could buy one property outright—or, with 90% LTC financing, you could put $40,000 down on each of five separate projects.

The private lending market's growth—projected to hit around $2 trillion in assets by 2025—shows just how far hard money has come. It's no longer a last-ditch option. Today's hard money borrowers are savvy investors who use short-term financing to gain a competitive edge and maximize returns in ways traditional loans simply can't match.

Understanding these basics helps you decide whether hard money financing fits your investment strategy, risk comfort level, and growth goals. Here's the bottom line: hard money loans aren't good or bad by nature—they're a specialized tool that works best in specific situations where speed, flexibility, and asset-based underwriting open doors that conventional financing would keep closed.

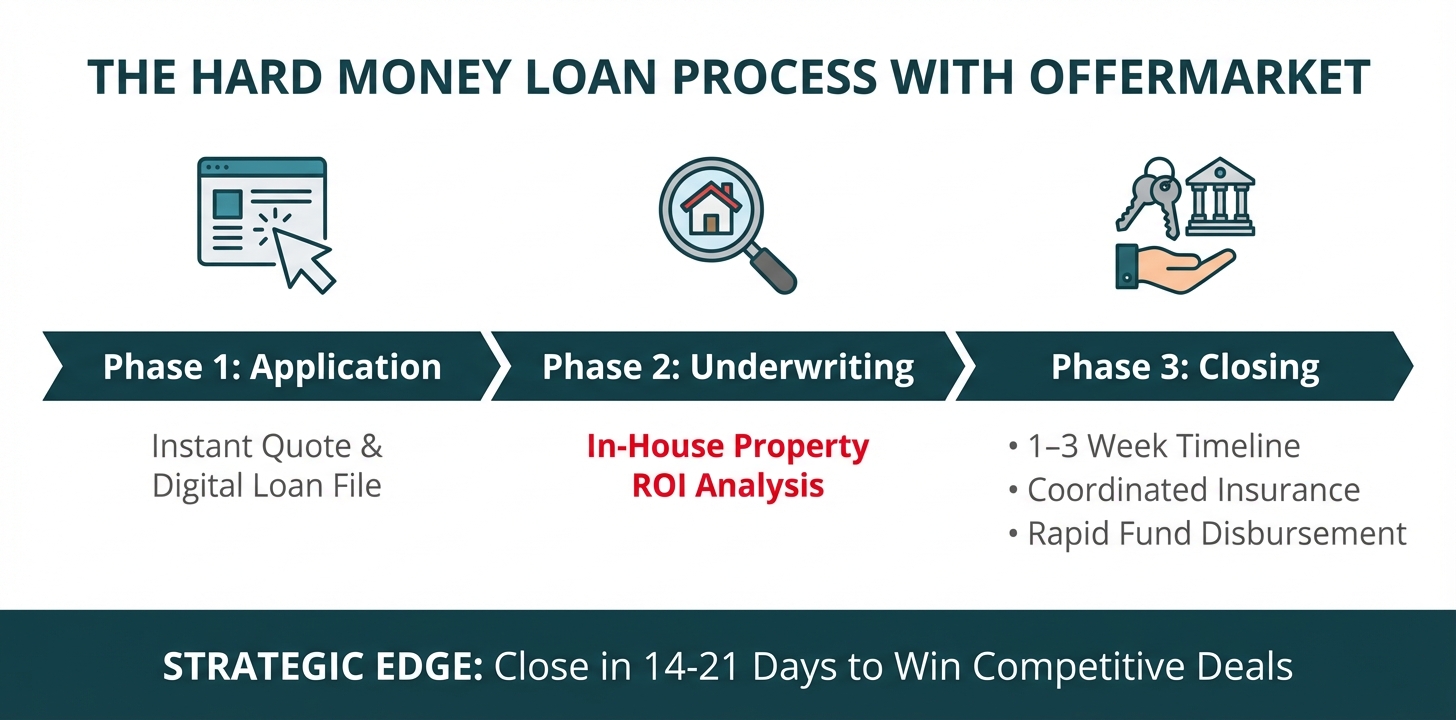

Steps to Get a Hard Money Loan: The Process with OfferMarket

Getting a hard money loan follows a structured but streamlined process built to fund investors fast. Knowing each step and gathering your documents ahead of time can seriously speed things up. Here's your complete walkthrough of the hard money loan process from application to closing, along with how OfferMarket keeps things moving efficiently.

1. Application: The Starting Line for Your Project

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

Your path to funding kicks off with a simple online application. Unlike traditional mortgages that bury you in personal financial paperwork, hard money lenders zero in on what really matters: the property's potential and whether the deal makes sense.

Pro Tip: Come prepared. Know your target property's purchase price, have a solid renovation budget in mind, and be realistic about your ARV. Accurate numbers from the start mean a smoother ride to closing.

2. Documentation: Building Your Loan File

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Here's why this matters for your bottom line. Traditional lenders often surprise you with hidden fees at closing. We take a different approach—laying out all costs upfront so you can review every line item, understand exactly what you're paying for, and calculate your true all-in costs before committing.

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

3. Move to Processing & Upload Remaining Documents

After thoroughly reviewing your preliminary Loan Terms in your Loan File, you're ready to formally begin the underwriting process. This is where you signal your intent to proceed by clicking "Move to processing" within your Loan File. This action lets OfferMarket's team know you're ready to roll and prepared to submit your documentation.

The Document Upload Phase:

Once you're here, head to the "Processing" section of your Loan File where you'll find a clear checklist of urgent section that's what we need from you.

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

OfferMarket's Speed Promise: Closing in Under 1-3 Weeks

This is where OfferMarket really shines compared to traditional lenders. Banks? They'll keep you waiting 30 to 60 days. Even some hard money lenders drag things out for weeks. We typically get you to the closing table in under 1-3 weeks. Many of our investors see funding in just 14-21 days from application to keys in hand.

And here's why that matters beyond convenience—it's your edge in competitive markets. When sellers are juggling multiple offers, your ability to close fast can win the deal, even if someone else bids higher. Sellers value certainty and speed, and a two-week close with verified financing beats a 45-day conventional loan closing every time.

Your Role in Expediting the Process:

Here's the deal: OfferMarket's ability to close quickly depends on getting all necessary documents from you right away. Let's break down how the timeline works:

- Days 1-3: Document review and initial underwriting

- Days 4-7: Property valuation, title search, and final underwriting

- Days 8-14: Loan approval and closing document preparation

- Days 14-19: Closing and funding

This timeline holds up when you submit complete, accurate documentation immediately after moving to processing. Every day you delay providing documents adds a day to your closing timeline. Incomplete or unclear documentation can stretch things out even further, since the underwriting team will need to circle back for clarification or additional information.

Pro Tips for Fast Processing:

- Submit everything at once: Instead of uploading documents one at a time, gather everything on the checklist and send it all together

- Ensure clarity and quality: Make sure scanned documents are legible and complete (all pages included)

- Respond immediately: When the processing team asks for additional information or clarification, get back to them within hours, not days

- Stay accessible: Be available by phone and email during business hours for quick questions

- Prepare your contractor: Have your contractor ready to provide additional detail on the scope of work if needed

The difference between a 10-day close and a 20-day close often comes down to document preparation and responsiveness. Investors who treat the document submission phase with urgency consistently close faster, secure better deals, and start generating returns on their investment sooner.

Follow OfferMarket's streamlined seven-step process and stay in close communication throughout. You'll be positioned to move quickly on profitable opportunities and run your fix and flip business at peak efficiency. The platform is designed to work at your pace—but the faster you move, the faster you can get funded and start your project.

4. Underwriting: Deal Analysis and Approval

Underwriting is where lenders dig deep into both the deal and the borrower. Here's the key difference: hard money underwriting focuses on the property's profit potential rather than your personal income.

What Underwriters Evaluate:

Property ROI Projections:

- Purchase price versus ARV to calculate potential profit

- Total renovation costs versus the projected value increase

- Holding costs including interest, insurance, taxes, and utilities

- Expected selling costs (agent commissions, closing costs, concessions)

- Minimum acceptable ROI thresholds (typically 15-20% after all costs)

Background and Fraud Checks:

- Criminal background checks on all personal guarantors

- Verification of identity and business entity legitimacy

- Review of previous foreclosures, bankruptcies, or loan defaults

- Cross-referencing property ownership records

- Verification that the borrower isn't using fraudulent documentation

Experience Tier Verification:

- Confirmation of previous projects claimed in investor resume

- Validation of property addresses and completion dates

- Assessment of project complexity and outcomes

- Determination of appropriate leverage based on proven track record

Deal Structure Analysis:

- Loan-to-cost ratio ensuring adequate borrower equity

- Loan-to-ARV ratio protecting lender position

- Exit strategy viability (sale timeline, refinance potential)

- Market conditions and absorption rates in the property's location

Timeline:

With complete documentation, underwriting typically takes 5-10 business days. However, missing documents, unclear SOWs, or questions about the borrower's experience can extend this timeline significantly.

OfferMarket's In-House Underwriting:

Here's something that sets OfferMarket apart: we handle all underwriting in-house. No outsourcing to third parties means you get consistent decision-making, faster turnaround times, and direct communication between underwriters and loan officers. When questions come up, they're resolved on the spot rather than bouncing between multiple parties.

Pro Tip:

Be completely transparent about your experience level and any past challenges. Underwriters will uncover inconsistencies, and honesty builds trust. If you're a first-time flipper, highlight your team—an experienced contractor, a knowledgeable agent—and your conservative deal structure rather than overstating your personal experience.

5-7. Closing: Finalizing the Deal

Once underwriting gives you the green light, you're in the home stretch. The closing phase is where legal documents get signed and funds hit the account.

Pre-Closing Requirements:

Title and Insurance Clearance:

- Title company conducts a title search to confirm clear ownership

- Any liens, judgments, or title issues must be resolved

- Title insurance policy is issued to protect the lender's interest

- Hazard insurance policy is secured with the lender named as loss payee

- Proof of insurance is provided to the lender before closing

Final Document Preparation:

- Promissory note outlining loan terms, payment schedule, and maturity date

- Deed of Trust or Mortgage securing the property as collateral

- Personal guaranty from business entity owners

- Closing Disclosure (CD) detailing all loan costs, fees, and payment terms

- Assignment of renovation draws and disbursement schedule

The Closing Appointment:

Many hard money lenders offer mobile closings, sending a notary directly to your location for added convenience. You'll review and sign all closing documents, typically including:

- Promissory Note

- Deed of Trust/Mortgage

- Personal Guaranty

- Closing Disclosure

- Truth in Lending Disclosure

- Borrower's Certification and Authorization

- Disbursement Authorization for renovation funds

Fund Disbursement:

Here's how your funds will flow once you close:

Acquisition Funds:

- Wired directly to the title company or seller

- Covers the purchase price minus your down payment

- Usually disbursed within 24-48 hours of signing closing documents

Renovation Funds:

- Held in escrow by the lender or a third-party escrow company

- Released in draws as you complete renovation milestones

- Requires inspection and approval before each draw

- Keeps your project accountable and on budget

Typical Closing Timeline:

According to industry data, hard money loans can close remarkably fast when you come prepared. With complete documentation and clear title, you could be closing in as little as 5-7 days from application. More complex deals or those requiring additional due diligence might take 10-14 days—still a fraction of the 30-60 days you'd wait with conventional mortgages.

OfferMarket's Closing Efficiency:

Our integrated platform removes the typical bottlenecks:

- Coordinated Insurance: We provide insurance quotes in-house, so you won't face delays hunting down proof of coverage

- Title Relationships: Our established partnerships with title companies in key markets mean faster title work and quicker issue resolution

- Digital Document Management: Review and prepare your documents through our secure online portal before your signing appointment

- Dedicated Support: Your assigned relationship manager coordinates all parties and keeps everything moving smoothly

Post-Closing: Getting Started on Your Project:

Once you've closed, it's time to roll up your sleeves and start your renovation. Understanding the draw process is crucial:

Draw Request Process:

- Complete a phase of work according to your approved SOW

- Submit a draw request with photos documenting completed work

- Lender or third-party inspector verifies work completion

- Funds are disbursed (typically within 24-48 hours of approval)

- Repeat for each subsequent phase until renovation is complete

Best Practices:

- Document everything with photos and receipts

- Stay in communication with your lender throughout the project

- Submit draw requests promptly to maintain cash flow

- Alert your lender immediately if scope changes are needed

Pro Tip:

Schedule your closing for early in the week (Monday or Tuesday) to ensure funds disburse before the weekend. This gives you a head start on work and helps you make the most of your loan term.

Getting Your Hard Money Loan Faster

Want to move through these steps quickly? Here's how to set yourself up for success:

Before You Find a Property:

- Form your business entity and gather all formation documents

- Build your investor resume with photos and details of past projects

- Connect with reliable contractors who can turn around quick estimates

- Get pre-qualified with lenders so you know exactly what you can borrow

When You Find a Property:

- Order a pre-inspection to catch major issues before making an offer

- Pull comparable sales to confirm your ARV numbers make sense

- Get contractor estimates as soon as you go under contract

- Submit your loan application within 24 hours of contract acceptance

During the Process:

- Respond to lender requests the same day whenever possible

- Provide complete documentation upfront rather than piecemeal

- Be available for phone calls and questions from underwriting

- Work with your title company to keep title work moving

When you understand each step and prepare ahead of time, you can move through the hard money loan process smoothly and close deals fast—even in competitive markets. OfferMarket's streamlined, technology-driven approach combined with comprehensive market insights makes this process even faster and more predictable for real estate investors. The result? Most median hared money loans closes in 16 days from application to funding—and you can see the proof yourself inside your Loan File. Just open the Closing tab to access your transparent Closing Calendar, where key milestones—like loan application, credit report, appraisal, underwriting, insurance, title work, and final approval—are mapped out with target dates. As each milestone is completed, you can track whether you're on pace or ahead of schedule with the “Ahead +X” indicator, which shows how many days faster you’re progressing. The quicker each milestone is completed, the more that number increases—automatically pulling your projected closing date closer.

Benefits & Risks of Hard Money Loans

Hard money loans fill a specific gap in real estate financing—and they do it well. They offer clear advantages that make them a go-to choice for certain investors, but they also come with challenges you'll want to think through carefully. Let's break down both sides so you can decide when this tool belongs in your toolkit.

Key Benefits

Speed-to-Market Advantage

Here's where hard money really shines. In a hot market, the investor who can close fast wins the deal. Hard money lenders typically get you to the closing table in 7-14 days. Compare that to the 30-60 day timeline for conventional financing, and you can see why speed matters. This speed advantage allows you to make cash-equivalent offers on properties, dramatically increasing your competitiveness when bidding on distressed properties, foreclosures, or time-sensitive opportunities.

Here's a real-world example: A wholesaler brings you an off-market property with significant equity potential, but they need to close within 10 days. Traditional bank financing simply cannot accommodate this timeline, but a hard money lender can. This speed-to-market capability has helped countless investors build their portfolios by accessing deals that slower-moving competitors simply miss out on.

Bypass Rigid Personal Income Verifications

Unlike conventional mortgages that scrutinize your W-2s, tax returns, and debt-to-income (DTI) ratios, hard money lenders focus primarily on the asset itself—the property and the deal's economics. This fundamental difference opens doors for you if you have excellent real estate acumen but don't fit the traditional lending mold.

Whether you're self-employed, an entrepreneur with complex tax returns showing minimal taxable income, or someone who has recently changed careers, you can access hard money financing without the mountain of personal income documentation banks require. What matters most to the lender is whether the property's after-repair value (ARV) and your renovation plan create a solid path to profitability.

High Leverage

Here's where things get exciting: hard money lending offers access to high leverage ratios—up to 90% loan-to-cost (LTC) and 100% of the renovation budget. This capital efficiency means you can control more properties with less of your own money, significantly amplifying your potential returns.

Let's break this down with a simple example. Say you're looking at a $200,000 purchase with a $50,000 renovation budget. A hard money lender offering 90% LTC and 100% rehab financing would provide $230,000 ($180,000 for acquisition + $50,000 for renovation). Your out-of-pocket? Just $20,000 as a down payment. This leverage frees up your capital so you can tackle multiple projects at once or keep reserves on hand for those unexpected expenses that always seem to pop up.

The ability to finance your entire renovation budget is a game-changer. Here's the truth: many investors don't struggle with buying properties—they struggle with funding the improvements that unlock real value. Hard money lenders solve this challenge by providing phased draws throughout your renovation, ensuring you have the capital you need to see the project through to completion.

Access to Distressed Properties

Traditional lenders tend to avoid properties in rough shape. They often require homes to be "habitable" or meet specific condition standards before they'll approve financing. This restriction cuts you off from some of the most profitable opportunities out there—distressed properties you can purchase well below market value.

Hard money lenders specialize in financing exactly these types of properties. They get it: a property's current condition matters far less than its potential value after renovation. Whether you're eyeing a fire-damaged home, a property with major structural issues, or a complete gut rehab, hard money lenders evaluate your deal based on the ARV, not the as-is condition.

This access to distressed properties opens the door to substantial profits. The most successful fix-and-flip investors consistently go after properties that traditional buyers and conventional financing simply can't touch. Hard money lending makes these deals possible for you.

Scalability Without DTI Limits

Conventional financing comes with strict debt-to-income ratio requirements, typically capping you at 43-50% DTI. If you're an active investor building a portfolio, these limits become a roadblock fast. Every property you finance conventionally adds to your debt load, and eventually you hit a ceiling that stops your growth—no matter how successful you've been or how much capital you have available.

Hard money lending removes this obstacle. Because lenders focus on the asset rather than your personal income, you can scale your portfolio without bumping into DTI ceilings. Experienced investors often maintain multiple simultaneous hard money loans, something virtually impossible with conventional financing. This scalability is a game-changer for investors pursuing the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) or running multiple fix-and-flip projects at the same time.

Minimal Documentation

Yes, hard money loans do require documentation—business entity formation papers, identification, scope of work, and proof of funds—but the process is far more streamlined than conventional mortgages. You won't need to dig up extensive employment verification, multiple years of tax returns, detailed explanations of every bank deposit, or lengthy letters explaining credit inquiries.

This simplified approach speeds up the approval process and takes a huge administrative weight off your shoulders. Many hard money lenders provide preliminary approval within 24-48 hours of application, with final approval hinging primarily on the property appraisal and title clearance.

Potential Risks

Short Maturities with Default Risk

Hard money loans typically carry 12-month terms, though some lenders offer extensions to 18-24 months for complex projects involving heavy additions or conversions. While these short terms work well for the fix-and-flip timeline, they create real risk if your project hits delays.

And let's be honest—construction delays happen for all kinds of reasons: permit issues, contractor problems, material shortages, unexpected structural discoveries, or market slowdowns affecting your sale timeline. If your project extends beyond the loan maturity date, you're looking at some challenging scenarios:

- Extension Fees: Many lenders charge 1-2% of the loan amount for extensions, plus potentially higher interest rates during the extension period.

- Forced Sale: You may need to sell the property before renovations are complete or before market conditions are ideal, cutting into your profit margin.

- Default: If you cannot secure an extension or complete the project, the lender may initiate foreclosure proceedings.

According to industry analysis, defaulting on a hard money loan means you'll face costs beyond what you originally agreed to—think higher interest rates and extra fees. The good news? You can manage this risk with realistic project planning, keeping solid reserves on hand, and mapping out a clear exit strategy before you sign on the dotted line.

Higher Interest Rates

Hard money loans come with higher interest rates than traditional mortgages—usually 8-12% versus 6-7% for conventional financing. Why the premium? Lenders are taking on more risk by financing distressed properties, closing quickly, and offering higher leverage ratios.

Here's the thing: context is everything. Hard money is a short-term tool built for projects that wrap up in months, not years. Run the numbers on a 12-month loan: the difference between an 8% hard money rate and a 6% conventional rate on $200,000 comes out to roughly $4,000. That's often a fair trade for the speed, flexibility, and leverage you're getting.

And here's something worth noting: higher interest rates haven't put the brakes on hard money lending. Investors clearly see the value, even with the added cost. Your job? Make sure your project's profit margin can handle these expenses and still deliver the returns you're after.

Origination Fees

Most hard money lenders charge origination fees—typically 1-2% of your loan amount—due upfront at closing. Let's put that in real terms: on a $250,000 loan, a 2% fee means $5,000 out of pocket right away. That's money that won't be available for your project, so factor it into your profitability calculations.

These fees usually aren't up for negotiation, though some lenders might budge based on loan size, your track record, or how strong the deal looks. Pro tip: when you're shopping around, don't just compare interest rates. Look at the total cost of capital—origination fees, extension fees, and any other charges that might pop up.

Transparent lenders like OfferMarket show you every fee upfront—no surprises for application processing, courier services, wire transfers, or document prep. Always ask for complete fee transparency and build these costs into your deal analysis before signing with any lender.

Smart Deal Analysis with ROI Requirements

Here's the good news: hard money lenders won't dig into your personal income like traditional banks do. But they will take a close look at your deal's numbers. Most lenders want to see projects hitting minimum ROI thresholds—typically 20-30% return on investment after all costs—before they'll approve your financing.

If your projected numbers fall short, here's what might happen:

- Lower loan amount: You'll need a bigger down payment to strengthen the deal's risk profile.

- Additional reserves required: The lender wants to see buffer capital for those unexpected costs.

- Loan declined: Sometimes the numbers just don't work for the risk involved.

Think of this scrutiny as a safety net for both of you. A lender passing on a marginal deal might actually be doing you a favor. That said, this means you won't be able to finance every property you come across—only the ones with solid profit potential that meet underwriting standards.

Understanding Your True Cost of Capital

Add up the higher interest rates, origination fees, potential extension fees, and interest reserves, and hard money can get expensive—especially if your project hits delays or margins tighten. That $50,000 profit you projected? It can shrink fast if renovation costs run $15,000 over budget and your timeline stretches three extra months.

When you factor in all fees, the total cost of capital on a hard money loan typically runs 12-18% annually—quite a bit higher than just the stated interest rate. Smart investors bake these costs into their deal analysis from day one, making sure there's enough profit margin to handle both the expected and the unexpected.

Real-World Scenarios: When Hard Money Makes Sense

Scenario 1: The Off-Market Opportunity

Sarah, a seasoned investor, found a distressed property listed on OfferMarket marketplace at $180,000. The property needs $60,000 in renovations and has an ARV of $320,000. The wholesaler needs to close in 10 days.

Sarah runs the numbers using OfferMarket's maximum allowable offer calculator and sees a potential profit of $50,000 after all costs, including hard money financing. She got a quote from OfferMarket Capital offering 90% LTC and 100% rehab funding, meaning she only needs $18,000 to get started. The loan closes in 12 days, she wraps up renovations in 4 months, and sells the property in month 5 for $315,000.

Total hard money costs (interest, origination, and fees): $18,000. Net profit: $47,000 on an $18,000 investment in 5 months—that's a 261% annualized return.

When hard money makes sense: Time-sensitive deals with solid profit margins where speed matters and your project timeline is realistic.

Scenario 2: The BRRRR Strategy

Marcus buys a property for $150,000 cash, puts $50,000 into renovations, and rents it for $1,800/month. After the rehab, the property appraises at $280,000. He taps into a hard money lender's "delayed financing" exception to refinance and pull out $224,000 (80% LTV), getting back his entire $200,000 investment plus an extra $24,000.

Now he owns a cash-flowing rental with zero dollars tied up in the deal—and his original capital is ready for the next opportunity. Hard money costs: roughly $8,000 in fees and interest for the 60-day refinance process.

When hard money makes sense: BRRRR investors who want to recycle capital quickly without waiting out conventional seasoning periods, particularly when rental income and ARV support the refinance.

Scenario 3: The Portfolio Constraint

Jennifer has flipped 15 properties successfully but has hit her DTI ceiling with conventional lenders. She spots a great opportunity but can't qualify for traditional financing because of her existing debt load. Hard money financing gets her in the door, she completes the project in 6 months, and walks away with a $40,000 profit.

When hard money makes sense: Experienced investors ready to scale beyond conventional lending limits who have solid track records and steady deal flow.

When Hard Money Might Not Be the Best Option

Scenario 1: The Marginal Deal

Tom finds a property for $220,000 requiring $80,000 in renovations with an ARV of $330,000. After calculating hard money costs, holding costs, selling expenses, and renovation costs, his projected profit is $15,000—only a 5% return on the total project cost.

Here's the reality: those thin margins leave zero wiggle room. If renovations run $10,000 over budget or the sale drags on an extra two months, Tom could break even—or worse, lose money. The higher cost of hard money financing simply makes this deal too risky to pursue.

When to avoid hard money: Deals with slim profit margins that can't absorb the higher cost of capital or those unexpected surprises that pop up.

Scenario 2: The Extended Timeline

Rachel has her eye on a property needing major structural work—foundation repair and an addition that'll take 10-12 months to complete. Here's the catch: hard money loans typically mature in 12 months, and let's be honest, complex projects almost always hit delays.

The risk of needing an extension—with those extra fees and higher rates—makes hard money a poor fit here. Rachel's better off exploring construction financing with longer terms or holding off until conventional financing becomes an option.

When to avoid hard money: Projects stretching beyond 12 months where extension risks and added costs outweigh the advantages.

Scenario 3: The First-Time Investor

David's eager to dive into real estate investing but has never tackled a renovation project. He spots a property needing significant work and applies for hard money financing. The challenge? His lack of experience means he only qualifies for 75% LTC instead of 90%, requiring a much bigger down payment. Plus, his renovation budget might be off-base and his timeline overly optimistic.

When you combine lower leverage, higher costs, and limited experience, you've got a recipe for substantial risk. David's smarter move? Start smaller with conventional financing or team up with a seasoned investor before tapping into hard money.

When to avoid hard money: First-time investors without proven track records, realistic budgets, or adequate reserves to handle unexpected challenges.

Making Smart Choices

Hard money lending isn't good or bad—it's simply a tool that works brilliantly for certain situations and not so well for others. The secret to using it wisely? Being honest with yourself:

- Do you have a time-sensitive opportunity that requires quick closing?

- Does your deal have sufficient profit margin to absorb the higher cost of capital?

- Can you realistically complete the project within 12 months?

- Do you have adequate reserves for unexpected expenses?

- Is your exit strategy clear and achievable?

If you're nodding yes to these questions, hard money financing can be a game-changer for building wealth through real estate. If you're shaking your head no to several, it might be worth exploring other financing routes or holding out for a deal that plays to hard money's strengths.

The savviest investors treat hard money as one piece of a bigger financing puzzle, deploying it strategically for the right projects while keeping doors open with conventional lenders, private money sources, and other capital partners. This balanced approach gives you maximum flexibility with minimum risk, setting you up for lasting success in real estate investing.

OfferMarket's Unique Competitive Advantage: An Integrated Platform for Real Estate Investors

Most hard money lenders stick to one thing: originating loans. OfferMarket took a different path. We've built a comprehensive, integrated platform that brings together the three essential services real estate investors actually need: loans, listings, and insurance. This three-pillar approach isn't just convenient—it's your competitive edge. It means better deals, faster closings, and smarter financing, whether you're just starting out or you've been investing for years.

The Power of Integration: Beyond Traditional Lending

Here's the thing about traditional hard money lenders: they only see what comes through their door via marketing or broker connections. OfferMarket flips that script. Our integrated model tears down those walls, creating what Berkadia calls "aligned incentives"—meaning "the broker understands your investment thesis and capital requirements from day one, avoiding mismatched loan terms." That changes everything about how lending decisions happen and how fast you can access capital.

When brokerage, lending, and insurance work together, something powerful happens. Each piece shares insights with the others, building a platform that gets the full picture—not just single transactions, but your entire investment journey. What does that mean for you? Faster, smarter lending decisions, plus help finding better opportunities and protecting what you've built.

Comprehensive Insurance Solutions: Protecting Your Investment

Real estate investment doesn't end when the loan closes—protecting your asset through appropriate insurance coverage is critical to long-term success. OfferMarket's integrated insurance services give you expert guidance and one-stop convenience that standalone lenders simply can't match:

Comprehensive Coverage Quotes: We don't leave you to figure out the insurance maze on your own. OfferMarket delivers insurance quotes right alongside your financing package. That means you see your true all-in costs from the start—loan payments and insurance premiums together. No surprises. This clarity helps you decide which properties make sense and how to structure your deals with confidence.

Right-Sized Protection: Here's a mistake we see all the time: investors either over-insure or under-insure their properties. Over-insurance drains your capital on premiums you don't need. Under-insurance? That can be devastating when a claim hits. We make sure your coverage fits your property's value, use case, and risk profile. Whether you're holding a vacant property during renovation, waiting to sell a completed flip, or collecting rent, we help you lock in the right coverage at the right price.

Expertise in Complex Insurance Documents: Let's be honest—insurance policies are packed with exclusions, endorsements, and fine print that can make your head spin. Our team knows how to navigate these documents so you understand exactly what's covered and what's not. This matters especially during renovations, when your coverage needs shift as the property moves from vacant to under construction to finished. We help you manage those transitions seamlessly, so you're never caught with a gap in protection.

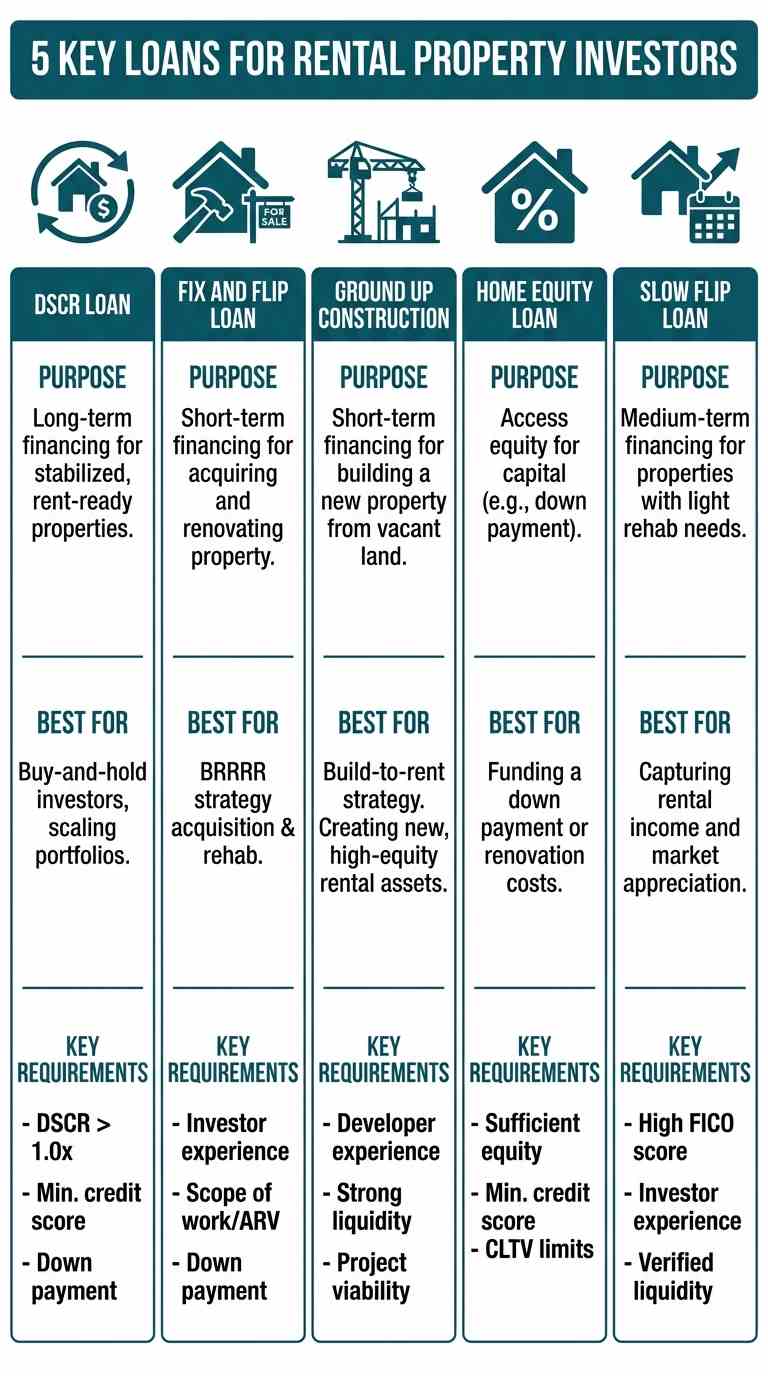

Wider Selection of Loan Products: Tailored Solutions for Every Strategy

Most single-service lenders offer one or two loan products. We work with multiple capital providers to bring you a full range of financing options tailored to your strategy. This partnership approach means investors can access the right capital for their specific strategy, whether they're just starting out or managing a large portfolio:

Fix and Flip Loans: These are your classic hard money loans built for the buy-renovate-sell playbook. You're purchasing a distressed property, putting in the work, and selling for profit. Expect high leverage (up to 90% LTC), 100% renovation funding, and terms that typically run 12-18 months—enough time to get in, transform the property, and get out with your returns.

DSCR Loans: Ready to shift from flipping to holding? Debt Service Coverage Ratio loans qualify based on what the property earns in rent, not what you earn personally. That's a game-changer when you're building a rental portfolio and your tax returns don't tell the whole story.

Slow Flip Loans: Some projects need more runway. These extended-term loans (18-24 months) are designed for complex renovations—think additions, conversions, or properties tangled up in permitting and approval processes. More time means less pressure to cut corners.

Low Balance DSCR Loans: Got your eye on a smaller rental property? Loans under $100,000 often get ignored by traditional lenders because they're costly to service. We see the opportunity others overlook.

HELOANs (Home Equity Loans): Tap into the equity you've already built. These fixed-rate, fixed-term loans are secured by your primary residence or existing rentals, giving you capital for down payments or renovation costs without touching your current mortgage.

These product diversity means OfferMarket can match you with the optimal financing structure for your specific situation, rather than forcing every deal into a one-size-fits-all product. An investor purchasing their first property might use a fix-and-flip loan, while a more experienced investor with multiple properties might leverage a HELOAN for down payments and a DSCR loan for long-term rental property financing.

The Result: Smoother, Faster, and More Cost-Effective Lending

When everything works together on one platform, you get real advantages that hit your bottom line. Research on marketplace lending benefits highlights that "speed – loan approval is substantially faster than the traditional bank" and "convenience – online applications and uploading supporting documents" are key advantages of platform-based lending approaches.

Faster Closings: Streamlined underwriting, built-in insurance quoting, and solid relationships with title companies and appraisers all add up to one thing: you close faster. We're talking 14-21 days instead of 30-60. In a competitive market where multiple investors are eyeing the same property, that speed advantage can be the difference between landing the deal and watching someone else walk away with it.

Potentially Lower Overall Costs: Interest rates and origination fees matter, but they're not the whole picture. The true cost of capital includes every expense tied to getting and managing your loan. OfferMarket's all-in-one approach cuts friction at every turn—finding properties, securing financing, obtaining insurance—which means fewer delays, lower soft costs, and better returns. Plus, with access to multiple capital providers, you get matched with the right loan product for your situation. No paying for features you don't need or settling for terms that don't fit.

Holistic Support: Here's what really sets OfferMarket apart: our integrated model gives you a single point of contact who truly gets your entire investment strategy—not just your immediate financing needs. This relationship-focused approach, backed by deep platform insights, turns what could be a simple transaction into a genuine partnership. As you grow and scale your portfolio, OfferMarket becomes your trusted guide on market selection, property evaluation, financing structure, and risk management—all powered by data and insights from across our platform.

In real estate investing, speed, accuracy, and cost-efficiency directly impact your bottom line. OfferMarket's integrated platform represents a smarter way for investors like you to access capital and execute your strategies. By bringing loans, listings, and insurance together in one cohesive ecosystem, we deliver advantages that single-service lenders simply can't offer.

Take the First Step Today

You now have the knowledge, the checklist, and the roadmap to secure hard money financing for your investment projects. The question is: what's your next move?

Get your instant quote from OfferMarket today. In just minutes, you'll see exactly what financing you qualify for, including your interest rate, loan amount, and monthly payments. There's no obligation, no credit impact, and no reason to wait.

Once you see your numbers, you can:

- Evaluate deals with confidence, knowing your exact financing capacity

- Make competitive offers on properties, backed by pre-qualification

- Build relationships with wholesalers and agents who know you're a serious buyer

- Create your Loan File and move to processing when you find the right opportunity

The properties you're considering won't wait. Competitive deals move quickly, and investors who can act fast—backed by reliable financing—are the ones who build successful portfolios.

Start your application with OfferMarket now and join the thousands of investors who have discovered that hard money financing isn't just accessible—it's the competitive advantage that transforms real estate investing from a side interest into a profitable business.

Your first deal is waiting. Your financing is ready. The only question left is: are you?

OfferMarket Loans

Check your rate

60 seconds · no credit pull