*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How a HELOC Works

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by the equity you've built in your property—functioning much like a credit card, but with your real estate as collateral. For real estate investors and landlords, understanding the mechanics of a HELOC is essential before considering it as a financing tool for your portfolio.

![**Task**: Create an educational infographic that visually explains the two-phase structure of a HELOC, showing the draw period and repayment period with clear visual distinction and timeline representation.

**Visual Structure**: A horizontal timeline infographic divided into two major sections (draw period and repayment period) with icons, descriptive text boxes, and visual indicators showing the key differences between each phase.

**ASCII Layout Reference**:

```

┌─────────────────────────────────────────────────────────────────────┐

│ HOW A HELOC WORKS: TWO PHASES │

├──────────────────────────────────┬──────────────────────────────────┤

│ DRAW PERIOD (10 YEARS) │ REPAYMENT PERIOD (10-20 YEARS) │

│ │ │

│ [CREDIT CARD ICON] │ [CLOSED LOCK ICON] │

│ Borrow & Repay Freely │ No More Borrowing │

│ │ │

│ Interest-Only Payments │ Principal + Interest │

│ Variable Rate │ Variable Rate Continues │

│ Flexible Access │ Payment Shock Common │

│ │ │

│ Example: $30,000 balance │ Example: $30,000 balance │

│ Monthly: ~$188 │ Monthly: ~$280 │

│ (at 7.5% interest) │ (at 7.5% over 15 years) │

└──────────────────────────────────┴──────────────────────────────────┘

```

**Image Section Breakdown**:

*Header Section*:

- Background: Deep Teal (#1b444a)

- Text:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772645041407_2t3d45.jpg?alt=media&token=91e84fbb-128b-4e68-8bde-c79a22753408)

Before we begin, a word of caution

If you're a real estate investor or landlord looking to leverage the equity in your properties, you've probably encountered the term "HELOC" (Home Equity Line of Credit). At first glance, a HELOC might seem like an attractive financing option—flexible access to capital, the ability to draw funds as needed, and interest-only payments during the draw period. But for serious real estate investors focused on portfolio growth, HELOCs often create more problems than they solve.

This comprehensive guide will walk you through exactly how a HELOC works, from the mechanics of the draw and repayment periods to the critical pitfalls that can derail your investment strategy. More importantly, we'll explain why experienced investors typically choose Home Equity Loans (HELOANs) instead—and how OfferMarket's HELOAN program provides a superior alternative designed specifically for real estate professionals.

Whether you're considering your first equity-based financing or you're a seasoned investor evaluating your options, understanding the full picture of how HELOCs function—and their limitations—is essential for making informed decisions that support your long-term wealth-building goals.

The Basic Structure: Two Distinct Phases

Unlike investor focused loans that provide a lump sum upfront, a HELOC operates in two distinct phases that fundamentally change how you access and repay funds.

The Draw Period: Your Access Window

During the draw period, which typically lasts 10 years (though some lenders offer 5, 7, or 15-year options), you have the flexibility to borrow money as needed up to your pre-approved credit limit. This is the "revolving" aspect—you can draw funds, repay them, and draw again, similar to how you'd use a credit card.

Most lenders structure payments during this phase as interest-only, meaning you're only required to pay the interest charges on your outstanding balance each month, not the principal. For example, if you have a $100,000 HELOC but have only drawn $30,000, your monthly payment is calculated only on that $30,000 balance.

The Repayment Period: When Everything Changes

After the draw period ends, your HELOC enters the repayment period, which typically spans 10 to 20 years. During this phase, three critical changes occur:

- You can no longer draw additional funds from the credit line

- Your outstanding balance converts into a fully amortizing loan

- Your monthly payments now include both principal and interest

This transition often results in "payment shock"—a sudden and substantial increase in your monthly obligation. What was once a manageable interest-only payment can double or triple overnight as you begin paying down the principal over the remaining term.

Variable Interest Rates: The Moving Target

One of the most significant characteristics distinguishing HELOCs from investor focused loans is the variable interest rate structure. HELOC rates are tied to a benchmark index, most commonly the U.S. Prime Rate, plus a margin determined by the lender based on your creditworthiness and loan-to-value ratio.

This means your interest rate—and consequently your monthly payment—can fluctuate throughout the life of the loan. When the Federal Reserve adjusts rates, your HELOC rate typically adjusts within one to two billing cycles. In the current market, HELOC rates have dropped to an average of 8.56%, representing the lowest point in 2024, but these rates remain subject to change based on economic conditions.

For real estate investors accustomed to modeling cash flows and calculating returns, this variability introduces a level of uncertainty that can complicate financial projections. A rate increase of just 1-2% can significantly impact your monthly carrying costs and overall investment returns.

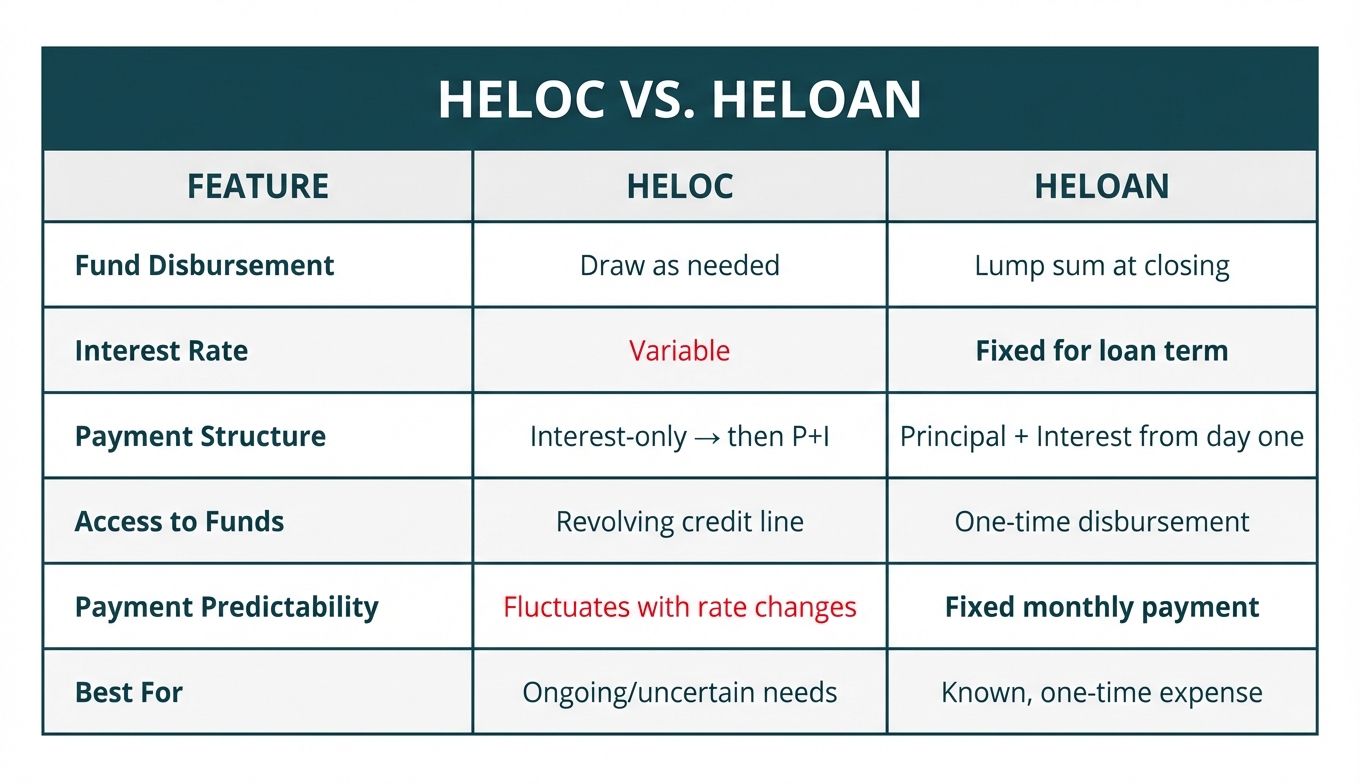

How HELOCs Differ HELOAN

To fully appreciate how a HELOC works, it's helpful to contrast it with a traditional home equity loan or mortgage:

This fundamental difference in structure explains why HELOCs have gained popularity among some homeowners—the flexibility to access funds only when needed can be appealing. However, for professional real estate investors, this same flexibility often introduces complications that can hinder portfolio growth and limit future financing options, as we'll explore in later sections.

Understanding these basic mechanics is just the beginning. The real complexity—and potential pitfalls—emerge when you examine how HELOCs interact with your broader investment strategy and future financing capabilities.

Why Real Estate Investors Often Prefer HELOANs Over HELOCs

For real estate investors, the choice between a HELOC and a HELOAN isn't just about accessing equity—it's about strategic portfolio management and predictable financial modeling. While HELOCs offer flexibility that appeals to homeowners managing personal expenses, experienced real estate investors typically gravitate toward HELOANs for reasons that directly impact their bottom line and growth trajectory.

The Cash Flow Predictability Advantage

Real estate investing is fundamentally a numbers game. Every successful investor builds detailed financial models that project income, expenses, and returns over specific timeframes. This is where the structural differences between HELOCs and HELOANs become critical.

A HELOAN provides a fixed, lump-sum payment at closing—exactly what you need to close on a new investment property, fund a complete renovation, or execute a strategic portfolio move. More importantly, that lump sum comes with a fixed interest rate for the entire life of the loan and a fully amortizing payment schedule that never changes. You know on day one exactly what your monthly payment will be in month 60, month 120, or any point until the loan is paid off.

This predictability is invaluable when you're calculating the return on investment for a rental property. Consider a typical scenario: You're analyzing a potential rental property that will generate $2,500 in monthly rent. You need to account for your mortgage payment, property taxes, insurance, maintenance reserves, and the payment on the HELOAN you'll use for the down payment. With a HELOAN's fixed payment, you can model your cash flow with confidence. If your HELOAN payment is $450 per month today, it will be $450 per month five years from now, regardless of what happens with interest rates.

Contrast this with a HELOC's variable rate structure. Your payment fluctuates with market conditions, making it nearly impossible to create reliable long-term projections. During the interest-only draw period, you might pay $200 one month and $275 the next as rates adjust. When the repayment period begins, you face payment shock—a dramatic increase that can disrupt carefully planned cash flow strategies. For an investor managing multiple properties and leveraging equity strategically, this unpredictability introduces unnecessary risk into financial planning.

The fixed-rate structure of a HELOAN also simplifies analysis for fix-and-flip projects. When you're calculating your holding costs—the total expenses you'll incur while renovating and marketing a property—you need precise numbers. A HELOAN allows you to know exactly what your financing will cost over your projected six-month or twelve-month hold period. This certainty directly impacts your maximum allowable offer on a property and your profit projections.

Superior Qualification Pathways for Investment Properties

Perhaps the most significant advantage HELOANs offer real estate investors isn't about the loan structure itself—it's about how you qualify for the financing. This is where the investor-focused HELOAN market has evolved far beyond traditional HELOC products.

Standard HELOCs almost universally require full documentation underwriting. Lenders want to see W-2s, tax returns, pay stubs, and detailed verification of your personal income. For traditional employees with straightforward income, this might be manageable. But for real estate investors—particularly those who are self-employed, own multiple properties, or strategically minimize taxable income through depreciation and other tax strategies—this documentation requirement becomes a significant barrier.

According to recent industry data, home equity lending has grown significantly, with more sophisticated products emerging to serve investor needs. Investor-focused HELOANs, such as those offered through specialized programs, provide qualification pathways specifically designed for real estate professionals.

DSCR (Debt Service Coverage Ratio) Qualification represents one of the most powerful tools available to real estate investors. Rather than scrutinizing your personal income, DSCR loans qualify you based on the subject property's rental income and its ability to cover all property-related expenses. The lender analyzes the property's rent roll and calculates whether the rental income sufficiently covers the proposed loan payment, property taxes, insurance, and HOA fees.

For example, if a property generates $3,000 in monthly rent and the total monthly obligations (including your new HELOAN payment) equal $2,400, you have a DSCR of 1.25—meaning the property generates 25% more income than needed to cover expenses. Most DSCR programs require a ratio of 1.0 or higher, though some allow ratios as low as 0.75 for experienced investors with strong compensating factors.

This qualification method is transformative for investors because it focuses on what truly matters: the property's ability to generate income. Your personal tax returns, which might show minimal income due to depreciation write-offs, become irrelevant. The investment property is underwritten on its own merits.

Bank Statement Loan Programs offer another sophisticated qualification pathway unavailable with traditional HELOCs. These programs allow self-employed investors to qualify based on deposits into business or personal bank accounts rather than tax returns. The lender analyzes 12 or 24 months of bank statements, applies a reasonable expense ratio (typically 25-50% depending on the program), and calculates your qualifying income from the net deposits.

For a real estate investor who operates as an LLC, receives rental income through multiple entities, or earns income from property management, wholesaling, or other real estate activities, bank statement qualification can unlock financing that would be impossible to obtain through traditional documentation. Your actual cash flow—the money hitting your accounts each month—becomes the basis for qualification rather than what appears on a tax return designed to minimize tax liability.

These alternative qualification methods are rarely, if ever, available with standard HELOCs. The HELOC market remains largely focused on traditional W-2 employees and requires conventional income documentation. For professional real estate investors, this fundamental difference in underwriting philosophy makes HELOANs not just preferable but often the only viable option for accessing home equity to fuel portfolio growth.

The Strategic Advantage for Portfolio Scaling

When you're actively building a real estate portfolio, every financing decision impacts your ability to acquire the next property. Recent research shows that roughly 25% of homeowners are considering home equity products, but for investors, the choice of product can either accelerate or hinder growth.

A HELOAN's lump-sum structure aligns perfectly with how real estate transactions work. You need a specific amount for a down payment, and you need it available at closing. You're not making gradual draws over time—you're executing a single transaction that requires immediate access to capital. The HELOAN delivers exactly this: full funding at closing that you can deploy immediately into your next investment.

The fixed-rate structure also protects you during market cycles. Real estate investors often work on multi-year strategies, acquiring properties during market opportunities and holding through various economic conditions. A HELOAN locked at a fixed rate provides certainty regardless of what happens with the Federal Reserve's monetary policy or broader interest rate trends. You're insulated from rate increases that could erode the profitability of deals you've already structured.

For investors using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), a HELOAN can serve as bridge financing with predictable costs. You know exactly what your carrying costs will be during the renovation and stabilization period, allowing you to calculate your all-in costs precisely before you refinance into permanent financing.

The combination of predictable payments, investor-friendly qualification methods, and lump-sum funding makes HELOANs the preferred tool for serious real estate investors who are focused on portfolio growth, accurate financial modeling, and strategic leverage management. While HELOCs serve a purpose in personal finance, they simply don't align with the operational realities and financial sophistication required in professional real estate investing.

The OfferMarket HELOAN: Built for Investor Success

OfferMarket's HELOAN program is specifically designed to address the unique needs of real estate investors and landlords who are serious about portfolio growth. Unlike retail HELOC products that create barriers to scaling, our HELOAN solution provides:

- Fixed rates and predictable payments for accurate cash flow modeling

- True liquidity that qualifies as cash reserves for your next purchase

- Transparent CLTV calculations that preserve your future borrowing capacity

- Flexible qualification through DSCR programs

- Fast closing timelines to help you capitalize on time-sensitive opportunities

- No restrictions on fund usage for investment property purchases

The difference isn't just about accessing your equity—it's about accessing it in a way that empowers your growth strategy rather than limiting it.

Take the Next Step: See Your HELOAN Terms Today

If you're a real estate investor or landlord with equity in your properties and a vision for portfolio expansion, it's time to explore how a HELOAN can accelerate your growth while avoiding the pitfalls that HELOCs create.

Get your instant quote from OfferMarket today. In just minutes, you'll see your potential loan amount, interest rate, and monthly payment—with no impact to your credit score and no obligation. Our team specializes in working with real estate investors and understands the unique financial structures and goals that drive your success.

Don't let a HELOC's hidden limitations restrict your portfolio growth. Discover how OfferMarket's HELOAN can provide the stable, strategic financing solution that serious investors rely on to scale their real estate businesses.

Get Your Instant HELOAN Quote Now →

Your next investment property is waiting—and the right financing strategy can make all the difference between seizing the opportunity and watching it pass by.

The Investor's Trap: 3 Critical HELOC Pitfalls That Can Derail Your Portfolio Growth

For real estate investors building a portfolio, a HELOC might seem like the ultimate financial tool—flexible credit at your fingertips whenever opportunity knocks. But experienced investors know that HELOCs come with hidden landmines that can severely restrict your ability to scale. These aren't minor inconveniences; they're structural limitations that can prevent you from acquiring your next property, force you into unfavorable refinancing terms, or artificially inflate your debt ratios when you need flexibility most.

Let's examine three critical pitfalls that catch even sophisticated investors off guard, and why understanding these mechanics is essential before you sign on that dotted line.

Pitfall #1: The Leverage (CLTV) Penalty—Your Unused Credit Counts as Debt

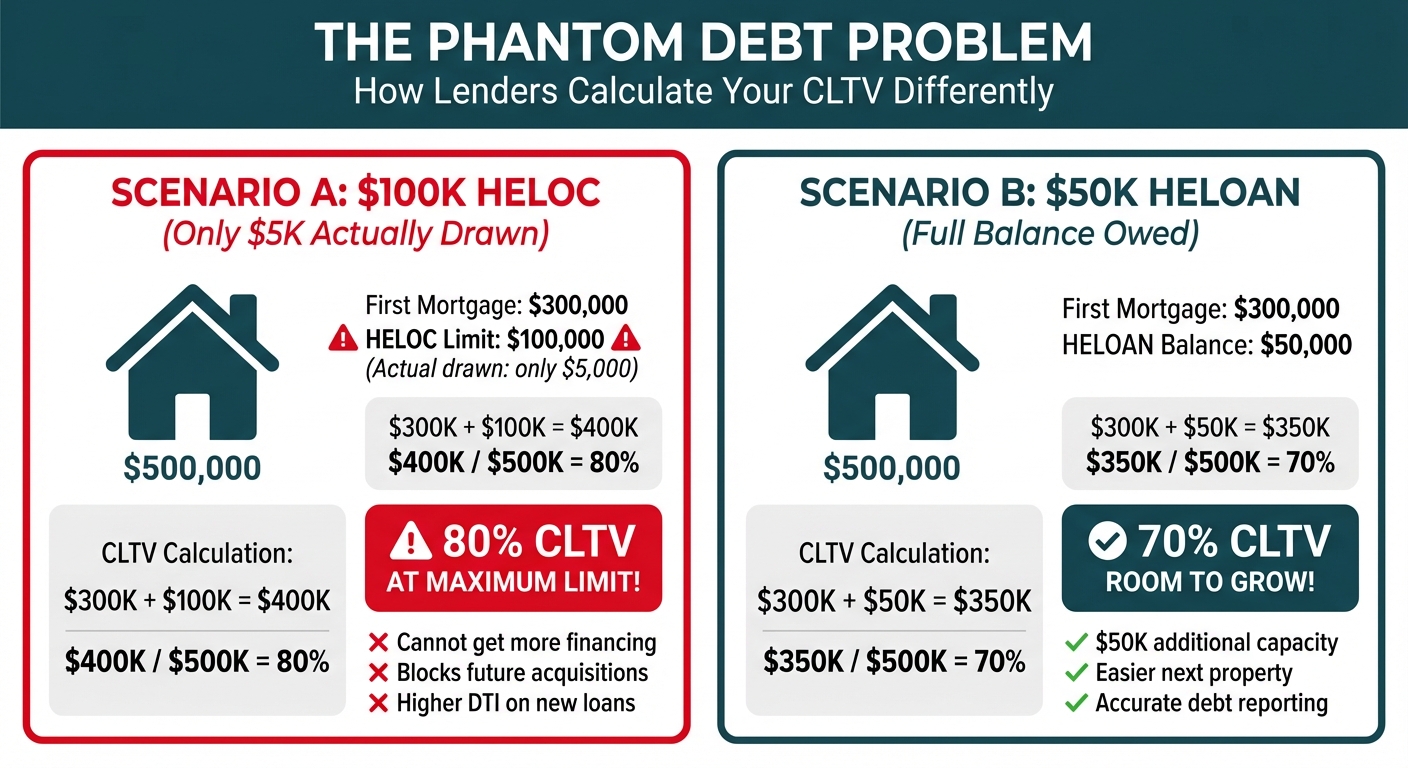

Here's a scenario that plays out constantly in underwriting offices: An investor applies for financing on a new rental property. They have a $100,000 HELOC on their primary residence but have only drawn $5,000 from it. They assume lenders will only count the $5,000 they actually owe. They're wrong.

When you apply for a new mortgage, lenders count your entire HELOC limit—not your current balance—as debt against that property.

This creates what I call the "phantom debt problem." Even though you haven't borrowed the money, underwriters must assume you could max out that credit line at any moment. From a risk management perspective, this makes sense for the lender, but it creates a massive constraint for investors trying to leverage their equity efficiently.

How the CLTV Calculation Works Against You

Let's walk through the math with a concrete example:

- Your home's current value: $500,000

- Existing first mortgage balance: $300,000

- HELOC limit: $100,000

- HELOC balance actually drawn: $5,000

When you apply for a loan on a new investment property, the lender evaluating your existing property will calculate:

CLTV = (First Mortgage + Total HELOC Limit) / Property Value

CLTV = ($300,000 + $100,000) / $500,000 = 80%

Notice they used the $100,000 limit, not the $5,000 balance. This matters enormously because most lenders cap investor loans at 75-80% CLTV when you have multiple properties. You've now hit that ceiling, meaning:

- You cannot take out additional financing against this property

- You cannot increase your HELOC limit

- Your debt-to-income ratio for qualifying on new conventional properties only includes the minimum monthly payment on your actual drawn balance (the $5,000)—not the full $100,000 limit. (If you use a DSCR loan, this personal debt is ignored entirely).

If you had instead taken a $50,000 HELOAN (fixed home equity loan) rather than a $100,000 HELOC, your CLTV would be calculated as:

CLTV = ($300,000 + $50,000) / $500,000 = 70%

This 10% difference in CLTV represents real borrowing capacity—potentially $50,000 in additional leverage you could access later when you need it for your next deal.

The Portfolio Impact

This penalty compounds as you scale. Each property with a HELOC artificially inflates your total leverage across your portfolio, making it progressively harder to qualify for additional acquisitions. Lenders aggregate these numbers, and suddenly you're hitting debt-to-income caps or portfolio loan limits not because of your actual debt, but because of unused credit lines.

For investors serious about scaling to 5, 10, or 20+ properties, this phantom debt can be the difference between approval and denial on your next deal.

Pitfall #2: The Liquidity Exclusion Rule—HELOC Funds Aren't "Real" Money to Lenders

This pitfall catches investors by surprise because it seems counterintuitive. You have $50,000 available on your HELOC. You draw it out and deposit it in your checking account. You now have $50,000 in cash. That should count as liquid reserves, right?

Wrong. Lenders explicitly prohibit you from using HELOC funds to satisfy reserve requirements or contribute to your cash-to-close on new property acquisitions.

Understanding Reserve Requirements

When you purchase an investment property, lenders require you to demonstrate "reserves"—liquid assets that could cover multiple months of mortgage payments (typically 3-6 months per property, increasing as you acquire more). These reserves prove you can weather vacancies, repairs, or economic downturns.

Acceptable reserve assets include:

- Checking and savings account balances

- Stocks, bonds, and mutual funds (typically counted at 70% of value)

- Retirement accounts like 401(k)s or IRAs (often counted at 60-70% due to early withdrawal penalties)

- Cash value of whole life insurance policies

Not acceptable:

- Funds drawn from a HELOC

- Funds drawn from a credit card cash advance

- Personal loans or lines of credit

Why Lenders Exclude HELOC Funds

From an underwriting perspective, HELOC funds represent borrowed money, not savings. If you use a HELOC to meet reserve requirements, you're essentially demonstrating reserves with debt—which defeats the entire purpose of the reserve requirement. Lenders need to see that you have genuine financial cushion, not that you can borrow your way through a rough patch (which would only increase your monthly obligations).

The same logic applies to your down payment and closing costs. If you show up to closing with $75,000 for a down payment, but the lender discovers through bank statements that this money came from a HELOC draw two weeks earlier, they'll reject it. You must demonstrate "sourced and seasoned" funds—money that's been in your account for at least 60 days and came from legitimate, non-borrowed sources.

The Strategic Implication

This creates a planning problem for investors who were counting on their HELOC as a liquidity tool for acquisitions. You might have $200,000 in available HELOC capacity across your properties, but none of it can be used to satisfy the two most critical financial requirements in a new purchase:

- Cash to close (down payment + closing costs)

- Post-closing reserves

This is why sophisticated investors often prefer a HELOAN structure. When you take a HELOAN, you receive a lump sum at closing. If you deposit this in your bank account and let it season for 60+ days, it becomes indistinguishable from any other cash savings—it's no longer classified as "borrowed funds" for the purpose of your next transaction. The debt is established, fixed, and factored into your DTI, but the cash becomes usable.

With a HELOC, you're perpetually in this gray zone where the funds are available but not truly usable for acquisition purposes, creating a false sense of liquidity.

Pitfall #3: The Cash-Out Refinance Trap—How HELOCs Trigger Worse Refinancing Terms

This is perhaps the most expensive pitfall because it affects the terms of what might be your largest loan. Here's the scenario: You have a first mortgage and a HELOC on a property. Interest rates drop, and you want to refinance your first mortgage to get a better rate. Simple enough, right?

Not quite. If you have an outstanding HELOC balance that you're paying off through the refinance, **your new loan will be classified as a "cash-out refinance" rather than a "rate-and-term refinance"**—and this classification costs you real money.

The Critical Difference Between Refinance Types

Rate-and-Term Refinance:

- Maximum LTV: Up to 75-80% for investment properties

- Interest rates: Standard pricing

- Underwriting: Standard requirements

- Purpose: Changing your interest rate, loan term, or switching from adjustable to fixed rate

Cash-Out Refinance:

- Maximum LTV: Typically capped at 70-75% for investment properties

- Interest rates: 0.25% to 0.75% higher than rate-and-term

- Underwriting: More stringent, higher reserves required

- Purpose: Extracting equity from the property

The difference in a 0.50% higher interest rate on a $400,000 loan costs you $2,000 per year, or $60,000 over a 30-year term. The lower maximum LTV might also mean you can't refinance at all if you're near the threshold, or you might be forced to pay down principal to qualify.

The Seasoning Requirements to Avoid Cash-Out Treatment

Fortunately, Fannie Mae and Freddie Mac have established specific guidelines that allow you to pay off a HELOC through a refinance and still receive rate-and-term treatment. According to Fannie Mae's guidelines, you must meet both of these conditions:

- The HELOC must be seasoned for at least 12 months (the HELOC was opened at least 12 months before your refinance application)

- You cannot have drawn more than $2,000 from the HELOC in the 12 months prior to your refinance

Let's break down why each requirement exists and how they create planning constraints.

The 12-Month Seasoning Requirement

The seasoning requirement prevents borrowers from opening a HELOC, immediately drawing funds, and then refinancing to convert that short-term borrowing into a long-term mortgage with better terms. Freddie Mac's refinance guidelines similarly require that the existing first lien mortgage be seasoned for at least 12 months when being paid off through a cash-out refinance.

For investors, this means you need to plan at least 12 months ahead. If you open a HELOC today, you cannot refinance your first mortgage and pay off that HELOC with rate-and-term treatment until at least a year has passed.

The $2,000 Draw Limit

This is the requirement that catches most people off guard. Even if your HELOC is five years old, if you've drawn more than $2,000 from it in the past 12 months, paying it off through a refinance triggers cash-out treatment.

The logic: if you've recently accessed equity through the HELOC, paying it off through a refinance is functionally equivalent to taking cash out—you're converting recently borrowed equity into your first mortgage.

This creates a planning dilemma. Let's say you have a HELOC with a $30,000 balance. Interest rates drop 1.5%, and you want to refinance. But you drew $10,000 from your HELOC eight months ago for a rental property repair. Now you have two options:

- Wait four more months until it's been 12 months since your last draw, then refinance with rate-and-term treatment

- Refinance now but accept cash-out refinance treatment with higher rates and lower max LTV

If rates are rising, waiting might cost you the opportunity entirely. If rates are stable or falling, waiting is clearly better—but you're stuck in limbo.

The Exception: Purchase-Related HELOCs

There is one important exception to these rules. If you used your HELOC as part of the original property purchase (for example, using a HELOC for the down payment in an 80-10-10 structure), you can pay it off through a rate-and-term refinance without meeting the seasoning and draw requirements. The logic here is that the HELOC was part of the original acquisition financing, not a subsequent equity extraction.

However, this exception is narrow and must be clearly documented. For most investors who opened a HELOC after purchasing the property, the standard rules apply.

Why This Matters for Portfolio Investors

As you scale your portfolio, you'll inevitably want to refinance properties—to lower rates, switch from adjustable to fixed, or remove PMI. If you have HELOCs attached to these properties, you're creating future refinancing constraints that might force you into unfavorable terms or prevent refinancing altogether.

Compare this to a HELOAN structure: The HELOAN is a separate second lien with a fixed balance. When you refinance your first mortgage, you can:

- Leave the HELOAN in place (subordination agreement allowing the new first mortgage to take priority)

- Pay off the HELOAN through the refinance without triggering cash-out treatment, since HELOANs don't have the same draw restrictions as HELOCs

This flexibility is invaluable when you're managing multiple properties and need to optimize your financing structure as market conditions change.

These three pitfalls—phantom debt from unused credit limits, inability to use funds for reserves or acquisitions, and cash-out refinance treatment—represent structural disadvantages that compound over time. For investors building serious portfolios, these aren't theoretical concerns; they're real constraints that affect deal flow, borrowing capacity, and overall returns.

This is precisely why experienced investors often prefer fixed home equity loans (HELOANs) over HELOCs. The predictability, cleaner underwriting treatment, and absence of these structural traps make HELOANs a more efficient tool for portfolio scaling—even if they seem less flexible on the surface.

The HELOC Process: A Deeper Dive

Understanding how a HELOC actually works requires breaking down its lifecycle into distinct phases and understanding the mechanics that govern your borrowing capacity. Unlike a traditional loan where you receive a lump sum, a HELOC operates more like a credit card secured by your home—but with significantly more complex rules and calculations.

Let's work through a practical example:

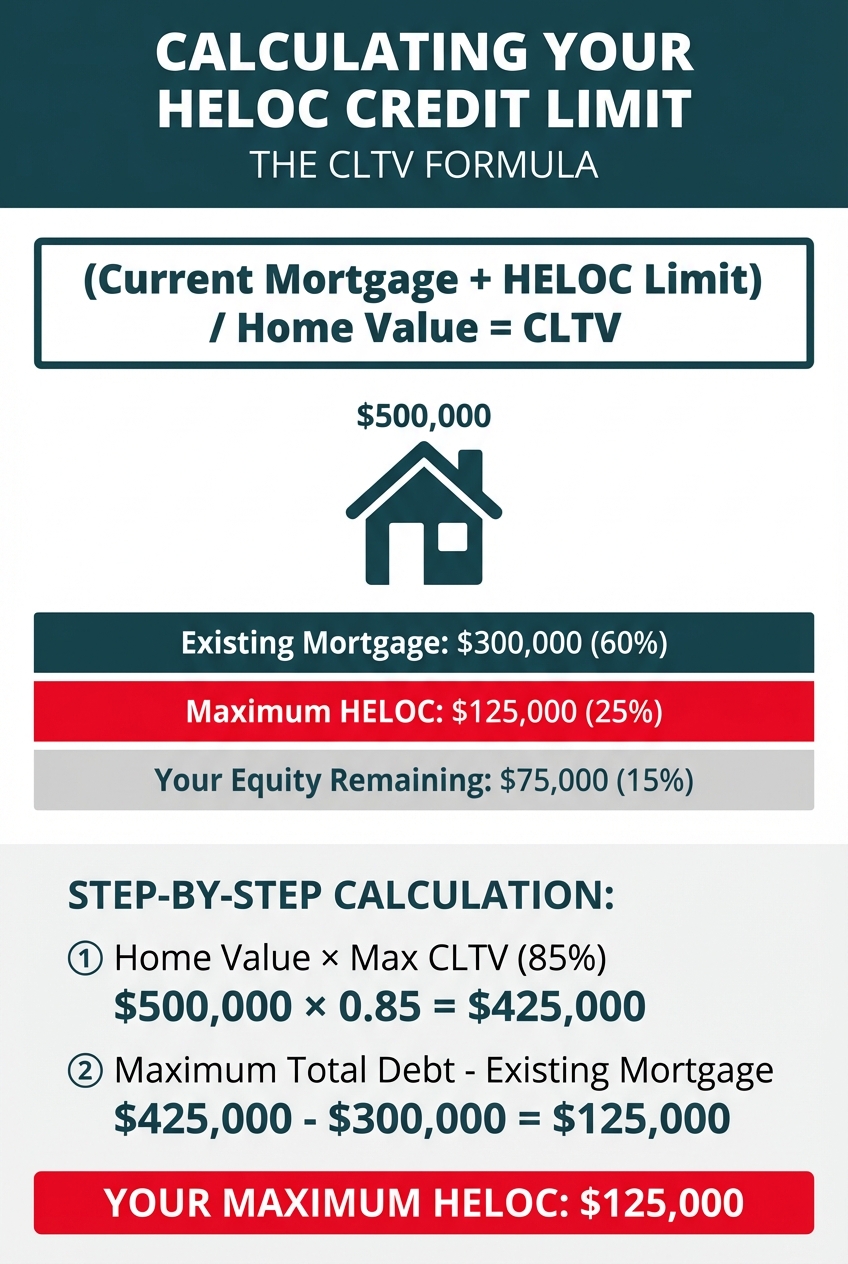

- Home's Current Market Value: $500,000

- Existing Mortgage Balance: $300,000

- Lender's Maximum CLTV: 85%

First, calculate the maximum total debt allowed:

$500,000 × 0.85 = $425,000

Then, subtract your existing mortgage:

$425,000 - $300,000 = $125,000 maximum HELOC

This means you could access up to $125,000 through a HELOC while staying within the lender's 85% CLTV threshold.

Important Considerations:

Your actual approved limit may be lower than the maximum CLTV calculation suggests. Lenders also evaluate your credit score, debt-to-income ratio, employment history, and payment history. Even if the math works in your favor, weak qualifications in other areas can reduce your approved credit line.

Additionally, the average CLTV for funded HELOCs is actually much lower than the maximum—around 51% according to recent industry data—suggesting that most borrowers either can't qualify for or don't need to tap their maximum available equity.

The Draw Period Explained: Flexible Access with Variable Costs

Once your HELOC is approved and funded, you enter what's called the **draw period**—typically lasting 5 to 10 years. This is the active phase where you can borrow, repay, and borrow again up to your credit limit, similar to how you'd use a credit card.

How You Access Your Funds

Lenders provide multiple convenient methods to tap your HELOC:

- Special Checks: You'll receive a checkbook linked to your HELOC account, allowing you to write checks directly against your credit line for any purpose.

- Debit Card: Many lenders issue a debit card tied to your HELOC, enabling you to make purchases or withdraw cash at ATMs.

- Online Transfers: Through your lender's online banking platform, you can transfer funds from your HELOC directly to your checking or savings account, usually within 1-3 business days.

- Wire Transfers: For larger amounts or time-sensitive needs, you can request wire transfers, though these typically incur additional fees.

Understanding Minimum Payments During the Draw Period

During the draw period, most HELOCs require only interest-only minimum payments on your outstanding balance. This creates an attractive short-term payment structure but requires careful planning.

Here's how it works:

If you have a $50,000 outstanding balance on your HELOC with a 7.5% variable interest rate, your monthly interest-only payment would be approximately:

($50,000 × 0.075) / 12 = $312.50 per month

However, this payment is based on your current balance, not your total credit limit. If you have a $100,000 credit line but have only drawn $50,000, you're only paying interest on the $50,000 you've actually borrowed.

The Variable Rate Reality

HELOCs almost universally carry variable interest rates tied to a benchmark index—most commonly the U.S. Prime Rate plus a margin determined by your creditworthiness. This means your interest rate, and therefore your minimum payment, can change monthly even if your balance remains constant.

For example, if the Federal Reserve raises rates and the Prime Rate increases from 7.5% to 8.0%, your monthly payment on that same $50,000 balance would rise to approximately $333.33—an increase of nearly $21 per month without you borrowing an additional dollar.

The Revolving Credit Advantage

The defining feature of the draw period is its revolving nature. Unlike other loans where each payment reduces your balance permanently, a HELOC allows you to:

- Borrow $30,000 for a kitchen renovation

- Pay down $10,000 over the next few months

- Borrow that $10,000 again for a different project

- Repeat this cycle as needed throughout the draw period

This flexibility makes HELOCs attractive for ongoing projects or situations where you need access to capital but aren't sure of the exact timing or amounts required.

The Repayment Period & "Payment Shock"

When your draw period ends, your HELOC undergoes a dramatic transformation that catches many borrowers off guard. This transition is called the repayment period, and it typically lasts 10 to 20 years.

What Changes During Repayment

Three critical changes occur when you enter the repayment period:

No More Borrowing: Your credit line closes permanently. Whatever balance you have at the end of the draw period becomes your final loan amount—you cannot draw additional funds.

Full Amortization Begins: Your loan "recasts" or "amortizes," meaning your payments now include both principal and interest, calculated to pay off the entire balance by the end of the repayment period.

Payment Amounts Surge: This is where "payment shock" occurs—your monthly payment can increase dramatically, sometimes doubling or tripling overnight.

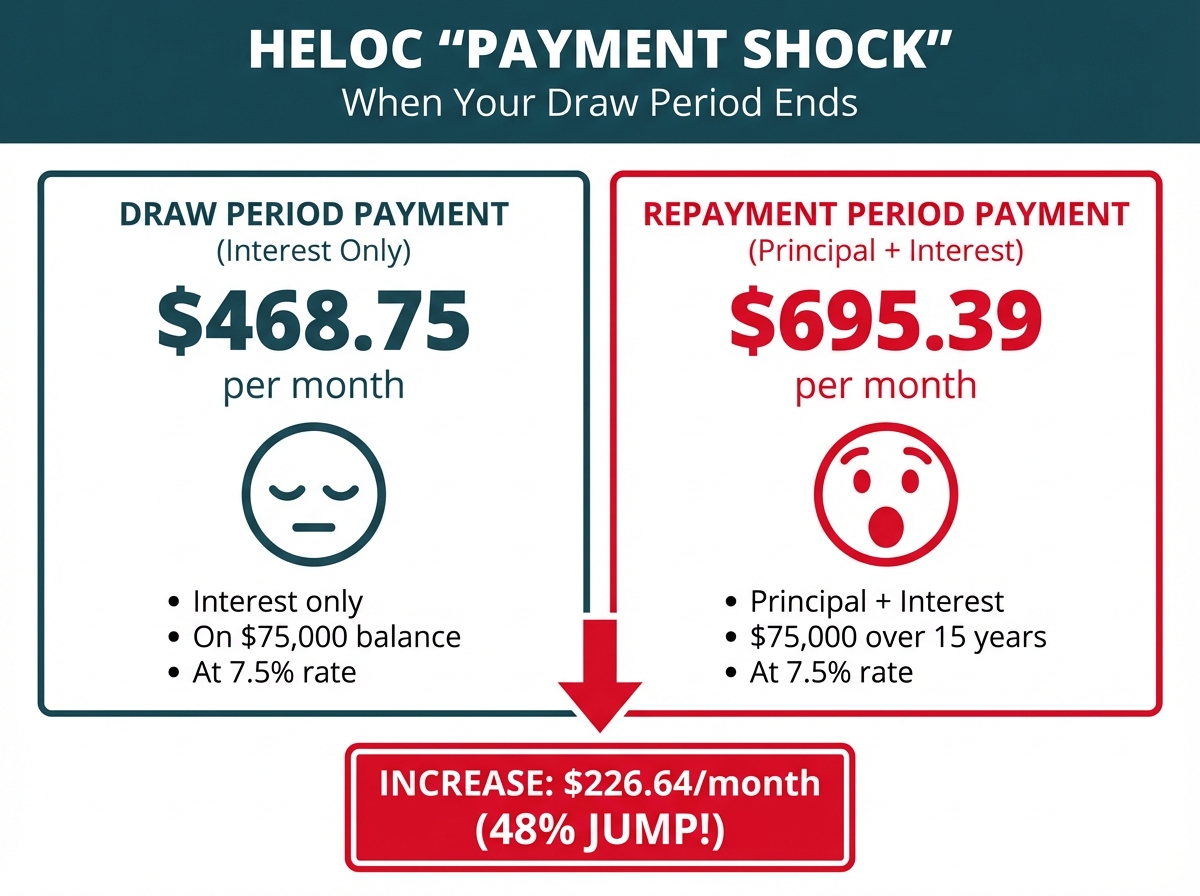

Understanding Payment Shock: A Real-World Example

Let's say you have a $75,000 balance when your 10-year draw period ends, and your HELOC enters a 15-year repayment period with a 7.5% interest rate.

During Draw Period (Interest-Only):

Monthly Payment = $468.75

During Repayment Period (Principal + Interest):

Monthly Payment = $695.39

That's an immediate increase of $226.64 per month—nearly a 50% jump—and this assumes your interest rate hasn't changed. If rates have risen during your draw period, the shock could be even more severe.

For investors managing multiple properties and calculating cash flow, this payment volatility creates significant financial planning challenges. You might structure a rental property investment around a $470 monthly HELOC payment, only to see that obligation jump to nearly $700 when the repayment period begins—potentially turning a cash-flowing property into a monthly loss.

The Refinancing Option

Some borrowers attempt to avoid payment shock by refinancing their HELOC balance into a new loan product before the repayment period begins. However, this strategy comes with its own complications—particularly the "cash-out refinance trap" we'll discuss in detail later. Market conditions, your credit profile, and your property's value at the time of refinancing all factor into whether this strategy makes financial sense.

The unpredictability of both variable rates and the dramatic payment increase at the end of the draw period is precisely why many sophisticated real estate investors prefer the stability of a fixed-rate HELOAN instead—a topic we'll explore in the next section.

Calculating Your Credit Limit: The CLTV Formula

Before a lender approves your HELOC, they need to determine exactly how much equity you can tap into. This calculation centers on your Combined Loan-to-Value (CLTV) ratio—a critical metric that measures your total debt against your home's current market value.

Here's how lenders calculate your maximum HELOC limit:

Step 1: Determine Your Home's Current Market Value

Lenders will typically require a professional appraisal to establish your property's current worth. This isn't optional—it's a standard requirement that protects both you and the lender by ensuring accurate equity calculations. The appraisal cost usually ranges from $300 to $600 and may be paid upfront or rolled into closing costs.

Step 2: Identify the Maximum CLTV Ratio

Most lenders cap your CLTV between 80% and 85% of your home's value, though some lenders may go as high as 90% or even 100% depending on your credit profile and the lender's risk tolerance. The CLTV limit represents the maximum total debt (your existing mortgage plus your new HELOC) that a lender will allow against your property.

Step 3: Apply the CLTV Formula

The formula is straightforward:

(1st Mortgage Balance + Total HELOC Limit) / Current Home Value = CLTV

When a HELOC Makes Sense (And When It Doesn't for Investors)

While this guide has highlighted the significant drawbacks of HELOCs for real estate investors, it's important to acknowledge that HELOCs aren't inherently bad financial products—they're simply designed for different borrowing scenarios than what most investors need. Understanding when a HELOC is appropriate versus when a HELOAN is superior can help you make the right financing decision for your specific situation.

Legitimate Use Cases for HELOCs

For certain homeowners and specific financial scenarios, a HELOC can be an excellent tool. The key is matching the product's characteristics—revolving credit, variable rates, and flexible draw periods—with situations that benefit from these features.

Unpredictable or Ongoing Expenses

HELOCs excel when you face expenses that will occur over an extended period but can't predict the exact timing or amounts. Home equity lines of credit function like credit cards, allowing you to borrow multiple times from a set credit limit based on your home's equity, making them ideal for:

- College tuition payments: When you need to pay semester-by-semester over four years, drawing only what you need each term

- Extended medical treatments: For ongoing healthcare costs where the total expense is unknown upfront

- Phased home renovations: When you're doing DIY improvements over months or years and buying materials as you go

In these scenarios, you avoid paying interest on money you haven't yet used, unlike with a lump-sum HELOAN where you receive all funds at closing.

Short-Term Borrowing with Quick Payoff Plans

If you have a concrete plan to borrow and repay within the draw period—ideally within 12-24 months—a HELOC's interest-only payments can minimize your monthly costs during that window. This works well for:

- Bridge financing: Covering a down payment on a new primary residence while waiting for your current home to sell

- Temporary cash flow gaps: Short-term business needs where you expect a large payment or contract completion within months

- Emergency reserves: Maintaining an available credit line for true emergencies, drawing only when absolutely necessary

The critical factor here is discipline and a realistic repayment timeline. If you're confident you'll pay off the balance before entering the repayment period, you can avoid the payment shock that catches many borrowers off guard.

Ultimate Flexibility Requirements

Some borrowers genuinely need the revolving nature of a HELOC—the ability to borrow, repay, and borrow again during the draw period. This makes sense when:

- You're managing variable income streams and need a safety net you can tap and replenish

- You're consolidating and paying off multiple debts strategically over time

- You want a financial cushion available without the commitment of taking a full loan upfront

HELOCs typically offer greater payment flexibility, which appeals to homeowners who value optionality over predictability.

Why Investor Needs Are Fundamentally Different

While the scenarios above represent valid HELOC use cases, they're primarily relevant to homeowners living in their primary residence with personal financial needs. Real estate investors operate under entirely different constraints and objectives that make HELOANs the superior choice.

Investors Need Predictable Acquisition Costs

When you're analyzing a rental property purchase or fix-and-flip opportunity, you need to know your exact financing costs to calculate whether the deal makes sense. A HELOC's variable rate introduces uncertainty into your pro forma:

- Your monthly payment can increase unexpectedly, eroding projected cash flow

- You can't accurately model your debt service coverage ratio with fluctuating payments

- Rising rates during a project can turn a profitable deal into a money-loser

A HELOAN provides fixed rates and fixed payments, allowing you to underwrite deals with confidence and lock in your costs at closing.

Investors Scale Through Sequential Acquisitions

Unlike homeowners making one-time purchases, investors build portfolios by acquiring multiple properties over time. This is where the CLTV penalty and liquidity exclusion rules become deal-killers:

- You need maximum borrowing capacity on each property to fund the next acquisition

- You must demonstrate cash reserves to qualify for subsequent mortgages

- Your ability to leverage existing properties directly impacts your portfolio growth rate

HELOANs count only the actual borrowed amount against your CLTV, not a theoretical credit limit. This preserves your borrowing power and keeps your debt-to-equity ratios favorable for future financing.

Investors Require Flexible Qualification Paths

Professional real estate investors often have complex income structures that don't fit traditional W-2 employment documentation:

- Multiple LLCs holding different properties

- Rental income from various sources

- Self-employment income that fluctuates seasonally

- Business bank accounts rather than personal pay stubs

Standard HELOCs almost universally require full-documentation underwriting with tax returns, W-2s, and pay stubs—documentation that may not reflect an investor's true financial capacity or liquidity. Investor-focused HELOANs offer alternative qualification methods like DSCR (qualifying based on the property's rental income) programs that align with how investors actually generate and manage income.

The OfferMarket Difference: Built for Investor Success

OfferMarket doesn't offer HELOCs because we've seen firsthand how they limit investor growth and create unnecessary complications. Instead, we specialize in investor focused HELOANs because they're purpose-built for the unique needs of real estate portfolio building.

Why We Focus on HELOANs:

- Fixed rates and payments enable accurate deal analysis and cash flow modeling

- Actual balance reporting preserves your ability to acquire additional properties

- Investor-friendly qualification through DSCR programs

- No revolving credit complications that trigger cash-out refinance treatment

- Streamlined closing process designed for investors who need to move quickly on opportunities

If you're a homeowner facing unpredictable personal expenses or need short-term flexibility with a clear payoff plan, a traditional HELOC from a retail lender might serve you well. But if you're a real estate investor focused on scaling your portfolio, maximizing leverage across multiple properties, and building long-term wealth through rental income or property appreciation, a HELOAN is the professional's choice.

The difference isn't just about product features—it's about aligning your financing strategy with your investment objectives. HELOCs are consumer products designed for homeowner flexibility. HELOANs are investor tools designed for portfolio growth.

Ready to Unlock Your Property's Equity? Your Next Steps

If you're a real estate investor ready to leverage your property's equity to scale your portfolio, the path forward is clearer than you might think. Unlike the complex and time-consuming process often associated with HELOCs, OfferMarket's HELOAN solution is designed specifically for investors who need speed, certainty, and flexibility.

The OfferMarket Instant Quote Process

Getting started takes just minutes, not weeks. Here's how it works:

Step 1: Request Your Instant Quote (3-5 Minutes)

Visit OfferMarket's platform and enter your basic property and financial information. Our proprietary technology instantly analyzes your scenario against multiple investor-friendly loan programs to identify your best options.

Step 2: Review Your Customized Terms

Within minutes, you'll receive a detailed quote showing:

- Your maximum loan amount based on your property's equity

- Fixed interest rate (no surprises or payment shock)

- Monthly payment amount

- Estimated closing costs

- Qualification pathway (DSCR)

Step 3: Choose Your Path Forward

If the terms align with your investment strategy, you can move forward immediately with a formal application. Our loan specialists will guide you through each step, ensuring you understand exactly what's required and when you can expect funding.

Timeline Expectations for Your HELOAN

Unlike traditional HELOCs that can take 2-6 weeks or longer to close, OfferMarket's streamlined investor-focused process is designed for speed:

Instant Quote System: Pop your basic property and financial details into our online portal, and you'll have a preliminary approval and rate quote in your hands within minutes.

Documentation Submission: Upload your investment documents through our secure portal—no faxing, no mailing, no hassle.

Underwriting: Our team gets real estate investors. We look at your whole portfolio strategy, not just one property at a time.

Appraisal Process: For qualifying properties, we offer desktop and drive-by appraisal options to keep things moving quickly.

Closing: Go digital with your closing, and expect funding in your account within 24-48 hours after you sign.

The exact timeline depends on how quickly you can provide required documentation and the complexity of your property situation, but our team works diligently to accelerate the process at every stage.

Real-World Investor Scenarios

Scenario 1: The Portfolio Expander

Maria owns three rental properties free and clear, each worth approximately $400,000. She wants to acquire two more properties to expand her portfolio. By securing a HELOAN on one property for $280,000 (70% LTV), she has the capital for two 25% down payments on $560,000 worth of new properties. Because it's a fixed-rate HELOAN rather than a HELOC, the new lenders calculate her actual debt—not an inflated credit limit—making it much easier to qualify for the new mortgages.

Scenario 2: The Value-Add Investor

James purchased a distressed 4-unit property that needs $150,000 in renovations. He owns another property with $200,000 in equity. Rather than taking a HELOC with variable payments that could spike during his renovation period, he secures a $140,000 HELOAN. The fixed monthly payment allows him to accurately calculate his holding costs and ensure the project remains profitable. He qualifies using the rental income from his existing property through a DSCR loan program, avoiding the need to document his complex self-employment income.

Scenario 3: The Debt Consolidator

Sarah has equity in her primary residence and wants to pay off high-interest credit cards and a business line of credit she used for property improvements. A HELOAN gives her a fixed, predictable payment to replace multiple variable-rate debts. When she's ready to refinance her primary mortgage in 18 months to take advantage of lower rates, the transaction qualifies as a rate-and-term refinance (not cash-out) because she's simply paying off an existing lien, resulting in better terms and lower costs.

Take Action: Get Your Instant Quote Today

The difference between successful real estate investors and those who struggle often comes down to having the right tools and capital at the right time. Don't let the limitations and hidden traps of a HELOC slow down your portfolio growth or create unexpected obstacles in your financing strategy.

Get your instant HELOAN quote from OfferMarket in under 5 minutes.

There's no obligation, no impact to your credit score for the initial quote, and no pressure. You'll simply see what's possible with your property's equity and how a HELOAN can support your specific investment goals.

Whether you're looking to acquire your next property, fund a renovation, consolidate debt, or simply have capital ready for the right opportunity, OfferMarket's investor-focused HELOAN programs provide the certainty, flexibility, and speed you need to scale your real estate portfolio with confidence.

Have questions about which qualification pathway is right for your situation? Our experienced loan specialists understand the unique challenges real estate investors face. Get instant quote to get in contact with our Onboarding Specialist so they can see your sample or actual deal in our system to discuss your specific scenario and explore your options.

Your property's equity is your most powerful tool for growth—make sure you're using it wisely.

OfferMarket Loans

Check your rate

60 seconds · no credit pull