*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Interest-Only HELOCs for Investment Properties

If you're a real estate investor looking to unlock the equity in your properties, you've probably come across the term "interest-only HELOC." But what exactly is it, and how can it help you grow your portfolio? More importantly, where can you even find lenders willing to offer this type of financing for investment properties?

Let's cut through the confusion. Interest-only Home Equity Lines of Credit (HELOCs) can be powerful tools for savvy investors—but they're not as common or straightforward as you might think, especially when it comes to non-owner-occupied properties.

![Task: Create a professional header infographic that introduces the concept of Interest-Only HELOCs for investment properties, featuring key statistics and a visual flow diagram.

Visual Structure: A horizontal infographic split into three main sections showing the progression from traditional financing to interest-only HELOCs, with statistical callouts and iconography.

ASCII Layout Reference:

```

┌─────────────────────────────────────────────────────────────┐

│ INTEREST-ONLY HELOCs FOR INVESTMENT PROPERTIES │

├───────────────┬─────────────────┬───────────────────────────┤

│ [ICON] │ [ICON] │ [ICON] │

│ Traditional │ Interest-Only │ Investment Property │

│ HELOC │ HELOC │ Requirements │

│ │ │ │

│ Principal + │ Interest Only │ • 700+ Credit Score │

│ Interest │ During Draw │ • 70-80% Max LTV │

│ Payments │ Period │ • Higher Rates │

└───────────────┴─────────────────┴───────────────────────────┘

│ KEY BENEFIT: Lower Initial Payments │

│ for Strategic Investment Opportunities │

└─────────────────────────────────────────────────────────────┘

```

Image Section Breakdown:

- Header section: White background (#FFFFFF) with text](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771534730179_vz53lw.jpg?alt=media&token=e1b1aee3-eb23-42c4-9f2f-d48f6d831995)

In this comprehensive guide, we'll walk you through everything you need to know about interest-only HELOCs for investment properties. You'll discover which lenders actually offer them (spoiler: they're harder to find than you might expect), understand how they work, learn about the risks involved, and explore whether they're the right choice for your investment strategy.

We'll also introduce you to alternative financing options that might serve you better—including why many successful investors at OfferMarket choose Home Equity Loans (HELOANs) over HELOCs for their investment properties.

Ready to make smarter financing decisions for your real estate portfolio? Let's dive in.

Where to Find Interest-Only HELOCs for Investment Properties

Let's be real: tracking down lenders who offer interest-only Home Equity Lines of Credit (HELOCs) for investment properties takes some legwork. Most financial institutions reserve these products for primary residences. But don't worry—options do exist for savvy real estate investors who want to tap into their property equity with flexible payment terms.

Lenders Offering Investment Property HELOCs

We've done the homework for you. Here are financial institutions that may offer interest-only HELOCs for investment properties:

Cornerstone Bank - Offers investment property HELOCs with 10-year interest-only payment plans. Their variable rates are competitive for non-owner-occupied properties. [Learn more about their investment property HELOC rates.

Citizens Bank - Provides HELOCs for investment property purchases through their FastLine® program, designed to help investors move quickly in competitive markets.

PenFed Credit Union - Known for offering HELOCs on investment properties with competitive rates and terms.

Alliant Credit Union - Offers HELOCs with an interest-only draw period of 10 years, followed by a repayment period of up to 20 years.

Fifth Third Bank - Provides HELOC options that may be available for investment properties.

Wells Fargo, Bank of America, and US Bank - These larger national banks sometimes offer investment property HELOCs to customers with established relationships. See who offers HELOCs on investment properties.

![Task: Create a comprehensive comparison infographic displaying lenders who offer interest-only HELOCs for investment properties, including their key features and requirements.

Visual Structure: A vertical infographic with a header section followed by six horizontal rows, each representing a different lender category with icons, key features, and distinguishing characteristics.

ASCII Layout Reference:

```

┌────────────────────────────────────────────────────────────┐

│ LENDERS OFFERING INVESTMENT PROPERTY HELOCs │

├────────────────────────────────────────────────────────────┤

│ [ICON] CORNERSTONE BANK │

│ • 10-year interest-only terms │

│ • Starting at 7.75% variable rate │

├────────────────────────────────────────────────────────────┤

│ [ICON] CITIZENS BANK │

│ • FastLine® program for quick closings │

│ • Competitive market advantage │

├────────────────────────────────────────────────────────────┤

│ [ICON] CREDIT UNIONS (PenFed, Alliant) │

│ • Member-focused flexible terms │

│ • Up to 20-year repayment periods │

├────────────────────────────────────────────────────────────┤

│ [ICON] NATIONAL BANKS (Wells Fargo, BofA, US Bank) │

│ • Relationship-based lending │

│ • Established customer preference │

├────────────────────────────────────────────────────────────┤

│ TYPICAL REQUIREMENTS ACROSS LENDERS │

│ Credit Score: 700+ | LTV: 70-80% | Equity: 20%+│

└────────────────────────────────────────────────────────────┘

```

Image Section Breakdown:

- Header: White background with](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1771534929156_wracwe.jpg?alt=media&token=acfaa1eb-ce17-4769-902d-156dff64e290)

The Scarcity Challenge

Here's the reality: investment property HELOCs are much harder to find than those for primary residences. Why? A few key reasons:

- Lenders see higher risk when the property isn't owner-occupied

- Default rates tend to be higher compared to primary residences

- Underwriting gets more complicated

- Interest rates climb and qualification criteria tighten

Most lenders offering investment property HELOCs will expect:

- Higher credit scores (typically 700+)

- Lower loan-to-value ratios (often 70-80% maximum)

- Significant equity in the property

- Strong debt-to-income ratios

- Proven history of property management experience

Why Successful Investors Often Choose HELOANs Instead

At OfferMarket, we've seen a clear pattern: our most successful clients typically choose Home Equity Loans (HELOANs) over HELOCs for their investment properties. Here's why:

Predictability - HELOANs come with fixed interest rates and steady payment amounts. That means you can budget with confidence and project your cash flow without any surprises.

Simpler Management - As your portfolio grows, juggling multiple variable-rate products with shifting payment structures gets messy fast. HELOANs keep things straightforward.

Lower Long-Term Risk - With a fixed-rate HELOAN, you won't face the payment shock that hits when a HELOC shifts from interest-only to full amortization. Your payments stay predictable.

Better Availability - More lenders offer HELOANs for investment properties than HELOCs. That means more options for you and potentially better terms to choose from.

Strategies for Finding Additional Lenders

Still set on securing an interest-only HELOC for your investment property? Here are some smart moves to explore:

Leverage Existing Banking Relationships - Banks where you already have accounts or loans are more likely to give your application a fair shake. A solid track record with them works in your favor.

Explore Local Credit Unions - Credit unions often have more flexible lending guidelines and genuinely want to help investors in their communities succeed.

Consult with Mortgage Brokers - Brokers who specialize in investment property financing have connections to lenders and products you won't find through a simple online search.

Network with Real Estate Investment Groups - Your fellow investors are goldmines for referrals. They can point you toward lenders who've already proven themselves.

Consider Portfolio Lenders - These lenders hold loans on their own books instead of selling them off. That gives them room to be more flexible with their lending criteria.

Explore Community Banks - Smaller local banks often provide personalized service and show more willingness to craft customized financing solutions for investors like you.

One important note: even when you find a lender offering investment property HELOCs, take time to evaluate the terms carefully. Look at interest rates (expect them to run higher than for primary residences), fee structures, and what happens when the draw period ends.

How Interest-Only HELOCs Work for Real Estate Investors

Interest-only Home Equity Lines of Credit (HELOCs) give you a flexible way to tap into your property's equity while keeping your monthly payments manageable during the early years of the loan. Let's break down how these financing tools work so you can decide if they're right for your investment strategy.

Definition and Basic Structure

Think of an interest-only HELOC as a credit card backed by your property's equity. Unlike investor focused loan where you get a lump sum, a HELOC lets you borrow what you need, when you need it, up to your approved limit. Here's the key difference: during the draw period (usually 5-10 years), you only pay interest on what you've borrowed—not the principal.

According to Bankrate, "An interest-only HELOC lets you borrow against your home's equity while paying just the interest for a set time, keeping initial payments low." For you as an investor, this means more cash stays in your pocket for your next deal or that renovation project you've been planning.

Difference Between Traditional and Interest-Only HELOCs

Here's where it gets interesting. The main difference comes down to what you're paying each month:

Traditional HELOC: You pay both principal and interest during the draw period. Higher monthly payments, but you're building equity faster.

Interest-Only HELOC: You pay just the interest during the draw period. The principal waits until the repayment period kicks in.

Why does this matter to you? It's all about cash flow. As Better explains, "Interest-only HELOCs calculate monthly payments differently than traditional HELOCs... A property investor could use money from an interest-only [HELOC]" to keep more capital working for you while minimizing what goes out the door each month.

How Interest-Only Payments Work

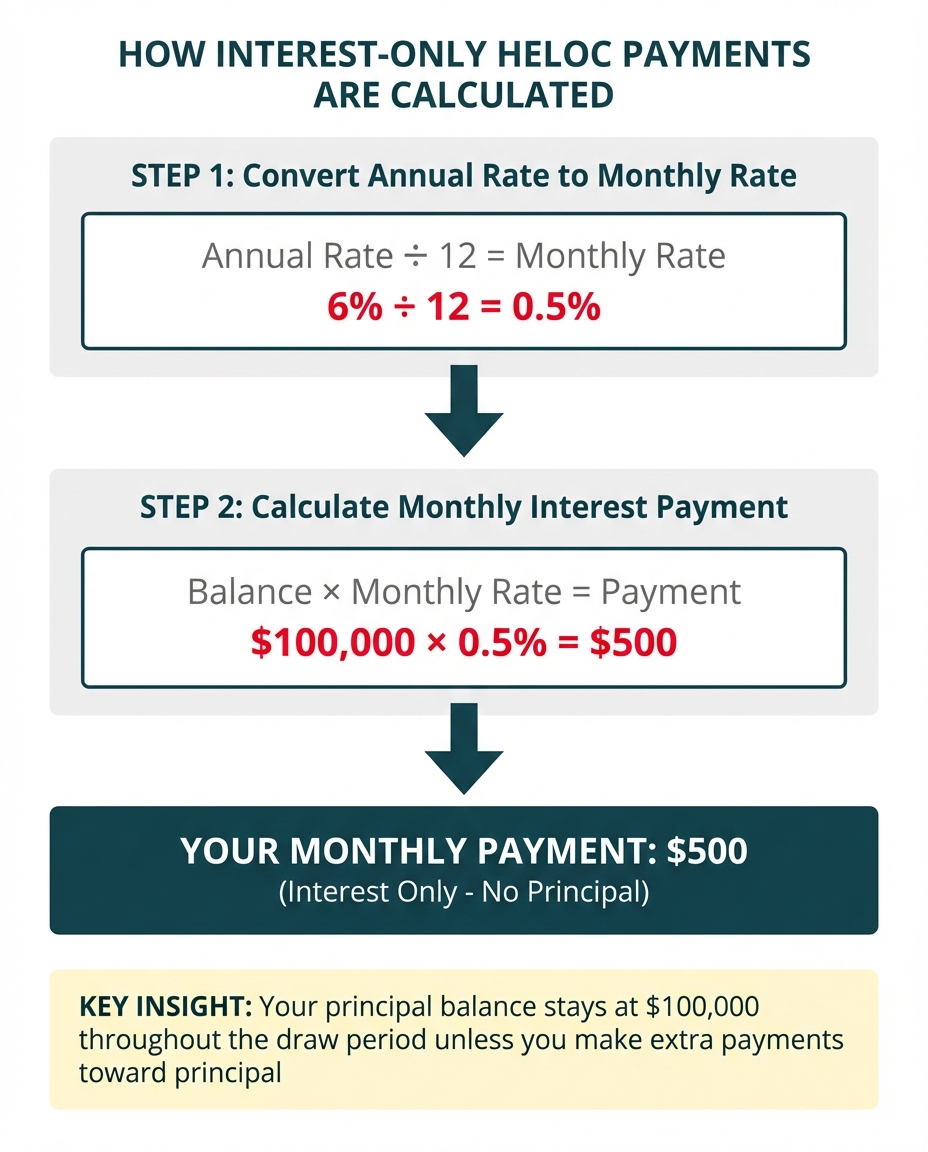

Let's break down interest-only payments so you know exactly what you're working with. The math is simple once you see it in action:

- Take your annual interest rate and divide by 12 to get your monthly rate

- Multiply your outstanding balance by that monthly rate

Here's a real-world example: Say you've tapped $100,000 from your HELOC at a 6% annual interest rate:

- Monthly interest rate: 6% ÷ 12 = 0.5%

- Monthly payment: $100,000 × 0.5% = $500

Keep in mind that HELOC interest rates are typically variable, so your payment can shift as market rates move. And here's the key thing to remember: paying only interest means your principal balance stays put unless you choose to pay extra.

Typical Terms and Conditions for Real Estate Investors

As a real estate investor, here are the terms and conditions you'll want to have on your radar:

Draw Period: This is your 5-10 year window to access your credit line while making interest-only payments.

Repayment Period: Once the draw period ends, you'll have 10-20 years to pay back both principal and interest. Heads up—this usually means higher monthly payments.

Loan-to-Value (LTV) Limits: Expect to borrow up to 80-85% of your property's value minus what you owe on your mortgage. Investment properties often come with tighter limits.

Variable Interest Rates: Most HELOCs are tied to the prime rate plus a margin, so rising rates mean rising payments.

Closing Costs and Fees: Budget for application fees, appraisal costs, and annual maintenance fees.

One more thing: investment properties typically face stricter requirements than primary residences. Think higher credit score thresholds, lower LTV ratios, and potentially steeper interest rates. Many lenders will also want to see proof of rental income or extra cash reserves.

Understanding these mechanics helps you strategically incorporate interest-only HELOCs into your financing toolkit, particularly for short-term capital needs or as bridge financing between property acquisitions and longer-term financing solutions.

Draw Period Mechanics

During the draw period—typically lasting 5 to 10 years—you can access funds up to your approved credit limit whenever you need them. This period gives you maximum flexibility as an investor, allowing you to:

- Withdraw funds multiple times up to your credit limit

- Make interest-only payments on the borrowed amount

- Repay and reborrow as your investment needs change

"The HELOC draw period is usually 10 years, where you can withdraw funds up to your limit," according to Citizens Bank. This extended access period makes HELOCs especially valuable when you're juggling multiple projects with different timelines.

Repayment Period Transition

When the draw period ends, the HELOC shifts to the repayment phase—a critical point you'll want to understand:

- You can no longer withdraw funds

- Payments increase to include both principal and interest

- The repayment period typically lasts 10-20 years

This transition can create significant cash flow changes. "During [the draw period], you're usually required only to pay interest on what you borrow. At the end of the draw period, you enter the repayment period," explains Bankrate. Plan your exit strategies accordingly, especially for fix-and-flip projects that might span this transition.

Interest Rate Structures

Most interest-only HELOCs come with variable interest rates tied to the prime rate. Here's what that means for you:

- You'll typically start with lower rates than fixed-rate options

- Your monthly payments will move up or down with market conditions

- Some lenders offer rate caps or let you convert to a fixed rate

As an investor, this variable structure means you'll want to plan your cash flow carefully and stay on top of rate risk. Our advice? Build a buffer for potential rate increases into your investment projections so you're never caught off guard.

Credit Line Availability and Borrowing Limits

How much can you actually borrow with an interest-only HELOC? It comes down to a few key factors:

- Your property's appraised value

- Your existing mortgage balance

- The lender's maximum loan-to-value (LTV) ratio

- Your credit profile

Here's the reality: most lenders cap combined loan-to-value ratios at 80-85% for investment properties, though this varies by institution. Let's break that down with a real example. Say your property is worth $500,000 and you have a $300,000 mortgage balance. If your lender allows 80% CLTV, your maximum HELOC amount would be approximately $100,000 ($500,000 × 80% = $400,000, minus the $300,000 first mortgage).

Strategic Applications for Investors

Interest-only HELOCs can be powerful tools in your investing toolkit. Here's how savvy investors put them to work:

- Quick access to renovation funds: Draw only what you need for each project phase

- Bridge financing: Cover short-term gaps between property acquisitions and sales

- Portfolio expansion: Use equity from existing properties to make down payments on new acquisitions

- Emergency reserves: Maintain liquidity for unexpected property expenses or opportunities

If you're managing multiple properties, the revolving nature of a HELOC gives you flexibility that traditional loans simply can't match. Your capital flows exactly where you need it, exactly when you need it.

Tax Implications of Interest-Only HELOCs for Real Estate Investors

If you're considering an interest-only HELOC, you'll want to understand the potential tax advantages these financial tools can offer.

While tax benefits should never be the sole reason for choosing a financing option, they can make a real difference in your bottom line.

Deductibility of HELOC Interest

Here's what you need to know: The Tax Cuts and Jobs Act (TCJA) changed the game for HELOC interest deductibility. From 2018 through 2025, you can only deduct HELOC interest when you use the funds to "buy, build, or substantially improve" the property securing the loan. This applies to loans totaling up to $750,000 ($375,000 for married filing separately).

When you're using a HELOC for investment properties, the tax treatment works differently than for your personal residence. According to Stessa, "From 2018 through 2025, the IRS treats interest paid on HELOCs or home equity loans secured by your primary or secondary homes as potentially deductible — but only if you use the proceeds to buy, build, or substantially improve the property securing the loan."

Business Expense Deductions for Investors

Here's where it gets interesting for real estate investors: when you use HELOC funds for business purposes on rental properties, the interest may qualify as a business expense on Schedule E rather than mortgage interest on Schedule A. What does this mean for you?

- The restrictions on how you use the funds may not apply when you claim the interest as a business expense

- You're not bound by the same limitations as personal mortgage interest

- You can take the deduction even if you don't itemize on your personal return

According to Landlord Studio, "HELOC interest can be tax-deductible under certain conditions. The Tax Cuts and Jobs Act (TCJA) suspended deductions for HELOC interest from 2018 to 2025 unless the funds are used to buy, build, or substantially improve the property securing the loan."

Record-Keeping Requirements

Want to maximize your tax benefits? Here's your checklist:

- Keep detailed records of exactly how you use your HELOC funds

- Save every receipt for property improvements and business expenses

- Work with a tax professional who knows real estate inside and out

- Consider keeping funds separate based on their purpose—it makes accounting much easier

Tax Strategy Considerations

The smartest investors know that financing strategy and tax strategy go hand in hand. An interest-only HELOC can be advantageous because:

- The revolving nature allows for strategic timing of expenses and deductions

- Lower initial payments can improve cash flow while still generating deductions

- The ability to draw and repay funds provides flexibility for tax planning across multiple tax years

Keep in mind that tax laws evolve regularly, and the current provisions regarding HELOC interest deductibility are scheduled to expire after 2025. Always consult with a qualified tax professional before making financing decisions based on potential tax benefits.

Timeline Alignment with Draw Period

The typical 10-year draw period of a HELOC gives you some serious advantages as a real estate investor:

- Multiple Project Cycles: You can knock out several fix-and-flip projects within a single draw period

- Portfolio Scaling: The revolving credit lets you grow your investment activities over time

- Strategic Timing: You control when you draw and repay, so you can move with the market

Funding Renovation Costs

Interest-only HELOCs shine when it comes to renovation financing:

- Incremental Draws: Unlike lump-sum loans, you pull funds as you need them for each renovation phase

- Cost Control: You only pay interest on what you've actually used at each stage

- Flexible Payment Schedule: Keep payments manageable during renovation when the property isn't bringing in income yet

- No Prepayment Penalties: Most HELOCs let you pay back early without extra fees

Exit Strategy Considerations

When you're working with an interest-only HELOC, smart planning for your exit is essential:

- Sale of Property: The simplest path forward—sell your renovated property and pay off the HELOC

- Refinance: Move into long-term financing through a cash-out refinance or investment property loan

- Rental Conversion: If the market shifts, pivot to a rental strategy and refinance with a DSCR loan

- Partial Paydown: Put your profits to work by reducing your HELOC balance while keeping the credit line open for your next project

Comparison with Hard Money Loans

Interest-only HELOCs bring some real advantages to the table when stacked against traditional hard money loans:

| Feature | Interest-Only HELOC | Hard Money Loan |

|---|---|---|

| Interest Rate | 8-12% (variable) | 10-15% (fixed) |

| Points/Fees | Minimal or none | 2-5 points upfront |

| Term | 10-year draw, 20-year repay | 6-24 months |

| Flexibility | Revolving credit line | One-time funding |

| Approval Process | 1-6 weeks | 3-10 days |

| Collateral | Primary or investment property | Project property |

If you've built solid equity in your existing properties, interest-only HELOCs can save you serious money compared to hard money loans. The trade-off? They won't fund as quickly when you need to move fast on a hot deal.

Here's something else to keep in mind: hard money loans typically require credit scores of 680-720, while HELOCs usually set the bar higher. That makes HELOCs a better fit for investors with stronger credit who want to put their existing equity to work.

Bottom line: Interest-only HELOCs are a smart addition to your financing toolkit. Used wisely, they offer the flexibility and cost savings that can boost your returns and help you grow your portfolio.

Using HELOC Funds for Investment Property Down Payments

Want to expand your real estate portfolio without draining your savings? Tapping into your primary residence equity through a Home Equity Line of Credit (HELOC) is a savvy move that many successful investors use to keep their cash working harder.

Leveraging Existing Equity

A HELOC lets you put the equity you've already built in your primary residence to work—funding your next investment opportunity. It's a smart move that's gained traction among investors who want to grow their portfolio without waiting years to save up liquid capital for down payments.

Here's the good news: many lenders are on board with this strategy:

"Yes, some lenders allow you to use a HELOC for the down payment to purchase a rental property. I just helped an investor in CT purchase a 3..." BiggerPockets

Strategic Applications for Investors

Your HELOC is a versatile tool in your investing toolkit. Here's how savvy investors put these funds to work:

- Full purchase financing for smaller investment properties

- Renovation costs to boost property value and returns

- Bridge financing to move fast when opportunity knocks

- Down payments on larger investment properties

Cash Flow Implications

Before you tap into your HELOC, let's make sure you understand how the numbers will play out:

- Initial Period: During the draw period (typically 5-10 years), you'll only pay interest on what you borrow—great for preserving cash flow

- Rental Income: Your property needs to generate enough rent to cover both the HELOC payment and your investment property mortgage

- Buffer Planning: Build in a 20-25% cushion between your expected rental income and total debt payments—that's how smart investors sleep well at night

Example Scenario with Numbers

Let's walk through a real-world example:

- Your primary residence value: $500,000

- Current mortgage balance: $300,000

- Available equity: $200,000

- HELOC at 80% LTV: $100,000 available

Using this HELOC for a $100,000 down payment on a $500,000 rental property:

- Monthly HELOC interest payment (at 7%): ~$583

- New rental property mortgage: $400,000 at 6% = ~$2,398/month

- Total monthly payments: $2,981

- Required rental income with 25% buffer: $3,726

As you can see, a HELOC can open the door to property acquisition while keeping your cash flow healthy and sustainable.

Long-term Sustainability Challenges

While HELOCs offer flexibility, they come with sustainability challenges:

"A HELOC can be used to purchase a number of things, including real estate." However, "You should have a plan to pay off the HELOC, ideally from the cash flow of the investment property." White Coat Investor

Here's the deal: variable interest rates on HELOCs can throw a wrench in your investment calculations, and when the repayment period kicks in (that's when you're paying principal plus interest), your cash flow might feel the squeeze. Smart investors always have an exit strategy in their back pocket—like refinancing the investment property to pay off the HELOC once you've built up enough equity.

The bottom line? When you structure it right with solid safety margins, using a HELOC for investment property down payments can help you grow your portfolio faster while keeping risk in check.

Is an Interest-Only HELOC Right for You?

Let's get real about interest-only HELOCs. They can be a game-changer for your real estate investments—but they're not a one-size-fits-all solution. Knowing when this financing tool works for you (and when it doesn't) is key to your investment success.

Ideal Scenarios for Interest-Only HELOC Use

Interest-only HELOCs really shine in these situations:

- Short-term capital needs: When you need fast access to funds for a time-sensitive deal, like a property that needs to close yesterday

- Bridge financing: Perfect for when you're between properties or waiting on another financing option to come through

- Renovation projects: A go-to for fix-and-flip investors who need flexible funding as project costs pop up

- Liquidity verification: Some lenders want to see proof of liquidity before approving investment loans—a HELOC checks that box

- Variable funding needs: When your capital requirements shift and you don't want to borrow (and pay interest on) one big lump sum

The revolving nature of a HELOC makes it especially handy when your funding needs are moving targets rather than fixed amounts. Unlike a home equity loan which provides a lump sum upfront, a HELOC lets you tap into your home equity when you need it, up to a set credit limit. Think of it as a financial safety net that gives you more control over how and when you access your funds.

When an Interest-Only HELOC Is Not Recommended

While interest-only HELOCs can be powerful tools, they're not the right fit for every investor:

- Long-term buy-and-hold strategies: Variable interest rates make HELOCs a risky choice for financing you'll carry for years

- Meeting cash-to-close requirements for DSCR loans: Most debt service coverage ratio lenders want to see verified cash in the bank, not available credit

- When predictable payments are essential: If your investment plan depends on knowing exactly what you'll owe each month

- Large, one-time capital needs: When you need a big chunk of money upfront with no plans to borrow again

- When interest rate stability is crucial: In a rising rate environment, variable HELOCs can throw your payment planning off course

According to the Wall Street Journal, "Both HELOCs and home equity loans let you access your available equity, but the right one for you depends on your goals and situation." The bottom line? Match your financing tool to your specific investment strategy and risk tolerance.

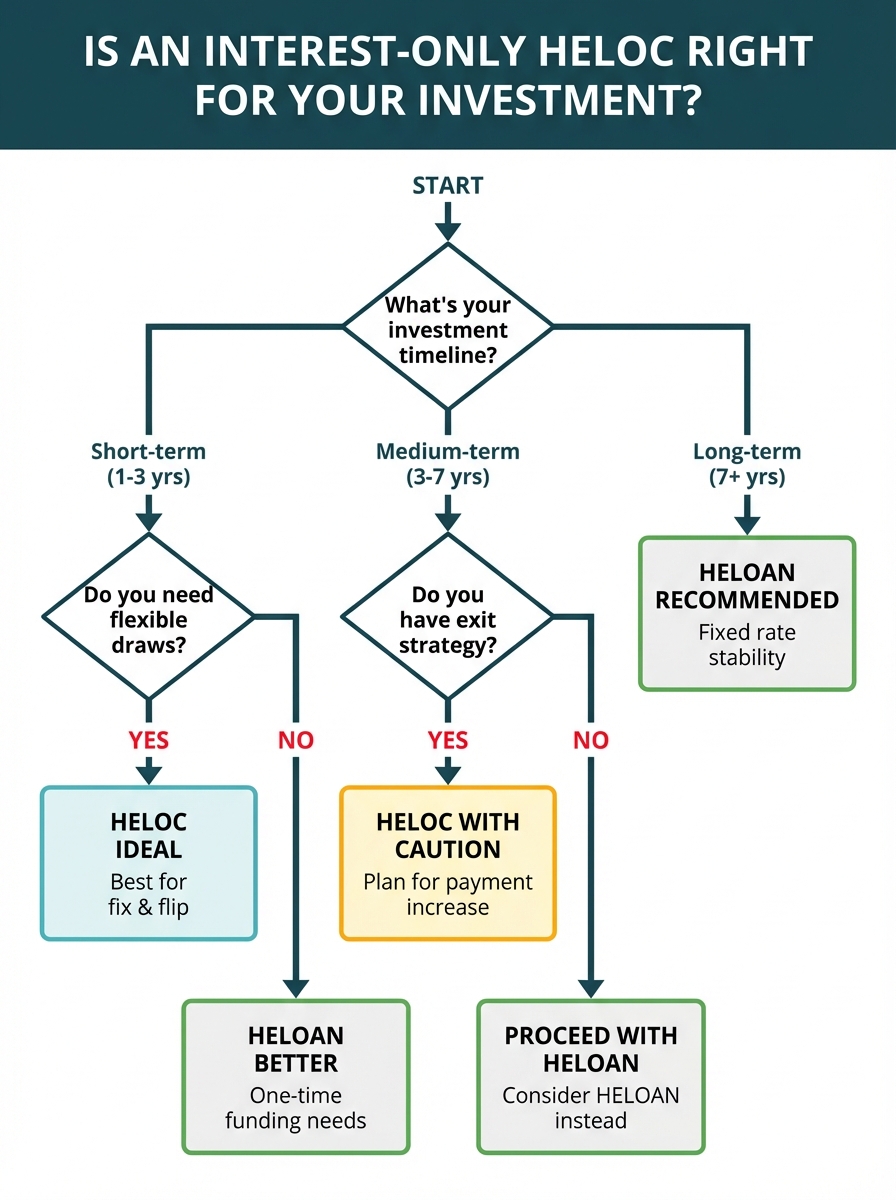

Investment Timeline Considerations

How long you plan to hold your investment matters—a lot:

Short-term investors (1-3 years): Interest-only HELOCs can work beautifully here. You'll likely sell before the draw period ends and repayment kicks in

Medium-term investors (3-7 years): Proceed carefully. Your investment might still be in play when your HELOC shifts to principal and interest payments

Long-term investors (7+ years): You're usually better off with a HELOAN featuring fixed rates and payments you can count on

Risk Tolerance Assessment

Before you commit to an interest-only HELOC, take an honest look at your comfort level with:

- Interest rate fluctuations: Can your investment handle a significant jump in rates?

- Payment shock: Are you ready for when those interest-only payments shift to principal and interest?

- Equity position changes: What's your game plan if property values take a dip?

- Lender changes to terms: Keep in mind that some HELOC providers can freeze or reduce credit lines when the economy gets rocky

Decision-Making Framework

Let's walk through a simple framework to help you figure out if an interest-only HELOC fits your investment strategy:

- Purpose: What's the money actually going toward?

- Timeline: How long do you need this financing to work for you?

- Exit strategy: What's your plan for paying back what you borrow?

- Cash flow impact: How will those early payments—and the bigger ones down the road—affect your returns?

- Alternative options: Have you stacked up the HELOC against other tools like HELOANs?

As noted by OfferMarket, "Unlike a HELOAN, which provides a lump sum, a HELOC allows you to borrow against your home equity as needed, up to a predetermined credit limit." That flexibility is powerful, but you'll want to weigh it against the risks for your unique situation OfferMarket.

Take time to think through these factors, and you'll be in a strong position to decide whether an interest-only HELOC supports your investment goals—or whether a different financing route makes more sense.

The Risks of Interest-Only HELOCs for Real Estate Investors

Interest-only HELOCs can be a powerful tool for real estate investors, but let's be real—they come with some serious risks you'll want to understand before making them part of your strategy.

Payment Shock After Draw Period

Here's the big one: payment shock when your draw period wraps up. During those first 5-10 years, you're cruising with interest-only payments. But once that period ends, you're on the hook for both principal and interest—and that monthly number can jump significantly.

This transition can result in dramatically higher monthly payments. According to a study published in the Journal of Economics and Business, many borrowers experience significant payment increases when their HELOCs convert from interest-only to fully amortizing loans. The research found that "payment shock in home equity lines of credit at the end of their draw period" can lead to financial strain for unprepared borrowers.

Here's the reality: in some cases, your monthly payments can more than double after the draw period ends. That's a serious cash flow crunch if you're juggling multiple properties. Data from the Federal Reserve shows that HELOC defaults tend to spike following the end of draw periods—proof that this payment shock catches many borrowers off guard.

Variable Rate Exposure and Impact on Cash Flow

Here's another factor to keep on your radar: unlike fixed-rate loans, interest-only HELOCs typically come with variable interest rates tied to an index like the prime rate. That means you're exposed to interest rate risk, and your payments can shift with market conditions.

If you're counting on steady cash flow from your rental properties, unexpected jumps in your HELOC payments can throw off your budget and eat into your returns. Even a small rate bump can make a noticeable dent when you're carrying the larger loan balances common in real estate investing.

Cash-Out Refinance Restrictions and Seasoning Rules

Many savvy investors use HELOCs as bridge financing, planning to refinance down the road. But here's what you need to know: most lenders have strict seasoning requirements before they'll approve a cash-out refinance. You're typically looking at a 6-12 month waiting period before you can refinance equity from a HELOC.

These rules can limit your flexibility and potentially keep you in a higher-interest HELOC longer than planned, adding to your overall financing costs.

Potential for Negative Amortization

Here's something important to understand: with interest-only payments, you're not chipping away at your principal balance during the draw period. And in some cases, if your minimum payment doesn't cover all the accrued interest (especially when rates are climbing), you could face negative amortization—meaning your loan balance actually grows over time.

This situation eats into your equity and can put you in a tough spot, particularly if property values in your market are flat or dropping.

Risk of Overleveraging Properties

Because HELOCs are relatively easy to qualify for and access, it's tempting to tap into more equity than you should. But overleveraging your properties can leave you vulnerable—one market dip, extended vacancy, or surprise repair bill could put your entire portfolio at risk.

Mitigation Strategies for HELOC Risks

The good news? You can protect yourself with some smart planning. Here's how:

Plan for repayment: Before you take out an interest-only HELOC, know your exit strategy. Will you sell the property? Refinance? Set aside funds for those higher payments once the draw period ends? Have a clear plan in place.

Stress test your investments: Run the numbers on a worst-case scenario. If rates hit their maximum, will your properties still cash flow? Make sure you can stay profitable even when conditions aren't ideal.

Maintain equity buffers: Don't borrow every dollar available to you. Keeping some equity in reserve gives you breathing room if the market shifts and helps protect you from foreclosure.

Consider fixed-rate alternatives: If you need capital for the long haul, a fixed-rate HELOAN might be a better fit. You'll get predictable payments without worrying about payment shock down the road.

Monitor and adjust: Stay on top of your HELOC terms, how much draw time you have left, and where interest rates are heading. Being proactive helps you avoid surprises and pivot your strategy when needed.

Understanding these risks puts you in the driver's seat. With the right approach, you can use interest-only HELOCs to grow your portfolio while keeping your investments protected from common pitfalls.

The Risks of Interest-Only HELOCs and How to Mitigate Them

Interest-only HELOCs can be powerful tools in your real estate investing toolkit, but let's be real—they come with risks that deserve your attention. The good news? With the right strategies, you can manage these risks and keep your investments on track.

Variable Rate Exposure

Here's the deal with interest-only HELOCs: their rates move with the market. Unlike fixed-rate loans that stay predictable, HELOCs are typically tied to benchmark indices like the prime rate, which means your payments can shift when economic conditions change.

"The Federal Reserve's interest rate decisions directly influence what you pay for variable-rate home equity lines of credit (HELOCs)," according to Bankrate. When the Fed raises rates, your HELOC payments climb right along with them—and that can eat into your returns and cash flow if you're not prepared.

Payment Shock After Draw Period

Here's where many investors get caught off guard. Those low interest-only payments during the draw period feel great, but when full amortization kicks in, your monthly payment can jump significantly. Planning ahead for this transition is key to keeping your investment strategy humming along smoothly.

Cash Flow Strain

If you're investing in rental properties, borrowing too much against your equity can squeeze your cash flow tight. According to Remote Cost Segregation, "Investors should keep borrowing below 50% of available equity, ensure positive cash flow even with HELOC payments, and maintain reserves for vacancies and repairs" to protect their investments from overleveraging.

Effective Risk Mitigation Strategies

1. Plan Repayment Timelines Aligned with Investment Exits

Match your HELOC strategy to your investment game plan. Running a fix-and-flip? Make sure your timeline allows you to pay back what you've borrowed when that property sells. For rental properties, develop a clear plan for transitioning from interest-only payments to full amortization or refinancing before the draw period ends.

2. Keep Your Eye on Market Rate Trends

Stay in the loop on Federal Reserve policies and interest rate forecasts. When rates look like they're heading up, think about drawing the funds you need sooner or exploring fixed-rate alternatives. On the flip side, when rates are steady or dropping, that's your chance to take full advantage of your HELOC's flexibility.

3. Build a Payment Increase Safety Net

Set aside a dedicated reserve fund specifically for handling payment increases. This financial cushion gives you peace of mind and keeps you from having to sell off investments when payments jump after the draw period or when interest rates climb.

4. Lock In Fixed-Rate Options When You Can

Many HELOC providers let you convert portions of your balance to fixed-rate loans. According to Alliant Credit Union, a smart strategy is to "establish plans for your use of the HELOC prior to applying" and consider locking in rates on portions of your balance when rates are favorable. Source

5. Pay Down Principal Early When Possible

Whenever you can, make principal payments during the draw period. This keeps your credit line available while cutting your interest costs and future payment obligations. Think about putting extra rental income or profits from other investments toward paying down your HELOC principal.

6. Consider Hedging Strategies for Larger Portfolios

If you're a sophisticated investor with a bigger portfolio, interest rate hedging instruments might make sense for you. Options like interest rate caps "protect borrowers from rate increases beyond a certain threshold, providing insurance against significant payment hikes while allowing benefit from rate decreases," as noted by Viking Capital.

By understanding these risks and putting smart mitigation strategies in place, you can tap into the benefits of interest-only HELOCs while protecting your investment returns and financial stability. The key is proactive planning rather than reactive management once challenges arise.

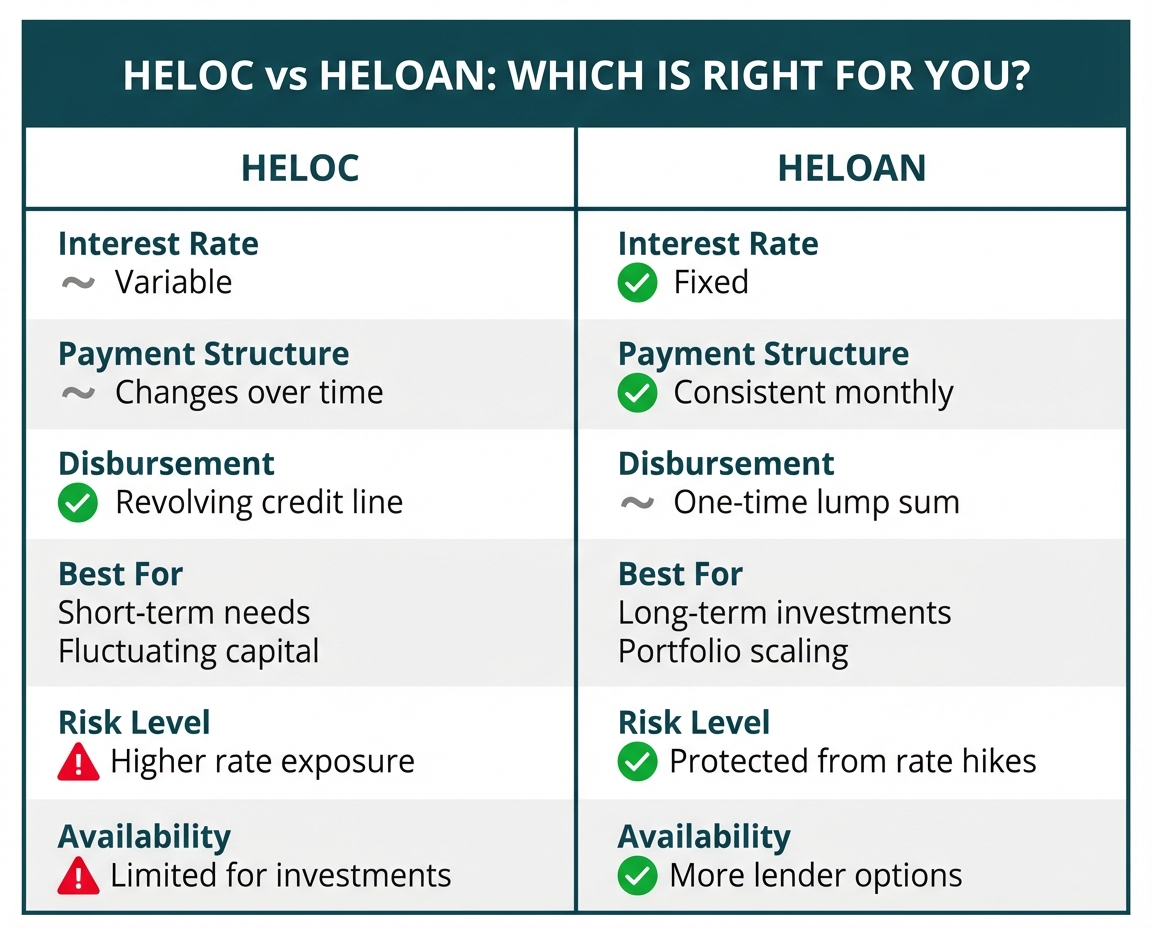

Alternatives to Interest-Only HELOCs: Why HELOANs May Be Better for Investors

When it comes to financing your investment properties, interest-only HELOCs aren't your only option. Home Equity Loans (HELOANs) bring some real advantages to the table—especially if you're a real estate investor ready to grow your portfolio.

Fixed-Rate, Lump-Sum Second Liens

Here's the deal: unlike HELOCs with their variable rates, HELOANs give you a one-time lump sum at a fixed interest rate for the life of the loan. That means you can plan with confidence—you'll know exactly what you're borrowing and what your payments will be from start to finish.

The fixed-rate structure protects you from market swings that can really shake up variable-rate products like HELOCs. According to Bankrate, HELOC rates hit recent lows at 7.31% as of February 2026, but here's the catch—those rates can shift dramatically with market conditions, leaving long-term investors guessing.

Predictable Payment Schedule

With a HELOAN, you get a straightforward amortization schedule with equal monthly payments throughout your loan term. This makes budgeting simple and reliable—and that's a game-changer when you're juggling multiple investment properties.

Here's what the payment structure typically looks like:

- Fixed monthly payment amount

- Consistent portion going to principal and interest

- Clear payoff date locked in from the start

Advantages for Landlords Scaling Portfolios

If you're managing several properties or gearing up to expand, HELOANs offer some standout benefits:

Simplified Cash Flow Management: Fixed payments across your properties make it easier to project your expenses and returns accurately.

Reduced Administrative Burden: Juggling multiple HELOCs—each with different draw periods, variable rates, and repayment timelines—gets complicated fast as your portfolio grows.

Long-Term Planning Capability: Here's the thing about HELOANs—their predictable nature puts you in the driver's seat. You can map out your investment strategy years ahead without losing sleep over payment shock or surprise rate jumps.

Risk Mitigation: Fixed rates act as your shield against interest rate hikes that could otherwise eat into your rental property cash flow.

Comparison: HELOANs vs. HELOCs for Investors

| Feature | HELOAN | HELOC |

|---|---|---|

| Interest Rate | Fixed | Variable (typically Prime + margin) |

| Disbursement | One-time lump sum | Revolving credit line |

| Payment Structure | Fixed monthly payments | Variable, interest-only during draw period |

| Predictability | High | Low to moderate |

| Best for | Long-term investments, portfolio scaling | Short-term needs, fluctuating capital requirements |

| Risk Level | Lower interest rate risk | Higher exposure to rate fluctuations |

| Administrative Complexity | Low | Increases with portfolio size |

Scenarios Where HELOANs Are Superior

Let's break down when HELOANs really work in your favor:

Portfolio Expansion: Growing your property count? The predictable payment structure of HELOANs makes calculating debt service coverage ratios straightforward—and that helps you qualify for your next deal.

Buy-and-Hold Strategy: If you're in it for the long haul, fixed rates mean your costs stay locked in while your investment returns stay protected.

Major Renovation Projects: Got a big rehab with a clear budget? The lump-sum disbursement gives you all the capital you need upfront—no guesswork required.

Debt Consolidation: Juggling multiple high-interest property debts? Rolling them into a single, lower-interest HELOAN simplifies your finances and saves you money.

Recession-Proofing: When the economy gets shaky, fixed-rate products deliver the stability that variable-rate options simply can't offer.

As noted by Cornerstone Bank, investment property equity lines typically have higher rates than primary residences, with rates starting around 7. 75% (Prime plus a margin). This premium makes the fixed-rate advantage of HELOANs even more attractive if you're serious about streamlining your financing strategy.

HELOCs certainly have their place for some investors, but if you're focused on growing a solid real estate portfolio without the guesswork, HELOANs often come out on top with their straightforward, predictable payments.

Other Financing Options Worth Considering

Interest-only HELOCs can be a useful tool, but they're not always the best fit for every investor. Let's walk through some alternatives that might align better with your investment approach, timeline, and goals.

DSCR Loans

If you own rental properties, Debt Service Coverage Ratio (DSCR) loans deserve your attention. These loans flip the script on traditional financing—instead of scrutinizing your personal income, lenders look at whether your property can pay for itself.

Here's what makes them stand out:

- Your property's income does the talking, not your W-2

- Finance as many properties as you want—no arbitrary limits

- Get to closing faster than with conventional loans

- Skip the tax returns and employment paperwork

The magic number? A 1.25 DSCR ratio, meaning your property needs to bring in 25% more than its debt payments. Got a solid rental with reliable tenants? This could be your sweet spot.

"DSCR loans are qualified based on the property's income rather than the borrower's personal income, making them accessible to investors with multiple properties or complex tax situations," according to[The Federal Savings Bank.

HELOANs (Home Equity Loans)

Think of HELOANs as the steady, reliable cousin to HELOCs. You get your funds in one lump sum, lock in a fixed rate, and enjoy the same payment month after month. This predictability makes them especially appealing if you're building a long-term investment strategy.

Advantages for investors:

- Fixed interest rates shield you from market swings

- Consistent payment amounts make budgeting straightforward

- One-time funding works perfectly for major renovations or property acquisitions

- Often lower closing costs than refinancing options

"HELOANs offer fixed rates and predictable payments, making them better for landlords scaling their portfolios compared to HELOCs, which become riskier to manage with larger portfolios due to their variable nature," notes Truss Financial Group.

Cash-Out Refinancing Options

Cash-out refinancing lets you unlock the equity you've built by replacing your current mortgage with a new, larger loan. You pocket the difference as cash to fund property improvements, new investments, or other business needs.

Strategic considerations:

- Often delivers lower interest rates than HELOCs or HELOANs

- Consolidates your financing into a single loan

- May extend your loan term, which can lower monthly payments

- Typically allows higher loan amounts compared to second liens

This approach works especially well if you purchased properties several years ago and have built solid equity through appreciation and mortgage pay-down.

Private Lending Arrangements

Looking for flexibility outside traditional lending channels? Private lending offers customized solutions with terms you can negotiate.

Benefits of private lending:

- Faster funding timelines

- More flexible qualification requirements

- Ability to finance properties that don't meet conventional standards

- Potential for interest-only or custom payment structures

Private lenders include individual investors, family offices, or specialized investment groups who understand real estate investing and can structure deals that fit your business model.

Business Lines of Credit

If you're a seasoned investor with an established business entity, a business line of credit could be your ticket to flexible funding—no real estate collateral required.

Here's why investors love them:

- They're not tied to specific properties

- You can use the funds for various business needs

- Many come with interest-only payment options

- You may enjoy tax benefits when using funds for business expenses

Cross-Collateralization Strategies

Ready to level up? Cross-collateralization lets you use multiple properties to secure a single loan or line of credit. Instead of tapping equity property by property, you're unlocking value across your entire portfolio.

Why this strategy works:

- You can access higher loan amounts

- Lenders often reward you with lower rates since their risk drops

- Fewer loans mean simpler management

- Those fully-paid properties? Now they're working harder for you

Every financing option brings something different to the table. The right choice depends on your goals, your timeline, and how much risk you're comfortable with. And here's the thing—your ideal solution will likely shift as your portfolio grows and the market changes.

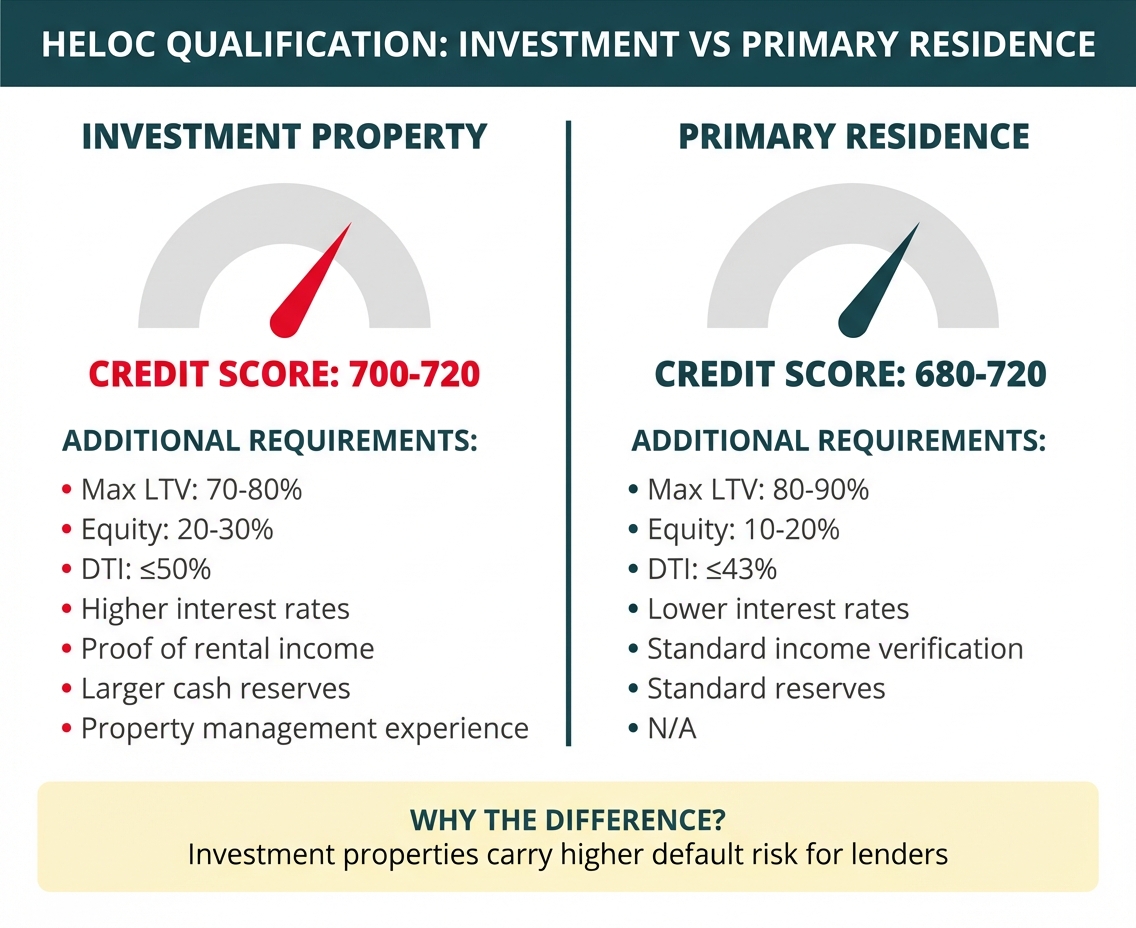

What Credit Score Do You Need for an Interest-Only HELOC on Investment Property?

Let's talk numbers. When you're going after an interest-only HELOC for an investment property, lenders hold you to a higher standard than they would for your primary home. Knowing what you're up against helps you prepare.

Credit Score Requirements

Most lenders want to see a credit score between 700-720 for investment property HELOCs. That's noticeably higher than the 680-720 range for primary residences. Why the difference? Lenders view investment properties as riskier bets.

Here's how Bankrate breaks it down:

| HELOC Criteria | Investment Properties | Primary Residences |

|---|---|---|

| Credit Score Minimum | 700-720 | 680-720 |

Bankrate explains that these tougher standards help lenders protect themselves when the property isn't owner-occupied.

Debt-to-Income (DTI) Considerations

Your debt-to-income ratio plays a big role in your approval odds. Most lenders want to see your DTI at 50% or below for investment property HELOCs, though this varies from lender to lender. Simply put, this number shows how much of your monthly gross income goes toward paying off debts.

Equity Requirements and LTV Restrictions

When it comes to investment properties, lenders want to see more skin in the game:

- You'll typically need at least 15-20% equity in your property

- Maximum loan-to-value (LTV) ratios usually top out at 70-80% for investment properties

- Some lenders get even more conservative, capping LTV at 65% for non-owner occupied properties

According to Better.com, "Investment property HELOCs typically allow a maximum combined loan-to-value (CLTV) ratio of 70-80%, compared to 80-90% for primary residences." The bottom line? You'll need to keep more equity in your investment property than you would in your primary home.

Property Qualification Factors

Not every investment property makes the cut for a HELOC. Here's what lenders look at:

- Property type and condition

- Rental income history and stability

- Location and market conditions

- Number of units (single-family homes typically have an easier path than multi-unit properties)

Documentation Requirements

Get ready to gather your paperwork. You'll likely need:

- Property insurance verification

- Proof of ownership

- Rental agreements or lease contracts

- Property appraisal

Here's the reality: qualifying for an investment property HELOC takes more effort than for your primary residence. Lenders see these loans as higher risk, so they dig deeper before saying yes.

The HELOC Application Process: What to Expect

Getting an interest-only HELOC for your investment property means navigating a clear application process. From start to finish, expect the journey to take 2-6 weeks—but coming prepared can speed things along considerably.

Step-by-Step Application Guide

- Pre-qualification: Most lenders offer a quick initial check to see if you meet their basic requirements—think of it as a first handshake.

- Formal application: Fill out the lender's application with your personal details and property information.

- Document submission: Gather and submit all required financial paperwork (we've got the full list below).

- Property appraisal: The lender arranges for a professional to assess your property's current market value.

- Underwriting: Here's where the lender digs into your application, credit history, and property details.

- Closing: Sign the final documents and wrap up any remaining requirements.

- Funding: Access your new credit line—typically within a few days after closing.

Required Documentation

Here's what you'll need to have ready:

- Proof of identity (government-issued photo ID)

- Property information (deed, mortgage statement, insurance policy)

- Investment property documentation (rental agreements)

- Credit history and score (lenders will pull this with your permission)

Timeline Expectations

According to Chase, "The traditional HELOC process usually takes 2-6 weeks from application to funding, depending on the lender and your financial profile" Chase. Here's how that breaks down:

- Application submission: Same day

- Document review: 2-5 business days

- Property appraisal: 1-2 weeks

- Underwriting: 1-4 weeks (this is where timing varies most)

- Closing and funding: 2-5 business days

Common Approval Challenges

Watch out for these potential roadblocks in your HELOC journey:

- Insufficient equity: Most investment property HELOCs require at least 20-30% equity built up.

- Credit issues: Late payments, high debt-to-income ratio, or recent bankruptcy can slow things down.

- Property type restrictions: Certain lenders may not extend HELOCs for specific investment property categories.

- Title issues: Outstanding liens, judgments, or other claims attached to your property.

Tips for Streamlining Approval

Prepare all documentation in advance: "You can significantly shorten this timeline by applying our acceleration strategies," notes Better, which includes having all paperwork ready before applying.

Check your credit report: Pull your report early and fix any errors before you apply.

Calculate your equity position: Get clear on your loan-to-value ratio before talking to lenders.

Respond quickly to requests: Fast replies to underwriter questions can cut days or even weeks from your timeline.

Consider digital-first lenders: Online lenders often have smoother processes that speed up approval times.

Get pre-approved: This helps you spot potential roadblocks before they slow you down.

Getting familiar with these steps in the HELOC application process puts you in the driver's seat—helping you move faster and boost your chances of approval for your investment property financing.

Why OfferMarket is the Right Partner for Real Estate Investors

Smart real estate investing takes more than money—it takes know-how, speed, and the right tools in your corner. OfferMarket is built specifically for investors like you, offering a full range of services tailored to your real estate investment goals.

Comprehensive One-Stop Shop Approach

OfferMarket gives you a real edge by bringing loans, listings, and insurance together in one place. This all-in-one approach means you skip the hassle of juggling multiple providers, saving you time and cutting through the complexity.

As industry experts point out, "The one-stop shop model is here to stay... From all the big benefits to some top options, consolidating services under one provider streamlines the entire investment process" Motto Mortgage. This model is especially powerful for real estate investors who need to act fast when the right opportunity comes along.

Financial Solutions Built for Investors

Here's the thing: OfferMarket isn't your typical retail lender. We get what real estate investors actually need. Whether you're exploring HELOAN, or DSCR loan, our team will help you find the financing option that fits your investment strategy and portfolio goals.

We don't believe in cookie-cutter solutions. Instead, we take a consultative approach—matching you with financing that works for your specific timeline and cash flow needs. It's about finding the right fit, not the fastest sale.

A Streamlined Process That Saves You Money

When you work with multiple providers, costs add up—administrative fees, hidden charges, the works. By bringing everything under one roof, OfferMarket cuts out those unnecessary expenses. As industry experts point out, "By consolidating services under one roof, you eliminate unnecessary administrative costs and hidden fees. A transparent pricing structure ensures you know exactly what you're paying for"

Plus, a streamlined process means faster approvals and quicker closings. In competitive markets, that speed can be the difference between landing a great deal and watching it slip away.

Real Market Knowledge You Can Count On

Our team brings deep experience in real estate investment financing. We understand both the lending side and the day-to-day realities of property investing. That means we can spot challenges before they become problems and offer solutions that balance your immediate needs with your long-term goals.

If you're weighing an interest-only HELOC against other financing options, this expertise matters. We'll help you understand the trade-offs and steer clear of common pitfalls.

Access to Multiple Financing Options

OfferMarket gives you access to a variety of financing solutions designed for different investment scenarios:

- HELOANs for investors who want predictable, fixed payments

- DSCR loans for rental property acquisitions

- Fix and Flip loans for short-term renovation projects

- Portfolio financing for experienced investors with multiple properties

Having these options at your fingertips means you'll never have to settle for financing that doesn't match your investment strategy just because nothing else is available.

Commitment to Investor Success

OfferMarket's business model is centered on building long-term relationships with investors like you. Instead of chasing transaction volume, the company focuses on your outcomes—because successful investors become repeat clients and referral sources.

This alignment of interests means OfferMarket is genuinely motivated to help you find the right financing solution for your specific needs, whether that's a HELOAN or another option that better fits your investment strategy.

Scheduling a Consultation with OfferMarket

Before you apply for an interest-only HELOC, connect with OfferMarket's financing specialists. Our team knows real estate investor financing inside and out, and we can help you:

- Figure out if an interest-only HELOC is the right move for your situation

- Pinpoint which properties in your portfolio are best suited for tapping equity

- Calculate how much equity you can realistically access

- See how this financing fits into your bigger investment picture

Think of OfferMarket's team as your personal guides—we offer tailored advice that generic online resources simply can't match.

Resources for Further Education on Real Estate Financing

Ready to keep learning? Here are some great ways to deepen your knowledge of real estate financing:

- Industry webinars and workshops

- Real estate investor associations

- Financial modeling tools specific to investment properties

- Networking with experienced investors who have successfully used HELOCs

The more you understand your financing options, the smarter your investment decisions become. Knowledge is your best tool for growing and managing a successful portfolio.

OfferMarket Loans

Check your rate

60 seconds · no credit pull