*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How to Flip Houses in 2026: Your Complete Step-by-Step Guide

House flipping remains one of the most exciting ways to build wealth through real estate, even as the market continues to evolve in 2025. But here's the reality: successful flipping isn't about what you see on TV. It takes strategic planning, solid financing, and the right partners in your corner.

This comprehensive guide walks you through every step of the house flipping process—from finding your first property to closing a profitable sale. Whether you're brand new to real estate investing or looking to scale your existing portfolio, you'll find actionable strategies and insider knowledge to help you flip smarter and more profitably.

New Section

Here is the comprehensive set of DSCR loan requirement tables based on the provided guidelines, formatted strictly in Markdown.

1. Cash Flow & Rent Requirements

| Label | Value / Cutoff / Rule |

|---|---|

| DSCR Formula | Gross Rental Income ÷ Qualifying PITIA (Principal, Interest, Taxes, Insurance, HOA). |

| Standard Minimum DSCR | 1.00x (Income covers debt). |

| Absolute Minimum DSCR | 0.75x (Available on specific programs like Product B, G, H, & Deephaven; often requires lower LTV & higher reserves). |

| Portfolio/Blanket Min DSCR | 1.15x - 1.20x (Aggregate portfolio coverage). |

| Short-Term Rental (STR) Min DSCR | 1.00x - 1.25x (Varies by program; Product B requires 1.25x, Product H allows 1.00x). |

| Rent Calculation (Long-Term) | Lesser of Actual Lease or Market Rent (Appraisal Form 1007). |

| Rent Calculation (Short-Term) | 12-month average actuals OR AirDNA projection (Purchase). Often requires a 20% expense haircut (multiply gross by 80% to find net income). |

| Rent Calculation (Unleased/Vacant) | 75% - 100% of Market Rent (Purchase usually 100%; Refinance often capped at 90% or 75%). |

| Lease Term Requirement | Long-term leases must generally be 12 months. Month-to-month allowed if rolled from original term. |

2. Asset & LTV Requirements

| Label | Value / Cutoff / Rule |

|---|---|

| Max LTV (Purchase/Rate-Term) | 80% (Typically requires FICO ≥ 680-700). |

| Max LTV (Cash-Out) | 70% - 75% (Standard). Often capped at 65% if DSCR < 1.00x. |

| Max LTV (Foreign National) | 60% - 70% (Product G allows up to 70% for Purchase; most others cap at 60-65%). |

| Max LTV (DSCR < 1.00x) | 65% - 75% (Leverage is restricted if property loses money). |

| Standard Reserve Requirement | 3 - 6 Months of PITIA (Varies by loan amount; loans >$1M often require 6-9 months). |

| Foreign National Reserves | 12 Months of PITIA. |

| DSCR < 1.00 Reserve Req | 6 Months of PITIA. |

| Cash-Out Seasoning | 6 Months on title required to use new appraised value (standard). Between 3-6 months often capped at cost basis. |

| Delayed Financing Cap | If owned < 6 months, loan amount capped at Cost Basis (Purchase Price + Documented Rehab). |

| Minimum Loan Amount | $75,000 - $100,000 (Varies by program; loans <$150k often require higher DSCR). |

| Small Loan Restriction | Loans < $150,000 often require 1.25x DSCR. |

3. Borrower & Entity Requirements

| Label | Value / Cutoff / Rule |

|---|---|

| Minimum FICO (Standard) | 680 (Unlocks most 75-80% LTV tiers). |

| Absolute Minimum FICO | 600 - 640 (Severely restricts LTV to ~60-65% or 70%). |

| FICO for STR Income | 720 (Often required to use AirDNA/STR income for qualification). |

| Eligible Entities | US LLCs, Corporations, Partnerships. (Foreign entities not allowed). |

| Ineligible Entities | Irrevocable Trusts, Land Trusts, Non-Profits/501(c)3. |

| Recourse Type | Full Recourse (Personal Guaranty required). Non-Recourse no longer available for portfolios per update. |

| Guarantor Ownership % | Any member owning ≥ 20-25% must sign Personal Guarantee. |

| First-Time Investor | Allowed but restricted: Max 75% LTV. Cannot use STR income. Cannot do Blanket loans. |

| First-Time Home Buyer | Ineligible (Must own a primary residence or other property). |

| Credit History (Mortgage) | 0x30x12 (No late mortgage payments in last 12 months). |

| Derogatory Event Seasoning | 36 - 48 Months (Bankruptcy, Foreclosure, Short Sale must be seasoned). |

| Foreign Nationals | Allowed. Must have valid Passport & Visa. Funds must be in US bank for 30+ days. |

4. Pitfalls & Edge Case Scenarios

| Label | Value / Cutoff / Rule |

|---|---|

| Vacant Property Refinance | 5% LTV Reduction typically applied if property is unleased at closing. |

| Declining Market | 5% LTV Reduction if appraisal indicates declining market. |

| Rural Properties | Ineligible or capped at 65% LTV. Cannot use STR income. |

| Flip Rule (Sales < 90 Days) | If seller owned < 90 days and price rose > 10%, 2nd Appraisal is required. |

| Short-Term Rental (STR) | Ineligible if First-Time Investor or DSCR < 1.00x. |

| Listing History | Cash-Out ineligible if property listed for sale in last 6 months (must be withdrawn). |

| Prepayment Penalty (PPP) | Allowed (1-5 Years). Restricted/Prohibited in: AK, MN, NM. Restricted thresholds in PA & OH. |

| Crypto Assets | Generally Ineligible for down payment unless liquidated to USD in US bank. Reserves @ 60% value. |

| "Bad Boy" Carve-outs | Required on all loans (even if non-recourse exceptions granted). Triggers full liability for fraud/waste. |

| Layered Entities | Guarantor must own ≥ 25% of every layer (Parent LLC -> Child LLC -> Borrower LLC). |

| Condotel / Co-op | Ineligible property types (unless specific non-warrantable exception applies). |

| State Specifics (FL) | Condo projects > 30 years old (or 25 near coast) & 5+ stories require Milestone Inspection. |

![**Task:** Create a professional hero infographic that visualizes the complete house flipping journey from start to finish, showing the 5 main phases with timeline and key metrics.

**Visual Structure:** Horizontal timeline flow chart spanning the full width of the image, with 5 distinct phases connected by arrows, each phase containing an icon, title, timeline duration, and 2-3 key bullet points.

**ASCII Layout Reference:**

```

┌─────────────────────────────────────────────────────────────────────────────┐

│ THE HOUSE FLIPPING JOURNEY 2025 │

├─────────────┬─────────────┬─────────────┬─────────────┬─────────────────────┤

│ PHASE 1 │ PHASE 2 │ PHASE 3 │ PHASE 4 │ PHASE 5 │

│ [SEARCH] │ [FINANCE] │ [RENOVATE] │ [STAGE] │ [SELL] │

│ │ │ │ │ │

│ 3-6 months │ 2-4 weeks │ 2-6 months │ 1-2 weeks │ 1-3 months │

│ │ │ │ │ │

│ • Research │ • Get pre- │ • Execute │ • Photo- │ • List property │

│ • Analyze │ approved │ scope │ graphy │ • Show & negotiate │

│ • Evaluate │ • Close │ • Manage │ • Stage │ • Close sale │

│ │ deal │ quality │ home │ │

└─────────────┴─────────────┴─────────────┴─────────────┴─────────────────────┘

Average Total Timeline: 9-15 months

Average Gross Profit 2024: $72,000

```

**Image Section Breakdown:**

- Header section: White background with](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1770916375807_z8wx3q.jpg?alt=media&token=8925441d-3aac-426d-80a8-77099b11af82)

Introduction to House Flipping: The Art of Profitable Real Estate Transformation

House flipping is a straightforward concept: buy a property below market value, renovate it strategically, and sell it for a profit—usually within six months to a year. This investment approach has drawn countless entrepreneurs and investors looking to build wealth through real estate, and for good reason. When done right, the returns can be impressive.

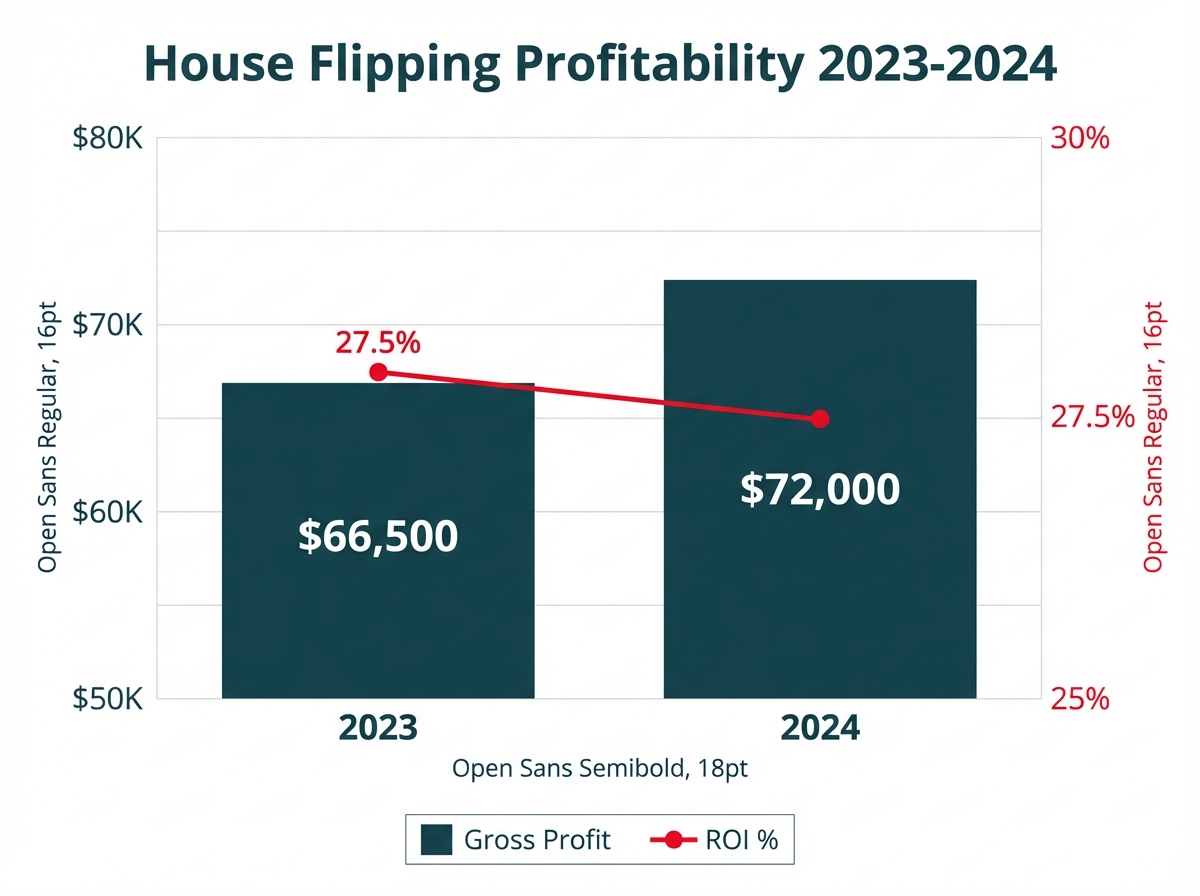

Let's talk numbers. Despite recent market shifts, house flipping still delivers solid profits. In 2023, the typical flip generated a 27.5% return on investment before expenses—that's an average gross profit of $66,500 per property. By 2024, gross profits climbed to $72,000, even though profit margins stayed near decade lows.

But here's what those numbers don't tell you. Making money in house flipping takes more than buying low and selling high. You need a solid game plan that covers:

- In-depth market knowledge: Knowing your local real estate trends, understanding neighborhood dynamics, and accurately assessing property values

- Financial acumen: Lining up the right financing, creating realistic renovation budgets, and calculating your true ROI

- Project management expertise: Keeping contractors on track, managing timelines, and maintaining quality standards

- Risk assessment capabilities: Spotting potential problems early and having backup plans ready

Here's the reality check on timing. Finding the right properties might take months or even years of searching. Building relationships with reliable lenders often takes several years. And assembling a trustworthy contractor network? That can easily require a decade of learning who delivers and who doesn't.

This is where OfferMarket becomes your go-to partner for house flipping success. We've built a complete platform that brings together fix-and-flip loans, free property listings, and insurance solutions designed specifically for investors like you. The result? You spend less time on paperwork and logistics, and more time finding and flipping great properties. Whether you're tackling your first flip or you're ready to scale up your portfolio, OfferMarket gives you the tools and support to flip smarter and more profitably.

Here's the reality of today's market: yes, higher interest rates and property values have tightened margins in some areas. But they've also created real opportunities—motivated sellers are out there, and smart investors are finding deals. With the right strategy and the right partners in your corner, house flipping is still one of the most effective ways to build wealth through real estate.

The House Flipping Process: Buy, Renovate, Sell

Let's break down what house flipping actually looks like. The formula is simple: buy a property below market value, renovate it strategically, and sell it for a profit. Simple to understand, but successful execution takes planning, patience, and a solid grasp of each phase.

Understanding the Buy-Renovate-Sell Cycle

1. Acquisition Phase (3-6 months) Expect to spend about 30-40% of your total project time here. This is where you'll focus on:

- Researching markets and hunting for properties

- Getting your financing lined up and approved

- Conducting thorough due diligence and inspections

- Negotiating the deal and closing

Here's something experienced flippers know: finding the right property can take up to six months. That's not wasted time—it's smart investing. Patience here means you're choosing properties with real profit potential instead of jumping into money pits.

2. Renovation Phase (2-6 months) This phase takes up roughly 40-50% of your time and covers:

- Locking in your renovation plans and pulling permits

- Finding, hiring, and managing reliable contractors

- Sourcing materials and keeping your supply chain moving

- Staying on top of quality and solving problems as they pop up

Your timeline here depends on the work involved. A cosmetic refresh might wrap up in 6-8 weeks, while major structural work could stretch to 4-6 months.

3. Selling Phase (1-3 months) The final 20-30% of your time investment goes toward:

- Staging and photography

- Marketing and showing the property

- Negotiating with potential buyers

- Closing the sale

Financial Structure of a Successful Flip

Smart house flipping starts with solid financial planning. Here's what you need to know:

Initial Capital Requirements:

- Down payment (typically 20-30% for fix-and-flip loans)

- Closing costs (3-5% of purchase price)

- Renovation budget (varies widely)

- Carrying costs during ownership (mortgage payments, utilities, insurance)

Financing Options:

- Fix-and-flip loans (shorter terms, higher interest rates)

- Hard money loans (quick funding, higher costs)

- Private lenders or partnerships

- Cash (optimal for maximum returns)

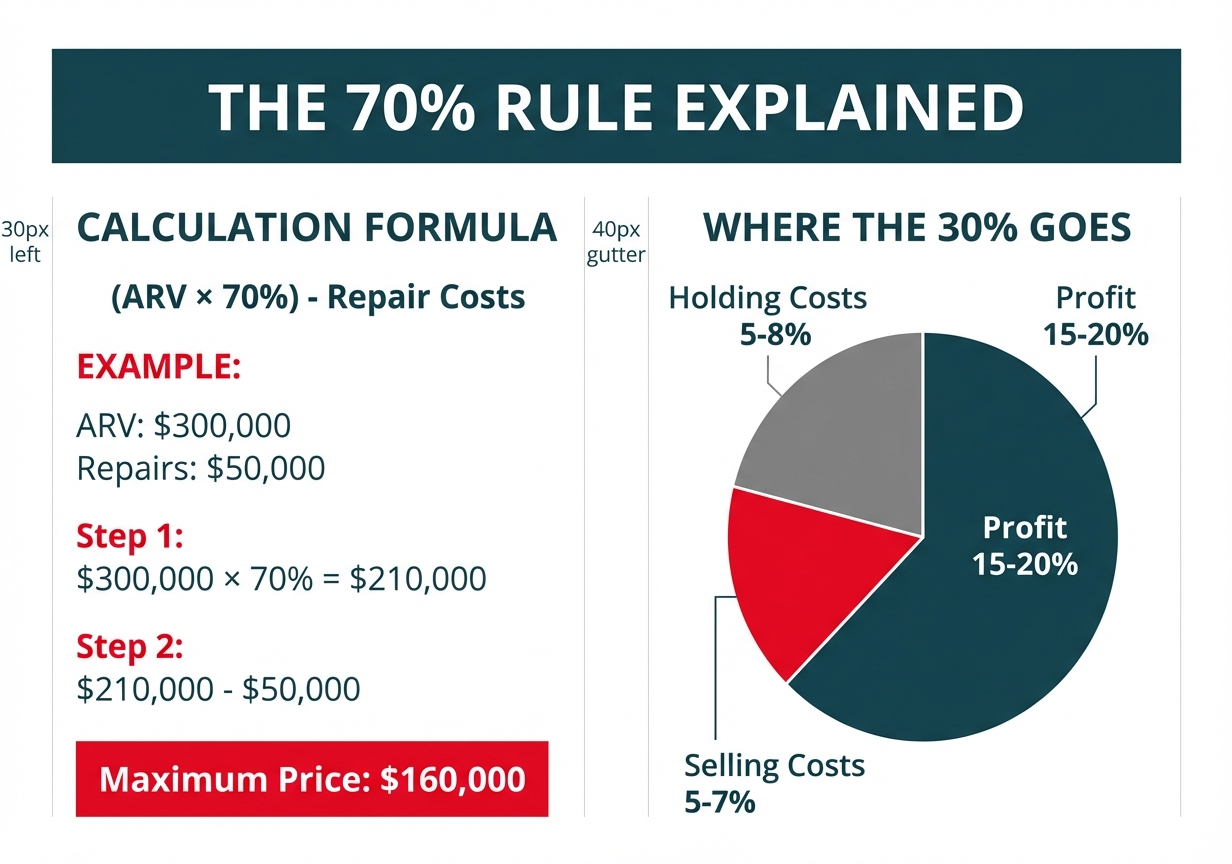

The 70% Rule Explained

The 70% rule is your go-to guideline for determining the maximum purchase price on a potential flip. Here's how it works:

Maximum Purchase Price = (ARV × 70%) - Repair Costs

Where:

- ARV (After-Repair Value) is what the property will be worth after renovations

- Repair Costs are your estimated renovation expenses

Let's walk through an example. Say a property's ARV is $300,000 and it needs $50,000 in repairs:

- Maximum Purchase Price = ($300,000 × 70%) - $50,000

- Maximum Purchase Price = $210,000 - $50,000 = $160,000

That 30% margin protects you by covering:

- Holding costs (mortgage payments, utilities, insurance)

- Selling costs (agent commissions, closing costs)

- Profit margin (typically 15-20%)

According to Investopedia, "Professional flippers often use the '70% rule': Never pay more than 70% of a property's after-repair value minus renovation costs".

Here's the reality though: in today's competitive markets, the 70% rule sometimes needs adjusting. As inventory tightens, experienced flippers may work with narrower margins, using a 75-80% rule instead. Your local market conditions and experience level will help you determine what works best for your situation.

Tax Implications of House Flipping

House flipping carries significant tax considerations:

- Short-term capital gains: Properties held less than a year are taxed as ordinary income, which can be substantially higher than long-term capital gains rates

- Self-employment taxes: If flipping is your primary business, you may be subject to an additional 15.3% self-employment tax

- Deductible expenses: Many costs associated with flipping are deductible, including:

- Renovation expenses

- Holding costs (interest, insurance, utilities)

- Marketing and selling costs

- Business expenses (mileage, home office, etc.)

Getting a handle on these tax implications is essential for accurately calculating your potential profit and setting up your flipping business the right way.

The house flipping process demands a solid time commitment across all phases, smart financial planning, and strategic use of principles like the 70% rule to keep your deals profitable in this competitive investment space.

Step 1: Research the Market - Finding Your Flip Opportunity

House flipping success begins long before you pick up a hammer—it starts with doing your homework on the market. In fact, experienced investors often spend up to a year researching markets before making their first purchase in a new area. This upfront investment of time pays off by lowering your risk and boosting your potential returns.

Identifying Profitable Flip Markets

The best house flipping opportunities are found in neighborhoods with these key characteristics:

- Strong appreciation trends - Look for areas with consistent 3-5% annual price growth

- Reasonable acquisition costs - Entry prices that leave room for a profitable exit after renovation

- High demand - Areas where listings don't sit long on the market

- Renovation potential - Neighborhoods with older housing stock ready for updates

- Neighborhood improvement signs - New businesses, infrastructure projects, or school improvements

According to research from WalletHub, cities with the best house-flipping potential balance renovation costs with market potential and quality of life factors across 26 key indicators.

How to Analyze Neighborhoods for Flipping Potential

When you're zeroing in on specific neighborhoods, keep these key metrics on your radar:

- Sales-to-list price ratio - Higher percentages point to stronger seller's markets

- Average days on market - The lower, the better for quick turnarounds

- Inventory levels - Tight inventory typically means stronger demand

- Price trends by property type - Pinpoint which housing types are gaining value fastest

- Renovation activity - Other flips nearby can be a green light for opportunity

- School ratings - Quality schools consistently boost property values

- Crime statistics - Dropping crime rates often signal a neighborhood on the rise

Don't underestimate the power of local knowledge here. As seasoned investors on BiggerPockets point out, "Local real estate agents and property managers are often the best sources of information about a neighborhood. They can provide insights that aren't available through online research".

Essential Market Research Tools

Smart flippers use a mix of digital and traditional research methods:

- Property listing platforms - OfferMarket's listing map, Zillow, Redfin

- Public records - Tax assessments, building permits, foreclosure data

- Neighborhood analytics - Walk Score, AreaVibes, City-Data

- Rental rate analysis - Rentometer, Zillow Rental Manager

- Renovation cost calculators - OfferMarket's fix and flip calculator

- Local news sources - For development plans and neighborhood trends

- Social media groups - Local real estate investment clubs and forums

Using OfferMarket's Tools for Market Research

OfferMarket gives you specialized tools built with house flippers in mind:

- Interactive Listings Map - Filter properties by location, price, and potential ROI

- Zip Code Alerts - Get instant notifications when new properties pop up in your target areas

- Fix and Flip Calculator - Map out renovation costs, holding expenses, and potential profits

- Direct Seller Communication - Reach motivated sellers without going through agents

- Market Trend Reports - Tap into data on neighborhood appreciation rates and sales metrics

- Insurance Quote Integration - Build accurate insurance costs into your investment numbers

Here's a pro tip: the most successful flippers spend 20-30% of their total project time on research before making any offers. This upfront investment dramatically boosts your success rates and helps you sidestep costly mistakes when choosing properties.

Keep in mind that market conditions shift constantly—what made a neighborhood perfect for flipping last year might not hold true today. Build a consistent research routine and revisit your market assumptions regularly so you can stay ahead of the curve.

Step 2: Secure Financing for Your House Flip

Getting the right financing in place is arguably the most critical step in your house flipping journey, and one that might take years to master as you build relationships with reliable lenders. Without proper funding lined up, even the most promising property opportunity can slip right through your fingers. Fix and flip loans are specialized financial products designed specifically for real estate investors like you who want to purchase, renovate, and sell properties for profit.

Understanding Fix and Flip Loans

Fix and flip loans are short-term financing solutions built around the unique needs of house flippers. Unlike conventional mortgages, these loans cover both the purchase price and renovation costs, making them a smart choice for investors who need quick access to capital.

According to recent data, the average interest rate for fix and flip loans ranges from 10.50% to 14%, with the average sitting around 11.50% as of late 2023. These rates run higher than traditional mortgages because of the increased risk and short-term nature of the loans.

Here's what you need to know about fix and flip loans:

- Loan Terms: Typically 6-18 months

- Loan-to-Value Ratio (LTV): Usually 65-90% of the purchase price

- Loan-to-Cost Ratio (LTC): Can cover up to 95% of total project costs

- Origination Fees: 1-3% of the loan amount

- Funding Speed: Often close within 7-14 days (compared to 30-45 days for conventional loans)

Comparing Financing Options for House Flippers

While fix and flip loans are popular, they're not your only option:

Hard Money Loans: Think of these as fix and flip loans' close cousin, typically funded by private investors. You'll see interest rates between 9% and 15%

Conventional Mortgages: The trade-off here is clear—lower interest rates (around 6-7% for investment properties) but you'll face stricter qualification hoops and longer waits to close

Home Equity Loans (HELONs): A smart play if you've built up solid equity in property you already own. You'll enjoy lower interest rates, though you're capped by your available equity

Private Money: This means partnering with individual investors. The upside? Terms are often negotiable. The catch? Costs can run higher

Cash: Straightforward and interest-free, but here's the reality—it ties up capital you could be spreading across multiple deals

Qualification Requirements for Fix and Flip Loans

Here's what lenders are looking at when you apply for a fix and flip loan:

- Credit Score: Aim for 680 or higher, though some lenders offer flexibility for lower scores

- Experience: Flipping experience helps, but don't worry if you're just starting out

- Down Payment: Plan on bringing 10-25% of the purchase price to the table

- Property Potential: Lenders want to see strong ARV (After-Repair Value) and a solid location

- Exit Strategy: Show them your clear roadmap for renovations and the eventual sale

OfferMarket's Competitive Loan Products

OfferMarket has built fix and flip loan products specifically to help you move faster and smarter:

- Higher LTC Ratios: Access up to 90% of your purchase and renovation costs

- Competitive Interest Rates: Starting at 9.75%**—that's below what most lenders offer

- Streamlined Application Process: Get pre-approved in as little as 24 hours

- Flexible Qualification Requirements: We work with investors at every experience level

- Draw Schedule Flexibility: Your renovation timeline drives the schedule, not ours

Here's what makes OfferMarket different: we bring financing, property listings, and insurance solutions together in one place. That means you skip the years of relationship-building with multiple providers and get straight to growing your portfolio.

Securing Pre-Approval Before Property Hunting

Getting pre-approved for financing before searching for properties gives you several advantages:

- Increased Negotiating Power: Sellers take pre-approved buyers more seriously

- Defined Budget: You'll know exactly what you can afford

- Faster Closing: Less waiting between offer acceptance and funding

- Competitive Edge: You can move quickly when the right property comes along

Here's how to secure pre-approval through OfferMarket:

- Complete the online application

- Submit required documentation (proof of income, assets, credit history)

- Receive your pre-approval letter with loan terms

- Start your property search with confidence

Understanding Loan Terms and Fees

Knowing the costs associated with your financing helps you project profits accurately:

- Interest Rate: The percentage charged on your outstanding loan balance

- Origination Fee: Upfront charge for processing the loan (typically 1-3%)

- Draw Fees: Charges for each disbursement of renovation funds

- Extension Fees: Costs for extending the loan term if needed

- Prepayment Penalties: Fees for paying off the loan early (good news—OfferMarket loans have none), refinance anytime without any prepayment penalties.

- Closing Costs: Title insurance, appraisal fees, and other closing expenses

When you understand these costs upfront, you can build them into your project budget and protect your profit margin from unwelcome surprises.

With the right financing through OfferMarket, you'll be ready to act fast when you spot that perfect flip opportunity—and you'll have terms designed to maximize your return on investment.

Finding and Evaluating the Right Property for Flipping

Spotting undervalued properties is one of the most important skills you can develop as a house flipper. While many investors struggle to find these hidden gems consistently, successful flippers use systematic approaches that give them a real advantage in competitive markets.

What Makes a Property "Undervalued"?

An undervalued property is one priced significantly below its current or potential market value based on comparable sales data and its highest and best use potential. Simply put, these are opportunities where you can add value through smart improvements and sell at a profit.

According to real estate financing experts, "To determine if a property is undervalued, compare its price with similar properties in the area, consider its condition, and evaluate its potential for appreciation". This assessment takes both solid data analysis and a trained eye for spotting potential.

Proven Methods for Finding Flip-Worthy Properties

1. Leverage Online Real Estate Platforms

- Popular sites like Zillow, Realtor, and Redfin let you search by price, location, and property type

- Set up alerts for price drops and new listings in your target neighborhoods

- Keep an eye out for properties sitting on the market longer than usual

2. Utilize OfferMarket's Specialized Platform Features

- Real-Time Alerts: Set up zipcode-specific alerts to get notified within seconds when potential flip properties become available

- Customized Filtering: Use OfferMarket's map interface to filter properties by your investment criteria including price range, property type, and condition

- Direct Seller Communication: Reach out to property owners directly through the platform without agent intermediaries, potentially saving you thousands in commission fees

- Streamlined Offer Submission: Submit offers directly through the platform, speeding up your acquisition process

3. Target Distressed Properties

- Pre-foreclosures and bank-owned properties often sell below market value

- Properties with delinquent taxes or code violations may signal motivated sellers

- Estate sales frequently offer below-market deals as heirs often prioritize quick sales

4. Research Public Records

- Property tax records can reveal owners facing financial difficulties

- Building permits can indicate incomplete renovation projects

- Divorce filings sometimes lead to quick property sales at reduced prices

According to Goliath Data, investors should "Start with Public Records" and then "Cross-Check With Zillow or Redfin" to validate potential opportunities (Goliath Data).

How to Evaluate Property Potential on OfferMarket's Marketplace

Found a property that catches your eye on OfferMarket? Here's a straightforward process to help you assess whether it's worth pursuing:

1. Start With the Photos

- Look past the surface-level stuff and focus on the bones of the property

- New to flipping? Stick with properties that just need cosmetic love—fresh paint, new floors, updated fixtures

- Got some experience under your belt? Structural projects can mean bigger profits, but know that you're taking on more risk

2. Dig Into the Property's History

- Review the property details carefully

- Look for price drops—they often signal a motivated seller

- Check past sale prices on Zillow to get a sense of how value has changed over time

3. Scope Out the Neighborhood

- Compare the property to similar nearby listings

- Estimate your ARV (After Repair Value) by looking at what renovated homes are selling for

- Keep an eye on neighborhood trends that could boost your property's value down the road

4. Watch for These Red Flags

- Foundation problems (cracks, floors that aren't level)

- Signs of water damage (stains, mold, that musty smell)

- Old electrical systems (knob and tube wiring, underpowered service panels)

- Outdated plumbing (galvanized pipes, weak water pressure)

- Structural concerns (sagging roofs, walls that lean)

How to Make Strong Offers Through OfferMarket

OfferMarket's direct offer system puts you in the driver's seat:

- Craft offers with your terms - Build in contingencies for inspections and financing that protect your interests

- Communicate directly with sellers - Ask questions about property condition without information being filtered through agents

- Negotiate efficiently - Adjust offers quickly based on new information

- Close faster - Streamline the purchase process once terms are agreed upon

Time Investment Reality Check

Here's the truth: finding the right property is usually the biggest time commitment in your flipping journey. Most successful investors spend 6-12 months actively searching before landing their ideal flip. Don't let that discourage you—this research phase is where deals are made or broken. Rushing into a purchase without proper evaluation? That's one of the fastest ways to turn a potential profit into a costly lesson.

By tapping into OfferMarket's specialized platform features, you can cut down your research time significantly while still doing your homework on potential properties.

Running the Numbers: Calculating ARV and Renovation Costs

Let's get to the heart of every successful flip: the math. Before you commit to any property, you need to nail down your potential profit. That means understanding ARV (After-Repair Value) and getting realistic about renovation costs. These numbers will tell you whether a deal is worth pursuing—or whether it's time to walk away.

Understanding After-Repair Value (ARV)

Think of ARV as your finish line—it's what your property will be worth once all the renovations are done. This number is the foundation of your entire flip strategy and directly determines your profit margin.

Here's the basic formula:

ARV = Current Property Value + Value Added Through Renovations

But here's the thing: calculating an accurate ARV takes more than plugging numbers into an equation. Industry experts recommend these proven methods:

Comparable Sales Analysis: Look at recently sold properties in the same neighborhood that match what your property will look like after renovations—similar square footage, bedrooms, bathrooms, and features.

Professional Appraisal: When in doubt, bring in a professional appraiser who knows the local market inside and out.

Value-Add Assessment: Estimate how much value each renovation will add to the property.

Market Condition Adjustments: Factor in market trends and seasonality.

As noted by Better, "Comparing similar properties that have recently sold in the area is one of the most common ways to determine ARV".

The 70% Rule: Your House Flipping Safety Net

Smart house flippers swear by the 70% rule. It's a straightforward formula that helps you figure out the maximum you should pay for a property:

Maximum Allowable Offer (MAO) = (ARV × 70%) – Estimated Renovation Costs

Why does this work? That 30% cushion covers your holding costs, selling costs, and profit. According to Wall Street Prep, "The 70% rule is most often used among house flippers, who fix and flip homes in a short timeframe".

Getting Your Renovation Costs Right

Here's the truth: underestimating renovation costs is the number one mistake new flippers make. It can wipe out your entire profit. Here's how to nail this critical step:

- Create a detailed scope of work: Write down every single repair and upgrade the property needs.

- Get multiple contractor bids: Never rely on just one estimate.

- Add a contingency buffer: We recommend padding your renovation budget by 10-20% for surprises.

- Break costs down by category: Keep structural repairs, cosmetic updates, and luxury upgrades separate.

- Research material costs: Prices change, so always get current quotes.

How OfferMarket's Fix and Flip Calculator Makes This Easy

OfferMarket's Fix and Flip Calculator does the heavy lifting for you. Just plug in:

- Purchase price

- Estimated renovation costs

- Holding time and costs

- Expected ARV

- Selling costs

In seconds, you'll see your potential profit margin, ROI, and whether the deal passes the 70% rule test. It's the perfect tool for quickly evaluating multiple properties so you can make confident, informed decisions.

Adjusting Comps for Accurate ARV

When using comparable properties to determine ARV, you'll need to make adjustments for differences between your target property and the comps. Here's what savvy investors account for:

- Square footage (typically $100-150 per square foot in most markets)

- Number of bedrooms and bathrooms

- Lot size and features

- Home condition and age

- Neighborhood desirability

- Special features (pool, garage, etc.)

As one experienced investor notes on Reddit, "The professor explains to adjust each comp to that of the subject property. This includes, square-footage, bathrooms, bedrooms and certain features".

Time Investment: Running the Numbers

Running your ARV and renovation calculations might feel like a lot of work upfront, but this step typically takes about 5-10% of your total time on a flip. Here's the thing: it's arguably the most important phase that separates successful flips from costly mistakes. Seasoned flippers can size up a deal in hours, while those just starting out might need a few days to gather the data and crunch the numbers accurately.

The good news? Once you master these calculations, you'll spot profitable opportunities faster and avoid the deals that look good on the surface but don't pencil out.

Planning High-ROI Renovations for Maximum Profit

Smart renovation planning is where profitable flips are made. The truth is, not all improvements deliver the same bang for your buck. Knowing which projects to prioritize can be the difference between a solid payday and a disappointing return.

Identifying High-ROI Renovation Projects

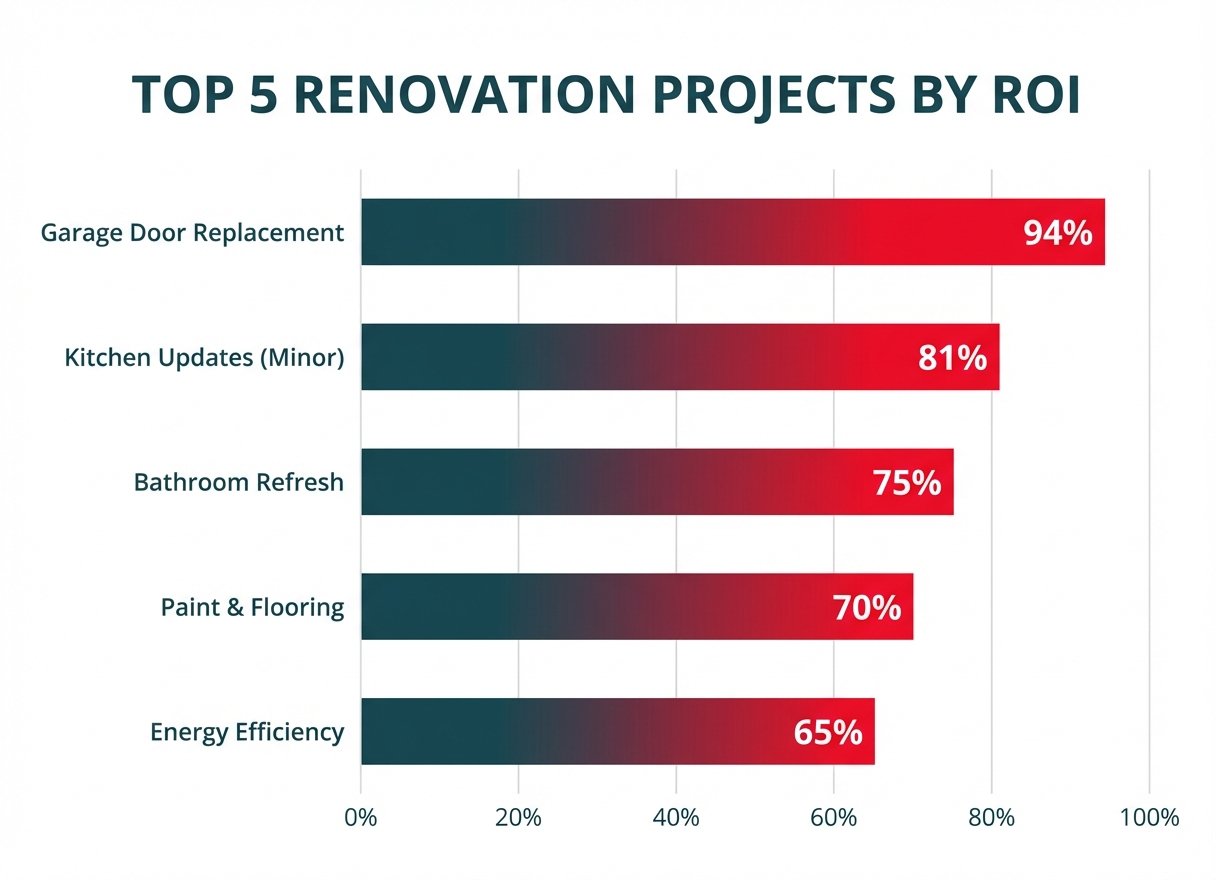

Market research consistently shows that certain renovations outperform others when it comes to returns. Here's where to focus your renovation dollars:

Exterior Improvements - First impressions matter tremendously in real estate. Garage door replacements consistently rank among the highest ROI projects, often returning nearly 94% of costs upon resale. Entry door replacements and updated home siding also provide excellent returns by dramatically improving curb appeal.

Kitchen Updates - Here's the deal: full kitchen remodels rarely recoup their entire cost. But minor to mid-range kitchen renovations can yield returns of up to 81%. Focus on updating cabinet fronts, installing new hardware, replacing countertops, and adding energy-efficient appliances rather than complete gut renovations.

Bathroom Refreshes - Mid-range bathroom updates consistently provide strong returns. Consider replacing outdated fixtures, reglazing tubs instead of replacing them, updating vanities, and installing new flooring.

Interior Paint and Flooring - These relatively low-cost improvements pack a serious punch. Fresh, neutral paint and new flooring create a clean canvas that helps buyers envision themselves in the home.

Energy Efficiency Upgrades - Today's buyers increasingly value energy efficiency. Electric heat pump HVAC conversions and other energy-saving improvements can provide strong returns while appealing to environmentally conscious buyers.

60%, deep teal text to the right of bars for bars <60%, Open Sans Bold, 20pt

- X-axis: Percentage scale from 0% to 100% in 20% increments, deep teal, Open Sans Regular, 14pt, centered below bars

- Grid lines: Light gray (#E0E0E0) vertical lines at 20% intervals for easy reading

**Technical Specifications:**

- Primary color: Deep Teal (#1b444a)

- Secondary color: Vivid Red (#ED072A)

- Bar gradient: Deep teal (#1b444a) to vivid red (#ED072A)

- Background: White (#FFFFFF)

- Grid lines: Light gray (#E0E0E0)

- Image dimensions: 900px x 650px

- Resolution: 300 DPI

- Bar lengths MUST be mathematically proportional: 94%, 81%, 75%, 70%, 65%

**Typography:**

- Title: Open Sans Bold, 36pt, deep teal

- Renovation names: Open Sans Semibold, 18pt, deep teal

- ROI percentages: Open Sans Bold, 20pt, white (on bars) or deep teal (beside bars)

- X-axis scale: Open Sans Regular, 14pt, deep teal

**Alignment:**

- Title centered horizontally

- Renovation names left-aligned with 30px left margin

- Bars left-aligned starting at 100px from left edge

- ROI percentages right-aligned at end of each bar (or 10px to the right for short bars)

- X-axis scale centered below chart area with 20px bottom margin

- Equal vertical spacing of 80px between bars

**Quality Control:**

- ABSOLUTELY NO SPELLING MISTAKES - verify all renovation names and percentages

- Bar lengths MUST be precisely proportional to percentages (94% bar is longest, 65% bar is shortest)

- Gradient must smoothly transition from deep teal to vivid red across each bar

- Grid lines must be perfectly vertical and align with x-axis labels

- All percentages must match the data in the article

- ROI values must be clearly readable against bar backgrounds

- Professional data visualization aesthetic

- Sufficient contrast for accessibility

**Alt Text:** A horizontal bar chart showing the top 5 renovation projects by return on investment for house flipping. Garage door replacement leads at 94% ROI with the longest gradient bar from deep teal to vivid red, followed by minor kitchen updates at 81%, bathroom refresh at 75%, paint and flooring at 70%, and energy efficiency upgrades at 65%. Each bar is proportionally sized to its ROI percentage with clear percentage labels." loading="lazy" style="max-width: 100%; height: auto; border-radius: 8px;">

60%, deep teal text to the right of bars for bars <60%, Open Sans Bold, 20pt

- X-axis: Percentage scale from 0% to 100% in 20% increments, deep teal, Open Sans Regular, 14pt, centered below bars

- Grid lines: Light gray (#E0E0E0) vertical lines at 20% intervals for easy reading

**Technical Specifications:**

- Primary color: Deep Teal (#1b444a)

- Secondary color: Vivid Red (#ED072A)

- Bar gradient: Deep teal (#1b444a) to vivid red (#ED072A)

- Background: White (#FFFFFF)

- Grid lines: Light gray (#E0E0E0)

- Image dimensions: 900px x 650px

- Resolution: 300 DPI

- Bar lengths MUST be mathematically proportional: 94%, 81%, 75%, 70%, 65%

**Typography:**

- Title: Open Sans Bold, 36pt, deep teal

- Renovation names: Open Sans Semibold, 18pt, deep teal

- ROI percentages: Open Sans Bold, 20pt, white (on bars) or deep teal (beside bars)

- X-axis scale: Open Sans Regular, 14pt, deep teal

**Alignment:**

- Title centered horizontally

- Renovation names left-aligned with 30px left margin

- Bars left-aligned starting at 100px from left edge

- ROI percentages right-aligned at end of each bar (or 10px to the right for short bars)

- X-axis scale centered below chart area with 20px bottom margin

- Equal vertical spacing of 80px between bars

**Quality Control:**

- ABSOLUTELY NO SPELLING MISTAKES - verify all renovation names and percentages

- Bar lengths MUST be precisely proportional to percentages (94% bar is longest, 65% bar is shortest)

- Gradient must smoothly transition from deep teal to vivid red across each bar

- Grid lines must be perfectly vertical and align with x-axis labels

- All percentages must match the data in the article

- ROI values must be clearly readable against bar backgrounds

- Professional data visualization aesthetic

- Sufficient contrast for accessibility

**Alt Text:** A horizontal bar chart showing the top 5 renovation projects by return on investment for house flipping. Garage door replacement leads at 94% ROI with the longest gradient bar from deep teal to vivid red, followed by minor kitchen updates at 81%, bathroom refresh at 75%, paint and flooring at 70%, and energy efficiency upgrades at 65%. Each bar is proportionally sized to its ROI percentage with clear percentage labels." loading="lazy" style="max-width: 100%; height: auto; border-radius: 8px;">

Cosmetic vs. Structural Improvements

When flipping houses, you'll need to decide between cosmetic and structural improvements. Here's what you need to know:

Cosmetic Improvements:

- Generally provide better ROI (60-80% or higher)

- Take less time to complete

- Require fewer permits and inspections

- Examples: painting, flooring, cabinet refacing, fixture updates

Structural Improvements:

- Typically yield lower ROI (40-60%)

- Take longer to complete

- Often require permits, inspections, and specialized contractors

- Examples: room additions, wall removal, foundation repairs, roof replacement

If you're just getting started in flipping, focus primarily on cosmetic improvements. This approach reduces your risk while maximizing your potential returns. However, don't ignore necessary structural repairs—these are essential for passing inspections and avoiding liability issues.

Creating a Detailed Renovation Plan

Before making an offer on a property, develop a comprehensive renovation plan:

Document Existing Conditions - Take detailed photos and measurements of the property.

Create Visual Plans - Use digital tools like Planner 5D, Floorplanner, or even simple sketching apps to visualize changes.

Build a Detailed Scope of Work - List every renovation task, no matter how small, including:

- Demolition requirements

- Electrical updates

- Plumbing changes

- Flooring installation

- Cabinet and countertop work

- Painting (interior and exterior)

- Fixture installations

- Landscaping improvements

Prioritize Projects - Rank renovations by:

- Necessity (structural/safety issues)

- ROI potential

- Visual impact

- Budget constraints

Here's a pro tip: Curb appeal upgrades are ROI accelerators because they impact click-through rate, showings, and buyer confidence before the front door even opens. That makes exterior improvements a smart starting point for your renovation planning.

Building a Realistic Timeline

Create a detailed timeline that accounts for:

- Permit acquisition - Allow 2-4 weeks depending on your locality

- Contractor scheduling - Build in buffer time between trades

- Materials delivery - Account for potential supply chain delays

- Inspection scheduling - Plan for both rough and final inspections

- Unexpected issues - Add a 15-20% time buffer for surprises

Here's what experienced flippers know: Plan for a 3-6 month total timeline from purchase to sale, with the renovation phase typically taking 6-12 weeks. This gives you room to handle the unexpected without blowing your budget.

Targeting the Right Buyer Profile

Your renovation plan should align with your target buyer's expectations:

- Research neighborhood demographics - Get to know who's actually buying in the area

- Identify price point expectations - Avoid over-improving for what the neighborhood can support

- Balance trendy vs. timeless - Mix in some current design touches while maintaining broad appeal

- Consider lifestyle factors - Think family-friendly features in suburban neighborhoods, low-maintenance designs where young professionals are buying

By tailoring your renovation plan to maximize ROI while appealing to your target buyer profile, you'll set your flip up for a faster sale and stronger profit margin. Keep in mind: you're not building your dream home—you're creating a marketable property that resonates with the widest possible pool of buyers in your target price range.

Finding and Vetting Reliable Contractors for Your House Flip

Here's the truth: finding reliable contractors is often one of the trickiest parts of house flipping, but it can absolutely make or break your project's timeline and profitability. This step takes real effort—many successful investors will tell you they spent years building a dependable contractor network.

Building Your Contractor Network

Strong contractor relationships are the backbone of successful house flipping. Here's how to start building yours:

Leverage referrals from real estate connections

- Ask fellow investors who they trust for quality work

- Connect with real estate agents who focus on investment properties

- Join local real estate investment groups to gather contractor recommendations

Scout in the field

- Stop by construction sites and introduce yourself to supervisors

- Spend time at home improvement stores like Home Depot and Lowe's to meet contractors

- As one experienced flipper on Reddit puts it: "Go around to construction sites and big box home improvement stores. Strike up a conversation with the people you see there."

Online research

- Check contractor ratings on trusted review platforms

- Look at social media profiles where contractors share their work

- Search local business directories for qualified professionals

Vetting Process for Contractors

Found some promising candidates? Great. Now let's make sure they're the real deal:

Initial screening

- Confirm they have proper licensing and insurance for your state

- Look up any complaints filed with the Better Business Bureau

- Read through online reviews and client testimonials

Interview process

- Start with a phone call to gauge how well they communicate

- Meet face-to-face to get a sense of their professionalism

- Be upfront about your expectations and project timeline

Portfolio review

- Ask to see photos from past renovation projects

- Get addresses of completed flips so you can do a drive-by

- Talk to their previous clients, especially fellow investors

Here's solid advice from Marquee Funding Group on building your vetting checklist: "Ask for their portfolio of work; Set up a phone call; Meet in person; Get a bid. You might find that some contractors fall off your list from step one."

Getting Accurate Bids

Nailing down accurate bids keeps your budget intact and your timeline on track:

Detailed scope of work

- Spell out exactly what the project involves

- Specify the quality and grade of materials you expect

- Use a standard bid form so you can compare apples to apples

Multiple bids strategy

- Get 3-5 bids for each major part of the project

- Compare costs line by line, not just the bottom number

- Ask about any big price differences to understand why

Red flags in bidding

- Bids that seem suspiciously low

- Vague estimates without itemized breakdowns

- Contractors who won't put things in writing

Managing Contractor Relationships

Strong contractor relationships can make or break your project:

Clear communication protocols

- Establish daily or weekly check-ins

- Document all changes in writing

- Create a system for addressing issues promptly

Payment structure

- Never pay full amounts upfront

- Structure payments based on completion milestones

- Hold back final payment until all work passes inspection

Setting expectations

- Provide detailed timelines with consequences for delays

- Clarify quality standards with examples

- Establish work hours and site rules

Warning Signs of Unreliable Contractors

Knowing how to spot a problematic contractor early can save your project from costly setbacks:

Professional red flags

- Reluctance to provide references or credentials

- No physical business address or proper business setup

- Pressure to make quick decisions or cash payments

Communication issues

- Inconsistent responsiveness

- Failure to document conversations

- Resistance to putting agreements in writing

Work quality concerns

- Showing up with inadequate tools or equipment

- Bringing untrained workers to the job site

- Cutting corners on visible finishing details

Taking the time to find, vet, and manage solid contractors is one of the smartest moves you can make as a flipper. Think of your contractor network as an asset that grows stronger with every successful project you complete together.

Step 5: Execute the Flip

Now comes the exciting part—turning your plans into reality. The execution phase is where your vision takes shape, but it's also where staying organized and making smart decisions really counts. Here's how to navigate this critical stage with confidence.

Setting a Realistic Timeline

Let's get real about timing. Industry data shows the average house flip takes roughly 4-6 months from purchase to sale. Of course, your timeline may look different depending on the scope of your project and what's happening in your local market.

"On average, a house flip takes around 4 to 6 months. However, this can vary based on individual circumstances, property condition, and market factors."

Here's what a realistic timeline looks like:

- Acquisition Phase: 2-4 weeks

- Renovation Phase: 2-3 months

- Sale Phase: 1-2 months

From Financing to Breaking Ground

Once you've found your property and locked in financing through OfferMarket's Fix and Flip loan program, here's your game plan:

- Prepare your downpayment - Have your funds ready in an accessible account

- Complete loan documentation - Submit all required paperwork promptly

- Obtain pre-approval - This gives you leverage when making offers

- Make your offer - Submit a competitive bid based on your ARV calculations

- Close on the property - Finalize the purchase with your lender

Don't let the closing period (typically 2-4 weeks) go to waste. Use this time to:

- Finalize your renovation plans

- Schedule contractor start dates

- Apply for necessary permits

- Order materials with long lead times

- Set up your project management system

Managing the Renovation Process

Draw Schedule Management

Most Fix and Flip loans work on a draw schedule, meaning funds are released in phases as you hit milestones:

- Initial draw - Typically covers acquisition and initial expenses

- Progress draws - Released after specific milestones are completed and inspected

- Final draw - Paid upon project completion

Connect with OfferMarket early to understand your specific draw schedule requirements—this directly impacts your cash flow and how you pay your contractors.

Permit and Inspection Navigation

Permits and inspections can make or break your timeline:

- Research requirements early - Different jurisdictions have varying requirements

- Budget for permit costs - These can range from hundreds to thousands of dollars

- Schedule inspections proactively - Build inspection wait times into your timeline

- Maintain good relationships with inspectors - Professional courtesy goes a long way

Quality Control Measures

Smart quality control throughout your project saves you from expensive do-overs:

- Regular site visits - Visit the property at least 2-3 times per week

- Photo documentation - Take pictures of work before, during, and after completion

- Milestone inspections - Check critical work before it's covered (plumbing, electrical)

- Contractor accountability - Hold weekly progress meetings with your team

Finishing Strong and Preparing for Sale

As you approach the finish line:

- Deep clean the property - First impressions matter

- Stage the home - Consider professional staging for maximum appeal

- Professional photography - Invest in quality listing photos

- List the property - Price it competitively based on your market research

- Field offers and negotiate - Aim for a quick sale without sacrificing profit

- Close the sale - Use proceeds to pay off your Fix and Flip loan

- Analyze your performance - Document what went well and what could improve

Here's the reality from investors who've been in the trenches:

"Our average flip from contract to closing is roughly 7 months. We have done some in as little as 8 weeks and others that stretch to a year." - (BiggerPockets Forum)

Smart flippers always build in contingency time, even with solid planning. Once you've closed and cashed out, take a moment to review your process before diving into your next deal on OfferMarket's marketplace. Every flip you complete sharpens your skills and streamlines your approach for the next one.

Insurance Essentials for House Flipping: Protecting Your Investment

Let's be real: house flipping comes with real financial risk. The right insurance coverage isn't optional—it's essential to your investment strategy. Without proper protection, one accident or unexpected event could eat up your profits or leave you in the red.

Types of Insurance Needed for House Flipping

Here's something many new flippers don't realize: standard homeowners insurance won't cut it for properties under renovation. You need specialized coverage designed for your situation:

Builder's Risk Insurance: This is your must-have policy during renovations. It covers your property against fire, theft, vandalism, and weather damage—including materials stored on-site.

Dwelling Policy: This gives you basic structural coverage when the property sits vacant or between renovation phases.

General Liability Insurance: This one's your safety net if someone gets hurt on your property or if your renovation work accidentally damages a neighbor's place.

Umbrella Policy: Think of this as extra protection that kicks in when your standard policies max out—especially important for high-value flips or projects in lawsuit-happy areas.

According to the National Real Estate Insurance Group, "When doing major renovations or flipping a property, you're exposed to a unique set of risks" that require specialized coverage solutions.

Construction Insurance Requirements

The construction phase of your flip comes with its own insurance hurdles. Here's what you need to know:

Materials Coverage: Make sure your policy protects building materials while they're being delivered and while they're sitting on-site. Material theft is a real headache for flippers.

Subcontractor Requirements: Working with subs? Confirm they carry their own insurance and think about adding them as additional insureds on your policy.

Permit Compliance: Heads up—many local governments won't hand over construction permits until you show proof of proper insurance coverage.

Coverage Duration: Builder's risk policies typically match your renovation timeline, usually 3-12 months, with extension options if your project runs longer than expected.

Protecting Your Investment with OfferMarket

At OfferMarket, we get the unique insurance challenges house flippers face, and we've built solutions to protect your investment from start to finish. Here's how we help:

Comprehensive Coverage Assessment: We dig into your specific project to spot any coverage gaps that could leave you vulnerable.

Construction-Specific Policies: We connect you with specialized builders risk policies designed for the realities of flip projects.

Competitive Quotes: Our network of real estate investment insurance specialists means you get solid coverage at rates that make sense.

Seamless Integration: Our insurance solutions work hand-in-hand with our financing and property listing services, creating a streamlined experience for your flipping business.

As noted by Obie Insurance, "Builders risk insurance often provides coverage for damages that can occur during the construction process, such as damages to materials, supplies, and" the structure itself—protection that's essential for any serious house flipper.

The Cost of Going Uninsured

Here's a common mistake we see: new flippers skimp on insurance to save a few bucks. But this shortcut can cost you big time. Let's look at some real-world scenarios:

- A fire wipes out your partially renovated property along with all your materials

- A neighborhood kid gets hurt after wandering onto your unsecured job site

- Your contractor's work causes water damage to the property next door

- Vandals break in and trash those expensive new appliances you just had delivered

Without the right coverage, any one of these situations could turn your profitable flip into a major financial setback.

When you work with OfferMarket to lock in the right insurance, you're protecting more than just this one project—you're safeguarding your entire investing future. Our instant quote system lets you see your insurance costs upfront so you can build them into your budget from day one.

How to Sell Your Flipped House for Maximum Profit

You've put in the work. Now it's time to cash in. Selling your flip is where everything comes together, and this final stage deserves just as much strategic thinking as your renovation did. Let's walk through how to squeeze every dollar of profit out of your sale.

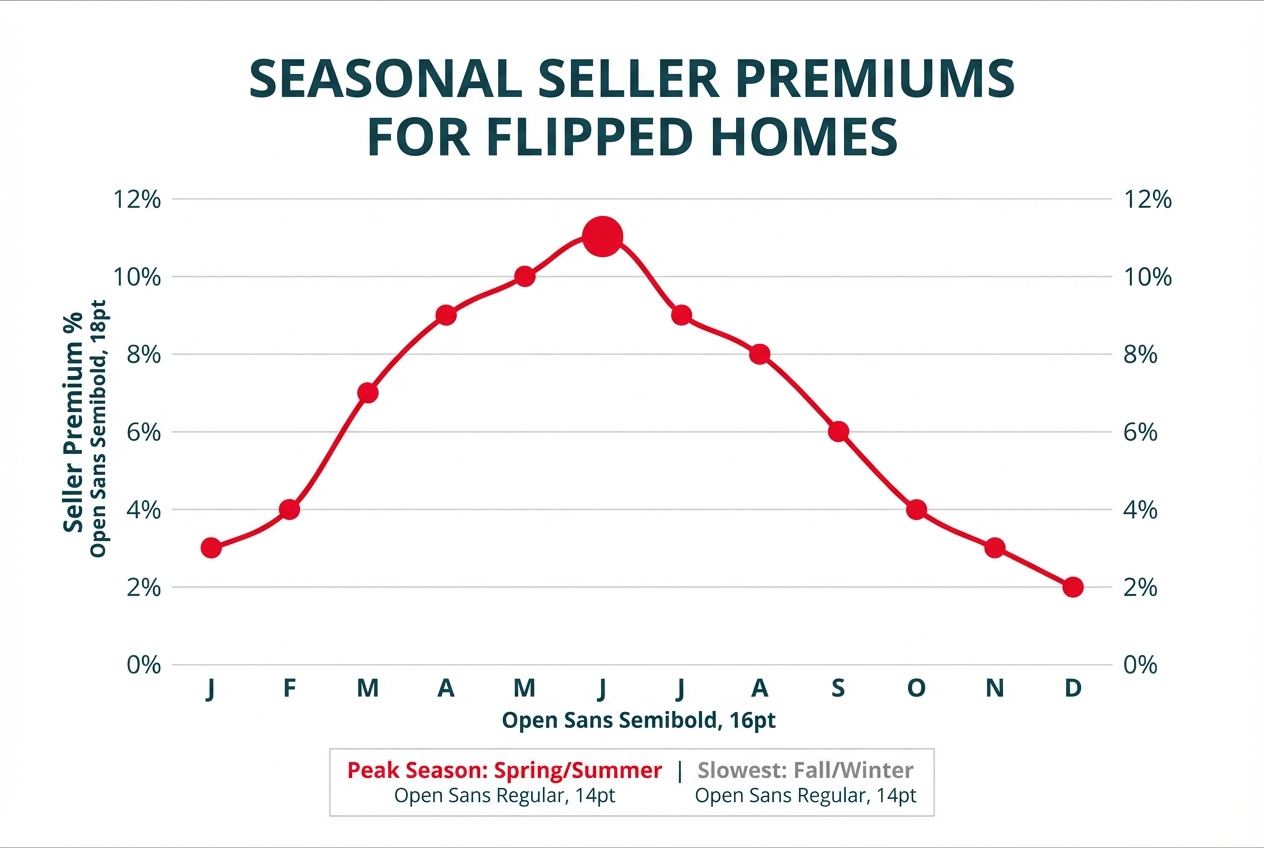

Timing the Market for Optimal Returns

Real estate markets have their rhythms, and understanding them can put more money in your pocket. The data is clear: spring and early summer typically deliver the best prices and fastest sales for sellers.

According to industry research: "June tends to be the best month of the year for home sales, with seller premiums at their peak. By September the seller premium drops by half."

The good news? Smart investors can find solid opportunities year-round:

- Spring (March-May): This is prime time—the biggest buyer pool and your best shot at top-dollar premiums

- Summer (June-August): Momentum stays strong as families rush to settle before school starts

- Fall (September-November): Fewer sellers means less competition, giving your property a chance to shine

- Winter (December-February): It's quieter, sure, but winter buyers are often serious and ready to move fast

Here's a pro tip: time your renovation to wrap up right before your local market heats up. This simple strategy can boost your profit margin by 5-10%.

Professional Staging That Sells

Staging does something powerful—it turns your flip from a house into a home buyers can picture themselves in. Yes, professional staging runs $2,000-$5,000, but it can bump your sale price by 5-15%. That's a solid return.

Here's what works:

- Neutral color palette: Cast a wide net with clean, contemporary tones that appeal to most buyers

- Strategic furniture placement: Guide the eye and showcase your property's strongest features

- Decluttered spaces: Let buyers see the real square footage and storage potential

- Lifestyle vignettes: Create scenes that spark imagination—a cozy reading nook, a functional home office

- Curb appeal focus: You only get one first impression, so make landscaping and exterior touches count

Working with a tighter budget? Virtual staging works great for online listings, or you can focus your dollars on the rooms that matter most: living room, kitchen, and primary bedroom.

Professional Photography and Virtual Tours

Let's be real: in today's market, buyers start their search online. Professional photography isn't optional anymore. Homes with pro photos sell 32% faster and typically fetch higher prices.

Invest in:

- High-resolution, wide-angle photography

- Drone footage for exterior and neighborhood views

- 3D virtual tours that allow remote viewing such as Matterport

- Video walkthroughs highlighting special features

These visual assets typically cost $300-$800 but provide enormous value by increasing visibility and buyer interest.

Strategic Pricing Strategies

Getting your price right from day one is essential for maximizing profit and minimizing time on market.

Here's how to price strategically:

- Comparative Market Analysis (CMA): Review recent sales of similar renovated properties in your area

- Strategic price points: Price just below round numbers ($499,900 instead of $500,000)

- Price for algorithms: Position your listing to show up in the maximum number of online searches

- Account for appraisal: Make sure your price can be supported by comparable sales for buyer financing

- Build in negotiation room: Price slightly above your bottom line to leave space for offers

One common pitfall? Overpricing based on what you spent on renovations rather than what the market will actually bear.

Comprehensive Marketing Plan

Don't stop at the MLS. Build a multi-channel marketing strategy:

- Social media campaigns: Show off those before-and-after transformation photos

- Email marketing: Reach out to local agents who have active buyer clients

- Open houses: Host well-timed events with refreshments to draw crowds

- Neighborhood marketing: Mail "just renovated" postcards to nearby homeowners

- Highlight premium features: Call attention to energy efficiency, smart home tech, or other standout upgrades

Leveraging OfferMarket for Your Flip Sale

OfferMarket gives you some real advantages when it's time to sell your completed flip:

- Commission savings: List your property without paying the traditional 5-6% agent commissions

- Direct buyer connections: Connect with motivated buyers actively searching for renovated properties

- Targeted visibility: Get in front of investors and homebuyers specifically looking for below market renovated homes

- Streamlined process: Handle offers, negotiations, and closing documents all in one place

- Market analytics: Use data on comparable sales and market trends to guide your pricing decisions

By listing your flip on OfferMarket, you keep thousands in potential profit that would otherwise go to commission fees—directly boosting your ROI.

Disclosure and Documentation

Build buyer confidence by providing comprehensive documentation of your renovation:

- Before and after photos

- Permits and inspection reports

- Warranty information for new appliances and systems

- Detailed list of improvements with associated costs

- Proof of professional work (licensed contractors)

This transparency puts buyers at ease and helps justify your asking price.

Keep in mind that the selling phase typically represents 5-10% of your total time investment in a flip project, but it can make or break your profitability. Give this crucial final stage the attention it deserves so your renovation efforts translate into maximum returns.

Common Mistakes to Avoid When Flipping Houses

House flipping can be an exciting and potentially profitable venture, but it's also packed with pitfalls that can quickly turn a promising project into a financial headache. Knowing these common mistakes is essential for both newcomers and seasoned investors who want to thrive in the competitive world of real estate flipping.

Underestimating Costs and Overestimating Profits

One of the biggest mistakes in house flipping is focusing only on gross numbers rather than net profits. Many investors get excited about the potential spread between purchase price and after-repair value (ARV) without factoring in all the expenses in between.

According to a detailed analysis on Investing Architect, "What creates the illusion of big profits in flipping homes is an incorrect focus on Gross numbers. Investors look at the After Repair Value (ARV) and purchase price, but fail to account for all the costs in between".

These overlooked costs typically include:

- Acquisition costs: Closing costs, title insurance, transfer taxes

- Holding costs: Mortgage payments, property taxes, utilities, insurance

- Renovation costs: Materials, labor, permits, unexpected repairs

- Selling costs: Agent commissions, closing costs, marketing expenses

- Financing costs: Interest payments, loan origination fees

A smart budget should include a 15-20% contingency fund to cover unexpected issues that will pop up during renovations.

Poor Property Selection

The foundation of a successful flip begins with selecting the right property. Many flippers make critical errors at this stage:

- Overpaying for properties: In competitive markets, investors often pay too much in bidding wars, immediately cutting into potential profits.

- Choosing the wrong neighborhood: Even a beautifully renovated home won't sell for top dollar in a declining area.

- Underestimating structural issues: Cosmetic fixes are predictable, but foundation problems, roof replacements, or electrical rewiring can quickly derail a budget.

Recent data from The Inquirer shows that "more people fail to make flipping work. Common mistakes include paying too much for properties, overestimating the sale price of renovated homes, and underestimating renovation costs".

Renovation Missteps

Even experienced flippers can stumble during the renovation phase. Here's what to watch out for:

Improper improvement selection: According to a 2019 study, nearly 30% of flippers installed the wrong countertops and cabinets in kitchens, leading to reduced appeal to target buyers.

Over-improving for the neighborhood: Adding luxury features in a mid-range neighborhood often results in being the most expensive house on the block—a position that rarely pays off.

Under-improving key areas: Cutting corners on kitchens and bathrooms, which typically deliver the highest ROI, can significantly hurt your final selling price.

DIY disasters: Tackling specialized work without proper skills to save money often leads to costly repairs and frustrating delays.

Financial and Insurance Oversights

Smart financing and proper insurance are crucial safeguards that many flippers overlook:

Insufficient capital reserves: Starting a flip without adequate cash reserves can force you to abandon the project if unexpected costs pop up.

Neglecting insurance coverage: It's easy to overlook, but skipping property insurance designed for renovation projects can leave you vulnerable to serious liability and unexpected losses.

Inappropriate financing: Taking on high-interest loans without fully understanding how they'll affect your bottom line? That's a quick way to watch your profits disappear.

Market Timing Errors

Real estate moves in cycles, and getting your timing right can make or break your profitability:

Ignoring market trends: Skip the research on seasonal patterns and neighborhood dynamics, and you might find yourself stuck with a property that won't move.

Extended holding periods: Here's the reality—every extra month your property sits unsold means more holding costs eating into your profits. With recent data showing home flipping profits at a 17-year low, getting your project done efficiently and sold quickly matters more than ever.

Misjudging buyer preferences: What looks great to you might not be what buyers in that neighborhood actually want.

Risk Mitigation Strategies

Smart house flippers protect themselves by following these proven approaches:

- Thorough due diligence: Before you buy, invest time in comprehensive property inspections, title searches, and neighborhood research.

- Conservative financial modeling: Factor in every expense and set aside contingency funds of at least 15-20%—you'll thank yourself later.

- Professional team building: Line up your trusted contractors, real estate agents, lenders, and insurance providers before you start your first project.

- Detailed project planning: Map out your renovation schedule with clear milestones and accountability built in.

- Exit strategy flexibility: Always have backup plans ready—whether that's selling, renting, or refinancing—in case the market shifts while you're mid-project.

By understanding and actively avoiding these common mistakes, you can significantly increase your chances of executing profitable house flips while minimizing risk. Remember that successful house flipping is more about methodical planning and execution than the dramatic transformations portrayed on television shows.

Scaling Your House Flipping Business: From One Property to Multiple Projects

Here's the exciting part: house flipping doesn't have to stay a one-property-at-a-time endeavor. Once you've nailed a few successful flips and dialed in your approach, scaling up can boost your profits and position you as a serious force in real estate investing.

Building a Repeatable Process

The key to scaling any business? Creating systems you can use again and again. As industry experts put it, "To have success and be able to scale, you need to get your processes down". That means documenting every step of your flipping journey:

- Property acquisition criteria and evaluation methods

- Renovation scope templates for different property types

- Standardized budgeting spreadsheets

- Contractor vetting and management procedures

- Marketing and sales strategies

When you systematize these elements, you're building a playbook that works across multiple properties at once—cutting down on decision fatigue and ramping up your efficiency.

Assembling a Reliable Team

Growth means letting go of some control. As a solo flipper, you might handle everything yourself, but scaling requires building a solid team:

- Project managers to oversee renovations

- Dedicated contractors and subcontractors

- Real estate agents specialized in your target markets

- Administrative support for paperwork and logistics

- Bookkeepers and accountants for financial management

"To scale your business to multiple flips at one time, you must have the team members in place. Most importantly, the construction crews. Time is money in this business," shares an experienced flipper on [BiggerPockets forums](https://www. biggerpockets.com/forums/67/topics/353563-scaling-our-flipping-business).

Leveraging Technology and Systems

The right tech stack can be a game-changer when you're juggling multiple projects:

- Project management software to keep renovation timelines on track

- Property analysis tools to quickly size up potential deals

- CRM systems to stay on top of buyer and seller relationships

- Accounting software for monitoring expenses across all your projects

- Virtual meeting platforms to keep your team aligned

With these tools in your corner, you can keep your finger on the pulse of every project without running yourself ragged trying to be everywhere at once.

Financing Strategies for Portfolio Growth

Let's be real: access to capital is the make-or-break factor when scaling. As Anchor Loans puts it, "With fix-and-flip financing, you can conserve your own capital to invest in multiple properties, while increasing your cash-on-cash ROI".

Here are some smart financing moves to consider:

- Laddered lending: Work with different lenders for different properties to stretch your available capital further

- Lines of credit: Set up revolving credit lines you can tap into across multiple projects

- Private money partnerships: Build relationships with investors who can back multiple deals

- Reinvestment strategy: Put your profits to work by funneling them into your next properties

OfferMarket's fix-and-flip loan products are built with scaling investors in mind. Our competitive rates and streamlined processes make it easier to manage multiple projects at once.

Market Specialization vs. Diversification

As you grow, you'll face a key decision:

- Go deep in one geographic area or property type, becoming the go-to flipper in that niche

- Spread out across markets to hedge against local downturns

Both paths have their advantages, but here's what we've seen work: master one market first, then expand. That solid foundation sets you up for growth that actually lasts.

By implementing these scaling strategies, you can transform your house flipping side hustle into a thriving business, potentially flipping dozens of properties each year and building real wealth through real estate.

Why OfferMarket Is Your Partner in House-Flipping Success

Let's be honest: successful house flipping comes down to having the right tools, resources, and partners in your corner. That's where OfferMarket shines—we bring together financing options, property listings, and insurance solutions all in one place, so you can focus on what matters most: growing your portfolio.

Everything You Need, All in One Place

Here's the reality: real estate investing has traditionally meant juggling multiple platforms, lenders, and insurance providers. It's exhausting and inefficient. OfferMarket changes that by giving you everything under one roof. As industry experts point out, "Digital banking platforms have the potential to improve efficiency, visibility and security" for real estate investors. We've taken this idea even further, building a complete ecosystem designed specifically for investors like you.

Financing Built for Flippers

OfferMarket offers financing products designed with your needs in mind:

- Fix and Flip Loans: Structured around your renovation timeline and budget

- DSCR Loans: Ideal if you're considering renting before selling

- Competitive Interest Rates: We often beat what traditional banks offer

- Fast Approval Process: Get funded quickly so you never miss a deal

Find Off-Market Properties Directly

Finding the right property at the right price? That's often the toughest part of flipping. OfferMarket's investment property marketplace makes it easier:

- Connect directly with sellers—no agent commissions eating into your profits

- Set up zipcode alerts so you're first to know about new listings in your market

- Use advanced filters to find properties that match your exact criteria

- Access off-market deals you won't find on traditional MLS listings

Don't Overlook Insurance During Renovations

Many flippers underestimate the importance of proper insurance coverage during the renovation phase. OfferMarket offers:

- Construction-specific insurance policies for active flips

- Coverage tailored to renovation projects

- Competitive quotes from 40+ insurance carriers

- Seamless integration with your financing and property acquisition

Real Investor Success Stories

Smart investors are already putting OfferMarket to work. One user pocketed over $15,000 in savings on their first flip by combining our competitive financing with direct property acquisition. Another investor shaved nearly three weeks off their project timeline thanks to our integrated approach. These aren't outliers—they're what happens when you have the right tools working together.

Data-Driven Investment Decisions

Let's be real: gut feelings don't cut it in today's market. As investment experts point out, "A real estate investment platform makes these lessons easier to follow by giving beginners the same data and tools professionals already use". With OfferMarket's comprehensive market data, ARV calculators, and renovation cost estimators, you'll make decisions backed by solid numbers—not guesswork.

When you partner with OfferMarket, you're getting more than a toolkit. You're tapping into a platform built specifically for the challenges real estate investors face every day. That means you can zero in on what actually moves the needle: spotting opportunities and maximizing your returns.

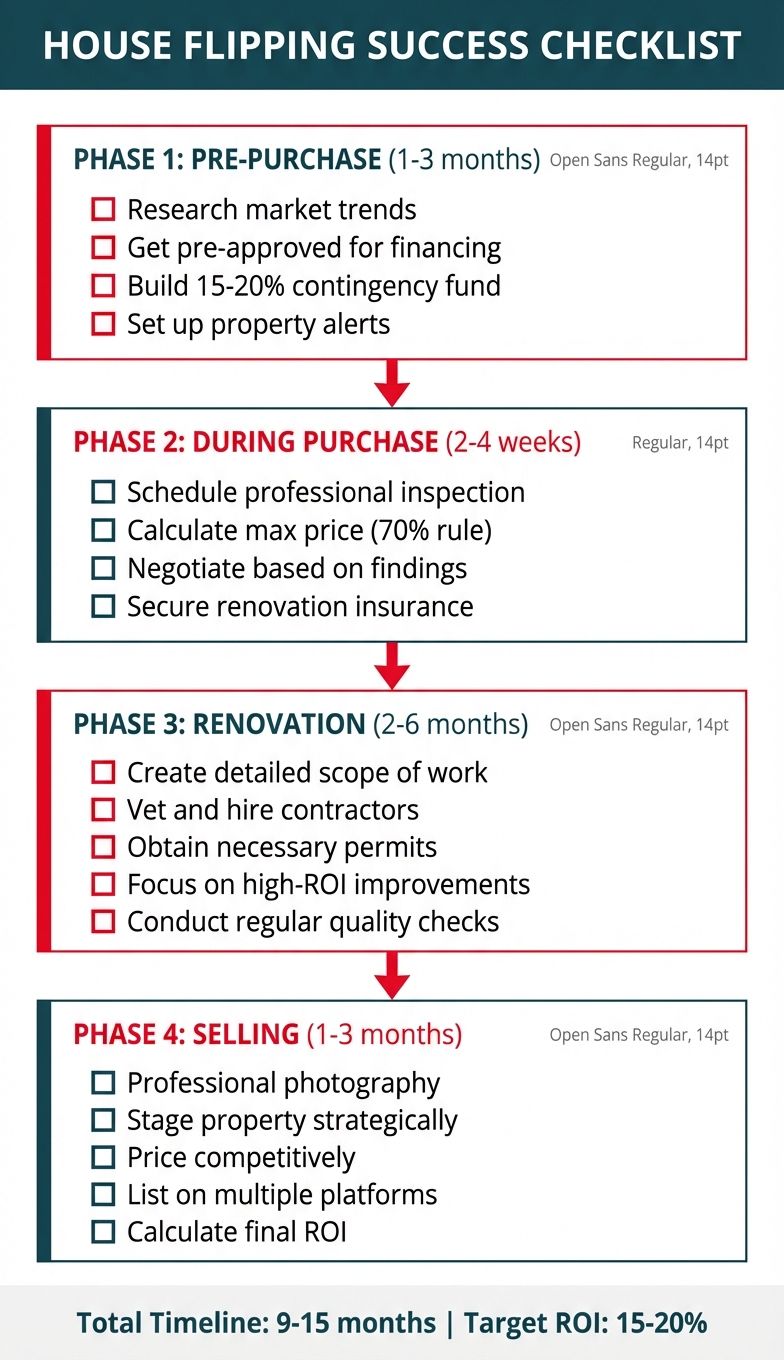

The Ultimate House Flipping Checklist: Your Path to Success

Here's the truth: successful flips don't happen by accident. They're the result of careful planning and disciplined execution. Use this comprehensive checklist to stay on track, sidestep expensive mistakes, and keep more profit in your pocket.

Pre-Purchase Checklist

Market Research (Timeline: 1-3 months)

- Research local real estate market trends and property values

- Identify target neighborhoods with growth potential

- Study recent sales of comparable properties

- Analyze rental rates in the area (backup exit strategy)

- Connect with local real estate agents for market insights

Financial Preparation (Timeline: 2-4 weeks)

- Calculate your available capital for down payment

- Determine your maximum purchase price

- Get pre-approved for a Fix and Flip loan

- Create a detailed budget for renovation costs

- Build in a 15-20% contingency fund for unexpected expenses

- Calculate potential ROI based on projected ARV

Property Hunting Toolkit (Timeline: Ongoing)

- Flashlight for inspecting dark areas

- Digital camera or smartphone for documentation

- Tape measure for verifying dimensions

- Moisture meter for detecting water damage

- Notebook for taking detailed notes

- Set up property alerts on OfferMarket's marketplace

Here's the deal: successful house flippers don't wing it. They follow a proven system. After you've analyzed the property and crunched your numbers, your next move is a professional home inspection and assessment. Then comes securing financing and mapping out your renovation game plan (Source).

During-Purchase Checklist

Property Evaluation (Timeline: 1-2 weeks per property)

- Schedule a professional home inspection

- Assess the property's structural integrity

- Verify all major systems (HVAC, electrical, plumbing)