*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

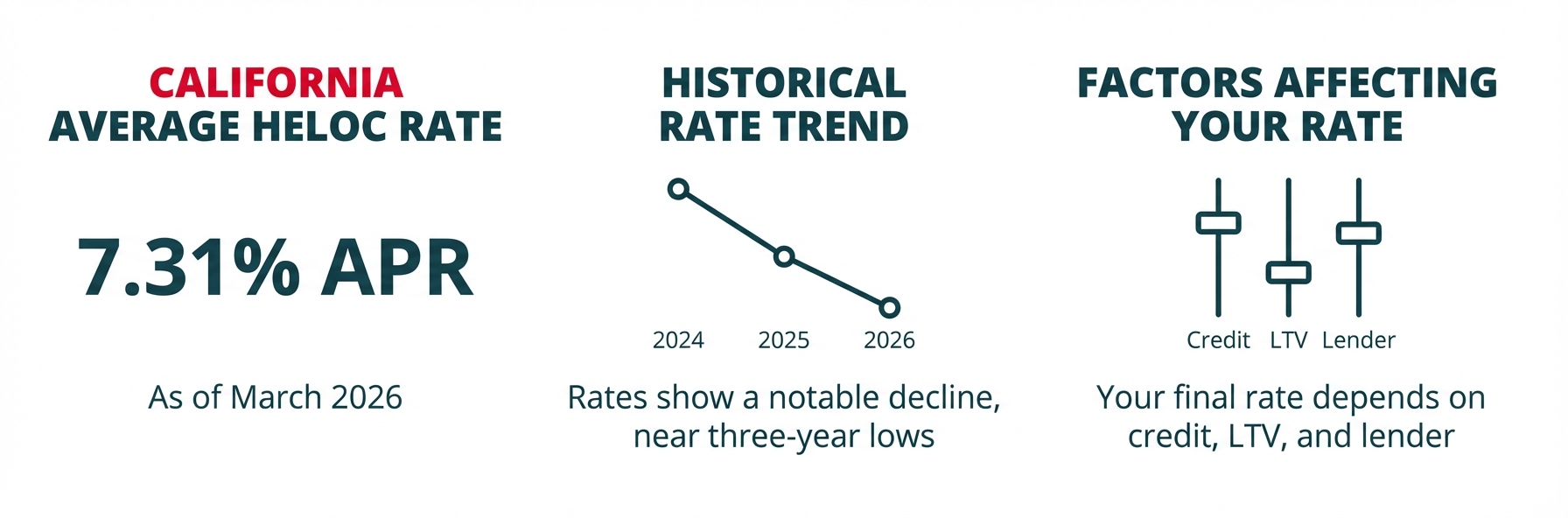

Current HELOC Rates in California (As of March 2026)

If you're a California real estate investor researching home equity lines of credit, you're likely here for one thing: the numbers. Let's cut straight to what HELOC rates actually look like in today's market.

As of March 2026, the average HELOC rate in California sits at approximately 7.31% APR, according to Bankrate's national survey of lenders. This represents a notable decline from previous years, with rates hovering near three-year lows. However, it's critical to understand that this is a market average—your actual rate will depend on several factors we'll explore throughout this guide.

HELOC Rates in California for Real Estate Investors (2026)

If you're a California real estate investor researching home equity lines of credit (HELOCs), you've probably noticed something frustrating: every lender advertises different rates, the numbers seem to change daily, and it's nearly impossible to get a straight answer about what you'll actually pay. You're not alone in this confusion.

Here's the reality: HELOC rates are complex, variable, and highly personalized. The "6.99% APR" you see plastered across a bank's website likely doesn't reflect what you'll actually receive—especially if you're using the HELOC to finance an investment property rather than improvements on your primary residence. And unlike investor focused mortgages with fixed rates, HELOCs come with variable interest rates that can fluctuate monthly, making it challenging to project your true borrowing costs.

This guide cuts through the marketing noise to give you the unvarnished truth about HELOC rates in California. We'll show you exactly how rates are calculated, what factors determine your specific rate, and—most importantly—why a fixed-rate Home Equity Loan (HELOAN) might be a smarter choice for your investment strategy.

Sample California HELOC Rates: What Major Lenders Are Offering

The table below provides a snapshot of current HELOC rates from major lenders serving California borrowers. These rates reflect what you might see with excellent credit (740+ FICO score) and a conservative loan-to-value ratio (below 70%) on a primary residence.

| Lender Type | Example Lender | Introductory APR Range | Variable APR Range (Prime + Margin) | Draw Period | Repayment Period | Maximum CLTV |

|---|---|---|---|---|---|---|

| National Bank | Bank of America | 6.50% - 7.25% (6-12 months) | Prime + 1.25% - 2.50% | 10 years | 20 years | 85% (primary) / 75% (investment) |

| National Bank | U.S. Bank | 7.20% - 7.75% (intro period) | Prime + 1.45% - 3.10% | 10 years | 20 years | 80% (primary) / 70% (investment) |

| Credit Union | Golden 1 Credit Union | 6.75% - 7.50% (varies) | Prime + 1.00% - 2.25% | 10 years | 15 years | 90% (primary) / 75% (investment) |

| Market Average | Bankrate Survey | N/A | 7.31% (fully indexed) | 10 years | 20 years | Varies |

Current Prime Rate: As of December 2025, the U.S. Prime Rate stands at 6.75%, as reported by major financial institutions including Bank of America. This benchmark rate directly influences your HELOC's variable rate and adjusts in response to Federal Reserve policy decisions.

Critical Disclaimer: Your Rate Will Vary

The rates shown above are for illustrative purposes only and represent best-case scenarios. Here's what will actually determine your rate:

Credit Score Impact: The rates above assume a credit score of 740 or higher. If your score falls below this threshold, expect to pay a significantly higher margin—potentially 1-3 percentage points more.

Property Type Matters: Investment properties are considered higher risk by lenders. If you're financing a rental property or fix-and-flip project, add 0.50% to 1.50% to the margins shown above. Some lenders may decline HELOC applications for investment properties altogether.

Loan-to-Value Ratio: The lower your combined loan-to-value (CLTV) ratio, the better your rate. The examples above assume a CLTV below 70%. If you're borrowing up to 80-85% of your home's value, expect higher rates and more stringent underwriting.

Loan Amount: Some lenders offer rate discounts for larger credit lines (typically $250,000+), while others may charge higher rates for smaller HELOCs (under $50,000).

Market Volatility: HELOC rates are tied to the Prime Rate, which fluctuates based on Federal Reserve policy. According to [Bankrate's analysis](, current HELOC borrowers can expect their interest rate and payments to adjust within one to two months after a Fed rate change. This means your 7.31% rate today could be 8.31% (or 6.31%) six months from now.

What This Rate Environment Means for California Investors

California's current HELOC rate environment presents both opportunities and challenges. While rates have declined to three-year lows, they remain significantly higher than the sub-4% rates available just a few years ago. For real estate investors, this creates a critical decision point: is a variable-rate HELOC the right tool for your investment strategy, or would a fixed-rate alternative provide more predictable cash flow?

The average HELOC rate of 7.31% compares favorably to other forms of credit available to investors. Credit cards currently average 19.59% APR, while personal loans sit at 12.26% APR, making home equity financing substantially more cost-effective for larger capital needs. However, home equity loans (HELOANs) with fixed rates are averaging 7.87% APR, offering rate stability for only a modest premium over variable HELOCs.

Throughout this guide, we'll help you understand not just what rates are available, but how to research them effectively, what factors influence your specific rate, and—most importantly—whether a HELOC is truly the best financing tool for your California real estate investment goals.

How to Research and Compare California HELOC Rates Like a Pro

The key to securing the best HELOC rate in California isn't luck—it's preparation and strategic comparison shopping. As a real estate investor, you need to approach HELOC research with the same analytical mindset you bring to property analysis. This section will walk you through a systematic process to gather competitive quotes and identify the best financing option for your specific situation.

Step 1: Identify "Non-Retail" Lenders

Traditional retail comparison sites (like Bankrate or NerdWallet) primarily list lenders that focus on owner-occupied properties. For an investment HELOC, you must shift your focus toward credit unions, local community banks, and specialized portfolio lenders. These organizations are more likely to keep loans on their own books rather than selling them to Fannie Mae or Freddie Mac, giving them the flexibility to offer investment-grade lines of credit.

Step 2: Verify Eligibility Early

Before diving into rate sheets, you must confirm that the lender even offers the product. Most major national banks (e.g., Chase, Wells Fargo) generally do not offer HELOCs on non-owner-occupied properties. When researching, check for these specific requirements:

Max Loan-to-Value (LTV): Most lenders cap investment HELOCs at 70% to 80% LTV, whereas primary residences often go to 90%.

Property Type: Confirm they allow 2–4 unit properties if your investment isn't a single-family home.

Occupancy Rules: Ensure the lender explicitly allows "Non-Owner Occupied" (NOO) status.

Step 3: Account for the "Investment Premium"

While retail sites show "teaser rates" for primary homes, investment property HELOCs almost always come with a pricing "add-on."

Rate Markup: Expect your interest rate to be 1.0% to 2.5% higher than the rates you see advertised on mainstream comparison sites.

Credit Requirements: While a 740 FICO might get you the best rate on a primary home, many investment HELOC lenders require a 760+ for their most competitive tiers.

Step 4: Consult Specialized Resources

Since standard aggregators often lack this data, your best research tools will be:

BiggerPockets Forums: Search for "Investment HELOC [Your State]" to find crowdsourced lists of lenders currently active in the space.

Local Credit Union Directories: Use the NCUA Credit Union Locator to find institutions in the same county as your investment property, as they often have the most aggressive niche products.

Mortgage Brokers: A broker who specializes in investor DSCR (Debt Service Coverage Ratio) loans often has "pocket" lenders that offer HELOCs to repeat clients.

![**Task:** Create an infographic comparison chart showing the pros and cons of three major lender categories (National Banks, Credit Unions, and Online Lenders) for California real estate investors seeking HELOCs.

**Visual Structure:** Three-column layout with each column representing a lender type. Each column contains the lender category name, representative icon, and two sections listing pros and cons with checkmarks and X marks.

**ASCII Layout Reference:**

```

+----------------------+----------------------+----------------------+

| NATIONAL BANKS | CREDIT UNIONS | ONLINE LENDERS |

| [Bank Building] | [Handshake Icon] | [Laptop Icon] |

+----------------------+----------------------+----------------------+

| PROS: | PROS: | PROS: |

| ✓ Established | ✓ Lower rates | ✓ Fast approval |

| reputation | (0.25-0.75% less) | (24-48 hours) |

| ✓ Wide branch | ✓ Personalized | ✓ Fully digital |

| network | service | process |

| ✓ Online tools | ✓ Flexible DTI | ✓ Competitive rates |

| ✓ Relationship | ✓ Community focus | ✓ Innovative tech |

| discounts | | |

+----------------------+----------------------+----------------------+

| CONS: | CONS: | CONS: |

| ✗ Higher rates | ✗ Membership | ✗ No in-person |

| than CUs | required | support |

| ✗ Strict investment | ✗ Lower max limits | ✗ Limited investor |

| property rules | ✗ Stricter for | experience |

| ✗ Less flexibility | investment props | ✗ Newer companies |

| ✗ Higher fees | ✗ Smaller networks | ✗ Less flexibility |

+----------------------+----------------------+----------------------+

```

**Image Section Breakdown:**

Header Row:

- Three equal columns, each 400px wide

- Column 1 header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772653850012_1oxbse.jpg?alt=media&token=af1db4d3-883c-4efd-ac71-3b5a3943859f)

National Banks (Chase, Bank of America, Wells Fargo, U.S. Bank)

Pros:

- Established reputation and financial stability

- Streamlined online application processes

- Potential relationship discounts if you have existing accounts

- Wide branch network for in-person support

Cons:

- Often less competitive rates compared to credit unions

- Stricter underwriting for investment properties

- Less flexibility in negotiating terms

- May have higher fees and more stringent requirements

California Credit Unions (Golden 1, Patelco, First Tech, Consumers Credit Union)

Pros:

- Typically offer rates 0.25% to 0.75% lower than national banks

- More personalized service and local decision-making

- Community-focused mission often translates to better customer care

- May be more flexible with debt-to-income ratios

Cons:

- Membership requirements (though often easy to meet)

- May have lower maximum HELOC limits

- Potentially stricter policies for investment properties

- Smaller branch networks

According to research on credit union HELOCs, credit unions evaluate several key factors including credit score, income stability, debt-to-income ratio, and loan amount when determining your rate—often with more flexibility than large banks.

Online Lenders (Figure, Spring EQ, LoanDepot)

Pros:

- Fast application and approval (sometimes within 24-48 hours)

- Completely digital process with minimal paperwork

- Competitive rates due to lower overhead costs

- Innovative technology for tracking and managing your line

Cons:

- No in-person support or local branches

- May have limited experience with complex investor scenarios

- Newer companies with less established track records

- Can be less flexible if you have unique circumstances

Step 4: Create Your HELOC Comparison Checklist

As you gather quotes, use this comprehensive checklist to compare offers side-by-side. Create a simple spreadsheet with each lender as a column and these factors as rows:

Rate Structure:

- Annual Percentage Rate (APR): The true cost of borrowing, including fees

- Introductory "Teaser" Rate: What's the promotional rate, and how long does it last (typically 6-12 months)?

- Post-Intro Variable Rate: What will your rate adjust to after the intro period?

- The Margin: The percentage points added to the Prime Rate—this is where you can negotiate

- Index: Confirm they use the Wall Street Journal Prime Rate (most do)

- Rate Caps: What's the periodic cap (how much can it increase per adjustment) and lifetime cap?

Loan Terms:

- Draw Period: How long can you access funds? (Standard is 10 years)

- Repayment Period: How long to pay back after draw period ends? (Standard is 20 years)

- Minimum Draw Requirement: Some lenders require you to draw a minimum amount at closing

- Minimum Monthly Draw: Are you required to use the line regularly?

Fees and Costs:

- Application Fee: Typically $0-$100

- Annual Fee: Ranges from $0-$100 per year

- Appraisal Fee: Usually $300-$600 in California

- Closing Costs: Can range from $0 to several thousand dollars

- Inactivity Fee: Charged if you don't use the line for extended periods

- Early Closure Fee: Penalty if you close the HELOC within the first 2-3 years

- Prepayment Penalty: Rare, but check to be sure

Flexibility Features:

- Convertibility: Can you convert some or all of your variable balance to a fixed rate?

- Payment Options: Interest-only during draw period, or required principal payments?

- Credit Limit Increases: Can you request an increase without a full refinance?

Step 5: Ask the Right Questions

When speaking with lenders, don't just accept the initial quote. As NerdWallet's HELOC guide emphasizes, shopping around with at least three lenders helps you find the optimal combination of features and interest rates. Here are critical questions to ask:

"What is your margin, and is it negotiable?" The margin is the lender's profit. If you have excellent credit and substantial equity, you may be able to negotiate a lower margin.

"Are there any relationship discounts available?" Some banks offer 0.25% rate reductions if you maintain a checking account or set up autopay.

"What is the rate for an investment property specifically?" Don't let them quote you the primary residence rate if your property is a rental.

"What happens if I don't use the full credit line?" Clarify any inactivity fees or minimum draw requirements.

"Can you provide a detailed fee breakdown in writing?" Get the Loan Estimate document to compare true costs.

"What is your typical timeline from application to funding?" For time-sensitive investment opportunities, speed matters.

Empowering Yourself as an Informed Consumer

The most successful real estate investors don't accept the first offer they receive. By conducting thorough research, comparing multiple lenders, and asking pointed questions, you position yourself to negotiate from strength. Remember: lenders want your business, especially if you're a creditworthy borrower with substantial home equity.

However, as you'll discover in the following sections, the variable nature of HELOC rates can create significant uncertainty for investment property financing—which is precisely why many sophisticated California investors are choosing fixed-rate HELOANs instead. Before you commit to a HELOC, make sure you understand exactly how your rate is calculated and what could cause your monthly payment to fluctuate dramatically.

Decoding Your HELOC Rate: Prime, Margins, and Variables Explained

Understanding how your HELOC rate is calculated isn't just financial literacy—it's essential for California real estate investors who need to project cash flow and evaluate whether a home equity line makes sense for their investment strategy. Unlike the fixed rates you might be familiar with from investor focused mortgages, HELOC rates are dynamic, and knowing what drives them helps you anticipate changes and negotiate better terms.

The Core Formula: Prime Rate + Margin = Your Fully Indexed Rate

Every HELOC rate in California follows a straightforward formula:

Prime Rate + Margin = Your Fully Indexed HELOC Rate

This two-part structure determines what you'll actually pay in interest. Let's break down each component.

![**Task:** Create an educational infographic explaining the HELOC rate calculation formula with a visual breakdown of Prime Rate and Margin components, including a concrete example with numbers.

**Visual Structure:** Top section shows the formula prominently, middle section breaks down the two components with definitions and current values, bottom section provides a worked example calculation.

**ASCII Layout Reference:**

```

+----------------------------------------------------------+

| HOW YOUR HELOC RATE IS CALCULATED |

+----------------------------------------------------------+

| |

| PRIME RATE + MARGIN = YOUR RATE |

| 7.50% + 1.50% = 9.00% |

| |

+---------------------------+------------------------------+

| PRIME RATE | MARGIN |

| [Graph Icon] | [Percentage Icon] |

| | |

| • Set by Wall Street | • Set by your lender |

| Journal | • Based on your credit |

| • Changes with Fed | • Typically 0.5% - 3.0% |

| policy | • Fixed for loan life |

| • Current: 7.50% | • Negotiable |

| • Adjusts quarterly | |

+---------------------------+------------------------------+

| |

| EXAMPLE CALCULATION: |

| |

| Prime Rate (WSJ)................... 7.50% |

| + Your Lender Margin............... 1.50% |

| = Your Fully Indexed Rate.......... 9.00% APR |

| |

| On $100,000 balance = $750/month interest |

| |

+----------------------------------------------------------+

```

**Image Section Breakdown:**

Title Section (Top):

- Main title:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772653891033_w0rytc.jpg?alt=media&token=775f8e79-a27b-47e5-9cd7-9b7a75028b5a)

The Prime Rate: The Foundation of Your HELOC Rate

The Prime Rate is a benchmark interest rate that banks use as a starting point for various consumer loans, including HELOCs. As of May 2025, the Wall Street Journal Prime Rate—the most widely used benchmark—stands at 7.50%. This rate isn't arbitrary; it's directly tied to the Federal Funds Rate, which is set by the Federal Reserve.

When the Federal Reserve raises or lowers the Federal Funds Rate to manage economic conditions, the Prime Rate typically moves in lockstep, usually adjusting by the same amount within days. For California real estate investors, this means your HELOC payment can increase or decrease multiple times throughout the year based on Federal Reserve policy decisions. According to Bankrate, lenders evaluate market conditions and adjust rates based on this benchmark index.

You can track the current Prime Rate on the Wall Street Journal's website, and it's worth monitoring Federal Reserve announcements if you're carrying a HELOC balance or planning to draw funds during periods of economic uncertainty.

The Margin: The Lender's Profit and Your Negotiating Point

The margin is the percentage points your lender adds on top of the Prime Rate. This is where the lender builds in their profit and accounts for the risk they're taking by lending to you. Importantly, the margin is fixed for the life of your HELOC—it won't change even as the Prime Rate fluctuates.

According to SCCU, margins typically range from -1% to 5%, though for California investment properties, you're more likely to see margins between 0.5% and 3%. The specific margin you receive depends on several factors:

- Your credit score: Higher scores mean lower perceived risk and smaller margins

- Your combined loan-to-value ratio (CLTV): More equity in your property results in better margins

- Property type: Investment properties carry higher margins than primary residences

- Loan amount: Some lenders offer margin discounts for larger lines of credit

Here's a practical example: If the Prime Rate is 7.50% and your lender assigns you a 1.5% margin, your fully indexed HELOC rate would be 9.00%. If the Fed raises rates by 0.25% and the Prime Rate increases to 7.75%, your new rate becomes 9.25%—and your monthly payment increases accordingly.

Introductory Rate vs. Variable Rate: Understanding Payment Shock

One of the most critical—and often misunderstood—aspects of HELOC pricing is the difference between introductory "teaser" rates and the variable rate that follows. This distinction can mean the difference between manageable payments and serious cash flow problems for real estate investors.

The Introductory Rate Trap

Many California lenders advertise eye-catching introductory rates to attract borrowers. You might see offers like "4.99% APR for the first 12 months" or "5.25% for six months." These promotional rates are typically well below the fully indexed rate and are designed to be temporary.

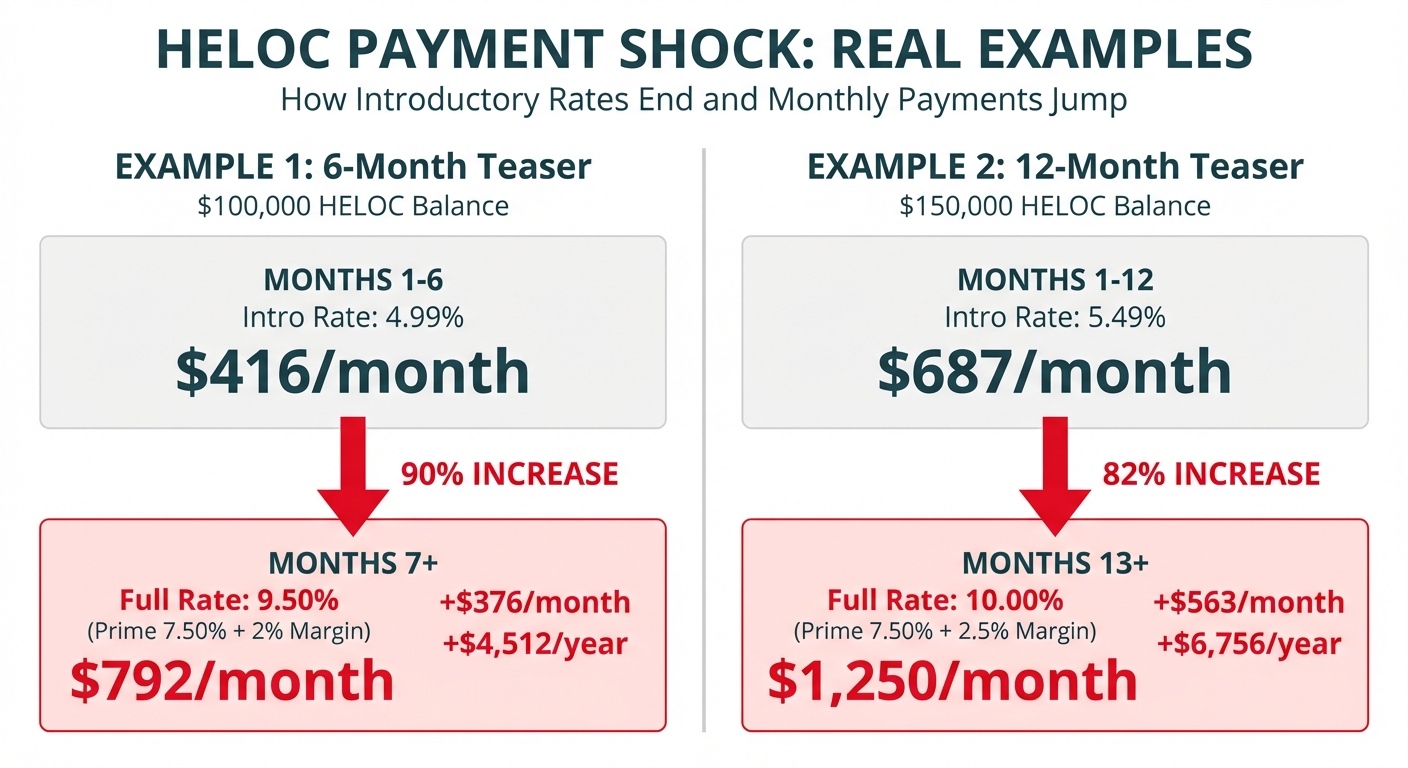

Let's walk through a real-world scenario that demonstrates the payment shock many investors experience:

Example 1: The Six-Month Teaser

- HELOC Amount: $100,000 (fully drawn)

- Introductory Rate: 4.99% for 6 months

- Fully Indexed Rate After Intro Period: Prime Rate (7.50%) + 2% Margin = 9.50%

During the first six months, your interest-only monthly payment would be approximately $416. This seems manageable, even attractive. However, once the introductory period ends, your payment jumps to approximately $792 per month—a 90% increase. If you're using this HELOC to fund a fix-and-flip project and your holding period extends beyond six months, this payment shock can severely impact your profit margins.

Example 2: The One-Year Promotional Rate

- HELOC Amount: $150,000 (for a down payment on a second investment property)

- Introductory Rate: 5.49% for 12 months

- Fully Indexed Rate After Intro Period: Prime Rate (7.50%) + 2.5% Margin = 10.00%

Your initial monthly payment: $687. After 12 months: $1,250. That's an additional $563 per month—$6,756 annually—that you need to account for in your investment property cash flow projections.

Why This Matters for California Real Estate Investors

California's real estate market is expensive, and many investors leverage HELOCs for substantial amounts. The difference between a 5% teaser rate and a 10% fully indexed rate on a $200,000 HELOC is over $800 per month. For investors running multiple properties or executing a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, this unpredictability makes financial planning extremely difficult.

The variable nature of HELOC rates means you're not just dealing with the end of the promotional period—you're also exposed to ongoing rate changes whenever the Federal Reserve adjusts its policy. During periods of rising rates, you could face multiple payment increases in a single year, each one eroding your investment returns.

This inherent unpredictability is precisely why many sophisticated California real estate investors are shifting away from HELOCs and toward fixed-rate HELOANs. With a HELOAN, you know your exact monthly payment from day one through the final payment, making it far easier to calculate your true cost of capital and project accurate returns on your investment properties.

Understanding the mechanics behind HELOC rates—the Prime Rate foundation, the fixed margin, and the temporary nature of introductory offers—empowers you to ask better questions when shopping for financing and to make more informed decisions about whether a variable-rate product truly serves your investment strategy.

What Factors Determine Your Specific HELOC Rate in California?

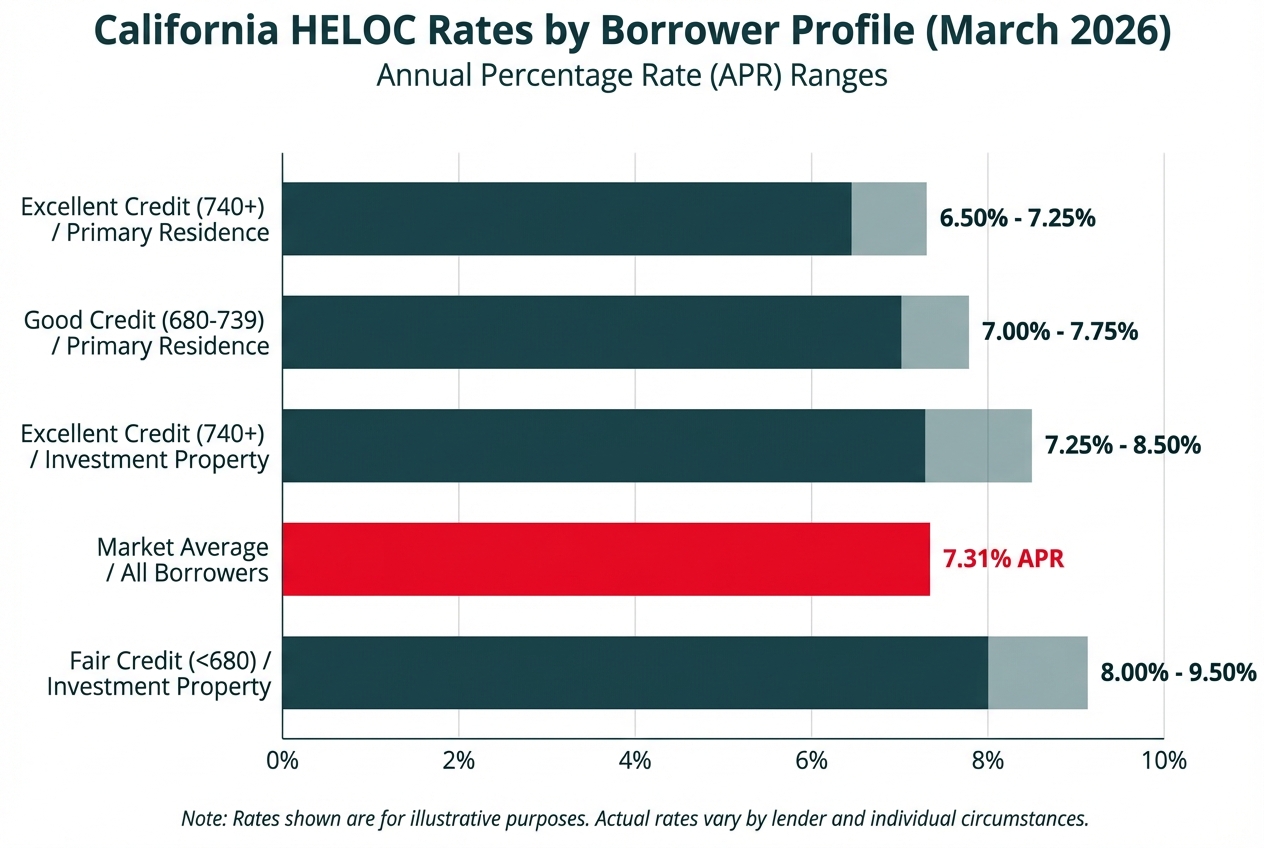

When you see advertised HELOC rates online or in marketing materials, those are best-case scenarios—typically reserved for borrowers with exceptional credit profiles and low-risk properties. The reality is that your actual rate will be personalized based on several key factors that lenders use to assess risk. Understanding these variables will help you anticipate what rate you'll realistically receive and identify areas where you might improve your borrowing position.

Your Credit Score: The Foundation of Your Rate

Your FICO credit score is the single most influential factor in determining your HELOC rate. Lenders use it as a proxy for how likely you are to repay the loan. Here's how California lenders typically tier their rates based on credit scores:

Excellent Credit (740+): This is the sweet spot. Borrowers in this range qualify for the lowest margins—typically 0.50% to 1.50% above the Prime Rate. If the Prime Rate is 8.50%, you might see a fully indexed rate between 9.00% and 10.00%. According to Figure, HELOC rates in California vary significantly based on your credit score, making this one of the most critical factors in your application.

Good Credit (680-739): You'll still qualify for competitive rates, but expect the margin to increase by 0.25% to 0.75%. Using the same Prime Rate example, your fully indexed rate might range from 9.25% to 10.75%.

Fair Credit (Below 680): This is where qualification becomes challenging, particularly for investment properties. Margins can jump to 2.50% or higher, and many lenders won't approve HELOCs for investment properties at all in this credit range. As Better notes, investment property HELOCs typically require a minimum credit score of 700-720, compared to just 650-680 for primary residences.

The difference between a 740 credit score and a 680 credit score can mean paying an extra $50 to $100 per month on a $100,000 HELOC balance—that's $600 to $1,200 annually just in additional interest costs.

Combined Loan-to-Value (CLTV): How Much Equity You're Leaving in the Property

Your Combined Loan-to-Value ratio measures the total debt you'll have against your property relative to its current market value. It's calculated using this formula:

CLTV = (Current Mortgage Balance + HELOC Limit) ÷ Current Home Value

For example, if your California investment property is worth $800,000, you owe $400,000 on your mortgage, and you want a $200,000 HELOC:

CLTV = ($400,000 + $200,000) ÷ $800,000 = 75%

Here's how CLTV affects your rate and approval:

Below 70% CLTV: You're in the best position. Lenders view this as low risk because you have substantial equity cushion. This typically qualifies you for the lowest available margin.

70-80% CLTV: This is the standard range for most borrowers. Rates are still competitive, but you'll see margins increase by 0.25% to 0.50% compared to the sub-70% tier.

80-85% CLTV: You're approaching maximum leverage. Expect significantly higher margins (an additional 0.50% to 1.00%) and more stringent underwriting. Some lenders cap investment property HELOCs at 75% CLTV and won't go higher.

Above 85% CLTV: Very few lenders will approve a HELOC at this level, especially for investment properties. If you do find one, the rate will be substantially higher.

The CLTV threshold is particularly important for California real estate investors because property values in the state are so high. A 5% difference in CLTV on an $800,000 property represents $40,000 in equity—a significant buffer that lenders carefully evaluate.

Property Type: Investment vs. Primary Residence Rate Differential

This is where California real estate investors face a notable disadvantage. Lenders categorize properties based on how they're used, and investment properties are considered higher risk for two reasons: first, borrowers are more likely to default on an investment property than their primary home during financial hardship; second, rental income can be variable and harder to verify than W-2 wages.

Here's the typical rate differential:

Primary Residence: Lowest margins, typically 0.50% to 2.00% above Prime Rate. Maximum CLTV often reaches 85-90%.

Investment Property: Margins are typically 0.50% to 1.50% higher than primary residence rates. So if a primary residence HELOC has a 1.50% margin, expect 2.00% to 3.00% for an investment property. Maximum CLTV is usually capped at 75%.

On a $150,000 HELOC balance, that extra 1.00% margin translates to $1,500 per year in additional interest costs. Over a 10-year draw period, you're looking at $15,000 in extra expense simply because the property generates rental income rather than serving as your home.

Additionally, investment property HELOCs often come with stricter debt-to-income requirements and may require larger cash reserves (typically 6-12 months of PITI payments) to be held in liquid accounts.

Loan Amount: Size Matters, But Not Always How You'd Expect

The size of your requested HELOC can influence your rate in two opposing directions:

Larger HELOCs ($250,000+): Some lenders offer rate discounts for larger lines of credit because the profit potential justifies the underwriting expense. You might see a 0.10% to 0.25% reduction in margin for HELOCs above $250,000 or $500,000. This is particularly relevant in California's high-value markets.

Smaller HELOCs (Under $50,000): Conversely, some lenders charge higher rates or additional fees for very small HELOCs because the administrative costs don't scale down proportionally. You might encounter minimum loan amounts of $25,000 or $50,000 with some California lenders.

The Sweet Spot: For most California lenders, the most competitive rates are typically found in the $100,000 to $300,000 range—large enough to be profitable for the lender but not so large that it requires exceptional income verification.

Why Your Quote Will Differ From Advertised Rates

Now you understand why that 6.99% rate you saw advertised doesn't match the 9.25% quote you received. The advertised rate likely assumed:

- A credit score of 760+

- A primary residence (not an investment property)

- A CLTV below 70%

- A loan amount in the lender's preferred range

- Perfect debt-to-income ratio

- Substantial cash reserves

If any of these factors don't align with your situation, your rate will be higher. The key is to shop around with realistic expectations based on your actual financial profile and property type. Get quotes from at least three to five lenders, and make sure you're comparing apples to apples—the same loan amount, same property type, and same CLTV—so you can identify which lender is truly offering the most competitive terms for your specific situation.

Why a HELOAN is Often the Better Choice for California Real Estate Investors

While HELOCs have their place in the home financing landscape, savvy California real estate investors increasingly turn to Home Equity Loans (HELOANs) for their investment strategies. The reason is simple: predictability and control are paramount when running the numbers on an investment property.

The Power of Predictable Cash Flow

When you're analyzing a fix-and-flip opportunity or planning a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, accurate ROI calculations depend on knowing your exact holding costs. HELOANs provide fixed interest rates and fixed monthly payments, which means you can project your financing costs with complete certainty for the life of the loan.

Consider this scenario: You're evaluating a distressed property in Riverside that needs $75,000 in renovations. With a HELOC's variable rate, your monthly payment could start at $450 but climb to $650 or more as rates fluctuate. That $200+ monthly swing directly impacts your profit margin and could turn a winning deal into a break-even proposition. With a HELOAN's fixed payment, you know from day one that you'll pay exactly $712 per month for the next 15 years—no surprises, no recalculations, no erosion of your projected returns.

Immediate Access to Capital When Opportunity Knocks

Real estate investing often requires acting quickly. When you find an undervalued property or need to close on a time-sensitive deal, a HELOAN provides immediate access to capital through a lump-sum distribution at closing. This is fundamentally different from a HELOC's revolving line of credit structure.

With a HELOAN, you receive all the loan proceeds upfront, making it ideal for:

- Down payments on investment properties: Secure your next rental property with 20-25% down without liquidating other investments

- Major renovation projects: Fund a complete rehab from demolition to finish work with one upfront sum

- Portfolio expansion: Purchase multiple properties or invest in larger commercial opportunities

- Seizing market opportunities: Act immediately when you find a below-market deal at auction or through your network

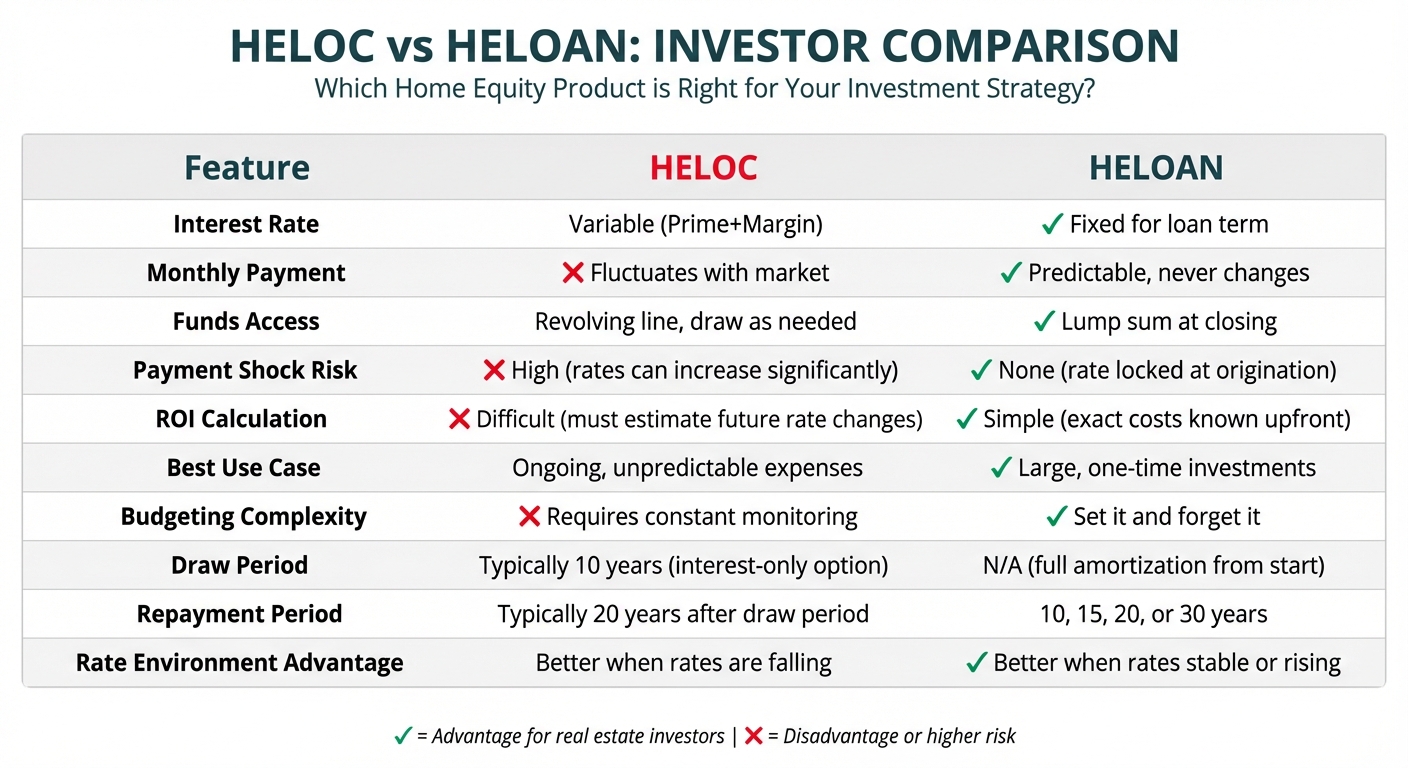

HELOC vs. HELOAN: A Side-by-Side Comparison for California Investors

| Feature | HELOC | HELOAN (OfferMarket) |

|---|---|---|

| Interest Rate | Variable (Prime + Margin) | Fixed for loan term |

| Monthly Payment | Fluctuates with market rates | Predictable, never changes |

| Funds Access | Revolving line of credit, draw as needed | Lump sum at closing |

| Payment Shock Risk | High (rates can increase significantly) | None (rate locked at origination) |

| ROI Calculation | Difficult (must estimate future rate changes) | Simple (exact costs known upfront) |

| Best Use Case | Ongoing, unpredictable expenses | Large, one-time investments |

| Budgeting Complexity | Requires constant monitoring | Set it and forget it |

| Draw Period | Typically 10 years (interest-only option) | N/A (full amortization from start) |

| Repayment Period | Typically 20 years after draw period | 10, 15, 20, or 30 years |

| Rate Environment Advantage | Better when rates are falling | Better when rates are stable or rising |

The OfferMarket Advantage for California Investors

At OfferMarket, we've built our HELOAN product specifically with real estate investors in mind. We understand that your time is valuable and that every day without capital is a day of lost opportunity. That's why we've created a streamlined, tech-forward application process that delivers competitive fixed rates without the bureaucracy of traditional lenders.

What sets us apart:

- Speed: Get pre-qualified in 60 seconds online, with full approval in days, not weeks

- Transparency: No hidden fees, no bait-and-switch tactics—the rate you see is the rate you get

- California Expertise: Our loan specialists understand the unique dynamics of California's real estate market, from Bay Area multifamilies to San Diego vacation rentals

- Investor-Focused: We underwrite with an investor's mindset, recognizing that investment properties require different analysis than primary residences

- Competitive Fixed Rates: Lock in today's rate and protect yourself from future market volatility

For California real estate investors who need to know their exact numbers, plan accurate budgets, and execute their investment strategies with confidence, a fixed-rate HELOAN from OfferMarket provides the financial foundation for long-term success.

Advanced Investor FAQ: HELOCs, HELOANs, and DSCR Loans in California

For sophisticated California real estate investors, understanding the nuances of home equity financing can mean the difference between a profitable deal and a missed opportunity. Below, we address the most technical questions we receive from experienced investors navigating the intersection of HELOCs, HELOANs, and DSCR loans.

Can I Use Un-Drawn HELOC Funds to Meet DSCR Loan Liquidity Requirements?

Short answer: No, almost never.

When applying for a DSCR (Debt Service Coverage Ratio) loan on an investment property, lenders typically require you to demonstrate liquid reserves—usually 6 to 12 months of PITIA (Principal, Interest, Taxes, Insurance, and Association dues). According to OfferMarket's DSCR loan requirements, these reserves must be liquid, verifiable assets such as cash in bank accounts, stocks, bonds, or retirement accounts.

An un-drawn HELOC line of credit, regardless of how much available credit you have, is viewed by underwriters as potential debt, not an asset. It represents borrowing capacity, not actual funds you currently possess. DSCR lenders need to see that you have real money set aside to cover mortgage payments during vacancy periods or unexpected expenses—not just the ability to borrow more money if needed.

The logic is straightforward: If the rental property experiences an extended vacancy or requires major repairs, the lender wants assurance you can cover the mortgage without immediately taking on additional debt. Allowing un-drawn credit lines to count as reserves would defeat this purpose entirely.

What does count as reserves?

- Checking and savings accounts

- Stocks, bonds, and mutual funds (typically 70% of value)

- Retirement accounts like 401(k)s and IRAs (typically 60-70% of vested balance)

- Cash value of whole life insurance policies

If you're planning a DSCR loan purchase and need to boost your reserves, consider leaving funds in liquid accounts rather than immediately deploying them elsewhere, or document other investment accounts that can be liquidated if necessary.

How Do I Refinance My Investment Property HELOC Without Triggering Cash-Out Classification?

This is one of the most sophisticated questions California investors ask, and getting it wrong can cost you significantly in terms of rates and qualification requirements.

The 12-Month Seasoning Rule

To refinance an existing HELOC as a "rate-and-term" refinance (which comes with better rates and more lenient underwriting than a cash-out refinance), your HELOC must be "seasoned" for at least 12 months. According to DSCR loan seasoning requirements, seasoning is measured from the recording date of your original HELOC to the application date of your new loan.

The $2,000 Draw Limit

Even if your HELOC has been open for more than 12 months, you must have drawn less than $2,000 from the line of credit in the 12 months preceding your refinance application. If you've drawn more than this amount, the transaction will be classified as a cash-out refinance, regardless of seasoning.

Why does this matter?

Cash-out refinances on investment properties come with:

- Higher interest rates (typically 0.375% to 0.75% higher)

- Lower maximum LTV ratios (often capped at 70-75% instead of 75-80%)

- More stringent underwriting requirements

- Potentially higher reserve requirements

Strategic planning tip: If you're considering refinancing your investment property HELOC in the near future, avoid drawing from it. Even a small $3,000 draw to cover a minor repair could force you into cash-out pricing, costing you thousands over the life of the loan. Instead, use other funding sources for short-term needs if you're within 12 months of a planned refinance.

What if I need to refinance sooner?

Some California lenders, particularly those specializing in DSCR loans, offer more flexible seasoning requirements. As noted by A Good Lender, certain DSCR loan programs have zero seasoning requirements, allowing you to refinance immediately after closing if market conditions warrant it. However, these loans will still be priced as cash-out transactions if you've drawn funds recently.

What Are Typical Closing Costs for a HELOC or HELOAN in California?

California closing costs for home equity financing can vary dramatically based on the lender, loan amount, property location, and whether you're financing a primary residence or investment property.

Standard Cost Breakdown:

Appraisal Fee: $400-$800

- Investment properties typically require full appraisals rather than automated valuations

- Complex properties or those in rural areas may cost more

- Some lenders offer appraisal waivers for low LTV loans on recently purchased properties

Title Search and Insurance: $300-$1,200

- California title costs are regulated but vary by county

- Investment properties may require additional endorsements

- If you've refinanced recently, you may qualify for a "reissue rate" discount

Recording Fees: $50-$200

- Set by county recorder's offices

- Los Angeles and San Francisco counties tend to be on the higher end

Loan Origination/Processing Fees: $0-$1,500

- Many lenders advertise "no-cost" HELOCs or HELOANs

- "No-cost" typically means fees are rolled into a slightly higher interest rate

- For large loan amounts ($250,000+), negotiate these fees down or request them to be waived

Credit Report Fee: $30-$100

Flood Certification: $15-$25

Document Preparation: $0-$500

Total Estimated Range: $0-$4,000

The "no-cost" option trade-off: Many California lenders, especially credit unions and online lenders, offer zero-closing-cost HELOCs and HELOANs. While this sounds attractive, you'll typically pay a 0.25% to 0.50% higher interest rate over the life of the loan. For a $200,000 HELOAN, that higher rate could cost you $10,000-$20,000 extra over a 15-year term—far more than the $2,000 in upfront costs you avoided.

Investment property consideration: Closing costs on investment properties are generally 10-20% higher than on primary residences due to additional underwriting requirements and risk-based pricing. Budget accordingly when running your deal numbers.

How Long Does the Home Equity Financing Process Take in California?

Timeline expectations vary significantly based on your chosen lender, property type, and transaction complexity.

Typical Timeline Breakdown:

Online Lenders (OfferMarket, Figure, Spring EQ): 2-3 Weeks

- Application and initial approval: 1-3 days

- Appraisal ordered and completed: 5-10 days

- Underwriting and final approval: 3-7 days

- Document signing and funding: 1-3 days

- Streamlined digital processes significantly reduce timeline

- Best for straightforward transactions with strong borrower profiles

Traditional Banks (Chase, Wells Fargo, BofA): 4-6 Weeks

- Application and initial review: 3-7 days

- Appraisal process: 7-14 days

- Underwriting: 10-14 days

- Closing preparation and funding: 5-7 days

- More documentation requirements and manual review processes

- May experience delays during high-volume periods

Credit Unions (Golden 1, Patelco): 3-5 Weeks

- Membership verification and application: 2-5 days

- Appraisal: 7-10 days

- Committee review (for large loans): 7-14 days

- Closing and funding: 3-5 days

- Often more personalized service but potentially slower approval processes

- Investment property loans may require additional committee approvals

Factors That Accelerate the Process:

- Pre-gathering all required documentation (tax returns, bank statements, property tax bills)

- High credit score (740+) and low LTV (<70%)

- Recent appraisal on file (within 6 months)

- Clear title with no liens or complications

- Strong, documented income for traditional loans or solid rental income for DSCR loans

Factors That Slow Things Down:

- Multiple properties requiring cross-collateralization analysis

- Title issues, easements, or property boundary disputes

- Appraisal comes in lower than expected, requiring renegotiation

- Investment properties in rural areas where appraiser availability is limited

- High LTV requests requiring additional underwriting scrutiny

California-specific timing considerations: California's robust consumer protection laws mean lenders must provide specific disclosures and waiting periods. For HELOCs, you have a three-day right of rescission after signing (for primary residences), which adds to the timeline. Investment properties don't have this requirement, potentially shaving a few days off the process.

Pro tip for time-sensitive deals: If you're eyeing a time-sensitive investment opportunity—such as an off-market deal or auction property—start your HELOAN or HELOC application process 4-6 weeks before you anticipate needing the funds. Having a pre-approved line of credit or loan in place gives you the speed of a cash buyer, a significant competitive advantage in California's fast-moving real estate market.

Get Your Personalized California HELOAN Rate in 60 Seconds

If you're a California real estate investor looking for predictable financing with a fixed rate and fixed monthly payment, a Home Equity Loan (HELOAN) from OfferMarket might be your best path forward. Unlike the variable-rate uncertainty of a HELOC, a HELOAN gives you the clarity and confidence you need to accurately project your investment returns.

Why Choose OfferMarket for Your California Home Equity Loan?

Streamlined Online Process: We've eliminated the paperwork maze. Our digital application takes just minutes to complete, and you can get a personalized rate quote in as little as 60 seconds—without any commitment and with zero impact on your credit score. No waiting on hold, no back-and-forth emails, just straightforward answers when you need them.

Competitive Fixed Rates: We specialize in working with California real estate investors, which means we understand your unique financing needs. Our fixed-rate HELOANs offer competitive pricing with the predictability that variable-rate HELOCs simply cannot match. When you're calculating your ROI on a fix-and-flip or analyzing a BRRRR deal, knowing your exact monthly payment for the life of the loan is invaluable.

California Real Estate Investment Expertise: Our loan specialists understand the California market inside and out. Whether you're leveraging equity from your primary residence to fund an investment property purchase, or tapping into equity from an existing rental to finance a major renovation, we speak your language. We know the challenges California investors face—from high property values to competitive markets—and we're here to help you move quickly when opportunity knocks.

Take Action Now: Simple Ways to Get Started

Get Your Free HELOAN Rate Quote

Ready to see what rate you qualify for? Our online tool provides a real-time, personalized HELOAN rate quote based on your California property and financial profile. The entire process takes about 60 seconds, requires no commitment, and won't affect your credit score.

Ready to see what your equity can do? Start with an instant quote, then talk to our loan team to explore your options. If you're not sure about anything, we’re just a phone call away at (443) 492-9941.

What Happens After You Apply?

Once you submit your application, here's what you can expect:

Instant Pre-Qualification: You'll receive your personalized rate quote and estimated loan amount within 60 seconds.

Document Upload: If you decide to move forward, you'll upload supporting documents (property information) through our secure portal.

Property Appraisal: We'll order an appraisal of your California property to confirm its current market value.

Final Approval: Our underwriting team reviews your complete application, typically within 3-5 business days.

Closing: Sign your documents (often electronically) and receive your lump-sum funding, usually within 1-3 weeks from application.

The entire process is designed to be as fast and frictionless as possible, because we know that in California's competitive real estate market, timing can make or break a deal. When you find that perfect investment property or need to move quickly on a renovation to maximize your return, OfferMarket is ready to help you access your equity without delay.

OfferMarket Loans

Check your rate

60 seconds · no credit pull