*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The 2026 Housing Act: A Green Light for Small Real Estate Investors

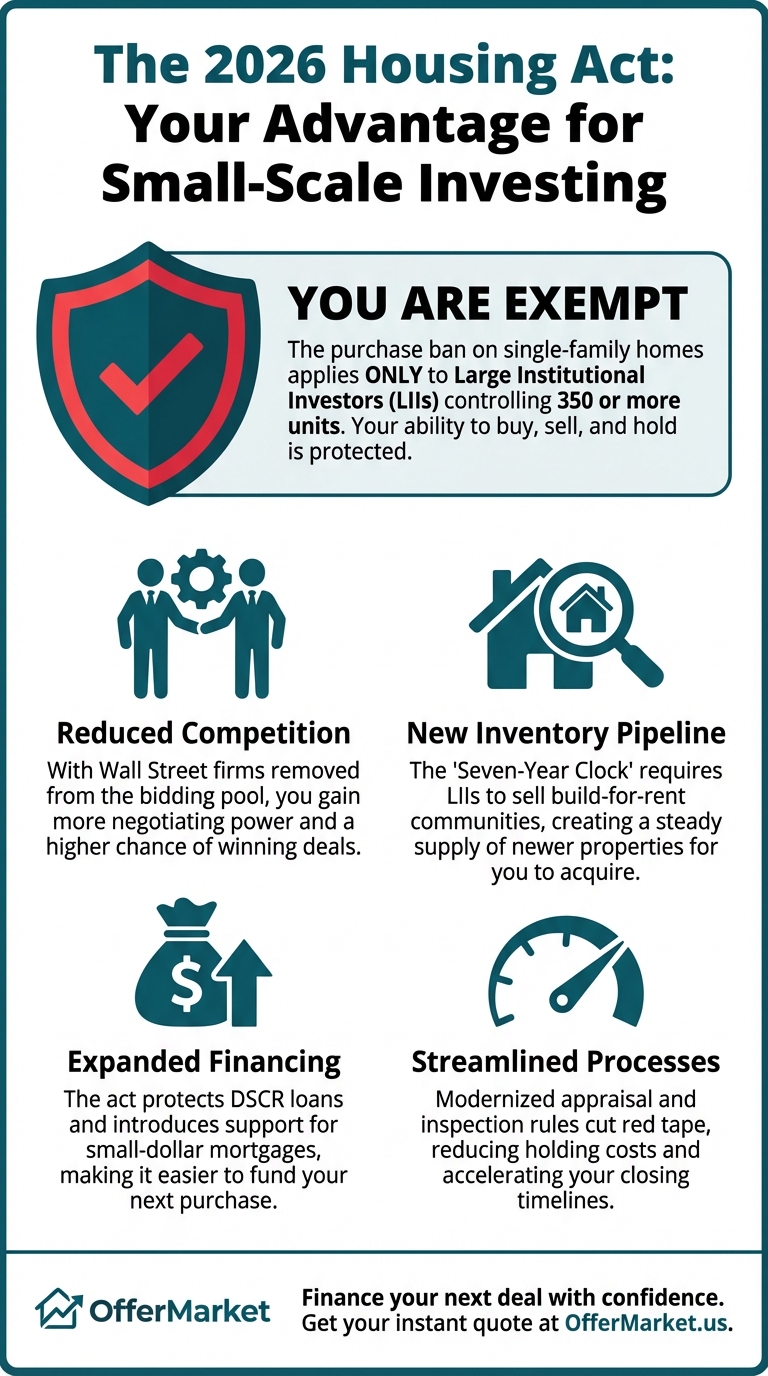

The 21st Century ROAD to Housing Act, passed by the Senate in March 2026, is not a barrier to your investment strategy; it is a strategic advantage. This legislation explicitly targets "Large Institutional Investors" (LIIs)—defined as any entity with investment control over 350 or more single-family rental units. If your portfolio, including all properties held across various LLCs you control, falls below this 350-unit threshold, you are exempt from the bill's purchasing restrictions.

The law is designed to level the playing field by curbing the market dominance of mega-firms, creating a more favorable environment for small-scale investors to acquire properties, secure financing, and grow their portfolios. Understanding the mechanics of this bill is the first step to capitalizing on the significant opportunities it presents.

This legislation effectively removes your largest, most aggressive competitors from the bidding pool for single-family homes. For years, small investors have been outbid by cash-rich institutional funds making non-contingent offers. The 21st Century ROAD to Housing Act reverses this trend, restoring market access and negotiating power to "mom-and-pop" investors.

Furthermore, the bill strengthens your ability to secure financing by protecting the DSCR loan market for investors like you, while also introducing measures to streamline appraisals and inspections, and create a future pipeline of high-quality rental inventory. This is not a red light for your business—it's a green light to accelerate your growth.

Debunking Common Myths About the Housing Affordability Bill 2026

Legislative changes often create uncertainty, and the 21st Century ROAD to Housing Act is no exception. Misinformation can spread quickly, causing unnecessary fear among the very investors the bill is designed to protect. It's crucial to separate fact from fiction to make informed decisions for your business. Let's address the most common myths head-on.

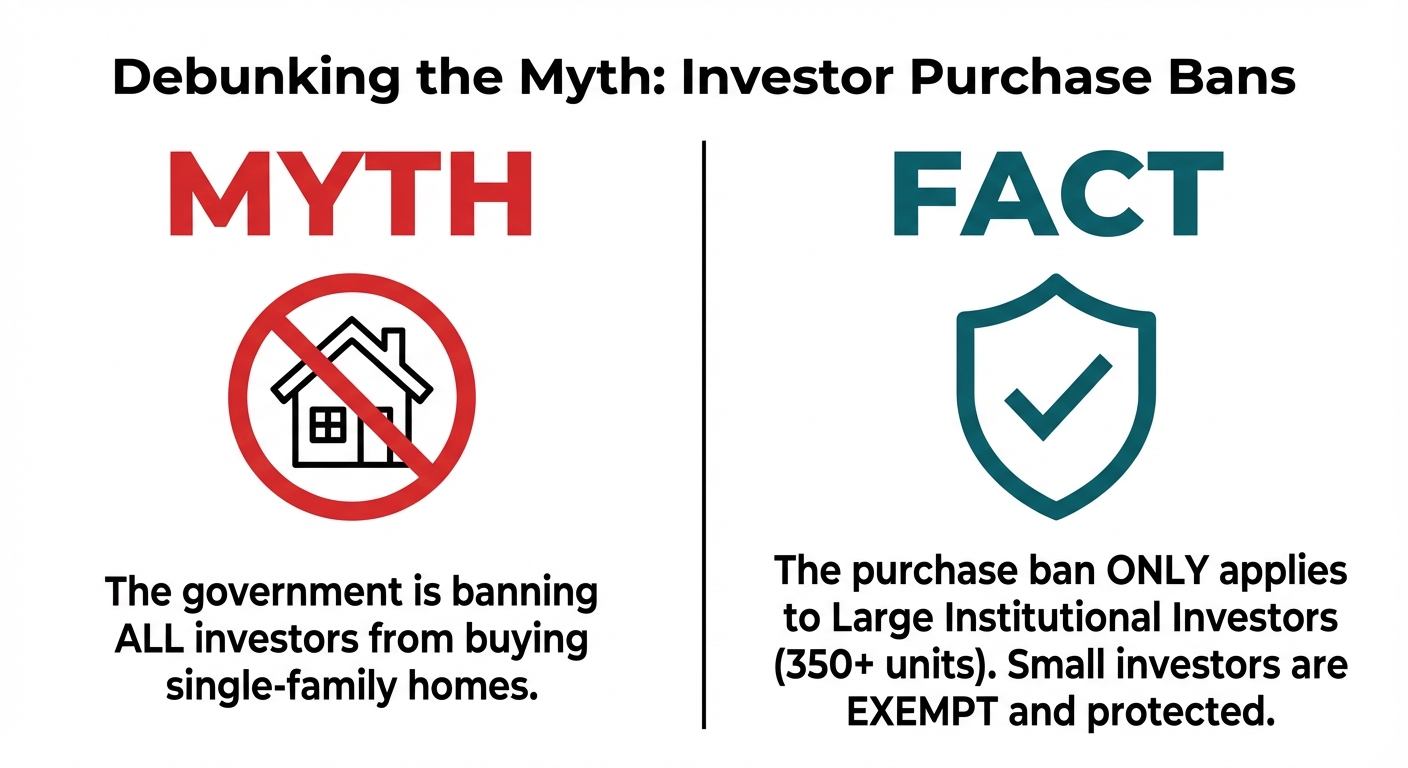

Myth: This bill bans all investors from buying single-family homes.

Fact: This is the most significant and widespread misconception. The bill's restrictions are surgically targeted at Large Institutional Investors (LIIs), which are clearly defined as entities controlling 350 or more single-family properties. If you are a small-scale investor operating under this threshold, your ability to purchase single-family homes is completely unaffected. The legislative language was carefully crafted to distinguish between "mom-and-pop" landlords, who are seen as a vital part of the housing ecosystem, and mega-corporations, whose rapid acquisitions have been linked to affordability challenges.

Myth: The government will force me to sell my rental properties.

Fact: The bill contains absolutely no provision that forces small-scale investors to sell their existing properties. The divestment mandate, often referred to as the "Seven-Year Clock," applies only to LIIs and only to newly constructed build-for-rent communities they develop after the law takes effect. Your current portfolio is secure. You can continue to hold your properties for as long as your investment strategy dictates, whether that's for long-term cash flow or future appreciation. The goal is to prevent future consolidation of housing stock by large firms, not to penalize existing small landlords.

Myth: DSCR loans and investing through an LLC will be restricted.

Fact: The legislation does not target financing methods or legal structures; it targets portfolio scale. Using an LLC to purchase investment properties remains a best practice for liability protection, and the law respects this. The government's enforcement will rely on "beneficial ownership" rules, meaning they will look at the ultimate individual controlling the assets, not the number of LLCs used. As long as the total number of properties under your control is below 350, you can continue using LLCs without issue. Consequently, the DSCR loan market, which is the primary financing vehicle for LLC-owned investment properties, remains fully intact and is implicitly encouraged for the small investors the bill champions.

Myth: This legislation will cause a housing market crash.

Fact: This is highly unlikely. The bill is designed to cool a specific segment of the market—bulk institutional purchases—not to trigger a widespread downturn. By removing LIIs, demand from one buyer class is reduced, which may temper the rapid price appreciation seen in some markets. However, this is more likely to lead to market stabilization rather than a crash. The underlying demand from primary homebuyers and small investors remains strong. Furthermore, the seven-year divestment rule for LIIs creates a phased and predictable release of new inventory, preventing a sudden market flood. As reported by housing economists at sources like the National Association of Realtors, market fundamentals are driven by supply, demand, and interest rates, and this bill aims to rebalance supply and demand in favor of individual owners, not destroy it.

Why the 21st Century ROAD to Housing Act Was Created

To fully grasp the opportunity this bill presents, it's essential to understand the legislative intent behind it. This was not a hastily drafted law aimed at penalizing property owners. It was a calculated response to a decade-long trend that has fundamentally reshaped the single-family housing market: the rise of the large institutional landlord.

Addressing the Rise of Large Institutional Ownership

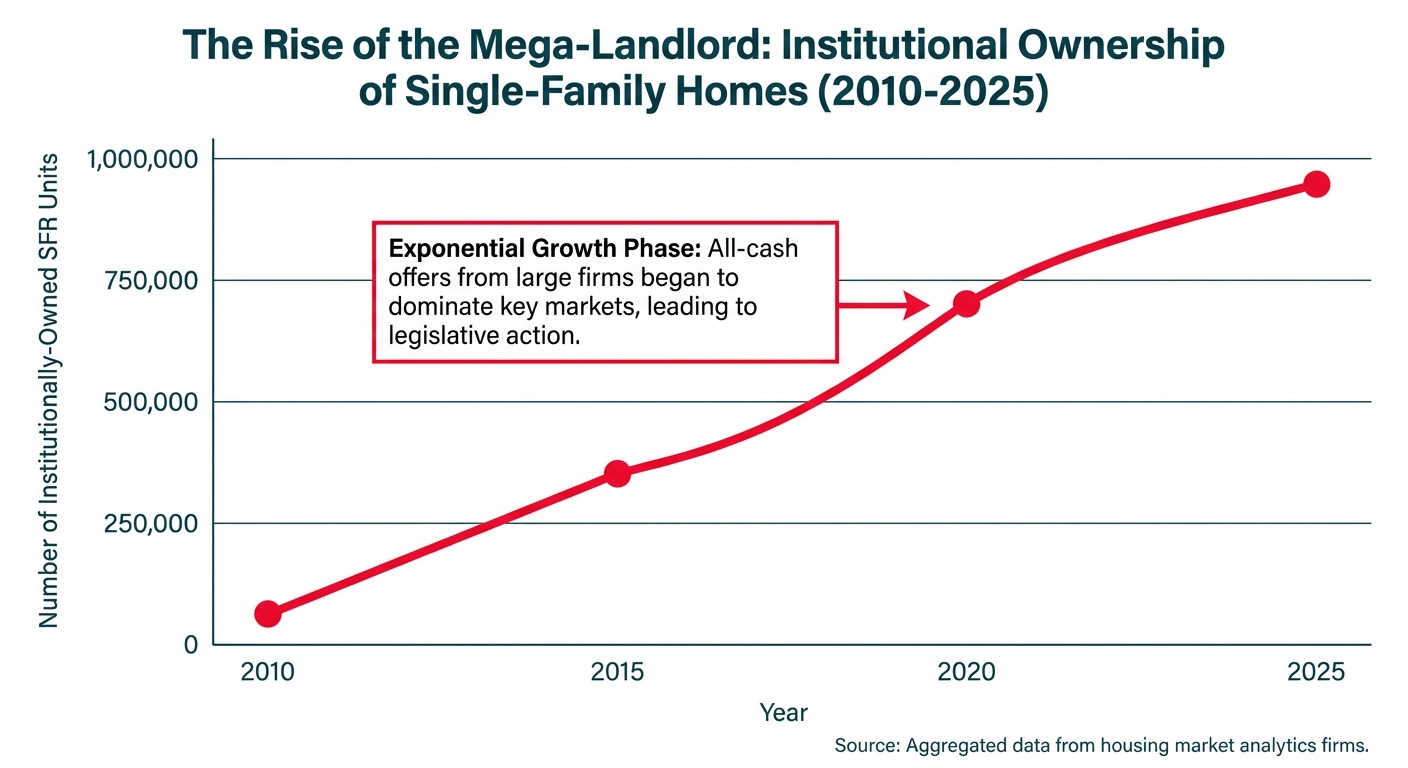

Following the 2008 financial crisis, billions of dollars in private equity capital flowed into the single-family housing market. Firms began buying thousands of foreclosed homes, converting them into rentals and creating a new asset class: the single-family rental (SFR) security. Over the next decade, this trend accelerated. According to data from real estate analytics firms, institutional ownership of single-family homes grew exponentially, with some firms amassing portfolios of over 80,000 properties. This concentration of ownership in the hands of a few large, publicly-traded companies raised alarms among policymakers.

The Problem of Cash-Rich Firms Pricing Out Buyers

The primary concern was the impact on housing affordability. LIIs, with their access to vast pools of capital, could make all-cash, no-contingency offers that individual homebuyers and small investors simply could not match. This created an uneven playing field, particularly in high-growth markets. A 2022 report highlighted in publications like HousingWire noted that in some metropolitan areas, institutional investors were purchasing nearly one-third of all single-family homes sold. This intense competition drove up prices, pushing homeownership out of reach for many families and making it nearly impossible for local investors to acquire new properties at reasonable prices. The bill's sponsors argued that this dynamic was detrimental to community stability and wealth creation for average Americans.

Protecting Housing Affordability for the Broader Market

The ultimate goal of the 21st Century ROAD to Housing Act is to restore balance. By limiting the ability of the largest players to continue expanding their portfolios, the law aims to slow down investor-driven price inflation. The legislative theory is that by reintroducing a more diverse pool of buyers—including aspiring homeowners and small-scale landlords—the market will function more efficiently and fairly. It's a targeted intervention designed to protect the traditional single-family market from becoming fully financialized and controlled by Wall Street, ensuring it remains accessible to the individuals and families who form the bedrock of local communities. For small investors, this means the market is being recalibrated in their favor.

You Are Exempt: The 350-Unit Threshold Explained

The single most critical piece of information in the 21st Century ROAD to Housing Act is the 350-unit threshold. This number is the bright line that separates small-scale investors, who are protected by the law, from the Large Institutional Investors (LIIs) the law seeks to regulate. Let's break down exactly what this means for you and your portfolio.

The Critical Distinction: No Forced Sales for Your Existing Properties

It bears repeating: if your portfolio is under 350 single-family units, you are not required to sell any of your properties. The forced divestment provisions in the bill are exclusively for LIIs. This distinction is fundamental to the bill's structure. Lawmakers recognized that small landlords are often local community members who provide essential housing, and forcing them to sell would be counterproductive and destabilizing. Your assets are safe, and your long-term hold strategies are not in jeopardy.

Defining a Large Institutional Investor (LII)

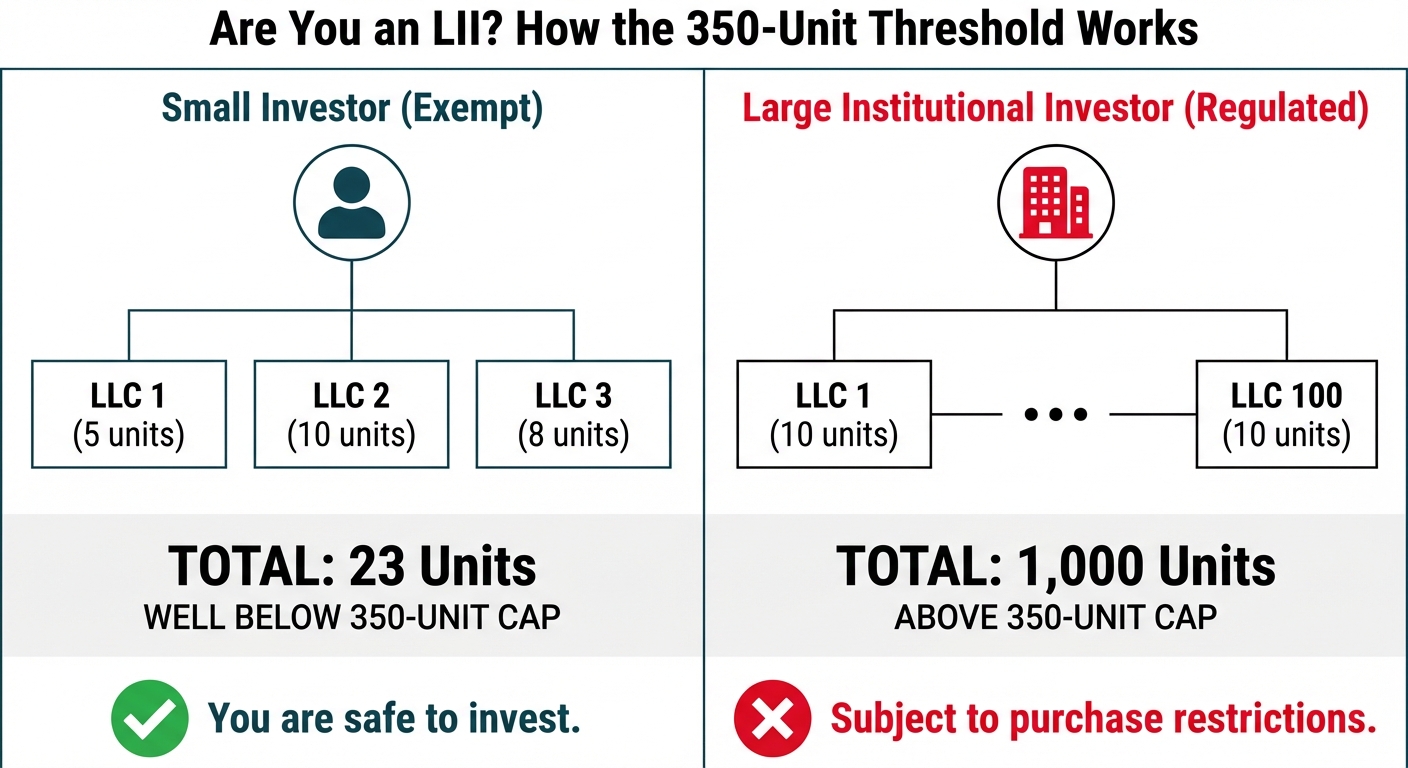

The bill defines an LII as any single entity—including its affiliates—that has direct or indirect investment control over 350 or more single-family homes located in the United States. The key phrase here is "investment control." This means the entity has the power to make key decisions about the properties, such as setting rents, approving capital expenditures, or deciding when to sell. This definition is designed to be comprehensive, preventing large firms from using complex legal structures to circumvent the law.

Calculating Your Portfolio Size Across All Controlled Entities and LLCs

To prevent loopholes, the legislation uses "beneficial ownership" and "control" as its guiding principles for aggregation. This means regulators will "look through" corporate structures to identify the ultimate owner.

For a Small Investor: Imagine you own three LLCs. LLC A owns 5 homes, LLC B owns 10 homes, and LLC C owns 8 homes. Because you are the ultimate beneficial owner of all three LLCs, your total portfolio size is calculated as 5 + 10 + 8 = 23 units. Since 23 is well below the 350-unit threshold, you are completely exempt from the purchase restrictions.

For a Large Institution: A private equity fund creates 50 separate LLCs, each of which buys 10 homes. While each individual LLC only owns 10 homes, the fund is the ultimate beneficial owner with investment control over all 50 LLCs. Therefore, its portfolio size is calculated as 50 x 10 = 500 units. Since 500 is above the 350-unit threshold, this fund is classified as an LII and is subject to the purchasing ban.

This aggregation rule ensures that the law targets the true scale of an operation, not the legal formalities. As a small investor, you can continue to use multiple LLCs for organization and liability protection without fear of being misclassified.

Confirmation That the Purchase Ban Does Not Apply to Small-Scale Investors

The text of the 21st Century ROAD to Housing Act and the associated committee reports explicitly state that the intent is to preserve the ability of individuals and small businesses to invest in real estate. The 350-unit figure was chosen after extensive market analysis to separate the largest national players from the regional and local investors who constitute the vast majority of landlords. Your business model—acquiring and managing a portfolio of 1-4 unit properties—is not the target of this legislation. In fact, it's the model the legislation aims to empower.

A New Competitive Edge: Outmaneuvering Institutional Cash

For over a decade, the greatest challenge for small investors has been competing with the seemingly limitless supply of institutional cash. The 21st Century ROAD to Housing Act fundamentally alters this dynamic, handing a significant competitive advantage back to you.

How the Removal of LIIs from the Bidding Pool Benefits You

When a desirable property hits the market, you will no longer be bidding against massive firms that can offer cash, waive all contingencies, and close in a matter of days. This has several immediate, practical benefits:

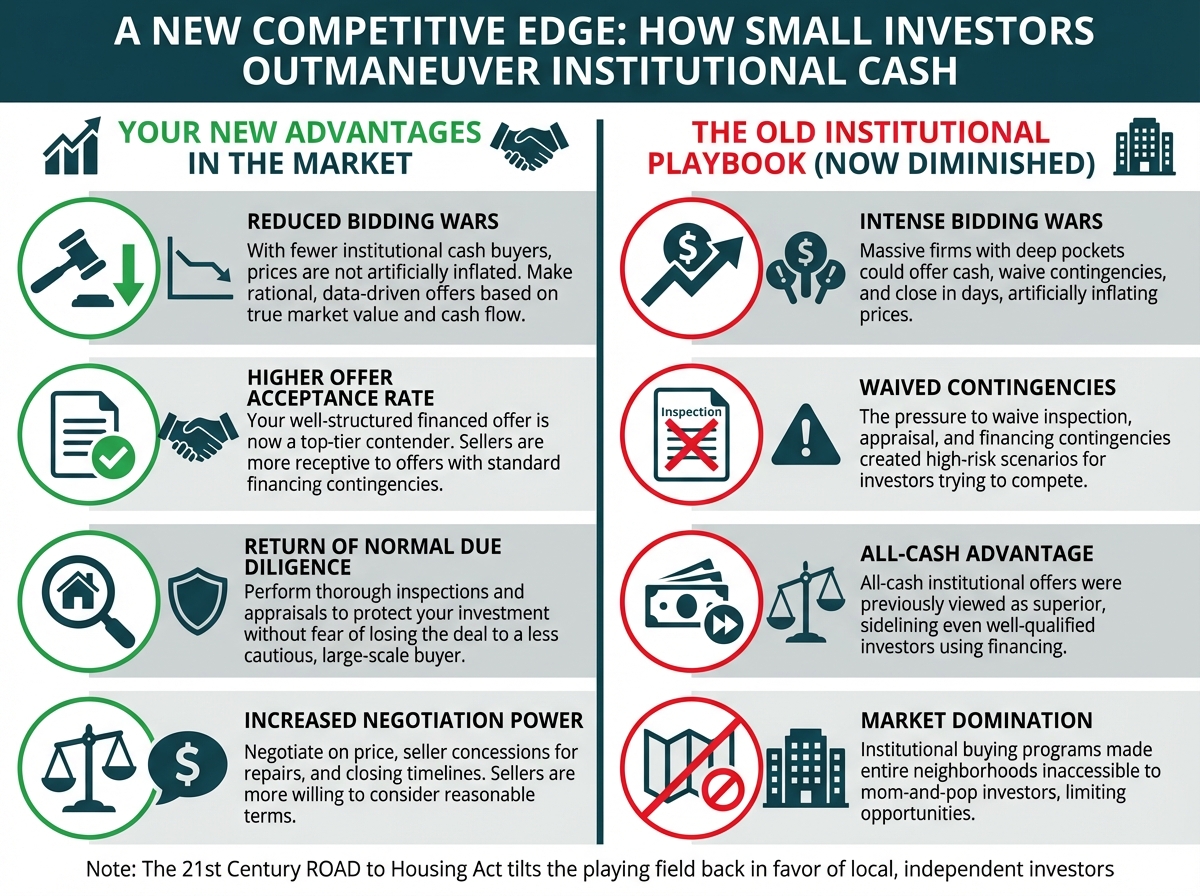

Reduced Bidding Wars: With fewer deep-pocketed buyers in the market, the likelihood of intense, multi-offer bidding wars decreases. This prevents prices from being artificially inflated and allows you to make more rational, data-driven offers based on the property's true market value and potential cash flow.

Higher Offer Acceptance Rate: Sellers and their agents will be more receptive to financed offers. Previously, an offer with a financing contingency, even from a well-qualified investor, was often viewed as inferior to an all-cash institutional offer. Now, your well-structured offer, backed by a reliable lender like OfferMarket, becomes a top-tier contender.

Return of Normal Due Diligence: The pressure to waive inspection, appraisal, and financing contingencies to compete with LIIs will dissipate. You can once again perform thorough due diligence to protect your investment without fear of losing the deal to a less cautious, large-scale buyer.

Increased Negotiation Power with Sellers

The shift in market dynamics also enhances your ability to negotiate. When sellers have fewer all-cash, "as-is" offers to choose from, they become more willing to consider offers with reasonable terms. You can negotiate on price, request seller concessions for repairs identified during an inspection, or ask for a closing timeline that better suits your financing needs. This return to traditional negotiation practices allows you to secure better deals and mitigate risks more effectively.

The Return of Market Access for Mom-and-Pop Investors

Ultimately, this legislation re-opens doors that had been closing for small investors. Markets that were once dominated by institutional buying programs are now accessible again. You can confidently analyze deals in your target neighborhoods, knowing that you have a fair chance of acquiring them. This isn't just about leveling the playing field; it's about tilting it back in favor of the local, independent investors who have historically been the backbone of the single-family rental market.

Unlocking Capital: Expanded Financing for Small Investors

A common fear surrounding new housing legislation is that it will tighten credit and make financing more difficult. The 21st Century ROAD to Housing Act does the opposite. By targeting portfolio size rather than lending practices, it protects and implicitly encourages the use of powerful financing tools for small investors.

The Bill Protects and Implicitly Encourages DSCR Financing

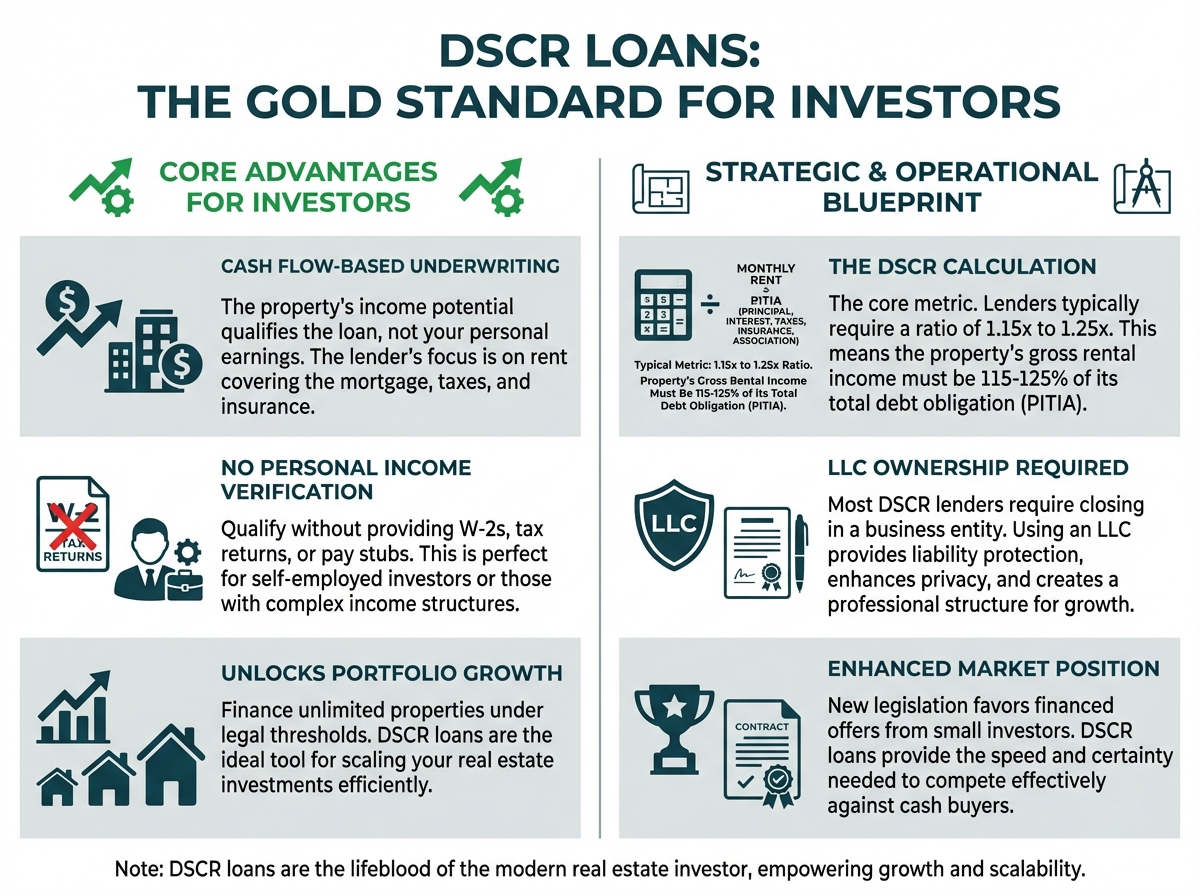

Debt Service Coverage Ratio (DSCR) loans are the lifeblood of the modern real estate investor. They allow you to qualify for a loan based on the property's income potential rather than your personal W-2 earnings. Since the new law focuses on the number of properties owned, not how they are financed, the entire DSCR lending industry remains robust for investors under the 350-unit cap.

In fact, the law indirectly strengthens the case for DSCR loans. With less competition from cash buyers, more investors will be able to successfully win contracts with financed offers. This will likely lead to an increase in demand for DSCR loans, and lenders will be eager to serve the now-empowered small investor market. Lenders like OfferMarket are perfectly positioned to meet this demand, providing the speed and certainty needed to compete effectively in this new environment.

DSCR Loans Remain the Gold Standard for Investors

The core mechanics of the DSCR loan remain unchanged and as powerful as ever:

Cash Flow-Based Underwriting: The lender's primary concern is whether the property's monthly rent will cover the proposed monthly mortgage payment (including principal, interest, taxes, and insurance), with a small buffer. A DSCR of 1.25x, for example, means the property's income is 125% of its debt obligation.

No Personal Income Verification: You don't need to provide tax returns, pay stubs, or W-2s. This is ideal for self-employed investors or those with complex income structures.

Unlimited Properties: While the new law caps LIIs at 350 units, most DSCR lenders, including OfferMarket, have long allowed investors to finance large portfolios, and this will continue for investors operating under the legal threshold.

Why LLCs Are Still the Ideal Structure for Financing Rental Properties

The vast majority of DSCR lenders require borrowers to close in the name of a business entity, typically an LLC. This protects both the lender and the borrower. The new legislation does not interfere with this standard practice. Using an LLC for each property or a series of properties continues to be the best strategy for:

- Liability Protection: It separates your personal assets from your business assets.

- Anonymity and Privacy: It keeps your personal name off of public property records.

- Scalability: It provides a clean, professional structure for managing and financing a growing portfolio.

Because the law's restrictions are tied to beneficial ownership, not the use of an LLC, the synergy between DSCR lending and the LLC structure remains the cornerstone of a sophisticated real estate investment strategy.

New Support for Small-Dollar and Niche Mortgages

Beyond protecting the core DSCR market, the 21st Century ROAD to Housing Act includes specific provisions designed to unlock capital for smaller, often-overlooked investment opportunities. These measures address long-standing friction points in the mortgage market, creating new avenues for portfolio growth.

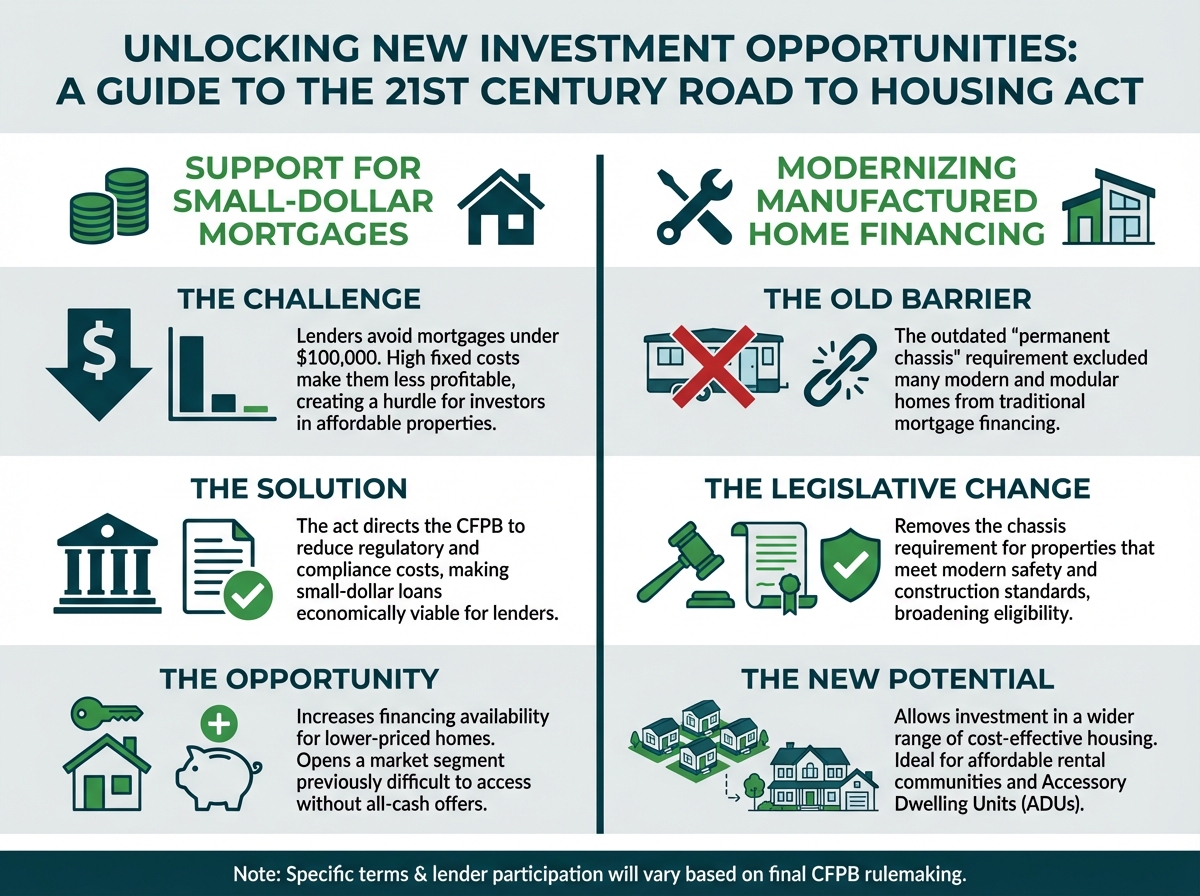

Overcoming Lender Reluctance for Mortgages Under $100,000

For years, lenders have been hesitant to originate small-dollar mortgages (often defined as those under $100,000 or even $150,000). The fixed costs of underwriting, compliance, and servicing a loan are roughly the same whether the loan is for $50,000 or $500,000. This makes small loans less profitable and, from a lender's perspective, less desirable. This has been a major hurdle for investors looking to buy affordable properties in many parts of the country.

The new act directs the Consumer Financial Protection Bureau (CFPB) to issue new rules that reduce the regulatory burden and compliance costs associated with originating small-dollar mortgages. By making these loans more economically viable for lenders, the bill aims to increase the availability of financing for lower-priced homes, opening up a segment of the market that was previously difficult to access without using all cash.

Financing Opportunities for Manufactured and Factory-Built Housing

The bill also modernizes lending rules for manufactured housing, a critical source of affordable rental units. Historically, a significant barrier to financing manufactured homes has been the requirement that the home be affixed to a "permanent chassis." This often excluded innovative or modular housing types from traditional mortgage financing.

The 21st Century ROAD to Housing Act removes this outdated "permanent chassis" requirement for properties that meet modern safety and construction standards. This change broadens the types of properties eligible for financing, allowing you to invest in a wider range of cost-effective housing solutions. This is particularly beneficial for investors looking to create affordable rental communities or add accessory dwelling units (ADUs) to existing properties.

Streamlining Your Deals: Modernized Appraisals and Inspections

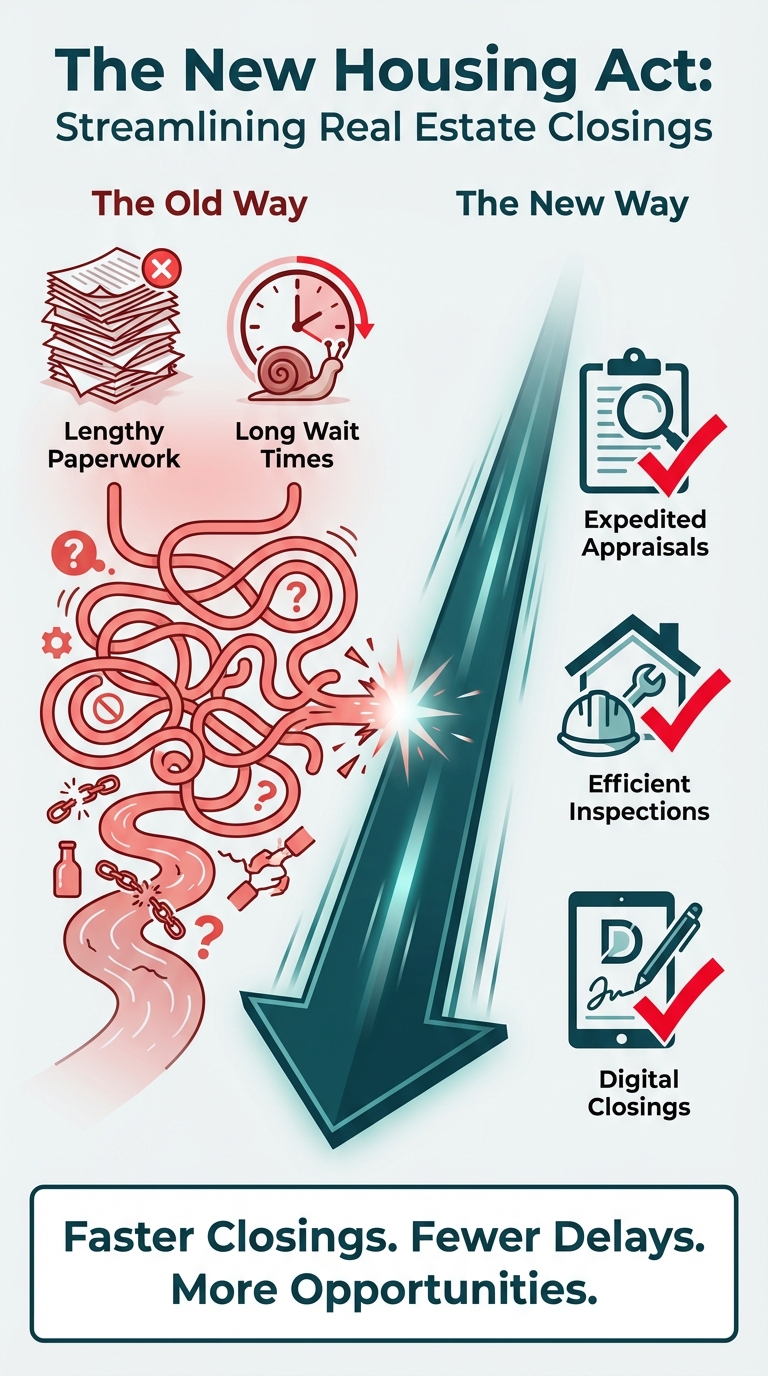

Time is money in real estate, and administrative delays can erode your profits. The new housing act recognizes this and introduces two key changes aimed at cutting red tape and accelerating the transaction process.

Accelerating the Appraisal Process

A shortage of licensed appraisers has been a persistent bottleneck in the real estate industry, leading to long wait times and high costs, especially in rural or underserved areas. The 21st Century ROAD to Housing Act addresses this head-on by allowing licensed appraisal trainees to perform a greater role in federally related appraisals, provided they are properly supervised.

By expanding the pool of professionals who can conduct appraisal work, the bill aims to:

- Reduce Turnaround Times: More appraisers mean less of a backlog, allowing your transactions to move from contract to closing more quickly.

- Lower Costs: Increased competition and efficiency in the appraisal industry can lead to lower fees for investors.

- Improve Market Coverage: A larger workforce makes it easier to get timely appraisals in all geographic areas, not just major metropolitan centers.

For an investor, a faster, more reliable appraisal process means shorter holding periods for properties being refinanced and a greater ability to close purchases on time, strengthening your offers in the eyes of sellers.

The Power of Reciprocal Inspections

For investors who participate in federal housing programs, such as providing rentals for Section 8 voucher holders, redundant inspections have long been a source of frustration and delay. A property might need separate inspections to comply with Low-Income Housing Tax Credit (LIHTC) standards, HOME Investment Partnerships Program rules, and Housing Choice Voucher (Section 8) requirements, even though the standards are often very similar.

The new law introduces "reciprocal inspections." This means that if a property passes a comprehensive inspection for one federal program (like LIHTC), that inspection can be accepted as satisfying the requirements for other federal programs.

This simple, common-sense reform will:

- Eliminate Redundant Work: You no longer have to schedule and host multiple, nearly identical inspections.

- Reduce Administrative Delays: This cuts down the time between finding a tenant and having them move in, reducing vacancy loss.

- Lower Holding Costs: By getting a voucher-holding tenant into a property faster, you start generating cash flow sooner, which is critical for any rental investment.

This change makes it significantly more efficient to work with federal housing assistance programs, a strategy many investors use to secure reliable, long-term tenants.

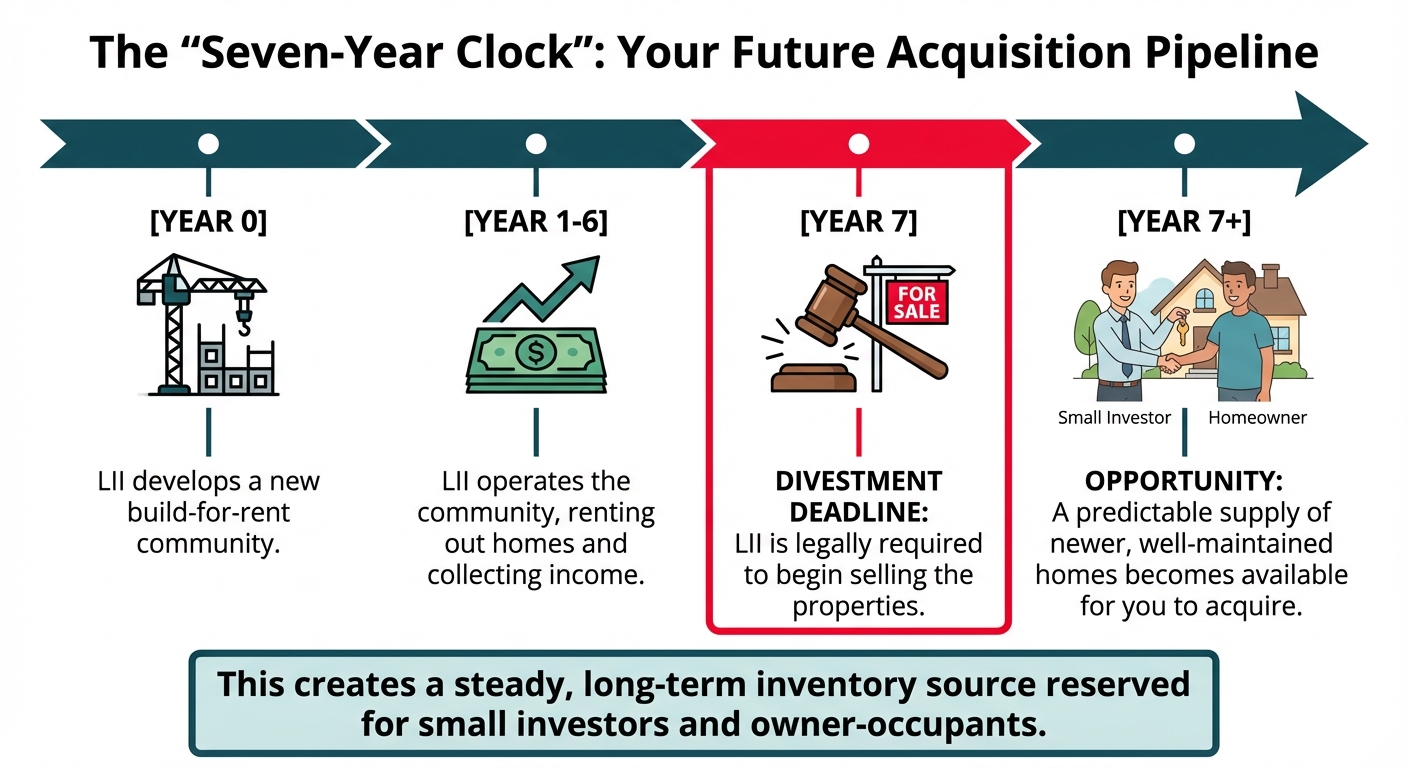

The Seven-Year Clock: A New Pipeline for Acquisitions

One of the most forward-looking components of the 21st Century ROAD to Housing Act is the "Seven-Year Clock," a provision that creates a predictable, long-term pipeline of acquisition opportunities specifically for small investors and individual buyers.

Understanding the LII Divestment Mandate

The rule is straightforward: any Large Institutional Investor (LII) that develops a new "build-for-rent" community of single-family homes must sell those homes within seven years of the project's completion. Critically, they are required to sell these properties to non-institutional buyers. This prevents them from simply selling entire communities to other large firms, ensuring the homes are returned to the traditional market.

A Predictable Future Supply of High-Quality Properties

This mandate creates a unique and powerful opportunity for strategic, long-term planning. For you, this means:

A Steady Stream of Inventory: Starting approximately seven years after the bill's passage, a new and predictable supply of rental properties will begin to hit the market. You can anticipate when and where these homes will become available by tracking LII development projects.

Newer-Vintage, Well-Maintained Homes: These will not be fixer-uppers. Build-for-rent communities are professionally managed and maintained, meaning the properties you'll have a chance to buy will be relatively new, in good condition, and likely already occupied by tenants.

Reduced Renovation Costs: Acquiring a 7-year-old, professionally managed property means you can avoid the heavy lifting and capital expenditure of a full gut renovation. These homes will be rent-ready from day one, allowing for immediate cash flow.

How Small Investors Get First Dibs on This Inventory

The law's requirement that LIIs sell to non-institutional buyers effectively gives you and other small investors a right of first refusal on a national scale. You will be competing with owner-occupant homebuyers, not other massive funds. This allows you to plan your long-term capital allocation and portfolio growth with a clear view of a future inventory source that is reserved specifically for buyers like you.

Strategic Pivot: How to Capitalize on the New Market Landscape

The 21st Century ROAD to Housing Act isn't just a change in regulations; it's a fundamental shift in the market environment. To thrive, you must adapt your strategy to leverage these new advantages.

Re-evaluating Your Acquisition Criteria and Target Markets

With LIIs removed from the equation, properties that were previously unattainable may now be within reach. It's time to:

Revisit "Turnkey" Properties: LIIs often targeted clean, rent-ready homes. With them gone, you'll face less competition for these properties, which require minimal upfront renovation and can generate cash flow immediately.

Analyze Formerly Hyper-Competitive Submarkets: Identify zip codes or neighborhoods that saw heavy institutional buying activity in the past. These areas are now "open for business" for small investors, and you may find deals that were previously impossible to secure.

Incorporate Small-Dollar Properties: With new financing support for mortgages under $100,000, consider expanding your criteria to include more affordable properties that can offer high cash-on-cash returns.

Building a Strategy to Absorb Newly Available Inventory

The "Seven-Year Clock" provides a unique opportunity for long-range planning. Start now by:

Tracking LII Development: Identify the large institutional players who are active in build-for-rent development in your target regions. Keep a record of their projects and completion dates.

Forecasting Future Capital Needs: Plan your finances so that you will have capital ready to deploy when this wave of inventory begins to hit the market in seven years. This could involve setting specific savings goals or establishing lines of credit.

Building Broker Relationships: Network with real estate agents in the areas where these communities are being built. Position yourself as a ready, willing, and able buyer for when these homes are listed for sale.

Leveraging Off-Market Deal Flow: Utilize the OfferMarket marketplace to monitor "pocket listings" and wholesale assignments that never reach the MLS. By subscribing to localized deal alerts now, you can track the lifecycle of distressed assets and new builds in your target zips. This allows you to identify which institutional-grade properties are being offloaded by wholesalers or smaller funds before they hit the broader market in seven years, giving you a "first-look" advantage over retail buyers.

The Importance of Having Pre-Approved, Reliable Financing Ready to Deploy

In this new market, speed and certainty of closing will remain your greatest competitive advantages, especially when bidding against owner-occupant buyers. While the institutional cash is gone, a strong, pre-approved financing commitment shows sellers you are a serious and capable buyer.

Get Pre-Approved: Before you even start making offers, get a full pre-approval for a DSCR loan. This demonstrates your buying power and allows you to close faster.

Work with a Tech-Enabled Lender: Lenders like OfferMarket use technology to streamline the underwriting and closing process. An instant quote and a fast, transparent process can be the deciding factor that gets your offer accepted.

Focusing on Portfolio Growth Now That the Competitive Field Has Leveled

The single biggest takeaway from this legislation is that the barriers to growth have been lowered. The excuses of "I can't compete with cash" or "Wall Street is buying everything" are no longer valid. This is the time to be aggressive. Focus on disciplined acquisition, leverage smart financing, and build your portfolio while the market dynamics are tilted in your favor.

Your Financing Partner in the New Era: OfferMarket

Navigating the new market landscape created by the 21st Century ROAD to Housing Act requires a financing partner that is as agile and forward-thinking as you are. OfferMarket's technology and loan products are perfectly aligned with the needs of small-scale investors in this new era.

Why OfferMarket's DSCR Loans Are Perfectly Aligned with the New Rules

The new law champions the small investor, and our DSCR loan program is built for precisely this audience. We focus on the property's cash flow, not your personal income, and we require closing in an LLC—the exact structure that the law protects and that savvy investors use to build their portfolios. We understand your business model because it's the only one we serve in the DSCR space.

Gaining a Competitive Advantage with Speed and Certainty of Closing

While you may no longer be competing with institutional cash, you are still competing. Your offer needs to stand out. We provide the tools to make that happen:

Instant Quotes: Our platform allows you to get a real-time, accurate loan quote in seconds. You can analyze a deal and understand your financing options before you even make an offer.

*Fast Closings:* Our streamlined, tech-driven process eliminates the delays common with traditional lenders. We can move from application to closing in a fraction of the time, giving your offer the power of speed.

Certainty of Execution: When we issue a pre-approval, it's backed by a robust underwriting process. Sellers and their agents can be confident in your ability to close, making your offer more attractive.

Empowering You to Act Decisively on New Opportunities

The 2026 Housing Act will unlock opportunities that were previously inaccessible. Whether it's a turnkey rental in a newly competitive submarket or a property from the future "Seven-Year Clock" pipeline, you need to be ready to act decisively. OfferMarket provides the financial backing and confidence you need to seize these opportunities the moment they arise. We are not just a lender; we are your strategic capital partner, dedicated to helping you grow your portfolio in this new, more favorable market.

Finance Your Next Deal with Confidence

Do not let legislative headlines create fear or hesitation. The noise and misinformation surrounding the 21st Century ROAD to Housing Act can be distracting, but the reality is clear: this is a pro-growth bill for investors like you.

The 2026 Housing Act is your signal to grow. It has cleared your biggest competitors from the field, protected your financing tools, and created a future pipeline of inventory. The market is yours for the taking. The time for waiting is over. The time for strategic, aggressive acquisition is now.

See how easily and quickly you can finance your next acquisition in this new environment. Don't let a great deal pass you by. Get the financing you need to build your portfolio with a partner who understands your business.

OfferMarket Loans

Check your rate

60 seconds · no credit pull