*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The 11 Best Investment Property Lenders of 2026

We've analyzed the top lenders in the space, focusing on their loan products, operational efficiency, and ideal customer profile. Whether you're a seasoned pro or just starting, this list will help you find the right capital partner.

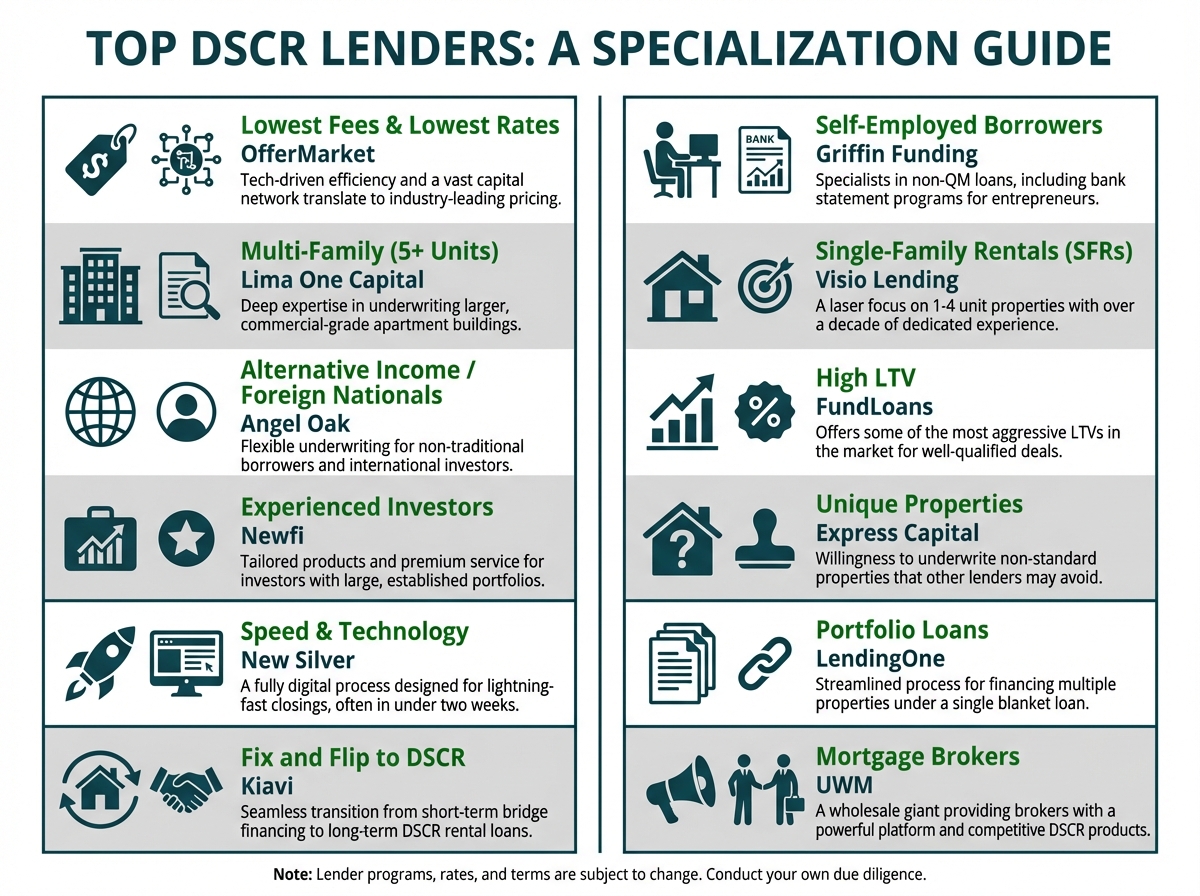

OfferMarket

- Best For: Tech-enabled DSCR and bridge loans for BRRRR investors.

- Specialization: OfferMarket stands out with its streamlined digital platform that provides investors with instant quotes and term sheets. This focus on technology allows for a faster, more transparent process from application to closing. They are built for investors looking to scale their portfolios efficiently.

- Loan Products: Their core offerings are designed to cover the full real estate investment lifecycle. This includes DSCR Rental Loans for long-term holds, Fix and Flip Bridge Loans for acquisition and rehab, and Portfolio Loans for consolidating multiple properties under a single financing vehicle.

- Key Strengths: A major advantage is their in-house underwriting and processing, which significantly speeds up closing times. They offer high leverage, often financing a large portion of both the purchase and renovation costs. Critically for savvy investors, OfferMarket lends to LLCs and does not report to personal credit bureaus, which protects the borrower's personal debt-to-income ratio (DTI) for future financing.

New Silver

- Best For: Fast, flexible financing for fix and flip and rental properties.

- Specialization: New Silver is a technology-forward lender that prioritizes speed and accessibility. Their platform includes proprietary tools like the FlipScout app, which helps investors analyze potential deals on the fly, a valuable asset in competitive markets.

- Loan Products: Their product suite is focused on short-term and transitional financing: Fix and Flip loans for rehab projects, Fix to Rent loans for investors who plan to rehab and then hold, and standard Rental Loans for stabilized properties.

- Key Strengths: New Silver is known for its quick approval process, often providing funding in a matter of days. A standout feature is their app-based construction draw management, which simplifies a historically cumbersome process. They are also more accommodating to investors with less experience, making them a good entry point for newer flippers.

Lima One Capital

- Best For: Experienced investors seeking a reliable partner for various property types.

- Specialization: Lima One has built a reputation as a national powerhouse with a broad range of products for both residential (1-4 units) and multifamily properties. They place a strong emphasis on customer service and building long-term relationships with their clients.

- Loan Products: They offer a comprehensive menu, including their Rental30 and Rental30 Premier loans for long-term financing, FixNFlip loans, New Construction financing for ground-up projects, and specialized Multifamily bridge loans for value-add opportunities.

- Key Strengths: As a nationwide lender, they have a deep understanding of markets across the country. A key differentiator is that Lima One Capital services its own loans, meaning borrowers deal with the same company throughout the life of the loan. Their value-add bridge financing is particularly attractive for multifamily investors looking to acquire and renovate larger properties.

Kiavi

- Best For: High-volume flippers needing a fast, repeatable technology platform.

- Specialization: Formerly known as LendingHome, Kiavi is heavily focused on using technology to provide speed and certainty of execution, primarily for fix-and-flip investors. Their entire process is designed to be fast, predictable, and scalable.

- Loan Products: Their main offerings are Fix and Flip Bridge Loans and DSCR Rental Loans. They have fine-tuned their bridge product to be one of the fastest and most efficient in the industry.

- Key Strengths: Kiavi's primary strength is its speed. They can often fund deals in less than 10 days. Their digital portal provides borrowers with complete transparency throughout the loan process, from application to draws to payoff. They offer high leverage on both the purchase price and the rehab budget, which is crucial for flippers looking to maximize their capital.

RCN Capital

- Best For: A wide range of borrowers, including foreign nationals and those with complex deals.

- Specialization: RCN Capital is a national, direct private lender known for its flexible underwriting and extremely broad product menu. They are often the go-to lender for non-standard scenarios that don't fit into a neat box.

- Loan Products: Their product list is extensive: Fix & Flip, long-term DSCR rental loans, Ground-Up Construction, and Portfolio Loans. They have specific programs tailored for short-term rentals (STRs).

- Key Strengths: A major advantage of RCN Capital is that many of their loan products require no income or employment verification, as the lending decision is based on the property's merits. They are one of the few lenders that comfortably finance short-term rentals and have robust options for both small and large multifamily properties, making them highly versatile.

WeLend

- Best For: Investors looking for competitive long-term DSCR loans.

- Specialization: WeLend has carved out a niche by focusing primarily on providing competitive 30-year fixed-rate DSCR loans. Their process is optimized for experienced investors who want a straightforward, no-frills experience for their buy-and-hold rental properties.

- Loan Products: While their main product is the 30-year DSCR Loan for 1-4 unit properties, they also offer Bridge Loans for investors who need short-term financing before stabilizing a property for a long-term loan.

- Key Strengths: Their primary competitive edge is often their interest rates on long-term rental loans. By specializing, they can streamline their process and pass on efficiency savings to the borrower. This makes them an excellent choice for investors whose main priority is locking in the best possible rate for a long-term hold.

Easy Street Capital

- Best For: Creative financing solutions for modern rental strategies.

- Specialization: Easy Street Capital has established itself as a leader in financing newer, more creative rental strategies. They were one of the early movers in using data to underwrite short-term rentals and have deep expertise in portfolio lending.

- Loan Products: Their flagship products are their DSCR Loans, which include a specialized program for short-term rentals (STRs). They also offer Portfolio Loans and Bridge Loans.

- Key Strengths: Their use of data from services like AirDNA to underwrite the potential income of an STR is a significant advantage for Airbnb and VRBO investors. They offer flexible portfolio blanket loans that allow investors to cross-collateralize multiple properties. Furthermore, they are comfortable with complex ownership structures, such as layered LLCs, which is a key need for sophisticated investors.

BridgeWell Capital

- Best For: Hard money financing for investors in specific Southeastern and Midwestern states.

- Specialization: BridgeWell Capital is a classic private hard money lender. Their focus is on asset-based underwriting, meaning the viability of the deal and the property's after-repair value (ARV) are more important than the borrower's credit history.

- Loan Products: Their offerings are straightforward and tailored for rehab projects: Hard Money Fix and Flip loans and general Private Money Loans for various real estate transactions needing fast, short-term capital.

- Key Strengths: As a hard money lender, their main strength is speed, often closing in a week or less. The approval is based almost entirely on the property's value, making them an excellent option for investors with a great deal but a less-than-perfect credit profile. Their loans are typically interest-only, which keeps monthly payments low during the renovation phase.

Fund That Flip

- Best For: Residential flippers and developers seeking debt and equity partnerships.

- Specialization: Fund That Flip operates a unique fintech model. They are a direct lender, but they also have a crowdfunding platform where accredited investors can invest in the loans, providing a vast and flexible pool of capital.

- Loan Products: They specialize in short-term financing for residential developers, including Fix and Flip Bridge Loans, New Construction loans, and more recently, DSCR Loans for stabilized rentals.

- Key Strengths: Their model allows them to offer very high Loan-to-Value (LTV) and Loan-to-Cost (LTC) options, sometimes financing up to 100% of the renovation costs. They are known for a fast and efficient draw process, which is critical for keeping construction projects on schedule. Fund That Flip also provides significant community and educational resources for their borrowers.

Rehab Financial Group

- Best For: Investors with lower credit scores or limited experience.

- Specialization: Rehab Financial Group (RFG) has a unique and compelling selling proposition: they offer 100% financing on both the purchase and rehab costs for fix-and-flip projects. They are a true asset-based lender that focuses almost exclusively on the deal's potential.

- Loan Products: Their products are designed for value-add projects: Fix and Flip, Fix to Hold (for BRRRR investors), and New Construction loans.

- Key Strengths: RFG's standout feature is their 100% financing option, which is a game-changer for investors who are capital-constrained. They have no FICO score minimums, removing a major barrier for many new or credit-challenged investors. Their underwriting focuses on the deal's profitability, making them one of the most accessible hard money lenders available.

Private Lender Link

- Best For: Sourcing multiple quotes from a wide variety of niche lenders.

- Specialization: It's important to note that Private Lender Link is not a direct lender. It is an online marketplace or directory that connects real estate investors with a vast network of hundreds of private and hard money lenders across the country.

- Loan Products: Through its network, an investor can find financing for virtually any type of real estate deal, from standard flips and rentals to more esoteric assets like land development or commercial properties.

- Key Strengths: The platform’s primary value is its breadth. If you have a unique property (e.g., a mixed-use building, a dome home) or a difficult scenario (e.g., bankruptcy, foreign national status), you can submit your loan request and get matched with niche lenders who specialize in that exact situation. The site also features user reviews, helping you vet potential lending partners.

Lender Comparison: Finding the Right Fit for Your Strategy

Choosing a lender isn't about finding the "best" one overall, but the best one for your specific deal. Here’s a quick guide to help you narrow down your options based on your investment strategy.

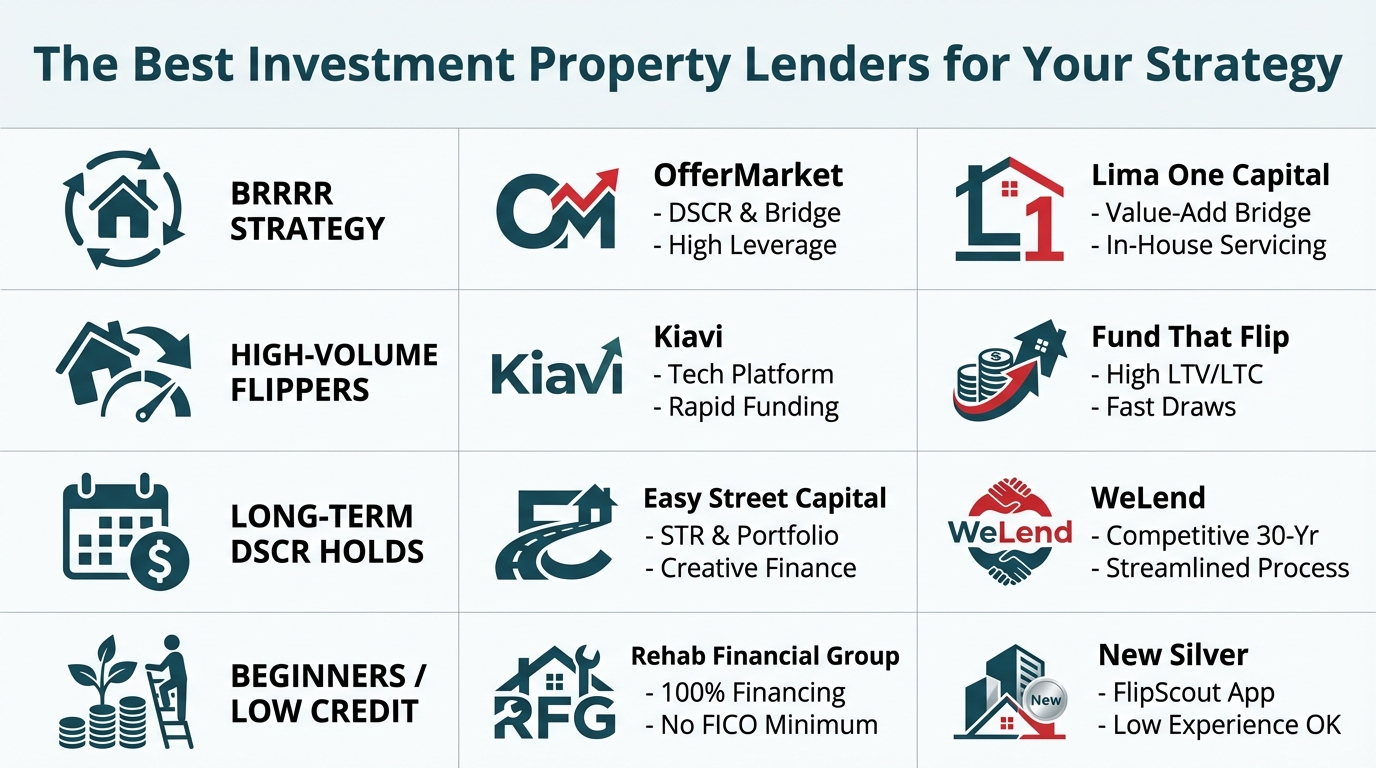

- Best for BRRRR Strategy: OfferMarket is a top choice due to its seamless integration of bridge loans for the "Buy" and "Rehab" phases and high-leverage DSCR loans for the "Refinance" phase. Lima One Capital is also excellent, offering robust value-add bridge financing and reliable long-term rental loan products.

- Best for High-Volume Flippers: Kiavi's technology platform is built for speed and repeatability, making it ideal for investors flipping dozens of homes a year. Fund That Flip is another strong contender, offering high leverage and a rapid draw process to keep multiple projects moving simultaneously.

- Best for Long-Term DSCR Holds: Easy Street Capital excels here, especially with their expertise in underwriting both long-term and short-term rentals. WeLend is a great option for investors focused purely on securing the most competitive 30-year fixed rates for traditional rental properties.

- Best for Short-Term Rentals (STRs): Easy Street Capital is a clear leader, using sophisticated data analytics for underwriting STR income. RCN Capital also has a dedicated and flexible program for STRs, accommodating various property types and borrower profiles.

- Best for Beginners or Low Credit: Rehab Financial Group is arguably the most accessible, with its 100% financing options and no FICO minimums. New Silver is also a great starting point, offering a user-friendly platform and being open to working with investors who have limited experience.

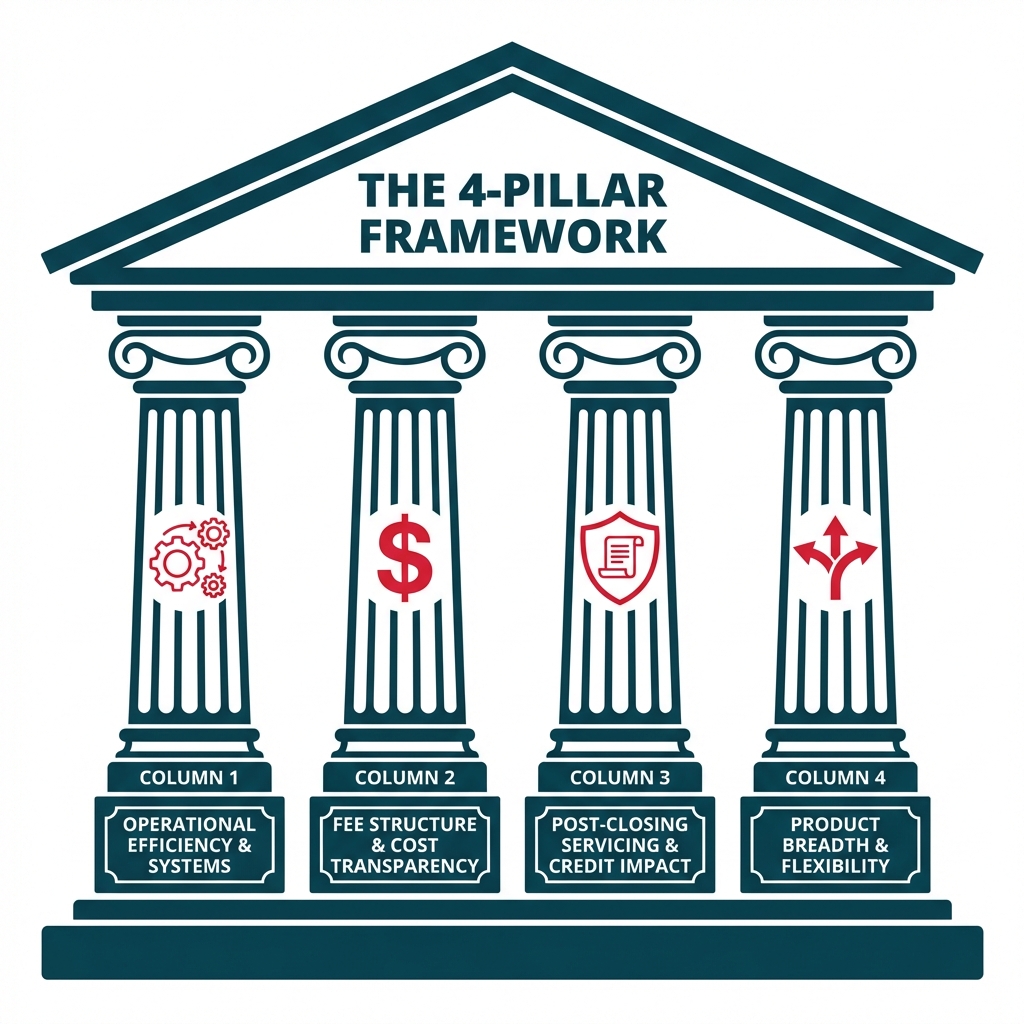

The 4-Pillar Framework for Vetting Any Investment Property Lender

Beyond any "best of" list, you need a durable framework for evaluating any potential capital partner. A cheap rate from an inefficient lender can cost you the deal, while a flexible lender with high fees might be perfect for a complex project. Use these four pillars to analyze any lender you consider.

Pillar 1: Operational Efficiency and Systems

In real estate, speed is a weapon. A seller accepting your offer often depends on your ability to close quickly. A lender's operational efficiency directly impacts your reputation and your ability to win deals.

- What to look for: A fully digital application process, instant or near-instant term sheets, and a clear online portal for document submission and tracking loan progress.

- Questions to ask: "What is your average time from application to close?" "Is underwriting done in-house or outsourced?" "How do you handle construction draws, and what is the typical turnaround time?"

- Red Flags: Lenders who require you to email sensitive documents, have no clear point of contact, or give vague, non-committal answers about their timeline.

Pillar 2: Fee Structure and Cost Transparency

The interest rate is only one part of the cost of capital. Lenders make money through a variety of fees, and a lack of transparency here can lead to costly surprises at the closing table.

- What to look for: A term sheet or loan estimate that clearly itemizes all lender fees. This includes origination points, processing fees, underwriting fees, legal fees, and any other charges.

- Questions to ask: "Can you provide me with a complete fee schedule?" "Are there any 'junk fees' I should be aware of?" "Is the origination fee calculated based on the loan amount or the total project cost?"

- Red Flags: Lenders who are hesitant to provide a detailed fee breakdown or who use vague terms like "administrative fees" without specifics. Be wary of a "bait and switch" where a low advertised rate is offset by exorbitant fees.

Pillar 3: Post-Closing Servicing and Credit Impact

Your relationship with the lender doesn't end at closing. Who services the loan and how that loan is reported are critically important for portfolio investors.

- What to look for: Lenders who service their own loans in-house often provide a more seamless experience. For investors looking to scale, the most important feature is a lender who makes business-purpose loans to an LLC and does not report the debt to the owner's personal credit report.

- Questions to ask: "Do you service your own loans, or will my loan be sold?" "Does this loan report to my personal credit bureaus (TransUnion, Equifax, Experian)?"

- Red Flags: A lender who can't give you a straight answer about who will service the loan. Any lender who reports a business-purpose loan to your personal credit is effectively limiting your ability to grow, as it will negatively impact your personal DTI ratio.

Pillar 4: Product Breadth and Edge-Case Flexibility

Your first deal with a lender might be a simple fix-and-flip. But what about your next one? A lender with a wide range of products can grow with you, saving you the time and effort of finding a new capital partner for every deal.

- What to look for: A lender that offers a full suite of products, such as bridge loans, DSCR rental loans, new construction, and portfolio loans. This creates a one-stop shop for your financing needs.

- Questions to ask: "If I use your bridge loan for a BRRRR, what does the refinance process into your DSCR loan look like?" "Do you have programs for short-term rentals or small multifamily properties?" "What's the most unusual deal you've funded?"

- Red Flags: Lenders who are rigid and only have one "box" that deals must fit into. The best lenders have the experience and flexibility to handle minor complexities without derailing the entire transaction.

How to Decode a Term Sheet: A 4-Point Inspection

Once a lender approves your loan in principle, they will issue a term sheet (also called a Letter of Intent or LOI). This is a non-binding document that outlines the proposed terms of the loan. Scrutinizing this document is essential. Here are the four key areas to inspect.

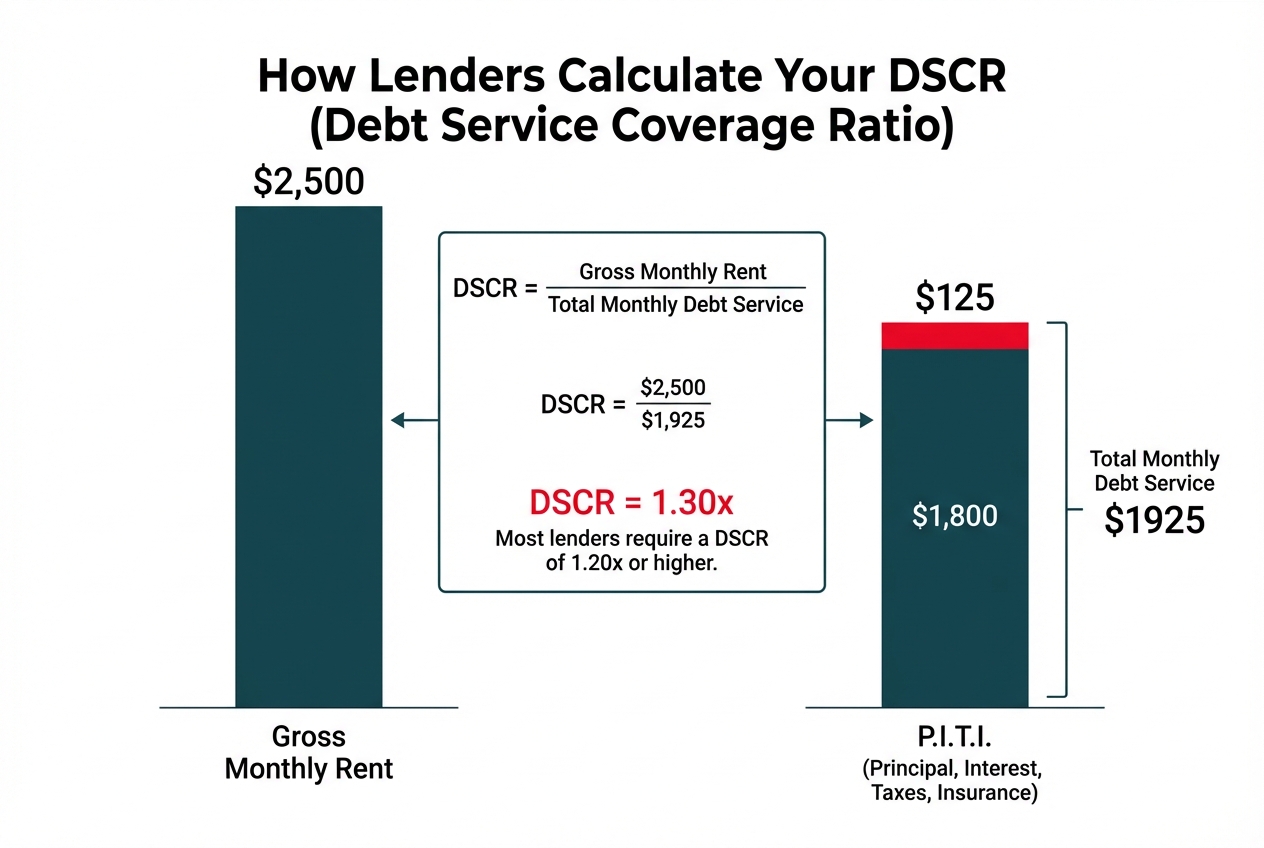

Point 1: The Income Calculation and DSCR Math

For any rental property loan, the most important metric is the Debt Service Coverage Ratio (DSCR). This ratio measures the property's ability to cover its debt obligations from its own cash flow. The formula is:

DSCR = Gross Rental Income / Total Debt Service (PITI)

- What to check: How is the lender calculating the "income" figure? Are they using the current in-place rent, or are they using a market rent figure from an appraiser's report? A lower income figure will result in a lower DSCR, which could mean you qualify for a smaller loan amount.

- Example:

- Gross Monthly Rent: $3,000

- Monthly PITI (Principal, Interest, Taxes, Insurance): $2,400

- DSCR = $3,000 / $2,400 = 1.25x

- Most lenders require a minimum DSCR of 1.20x to 1.25x. If the lender's underwriting uses a lower market rent of $2,800, your DSCR drops to 1.16x, and you may no longer qualify for the loan.

Point 2: Leverage Caps and Seasoning Requirements

Leverage refers to the amount of the deal the lender is willing to finance, expressed as Loan-to-Value (LTV) or Loan-to-Cost (LTC). Seasoning refers to how long you must own a property before you can refinance it based on its new, appraised value.

- What to check: For a purchase, what is the maximum LTV? For a refinance or BRRRR, what is the LTV, and what are the seasoning requirements? Some lenders require you to own the property for 6-12 months before allowing a cash-out refinance based on the after-repair value (ARV). Lenders with little to no seasoning requirements are highly valuable for the BRRRR strategy.

- Example: You buy a property for $100k and put $50k into rehab. Its ARV is now $220k. A lender with a 6-month seasoning requirement will make you wait to pull your cash out. A lender with no seasoning requirement and a 75% LTV cash-out refi product will give you a loan for $165k ($220k * 0.75), allowing you to pull out all of your original capital ($150k) plus an extra $15k.

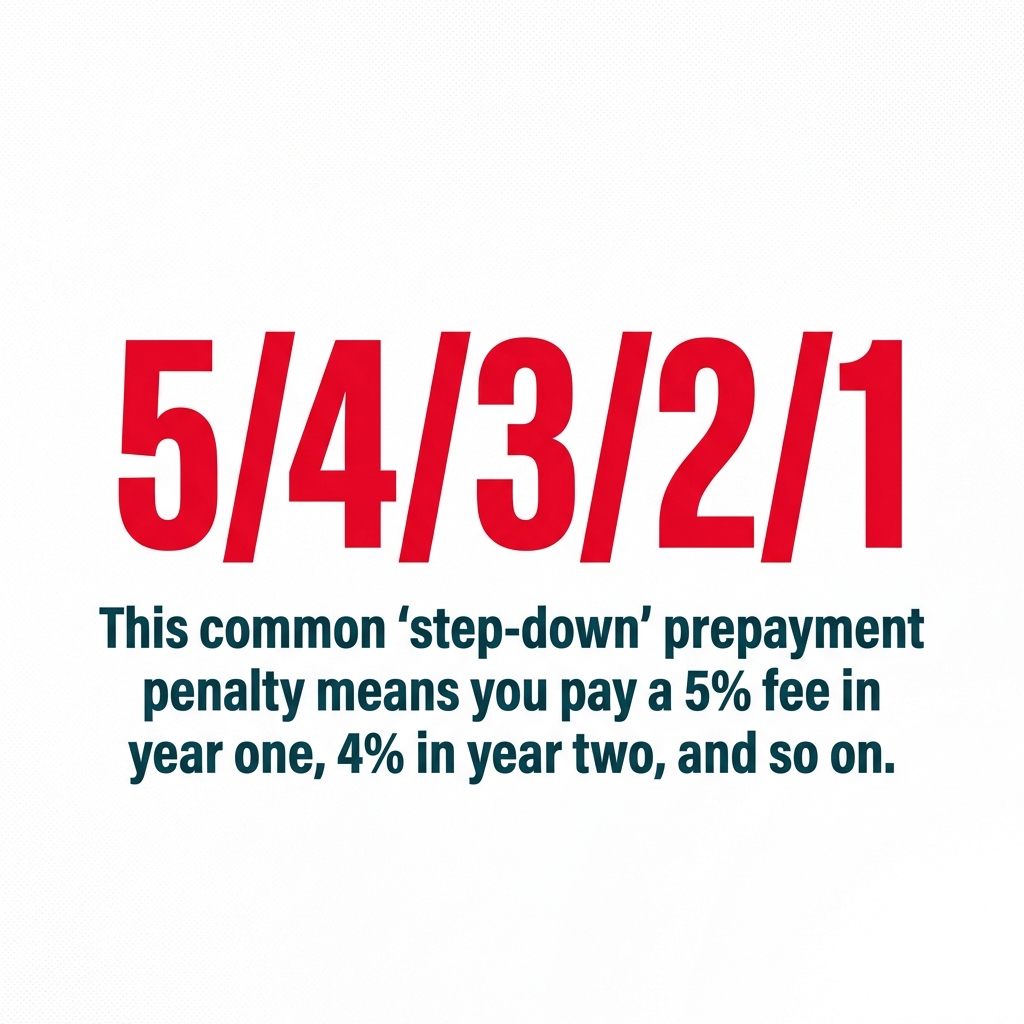

Point 3: The Prepayment Penalty Structure

Most long-term loans for investment properties (like DSCR loans) come with a prepayment penalty. This is a fee charged to the borrower for paying off the loan early. It protects the lender's expected return on investment.

- What to check: What is the structure and duration of the penalty? A common structure is a "step-down" penalty, such as "5/4/3/2/1." This means if you pay off the loan in the first year, you pay a penalty equal to 5% of the outstanding balance. In year two, it's 4%, and so on. After five years, there is no penalty.

- Why it matters: If you plan to sell or refinance the property within a few years, a long and expensive prepayment penalty can significantly eat into your profits. A 3-year penalty is much more flexible than a 5-year one. Some lenders offer the option to "buy down" the penalty (e.g., pay a higher interest rate for a shorter penalty period).

Point 4: Liquidity and Reserve Requirements

Lenders want to see that you have enough cash on hand to cover unexpected expenses and closing costs. These are known as liquidity or reserve requirements.

- What to check: How much liquidity does the lender require, and how is it calculated? A common requirement is 6 months of PITI payments in reserves. For a property with a $2,000 monthly PITI, you would need to show $12,000 in a bank account.

- Important questions: Can these funds be in retirement accounts (like a 401k or IRA), or do they need to be in a liquid checking/savings account? Do they require reserves for just the subject property, or for all properties in your portfolio? A lender with flexible reserve requirements can make it much easier to qualify for a loan, especially as you scale.

Why Our Platform Streamlines Your Next Investment

Understanding how to vet lenders and decode term sheets highlights the exact pain points OfferMarket was built to solve. We combine technology with expert service to provide a superior borrowing experience for real estate investors.

Operational Efficiency

Our proprietary platform allows you to enter your deal specifics and receive an instant, bindable loan term sheet in minutes, not days. This speed allows you to make aggressive offers with confidence, knowing your financing is already lined up. Our entire process, from application to closing, is managed through a seamless digital portal.

Transparent Costs

There are no surprises with OfferMarket. Your instant term sheet provides a full, transparent breakdown of your interest rate and all associated fees. We don't charge hidden junk fees, ensuring the numbers you see upfront are the numbers you get at closing.

Investor-Focused Servicing

We are a capital partner dedicated to helping you scale. We lend to your LLC, and our loans never report to your personal credit bureaus. This is a core feature of our service, designed to protect your personal DTI and preserve your ability to qualify for future loans, whether for investments or a new primary home.

Complete Product Suite

OfferMarket is your partner for the entire investment lifecycle. Use our Fix and Flip Bridge Loans to acquire and renovate a property, then seamlessly refinance into our long-term DSCR Rental Loan with no seasoning requirements. This integrated approach simplifies the BRRRR process and helps you grow your portfolio faster with a single, reliable capital partner.

Take the Next Step: Get Your Instant Quote

Ready to see how your next deal numbers work with a modern, efficient lender?

- Generate an instant term sheet: Get real-time, bindable terms for your specific rental or flip deal in under five minutes.

- Analyze your deal: Use our free DSCR Calculator to stress-test your cash flow and potential ROI.

- Explore our guidelines: Dive deep into our specific loan product pages to see detailed underwriting guidelines.

- Talk to an expert: Schedule a call with one of our experienced loan officers to discuss your portfolio, your growth strategy, and how we can help you achieve your goals.

OfferMarket Loans

Check your rate

60 seconds · no credit pull