*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

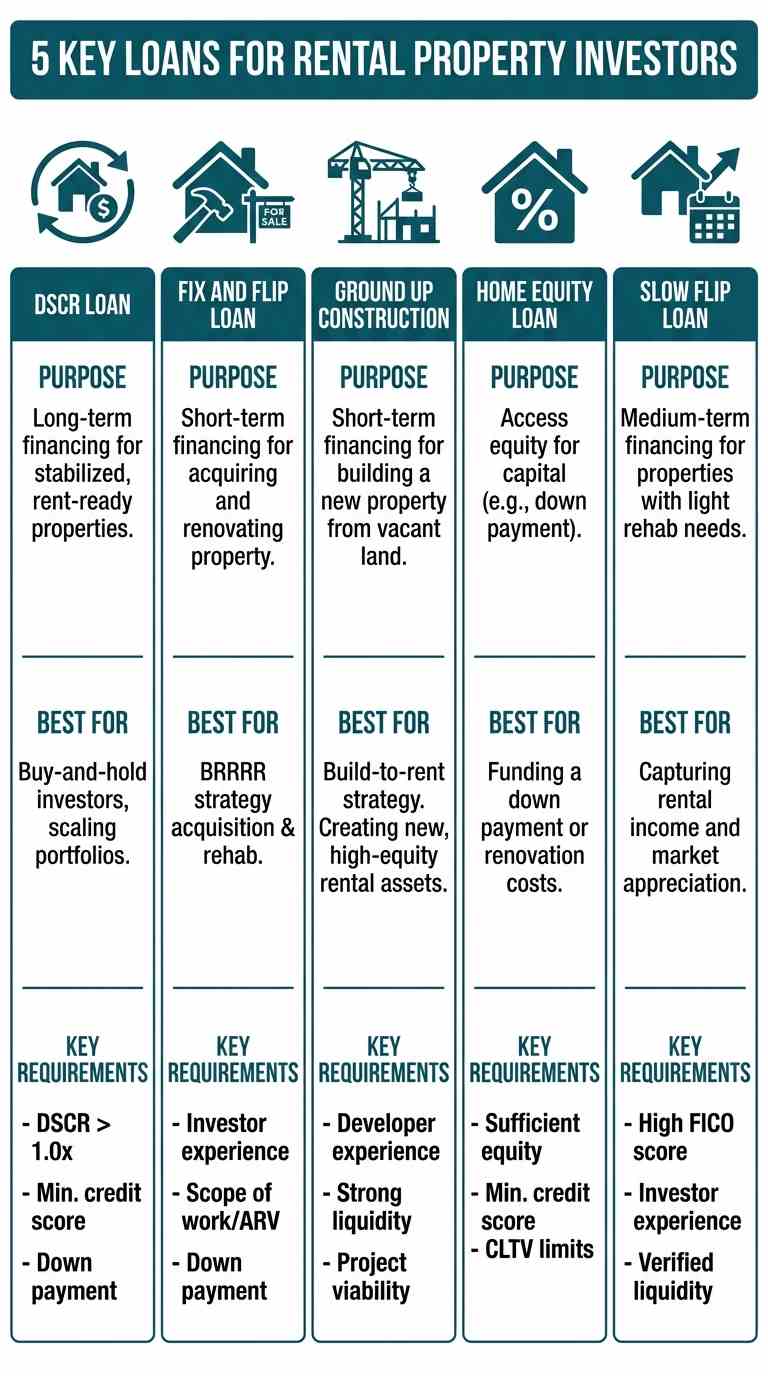

A Strategic Overview of Real Estate Investor Loans

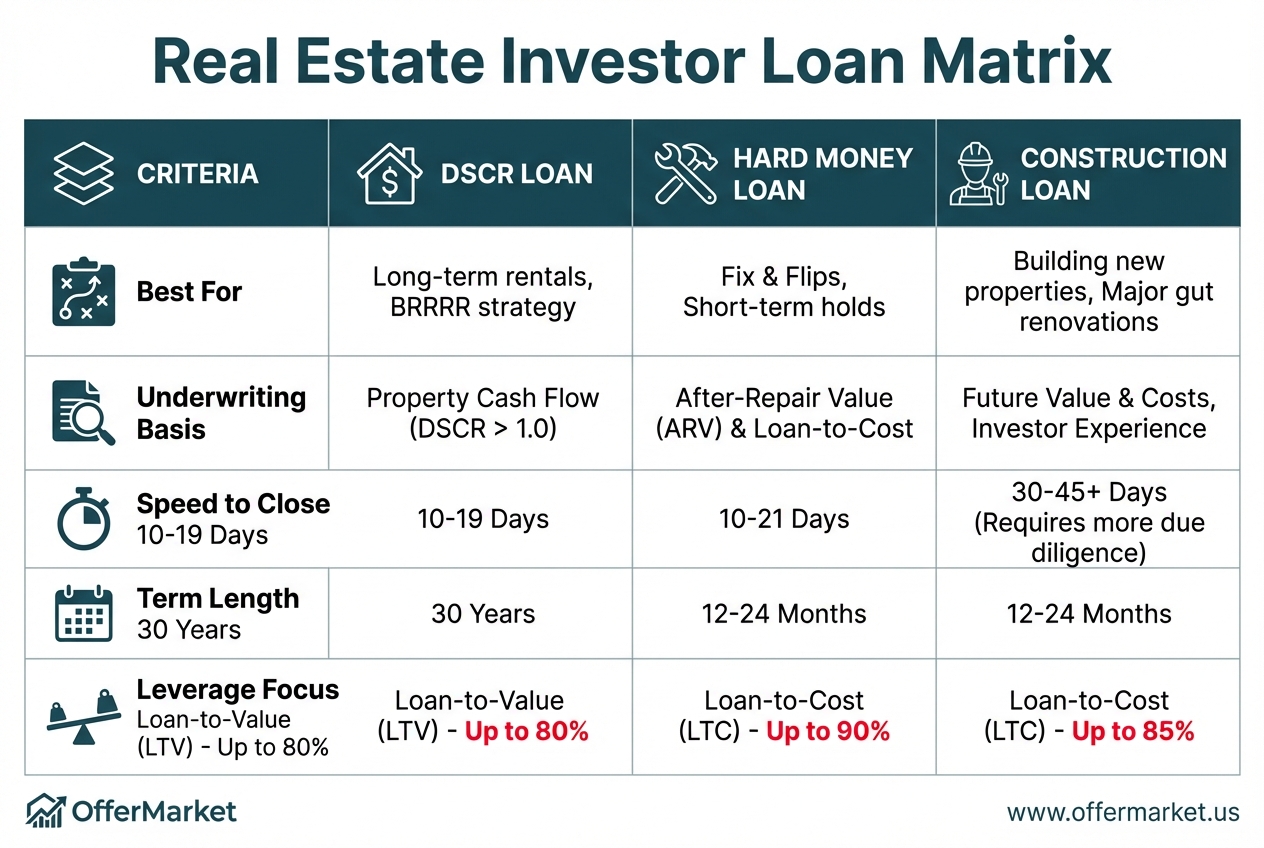

The most critical decision after finding a deal is choosing the right financing. The loan you select directly impacts your cash-to-close, monthly holding costs, and overall profitability. For real estate investors, financing is not one-size-fits-all; it's a strategic choice tailored to the specific property and business plan. The primary loan types fall into two main categories: asset-based loans, which focus on the property's potential, and conventional loans, which focus on your personal financial history.

Asset-based loans, like DSCR loans and Hard Money loans, are the workhorses of professional real estate investing. Lenders underwrite these loans based on the property's metrics—its income-generating potential or its after-repair value (ARV)—rather than your personal debt-to-income ratio (DTI). This allows investors to scale their portfolios without being limited by their W-2 income. Conversely, conventional investment property loans rely heavily on personal income verification, tax returns, and DTI calculations, making them a viable but less scalable option.

Buy and Hold/BRRRR: The goal is long-term rental income. A DSCR loan is the perfect exit financing, allowing you to refinance out of a short-term loan and hold the property based on its cash flow.

Fix and Flip: This is a short-term, value-add play. A Hard Money loan provides the speed and leverage on purchase and renovation costs (Loan-to-Cost) needed to acquire and improve a property quickly.

New Construction: For building from the ground up, a Ground-Up Construction loan is necessary. It funds the project in stages (draws) as work is completed.

Turnkey Rental Purchase: For a rent-ready property, a DSCR loan is often the best fit from day one, offering a streamlined closing based on the existing or projected rental income.

Your decision will ultimately hinge on four key factors: speed of closing, leverage (the amount the lender will finance), cost (interest rates and fees), and the loan term. Hard money excels in speed and leverage for short-term projects, while DSCR loans offer stable, long-term financing for cash-flowing assets.

DSCR Loans: Financing for the Buy-and-Hold Investor

DSCR (Debt Service Coverage Ratio) loans are the cornerstone of financing for long-term rental property investors. Their power lies in a simple, revolutionary concept: the property's income must be sufficient to cover its debt obligations. Lenders qualify the property, not the borrower's personal income. This approach completely removes personal DTI from the equation, allowing investors to acquire multiple properties without hitting a ceiling imposed by their W-2 salary.

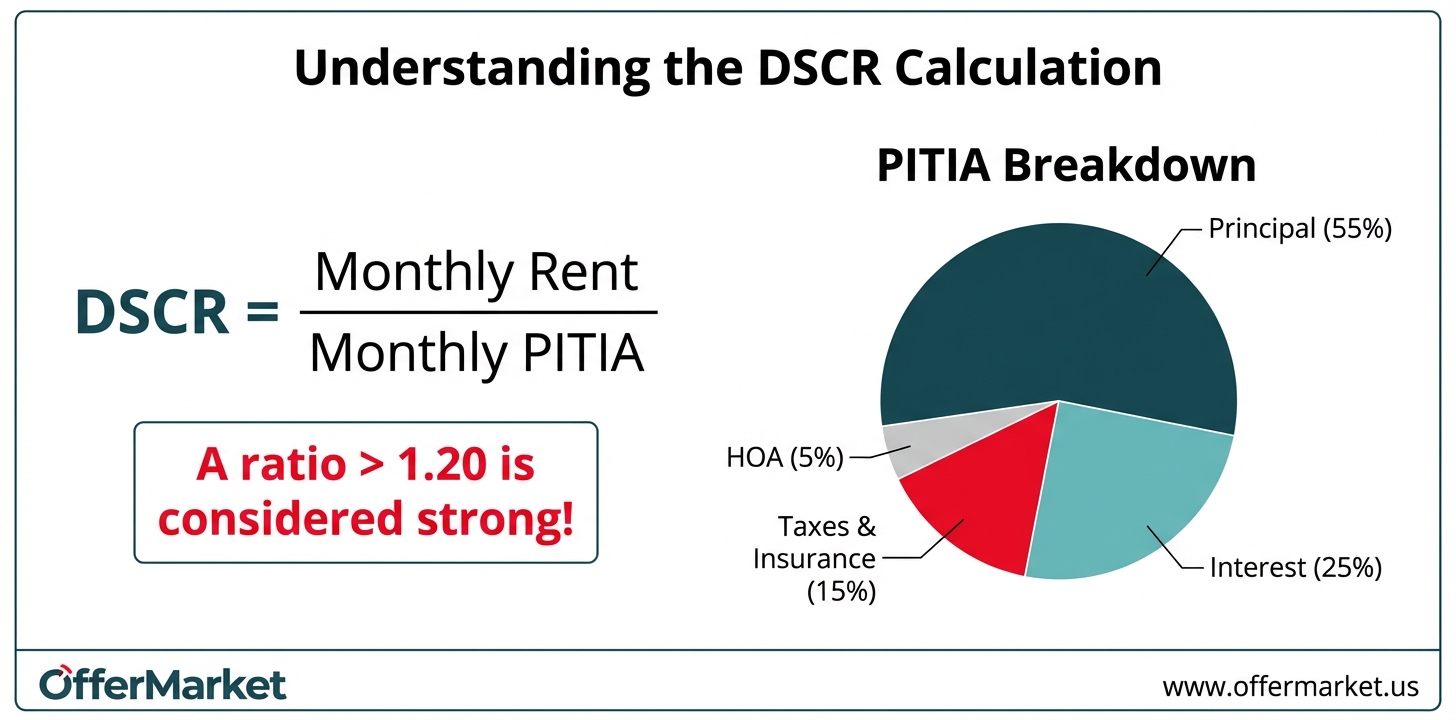

The Core Mechanic: Underwriting Based on Property Cash Flow

The entire underwriting process for a DSCR loan revolves around a single ratio. This ratio compares the property's gross rental income to its total housing expense, known as PITIA.

PITIA = Principal + Interest + Taxes + Insurance + Association Dues

A lender wants to see that the rental income is greater than the total expense. The resulting ratio determines eligibility and can influence the interest rate you receive. Most lenders require a DSCR of at least 1.20, meaning the property's income is 120% of its expenses. Some programs allow for ratios down to 1.0, and in some cases, even slightly below for well-qualified borrowers with significant compensating factors like high credit and liquidity.

Calculating Your DSCR

The formula is straightforward:

DSCR = Monthly Rental Income / Monthly PITIA

Let's walk through a practical example:

- You are buying a single-family rental property.

- Gross Monthly Rental Income: $3,000

- Proposed Monthly Mortgage (Principal & Interest): $1,800

- Monthly Property Taxes: $300

- Monthly Insurance: $100

- Monthly HOA Dues: $50

First, calculate the total monthly PITIA:

$1,800 (P&I) + $300 (T) + $100 (I) + $50 (A) = $2,250

Next, calculate the DSCR:

$3,000 / $2,250 = 1.33 DSCR

A DSCR of 1.33 is considered strong and would likely qualify for the best terms available. You can model different scenarios for your own deals using a DSCR Calculator to instantly see your DSCR.

Lender Requirements

While personal income isn't used for qualification, lenders still have minimum requirements for the borrower to ensure they are a reliable partner. These typically include:

Minimum Credit Score: Most DSCR lenders require a minimum FICO score of 680. Borrowers with scores above 720 will generally receive the most favorable interest rates and terms.

Reserve Requirements: Lenders need to see that you have enough liquid assets to cover expenses during potential vacancies. The standard requirement is 6 months of PITIA in reserves, held in a verifiable bank or brokerage account. For investors with larger portfolios, this requirement may increase.

Experience: While many programs are available for first-time investors, having a track record of owning and managing rental properties can unlock better terms, including higher leverage and lower rates.

DSCR for Short-Term Rentals

The DSCR model has also been adapted for the booming short-term rental (STR) market, such as properties listed on Airbnb and Vrbo. Since STRs don't have a long-term lease, lenders cannot use a standard rental agreement for underwriting. Instead, they rely on third-party data to project income.

Lenders use specialized appraisal reports that include data from services like AirDNA, which analyzes the performance of comparable short-term rentals in the immediate area. The report will provide a projected average daily rate (ADR), occupancy rate, and resulting gross monthly income. This projected income is then used in the DSCR calculation, allowing investors to finance vacation rentals and other STRs based on their high-income potential.

DSCR Loan Leverage and Common Pitfalls

Understanding the leverage and rules associated with DSCR loans is crucial for effectively executing investment strategies like BRRRR. While these loans are flexible, they have specific guidelines that can impact your cash-out potential and timeline.

Maximizing Leverage: LTV Limits

Leverage is expressed as Loan-to-Value (LTV), the percentage of the property's appraised value that the lender will finance.

Purchase: For buying a new rental property, investors can typically secure up to 80% LTV. This means you would need a 20% down payment plus closing costs.

Rate-Term Refinance: If you are refinancing an existing loan to get a better rate or term without taking cash out, you can also typically get up to 80% LTV.

Cash-Out Refinance: This is the key to the "Refinance" step in the BRRRR method. After renovating a property and increasing its value, you can refinance to pull your capital back out. For cash-out refinances, lenders generally cap the LTV at 75%.

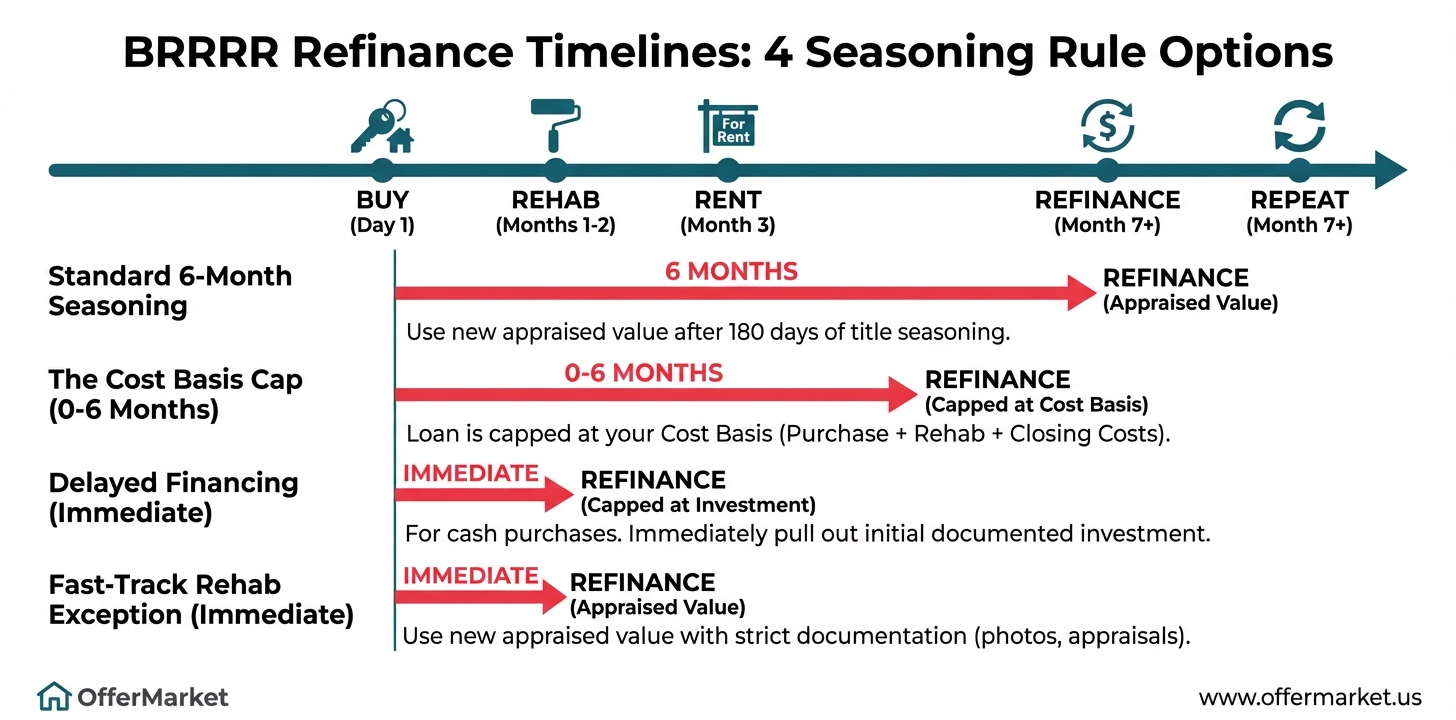

The 6-Month Seasoning Rule

One of the most important concepts in the BRRRR strategy is "seasoning." Most lenders impose a seasoning period, typically six months, before they will allow you to do a cash-out refinance based on the new, after-repair value of the property.

This means you must own the property for at least six months before you can extract your equity. This rule is in place to prevent risky, speculative flipping. It ensures that the value increase is stable and not just a temporary market fluctuation. Planning for this six-month hold is a critical part of your financial projections for any BRRRR deal. Some lenders may offer exceptions, but this is the industry standard.

No Seasoning DSCR Refinance

OfferMarket has a no seasoning product for refinance. The Loan to Value (amount they can loan) will depend on the costs they got for the property (purchase price + rehab if any). For example:

As is value: 300k Purchase price: 200k Rehab: 20k

The LTV will be depending on the 220k not the as is value. If you would like to get the LTV from the as is value, there is a condition for us to base it on the 300k. But still max loan amount is 220k.

Navigating Vacancies

Lenders prefer to finance stabilized, income-producing assets. If you are purchasing a property that is currently vacant, or refinancing a property between tenants, it can affect your loan terms. When a property is not leased at the time of closing, many lenders will reduce the maximum LTV, often from 80% down to 75% for a purchase. This is to mitigate the risk of the property not being able to generate income immediately to cover the new mortgage payment. To secure the highest leverage, it's best to have a signed lease agreement in place before you close on your DSCR loan.

Ideal Use Cases

The structure of DSCR loans makes them perfectly suited for specific investment strategies:

The BRRRR Strategy: This is the quintessential use case. You buy a distressed property with a short-term hard money loan, renovate it, rent it out to a qualified tenant, and once it's seasoned for six months, you execute a cash-out refinance with a DSCR loan to pull out your original capital and repeat the process.

Portfolio Expansion: For investors looking to buy multiple properties, DSCR loans provide a scalable financing solution that isn't limited by personal DTI. You can acquire properties as long as they cash flow.

Financing Turnkey Rentals: If you are buying a property that is already renovated and has a tenant in place, a DSCR loan is the most efficient way to finance the purchase from the start.

Fix & Flip Loans: The Engine of Value-Add Investing

Fix and flip loans, commonly known as hard money loans or bridge loans, are the preferred financing tool for investors who specialize in acquiring, renovating, and selling properties for a profit. Unlike long-term mortgages, these are short-term, asset-based loans designed for speed and high leverage on the total cost of a project, not just the purchase price.

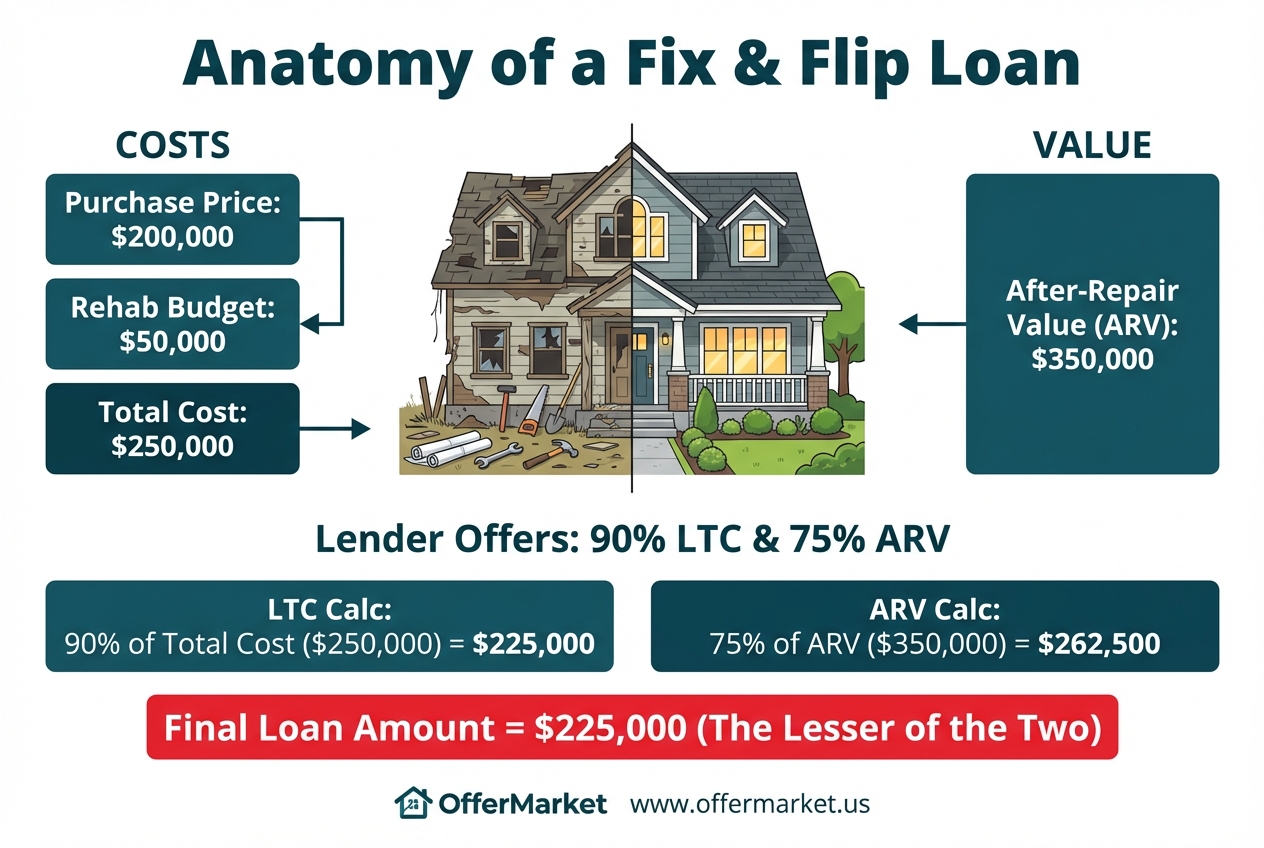

Understanding the Leverage Model: LTC and ARLTV

The power of a fix and flip loan comes from how it's structured. Lenders base the loan amount on two key metrics:

Loan to Cost (LTC): This is the percentage of the total project cost (purchase price + renovation budget) that the lender will finance.

After Repair Loan to Value (ARLTV): This is the percentage of the property's future appraised value after all renovations are complete.

The lender will typically fund the lesser of these two calculations. For example:

- Purchase Price: $200,000

- Renovation Budget: $50,000

- Total Project Cost: $250,000

- After Repair Value (ARV): $350,000

Let's say the lender offers terms of 90% LTC and 75% ARLTV.

- LTC Calculation: 90% of $250,000 = $225,000

- ARLTV Calculation: 75% of $350,000 = $262,500

In this scenario, the total loan amount would be capped at $225,000, as it is the lesser of the two figures. This structure allows investors to finance a significant portion of the renovation, minimizing their out-of-pocket expenses.

How Construction Draws Work

The renovation portion of the loan is not given to the borrower as a lump sum at closing. Instead, it is held in an escrow account by the lender. The funds are disbursed in stages, known as "draws," as work is completed. This protects the lender by ensuring their capital is being used to increase the property's value. The process typically works as follows:

- Initial Funding: At closing, the lender funds the purchase price portion of the loan.

- Work Completion: The investor uses their own capital to complete the first phase of the renovation as outlined in the agreed-upon Scope of Work (SOW).

- Draw Request & Inspection: The investor submits a draw request to the lender. The lender then sends an inspector to the property to verify that the work has been completed to a satisfactory standard.

- Reimbursement: Once the inspection is approved, the lender releases funds from the escrow account to reimburse the investor for the work completed.

This cycle repeats until the renovation is finished and all construction funds have been disbursed.

The Experience Tiers

Hard money lenders value experience above all else. A proven track record of successful flips reduces the lender's risk, and they reward this with better terms. Borrowers are often categorized into experience tiers:

- Tier 1 (Beginner): 0-2 flips in the last 24 months. May receive terms like 85% LTC and 70% ARLTV with slightly higher interest rates.

- Tier 2 (Intermediate): 3-9 flips. Terms might improve to 90% LTC and 75% ARLTV.

- Tier 3 (Expert): 10+ flips. These borrowers can command the best terms, potentially including 90% LTC / 75% ARLTV, lower interest rates, and a more streamlined draw process.

Typical Loan Structure

Fix and flip loans are built for a specific purpose and their structure reflects that:

- Term: Short-term, typically 12 to 24 months.

- Interest: Interest-only payments are standard. This keeps holding costs low during the renovation phase when the property is not generating income. The principal is due as a balloon payment when the property is sold or refinanced.

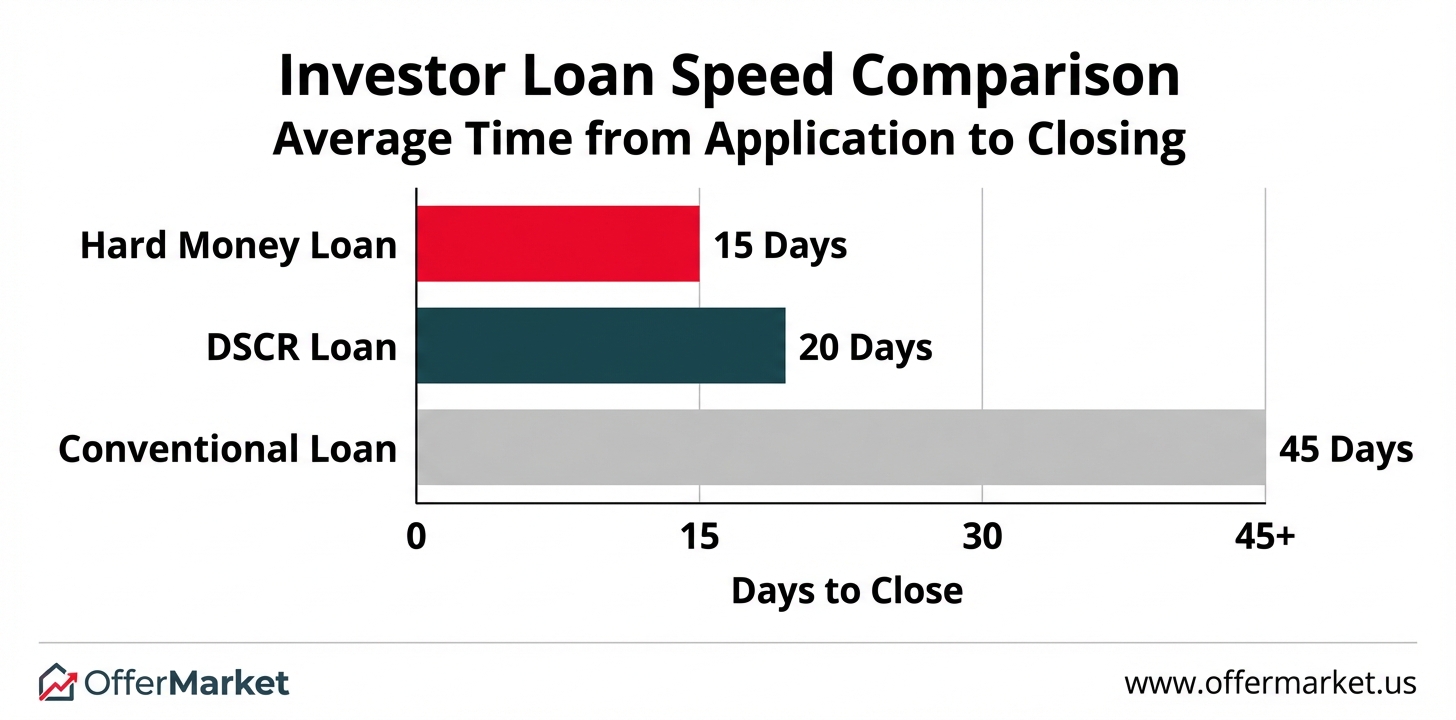

- Speed: Speed is a key advantage. Hard money loans can often close in 10-21 days, allowing investors to compete with cash buyers for in-demand properties.

Fix & Flip Pitfalls and Financial Drains

While fix and flip loans are powerful, they come with strict rules and potential pitfalls that can quickly erode profits or even kill a deal. Understanding these risks is just as important as understanding the leverage.

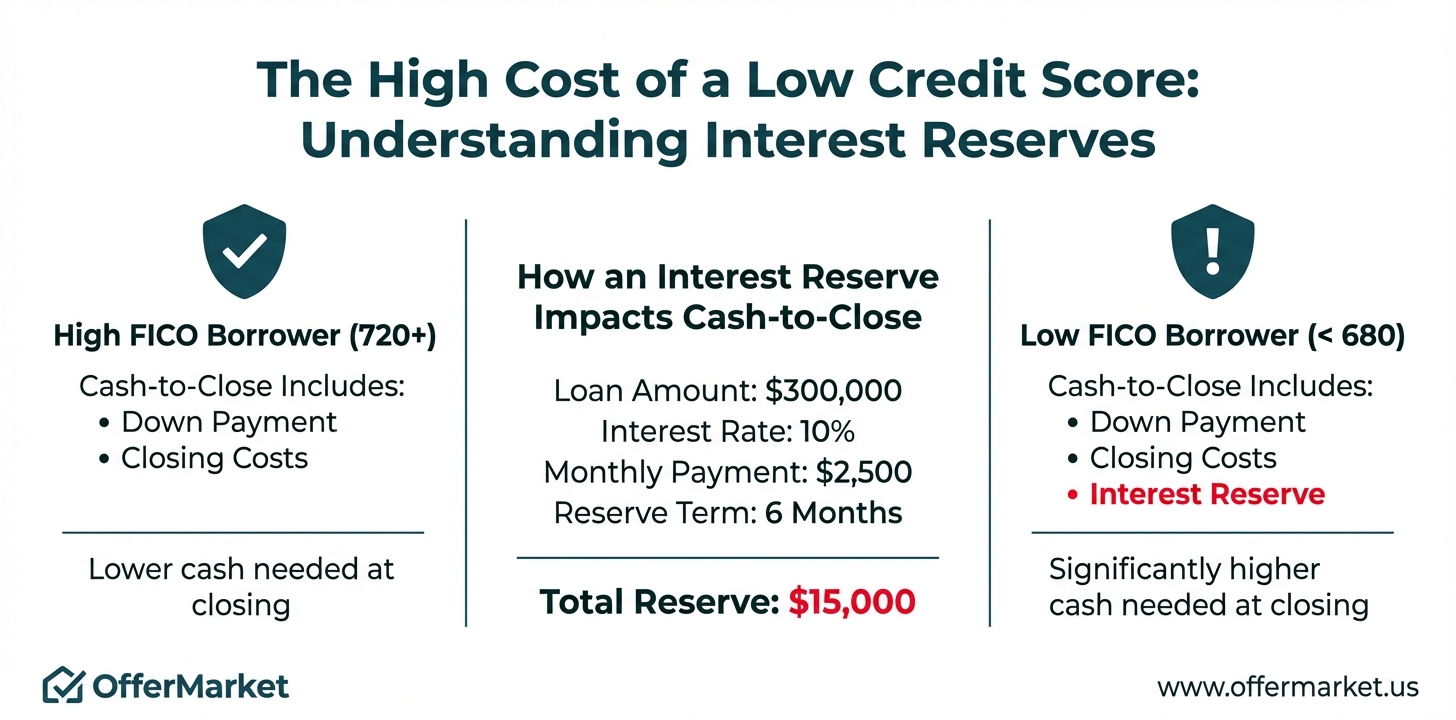

The High Cost of Low Credit

Hard money lenders are primarily focused on the asset, but the borrower's creditworthiness still plays a significant role, especially in determining cash-to-close requirements. Borrowers with lower FICO scores (typically below 680) are often required to have an "interest reserve."

An interest reserve is a portion of the loan proceeds set aside at closing to cover a set number of monthly interest payments (e.g., 3-6 months). This amount is held by the lender and used to make the payments automatically. While it ensures payments are made on time, it significantly increases the amount of cash a borrower needs to bring to the table, as it's funded out of their pocket and reduces the net loan proceeds available for the project.

Example:

- Loan Amount: $300,000

- Interest Rate: 10% (annual)

- Monthly Interest Payment: $2,500

- Required Interest Reserve: 6 months

- Total Reserve Amount: 6 x $2,500 = $15,000

This $15,000 would need to be funded by the borrower at closing in addition to their down payment and other closing costs.

Scope of Work (SOW) Restrictions

The SOW is the detailed blueprint for your renovation, and lenders scrutinize it carefully. They have specific rules about how renovation funds can be used, particularly in the early stages. Lenders will not allow you to "front-load" the budget with soft costs. This means you cannot use the first draw to pay for things like architectural plans, permits, or large upfront demolition costs. Lenders want to see tangible value being added to the property with each draw. The first draw is almost always a reimbursement for foundational work like framing, rough-in plumbing, and electrical, not for paying off initial administrative expenses.

Common Deal Killers

Many promising flips fail due to a few common, avoidable mistakes:

Inaccurate ARV: The entire financial model of a flip rests on the After Repair Value. If you overestimate the ARV, your profit margin disappears. It is crucial to run conservative comparable sales (comps) and get a realistic valuation from an experienced real estate agent or appraiser. Relying on overly optimistic "Zestimates" from sites like Zillow can be a fatal error.

Budget Overruns: Underestimating the renovation cost is the fastest way to drain your capital. Always include a contingency fund of 10-15% of the total rehab budget to cover unexpected issues like hidden mold, foundation problems, or termite damage.

Timeline Delays: Every month you hold the property, you are paying interest, taxes, and insurance. Permitting delays, contractor issues, or slow inspections can extend your timeline and eat directly into your profits. A well-planned project schedule is essential.

Exit Strategy is Key

A fix and flip loan is a temporary bridge, not a destination. From day one, you must have a clear and viable exit strategy. There are two primary paths:

**Sell:** This is the traditional flip. Your goal is to sell the property on the open market for a profit after renovations are complete. You must factor in realtor commissions, closing costs, and capital gains taxes into your profit calculations.

Refinance: This is the "BRRRR" exit. Instead of selling, you refinance into a long-term rental loan, typically a DSCR loan. This allows you to pull your capital out while retaining the property as a cash-flowing asset. To execute this successfully, you must ensure your numbers work for the DSCR refinance from the very beginning, accounting for the 6-month seasoning rule and LTV limits.

Your choice of exit strategy dictates your renovation choices, your timeline, and your ultimate financial outcome. Having a plan B is also critical in case the market shifts during your project.

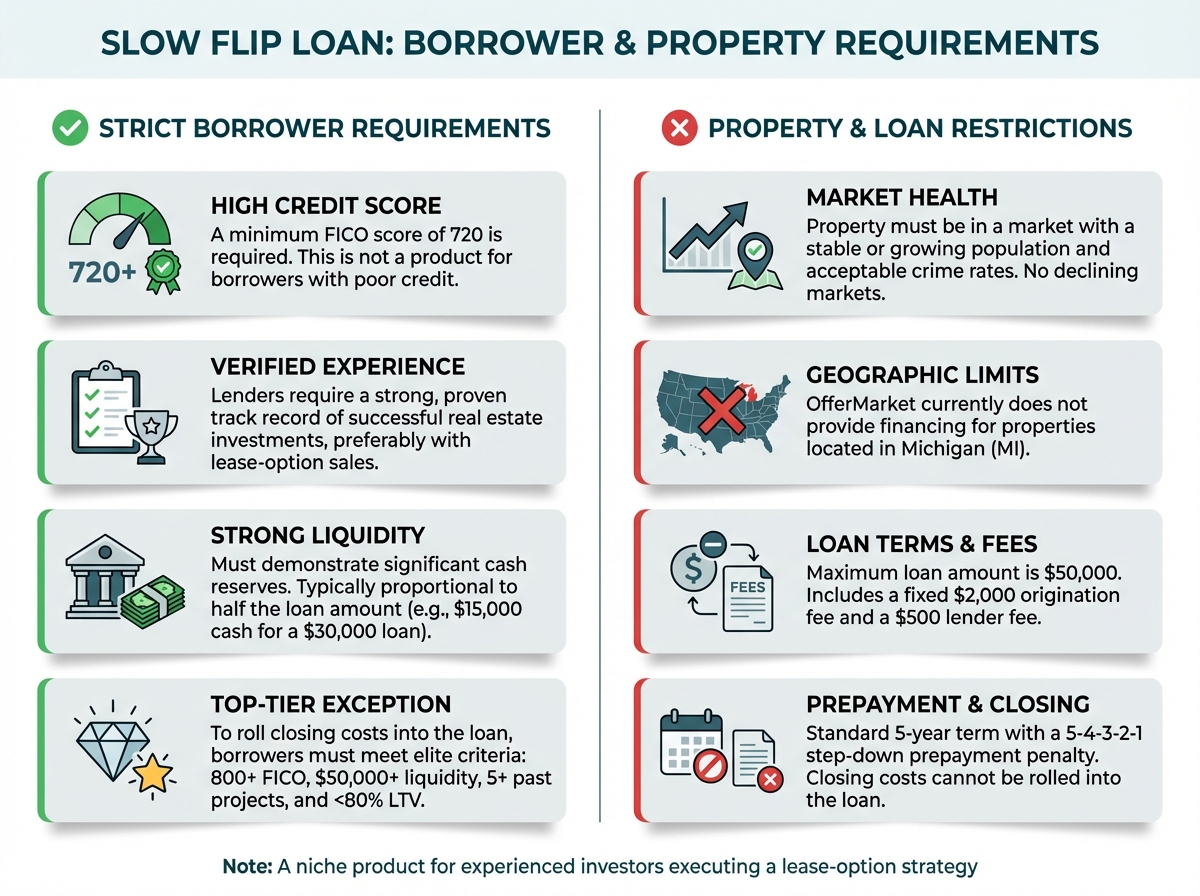

Slow Flip Loans: A Niche Product for a Specific Strategy

The "slow flip" is a unique real estate investment strategy, and it requires an equally unique financing product. A Slow Flip loan is a small-balance, short-term loan specifically designed for properties that are being sold via a lease-option agreement, also known as a rent-to-own contract. This isn't a loan for traditional flips or long-term rentals; it's a micro-loan, typically ranging from $25,000 to $50,000, that bridges the gap for an investor who has a tenant-buyer already in place.

Defining the Slow Flip

In a slow flip, an investor buys a property, performs minor cosmetic repairs, and then sells it to a tenant-buyer who may not currently qualify for a traditional mortgage. The tenant-buyer leases the property for a set period (e.g., 1-3 years) while working to improve their credit or save for a down payment. A portion of their monthly rent payment is often credited toward the final purchase price. The Slow Flip loan provides the initial capital for the investor to acquire and lightly prep the property for this arrangement.

Strict Borrower Requirements

Because of the niche nature and small loan amounts, lenders offering Slow Flip loans have very stringent requirements for the borrower. This is not a product for beginners. Typical requirements include:

- High FICO Score: A minimum credit score of 720 or higher is often required.

- Verified Experience: Lenders need to see a strong track record of successful real estate investments, often including previous experience with lease-option sales.

- Strong Liquidity: Borrowers must demonstrate significant cash reserves. Lenders want to see that the investor has the financial stability to handle any issues that may arise during the lease term. Typically proportional to half of the requested loan amount (e.g., verifying $15,000 in cash for a $30,000 loan).

Property & Market Restrictions

- Market Health: The property must be located in an area with acceptable crime rates and a stable or growing population; markets with declining populations will not be funded.

- Geography: OfferMarket does not lend in Michigan (MI).

Cost and Prepayment Penalties

Loan Terms & Mechanics

Loan Limits & Fees: The maximum allowable loan amount is $50,000. Fixed costs include a $2,000 origination fee and a $500 lender fee, and any assignment fees involved in the transaction will be directly deducted.

Duration & Prepayment Penalty: The standard loan term is 5 years accompanied by a 5-4-3-2-1 step-down Prepayment Penalty (PPP) structure. For lower loan amounts, this may occasionally be reduced to a 3-year term and PPP with management approval.

Closing Costs & Leverage: Closing costs cannot be rolled into the loan and the loan cannot exceed 100% of the purchase price.

The Exception for Rolling in Closing Costs

Lenders will allow you to roll closing costs into the loan (funding greater than 100% of the purchase price) only if your profile meets all of the following top-tier criteria:

- Credit score of 800+

- Verified liquidity of $50,000+

- Experience of 5+ past projects

- A Loan-to-Value (LTV) against the "as-is" appraised value of less than 80%

Ground-Up Construction Loans: Building from Scratch

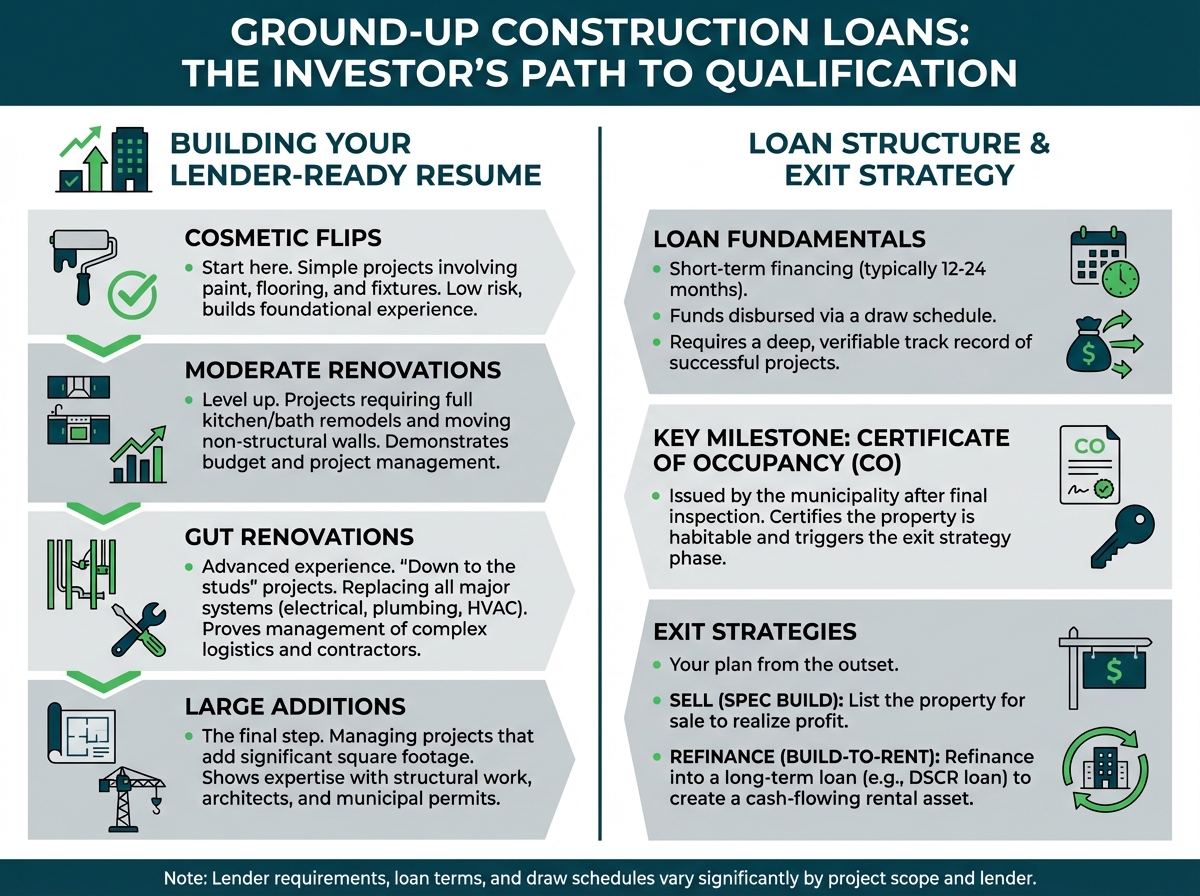

Financing new construction is one of the most complex and high-stakes areas of real estate investment lending. Ground-up construction loans provide the capital to take a project from a vacant lot to a finished, habitable building. These loans are structured similarly to fix and flip loans, with funds disbursed via a draw schedule, but the scale, risk, and qualification requirements are significantly higher.

High Barrier to Entry: The Experience Requirement

Lenders will not entrust a six- or seven-figure construction loan to an inexperienced investor. The single most important qualification factor is a deep and verifiable track record of successfully managing large-scale construction projects. Lenders will want to see a portfolio of completed projects, including detailed budgets, timelines, and proof of profitability. For new construction loans, a resume of a few simple cosmetic flips is not sufficient. Lenders need to see that you can manage a complex process involving architects, engineers, general contractors, and municipal building departments.

Proving Experience: The Path to New Construction

How can an investor build the necessary resume to qualify? The most common path is to work your way up through progressively larger and more complex renovation projects.

- Cosmetic Flips: Start with simple projects that involve paint, flooring, and fixtures.

- Moderate Renovations: Move on to projects that require moving some non-structural walls, and full kitchen and bath remodels.

- Gut Renovations: Successfully complete multiple "down to the studs" renovations where you are replacing all major systems (electrical, plumbing, HVAC) and reconfiguring the layout.

- Large Additions: Manage projects that involve adding significant square footage to an existing structure.

By successfully executing these types of projects, you can demonstrate to a lender that you have the experience to manage budgets, timelines, and contractors, making you a credible candidate for a ground-up construction loan.

Essential Documentation

The documentation required for a construction loan is extensive and non-negotiable. Before a lender will even consider an application, you must provide a complete package, including:

- Stamped Architectural Plans: Professionally drafted, finalized plans that have been approved by an architect or engineer.

- Approved Building Permits: You must have already navigated the municipal approval process and have permits in hand. This proves the city has approved your project. Information on local permitting can usually be found on your city or county's official government website (e.g., by searching for "[Your City] building permits").

- Detailed Line-Item Budget: A comprehensive budget that breaks down every single cost, from foundation concrete to doorknobs.

- General Contractor (GC) Vetting: The lender will vet your chosen GC, reviewing their license, insurance (including builder's risk insurance), and track record.

The Path to Permanent Financing

A construction loan, like a hard money loan, is a short-term solution (typically 12-24 months). The loan is designed to get you through the build phase. Your exit strategy must be planned from the outset. Once the final inspection is passed and the municipality issues a Certificate of Occupancy (CO), the property is officially habitable. At this point, you will execute your exit:

- If Selling (Spec Build): You will list the property for sale on the market.

- If Holding (Build-to-Rent): You will refinance the construction loan into a long-term, permanent financing product like a DSCR loan. This pays off the construction lender and leaves you with a stabilized, cash-flowing rental property.

Beyond the Core Four: Other Investor Financing Options

While DSCR, Hard Money, and Construction loans are the primary tools for most investors, several other financing options exist that can be the right fit for specific situations.

Conventional Investment Property Loans

This is the most traditional route. A conventional loan is one that conforms to the guidelines set by Fannie Mae or Freddie Mac.

When It Makes Sense: This option is best for investors who are just starting out (buying their first 1-4 properties) and have a strong, stable W-2 income and a low personal debt-to-income (DTI) ratio. If you can easily qualify based on your personal finances, you can often secure the lowest interest rates available.

Pros:

- Lower interest rates and fees compared to private or hard money.

- 30-year fixed terms provide long-term stability.

Cons:

- Strict DTI Requirements: Your personal income must support the new mortgage payment in addition to all your other debts.

- Slow and Document-Intensive: The underwriting process requires tax returns, pay stubs, and bank statements, and can take 30-45 days or more.

- Loan Limits: Fannie Mae and Freddie Mac limit the number of financed properties an individual can have (typically up to 10). This makes it difficult to scale a large portfolio.

Portfolio Loans

A portfolio loan is a non-conventional loan offered by a bank or lender that they keep on their own books instead of selling it on the secondary market. This gives them more flexibility with underwriting guidelines. A common type of portfolio loan for investors is a "blanket mortgage."

When It Makes Sense: For experienced investors who own multiple properties (often 5+) and want to consolidate their financing or tap into their portfolio's equity.

Pros:

- One Loan, One Payment: Simplifies managing finances for multiple properties.

- Flexible Underwriting: The lender can look at the performance of the entire portfolio rather than just one property.

- Cross-Collateralization: Allows you to use the equity in stabilized properties to acquire new ones.

Cons:

- Release Clauses: If you want to sell one property from under the blanket loan, the process can be complex and may require a partial paydown of the loan balance.

- Less Common: Finding lenders who offer competitive portfolio loans can be more challenging.

Private Money Loans

Private money is similar to hard money, but it comes from private individuals or small groups of investors rather than an established lending institution.

When It Makes Sense: When a deal doesn't fit into any traditional box. Perhaps the property is unique, the borrower's situation is unusual, or extreme speed is needed. These loans are relationship-based.

Pros:

- Maximum Flexibility: Terms are entirely negotiable between the borrower and the private lender.

- Speed: Can be the fastest financing available if you have a trusted private lender.

Cons:

- Higher Cost: Often the most expensive form of financing, with high interest rates and points.

- Relationship-Dependent: Access to private money depends on your personal and professional network.

- Less Reliable: An individual lender's capacity to fund a deal can be less certain than an institution's.

Comparing Options: A High-Level Look

| Feature | Conventional Loan | Portfolio Loan | Private Money Loan |

|---|---|---|---|

| Best For | Investors with low DTI & W-2 income | Experienced investors with 5+ properties | Unique deals needing speed & flexibility |

| Underwriting | Personal DTI, credit, tax returns | Overall portfolio cash flow & equity | Relationship & deal-specific merits |

| Speed | Slow (30-45+ days) | Moderate (30 days) | Very Fast (Can be <7 days) |

| Scalability | Low (Limited to ~10 properties) | High (Consolidates properties) | Moderate (Depends on lender's capital) |

| Cost | Low | Moderate | High |

How OfferMarket Streamlines Your Financing

Navigating the complex world of investor financing can be fragmented and inefficient. Investors often have to work with different lenders for different types of deals—a hard money specialist for flips and a separate bank for long-term rentals. OfferMarket is built to solve this problem by providing a single, streamlined platform for all of your real estate investment financing needs.

A Unified Platform

Whether your strategy is to fix and flip, build from the ground up, or acquire a portfolio of cash-flowing rentals, you can access the right financing through one simple, intuitive process. Our platform brings DSCR, Hard Money, and Construction loans under one roof, saving you the time and hassle of managing multiple lender relationships. One application gives you access to a full suite of products tailored to your specific deal.

Competitive Terms and High Leverage

Our goal is to help you maximize your return on investment. We achieve this by offering some of the most competitive terms and highest leverage in the industry. For flippers, this means securing up to 90% of your project costs. For buy-and-hold investors, it means maximizing your cash-out refinance to pull capital for your next deal. We structure our loans to help you keep more of your money working for you.

Technology-Driven Efficiency

The traditional lending process is notoriously slow and paper-intensive. We leverage technology to create a faster, more transparent, and user-friendly experience. Our online portal allows you to submit applications, upload documents, and track the status of your loan in real-time. This efficiency means we can close loans in a fraction of the time it takes traditional banks, giving you a critical advantage in a competitive market.

Investor-Focused Support

We are more than just a lender; we are a partner in your success. Our team is comprised of lending experts who are also real estate investors themselves. We understand the nuances of your deals because we've been in your shoes. We can provide expert guidance to help you choose the right loan product for any deal, ensuring your financing is perfectly aligned with your investment strategy.

Take the Next Step: Analyze Your Deal and Get Funded

Knowledge is the first step, but action is what closes deals. Now that you understand the landscape of real estate investor loans, it's time to apply it to your own projects.

Get an Instant Quote: The fastest way to see what's possible is to get real numbers for your deal. Get an instant quote on our website to see your potential loan terms in minutes.

Model Your Scenarios: Don't guess, calculate. Use our powerful online tools, like the DSCR Calculator, to analyze the cash flow of a potential rental property and ensure the numbers work.

Connect with a Lending Expert: Every deal is unique. If you have questions about a complex project or want to discuss your long-term investment goals, contact our team of lending specialists. We're here to help you find the perfect financing solution to scale your business.

OfferMarket Loans

Check your rate

60 seconds · no credit pull