*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The Ultimate Guide to Fix and Flip Funding (From LTC to Closing)

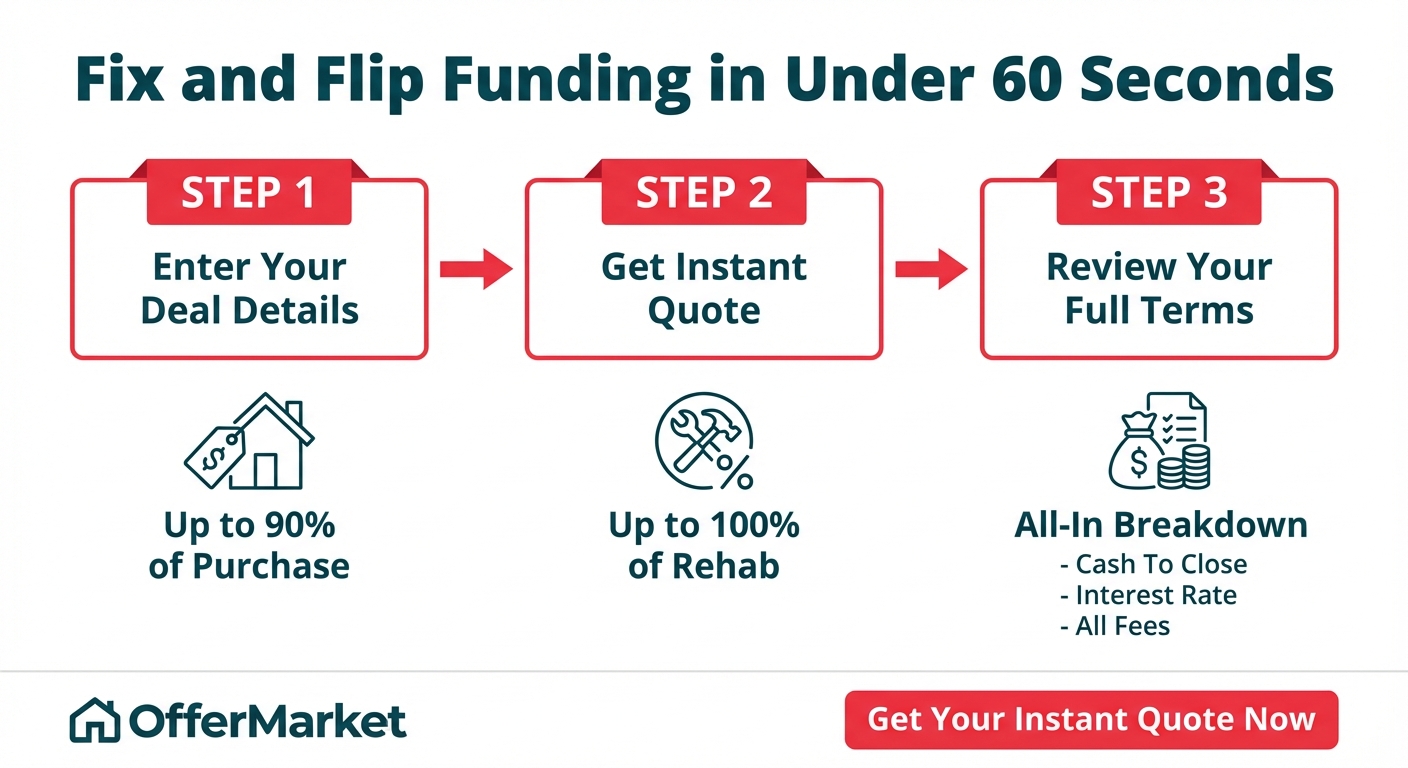

Getting fast, reliable fix and flip funding starts with understanding your terms. With OfferMarket, you can receive a detailed, transparent loan term sheet in under one minute. Our instant quote system is designed to give you a comprehensive breakdown of your loan, including the purchase component, which can be up to 90% of the purchase price, and the repair component, with financing up to 100% of your rehab budget. This immediate feedback allows you to vet your deal's numbers against real-world financing scenarios instantly.

When you get an instant quote, your deal is entered directly into our system.

This allows our capital markets team to immediately begin searching for opportunities across our network of capital providers to secure even better terms than what's initially quoted. The generated loan terms you receive set clear expectations from the start, showing you the precise cash-to-close amount required, a full breakdown of all fees, the interest rate, and the loan structure. There are no hidden costs or last-minute surprises. Give us a shot now; in less than a minute, you’ll have a competitive term sheet in hand to compare against other lenders, giving you a powerful head start in your search for the best fix and flip funding.

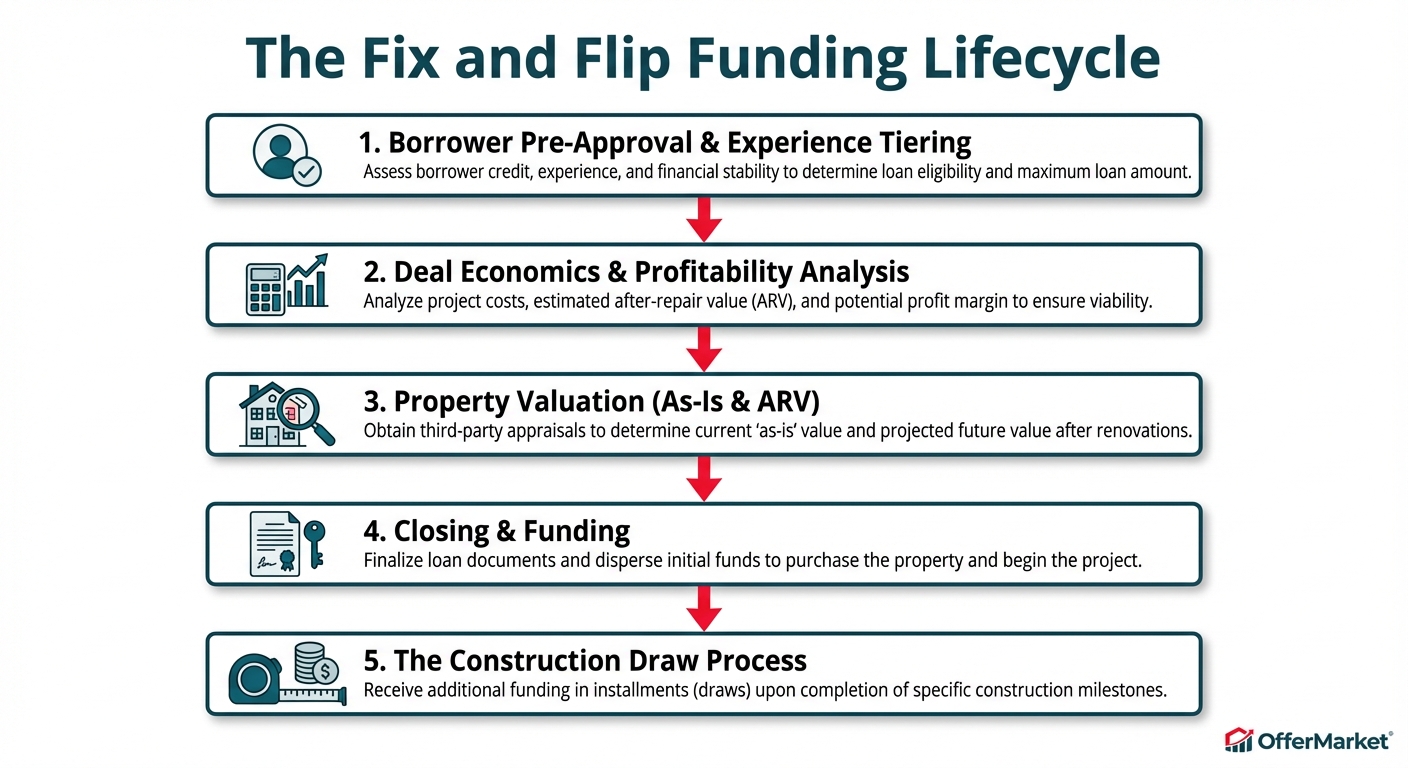

The Fix and Flip Funding Lifecycle

Understanding the lifecycle of a fix and flip loan is crucial for a smooth and profitable project. From the moment you're approved to the final draw for your renovation, each phase has specific requirements and expectations. Lenders structure this process to mitigate risk while providing you with the capital needed to execute your business plan.

Borrower Pre-Approval and Experience Tiering

Before you even put a property under contract, the first step is getting pre-approved with a lender. This isn't just a formality; it's where the lender assesses your viability as a borrower. Lenders categorize investors into experience tiers, which directly impacts the loan terms you'll be offered.

- Tier 1 (Beginner): 0-2 flips completed in the last 24-36 months. These borrowers typically receive more conservative terms, such as 85% Loan-to-Cost (LTC) and may be required to hold interest reserves.

- Tier 2 (Intermediate): 3-5 flips completed. These investors have a proven track record and can often access better terms, like 90% LTC and potentially waived interest reserves if their credit is strong.

- Tier 3 (Expert): 6+ flips completed. Top-tier investors are seen as low-risk and can command the best terms, including the highest leverage, lowest rates, and fewest restrictions.

During pre-approval, lenders will review your credit report, liquidity (cash on hand), and any past real estate experience. Having this done upfront allows you to make offers with confidence, knowing your financing is lined up.

Deal Economics and Profitability Analysis

Once you have a property under contract, the lender's underwriting team will perform a deep dive into the deal's economics. They are essentially investing alongside you and need to be confident in the project's profitability. They will analyze:

- Purchase Price: Is the price supported by recent comparable sales (comps) in the area?

- Rehab Budget: Is your Scope of Work (SOW) detailed and are the costs realistic for the market? An inflated or insufficient budget is a major red flag.

- After Repair Value (ARV): Is your projected ARV achievable based on comps of recently sold, renovated properties nearby?

- Profit Margin: Lenders need to see a healthy potential profit. Most hard money lenders look for a projected net profit of at least 10-15% of the ARV. This ensures you are sufficiently motivated to see the project through to completion, even if unexpected costs arise.

Using a fix and flip calculator is an essential step to model your costs, including loan interest, closing costs, and carrying costs, to ensure your deal meets these profitability thresholds.

Property Valuation: As-Is and After Repair Value (ARV)

The property's value is the cornerstone of the loan's security. Lenders will order a third-party appraisal to determine two key figures:

- As-Is Value: The current market value of the property in its existing condition, before any renovations are made. This helps the lender understand the initial collateral value.

- After Repair Value (ARV): The appraiser's professional opinion of the property's market value after all the proposed renovations in your Scope of Work are completed to a professional standard.

The appraiser will use your detailed SOW to understand the planned upgrades and will find comparable sales of recently renovated homes in the immediate vicinity to support their ARV conclusion. An accurate, well-supported ARV is arguably the most critical component of the loan application.

Closing, Funding, and The Construction Draw Process

Once the appraisal is in and the underwriting is complete, you'll move to closing. At the closing table (or through a remote closing process), you will sign the loan documents and pay your cash-to-close amount (down payment + closing costs). The lender then funds the loan, and the seller is paid.

The portion of the loan allocated for repairs is not given to you in a lump sum at closing. Instead, it is held in an escrow account by the lender. You will access these funds through a construction draw process:

- Complete a Phase of Work: You use your own capital to complete a portion of the renovation as outlined in your SOW (e.g., demolition and framing).

- Request a Draw: You submit a draw request to the lender, detailing the work that has been completed.

- Inspection: The lender sends an inspector to the property to verify that the work has been done and matches the SOW.

- Release of Funds: Once the inspection is approved, the lender reimburses you for the completed work by releasing a "draw" from your rehab escrow account.

This process repeats itself until the project is complete. It protects the lender by ensuring their funds are being used as intended and that the property's value is increasing according to plan.

Understanding Key Fix and Flip Loan Metrics

To navigate the world of hard money lending, you must be fluent in its language. Lenders use a specific set of metrics to evaluate the risk and viability of every deal. Mastering these concepts will allow you to structure your deals for a higher likelihood of approval and better terms.

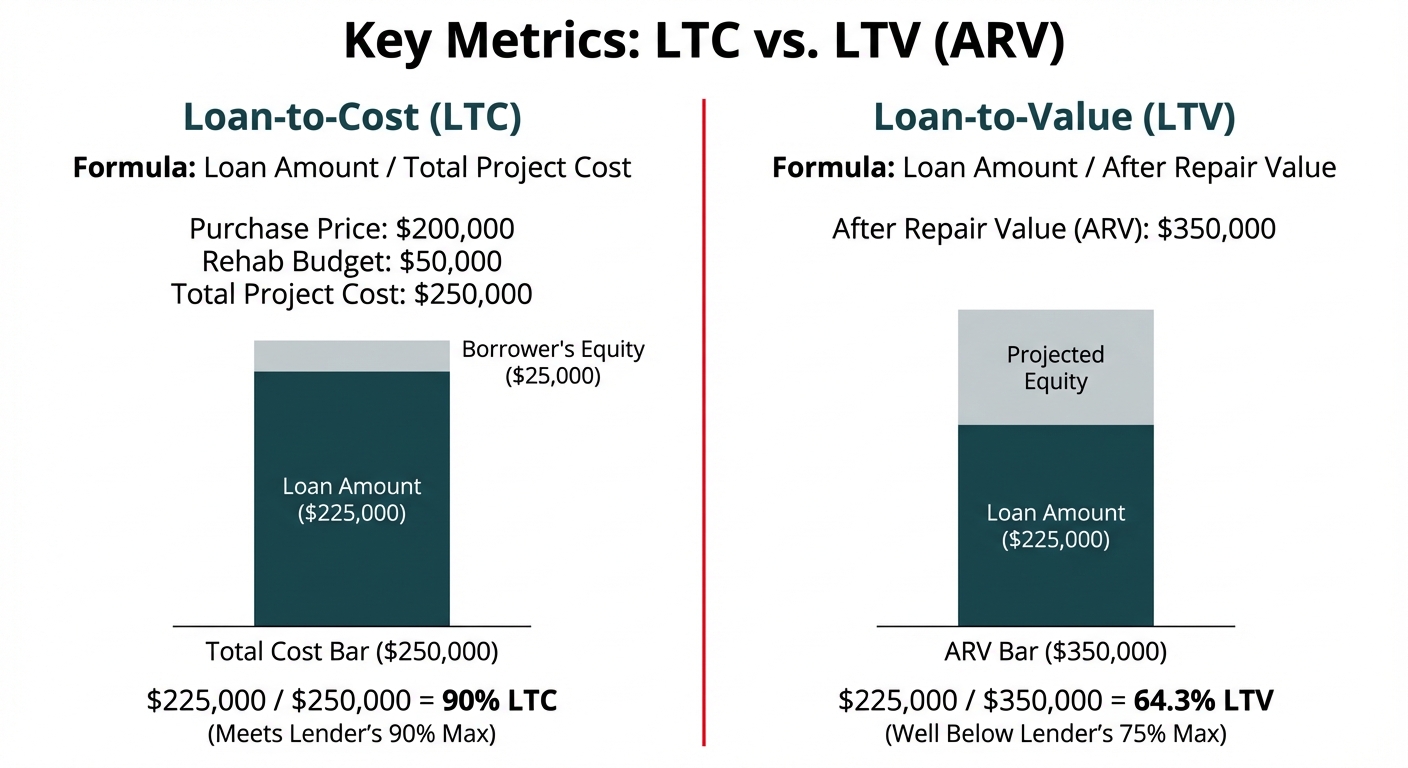

Loan-to-Cost (LTC) Explained

Loan-to-Cost, or LTC, is the primary metric used in fix and flip funding. It measures the total loan amount as a percentage of the total project cost (purchase price + renovation costs).

Formula: LTC = (Loan Amount / (Purchase Price + Renovation Costs)) * 100

For example, if you are buying a property for $200,000 and have a renovation budget of $50,000, your total project cost is $250,000. If a lender offers you a loan at 90% LTC, your loan amount would be:

$250,000 (Total Cost) * 0.90 (90% LTC) = $225,000 (Loan Amount)

In this scenario, you would be responsible for the remaining 10% of the cost ($25,000) plus closing costs. A higher LTC means less cash out of your pocket. Lenders typically offer up to 90% LTC for experienced investors and around 85% LTC for beginners.

Loan-to-Value (LTV) and After Repair Value (ARV)

While LTC governs the loan amount based on your costs, Loan-to-Value (LTV) acts as a crucial guardrail. LTV measures the loan amount as a percentage of the property's appraised value. For fix and flip loans, the most important LTV metric is based on the After Repair Value (ARV).

Formula: LTV = (Loan Amount / ARV) * 100

Lenders will cap the LTV, typically at 70% or 75% of the ARV, regardless of the LTC. This protects them from over-leveraging a property in case the market shifts or the ARV was overly optimistic.

Let's continue the previous example:

- Total Cost: $250,000

- Loan Amount: $225,000 (at 90% LTC)

- Let's say the ARV is appraised at $350,000.

The LTV would be: ($225,000 / $350,000) * 100 = 64.3% LTV

Since 64.3% is well below the typical 75% LTV cap, the loan would be approved at the full $225,000. However, if the ARV was only $300,000, the maximum loan amount would be capped at 75% of that, which is $225,000. In this case, the deal still works. But if the ARV was only $280,000, the max loan would be $280,000 * 0.75 = $210,000. The lender would reduce your loan amount from the $225,000 calculated by LTC down to $210,000 to meet their LTV requirement.

Return on Investment (ROI) Test for Underwriting

Lenders want to back successful projects. To that end, they often perform their own quick ROI analysis to ensure the deal is sufficiently profitable for you, the borrower. A common benchmark is that the projected gross profit should be at least 20% of the total project cost, or that the net profit is at least 10-15% of the ARV.

Let's use our running example:

- ARV: $350,000

- Total Costs (Purchase + Rehab): $250,000

- Projected Gross Profit: $350,000 - $250,000 = $100,000

From this gross profit, you must subtract holding costs (loan interest, insurance, taxes, utilities) and selling costs (realtor commissions, closing costs). Let's estimate these at $40,000.

- Projected Net Profit: $100,000 - $40,000 = $60,000

The lender's ROI test:

$60,000 (Net Profit) / $350,000 (ARV) = 17.1%

Since 17.1% is above the typical 10-15% threshold, this deal passes the profitability test. If the projected profit were too thin, a lender might decline the loan, viewing it as too risky for the borrower.

Calculating Cash-to-Close and Interest Reserves

"Cash-to-Close" is the total amount of liquid funds you need to bring to the closing table. It's more than just your down payment.

Components of Cash-to-Close:

- Down Payment: The portion of the total project cost not covered by the loan (e.g., the 10% in a 90% LTC loan).

- Origination Points: A fee charged by the lender to originate the loan, typically 1-3% of the loan amount.

- Third-Party Closing Costs: Fees for appraisal, title insurance, attorney/escrow fees, recording fees, etc. These can range from $3,000 to $7,000 or more, depending on the loan size and location.

- Interest Reserves: This is a portion of the loan proceeds that the lender holds back to make the monthly interest payments on your behalf. It's a risk-mitigation tool. Lenders typically require 3-6 months of interest payments to be held in reserve, especially for less experienced borrowers or those with lower credit scores.

Example Calculation:

- Loan Amount: $225,000

- Down Payment (10% of $250k cost): $25,000

- Origination Fee (2 points): $225,000 * 0.02 = $4,500

- Third-Party Costs (estimate): $5,000

- Interest Rate: 10% annual (0.833% per month)

- Monthly Payment: $225,000 * 0.00833 = $1,875

- Interest Reserve (6 months): $1,875 * 6 = $11,250

Total Cash-to-Close: $25,000 (Down Payment) + $4,500 (Points) + $5,000 (Costs) = $34,500

In this case, the $11,250 interest reserve is typically funded from the loan proceeds, not paid out of pocket, but it reduces the initial funds available for construction. Stronger borrowers can often get the interest reserve requirement waived, significantly reducing their cash-to-close burden.

Required Documentation for Fast Underwriting

A lender's speed is often limited by the borrower's preparedness. To ensure a fast and smooth underwriting process, you should have your documentation organized and ready to submit from day one. A disorganized submission can cause days or even weeks of delays.

Property and Purchase Contract Requirements

This paperwork is specific to the property you are acquiring.

- Fully Executed Purchase and Sale Agreement: This is the contract signed by you (or your entity) and the seller. It must include the property address, purchase price, and all addenda.

- Proof of Earnest Money Deposit: A copy of the cleared check or wire transfer receipt showing you have paid the earnest money deposit to the title or escrow company.

- Title Company/Closing Agent Information: The name, address, and contact information for the professional who will be handling the closing.

Business Entity Documentation: LLCs and Corporations

Most hard money lenders require borrowers to take title in a business entity, not their personal name. This provides a layer of liability protection and is standard practice in commercial lending.

- Articles of Organization (for LLCs) or Incorporation (for Corporations): The foundational document filed with the state to create your entity.

- Operating Agreement (for LLCs) or Bylaws (for Corporations): This internal document outlines the ownership structure and operating rules of your company. It must be signed by all members/shareholders.

- Certificate of Good Standing: A recent document from your Secretary of State proving your entity is active and compliant.

- Employer Identification Number (EIN) Letter: The document from the IRS assigning your company its tax ID number.

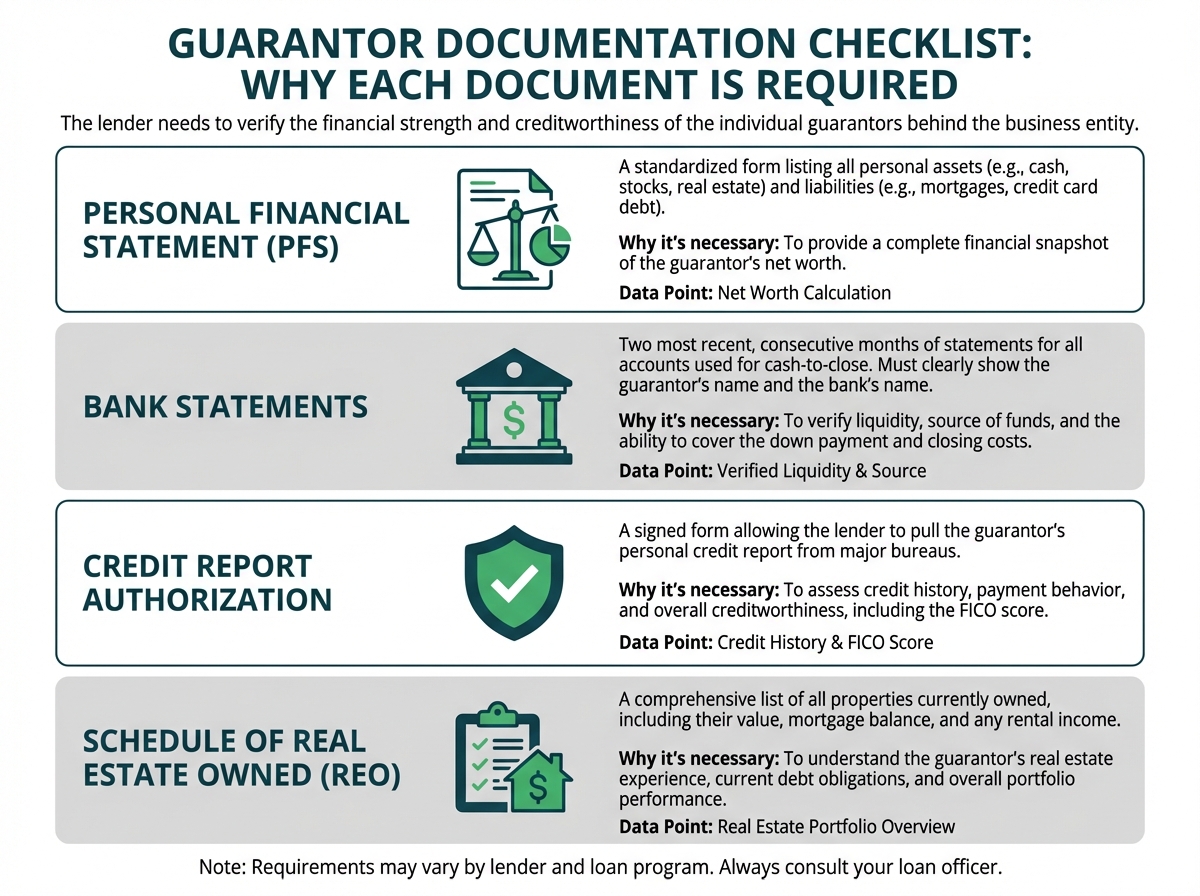

Borrower Financials: Bank Statements and Credit Reports

The lender needs to verify the financial strength and creditworthiness of the individual guarantors behind the business entity.

- Personal Financial Statement (PFS): A standardized form where you list all your personal assets (cash, stocks, real estate) and liabilities (mortgages, credit card debt).

- Bank Statements: Typically the two most recent, consecutive months of statements for all accounts you will use to show liquidity for the cash-to-close. The statements must show your name and the bank's name.

- Credit Report Authorization: A signed form allowing the lender to pull your personal credit report from the major bureaus like Experian or Equifax.

- Schedule of Real Estate Owned (REO): A list of all properties you currently own, including their value, mortgage balance, and rental income if applicable.

Project Documentation: Scope of Work (SOW) and Permits

The lender needs to understand exactly what you plan to do to the property to justify the rehab budget and the ARV.

- Detailed Scope of Work (SOW): This is one of the most critical documents. It should be a line-item breakdown of every single task, from demolition to final paint, with a corresponding cost for labor and materials. A vague SOW is a major red flag for underwriters.

- Contractor Bids (if applicable): If you are using a general contractor, provide their signed bid that matches your SOW.

- Plans and Permits (if applicable): For larger projects involving additions, structural changes, or significant electrical/plumbing work, the lender will require copies of the architectural plans and any permits already approved by the local building department.

How to Maximize Leverage and Preserve Liquidity

The savviest real estate investors know that smart financing is about more than just getting a loan; it's about structuring that loan to maximize leverage and keep as much cash in their pockets as possible. This liquidity can then be used for the next deal, allowing you to scale your business faster.

Using Experience to Achieve 90% LTC

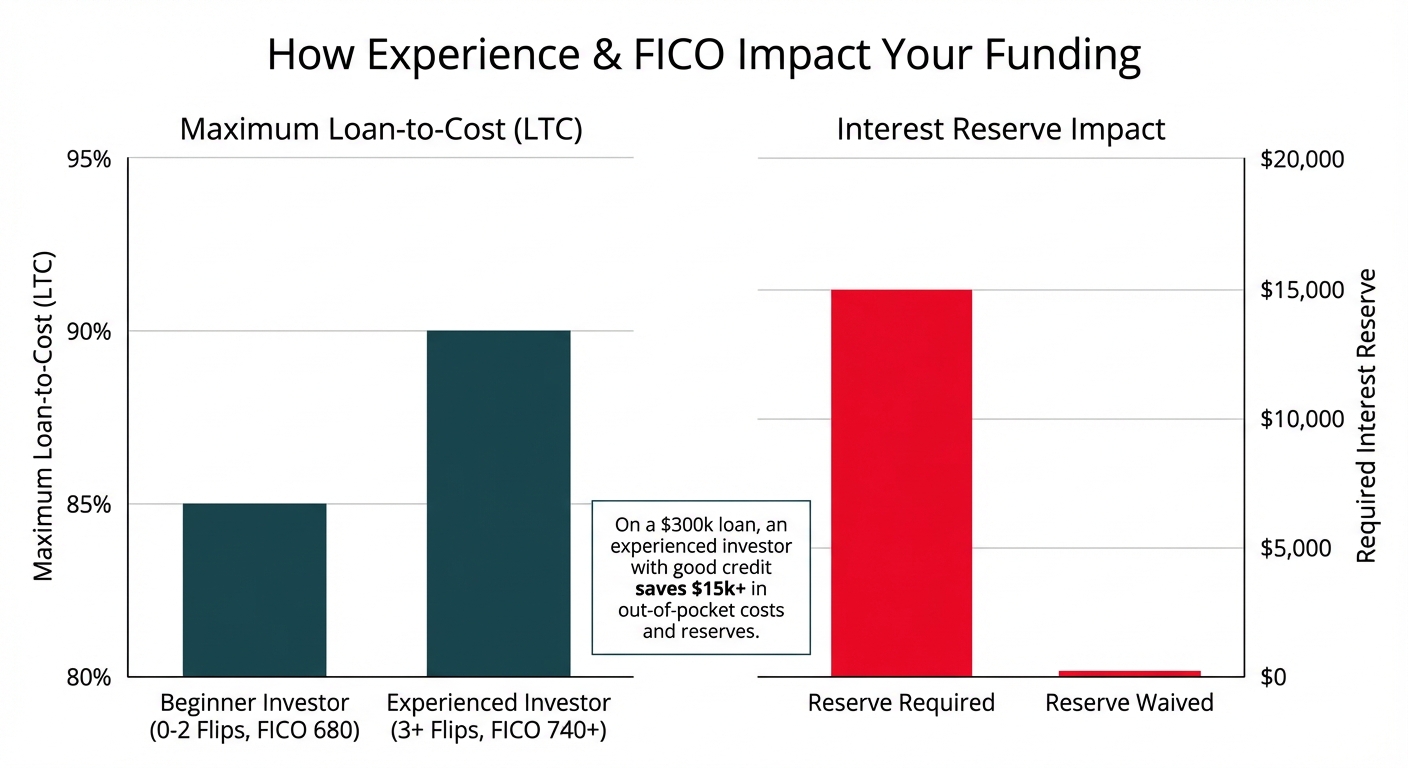

The single most effective way to maximize leverage is to build a track record of successful projects. As mentioned in the tiering system, lenders reserve their highest leverage—typically 90% LTC on purchase and 100% on rehab—for experienced investors.

- Beginner (0-2 flips): Expect 85% LTC. On a $250,000 total project, that's a $37,500 down payment.

- Experienced (3+ flips): Can achieve 90% LTC. On the same $250,000 project, that's a $25,000 down payment.

That's a $12,500 difference in out-of-pocket cash. By successfully completing your first few deals, even if at slightly less favorable terms, you are "buying" your way into the top tier of financing for all future projects. Diligently document every project you complete—including the HUD-1 settlement statements from both the purchase and the sale—to build your portfolio for future lender reviews.

The Role of FICO in Avoiding Interest Reserves

A high FICO score is a powerful tool for preserving liquidity. While experience often dictates your LTC, your credit score is the primary driver of whether a lender will require an interest reserve.

An interest reserve is when the lender withholds 3-6 months of interest payments from your loan proceeds at closing. While this means you don't have to make monthly payments out of pocket, it can tie up a significant amount of your capital that could otherwise be used for construction.

- FICO below 700: An interest reserve is almost always mandatory.

- FICO above 720-740: Most lenders will waive the interest reserve requirement for experienced borrowers.

On a $300,000 loan at 10% interest, a 6-month reserve is $15,000. Having that requirement waived means you have an extra $15,000 in your initial construction draw, dramatically improving your project's cash flow. Protecting your personal credit is a core component of a successful real estate investment strategy.

Structuring Your Scope of Work for Faster Reimbursement

The construction draw process is reimbursive, meaning you have to spend your money first. This can create cash flow crunches. A strategically structured Scope of Work can help mitigate this.

Instead of listing items chronologically, group them into draw schedules that front-load high-impact, high-cost items that can be completed early. For example, completing demolition, framing, and rough-in plumbing/electrical might represent a significant portion of your budget. By making that "Draw 1," you can request a large reimbursement early in the project, replenishing your capital to fund the next phases. A poorly planned SOW might have you waiting to be reimbursed for big-ticket items until the very end, straining your finances.

Negotiating and Structuring Seller Credits

A seller credit, or seller concession, is when the seller agrees to pay a portion of the buyer's closing costs. This can be a powerful way to reduce your cash-to-close.

For example, on a $200,000 purchase, you might negotiate a 3% seller credit ($6,000). To do this, you could offer $206,000 for the property with a $6,000 credit back at closing. The seller nets the same amount, but you now have $6,000 of their money to apply toward your closing costs.

Important Caveat: Lenders have rules about seller credits.

- They cannot be used for the down payment.

- They are typically capped at 3-6% of the purchase price.

- The property must still appraise for the higher, "grossed-up" purchase price ($206,000 in our example).

When structured correctly, a seller credit can cover most, if not all, of your third-party closing costs and origination points, preserving thousands of dollars of your liquidity.

Advanced Underwriting Rules and Hidden Traps

Beyond the standard metrics, lenders have a complex set of internal underwriting rules that can trip up even experienced investors. Understanding these "hidden traps" can be the difference between a smooth approval and a last-minute denial.

The Experience-FICO Partnership Rule

Many borrowers assume that if they are strong in one area (e.g., extensive experience), it can make up for a weakness in another (e.g., a borderline FICO score). This is often not the case. Many lenders have a "partnership rule" where you must meet the minimum threshold for both experience and credit to qualify for the best programs.

For example, to get 90% LTC, the rule might be "3+ flips in the last 24 months AND a 700+ FICO score." An investor with 10 flips but a 670 FICO might be downgraded to an 85% LTC product. An investor with a 780 FICO but only one flip will also be in the 85% LTC bucket. You need both keys to unlock the best terms.

Exceptions for Lending Over 100% of Purchase Price

While it sounds impossible, some lenders will fund over 100% of the purchase price in specific situations. This does not mean they are giving you a no-money-down loan. It happens when an investor finds an incredible off-market deal where the purchase price is significantly below the "as-is" value, and there is a substantial rehab budget.

Scenario:

- Purchase Price: $100,000

- Rehab Budget: $80,000

- Total Project Cost: $180,000

- Loan at 90% LTC: $162,000

In this case, the loan amount of $162,000 is more than 100% of the $100,000 purchase price. The lender will fund the full $100,000 purchase and place the remaining $62,000 into the rehab escrow. This is only possible if the deal still meets the LTV guardrail (e.g., the $162,000 loan is less than 75% of the ARV). This structure is reserved for strong borrowers with deeply discounted properties.

Minimum Net Worth Requirements for Guarantors

For larger loan amounts, typically over $750,000 or $1 million, many lenders impose a minimum net worth requirement on the personal guarantor. A common rule is that the guarantor's liquid net worth (excluding primary residence equity) must be equal to or greater than the total loan amount.

This is to ensure that if the project goes completely sideways, the borrower has other assets that could be used to make the lender whole. If you plan to scale up to larger, multi-million dollar projects, building your personal balance sheet becomes just as important as building your flip portfolio.

Wholesale Assignment Fee Caps and Restrictions

If you are acquiring a property through a wholesale transaction, be aware that lenders have strict rules on financing the assignment fee. Most lenders will cap the assignment fee they are willing to finance at 5-10% of the purchase price.

For example, if the original contract price is $150,000 and the wholesaler's assignment fee is $30,000, your final purchase price is $180,000. Some lenders may only recognize the original $150,000 as the true purchase price and cap the fee they will finance at, say, $15,000 (10%). This means you would have to pay the other $15,000 of the fee out of pocket, in addition to your regular down payment and closing costs. Always discuss the assignment fee with your lender upfront to avoid surprises.

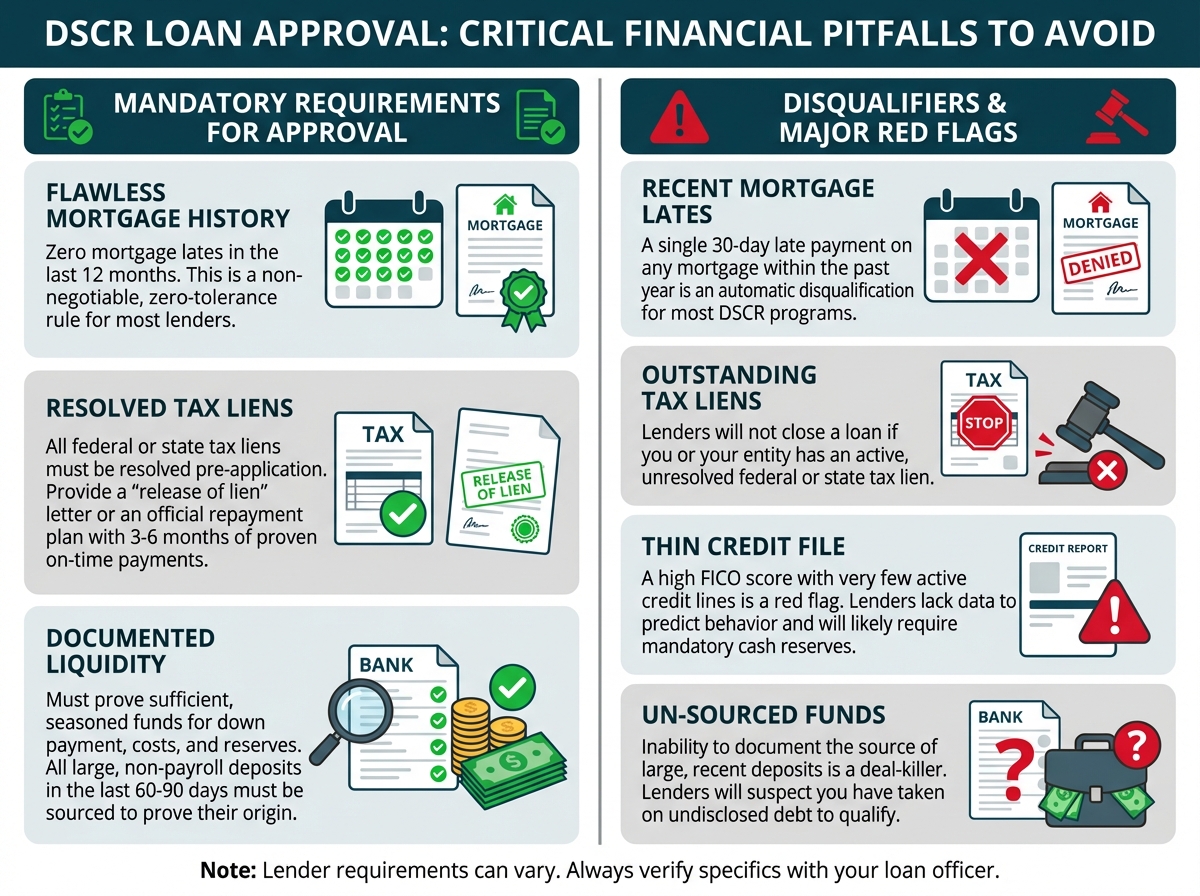

Critical Credit and Financial Gotchas

Your financial house must be in perfect order when applying for a fix and flip loan. Lenders have very little tolerance for credit blemishes or poorly documented finances, as these are seen as indicators of high risk.

Thin Credit Files and Mandatory Reserves

A "thin credit file" is one where the borrower has a good score but very few open and active trade lines (e.g., only one credit card and no auto or mortgage loans). Even with a 750 FICO, a thin file can make lenders nervous because there isn't enough data to predict future payment behavior. In these cases, a lender will almost certainly impose a mandatory interest reserve as a compensating factor, even if they would normally waive it for that FICO score.

Zero Tolerance Policy for Mortgage Lates

This is a non-negotiable rule for nearly every hard money and DSCR lender in the country: zero mortgage lates in the last 12 months. A single 30-day late payment on any mortgage on your credit report within the past year is an automatic disqualification for most programs. Lenders view this as the ultimate sign of financial distress. Before applying for a loan, pull your own credit and ensure your mortgage history is flawless.

Resolving Federal and State Tax Liens

Lenders will not close a loan if there is an outstanding federal or state tax lien on you or your business entity. Before you even apply, you must resolve these issues. You typically have two options:

- Pay the Lien in Full: Provide the lender with a "release of lien" letter from the IRS or state agency.

- Enter a Formal Repayment Plan: If you cannot pay the lien in full, you must have an official, approved installment agreement with the tax authority. You will need to provide the lender with a copy of this agreement and proof that you have made at least 3-6 consecutive, on-time payments.

Documenting Sufficient Liquidity for Approval

You must be able to prove you have enough cash for the transaction (down payment, closing costs) and often post-closing reserves (a few months of mortgage payments). Lenders are very strict about how these funds are documented.

- Sourcing and Seasoning: Any large, non-payroll deposits in your bank statements from the last 60-90 days must be "sourced." This means you have to prove where the money came from (e.g., a gift letter, sale of an asset). Lenders need to ensure you didn't just take out a short-term, undisclosed loan to qualify. Funds that have been in your account for more than 90 days are considered "seasoned" and typically don't require sourcing.

- Acceptable Assets: Liquidity can be shown in checking/savings accounts, brokerage accounts (typically valued at 70% of their face value to account for market volatility), and sometimes business bank accounts, provided your operating agreement allows you to use those funds for this purpose.

Geographic Restrictions and Loan Size Limitations

Not all lenders will lend on all properties in all areas. Lenders manage their portfolio risk by setting geographic and loan-size boundaries. Understanding these limitations can save you from wasting time pursuing a lender who won't fund your deal.

Prohibited Metropolitan Areas for Large Loans

Lenders aim to avoid over-concentration in any single market. If a lender already has tens of millions of dollars deployed in a specific Metropolitan Statistical Area (MSA) like Phoenix or Atlanta, they may temporarily stop lending there, or at least stop funding larger loans (e.g., >$1M) in that market. This is not a reflection on your deal, but rather a portfolio management decision by the lender. It's always wise to ask a potential lender upfront if they have any current restrictions on your target market.

Navigating Market-Specific Underwriting Nuances

Underwriters don't just look at your property; they look at the market it's in.

- Declining Markets: In areas where property values are stagnant or declining, underwriters will be much more conservative. They may reduce their maximum LTV from 75% to 70% or require a larger profit margin on the deal to buffer against further price drops.

- Rural Properties: Many national lenders will not fund projects in rural areas. They define "rural" based on population density and distance from a major MSA. These properties often have fewer comparable sales, making the ARV harder to prove, which increases the lender's risk.

- Judicial vs. Non-Judicial Foreclosure States: Lenders may have slightly stricter terms in states where the foreclosure process is long and costly (judicial states) compared to states where it is faster (non-judicial states).

How Loan Size Impacts Lender Scrutiny

The level of underwriting scrutiny increases exponentially with the loan size.

- <$500k Loan: Standard documentation is usually sufficient. The underwriting is more of a checklist process.

- $500k - $1.5M Loan: Expect a more thorough review. The lender may want to see a more detailed financial history, a more robust SOW, and may scrutinize the appraiser's report more heavily.

- >$1.5M+ Loan: These loans often require a "full credit committee" review. The lender may require a second appraisal from a different firm, a detailed P&L and balance sheet for your business, and a much higher net worth and liquidity requirement for the guarantor.

Strategic Market Selection for Your Next Flip

As you grow your business, consider these lending factors in your market selection. Targeting markets where lenders have a strong appetite for business can make securing financing much easier. Before entering a new market, network with other local investors and brokers to find out which private money lenders are most active and competitive in that specific area. A great deal is only great if you can get it funded.

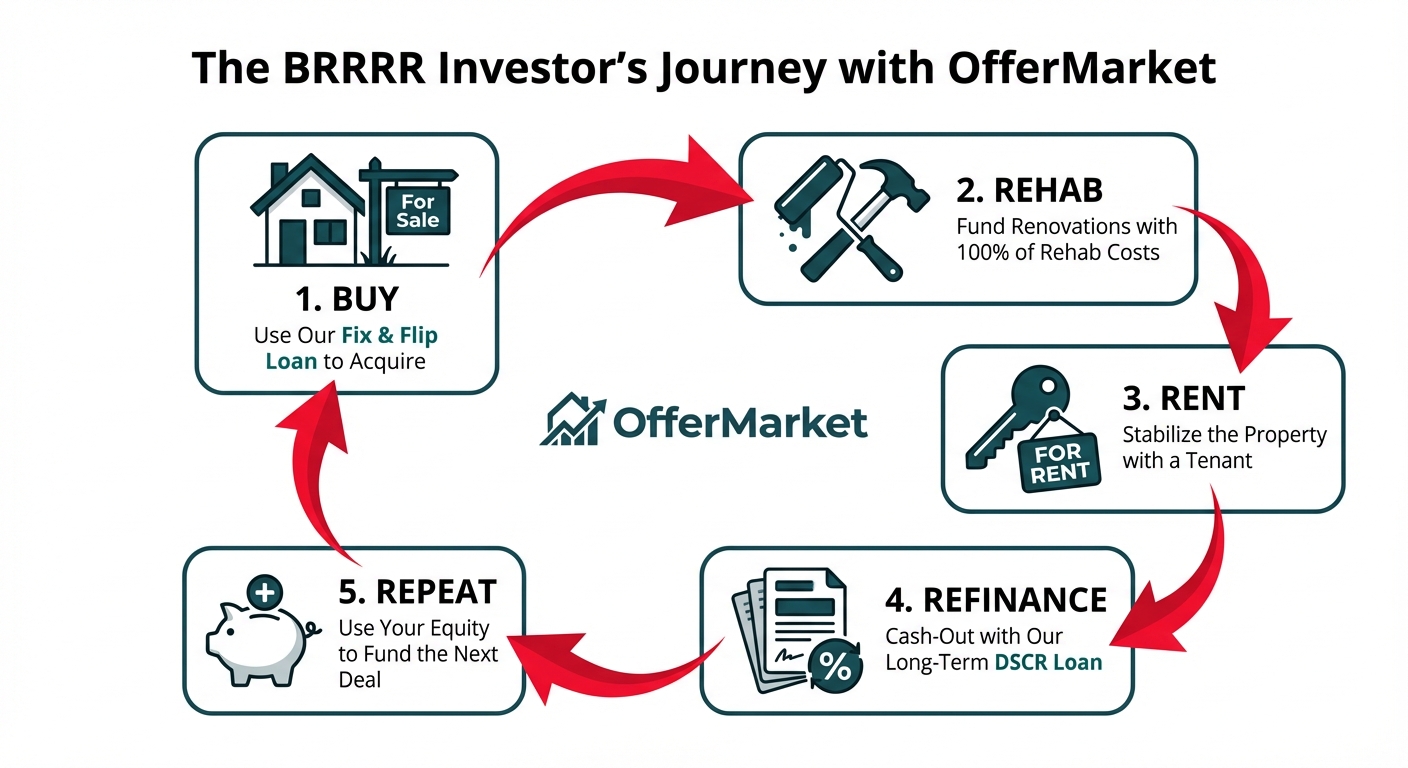

OfferMarket specializes in Fix and Flip and DSCR loans

Choosing the right lending partner is about more than just one transaction; it's about finding a partner who understands your long-term strategy. At OfferMarket, our loan products are specifically designed for the modern real estate investor, particularly those employing the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

OfferMarket is specifically designed to work with BRRRR investors

Our fix and flip funding is the perfect tool for the "Buy" and "Rehab" phases of your project. We provide the high-leverage, fast-execution capital you need to acquire and transform properties. But our support doesn't end when the renovation is complete.

Our Fix and flip loans are designed for a DSCR refinance exit

We understand that the goal for many investors is not to sell, but to build a long-term rental portfolio. That's why our fix and flip loan program is engineered for a seamless transition into a long-term DSCR loan. A DSCR (Debt Service Coverage Ratio) loan qualifies you based on the property's rental income, not your personal income. Once your renovation is complete and you've placed a tenant, we can help you refinance out of the short-term flip loan and into a 30-year fixed-rate DSCR loan, allowing you to pull your capital out and move on to the next deal.

Get a term sheet from us in under 1 minute to kick off your lender search now

Your next successful project starts with knowing your numbers. Don't waste days waiting for other lenders to get back to you. Get an instant quote from OfferMarket right now. In less than a minute, you'll have a transparent, comprehensive term sheet that gives you the data you need to make smart investment decisions and provides a powerful benchmark to start your lender search.

OfferMarket Loans

Check your rate

60 seconds · no credit pull