*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

New FinCen BOI Report Fee Just Landed on Settlement Statements

If you've recently closed on a residential property purchase through an LLC or other entity using cash or non-bank financing, you've probably spotted a new line item on your settlement statement: the FinCEN Reporting Fee. Based on OfferMarket's analysis of settlement statements across numerous transactions, this fee typically averages $250, though you can expect to see charges ranging anywhere from $200 to $400 depending on your title company and the complexity of your transaction.

This fee became a standard part of closings on March 1, 2026, when the Financial Crimes Enforcement Network's (FinCEN) Residential Real Estate Rule officially took effect. Here's the bottom line: it's not a tax, it's not a government filing fee you can pay directly, and it's not optional—it's simply the cost of federal compliance that your title company is now legally required to perform on certain types of real estate transactions.

![**Task:** Create a professional infographic displaying the typical FinCEN Reporting Fee range and average cost that appears on settlement statements.

**Visual Structure:** Horizontal layout with a centered large number display showing the average fee, flanked by minimum and maximum values on either side, with a visual range indicator bar below.

**ASCII Layout Reference:**

```

+----------------------------------------------------------+

| |

| $200 [====== $250 ======] $400 |

| MINIMUM AVERAGE MAXIMUM |

| |

| [==========================================] |

| Typical Fee Range |

| |

+----------------------------------------------------------+

```

**Image Section Breakdown:**

- Top section: Large](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772588432229_5pxoid.jpg?alt=media&token=c0fbed36-d39a-47f4-a01d-2b02ddb1996c)

As a Buyer, Can I Pay the Fee Myself?

The short answer: No.

This is one of the most common questions we hear from real estate investors when they spot the FinCEN Reporting Fee on their settlement statement. And honestly, the logic makes sense—if you can file your LLC's Beneficial Ownership Information (BOI) report yourself for free on the FinCEN website, why can't you handle this Real Estate Report the same way and pocket that $200-400?

Here's the deal: the law simply doesn't allow it. Let's break down exactly why you can't bypass the title company and self-file, even if you're ready and willing to do the legwork.

Understanding the "Reporting Cascade"

FinCEN's Residential Real Estate Rule doesn't give you—the buyer—any say in who files the report. Instead, the rule creates a strict seven-tier "cascade" of potential reporting persons based on their role in the transaction. Responsibility flows down this list in order:

- The Settlement Agent (typically the title company or closing attorney)

- The person who prepares the settlement statement

- The person who files the deed of transfer with the county

- The title insurance underwriter

- The real estate agent representing the transferee (buyer)

- The real estate agent representing the transferor (seller)

- Any other person involved in the closing

In nearly every standard real estate transaction, the title company lands squarely at position #1 on this list. Once they are involved in the deal, they become the legally designated "Reporting Person"—and that responsibility cannot be transferred to you.

You Are the Subject, Not the Reporter

Here's what trips up a lot of investors: You're not part of the reporting chain at all. As the buyer (or "transferee" in legal speak), you're actually the subject of the report—the person whose information gets collected and sent to the federal government.

Think of it like a background check. You can't run your own FBI background check and hand it to an employer. A designated third party handles it because they're accountable for getting it right. Same deal here.

Why Title Companies Cannot Delegate This Responsibility

You might be thinking: "Can't the title company just sign something letting me take care of it?" Here's the thing—FinCEN does have something called a "Designation Agreement," where professionals in the reporting chain can shift responsibility to someone else on that list.

But here's the key point: You, as the buyer, aren't on that list. The title company can only pass the baton to another professional involved in the closing (like the deed filer or underwriter)—not to you.

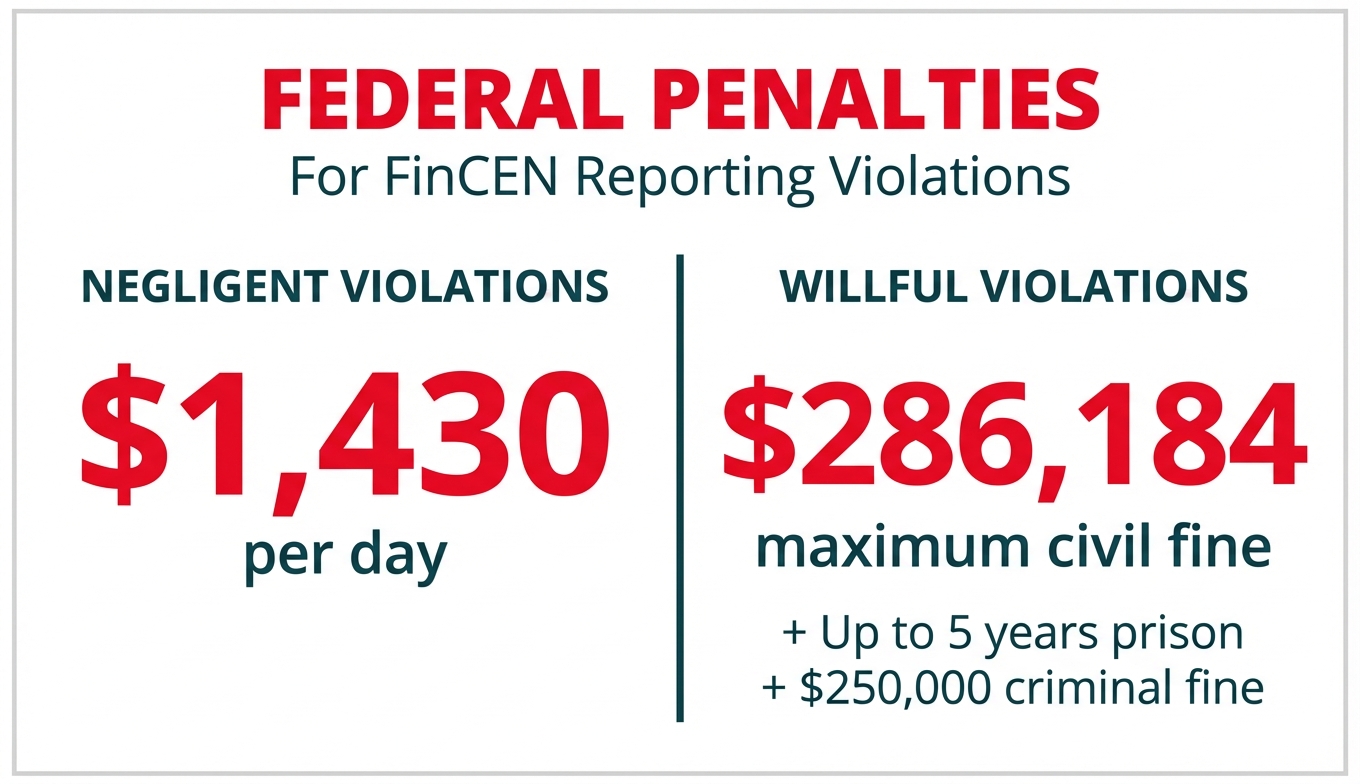

Even if they wanted to let you handle it, they're the ones on the hook. Title companies face serious federal penalties for non-compliance:

- Negligent violations: Civil penalties of up to $1,430 per day the violation continues

- Willful violations: Civil penalties up to $286,184, plus potential criminal penalties including up to five years in prison and fines up to $250,000

No title company is going to take on that risk just so an investor can "save a few hundred dollars" by self-filing. If you make a mistake, forget to file, or submit incomplete information, the government doesn't come knocking on your door—they go after the title company. The $200-400 fee you see on your settlement statement is what they're charging to assume this massive legal liability on your behalf.

Don't Confuse the RRE Report with the BOI Report

This mix-up happens all the time, so let's clear it up. There are actually two different FinCEN reports that real estate investors need to know about:

The BOI Report (Beneficial Ownership Information):

- This is a one-time filing for your LLC or corporation

- You file it yourself, directly with FinCEN, completely free

- It's about your entity's ownership structure, not a specific property transaction

- You can (and should) handle this yourself at FinCEN.gov

The RRE Report (Residential Real Estate):

- This is a transaction-specific report filed every time you buy a qualifying property

- It must be filed by the designated "Reporting Person" (the title company)

- It's about the specific real estate deal happening right now

- This is what the $200-400 fee on your settlement statement covers

Here's the simple way to think about it: The BOI report tells the government who owns your LLC. The RRE report tells the government your LLC just bought a house with cash. Different purposes, different filing requirements, and completely different rules about who can submit them.

What You Can Do

You can't file the Real Estate Report yourself, but you're not completely on the sidelines here:

Provide Information Promptly: The title company will send you a secure form (often through a portal like EagleID or similar software) to collect your entity and beneficial owner information. Getting this back quickly and accurately reduces their administrative burden—though honestly, it rarely reduces the fee since most of their cost is tied up in liability and compliance infrastructure.

Verify Your Entity Qualifies for an Exemption: If your LLC or trust falls under one of FinCEN's 16 exemption categories (more on this later in the article), you can provide documentation to the title company. If you're truly exempt, they won't need to file the report and shouldn't charge you the fee.

Structure Future Deals Differently: If this reporting requirement doesn't fit how you like to invest, consider other approaches. Traditional bank financing exempts the transaction from this rule. You could also buy properties in your personal name first, then transfer them to your entity later—just know this comes with its own set of risks and costs to weigh.

Here's the bottom line: The FinCEN Reporting Fee isn't optional, and you can't DIY it. It's simply a cost of doing business when you're making all-cash entity purchases under these new rules. Once you understand why it exists and what you're paying for, you can budget accordingly and skip the closing-table surprises.

Does This Rule Apply to Your Deal? A Four-Point Checklist

Before you worry about that fee on your settlement statement, let's figure out whether your transaction actually triggers the reporting requirement. FinCEN designed this rule to target a specific subset of real estate deals—not every property purchase falls under the new reporting mandate.

Here's a simple four-point checklist to assess whether your transaction is reportable. If your deal checks all four boxes, the FinCEN Reporting Fee is legitimate and required by federal law.

![**Task:** Create a comprehensive checklist infographic showing the four criteria that determine if a real estate transaction requires FinCEN reporting.

**Visual Structure:** Four-box grid layout (2x2) with large checkboxes, clear criteria titles, and brief descriptions for each criterion.

**ASCII Layout Reference:**

```

+----------------------------------------------------------+

| IS YOUR TRANSACTION REPORTABLE? |

| 4-Point Checklist |

+----------------------------------------------------------+

| |

| [✓] 1. RESIDENTIAL PROPERTY [✓] 2. ENTITY BUYER |

| 1-4 family homes, LLC, corporation, |

| condos, townhouses, partnership, |

| or residential land or trust |

| |

| [✓] 3. NON-FINANCED [✓] 4. NO EXEMPTIONS |

| Cash or non-bank No life-event or |

| financing (hard money, entity-level |

| private loans, etc.) exemptions apply |

| |

| ► All 4 boxes checked = Reportable Transaction |

+----------------------------------------------------------+

```

**Image Section Breakdown:**

- Header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772587432567_87him0.jpg?alt=media&token=b763bcc4-6049-41e6-8b0f-46d7fffa2982)

Criterion 1: The Property is "Residential"

First things first: What type of property are you buying?

Covered Properties:

- Single-family homes

- Duplexes, triplexes, and fourplexes (1-4 family residential properties)

- Condominiums

- Townhouses

- Co-operative apartments (co-ops)

- Vacant land that is zoned for residential use or that you plan to develop with a 1-4 family residence

The key distinction here is residential versus commercial use. According to FinCEN's official guidance, residential real property specifically means property designed or intended for occupancy by 1-4 families.

Exempt Properties:

- Apartment buildings with 5 or more units

- Office buildings

- Retail properties

- Industrial facilities

- Agricultural land (unless you're building a residence on it)

- Mixed-use properties where the commercial component is the primary use

Investor Tip: Buying vacant land? Here's what you need to know: it all comes down to intent and zoning. If the land is zoned residential and you're planning to build a single-family rental or small multifamily property (up to 4 units), you'll need to report. But if you're scooping up farmland or commercially zoned property, you're off the hook.

Criterion 2: The Buyer is a Legal Entity or Trust

The second criterion zeroes in on who appears as the buyer on the deed.

Covered Buyers:

- Limited Liability Companies (LLCs) of any type

- Corporations (S-Corps, C-Corps)

- Partnerships (Limited Partnerships, Limited Liability Partnerships)

- Trusts of any kind (Revocable Living Trusts, Irrevocable Trusts, Land Trusts, etc.)

Bottom line: if you're purchasing property under any legal entity or trust—even as the sole owner—the transaction may need to be reported.

Exempt Buyers:

- Individuals buying in their own name (e.g., "Jane Smith" or "John and Mary Doe")

Here's why this matters to you as an investor. Most savvy investors use LLCs or trusts to hold rental properties—and for good reason: liability protection and estate planning benefits are huge. But here's the trade-off: these structures trigger FinCEN reporting requirements when combined with the other criteria.

Important Note: Even if you're running a single-member LLC where you're the only player, the entity is considered the buyer—not you personally. That legal separation between you and your LLC? That's precisely what creates the reporting obligation.

Criterion 3: The Transaction is "Non-Financed"

Here's where things get a little tricky for many investors. FinCEN has a very specific definition of "non-financed," and it's probably not what you're picturing when you think about cash versus financed deals.

A transaction qualifies as "non-financed" when it doesn't involve a loan or line of credit from a financial institution that's already subject to federal Anti-Money Laundering (AML) requirements. Translation? We're talking about traditional banks, credit unions, and regulated mortgage lenders.

Funding Sources That Trigger Reporting:

- All-cash purchases (wire transfers, cashier's checks, personal funds)

- Hard money loans from private lenders

- Private money loans from individuals or unregulated funds

- Seller financing arrangements

- Loans from foreign banks or non-U.S. financial institutions

- Bridge loans from non-regulated lenders

- Cryptocurrency or other alternative payment methods

Funding Sources That Are Exempt:

- Traditional mortgages from banks

- Loans from credit unions

- Mortgages from federally regulated mortgage companies

- Home equity lines of credit (HELOCs) from regulated institutions

According to FinCEN's Residential Real Estate Rule, the exemption makes sense when you think about it: regulated financial institutions already run thorough "Know Your Customer" (KYC) checks and maintain their own AML compliance programs. When a bank underwrites your loan, they've already verified who you are and where your money's coming from—so the FinCEN report would just be duplicating that work.

The Gray Area: What happens when you're mixing cash and financing? Here's the rule of thumb: if any portion of your purchase involves a loan from a regulated financial institution that's secured by the property you're buying, the entire transaction is typically exempt. But let's say you're putting down 80% cash and borrowing 20% from a private lender—that deal is reportable.

Heads Up for Investors: This criterion tends to surprise most house flippers and cash buyers. Many investors pride themselves on their ability to close quickly with cash or private funding—but here's the thing: these are exactly the transactions FinCEN wants to keep an eye on. If you're using your self-directed IRA, a business line of credit from a non-bank lender, or pooled investor funds, your deal is likely reportable.

Criterion 4: No Major Exemptions Apply

Even if your transaction checks the first three boxes, certain types of transfers get a pass from the reporting requirement.

Common Life-Event Exemptions:

- Transfers resulting from a death (inheritance, estate distribution)

- Transfers due to divorce or legal separation

- Transfers related to bankruptcy proceedings

- Transfers made as a gift (with no consideration exchanged)

- Transfers between spouses or domestic partners

- Transfers to satisfy a court order or judgment

These exemptions make sense—they cover property transfers that happen for personal or legal reasons that have nothing to do with money laundering.

Entity-Level Exemptions (Brief Introduction):

FinCEN also gives a pass to 16 specific categories of entities. These exemptions typically apply to heavily regulated companies or large businesses that are already under significant government oversight.

Examples of exempt entities include:

- Publicly traded companies

- Banks and credit unions

- Insurance companies

- Registered investment companies and advisers

- Accounting firms

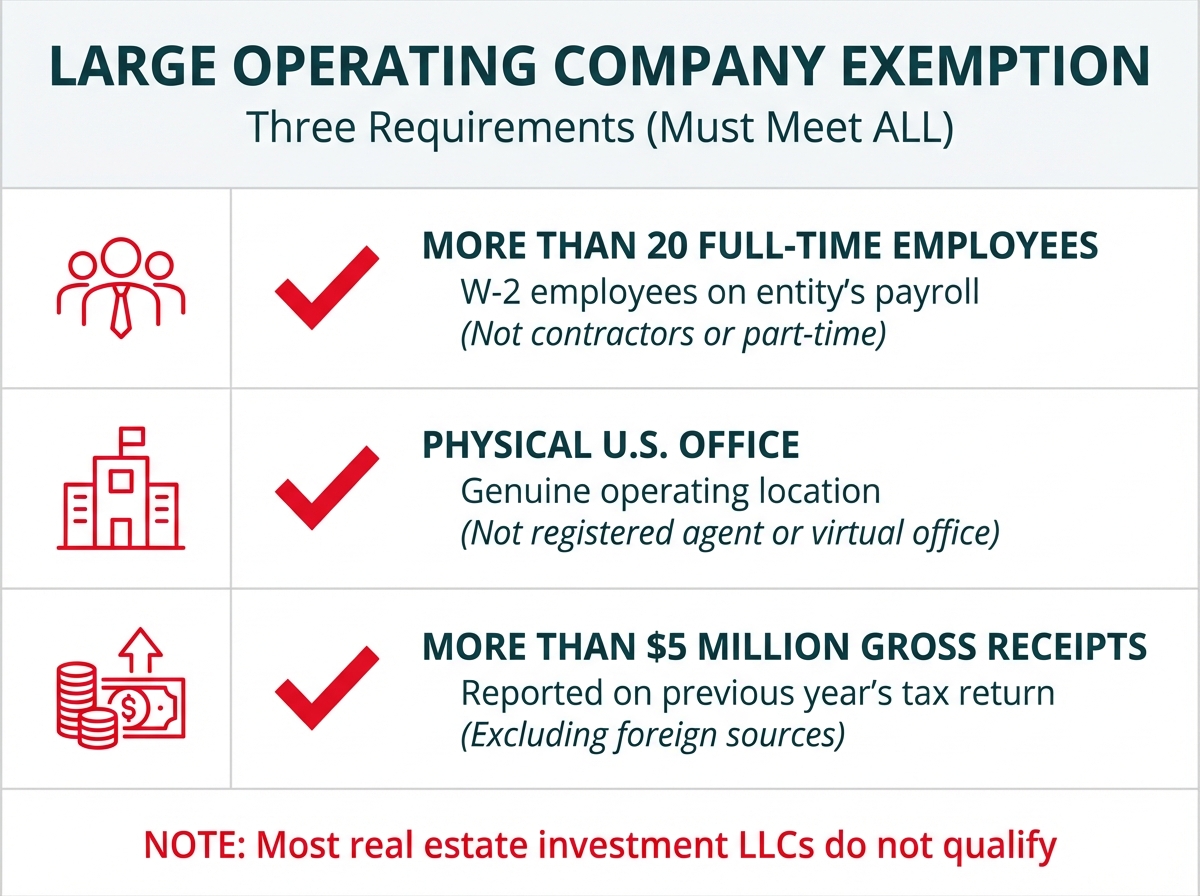

- "Large operating companies" (businesses with 20+ full-time U.S. employees, a physical U.S. office, and over $5 million in gross receipts)

Here's What This Means for You: The vast majority of small to medium-sized real estate investment LLCs will not qualify for these entity-level exemptions. If you have a typical single-member LLC that holds rental properties or flips houses, you don't meet the criteria for exemption. We'll dig deeper into these exemptions later in this article, but for now, assume your investment entity is subject to the rule unless you know for certain that you qualify for an exemption.

Self-Assessment Summary:

If you can answer "yes" to all four of these questions, your transaction is reportable and the FinCEN fee on your settlement statement is legitimate:

- ✓ Is the property residential (1-4 family)?

- ✓ Is the buyer an LLC, corporation, partnership, or trust?

- ✓ Is the deal funded without a traditional bank mortgage?

- ✓ Does the transaction fall outside the life-event and entity exemptions?

If you answered "no" to even one of these questions, the reporting requirement doesn't apply to your deal—and you should ask why that fee is showing up on your closing documents.

The Closing Process: What to Expect and What You'll Need to Provide

When your transaction triggers FinCEN reporting, you'll encounter an extra step at closing that catches many investors off guard. Let's walk through what happens behind the scenes—and why you're paying for it—so you can plan ahead and gather everything you need without last-minute scrambling.

Understanding the FinCEN Reporting Fee On Your Statement

You'll typically see a line item between $200 and $400 on your settlement statement, though some title companies charge more if your ownership structure is complicated. This isn't just a random add-on—it reflects real costs the title company takes on to keep your transaction compliant with federal law.

Here's What You're Actually Paying For:

Administrative Labor: Someone at the title company has to collect, review, and verify information about your entity and every beneficial owner. That means chasing down incomplete forms, making sure ID documents are legible and current, and double-checking that everything lines up. When you've got multiple owners or a layered trust structure, this work can eat up several hours.

Technology and Security Infrastructure: Title companies must use secure, encrypted portals to handle your sensitive personal information. These platforms (such as EagleID or similar systems) aren't free—they come with annual licensing fees, regular security updates, and must comply with federal data protection standards. The technology needs to meet FinCEN's strict requirements for how data is transmitted and stored.

Mandated Five-Year Secure Data Storage: Here's something important to understand: the reporting person must keep all beneficial ownership information and supporting documentation for five full years after closing. This goes beyond simply filing papers in a cabinet. The data must live in secure, encrypted databases with proper access controls, backup systems, and disaster recovery protocols. That ongoing cost of maintaining this secure archive? It's baked into your upfront fee.

Electronic Filing Costs: Getting the Real Estate Report to FinCEN requires specialized software that talks to the government's reporting system. There are real costs tied to each filing—system access fees plus the labor needed to accurately complete and transmit the report through FinCEN's portal.

Liability and Risk Premium: Here's the big one. The title company takes on significant legal and financial risk. If they fail to file, file incorrectly, or miss a deadline, they're looking at federal penalties exceeding $1,400 per day for negligence—and potentially criminal charges for willful violations. The fee includes a risk premium to cover this substantial liability exposure.

The "Reporting Cascade": Why the Title Company is in Charge

You might be thinking: why can't I just file this report myself and skip the fee? Great question. The answer lies in FinCEN's carefully structured hierarchy of responsibility, called the Reporting Cascade.

The rule establishes a clear pecking order for who's legally on the hook to file the Real Estate Report:

- The Settlement Agent (Title Company or Closing Attorney)

- The Professional Who Prepares the Settlement Statement

- The Professional Who Files the Deed of Transfer

- The Title Insurance Underwriter

The responsibility falls to the first person on this list who is involved in the transaction. In most standard residential real estate closings, the title company sits at the #1 position as the settlement agent. They're the ones running the show—coordinating the closing, disbursing funds, and making sure all documents are properly executed and recorded.

Why the Title Company Can't Delegate This Responsibility:

Here's the thing: even though you're the subject of the report (the buyer whose ownership is being disclosed), you're not a "Reporting Person" under FinCEN's definition. The cascade only includes licensed professionals who are already subject to federal oversight. While the rule does allow for a "Designation Agreement" where parties on the cascade can shift responsibility to each other, this agreement can only happen between the professionals on the list—not with you, the buyer.

From the title company's perspective, letting you self-file simply isn't an option. If you made an error, filed late, or forgot to file entirely, the title company would still be on the hook with the federal government. That $200-400 fee covers more than just paperwork—it reflects the legal responsibility they're taking on to ensure this federal requirement is handled correctly and on time.

Information You (The Investor) Will Need to Provide

To complete the Real Estate Report, the title company will need detailed information about both your purchasing entity and every individual who qualifies as a "beneficial owner." Expect to receive a secure online form (typically through an encrypted portal) within days of opening escrow.

About the Buying Entity:

- Full Legal Name: Exactly as it appears on your formation documents (e.g., "ABC Properties Holdings, LLC")

- Taxpayer Identification Number (EIN): Your entity's federal tax ID number

- Principal Business Address: The physical street address where your entity conducts business (P.O. boxes are not acceptable)

About Each "Beneficial Owner":

Here's where things can get a bit tricky, so let's break it down. FinCEN defines a beneficial owner as any individual who either:

- Owns or controls 25% or more of the ownership interests in the entity, OR

- Exercises substantial control over the entity

According to FinCEN's guidance, "substantial control" means senior officers (think President, CFO, General Counsel), managing members of an LLC, individuals with authority to appoint or remove senior officers, or anyone who directs, determines, or has substantial influence over important decisions made by the entity.

For each beneficial owner, you'll need to provide:

- Full Legal Name: Exactly as it appears on their government-issued ID

- Date of Birth: Complete date (month, day, and year)

- Residential Address: The individual's current home address (not the entity's business address)

- Government-Issued Photo ID: A clear, legible copy of a non-expired identification document

Acceptable identification documents include:

- State-issued driver's license

- U.S. passport

- State, local government, or tribal identification card

- Foreign passport (if no U.S. document is available)

Here's the deal: If you're the sole member of your LLC and also serve as the managing member, you wear both hats—you're a 25%+ owner AND someone who exercises substantial control. That means you'll need to provide all of this information about yourself. Got multiple members in your LLC? Each person who meets either criterion needs to be reported.

The title company will check that the photo on your ID matches your name and confirm the document is current. They'll also cross-reference your entity information with your formation documents. Any discrepancies or missing details will slow down your closing, so do yourself a favor and provide complete, accurate information right from the start.

Privacy Consideration: Here's some reassuring news: the Real Estate Report is not public record. It's stored in a secure federal database that only law enforcement, national security agencies, and certain regulatory bodies can access. You won't find it in county records, on the MLS, or in any public property database.

Strategic Planning: How to Legally Avoid the Reporting Requirement and Fee

The FinCEN Residential Real Estate Rule is now part of the landscape for many investors, but you've got options. With some smart structuring of your purchases, you can potentially avoid both the reporting requirement and the fee altogether. Let's walk through three legitimate strategies—each comes with its own considerations.

Option 1: Use Traditional Bank Financing

The most straightforward way to bypass the FinCEN reporting requirement? Get a mortgage from a federally regulated financial institution. When you finance through a bank, credit union, or licensed mortgage company, your transaction is automatically exempt from the RRE reporting rule.

Here's why this works: These lenders already operate under strict federal Anti-Money Laundering (AML) and "Know Your Customer" (KYC) regulations. They verify your identity, source of funds, and beneficial ownership as part of their standard underwriting. FinCEN views this existing oversight as sufficient—no additional real estate report needed.

The Pros:

- No FinCEN Reporting Fee: That $200-$400 line item won't show up on your settlement statement.

- No Additional Paperwork: Beyond your standard loan application, you won't need to gather the detailed beneficial ownership documentation the RRE rule demands.

- Leverage Your Capital: Financing lets you keep cash available for other investments or renovations.

The Cons:

- Slower Closing Process: Bank-financed deals typically take 30-45 days to close, versus 7-14 days for all-cash transactions—which can put you at a disadvantage in competitive markets.

- Stricter Underwriting: Regulated lenders have property condition requirements, debt-to-income ratio limits, and credit score minimums that can disqualify certain deals or investors.

- Interest Costs: Even at favorable rates, mortgage interest adds to your total acquisition cost over time.

- Property Restrictions: Many lenders won't finance properties in poor condition, limiting your ability to buy distressed assets that need significant rehab.

Bottom Line: If you're purchasing stabilized, rent-ready properties and aren't in a rush, traditional financing can eliminate the reporting burden entirely. But here's the reality for fix-and-flip investors or those buying at auction—this option often just doesn't fit your timeline or deal type.

Option 2: Purchase as an Individual, Then Transfer to an Entity

Here's a strategy some investors explore: buying the property in your personal name and then transferring it to your LLC or trust after closing via a quitclaim deed. Since you—a natural person, not an entity—made the initial purchase, it doesn't trigger the FinCEN reporting requirement.

How it works: You close on the property as "Jane Smith" rather than "Jane Smith, LLC." After closing, you execute a quitclaim deed transferring the property from yourself to your LLC. The original purchase—the one that would have been reportable—was made by an individual, so the RRE rule doesn't apply.

CRITICAL WARNINGS—Let's Be Real About the Risks Here:

Due-on-Sale Clause Violation: If you used a mortgage to purchase the property, transferring it to an LLC may trigger the "due-on-sale" clause in your loan agreement. This gives your lender the right to demand immediate repayment of the entire loan balance. Now, many lenders don't enforce this clause for transfers to single-member LLCs (especially if you keep making payments), but it's entirely within their legal right to do so. One phone call from your lender could quickly become a financial headache you didn't plan for.

Transfer Tax Exposure: Some states and municipalities impose transfer taxes whenever real property changes hands—even if it's simply from you to your own LLC. Depending on your jurisdiction, this could cost hundreds or even thousands of dollars—potentially more than you would have paid in FinCEN reporting fees in the first place.

Title Insurance Complications: Here's something many investors overlook: your title insurance policy was issued to you as an individual. When you transfer the property to an LLC, you may need to update or re-issue the policy to ensure your entity is properly covered. Some title companies charge a fee for this endorsement, and in worst-case scenarios, you could find yourself with a coverage gap if a title defect surfaces down the road.

Temporary Liability Exposure: Let's talk about one of the main reasons you set up an LLC in the first place—protecting your personal assets from liability. Here's the catch: from the moment you close until the moment the quitclaim deed is recorded, you own the property in your personal name. If a tenant, contractor, or visitor is injured on the property during this window—even if it's just a few days—you could be personally on the hook.

Lender Relationship Risk: Even if your lender doesn't immediately call the loan, violating the due-on-sale clause can sour your relationship with that institution. This could make it harder to secure financing for your next deal.

Our Strong Recommendation: Don't try this strategy without consulting both a real estate attorney and a CPA who understand your specific situation. The potential savings on a reporting fee simply aren't worth the legal and financial risks you'd be taking on.

Option 3: Qualify for an Entity-Level Exemption

The Corporate Transparency Act—the broader law that created the BOI reporting framework—includes 23 specific exemptions for certain types of entities that are already subject to substantial federal oversight. If your investment entity qualifies for one of these exemptions, you may be able to skip both the BOI report for your LLC and the RRE report for your property purchases.

Key Exemptions That May Apply to Real Estate Investors:

While most small to medium-sized real estate investment LLCs won't qualify, it's worth knowing what's out there. The CTA specifically sets forth 23 exemptions to its definition of reporting company, including:

Publicly Traded Companies: If your entity's securities are listed on a U.S. stock exchange (this likely doesn't apply to most real estate LLCs).

Banks and Credit Unions: Any entity chartered under federal or state banking laws and regulated by a federal banking agency.

Registered Investment Companies and Investment Advisers: Entities registered with the SEC under the Investment Company Act or Investment Advisers Act.

Venture Capital Fund Advisers: Investment advisers registered with the SEC and identified as exempt venture capital fund advisers on Form ADV.

Insurance Companies: State-licensed insurance companies or insurance producers.

Accounting Firms: Public accounting firms registered under the Sarbanes-Oxley Act.

Public Utilities: Entities providing telecommunications, electrical power, natural gas, or water services that are subject to state public utility commission regulation.

Tax-Exempt Entities: Organizations described in Section 501(c) of the Internal Revenue Code (keep in mind, most real estate LLCs are set up for profit, not as nonprofits).

Large Operating Companies: Here's the exemption that might catch your eye as a successful real estate investor, but fair warning—the bar is set pretty high. To qualify, your entity must check ALL of these boxes:

- More than 20 full-time employees in the United States. The exemption requires that the entity itself employ more than 20 full-time employees—not contractors, not part-time workers, and not employees of a management company you hire. We're talking W-2 employees on your entity's payroll.

- A physical office in the United States. A registered agent address or virtual office won't cut it here. You need a genuine, physical operating location.

- More than $5 million in gross receipts or sales reported on the previous year's federal income tax return, excluding receipts from sources outside the United States.

Subsidiaries of Exempt Entities: If your LLC is wholly owned by a company that already qualifies for an exemption (such as a large operating company or publicly traded parent), the subsidiary may also be exempt.

Let's Get Real for a Moment:

If you're running a small portfolio of rental properties—even if you own 10 or 20 units—you're almost certainly not going to hit that "Large Operating Company" bar. Most landlords work with property management companies rather than bringing on 20+ full-time employees directly. And while your rental income might climb past $5 million annually with a solid portfolio, checking both the employee and physical office boxes at the same time? That's pretty uncommon in our world.

Here's What This Means for You:

Unless your real estate business has evolved into a major operation with a sizable direct team, plan on your entity not qualifying for an exemption. In practical terms:

- You'll need to file a BOI report for your LLC (good news: you can handle this yourself at no cost).

- You'll keep seeing that FinCEN Reporting Fee pop up on settlement statements for non-financed purchases.

A Quick Heads-Up: If you think your entity might actually qualify for an exemption, make sure you document everything carefully. Your title company may ask for proof to waive the reporting fee, and you'll want that paperwork handy if FinCEN ever comes knocking.

The Bottom Line:

For most real estate investors, the FinCEN Reporting Fee is just another line item when purchasing properties through entities with non-bank financing. While the three options we covered offer potential ways around it, each brings its own hurdles or trade-offs. The smartest move for most of you? Accept the fee, get your information submitted quickly, and keep your focus where it belongs—finding and managing profitable real estate investments.

What Exactly Does This Fee Cover?

The FinCEN Reporting Fee covers the administrative work and legal responsibility that title companies now take on when handling reportable transactions. Here's what your money is actually going toward:

Data Collection and Verification: Your title company must identify every "beneficial owner" of your purchasing entity—that means anyone who owns 25% or more of the LLC or exercises substantial control over it. They need to collect full legal names, dates of birth, residential addresses, and copies of government-issued photo IDs for each owner. This information must be verified for accuracy, since errors can result in federal penalties.

Secure Technology Infrastructure: Title companies have invested in specialized software platforms and secure portals (many use systems like EagleID or similar compliance tools) to collect this sensitive personal information. These systems must meet strict cybersecurity standards to keep your data safe from breaches.

Five-Year Secure Storage: Federal regulations require title companies to maintain all collected beneficial ownership information in a secure, retrievable format for a minimum of five years. This isn't just filing away a PDF—it requires ongoing data security infrastructure, regular backups, and compliance with data protection standards.

Electronic Filing with FinCEN: The title company prepares and submits a detailed "Real Estate Report" to FinCEN's secure database. This report covers the property, the transaction, the reporting person, the seller, the purchasing entity, and all beneficial owners. The deadline? The last day of the month following closing or within 30 days—whichever comes later.

Legal Liability and Risk: Here's the big one. The title company takes on significant legal exposure by handling this reporting responsibility. If they miss a filing, file late, or submit inaccurate information, they're looking at federal penalties that can exceed $1,400 per day for negligent violations. Willful violations? Even steeper fines and potential criminal charges. Your fee helps cover their liability insurance and risk management costs.

![**Task:** Create a detailed infographic breaking down what the FinCEN Reporting Fee covers, showing five main components with icons and descriptions.

**Visual Structure:** Vertical layout with five horizontal sections, each containing an icon on the left and description text on the right, with a header at the top.

**ASCII Layout Reference:**

```

+----------------------------------------------------------+

| WHAT YOUR FEE COVERS: 5 KEY COMPONENTS |

+----------------------------------------------------------+

| [ICON] Data Collection & Verification |

| Identity verification for all beneficial owners |

+----------------------------------------------------------+

| [ICON] Secure Technology Infrastructure |

| Encrypted portals and compliance software |

+----------------------------------------------------------+

| [ICON] Five-Year Secure Storage |

| Maintained records with backup systems |

+----------------------------------------------------------+

| [ICON] Electronic Filing with FinCEN |

| Submission of detailed Real Estate Report |

+----------------------------------------------------------+

| [ICON] Legal Liability & Risk Coverage |

| Protection against $1,400+/day penalties |

+----------------------------------------------------------+

```

**Image Section Breakdown:**

- Header section:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772584436498_t5al3a.jpg?alt=media&token=585930d5-d09a-4ea6-b2a7-d386253f5594)

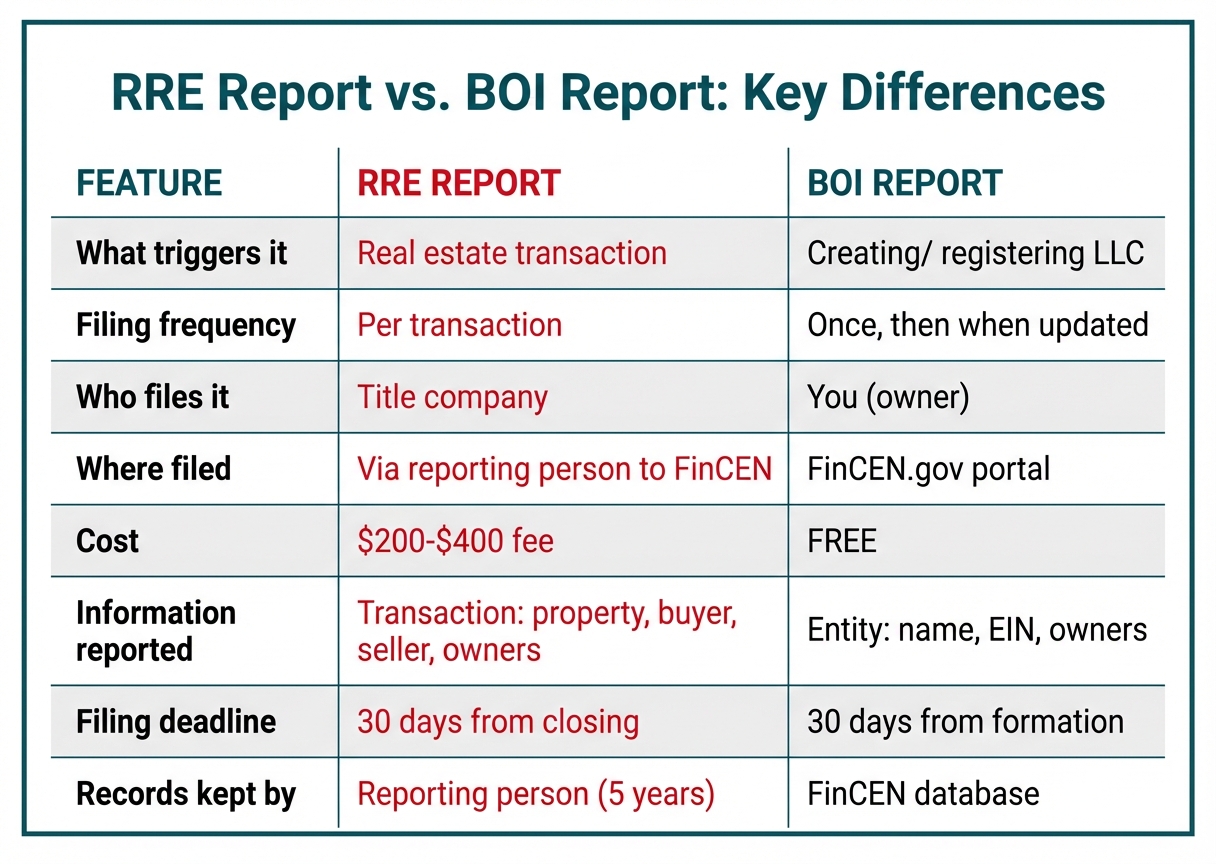

How This Differs from the BOI Report

Here's something important to keep straight: the FinCEN Reporting Fee on your settlement statement is completely separate from the Beneficial Ownership Information (BOI) report you may have filed (or still need to file) for your LLC with FinCEN.

The BOI report is an entity-level filing. You complete it once for your company and update it when ownership changes. You handle this yourself, directly with FinCEN, at no cost through their online portal.

The Real Estate Report (what your settlement statement fee covers) is transaction-specific. It gets submitted for each qualifying property purchase. Your title company files this one—not you—and it's tied to the specific property you just bought and the details of that particular closing.

Here's an easy way to remember it: The BOI report tells the government "who owns this LLC." The Real Estate Report tells them "this LLC just bought this specific property with cash, and here are the people behind it." " Both serve the government's goal of increasing transparency in business ownership and real estate transactions, but they're distinct compliance requirements with different filing parties and different purposes.

Here's the bottom line: The FinCEN Reporting Fee is simply part of doing business in the post-March 2026 regulatory landscape. Yes, it adds a few hundred dollars to your closing costs—but think of it as the cost of compliance with the federal government's new transparency requirements for non-financed entity purchases of residential real estate.

The "Why" Behind the Rule: FinCEN's War on Anonymous Real Estate Deals

Before we get into the nuts and bolts of the fee, let's talk about why this reporting requirement exists. This isn't red tape for the sake of red tape—it's a direct response to a real national security issue that's been quietly growing in American real estate for decades.

Who is FinCEN?

The Financial Crimes Enforcement Network—FinCEN for short—is a bureau within the U.S. Department of the Treasury. Since 1990, they've had one clear mission: protect our financial system from bad actors, fight money laundering, and strengthen national security by gathering and sharing financial intelligence.

Think of FinCEN as the government's financial detective squad. They don't make arrests, but they collect suspicious activity reports from banks, casinos, money service businesses, and—starting in 2026—certain real estate professionals. That intelligence then flows to law enforcement at every level, from local police tracking drug money to federal agents following terrorist financing trails.

For most of its existence, FinCEN kept its eyes on the usual suspects: banks, credit unions, and wire transfer services. Real estate? Despite being a massive piece of the American economic pie, it flew under the radar for years. That all shifted when investigators started connecting the dots between anonymous property purchases and some seriously bad actors.

The Problem: Why Real Estate is a Target for Money Laundering

Here's the deal: U.S. real estate has long been a favorite playground for money launderers worldwide. And when you break it down, the reasons make a lot of sense from a criminal's perspective:

Stable Asset Value: Unlike stocks or commodities that can tank overnight, real property—especially in hot markets like New York, Miami, Los Angeles, and San Francisco—tends to hold steady. A criminal can stash $5 million in dirty money into a Manhattan condo and feel pretty confident it'll still be worth $5 million (or more) down the road.

Appreciation Potential: But it gets better for the bad guys. U.S. real estate has historically gone up in value, meaning illicit funds don't just get "cleaned"—they actually grow. A luxury property snagged for $10 million with laundered cash might fetch $15 million five years later. That's legitimacy and profit rolled into one.

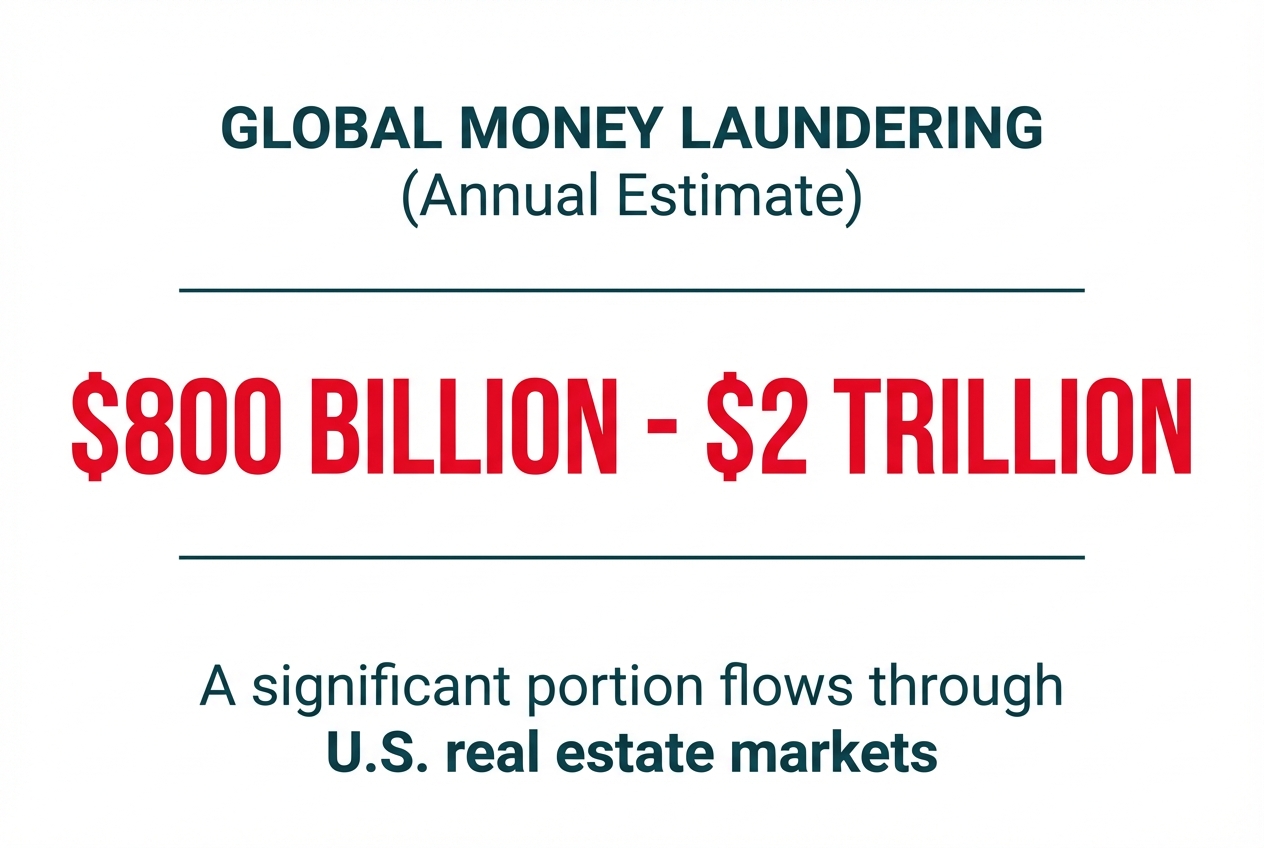

Previous Lack of Transparency: Here's where things really went sideways. For decades, there was zero federal requirement to identify who actually owned a property when it was purchased through a legal entity. A shell company—basically an LLC or trust with no real operations—could scoop up a $50 million penthouse, and all the public record would show is "123 Main Street Holdings LLC." The actual people behind that purchase? Complete ghosts.

This wasn't just some hypothetical concern. Investigative journalism has revealed that America's cities have been "bought up, bit by bit, by anonymous shell companies using piles of cash," with everything from modest single-family homes to luxury condos being snapped up by entities hiding their true owners. The scale of the problem is staggering: experts estimate that between $800 billion to $2 trillion are laundered globally every year, with a significant chunk flowing straight through real estate markets.

FinCEN's own advisories have documented cases where beneficial owners used networks of shell companies to receive millions in wire transfers, then turned around and used those funds to purchase U.S. property. These weren't just financial crimes—they were often connected to drug trafficking, human trafficking, corruption by foreign officials, and even terrorism financing.

Here's how simple the playbook was: A corrupt foreign official would steal money from their country's treasury, wire it through a series of shell companies in tax havens, then use a U.S.-based LLC (formed in a matter of hours online) to buy a luxury condo in Miami with cash. The property would sit empty or be rented out, and years later, it would be sold—with the proceeds now appearing as legitimate "real estate investment returns." Just like that, dirty money became clean.

The Solution: The Residential Real Estate (RRE) Rule

That's where the RRE Rule comes in. Effective March 1, 2026, this regulation represents FinCEN's most aggressive move yet to "pull back the curtain" on these anonymous transactions.

The rule is smartly targeted: it zeroes in on the specific type of transaction most associated with money laundering risk—all-cash purchases of residential property by legal entities. These deals have historically been the perfect storm of anonymity (entity ownership), liquidity (cash transactions), and value (residential real estate).

Here's the key takeaway: the goal is transparency, not prohibition. The government isn't saying you can't buy property through an LLC or with cash. What it's saying is: "If you're going to do this type of transaction that has historically been abused by criminals, we need to know who you actually are."

For legitimate real estate investors—which is the vast majority of you reading this article—the RRE Rule is more of an administrative inconvenience than a substantive burden. You were already planning to buy that rental property with your LLC. You were already planning to pay cash or use a private lender. The only difference now is that the title company will collect some additional information about you and file a report with the federal government.

But for the corrupt oligarch trying to hide stolen wealth, or the drug cartel looking to legitimize proceeds from illegal operations, this rule is a game-changer. The veil of anonymity that previously protected these bad actors is being pulled back, making U.S. real estate a far less attractive place to park dirty money.

Here's the bottom line: this regulation isn't designed to penalize you for using smart business structures or for paying cash. It's designed to close a loophole that has allowed some of the world's worst actors to exploit the American real estate market. If you're a law-abiding investor with nothing to hide, the RRE Rule simply formalizes information that you would likely have provided anyway in any professional transaction.

Common Questions, Pitfalls, and Important Distinctions

Myth vs. Fact: Can I Self-Report to Save the Fee?

Here's a question we hear all the time from investors: "Can I just file the Real Estate Report myself and skip that $200-$400 title company fee?" The short answer is no—and once you understand how FinCEN set up the rules, you'll see exactly why.

The Myth: "I can file this report myself on the FinCEN website, just like I do with my LLC's annual filings, and save hundreds of dollars at closing."

The Reality: FinCEN's Residential Real Estate Rule creates what's called a "reporting cascade"—a specific chain of professionals who are legally on the hook for filing. Notice we said professionals, not buyers. According to FinCEN's official guidance, responsibility falls to the first person on this list who's part of your transaction:

- The Settlement Agent (typically the title company or closing attorney)

- The person who prepares the settlement statement

- The person who files the deed of transfer

- The title insurance underwriter

Here's the key point: you, as the buyer (the "transferee"), aren't on this list. You're the subject of the report, not an authorized filer. Since the title company sits at the top of this cascade in nearly every professional closing, they're legally required to file. If they drop the ball, they—not you—face federal penalties that can top $1,400 per day for negligent violations, or even criminal charges for willful ones.

Why Title Companies Won't Let You Take Over:

Now, FinCEN's rule does allow for something called a "Designation Agreement" where parties on the cascade can shift responsibility to someone else on the list. But here's the catch—this doesn't extend to buyers. Title companies take on real legal and financial risk with this federal compliance duty. That fee you're paying covers more than just someone's time to file. It includes:

- Secure data collection and storage systems

- Liability insurance for handling your sensitive personal information

- The requirement to keep these records on file for five years

- Legal exposure if anything gets reported incorrectly

Bottom line: most title companies won't hand off this responsibility to an outside party (especially you, the buyer). Why? Because if you make a mistake or forget to file, the government still comes knocking on their door.

The $250 average fee is what they charge for assuming this risk on your behalf.

Critical Distinction: Real Estate Report (RRE) vs. Beneficial Ownership Information (BOI) Report

Here's where many investors get tripped up: these are two completely separate FinCEN reporting requirements. Yes, both involve reporting ownership information, but that's where the similarities end. Let's break down exactly how they differ—and why it matters for your wallet.

The Bottom Line: If you own an LLC that holds rental properties, you'll likely need to file both types of reports. Don't let this catch you off guard—now you know exactly what to expect. The BOI report is something you file yourself, once, for free, when you create your LLC. The RRE report is what the title company files (and charges you for) every time that LLC buys a property in a non-financed transaction.

Heads Up, Auction Buyers: Non-Judicial Foreclosures Need Your Attention

If you're an investor who loves snagging deals at foreclosure auctions, there's a new compliance wrinkle you need to know about under the FinCEN rule. Buying a residential property for cash on the courthouse steps through an LLC, trust, or other legal entity? That's a reportable event—but figuring out who actually files the report can get a little tricky.

Here's Where It Gets Complicated:

In traditional foreclosure sales—especially non-judicial foreclosures in states like Texas, Georgia, Arizona, and California—there's often no title company or settlement agent involved at the actual sale. Your process might look something like this:

- Show up to the auction with a cashier's check

- Win the bid

- Walk away with a Trustee's Deed or Sheriff's Deed

- Record that deed yourself (or have an attorney handle it)

See the problem? There's no "settlement agent" to take the lead on reporting. Under FinCEN's guidance, the responsibility rolls downhill to the next person in line—and that could very well be whoever files the deed of transfer. That might be you, your attorney, or a title company you bring in after the sale to sort out the title.

So What Does This Mean for You?

- You might be on the hook for reporting: If you or your attorney are the ones recording the deed with the county, you could be legally responsible for submitting the Real Estate Report to FinCEN within 30 days.

- The penalties are no joke: Miss the filing deadline and you're looking at civil penalties up to $1,416 per violation per day. Intentionally skip it? That could mean criminal charges.

- The report isn't exactly simple: According to Perkins Coie's analysis, the FinCEN Real Estate Report has 111 fields covering everything from transferee and transferor details to beneficial owners and transaction specifics.

Best Practices:

- Engage a title company post-auction: Even if you skip one for the initial purchase, bringing in a title company to handle the deed recording shifts the reporting responsibility to them. Yes, there's a fee involved, but it's often worth the peace of mind.

- Consult with a real estate attorney: Planning to make auctions a regular part of your investment strategy? Partner with an attorney who knows FinCEN compliance inside and out. They'll help you build a reliable process for staying on top of reporting deadlines.

- Don't assume exemptions apply: Here's a common trap: some investors think foreclosure sales get a pass from the RRE rule. They don't. Those "involuntary transfer" exemptions? They protect the seller (the foreclosed homeowner or lender), not you as the buyer.

Common Mistakes Investors Make (and How to Avoid Them)

Mistake #1: Waiting Until Closing to Gather Beneficial Owner Information

Picture this: you're days away from closing, and suddenly your title company fires off an urgent email demanding personal details and photo IDs for every beneficial owner of your LLC. Now you're chasing down business partners who might be traveling or simply not checking their phones. That's a recipe for closing delays.

Solution: The moment you go under contract, get ahead of it. Reach out to your title company and ask whether your transaction triggers FinCEN reporting. If it does, start collecting what you need right away: full legal names, dates of birth, residential addresses, and clear copies of government-issued IDs for anyone owning 25% or more of your entity or exercising substantial control.

Mistake #2: Assuming Your "Large" Investment Company is Exempt

FinCEN offers 16 exemptions from Beneficial Ownership Information (BOI) reporting, and some carry over to the Real Estate Report. The "large operating company" exemption trips up a lot of investors. To qualify, your entity needs:

- More than 20 full-time employees in the United States

- A physical office in the U.S.

- More than $5 million in gross receipts or sales reported on the previous year's federal tax return

Here's what we see all the time: mid-sized real estate investment firms assume they're in the clear, but they often miss the mark on one of these three criteria. The usual culprits? Employee count or the physical office requirement.

Solution: Skip the guesswork on your exemption status. Have your CPA or attorney review the full list of exemptions against your entity's structure and operations. If you do qualify, give your title company written notice before closing so they can remove the fee from your settlement statement.

Mistake #3: Confusing "Non-Financed" with "No Mortgage"

Some investors think that as long as they're steering clear of a traditional bank mortgage, they can get creative with their financing and sidestep the reporting requirement. This leads to strategies like:

- Using a line of credit from a non-bank lender

- Structuring the deal as a "lease with option to purchase" followed by a cash-out

- Having a business partner "lend" them the money with a promissory note

The Reality: FinCEN defines "non-financed" as any transfer that doesn't involve a loan from a financial institution subject to federal anti-money laundering (AML) program requirements. We're talking traditional banks, credit unions, and federally regulated mortgage companies. Private lenders, hard money lenders, and even sophisticated financing structures like seller carrybacks? They all count as "non-financed" for reporting purposes.

Solution: If avoiding the reporting requirement matters to you, your only reliable path is using a loan from a traditional, federally regulated lender. Even then, check with your lender to confirm they're subject to the Bank Secrecy Act's AML requirements.

Mistake #4: Ignoring the 30-Day Deadline

The Real Estate Report must be filed within 30 calendar days of the closing date. Yes, this deadline falls on the title company—not you. But here's the thing: if you're slow getting them your information, you could push them past this window. That means penalties for them and potentially a strained relationship that could affect your future deals.

Solution: Treat the title company's information requests with the same urgency as you would a lender's underwriting conditions. Respond within 24-48 hours, and double-check that all information is accurate before submitting it.

Conclusion: Adapting to the New Normal of Real Estate Compliance

The FinCEN Residential Real Estate reporting fee isn't going away—it's simply part of doing business now for real estate investors who use entities to purchase property with non-traditional financing. As of March 1, 2026, this federal compliance requirement has changed the closing process for all-cash entity transactions, adding both a line item to your settlement statement and a new layer of due diligence to your investment strategy.

The Bottom Line: This Fee is Legitimate and Unavoidable

For transactions that meet all four criteria—residential property, purchased by an entity or trust, using non-financed funds, with no applicable exemptions—the reporting requirement is mandatory under federal law. The $200-$400 fee you're seeing from title companies reflects the real administrative burden, technology costs, secure data storage requirements, and legal liability they take on by serving as the designated "Reporting Person" under FinCEN's Residential Real Estate Rule.

This isn't a discretionary charge or a "nice-to-have" service. It's a federally mandated compliance obligation with serious penalties for non-compliance—including fines exceeding $1,400 per day and potential criminal charges for willful violations. Your title company isn't padding their profits with this fee; they're protecting themselves (and you) from federal enforcement action.

Actionable Steps for the Prepared Investor

The most successful real estate investors will be those who treat this new requirement as just another part of professional property acquisition. Here's how to stay ahead:

Before You Make an Offer:

- Review your entity structure with your attorney and CPA to determine if any of the 16 exemptions apply to your investment vehicle

- Know which of your planned transactions will trigger reporting (and which won't)

- Factor the reporting fee into your acquisition costs and underwriting models

- Consider whether traditional financing or individual ownership might work better for your specific deal

During Due Diligence:

- Gather the required documentation for all beneficial owners of your entity before you go under contract

- Make sure you have current, non-expired government-issued photo IDs for everyone who owns 25% or more of the buying entity

- Verify that your entity's formation documents clearly identify all individuals who exercise "substantial control"

- Update your LLC operating agreement or trust documents if ownership structures have changed since formation

At Closing:

- Respond right away when your title company sends the information collection portal link

- Provide complete, accurate information the first time to avoid delays

- Don't wait until the day before closing to submit your beneficial ownership data

- Ask questions early if you're unsure about any aspect of the reporting requirement

After Closing:

- Keep copies of the information you provided for your own records

- Remember that this is separate from your entity's BOI report (which you still need to file directly with FinCEN for free)

- Update your standard operating procedures to include RRE compliance as a routine part of your acquisition checklist

What's Next: Enforcement and Evolution

While the rule officially took effect on March 1, 2026, enforcement patterns are still emerging. FinCEN has historically focused its enforcement efforts on willful violations and patterns of non-compliance rather than isolated, good-faith mistakes. However, as the agency builds its database and refines its analytical capabilities, we can expect:

- Increased scrutiny of repeat filers: Investors who close multiple transactions may face additional review if patterns suggest potential structuring or evasion

- Enhanced data matching: FinCEN will likely cross-reference Real Estate Reports with BOI filings, tax records, and other government databases to identify discrepancies

- Evolving exemptions: As the rule is implemented, FinCEN may issue additional guidance clarifying edge cases or expanding exemptions based on industry feedback

- Technology improvements: The reporting portal and processes will likely become more streamlined as title companies and FinCEN gain experience with the system

The Opportunity in Adaptation

Here's what sets successful investors apart: they don't fight change—they adapt to it. Regulations shift, markets move, and new compliance requirements pop up. The investors who win are the ones who see these changes as the new standard for doing business professionally.

The FinCEN reporting requirement actually works in your favor if you're already running a tight ship with proper entity structures, organized documentation, and trusted advisors on your team. While other buyers scramble to gather information at the last minute and deal with closing delays, you'll breeze through because compliance is already baked into how you operate.

And here's a bonus: increased transparency in residential real estate makes it tougher for bad actors to use dirty money to compete for properties. A cleaner market is a more predictable market—and that's good news for investors who are in it for the long haul.

Your Next Steps

Don't let this new requirement throw you off your game or slow down your investing momentum. Instead:

Educate yourself: You've taken the first step by reading this guide. Share it with your team, your partners, and your advisors.

Audit your entities: Review your current LLC and trust structures to ensure they're properly documented and that beneficial ownership is clear.

Build your compliance toolkit: Create a folder (digital or physical) with copies of all beneficial owners' IDs, entity formation documents, and EIN letters so you're always ready to respond to title company requests.

Strengthen your professional network: Work with title companies, attorneys, and CPAs who understand the RRE rule and can guide you through complex scenarios.

Stay informed: Subscribe to updates from FinCEN, your state's real estate commission, and industry organizations to stay ahead of any changes or clarifications to the rule.

The real estate investment world looks different now, but here's the good news: the core principles of building wealth through property haven't changed one bit. Buy smart, manage wisely, and run your business like a pro. Think of the FinCEN reporting requirement as just another tool in your professional toolkit—and now you know exactly how to use it.

Welcome to the new era of transparent real estate investing. You've got this.

OfferMarket Loans

Check your rate

60 seconds · no credit pull