*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loan Requirements at OfferMarket

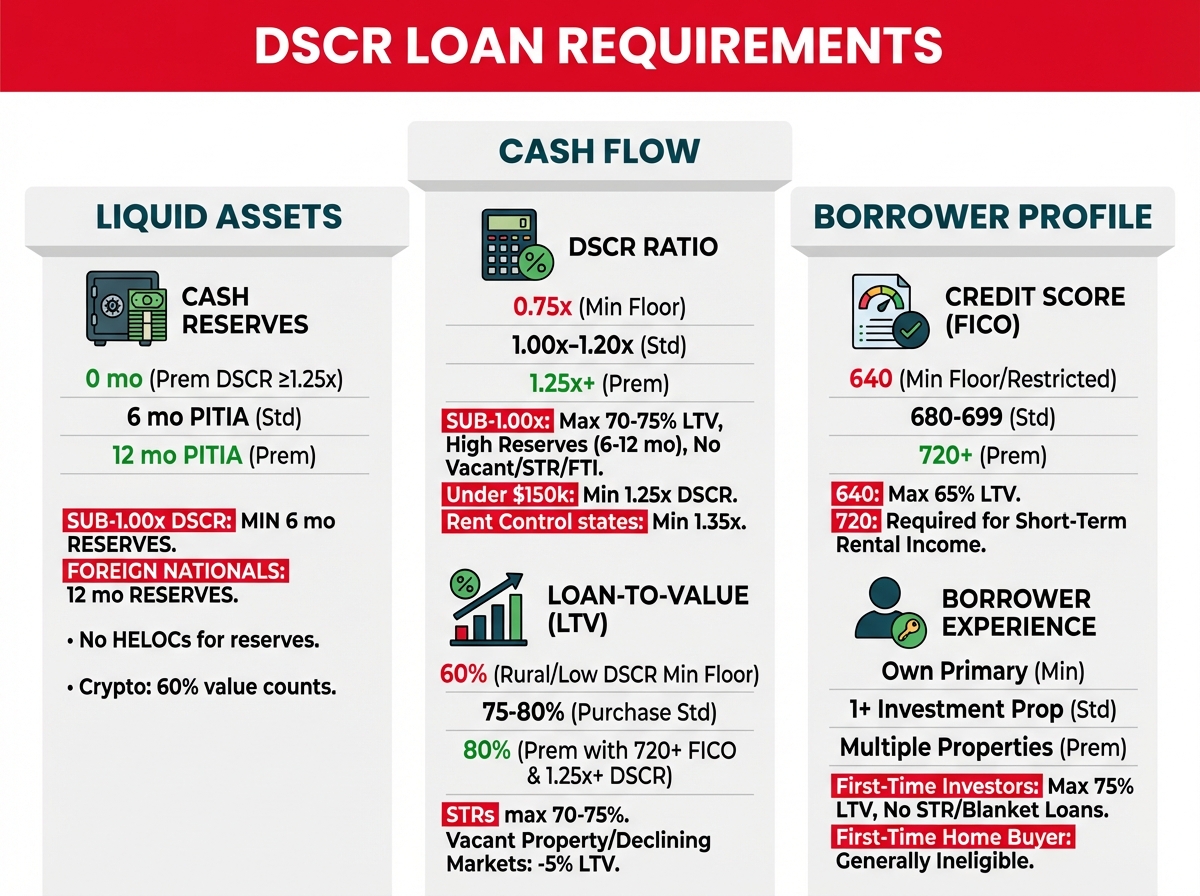

Before we break down each requirement, let's give you the full picture in one place. This table lays out everything you need to know—credit score tiers, DSCR minimums, leverage limits, reserve requirements, and eligibility restrictions—across all major DSCR loan programs.

| Requirement Category | Minimum Threshold | Standard Tier | Premium Tier | Penalties & Restrictions |

|---|---|---|---|---|

| Credit Score (FICO) | 640 (Absolute Floor) | 680-699 | 720+ | • 640: Max 65% LTV, severely restricted • 680: Access to 75-80% LTV standard programs • 720: Required for Short-Term Rental income • 740: Required for cash-out on vacant renovated properties |

| DSCR Ratio | 0.75x (Absolute Minimum) | 1.00x-1.20x | 1.25x+ | • 0.75-0.99x: Max 70-75% LTV, 6-12 month reserves required, no STR income, no first-time investors • Sub-1.00x: Cannot be vacant/unleased, cannot be rural • 1.25x: Required for loan amounts under $150k • 1.35x: Required in rent control states |

| Loan-to-Value (LTV) | 60% (Foreign Nationals) | 75-80% (Purchase/R&T) 65-70% (Cash-Out) |

80% (720+ FICO, 1.25x+ DSCR) | • First-time investors: Max 75% LTV • Sub-1.00x DSCR: Max 70-75% LTV • Vacant properties: -5% LTV reduction • STRs: Max 70-75% LTV • Declining markets: -5% LTV reduction • Rural properties: Max 65% LTV |

| Cash Reserves | 0 months (DSCR ≥1.25x) | 6 months PITIA | 12 months PITIA | • Sub-1.00x DSCR: Minimum 6 months required • Foreign Nationals: 12 months required • STRs with lower DSCR: 6-12 months • Cannot use HELOCs for reserves • Crypto: Only 60% of value counts (if allowed) |

| Credit Depth | 3 tradelines (12+ months) OR 2 tradelines (24+ months) |

3+ tradelines (12+ months) | 4+ tradelines (24+ months) | • 0x30x12: No mortgage lates in last 12 months • Collections/Judgments: Must be paid at closing (except medical <$2k) • BK/FC/Short Sale: 36-48 month seasoning required |

| Borrower Experience | Must own primary residence | 1+ investment property (12+ months) | Multiple properties | • First-time investors: Max 75% LTV, no STR income, no blanket loans • First-time home buyers: Generally ineligible • Experienced investors: Full program access |

| Property Type | 1-4 Unit Residential | 1-4 Unit + STR | 5-10 Unit Multifamily | • 5-9 units: 1. 15x minimum DSCR • STRs: 720+ FICO, 1.00-1.25x DSCR, 20% expense haircut • Rural: Max 65% LTV, purchase only, no STR income • Condos (FL): Milestone inspection if 30+ years old (25+ if coastal) |

| Property Condition | C1-C4 (Lease Ready) | C1-C3 | C1-C2 | • C5-C6: Ineligible until repairs completed • No escrow holdbacks allowed • Unpermitted ADUs: Income excluded without comps |

| Residency Status | US Citizen/Permanent Resident | US Citizen/Permanent Resident | US Citizen | • Foreign Nationals: 60-65% max LTV, 12-month reserves, funds seasoned 30-60 days • Non-Permanent Resident Aliens: Valid visa + US credit required • ITIN: Generally ineligible |

| Entity Structure | Individual/Domestic LLC | Domestic LLC (Good Standing) | Domestic LLC (Good Standing) | • 20-25%+ owners must personally guarantee • Guarantors need 51%+ aggregate ownership • Background checks required (no financial crimes in 10 years) • Layered LLCs: 25% ownership through all levels • Trusts cannot be LLC members |

| Occupancy Status | Leased (Active Lease) | Leased or Market Rent | Leased or Market Rent | • Vacant on Refi: -5% LTV, only 75-90% of market rent counts • Purchase: 100% of market rent allowed |

| Loan Amount | $75,000 | $100,000-$2,000,000 | $150,000+ | • Under $150k: 1.25x minimum DSCR required • Over $2M: Program-specific requirements |

Here's the key takeaway from OfferMarket's comprehensive guide: these requirements don't exist in isolation—they work as a complete system. If you're lighter in one area (say, a lower credit score), you'll typically need to bring more strength somewhere else (like a higher DSCR or bigger down payment).

How to Use This Table

- Start with your credit score – This sets your baseline eligibility and determines how high your LTV can go

- Calculate your property's DSCR – Use our DSCR loan calculator which will guide you through the process

- Identify your borrower experience level – If you're a first-time investor, this will shape your options more than you might expect

- Check for property-specific restrictions – STRs, rural locations, and vacant properties come with their own set of limitations

- Determine required reserves – Your DSCR and property type will tell you what you need to have set aside

Here's the key takeaway from this table: DSCR loan requirements work as a team. You can't just nail one requirement and call it a day. Got a solid 720 credit score but a 0.80x DSCR? Expect tighter LTV caps and higher reserve requirements. Sitting pretty with a 1.40x DSCR but a 650 credit score? Your credit tier will still hold you back.

Coming up, we'll walk you through exactly how these requirements play together, the common pitfalls that can derail your deal, and smart strategies to position your application for the best possible terms and approval chances.

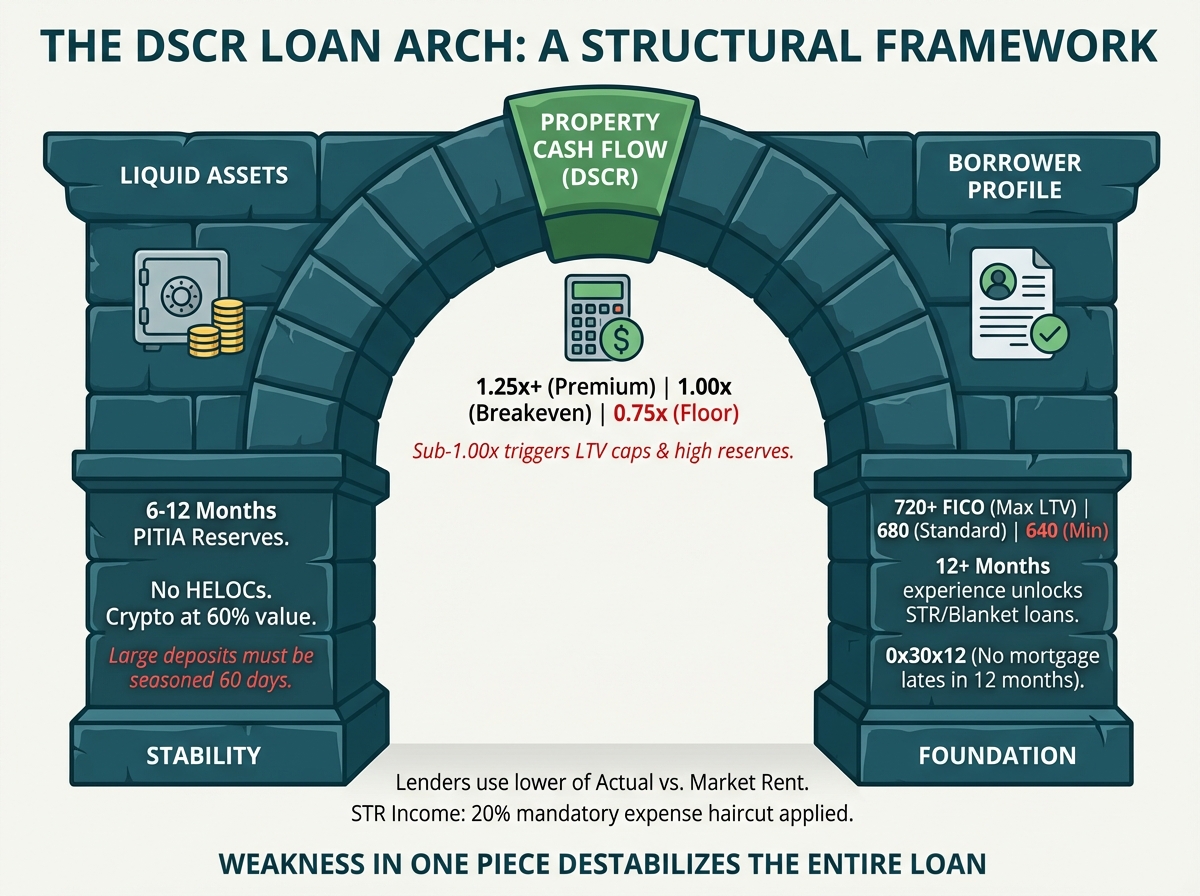

The "Structural Integrity" of DSCR Loan Requirements

Picture DSCR loan requirements like an architectural arch—a time-tested structure that works because every piece supports the others. Weaken one element, and the whole thing comes down. This isn't just a helpful visual; it's exactly how lenders look at your DSCR loan application.

Here's what makes DSCR loans different: instead of focusing on your W-2 income and job history like traditional mortgages, DSCR loans zero in on what the property itself can earn. That's a whole different ballgame. The arch model shows you why lenders look at three connected pieces: your property's cash flow (the keystone at the top), your liquid assets (supporting one side), and your borrower profile (supporting the other).

Cash Flow: The Keystone That Holds Everything Together

At the center of the arch sits the keystone—the wedge-shaped stone that locks all other pieces in place. In DSCR lending, that keystone is your property's cash flow, measured by the Debt Service Coverage Ratio itself.

The DSCR metric shows lenders whether you can repay your loan based on what your property brings in each month. The math is straightforward: divide your gross rental income by your total monthly debt obligations (Principal, Interest, Taxes, Insurance, and Association fees—PITIA). A DSCR of 1.25x means your property brings in $1.25 for every $1.00 you owe in debt service.

This ratio isn't pulled out of thin air. Lenders set minimum DSCR thresholds because they need confidence that your property can carry its own weight—with breathing room for vacancies, repairs, and market shifts. The absolute floor across most programs is 0.75x, but expect steep trade-offs at that level. At 1.00x, your property breaks even each month. The sweet spot? Most competitive programs want to see 1.25x or higher before they'll offer you maximum leverage and the best terms.

When your DSCR dips below 1.00x—meaning your property loses money each month—the whole loan structure gets shaky. Lenders will tighten up: expect a lower maximum loan-to-value ratio (often capped at 65-70% LTV), bigger cash reserve requirements (typically 6-12 months of PITIA), and restrictions on using short-term rental income or refinancing vacant properties. Your keystone has cracked, and other parts of the structure need to pick up the slack.

Here's a trap that catches many investors off guard: the "Actual vs. Market Rent Trap." If your property has a tenant, lenders use the lower of your actual lease amount or the appraiser's market rent estimate. So if you're collecting $2,500 monthly but market rent comes in at $2,200, your DSCR calculation uses $2,200—no matter what your tenant actually pays you. This single miscalculation can drop your DSCR from 1.30x to 1.15x, potentially costing you 5% in leverage or triggering additional reserve requirements.

Short-term rental properties face even tougher standards. Lenders apply a mandatory 20% expense haircut to your gross Airbnb or VRBO revenue to account for cleaning, management, and marketing costs. So if your property brings in $60,000 annually in STR income, lenders only credit you with $48,000 ($60,000 × 80%) when calculating your DSCR. On top of that, STR properties typically require a minimum 1.15x to 1.25x DSCR—quite a bit higher than the 1.00x standard for traditional rentals.

Assets: The Left Abutment Providing Financial Stability

The left side of our arch represents your liquid assets—the cash reserves that act as your safety net when rental income hits a rough patch. Just as an abutment must be strong enough to handle the arch's lateral thrust, your reserve position needs to be solid enough to carry you through vacancies, major repairs, or tenant defaults.

Most DSCR programs require 6 to 12 months of PITIA in liquid, verifiable reserves. This isn't money you'll necessarily spend at closing—it's proof that you can keep the property running through tough times. For a property with a $3,000 monthly PITIA, you'd need $18,000 to $36,000 in accessible funds.

Here's where it gets tricky: the definition of "acceptable reserves" is stricter than most investors realize. Funds must be fully liquid and verifiable through standard bank statements, retirement account statements, or investment account statements. A Home Equity Line of Credit (HELOC) won't cut it for reserve requirements, even if you have plenty of available credit. Cryptocurrency? That's heavily restricted—some programs accept Bitcoin or Ethereum if verified through Coinbase within 30 days of closing, but they'll only credit you with 60% of the current value to cushion against volatility.

One more thing to keep in mind: the reserve requirement scales with risk. If your DSCR falls below 1.00x, lenders automatically trigger a minimum 6-month reserve requirement, no matter how strong your credit score or how much experience you have. Foreign national borrowers face a mandatory 12-month reserve requirement, even with a strong DSCR. First-time investors purchasing properties in declining markets may see reserve requirements increase to 12 months as well.

Here's a critical trap many investors stumble into: the "Source and Seasoning" requirement. Large deposits that show up in your bank accounts within 60 days of closing must be fully documented and explained. If you sell stocks, receive a gift, or transfer money between accounts, you'll need to provide a complete paper trail. Cash deposits—even from legitimate sources—are nearly impossible to document acceptably. If you're planning to use recently liquidated assets for your down payment or reserves, make sure those funds are deposited and seasoned in a U.S. bank account at least 60 days before you apply.

Some capital providers require "Interest Reserves at Closing"—essentially prepaying 3 months of mortgage interest upfront. While this money ultimately covers your first few mortgage payments, it increases your cash-to-close by thousands of dollars and must be factored into your liquidity calculations.

Borrower Profile: The Right Abutment Demonstrating Creditworthiness

The right side of our arch represents you—the borrower. Your credit history, score, and investment experience form the foundation that supports the entire lending structure.

Here's the deal: DSCR loans demand higher credit quality than conventional mortgages precisely because lenders aren't verifying your employment income. The absolute floor is a 640 FICO score, but this severely limits your options, often capping leverage at 65% LTV. The sweet spot is 680 FICO, which unlocks most programs at 75-80% LTV. Want premium pricing and maximum leverage? You'll need a 720+ FICO.

But credit score alone won't cut it—lenders examine credit depth and recent payment history with surgical precision. You'll need at least 3 tradelines reporting for 12+ months, or 2 tradelines reporting for 24+ months. These tradelines must show active, responsible credit management—authorized user accounts and closed accounts don't count toward the minimum.

The "0x30x12" rule is set in stone: you can't have any 30-day late payments on any mortgage or rental payment history in the last 12 months. Even a single late mortgage payment—even if you've caught up since—will result in an automatic decline or mean you'll need to wait until that mark falls outside the 12-month window.

Major credit events like bankruptcies, foreclosures, or short sales need to be fully seasoned (discharged or completed) for 36 to 48 months, depending on the program. Collections and judgments must be paid in full before or at closing, with exceptions only for medical collections or combined balances under $2,000.

The "Borrower Experience" factor creates two distinct paths. If you don't qualify as an "Experienced Investor"—typically meaning you've owned at least one investment property for 12+ months—you're considered a first-time investor and will face some real limitations:

- Maximum leverage capped at 75% LTV

- No ability to use short-term rental income

- No access to cross-collateralized (blanket/portfolio) loans

- Must already own a primary residence

If you've never owned any property (making you a "First-Time Home Buyer"), DSCR loans are generally off the table entirely.

When you have multiple guarantors on a loan, lenders typically look at the lowest representative credit score (the middle score from three bureaus) among all of them. So if you're partnering with someone who has great cash reserves but a 650 FICO score, their credit profile will pull down the entire application, pushing you into a lower LTV tier or higher interest rate.

How the Arch Fails: Understanding Structural Collapse

The arch analogy really clicks when you see how weakness in one area puts extra pressure on the others—or brings the whole structure down.

Scenario 1: Weak Keystone (Low DSCR) If your property's DSCR comes in at only 0.85x, lenders will look for stronger support elsewhere. Your maximum LTV drops to 70%, meaning you'll need a larger down payment (a stronger asset position). Reserve requirements increase to 12 months (stronger asset position). And if your FICO is below 720, you may be declined entirely (weak borrower position cannot compensate for weak cash flow).

Scenario 2: Weak Left Abutment (Insufficient Reserves) Here's the deal: if you've only got 3 months of reserves when 6 are required, lenders simply can't approve your loan—even with a stellar 1.50x DSCR and a 780 credit score. The imbalance is just too risky. Your move? Either bulk up those reserves or reduce your loan amount (which lowers your monthly PITIA and brings down the reserve requirement).

Scenario 3: Weak Right Abutment (Poor Credit or First-Time Investor) First-time investor with a 680 FICO? You're automatically capped at 75% LTV, no matter how strong your DSCR or reserves look. Your borrower profile just can't support higher leverage yet. The path forward: strengthen that right abutment by gaining investment experience (buy a property and hold it for 12 months) or boost your credit score above 720.

The arch model reveals exactly why DSCR loans demand a holistic evaluation. Lenders aren't simply checking boxes—they're stress-testing the structural integrity of your entire financial picture against the property's income potential. Master this framework, and you'll pinpoint your weakest link and strategically strengthen it before applying. The result? Better approval odds and more favorable terms.

Understanding DSCR: The Keystone of Your Loan Structure

The Debt Service Coverage Ratio (DSCR) is hands-down the most critical metric in determining your loan eligibility and terms. The calculation itself is simple: Gross Rents ÷ PITIA (Principal, Interest, Taxes, Insurance, and HOA fees). This ratio shows lenders whether your property generates enough income to cover its debt obligations—and by how much.

But don't let that simple formula fool you. Beneath it lies a complex web of thresholds, penalties, and edge cases that can dramatically shift your loan terms or even disqualify your deal entirely.

The DSCR Threshold Hierarchy

DSCR loans work on a tiered system where your ratio determines not just approval, but your maximum leverage, reserve requirements, and eligible property types. Let's break down what each level means for you:

0.75x – The Absolute Floor

This is the lowest DSCR most programs will accept. At this level, your property is running at a monthly loss, and lenders see it as a bet on future appreciation or rent growth. Here's what to expect: leverage typically caps at 65% LTV, you'll need 6-12 months of PITIA in cash reserves, and you won't be able to use short-term rental income, purchase rural properties, or qualify as a first-time investor.

1.00x – The Break-Even Benchmark

A DSCR of exactly 1.00x means your rental income covers your debt service dollar for dollar—no profit, no loss. While this meets the minimum for most programs, lenders still apply conservative underwriting. You'll see reduced LTV caps (typically 70-75% for purchases), mandatory reserve requirements, and restrictions on property type and borrower experience.

1.25x – The Sweet Spot

This is where DSCR loans really start working in your favor. A 1.25x ratio means your property brings in 25% more income than you need to cover debt service—giving you a healthy buffer for vacancies and surprise repairs. This threshold is required for smaller loan amounts under $150,000 and opens the door to competitive rates and terms for most investors. According to JP Morgan's analysis of commercial real estate lending, lenders typically require DSCR minimums between 1.20x and 1.25x to ensure solid cash flow coverage.

Higher Thresholds for Specialized Scenarios

Certain property types and loan structures call for even stronger coverage ratios. Portfolio loans require a minimum 1.05x DSCR, while 5-10 unit multifamily properties need at least 1. 15x. If your FICO score falls below 720, expect a 1.20x minimum. Properties in rent-controlled states require 1.35x to account for limited rent growth potential.

The Sub-1.00x Penalty Structure

Operating below a 1.00x DSCR—meaning your property loses money each month—comes with some significant hurdles. Here's what you need to know about how lenders protect themselves (and what it means for your deal):

Leverage Restrictions

Your maximum LTV takes a hit. For purchase and rate-term refinances, you're typically looking at 70-75% LTV caps. Cash-out refinances? Even tighter at 65-70% LTV, depending on your credit score. Bottom line: plan on bringing more cash to the closing table.

Mandatory Reserve Requirements

You'll need to show liquid reserves covering at least 6 months of PITIA payments. Higher-risk profiles may face 12-month requirements. Keep in mind: HELOCs and retirement accounts with early withdrawal penalties don't count here.

Total Exclusions

At sub-1.00x DSCR, certain doors simply close. Short-term rental income won't qualify. Vacant property refinances are off the table. Rural properties and first-time investors are excluded. Lenders draw these hard lines because negative cash flow combined with additional risk factors just doesn't pencil out for them.

The Actual vs. Market Rent Trap

Here's something that catches many investors off guard: how lenders calculate "Gross Rents." When your property has a tenant, lenders use the lesser of your actual lease amount or the appraiser's market rent estimate from Form 1007.

Let's walk through a real example: Say your tenant pays $2,500/month, but the appraiser pegs market rent at $2,200/month. Your DSCR gets calculated using $2,200—not what you're actually collecting. That 12% haircut could drop you from a solid 1.30x DSCR to 1.16x, potentially bumping your rate or reducing your leverage.

The flip side of this equation creates its own challenges. If your actual lease is $2,800 but market rent is $2,200, lenders will generally cap allowable rent at 120% of market average ($2,640). You'll need to show you've consistently collected this above-market rent for 2-3 months through bank statements with verified deposits.

Vacant Property Penalties

Refinancing an unleased property comes with automatic penalties that account for lease-up risk and potential vacancy periods. Here's what you need to know:

The 75% Rent Credit

Rather than using 100% of the appraiser's projected market rent, lenders will only credit you with 75% of that amount in your DSCR calculation. So if market rent is $2,000/month, your qualifying income drops to $1,500/month—a 25% reduction that can seriously impact your ratio.

Some programs offer a bit more flexibility, allowing 90% of market rent, but that's still a meaningful reduction. Good news: this penalty typically applies only to refinances. Purchase transactions generally allow 100% of market rent since you're buying at current market value.

The 5% LTV Reduction

Here's where it gets tougher. On top of the rent credit reduction, vacant properties face a mandatory 5% decrease in maximum LTV. If you would normally qualify for 80% LTV, you're now capped at 75%. When you combine this with the rent credit penalty, vacant refinances require more capital and become more expensive overall.

Short-Term Rental Income Haircuts

Using Airbnb or VRBO income to qualify? This is where DSCR lending gets the most complex:

The 20% Expense Factor

Lenders understand that short-term rentals come with higher operating costs than traditional leases. To account for cleaning, marketing, management fees, and higher vacancy rates, they apply a mandatory 20% expense haircut to your gross revenue. According to DSCR loan specialists at Kiavi, this calculation takes your 12-month historical revenue (or AirDNA projected revenue for purchases) and multiplies it by 80% before dividing by PITIA.

For example, if your property generates $60,000 in annual STR revenue, your qualifying income becomes $48,000—a $12,000 reduction that directly impacts your DSCR calculation.

The 60% Occupancy Minimum

For purchase transactions using AirDNA projections, the report must show a minimum 60% occupancy rate. If your target market has seasonal swings or inconsistent booking patterns, you may not hit this threshold—and that means STR income won't count at all.

The 720 FICO Requirement

Here's a big one: you'll need a credit score of 720 or higher to use short-term rental income. That's a notable step up from the standard 680 FICO benchmark, which means a good number of investors simply won't qualify for this option.

Elevated DSCR Minimums

STR properties typically need DSCR ratios between 1.00x and 1.25x depending on the lender—higher than the 0.75x floor you'd see with traditional rentals. Pair that with the 20% expense haircut, and your property needs to pull in significantly more revenue to make the cut.

Leverage Reductions

Even when you check all the other boxes, STR properties come with a 5% LTV reduction from standard guidelines and are often capped at 70-75% maximum LTV. Bottom line? You'll need more cash at closing compared to a traditional rental bringing in the same revenue.

First-Time Investor Prohibition

If you haven't owned at least one investment property for 12+ months, short-term rental income is off the table for qualification purposes. It doesn't matter how strong your DSCR looks—this is a hard rule that creates a real barrier for newer investors trying to break into the STR space with DSCR financing.

Getting familiar with these calculation details and penalty structures is key to putting together deals that actually make it to the finish line. Whether it's choosing actual vs. market rent or accounting for the STR expense haircut, these details can be the difference between locking in great terms and getting a flat-out denial.

Cash Reserve Requirements: The Safety Net Lenders Demand

Think of cash reserves as your financial backup plan—the cushion lenders want to see so they know you can handle vacancies, surprise repairs, or market dips. With conventional mortgages, reserve requirements might be minimal or even waived. But DSCR loans? They require substantial liquid assets because there's no personal income verification in the picture.

Standard Reserve Requirements

Here's the deal: most DSCR lenders want you to have 6 to 12 months of PITIA (Principal, Interest, Taxes, Insurance, and Association dues) sitting in verified liquid reserves. Your exact number depends on a few key factors:

- Credit score tiers: Better credit can mean lower reserve requirements

- DSCR ratio: Properties with sub-1.00x DSCR automatically trigger minimum 6-month reserve requirements

- Loan-to-value ratio: More leverage usually means more reserves needed

- Borrower experience: New to investing? Expect stricter reserve mandates

- Property type: Short-term rentals and multi-unit properties often require additional reserves

According to industry standards, many lenders prefer reserves equal to 3-6 months of PITIA payments as a best practice, though requirements can stretch to 12 months for riskier profiles.

What Qualifies as Acceptable Reserves

Not all assets are created equal in the eyes of lenders. Here's what counts—and how much credit you'll get:

Fully Acceptable Assets (100% Credit)

- Checking and savings accounts in U.S. FDIC-insured institutions

- Money market accounts

- Certificates of deposit (CDs), though early withdrawal penalties may apply

- Verified stocks, bonds, and mutual funds in brokerage accounts

- Retirement accounts (401(k), IRA, SEP-IRA) with 60% to 70% of the vested balance counted due to potential tax penalties and early withdrawal fees

Partially Acceptable Assets (Discounted Value)

- Cryptocurrency holdings verified through Coinbase within 30 days of the Note date receive only 60% credit of current valuation to account for extreme volatility

- Business accounts may be acceptable but often require additional documentation proving the funds won't disrupt business operations

Critical Reserve Exclusions

Here's where things get strict. Several common asset types are completely off the table for reserve requirements:

Absolutely Ineligible

- Home Equity Lines of Credit (HELOCs): You cannot use an existing HELOC to satisfy cash-to-close or reserve liquidity requirements, HELOAN proceed however are fine.

- Borrowed funds: Personal loans, credit card cash advances, or any debt-based liquidity

- Unseasoned cryptocurrency: Virtual currency used for earnest money deposits or that hasn't been converted to U.S. dollars in a U.S. institution

- Pledged assets: Any funds you've already put up as collateral for another loan

- Non-liquid retirement accounts: Pensions you can't touch without leaving your job

Seasoning Requirements Here's something that catches many investors off guard: large deposits that pop up suddenly in your accounts will raise red flags. Most lenders want to see:

- 30 to 60 days of seasoning for any large deposits (we're talking deposits that exceed 25% of your monthly income or total reserves)

- A complete paper trail for gifts, inheritances, or when you've sold off assets

- Written explanations for any unusual financial activity

Special Requirements for Foreign Nationals

If you're a foreign national borrower, expect stricter reserve requirements—lenders see additional risk here, and the numbers reflect that:

- Minimum 12 months of PITIA reserves (that's double what domestic borrowers need)

- Maximum 60% to 65% LTV no matter how strong your credit looks

- Your funds must be converted to USD and sitting in a U.S. FDIC-insured bank account

- 30 to 60 days of seasoning required for all funds in your U.S. account before you close

- Valid passport and visa documentation (when applicable)

- U.S. credit history is strongly preferred, though some programs will work with foreign credit reports if they're translated

Interest Reserves at Closing: The Hidden Cash Requirement

Here's one that surprises a lot of investors: some capital providers require an interest reserve at closing. This means you'll need to bring 3 months of interest payments upfront to the closing table.

How It Works

- The lender collects 3 months of interest as a prepaid reserve

- This money goes into an escrow account and covers your first three monthly mortgage payments

- You're not losing this money (it's paying future bills), but it does significantly bump up your cash-to-close

Impact on Your Deal Let's put real numbers to this. Say you're borrowing $400,000 at 8% interest—your monthly interest-only payment comes to roughly $2,667. A 3-month interest reserve tacks on $8,000 to your closing costs. That's money many investors simply don't factor in when they're running their initial numbers.

This requirement creates "settlement statement shock" for unprepared borrowers. Always confirm whether your specific lender requires interest reserves during the initial quote phase, as it can make or break your deal economics.

Calculating Your Total Reserve Needs

Let's break down exactly how to figure out your reserve requirement with a simple formula:

Monthly PITIA × Required Months of Reserves = Minimum Reserve Requirement

Here's a real-world example. Say your property has:

- Principal & Interest: $2,400

- Property Taxes: $400

- Insurance: $150

- HOA Dues: $50

- Total Monthly PITIA: $3,000

With a 6-month reserve requirement, you'll need $18,000 in verified liquid assets after closing. Remember, this is on top of your down payment and closing costs.

Strategic Reserve Planning

Here's how savvy investors set up their reserves for maximum flexibility:

- Maintain separate accounts: Keep reserve funds in a dedicated savings account rather than mixing them with your operating capital

- Document everything: Hold onto 60 days of bank statements showing consistent balances

- Plan for seasoning: Move funds into position 60+ days before applying to avoid sourcing headaches

- Consider opportunity cost: Weigh the reserve requirement against potential returns from putting that capital to work elsewhere

- Build cushion: Keep reserves 10% to 20% above the minimum to handle market swings in stocks or cryptocurrency

According to DSCR lending guidelines, adequate reserves aren't just a box to check for approval—they're your safety net that protects both you and the lender from market shifts and surprise property expenses.

Credit Score and History Requirements

Your credit profile is the bedrock of DSCR loan eligibility, but here's the thing: unlike conventional mortgages, these loans look at more than just a three-digit score. Lenders dig into both your credit score and the depth of your credit history to gauge risk since they're not verifying your personal income.

Credit Score Tiers and Their Impact

DSCR loan programs work on a tiered system where your credit score directly shapes your maximum leverage and loan terms. Here's what you need to know:

640 FICO (The Absolute Floor): This is the lowest credit score most DSCR programs will accept. But here's the catch—borrowers at this level face tight restrictions, usually capped at 65% loan-to-value (LTV) ratios. Most DSCR loan programs require a minimum credit score of 640, though some lenders set their floor at 660 or higher based on other risk factors.

680 FICO (The Standard Benchmark): This is where doors start opening. At 680, you can access standard program features, including 75% to 80% LTV on purchases and competitive interest rates. Lenders typically require a minimum credit score of 680 for a DSCR loan, making this the sweet spot for most real estate investors who want favorable terms.

720 FICO (The Premium Tier): Planning to qualify using Airbnb or VRBO income from a short-term rental? You'll need to hit this mark. The higher threshold reflects the extra risk lenders see in vacation rental cash flows.

740 FICO (The Exception Tier): This score is required for cash-out refinances on recently renovated properties that are currently vacant. This scenario stacks multiple risk factors—no active lease, recent value appreciation, and cash extraction—so lenders want the strongest credit profile to balance things out.

Co-Borrower Scoring: When multiple guarantors apply together, lenders typically use the lowest representative score (the middle score from three credit bureaus) among all guarantors. That said, some programs may use the highest score instead.

Credit Depth: Beyond the Score

A strong credit score is great, but it's not the whole picture. Lenders also look at your credit "depth"—proof that you've managed credit responsibly over time:

Tradeline Minimums: You'll need to show either:

- At least 3 active tradelines (credit accounts) reporting for 12+ months, OR

- At least 2 active tradelines reporting for 24+ months

These tradelines can include credit cards, auto loans, student loans, or other installment accounts. The key is establishing a pattern of consistent payment history over time.

The 0x30x12 Housing History Rule

Here's where lenders pay extra close attention: your mortgage payment history. The "0x30x12" rule is straightforward—you can't have any 30-day late payments on any mortgage or rental payment within the last 12 months. This covers:

- Your current primary residence mortgage

- Any existing investment property mortgages

- Documented rental payment history (if you currently rent)

Here's the reality: a single late mortgage payment in the past year can take you out of the running, no matter how strong your credit score is or what caused the delay.

Derogatory Event Seasoning

Major credit events need time to age before you can qualify. Here's what you need to know:

Bankruptcies: Chapter 7 or Chapter 13 bankruptcies must be discharged for at least 36 to 48 months, depending on the specific program and your overall credit profile.

Foreclosures and Short Sales: These events typically require 36 to 48 months of seasoning from the completion date before you're back in the game.

Collections and Judgments: All outstanding collections and judgments must be paid in full prior to or at closing. Good news: some lenders make exceptions for medical collections or combined balances under $2,000, allowing them to remain unpaid.

One important detail: the seasoning period starts from the discharge or completion date, not when you first filed or defaulted. Lenders verify these dates through your credit report and may ask for supporting documentation.

First-Time Investor Restrictions

DSCR lenders draw a clear line between experienced and first-time investors. If you don't meet the "Experienced Investor" definition—typically owning at least one investment property for the last 12 months—you'll face some notable restrictions:

LTV Restrictions: Your maximum leverage gets capped, usually at 75% LTV, regardless of your credit score or how well the property cash flows.

Short-Term Rental Prohibition: You won't be able to use Airbnb, VRBO, or other short-term rental income to qualify for the loan.

Blanket/Portfolio Loan Exclusion: You can't use cross-collateralized loans that bundle multiple properties under one mortgage.

Primary Residence Requirement: You need to already own a primary residence. Lenders want to see that you've got homeownership experience under your belt before they'll back your rental property investments.

First-Time Home Buyer (FTHB) Ineligibility

If you've never owned any property—no primary residence, no investment property—you're typically not eligible for a DSCR loan. These programs are built for investors who already have a track record in housing, not for folks buying their very first property.

Residency and Citizenship Constraints

U.S. Citizens and Permanent Residents: You'll face the standard eligibility requirements with no extra hoops to jump through.

Non-Permanent Resident Aliens: If you're on a work visa (like an H1-B), you can qualify, but you'll need a valid U.S. credit score and an unexpired visa with enough time left on it.

Foreign Nationals: You can apply, but expect tighter restrictions:

- Leverage is capped at 60% to 65% LTV maximum

- You'll need 12 months of PITIA (Principal, Interest, Taxes, Insurance, and Association fees) sitting in cash reserves

- Funds must be sourced, converted to U.S. dollars, and parked in a U.S. FDIC-insured bank account for 30 to 60 days before closing

- Expect higher interest rates to offset the lender's perceived risk

ITIN Borrowers: If you have an Individual Taxpayer Identification Number (ITIN), you're generally not eligible for DSCR loans. There are rare exceptions if your ITIN is used only for reporting passive income taxes rather than U.S. employment income.

Getting clear on these credit and borrower requirements upfront helps you gauge your eligibility before you dive into the application process—potentially saving you months of chasing deals that were never going to work.

Property Eligibility: What Types of Real Estate Qualify for DSCR Loans?

Not all investment properties are created equal in the eyes of DSCR lenders. Knowing which property types qualify—and which ones face restrictions or don't make the cut—is key to putting together a successful deal. DSCR loans are built for income-producing residential real estate, but the details matter when it comes to property condition, location, and special use cases.

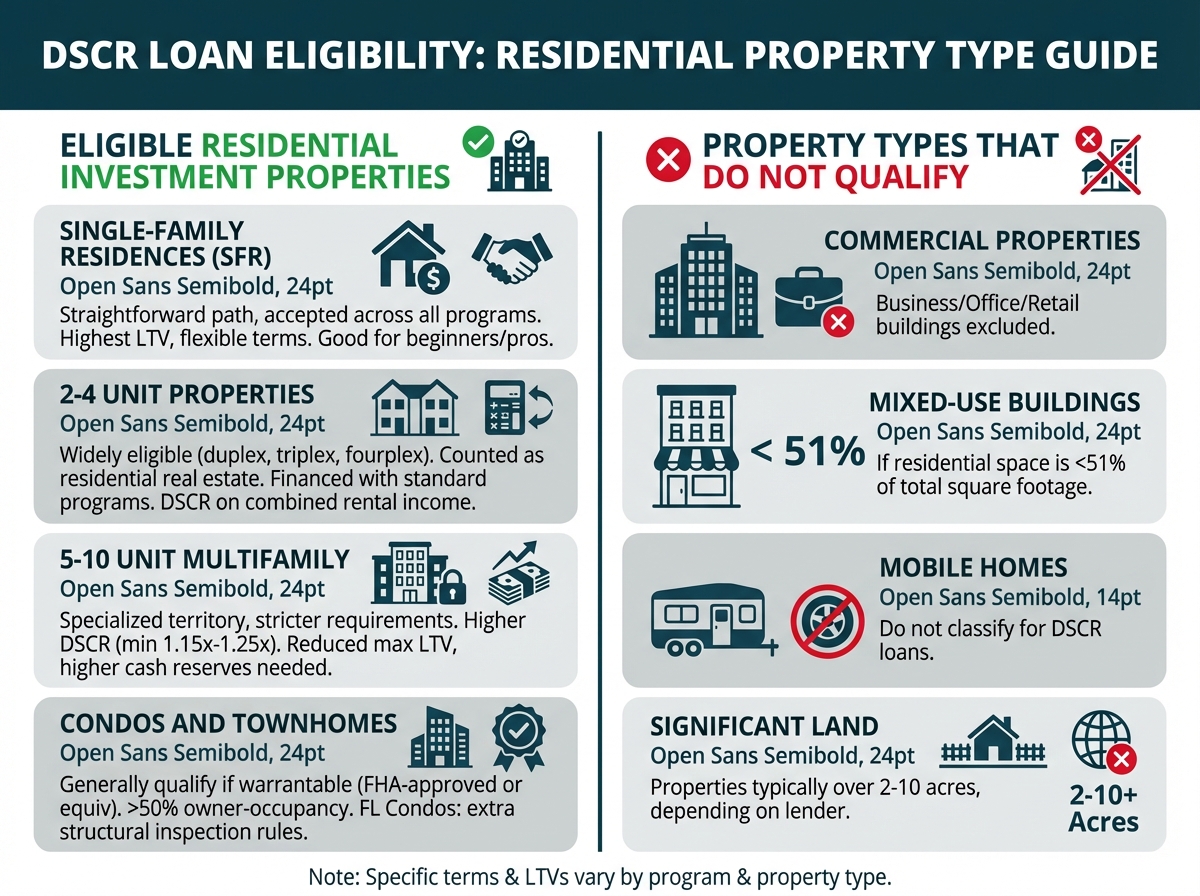

Eligible Property Types

DSCR loans work for a variety of residential investment properties, though the specific requirements shift based on the number of units:

Single-Family Residences (SFR): This is your most straightforward path. Single-family homes are accepted across all DSCR programs. These properties typically qualify for the highest loan-to-value ratios and most flexible terms, making them a solid choice whether you're just starting out or you've been investing for years.

2-4 Unit Properties: Duplexes, triplexes, and fourplexes are also widely eligible for DSCR financing. According to NewFi, these multi-unit properties still count as residential real estate and can be financed with standard DSCR loan programs. Keep in mind that lenders will calculate the DSCR using the combined rental income from all units.

5-10 Unit Multifamily Properties: Larger multifamily buildings move into more specialized territory. These properties can qualify under certain DSCR programs, but expect stricter requirements. You'll typically need a minimum DSCR of 1.15x to 1.25x—noticeably higher than the standard 1.00x threshold for smaller properties. On top of that, these larger buildings often come with reduced maximum LTV ratios and may require you to hold more cash in reserve.

Condos and Townhomes: Condominiums and townhomes generally qualify, as long as they meet specific warrantability requirements. The project needs to be FHA-approved or meet equivalent standards, and owner-occupancy ratios typically need to exceed 50%. For Florida condos specifically (covered below), you may also need to meet additional structural inspection requirements.

Property Types That Don't Qualify: DSCR loans aren't a fit for every property type. Commercial properties, mixed-use buildings where residential space makes up less than 51% of the total square footage, mobile homes, and properties with significant land (typically over 2-10 acres, depending on the lender) won't make the cut. As LendingOne points out, your property needs to be classified as residential investment real estate to qualify.

Property Condition Requirements: The C1-C4 Standard

Here's something important to know: DSCR loans require your property to be "lease-ready" at closing. Unlike renovation loans that let you hold back funds in escrow for repairs, DSCR financing means your property must be move-in ready—no deferred maintenance or safety concerns allowed.

Appraisers use a standardized rating system to assess property condition:

- C1 (New Construction): Fresh off the build with zero deferred maintenance

- C2 (Like New): Well-maintained with minimal wear

- C3 (Average): Normal wear and tear that makes sense for the property's age

- C4 (Fair): Some deferred maintenance but nothing structural

- C5 (Poor): Significant deferred maintenance that needs immediate attention

- C6 (Unsound): Structural damage or habitability issues

If your property appraises at C5 or C6, it's a no-go for DSCR financing until you complete all repairs and get a fresh inspection. The "no escrow holdback" rule means you can't close on a DSCR loan planning to fix things up afterward. Your property must pass inspection at C1-C4 condition before any lender will give you the green light.

Location-Based Restrictions and Penalties

Your investment property's location can make a big difference in your loan terms—or knock it out of the running altogether.

Rural Property Caps: Properties classified as "rural" face tighter restrictions. Generally, a property gets the rural label if it's on a dirt road, sits more than 5 miles from comparable sales, or comes with extra acreage (usually over 2-10 acres, though this varies by lender program). Check if your property is rural using our rural property check guide.

Rural properties are often capped at just 65% LTV, restricted to purchase transactions only (no refinances), and explicitly forbidden from using short-term rental income for qualification. Here's the deal: rural properties carry higher risk because there's limited comparable sales data and potentially longer marketing times if foreclosure becomes necessary.

Declining Market Reductions: When an appraiser checks that box indicating your property sits in a "declining market"—meaning home values have been dropping consistently over the past 12 months—lenders automatically knock 5% off your maximum LTV. So if you'd normally qualify for 80% LTV, that declining market designation brings you down to 75% LTV. The bottom line? You'll need a larger down payment or have less equity available for cash-out refinances.

Rent Control States: Properties in rent-controlled areas (think California, New York, Oregon, and certain cities elsewhere) must meet a minimum DSCR of 1.35x. Why the higher bar? Lenders can't count on future rent increases to maintain debt service coverage when laws cap how much you can raise rents each year—sometimes below inflation. They offset this long-term cash flow risk by requiring stronger coverage ratios from the start.

Accessory Dwelling Units (ADUs): The Comparable Requirement

Accessory Dwelling Units—basement apartments, garage conversions, standalone cottages—are absolutely permitted under DSCR loan guidelines. But here's what you need to know: using that ADU rental income to qualify comes with one critical requirement.

To include ADU rental income in your DSCR calculation, your appraiser needs to find at least one comparable sale and one comparable rental property nearby that also has an ADU. Without these comparables, lenders simply can't verify the ADU's market value or rental income potential—and they'll exclude that income entirely from your DSCR calculation.

This requirement creates a catch-22 in emerging ADU markets. Even if your property has a legal, permitted ADU generating strong rental income, you cannot use that income to qualify if ADUs are uncommon in your specific neighborhood. The zoning must legally permit ADUs, and the appraiser must document that similar properties with ADUs are actively renting in the local market.

Florida Condo Milestone Inspections: A Critical Hurdle

If you're eyeing a condominium in Florida, the building's age and proximity to the coast can trigger a deal-killing requirement. Following the tragic Surfside condominium collapse in 2021, Florida enacted strict structural inspection laws that now directly impact DSCR loan eligibility.

Here's what you need to know: For condominiums over 30 years old—or just 25 years old if located within 3 miles of the coast—and standing greater than 5 stories tall, you must provide a formal structural "milestone inspection" report. This inspection must be conducted by a licensed engineer and must confirm there are no structural integrity issues, safety hazards, or deferred maintenance concerns that could compromise the building's stability.

The bottom line? Without an acceptable milestone inspection report, the condominium project is completely ineligible for DSCR financing. This requirement adds both time and cost to Florida condo acquisitions, as these inspections can take weeks to schedule and cost several thousand dollars. And here's the tough part: if the inspection reveals structural deficiencies, the entire building may be deemed uninvestable until the HOA completes major capital improvements—a process that could stretch months or even years.

Strategic Considerations for Property Selection

Here's some advice that can save you real headaches: Understanding these property eligibility requirements before you start shopping prevents you from wasting time on deals that will never close. Before making an offer, verify that the property type is eligible, confirm it will appraise in C1-C4 condition, research whether the location triggers any rural or declining market penalties, and for ADUs or Florida condos, ensure all special requirements can be met.

The most successful DSCR loan investors choose properties strategically, avoiding edge cases and selecting real estate that fits cleanly within standard eligibility parameters. When in doubt, consult with an experienced DSCR lender before signing a purchase agreement—a five-minute conversation can prevent a costly mistake.

Entity Structuring and Documentation

Here's the deal: how you structure your borrowing entity can make or break your DSCR loan. Unlike conventional mortgages that typically close in your personal name, DSCR loans are business-purpose loans—and lenders actively encourage (often require) them to be held in formal business entities. Getting clear on entity structuring, ownership thresholds, and documentation requirements now will help you sidestep those frustrating last-minute deal killers.

Eligible and Ineligible Entity Types

DSCR lenders accept most standard U.S.-domiciled business entities, but knowing what's off the table is just as important:

Eligible Entities:

- Limited Liability Companies (LLCs)

- Corporations (C-Corps and S-Corps)

- Limited Partnerships (LPs)

Ineligible Entities:

- Irrevocable trusts

- Land trusts

- Non-profit organizations (501(c)(3) or 501(c)(4))

- Foreign-domiciled entities (companies formed outside the United States)

Let's talk trusts for a moment. While some lenders may work with revocable living trusts on a case-by-case basis, irrevocable trusts are a universal no-go. Why? They create legal separation that prevents lenders from enforcing personal guarantees. Non-profits face similar restrictions—their tax-exempt status and governance structures simply don't align with commercial DSCR lending.

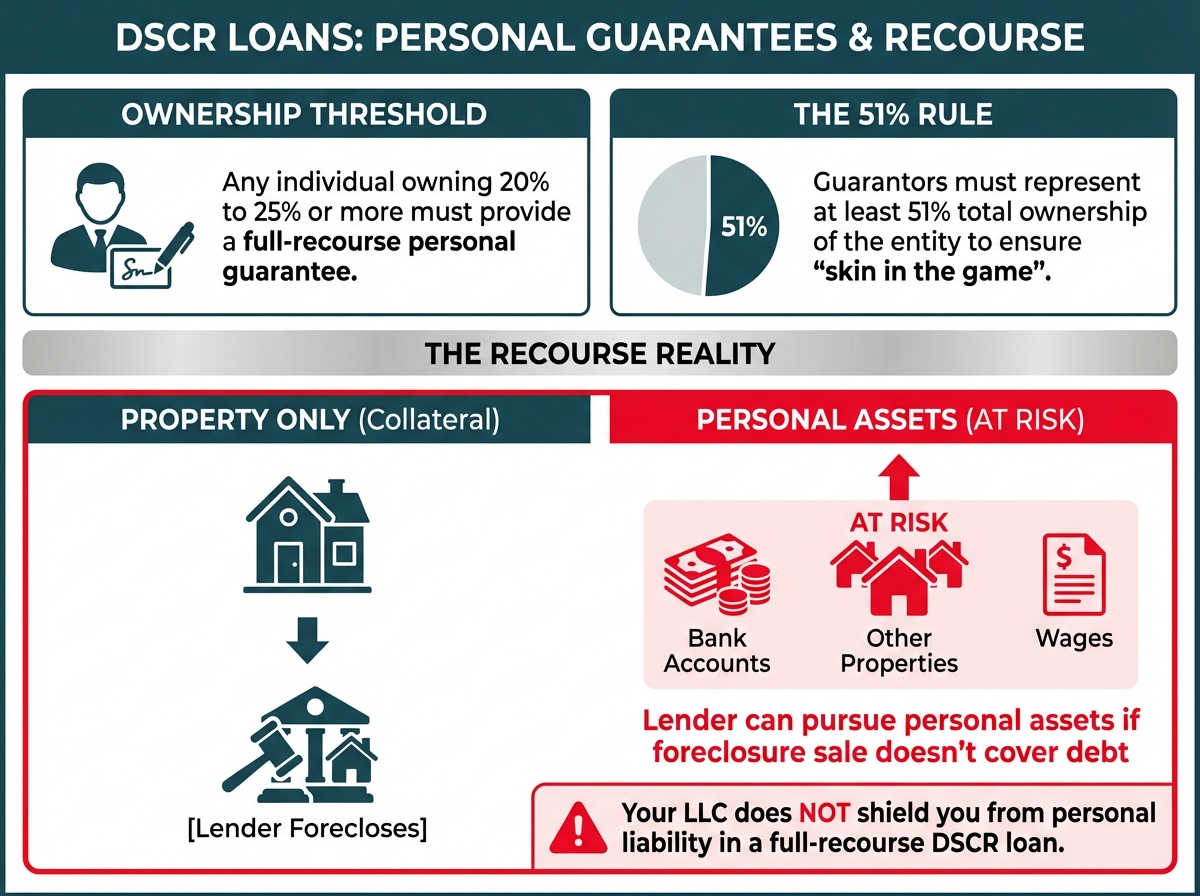

The 20-25% Guarantor Rule and Full-Recourse Requirements

Here's something that catches many investors off guard: DSCR loans to entities require full-recourse personal guarantees. Your LLC structure won't shield you from personal liability on these loans.

The industry-standard ownership threshold works as follows:

Individual Guarantor Requirements:

- Any individual owning 20% to 25% or more of the borrowing entity must sign a full-recourse personal guarantee

- Some programs use a 19% threshold for standard rental and fix-and-flip loans

- The exact percentage varies by capital provider, but 25% is the most common benchmark

Aggregate Guarantor Requirements:

- In aggregate, the individuals providing personal guarantees must represent at least 51% ownership of the borrowing entity

- This ensures that those signing have real skin in the game—not just minority stakeholders trying to secure financing

What Full-Recourse Means: Here's the straight talk: when you sign a full-recourse guarantee, you're personally on the hook for the entire loan amount. If the property goes into foreclosure and the sale doesn't cover what's owed, the lender can come after your personal assets—bank accounts, other properties, even wages—to make up the difference. This is a big distinction from non-recourse loans, where the lender's only option is to foreclose on the property itself.

Required Documentation Package

To close a DSCR loan in your entity's name, you'll need to put together a solid documentation package. This proves your entity legally exists, is in good standing, and that you have the authority to take on debt secured by real property:

Core Entity Documents:

Articles of Organization or Certificate of Formation - This is the foundational document you filed with your state to officially create your LLC or corporation.

Operating Agreement, Partnership Agreement, or Corporate Bylaws - Here's where many investors trip up: this document must specifically grant you the authority to encumber real property on behalf of the entity. Those generic templates you downloaded online? They often miss this crucial language and will get rejected.

Certificate of Good Standing - This state-issued document confirms your entity is current on all filings and authorized to do business. Most lenders require this to be dated within 30 to 90 days of closing, so timing matters.

Employer Identification Number (EIN) - Issued by the IRS, or an executed W-9 form showing the entity's tax identification number.

Personal Documentation for All Guarantors:

Government-Issued Photo ID - Driver's license or passport for each guarantor.

Third-Party Background and Fraud Checks - Every guarantor must undergo comprehensive screening. Here's the bottom line: any felony or misdemeanor convictions involving financial fraud, embezzlement, money laundering, or other financial crimes within the last 10 years will result in automatic loan decline. No exceptions here.

Layered LLC Ownership and Maximum Owner Limits

Many savvy investors use "layered" or "series" LLC structures—think of it as a parent LLC owning a subsidiary LLC, which then owns the borrowing LLC. Good news: these structures are allowed. But heads up—they do trigger extra scrutiny and tighter ownership requirements.

Layered LLC Rules:

When you set up ownership through multiple entity layers, the personal guarantor needs to maintain the minimum ownership stake (typically 25%) and signing authority across:

- The borrowing LLC (the entity taking title to the property)

- All parent LLCs up the ownership chain

Let's break this down with an example: Say John owns 30% of Parent LLC, which owns 100% of Borrowing LLC. John's effective ownership in Borrowing LLC is 30%—he meets the threshold and can guarantee the loan. But here's where it gets tricky: if John owns 30% of Parent LLC, which only owns 50% of Borrowing LLC (with another entity owning the rest), his effective ownership drops to just 15%. That's below the threshold.

Important to Know: Trusts cannot be members of the borrowing LLC in layered structures. If your Parent LLC includes a trust as one of its members, the entire structure becomes ineligible for financing.

Maximum Owner Limits:

Some DSCR programs cap the borrowing entity at 4 owners, members, or shareholders. Why? This helps:

- Keep underwriting and documentation straightforward

- Minimize the risk of partner disputes

- Maintain clear decision-making authority

Got 5 or more members in your LLC? You'll likely need to restructure before applying—either by consolidating ownership among fewer individuals or creating a parent entity to hold the interests of your multiple investors.

Background Checks and Automatic Decline Triggers

Here's something that catches a lot of investors off guard: the background check. Every guarantor gets screened through third-party services, and certain findings will stop your loan in its tracks.

Automatic Decline Triggers:

- Felony convictions for financial crimes (fraud, embezzlement, money laundering) within the past 10 years

- Misdemeanor convictions for financial crimes within the past 10 years

- Active warrants or pending criminal charges related to financial misconduct

- Proven involvement in mortgage fraud schemes or identity theft

Good News About Non-Financial Crimes: A DUI or non-financial misdemeanor won't automatically disqualify you. Lenders typically review these situations individually, so don't assume the worst if your record isn't spotless.

The "Straw Borrower" Refinance Trap

Refinancing a property your entity already owns? Here's a curveball to watch for. Lenders will pull your original purchase settlement statement, and if someone who isn't a current guarantor appears on those documents, they'll want a full credit and background check on that person—even if they walked away from the deal years ago.

Why? Lenders are guarding against "straw borrower" schemes, where someone with credit problems or a problematic history hides behind a partner with a clean record. The bottom line: if that original partner has disqualifying issues, your refinance could get denied even though they're completely out of the picture now.

Strategic Considerations for Entity Structuring

For Solo Investors: Keep it simple. Form a single-member LLC in the state where you're buying. You'll get liability protection without unnecessary paperwork headaches.

For Partnerships: Get your operating agreement buttoned up. Make sure it spells out:

- Each member's ownership percentage

- Who has authority to make decisions on real estate transactions

- The exit plan if one partner wants out

For Portfolio Investors: Think strategically about your structure. Should each property sit in its own LLC, or does one LLC holding multiple properties work better for your goals? The right answer depends on your specific situation. While separate LLCs provide maximum liability protection, they create more administrative overhead. A single LLC simplifies management but could expose your entire portfolio if one property faces a lawsuit.

For Privacy-Conscious Investors: Some states (like Wyoming, Delaware, and Nevada) offer greater privacy protections for LLC owners. That said, keep in mind that DSCR lenders will still require full disclosure of all 20%+ owners regardless of what's publicly visible in state records.

Entity structuring requirements for DSCR loans are more complex than most investors initially realize, but here's the good news: they're entirely manageable with proper planning. The key is to establish your entity structure early in the process—ideally before you even start property shopping—so you're not scrambling to form LLCs, obtain Certificates of Good Standing, or restructure ownership percentages while under contract.

Common Pitfalls and How to Avoid Them

Understanding DSCR loan requirements is only half the battle. The other half is navigating the operational landmines that can derail your transaction at the last minute. These aren't just theoretical concerns—they're the real-world tripwires that cause deals to fall apart after you've already invested time, money, and emotional energy. Let's walk through these pitfalls by category so you know exactly what to watch for.

Cash Flow Traps: When Your Rental Income Doesn't Count the Way You Think

The DSCR formula seems simple enough: divide your gross rental income by your total monthly housing payment (PITIA). But lenders have developed sophisticated rules to prevent borrowers from inflating income projections, and these rules create several traps you'll want to avoid.

The Actual vs. Market Rent Discrepancy

If your property currently has a tenant in place, you might assume the lender will use your actual lease amount to calculate DSCR. Not so fast. Lenders will always use the lesser of your actual executed lease or the appraiser's estimate of market rent. This protects them from borrowers who have artificially inflated leases with friends or family members.

Here's where it gets tricky: even if your actual lease is legitimately higher than market rent, most lenders will cap the allowable rent at 120% of the market average. You'll need to show you've been successfully collecting that higher rent for at least 2-3 months. If you just signed a new lease at an above-market rate, the lender may not give you credit for it until you've built up a consistent collection history.

The Short-Term Rental Income Haircut

Short-term rentals come with their own set of hurdles when it comes to DSCR calculations. If you're counting on Airbnb or VRBO income to qualify, lenders will take your 12-month historical revenue (or projected AirDNA revenue for purchases) and automatically shave off 20% for expenses. This covers cleaning fees, management costs, marketing expenses, and vacancy between bookings.

And there's more to consider. STR properties typically require a higher minimum DSCR (often 1.15x to 1.25x instead of the standard 1.00x), a minimum 720 credit score, and are off-limits to first-time investors. The occupancy projections from AirDNA must also show at least 60% occupancy, or the income won't count at all.

The Sub-1.00x DSCR Reality

Some programs do allow DSCR ratios as low as 0.75x, meaning the property operates at a monthly loss. While this might sound like a helpful fallback, these "no-ratio" loans come with steep trade-offs: you can't use short-term rental income, cash-out refinances at maximum leverage aren't an option, rural properties are off the table, and you'll need 6 to 12 months of cash reserves at closing. For most investors, a sub-1.00x DSCR essentially puts the property out of reach under reasonable financing terms.

Valuation Traps: When Your Property Isn't Worth What You Think

Property valuation issues derail more deals at the last minute than almost any other factor. Lenders have developed strict seasoning requirements and cost basis limitations to prevent value inflation schemes.

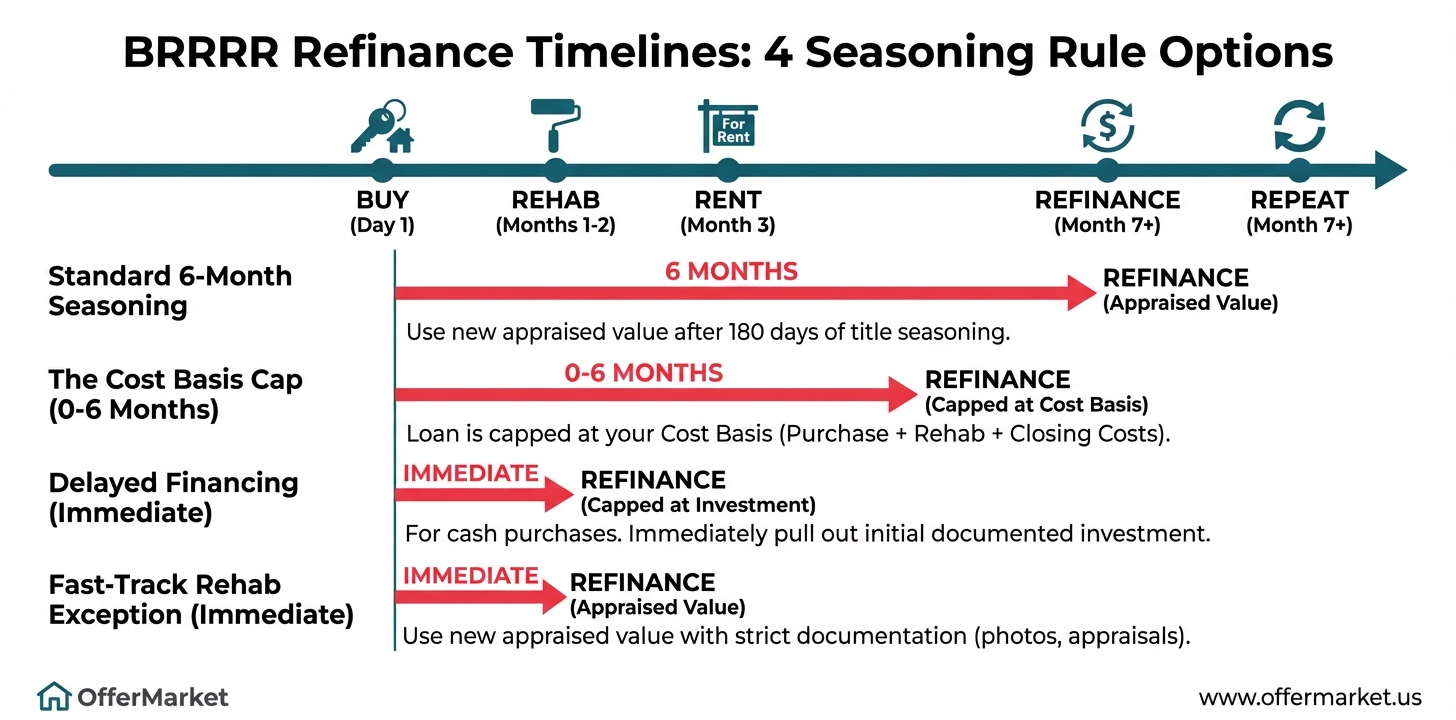

The Delayed Financing Cost Basis Trap

Here's a common scenario: you buy a property in cash, planning to refinance shortly after and pull your capital back out. This strategy—called "delayed financing"—absolutely works, but you need to know the rules. If you refinance within the first 6 months of ownership, lenders will cap your new loan amount at your cost basis: that's your original purchase price plus documented rehabilitation costs.

That word "documented" is doing a lot of heavy lifting here. Did you handle cosmetic renovations yourself? Pay contractors in cash without keeping formal invoices, contractor licenses, or a detailed Scope of Work? Those costs won't count toward your cost basis. You'll be stuck at your original purchase price, even if the property now appraises much higher. This trap has caught countless investors off guard, leaving tens of thousands of dollars locked up in properties they expected to refinance quickly.

The 6-to-12 Month Cash-Out Waiting Period

Want to do a standard cash-out refinance based on current appraised value instead of cost basis? You'll typically need to own the property for 6 to 12 months first, measured from Note date to Note date. Different lenders have different seasoning requirements, and properties in declining markets may require even longer waiting periods.

Here's the cash flow challenge this creates: you might renovate and lease a property in just 90 days, but your equity stays locked up for another 3-9 months. Keep this timeline in mind when planning your capital deployment strategy.

The "Flip" Rule (HPML Trigger)

Buying a property where the seller purchased it within the last 90 days and bumped the price more than 10%? Or acquired it 91-180 days ago with a price increase over 20%? You've triggered a federal anti-flipping rule called the HPML (High-Priced Mortgage Loan) provision. The result: you'll need to pay for a second, completely independent appraisal to verify the value is legitimate. This adds both cost and time to your transaction, and if the second appraisal comes in lower, your deal may fall apart entirely.

Collateral Traps: When Your Property Doesn't Qualify

Not all investment properties are created equal in the eyes of DSCR lenders. Certain property characteristics can reduce your leverage, increase your costs, or disqualify you entirely. Let's break down what to watch for.

The "Lease Ready" Condition Requirement

Here's something many investors don't realize: DSCR loans don't allow escrow holdbacks for repairs. Your property must appraise in C1 to C4 condition—that's good to average condition with no significant deferred maintenance. If the appraiser marks it as C5 or C6, meaning major repairs are needed, there are structural issues, or habitability hazards exist, your loan stops in its tracks until you complete repairs out-of-pocket and get a re-inspection.

This creates a real Catch-22 for value-add investors: you need the loan to fund the repairs, but you can't get the loan until the repairs are done.

Unpermitted Accessory Dwelling Units (ADUs)

Good news: ADUs are allowed under most DSCR programs. But here's the catch—the zoning must legally permit them, and you need a certificate of occupancy. Even more important: if you want to use that ADU rental income to boost your DSCR calculation, the appraiser must find at least one comparable sale and one comparable rent in the area that also has an ADU. No comps? That ADU income gets completely excluded from your DSCR calculation, which could sink your loan approval.

Declining Market and Rural Property Haircuts

If the appraiser checks the box indicating your property is in a "declining market," expect most lenders to automatically reduce your maximum LTV by 5%. Rural properties face even tougher restrictions. If your property sits on a dirt road, is more than 5 miles from comparable sales, or sits on more than 2-10 acres (depending on the program), you're looking at caps around 65% LTV, purchase-only restrictions (no refinances), and a complete ban on using short-term rental income.

Borrower Traps: When Your Experience (or Lack Thereof) Costs You

Your investment track record plays a big role in shaping your loan terms. Certain borrower profiles can trigger automatic penalties—or even disqualification.

The "First-Time Investor" Penalty

Haven't owned an investment property for at least 12 months? You'll be classified as a first-time investor. Here's what that means for you: your LTV is typically capped at 75% (compared to 80% for experienced investors), short-term rental income is off the table entirely, and you won't have access to "Blanket" or "Portfolio" loans that let you finance multiple properties at once.

The "Straw Borrower" Refinance Review

Refinancing a property you already own? Expect lenders to take a close look at your original purchase settlement statement. If someone who isn't a guarantor shows up on those documents, the lender may require a full credit and background check on that individual. This safeguard exists to prevent "straw borrower" arrangements—where someone with strong credit fronts for a partner with credit issues or a problematic history. If that person's background raises red flags, your refinance could be declined, even if you've been successfully managing the property for months or years.

Legal and Financial Traps: The Hidden Costs and Restrictions

Property and borrower qualifications aren't the only hurdles. Several legal and financial requirements can catch investors off guard.

State-Specific Prepayment Penalty Restrictions

DSCR loans typically come with prepayment penalties—often structured as a 5-4-3-2-1% step-down over five years. But here's the thing: state laws trump lender policies. In Alaska, New Mexico, and Minnesota, prepayment penalties are completely prohibited. Pennsylvania and Ohio restrict or ban them for smaller loan amounts, with thresholds that adjust annually. When prepayment penalties aren't allowed, lenders usually offset this by charging higher base interest rates—typically around 0.

25% to 0.50% higher—to offset their lost penalty protection.

Mandatory Rent Loss Insurance

Here's something that catches many investors off guard: standard hazard insurance won't cut it for DSCR loans. You'll need to carry 6 months of "Business Interruption" or "Rent Loss" insurance as part of your policy. This coverage has your lender's back if your property becomes uninhabitable due to a covered loss (think fire or major damage) and rental income stops while repairs are underway. Too many investors don't discover this requirement until they're days from closing, only to find their insurance agent needs extra time to add the endorsement—potentially pushing back their closing date.

Getting familiar with these pitfalls before you dive into the loan process can save you thousands of dollars and weeks of frustration. The smart move? Partner with a lender who knows these tripwires inside and out and can help you structure your deal to sidestep them from day one.

Strategic Tips for Securing a DSCR Loan

Knowing DSCR loan requirements is just the starting point—understanding how to strategically position yourself to meet and exceed these requirements is what sets successful real estate investors apart from those who struggle to qualify. Here are practical strategies to strengthen your loan application and lock in the best possible terms.

Improving Your DSCR

Your Debt Service Coverage Ratio is the foundation of your loan approval. If your property's cash flow isn't quite hitting lender thresholds, you've got several levers to pull:

Increase Rental Income

The most straightforward way to boost your DSCR is to increase the numerator—your rental income. Here's how:

- Raise Rents to Market Rate: If your current lease is below market, plan a rent increase at the next renewal. Lenders use the lesser of actual lease or market rent, so bringing your actual rent up to market levels eliminates this discount.

- Add Income Streams: If local zoning allows, consider adding a legal ADU (Accessory Dwelling Unit) to generate additional rental income. Remember that the appraiser must find comparable properties with ADUs in your area for this income to count.

- Reduce Vacancy: For short-term rentals, focus on boosting your occupancy rate above that 60% minimum threshold. Higher occupancy means higher gross revenue, which improves your DSCR even after the 20% expense haircut.

- Optimize Short-Term Rental Pricing: Consider using dynamic pricing tools to capture maximum revenue during peak seasons while staying competitive when things slow down.

Reduce Your PITIA

The denominator of your DSCR calculation—your total debt service—can often be lowered through smart financing choices:

- Extend Your Amortization Period: Opting for a 30-year amortization instead of a 20-year or 15-year term cuts your monthly principal and interest payments significantly, giving your DSCR an immediate boost. Yes, you'll pay more interest over time, but the improved cash flow could be what gets you from denial to approval.

- Shop for Lower Interest Rates: Even shaving 0.25% off your interest rate can make a real difference in your monthly payment and DSCR. This is where partnering with a lender like OfferMarket, with access to multiple capital providers, really pays off.

- Challenge Your Property Tax Assessment: Think your property taxes are too high compared to similar properties? Consider filing an appeal with your local assessor's office. Lower taxes mean lower PITIA—simple as that.

- Optimize Your Insurance Coverage: You need adequate coverage, including that mandatory 6-month rent loss insurance, but that doesn't mean you can't shop around. Finding competitive rates reduces your insurance costs without leaving you exposed.

- Pay Down Existing Debt: Got other high-interest debts tied to the property? Paying those off before applying for a DSCR loan lowers your total debt service obligations.

Meeting Reserve Requirements

Cash reserves often trip up investors who otherwise check all the boxes. Here's how to ensure you meet these requirements:

Acceptable Reserve Sources

Lenders have clear guidelines on what qualifies as reserves. Here's what works:

- Cash in U.S. Bank Accounts: Your simplest path forward. Just make sure your funds are parked in FDIC-insured institutions.

- Stocks, Bonds, and Mutual Funds: Good news here—these typically count at 100% of current value when held in standard brokerage accounts.

- Retirement Accounts (401k, IRA): You can use these, but expect lenders to count only 60-70% of your vested balance (they're factoring in those early withdrawal penalties).

- Other Real Estate Equity: Some programs let you tap into equity from other investment properties, though this option isn't as widely available.

Unacceptable or Restricted Sources

- Cryptocurrency: Here's the deal—some programs will work with crypto, but you'll need to convert it to U.S. dollars in a U.S. institution first. Expect lenders to credit only about 60% of the value given market swings.

- Home Equity Lines of Credit (HELOCs): These won't fly for reserve requirements.

- Gift Funds: Not going to work for reserves (though some programs may accept them for your down payment).

- Pending Asset Sales: Your funds need to be liquid and verified today—future sales don't count.

Seasoning Requirements

Big deposits will raise questions, so let's keep things smooth:

- Season Your Funds: Planning to liquidate assets or move large sums? Do it at least 60 days before your loan application. Most programs want to see funds sitting in your account for 30-60 days.

- Document Everything: Keep a clear paper trail for any large deposits—that means sale agreements, transfer confirmations, and tax documents.

- Foreign Nationals: You'll need to convert your funds to USD and have them in a U.S. bank account for 30-60 days before closing.

Avoiding First-Time Investor Penalties

Here's something important to know: if you haven't owned an investment property for at least 12 months, you'll run into some hurdles. We're talking maximum 75% LTV, no short-term rental income consideration, no portfolio loans, and you'll need to already own a primary residence.

The "Practice Property" Strategy

The smartest way to sidestep these penalties? Buy a qualifying investment property first. Here's your game plan:

- Start Small: Pick up a single-family rental using traditional financing—conventional loan, FHA, or even seller financing all work great.

- Season Your Investment: Hold onto this property and run it for at least 12 months. Keep those mortgage payments on time every single month (that's the 0x30x12 requirement).

- Document Your Experience: Keep detailed records of everything—leases, rent payments, property management, and maintenance. This paperwork proves your chops to future lenders.

- Leverage Your Status: Once you hit that 12-month mark, congratulations—you're now an "experienced investor." That unlocks much better DSCR loan terms: higher LTV, the ability to use STR income, and access to portfolio loans.

Alternative Paths

Not keen on waiting 12 months? You've got options:

- Partner with an Experienced Investor: Structure your LLC with a partner who already qualifies as experienced and holds at least 25% ownership. Some programs will waive those first-time investor restrictions.

- Accept the Limitations: Got a solid deal with conservative leverage needs (75% LTV or less)? You can move forward as a first-time investor—just know you'll face some restrictions.

Optimizing Entity Structure

Most DSCR loans close in an LLC's name, but how you set up that entity really matters.

Proper LLC Setup

- Form in the Right State: You can form your LLC anywhere, but it must be domestic (U.S.-based) and in Good Standing. Delaware and Wyoming are popular for asset protection, though your property state might be simpler for compliance.

- Maintain Good Standing: Get a Certificate of Good Standing dated within 30-90 days of closing. That means filing annual reports and paying state fees on time.

- Draft Proper Operating Agreements: Your Operating Agreement needs to explicitly give the signor authority to encumber real property. Use an attorney or quality legal template service—generic online forms often lack this critical language.

- Obtain an EIN: Apply for an Employer Identification Number through the IRS. This is required for the loan application.

Guarantor Planning

The 25% ownership threshold is critical:

- Strategic Ownership Splits: If you have partners, structure ownership so that individuals with the strongest credit profiles hold at least 25% and can serve as guarantors.

- Avoid Problematic Partners: Any individual owning 25% or more must pass background checks. Any felony or misdemeanor involving financial fraud, embezzlement, or financial crimes within the last 10 years results in automatic decline.

- Aggregate Requirements: The individuals providing personal guarantees must represent at least 51% ownership of the entity in aggregate.

- Keep It Simple: If you use a parent LLC structure, the guarantor must maintain 25% ownership and signing rights through all layers. Simpler structures are easier to qualify.

What to Avoid

- Never Use Irrevocable Trusts: These are completely prohibited as borrowing entities.

- Steer Clear of Non-Profits: 501(c)(3) or 501(c)(4) organizations cannot obtain DSCR loans.

- Watch Your Owner Count: Some programs cap the borrowing entity at 4 owners maximum.

Timing Your Refinances

Understanding seasoning periods is key to maximizing your capital efficiency.

The 6-Month Delayed Financing Window

If you purchased a property in cash and want to pull your money back out quickly:

- 0-6 Months: You can only borrow up to your cost basis (purchase price + documented rehab costs). Save every invoice, receipt, and contractor agreement. Without documentation, you're capped at your original purchase price regardless of the new appraised value.

- After 6-12 Months: You can refinance based on the current appraised value, though you'll still need to meet standard DSCR requirements.

The Cash-Out Refinance Timeline

For standard cash-out refinances:

- Wait 6-12 Months: Most programs require you to have owned the property for at least 6-12 months (Note date to Note date) before you can do a cash-out refinance based on current value.

- Plan Your Renovations: Got big improvements in mind? Complete them before the 6-month mark so the increased value shows up when you refinance.

- Consider Rate-and-Term First: Need to refinance sooner? A rate-and-term refinance (no cash out) typically comes with shorter seasoning requirements.

Avoiding the Flip Rule (HPML)

Buying from a seller who recently acquired the property? Here's what you need to know:

- 90-Day Rule: If the seller owned the property for less than 90 days and bumped up the price by more than 10%, you'll need two full appraisals.

- 180-Day Rule: If the seller owned for 91-180 days and increased the price by more than 20%, the same two-appraisal requirement kicks in.

- Solution: When possible, time your purchase to fall outside these windows, or budget for the additional appraisal cost and potential delays.

Working with Experienced DSCR Lenders

Choosing the right lending partner might be the most important strategic decision you'll make. Here's why working with a specialized DSCR lender like OfferMarket gives you a real edge:

Access to Multiple Capital Providers

Not all DSCR programs are created equal. Different capital providers bring different:

- Risk Tolerances: Some allow 0.75x DSCR, others require 1.25x minimum.

- Property Type Preferences: Some specialize in short-term rentals, others focus on traditional long-term rentals.

- Geographic Footprints: Some steer clear of rural properties or declining markets, others are more flexible.

- Pricing Structures: Interest rates, points, and fees vary significantly between providers.

A lender with access to multiple capital sources can shop your deal to find the best fit, rather than squeezing you into a one-size-fits-all program.

Expertise in Complex Scenarios

DSCR loans come with countless edge cases and pitfalls. An experienced lender can:

- Pre-Underwrite Your Deal: Spot potential issues before you're under contract, saving you time and earnest money.

- Structure Around Obstacles: If you have a challenging scenario (sub-1.00x DSCR, rural property, vacant unit), they know which programs are most flexible and how to present your application for maximum approval odds.

- Navigate Documentation: They know exactly what documentation each capital provider requires and can guide you through entity formation, reserve verification, and income calculation.

- Avoid Timing Pitfalls: They understand seasoning requirements and can advise on optimal timing for purchases versus refinances.

Integrated Services

Here's where OfferMarket really shines—we bring DSCR lending, property listings, and insurance services together under one roof:

- Property Acquisition: Access to off-market and on-market investment properties that already meet DSCR lending criteria.

- Insurance Bundling: A streamlined process for obtaining the required hazard insurance plus mandatory 6-month rent loss coverage.