*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The 2026 DSCR Lender Power Rankings

Choosing a DSCR lender is one of the most critical decisions a real estate investor will make. The right partner can accelerate your growth with favorable terms and a smooth process, while the wrong one can stall a deal with delays, hidden fees, and frustrating communication. To bring clarity to this crowded field, we've conducted an exhaustive analysis of the top DSCR lenders in the market. Our power rankings are designed to help you quickly identify the strongest contenders based on your specific needs.

How We Evaluated The Lenders

Our evaluation process went far beyond a simple comparison of advertised interest rates. We took a holistic, investor-centric approach, weighing the factors that have a real-world impact on your profitability, stress levels, and ability to close deals. Our team of real estate and mortgage experts assessed each lender against a rigorous set of criteria:

- Rates & Fees: This is the most obvious factor, but we dug deep. We compared the interest rates, origination points, processing fees, underwriting fees, and other lender charges. We looked for transparency and lenders who offer competitive pricing without nickel-and-diming borrowers with junk fees.

- Loan Options & Flexibility: A one-size-fits-all approach doesn't work in real estate. We prioritized lenders who offer a wide range of options, including various prepayment penalty structures, interest-only periods, 40-year amortization, and the ability to finance different property types (SFR, 2-4 units, 5+ units, short-term rentals).

- Customer Service & Expertise: When a deal is on the line, you need a responsive and knowledgeable loan officer. We assessed the quality of customer support, the expertise of their lending teams, and their ability to guide investors through complex scenarios. We valued dedicated advisors over call-center models.

- Speed & Technology: In a competitive market, the ability to close quickly is a massive advantage. We analyzed each lender's application process, underwriting timeline, and overall closing speed. Lenders with streamlined, tech-enabled platforms that reduce paperwork and accelerate timelines scored highly.

- Market Reputation & Reviews: We scoured industry forums, read countless online reviews, and considered the lender's track record and standing within the real estate investment community. A long history of satisfied clients and positive feedback is a strong indicator of a reliable partner.

By balancing these quantitative and qualitative factors, we've created a nuanced and practical ranking system that reflects the true value each lender brings to the table.

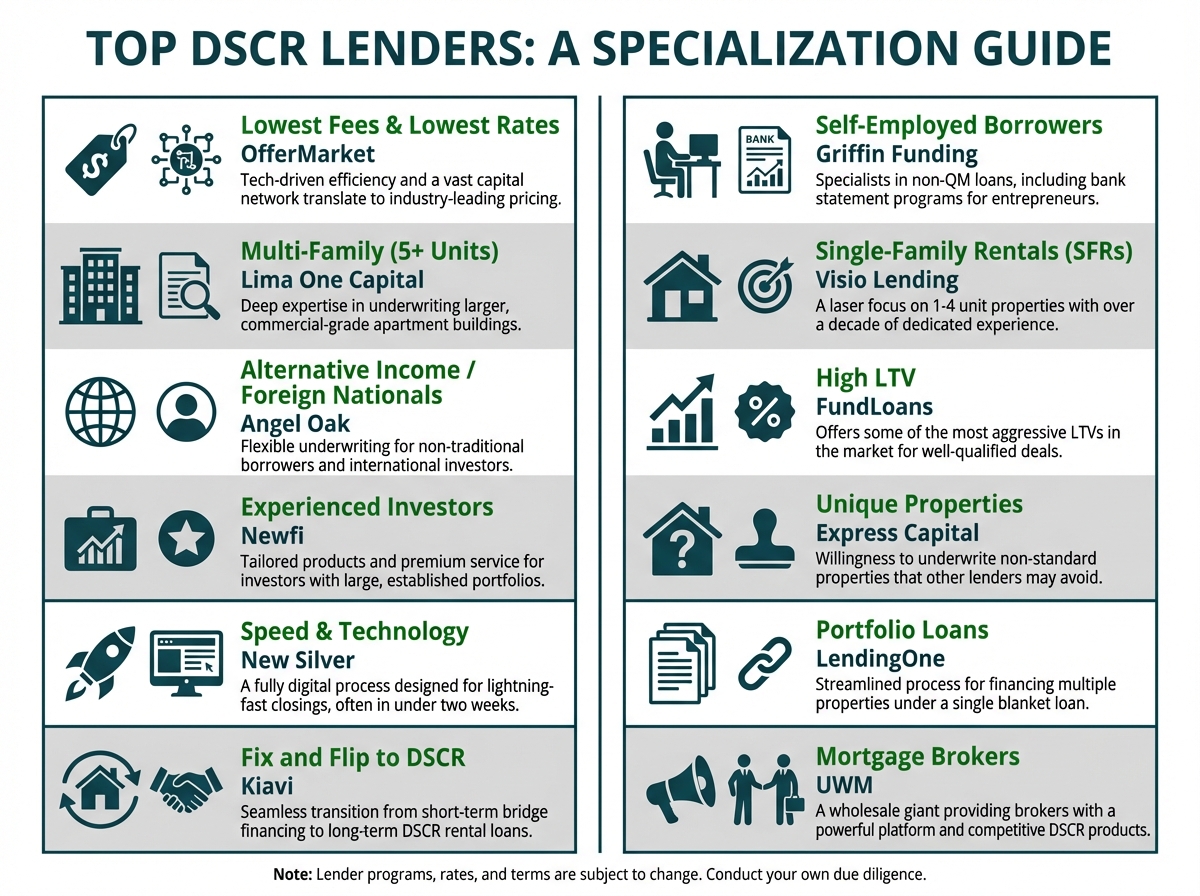

The Best DSCR Lenders by Category

| Category | Lender | Why They Stand Out |

|---|---|---|

| Lowest Fees & Lowest Rates | OfferMarket | Tech-driven efficiency and a vast capital network translate to industry-leading pricing. |

| Multi-Family (5+ Units) | Lima One Capital | Deep expertise in underwriting larger, commercial-grade apartment buildings. |

| Alternative Income / Foreign Nationals | Angel Oak | Flexible underwriting for non-traditional borrowers and international investors. |

| Experienced Investors | Newfi | Tailored products and premium service for investors with large, established portfolios. |

| Speed & Technology | New Silver | A fully digital process designed for lightning-fast closings, often in under two weeks. |

| Fix and Flip to DSCR | Kiavi | Seamless transition from short-term bridge financing to long-term DSCR rental loans. |

| Self-Employed Borrowers | Griffin Funding | Specialists in non-QM loans, including bank statement programs for entrepreneurs. |

| Single-Family Rentals (SFRs) | Visio Lending | A laser focus on 1-4 unit properties with over a decade of dedicated experience. |

| High LTV | FundLoans | Offers some of the most aggressive LTVs in the market for well-qualified deals. |

| Unique Properties | Express Capital | Willingness to underwrite non-standard properties that other lenders may avoid. |

| Portfolio Loans | LendingOne | Streamlined process for financing multiple properties under a single blanket loan. |

| Mortgage Brokers | UWM | A wholesale giant providing brokers with a powerful platform and competitive DSCR products. |

In-Depth Lender Reviews

A table is a great starting point, but the devil is in the details. Here, we take a closer look at what makes each of our category winners a top choice for real estate investors in 2026.

Best for Lowest Fees and Lowest Rates: OfferMarket

- Overview: OfferMarket isn't just a lender; it's a comprehensive real estate investment platform built from the ground up by investors, for investors. Their philosophy is simple: leverage technology to create radical efficiency and pass the savings directly to the client. This approach allows them to offer some of the most competitive DSCR loan terms in the entire industry.

- Why They Won: The secret to OfferMarket's pricing is their vertically integrated model and diversified capital strategy. By integrating lending, an off-market listings marketplace, and insurance services, they reduce friction and overhead. More importantly, they aren't a single direct lender; they operate as a capital partner with access to a wide array of funding sources. This allows them to shop for the best possible execution for your specific loan scenario, ensuring you get the lowest rate and fees available.

- Key Features:

- Instant Online Quote Tool: Get a transparent, real-time quote in seconds without impacting your credit score.

- Streamlined Digital Application: A simple, intuitive online portal that eliminates mountains of paperwork.

- Dedicated Loan Advisors: Access to expert advisors who understand real estate investing and can guide you through the process.

- Integrated Ecosystem: Access to off-market deals and streamlined insurance quoting, all in one place.

- Ideal Borrower: The investor who is laser-focused on maximizing cash flow and long-term ROI. Whether you're a first-timer or a seasoned pro, if you prioritize a fast, digital, and cost-effective financing experience, OfferMarket is built for you.

Best for Multi-Family (5+ Units): Lima One Capital

- Overview: Lima One Capital has established itself as a powerhouse in the private lending space, with a particular strength in financing larger residential and multi-family properties. They have the experience and balance sheet to handle complex deals that fall outside the scope of many smaller DSCR lenders.

- Why They Won: Financing a 15-unit apartment building is fundamentally different from financing a single-family rental. It requires a deeper understanding of commercial underwriting, lease analysis, and property operations. Lima One excels here. Their team is adept at evaluating rent rolls, operating expenses, and market conditions for commercial-grade assets, allowing them to offer tailored solutions for multi-family investors.

- Key Features:

- Bridge-to-Perm Programs: Finance the acquisition and renovation of a value-add multi-family property, then seamlessly convert to a long-term DSCR loan.

- Experience with 5-20+ Unit Properties: They are comfortable with the scale and complexity of larger apartment buildings.

- Flexible Underwriting: They can underwrite deals based on pro-forma (post-renovation) income for value-add projects.

- Ideal Borrower: The real estate investor who is scaling up into larger multi-family assets. If you're acquiring or refinancing apartment buildings with 5 or more units, Lima One has the specialized expertise you need.

Best for Alternative Income & Foreign Nationals: Angel Oak

- Overview: Angel Oak Mortgage Solutions has built its brand on being a leader in the non-QM (non-qualified mortgage) space. Their core competency is underwriting loans for borrowers who don't fit into the neat little boxes of conventional lending. This expertise translates directly to their DSCR program, making them an excellent choice for non-traditional investors.

- Why They Won: Many DSCR lenders still have overlays that can be challenging for certain borrowers. Angel Oak stands out for its flexibility. They have robust programs for foreign nationals who may lack a U.S. credit history, as well as for investors using entities like LLCs with complex ownership structures. Their underwriting team is skilled at looking at the complete picture to make a common-sense lending decision.

- Key Features:

- Foreign National Program: A dedicated program designed to serve international investors purchasing U.S. rental properties.

- No Income/Employment Verification: True to the spirit of DSCR, they focus solely on the property's cash flow.

- Interest-Only Options: Offer flexibility for investors looking to maximize monthly cash flow.

- Ideal Borrower: The international investor looking to capitalize on the U.S. real estate market, or the domestic investor with a complex or non-traditional financial profile.

Best for Experienced Investors: Newfi

- Overview: Newfi Lending is a non-QM lender that caters to a more sophisticated clientele. While they serve a broad range of borrowers, their products and service levels are particularly well-suited for experienced investors who manage substantial portfolios and require a higher level of service and customization.

- Why They Won: Experienced investors value efficiency, reliability, and a partner who understands their long-term strategy. Newfi delivers on this with a white-glove service model and loan products designed for portfolio growth. They offer competitive portfolio loans and have the infrastructure to handle multiple transactions simultaneously for a single client, making them an efficient one-stop shop for active investors.

- Key Features:

- Portfolio Loan Solutions: Streamlined financing for investors looking to refinance multiple properties at once.

- Experienced Loan Officers: Their team is accustomed to working with high-net-worth individuals and seasoned real estate professionals.

- Flexible Guidelines: They often have more flexible guidelines around cash-out limits and the number of financed properties for well-qualified borrowers.

- Ideal Borrower: The seasoned real estate investor with a portfolio of 10+ properties who values a long-term relationship with a lender that can support their continued growth.

![1. Task: Create an infographic that explains the core components of a DSCR loan for real estate investors.

2. Visual Structure: A vertically oriented infographic with a clear title at the top, followed by three distinct sections arranged in a column. Each section will have an icon, a heading, and a brief explanatory text.

3. ASCII Layout Reference:

```

+------------------------------------------+

| The Anatomy of a DSCR Loan |

|------------------------------------------|

| [Icon: Calculator] |

| Debt Service Coverage Ratio (DSCR) |

| The core metric. It's the Gross |

| Rental Income divided by the |

| P.I.T.I.A. Most lenders require a |

| ratio of 1.20+ |

|------------------------------------------|

| [Icon: House with % sign] |

| Loan-to-Value (LTV) |

| How much you can borrow. Typically |

| up to 80% for purchases and 75% |

| for cash-out refinances. |

|------------------------------------------|

| [Icon: Person with X over them] |

| No Personal Income Check |

| Your W-2 or tax returns don't |

| matter. The property's cash flow |

| is what qualifies the loan. |

+------------------------------------------+

```

4. Image section breakdown:

- **Header Section:** The title](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773252726722_2lgo9l.jpg?alt=media&token=2e97115f-cd33-4534-a2af-5d019f93a6e3)

Best for Speed & Technology: New Silver

- Overview: New Silver operates on the principle that in real estate, speed wins. They have built a technology platform from the ground up to automate and accelerate every step of the loan process, from application to closing. They started in the fix-and-flip space, where speed is paramount, and have brought that same urgency to their DSCR product.

- Why They Won: While many lenders talk about technology, New Silver truly lives it. Their online application can be completed in minutes, and their system provides instant feedback and document requests. By leveraging data and algorithms, they have streamlined their underwriting process, enabling them to close loans in a fraction of the time it takes traditional lenders. For investors competing with cash offers, this speed can be the difference between winning and losing a deal.

- Key Features:

- Fully Digital Experience: A seamless online platform for application, document submission, and loan tracking.

- Rapid Closing Times: Consistently one of the fastest in the industry, often closing in 10-15 business days.

- Transparent Process: Real-time updates and clear communication keep borrowers informed at every stage.

- Ideal Borrower: The tech-savvy investor who needs to move quickly in a competitive market. If your strategy involves making aggressive offers with short closing timelines, New Silver's platform is a significant competitive advantage.

Best for Fix and Flip to DSCR: Kiavi

- Overview: Kiavi (formerly LendingHome) is a fintech giant in the real estate lending space. They are one of the largest providers of short-term bridge loans (fix-and-flip loans) in the country. They have leveraged this massive customer base and technological infrastructure to offer a highly competitive long-term DSCR rental loan, creating a seamless path for investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

- Why They Won: For BRRRR investors, the refinance step is the most critical and often the most challenging. Kiavi has solved this by creating a one-stop-shop solution. An investor can get a bridge loan from Kiavi to acquire and renovate a property. Once the property is stabilized and rented, Kiavi makes it incredibly easy to refinance that bridge loan into their long-term DSCR product. This eliminates the uncertainty and hassle of finding a new lender for the refi, streamlining the entire BRRRR process.

- Key Features:

- Bridge-to-Rental Program: A dedicated product that combines short-term and long-term financing into one cohesive process.

- High Volume & Experience: As a major player, they have immense experience and data, leading to reliable execution.

- Tech-Forward Platform: A user-friendly online portal for managing both fix-and-flip and rental loans.

- Ideal Borrower: The BRRRR investor. If your primary strategy is to buy distressed properties, add value through renovations, and then hold them as long-term rentals, Kiavi's integrated financing solution is tailor-made for you.

Best for Self-Employed Borrowers: Griffin Funding

- Overview: Griffin Funding is a mortgage company that has carved out a niche by specializing in non-QM and self-employed loan solutions. They understand that entrepreneurs, freelancers, and business owners often have complex income situations that don't fit the rigid requirements of conventional lending.

- Why They Won: While all DSCR loans are technically "no-doc" regarding personal income, some lenders have overlays or a company culture that is still more comfortable with traditional W-2 borrowers. Griffin Funding's DNA is rooted in serving the self-employed. They are experts in programs like bank statement loans for primary residences, and they bring that same flexible, entrepreneurial-friendly mindset to their DSCR program. They understand the unique challenges and opportunities that self-employed investors face.

- Key Features:

- Deep Non-QM Expertise: This is their core business, not a side product.

- Bank Statement Programs: While not needed for DSCR, their expertise in this area shows their commitment to self-employed borrowers.

- Investor-Friendly Underwriting: They are accustomed to working with borrowers who have non-traditional financial profiles.

- Ideal Borrower: The self-employed real estate investor. If you're a business owner, consultant, or gig economy worker, you'll appreciate working with a lender that inherently understands and caters to your financial situation.

Best for Single-Family Rentals (SFRs): Visio Lending

- Overview: In an industry where many lenders try to be everything to everyone, Visio Lending has taken the opposite approach. Since its inception, Visio has focused almost exclusively on providing long-term financing for single-family (1-4 unit) rental properties. This singular focus has made them true specialists.

- Why They Won: Visio's laser focus on the SFR space gives them a significant edge. Their entire process, from origination to servicing, is optimized for this specific asset class. They have underwritten tens of thousands of SFR loans, giving them unparalleled data and expertise in valuing these properties and understanding their rental markets. They are a well-oiled machine for the bread-and-butter of most real estate investors' portfolios.

- Key Features:

- SFR Specialization: Their deep expertise in 1-4 unit properties leads to a smooth and predictable process.

- Decade of Experience: One of the pioneers in the DSCR loan space, with a long and proven track record.

- Streamlined Process: Their focus allows them to create a highly efficient system for originating and closing SFR loans.

- Ideal Borrower: The investor whose portfolio is primarily composed of single-family homes, duplexes, triplexes, and quads. If you specialize in SFRs, it makes sense to work with a lender who does the same.

Best for High LTV: FundLoans

- Overview: FundLoans is a wholesale and non-delegated correspondent lender known for its aggressive non-QM programs. They are often willing to push the envelope on guidelines, providing solutions for borrowers who need more leverage than what is typically offered by more conservative lenders.

- Why They Won: Loan-to-Value (LTV) is a critical lever for investors looking to minimize their capital contribution to a deal. FundLoans consistently offers some of the highest LTVs available in the DSCR market. For strong borrowers with properties that cash flow well, they may offer up to 80% LTV on cash-out refinances, whereas most competitors cap out at 70% or 75%. This extra leverage can be a game-changer for investors looking to pull out capital to fund their next acquisition.

- Key Features:

- Aggressive LTVs: Industry-leading leverage for both purchases and cash-out refinances.

- Flexible Underwriting: A willingness to consider compensating factors to approve loans at higher LTVs.

- Broker-Focused: They work through mortgage brokers, providing them with a powerful product to offer their investor clients.

- Ideal Borrower: The experienced investor with a strong deal who wants to maximize leverage. If your goal is to pull out as much capital as possible from a property to scale your portfolio faster, FundLoans is a lender to consider.

Best for Unique Properties: Express Capital

- Overview: Express Capital is a private lender that prides itself on its common-sense underwriting and ability to fund deals that don't fit the standard lending box. They take a more holistic and story-based approach to underwriting, looking at the totality of a deal rather than just checking boxes.

- Why They Won: What happens when you have a great deal on a property with unique zoning, a non-standard layout (e.g., a single-family home with an unpermitted ADU), or is located in a very rural market? Many lenders will simply say no. Express Capital is more likely to say, "Tell us more." Their team is skilled at assessing unique situations and finding ways to get comfortable with properties that might scare off more rigid, larger institutions.

- Key Features:

- Common-Sense Underwriting: They look beyond the black-and-white guidelines to the fundamental strengths of a deal.

- Flexibility on Property Types: More open to mixed-use, rural, or non-conforming properties.

- Direct Access to Decision Makers: A smaller, more agile structure often allows for quicker decisions on complex files.

- Ideal Borrower: The investor who finds great opportunities in non-standard assets. If you specialize in properties that are a little "outside the box," you need a lender with the flexibility and creativity to match.

Best for Portfolio Loans: LendingOne

- Overview: LendingOne is another major player in the business-purpose lending space, offering a full suite of products for real estate investors. One of their standout offerings is their portfolio loan program, designed to help investors with multiple properties consolidate their financing.

- Why They Won: Managing individual loans for 5, 10, or 20 different properties can be an administrative nightmare. A portfolio loan, also known as a blanket loan, allows an investor to place a single loan across multiple properties. This simplifies bookkeeping, creates a single monthly payment, and can be used to "un-stick" equity from the entire portfolio. LendingOne has a well-defined and efficient process for underwriting and closing these complex loans, making them a leader in this niche.

- Key Features:

- Dedicated Portfolio Loan Program: A specialized product and team focused on blanket loans.

- Streamlined Underwriting: An efficient process for evaluating multiple properties at once.

- Cross-Collateralization: Allows investors to leverage equity across their entire portfolio to maximize cash-out potential.

- Ideal Borrower: The established investor with five or more properties who is looking to simplify their debt management and unlock equity on a portfolio-wide basis.

Best for Mortgage Brokers: UWM (United Wholesale Mortgage)

- Overview: UWM is the largest wholesale mortgage lender in the United States. They do not work directly with borrowers; instead, they provide the back-end technology, loan products, and underwriting for a vast network of independent mortgage brokers. They have a strong and competitive suite of DSCR loan products.

- Why They Won: For investors who prefer to work with a local mortgage broker, UWM is often the power behind the throne. They equip brokers with industry-leading technology that makes the process faster and more efficient. Their pricing on DSCR loans is highly competitive, and their brand is synonymous with speed and reliability in the broker community. By choosing a broker who works with UWM, investors can get the best of both worlds: the personalized service of a local expert and the power of a national lending giant.

- Key Features:

- Wholesale-Only Model: They are 100% committed to supporting the independent mortgage broker channel.

- Cutting-Edge Technology: Platforms like Blink+ and UWM Portal streamline the process for brokers and their clients.

- Competitive Pricing & Products: A full suite of DSCR options with aggressive rates.

- Ideal Borrower: The real estate investor who has a trusted relationship with an independent mortgage broker. If you prefer this service model, ask your broker if they are partnered with UWM.

How Top Real Estate Investors Choose the Right DSCR Lender for Their Strategy

The top investors in the game know that the advertised interest rate is just the tip of the iceberg. The best financing deal isn't always the one with the lowest rate; it's the one that best aligns with their specific investment strategy, minimizes costs, and provides the flexibility they need to execute their business plan. They treat choosing a lender with the same diligence they apply to finding a property. It's a critical part of the deal's success.

This means looking beyond the marketing slogans and dissecting the loan terms to understand the true cost and structure of the financing. It involves a methodical vetting process to ensure the lender is not just a provider of capital, but a reliable partner for the long haul.

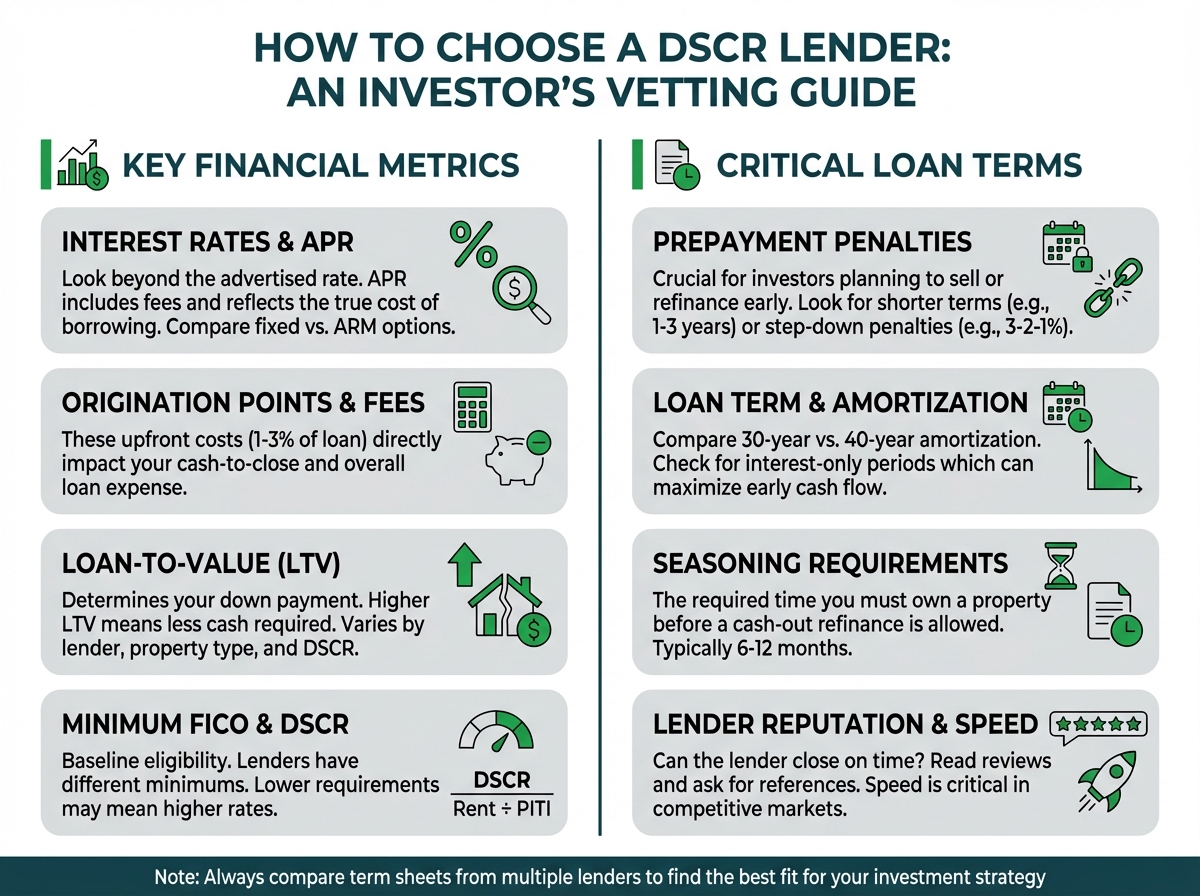

Key Comparison Criteria: Looking Beyond the Interest Rate

When you receive a loan quote or a Loan Estimate, it's tempting to let your eyes jump straight to the interest rate. But seasoned investors know the real story is told in the details. Here are the critical components you must analyze to make a true apples-to-apples comparison.

Interest Rates & APR

- Interest Rate: This is the percentage charged on the principal loan amount. It directly determines your monthly payment. Rates can be fixed, meaning the rate stays the same for the entire loan term (usually 30 years), providing predictable payments. Or they can be Adjustable-Rate Mortgages (ARMs), where the rate is fixed for an initial period (e.g., 5, 7, or 10 years) and then adjusts periodically based on a specific index. ARMs can offer a lower initial rate but introduce long-term uncertainty.

- Annual Percentage Rate (APR): This is the true cost of borrowing. The APR includes the interest rate plus the lender's origination points and other finance charges, expressed as an annualized percentage. A loan with a slightly higher interest rate but zero points could have a lower APR (and be a better deal) than a loan with a lower rate but two origination points. Always compare APRs, not just interest rates.

Origination Points & Fees

These are the upfront costs charged by the lender to create the loan. They can significantly impact your total cash-to-close.

- Origination Points: One point is equal to 1% of the loan amount. Lenders may charge points to cover their costs or as a way to "buy down" the interest rate. For example, on a $300,000 loan, one point is $3,000.

- Processing & Underwriting Fees: These are flat fees (e.g., $995 - $1,495) that cover the administrative costs of assembling and evaluating your loan file.

- Other Fees: Scrutinize the loan estimate for other lender-specific fees like application fees, wire fees, or "junk fees." Third-party costs like the appraisal, title insurance, and escrow fees will be similar across lenders, but the fees in "Box A" of the Loan Estimate are what the lender directly controls.

Loan-to-Value (LTV)

LTV represents the loan amount as a percentage of the property's appraised value. It determines how much of your own capital you need to bring to the deal.

- Purchase: The standard maximum LTV for a DSCR loan purchase is 80%, meaning you'll need a 20% down payment plus closing costs.

- Rate/Term Refinance: When refinancing to get a new rate or term without taking cash out, LTVs can also go up to 80%.

- Cash-Out Refinance: This is a key tool for investors. The maximum LTV is typically lower, ranging from 70% to 80% (though 75% is most common). A higher LTV allows you to pull more capital out of the property to reinvest elsewhere. Your credit score and the property's DSCR will heavily influence your maximum LTV.

![1. Task: Create a horizontal bar chart that visually compares common LTV (Loan-to-Value) limits for different types of DSCR loan transactions.

2. Visual Structure: A clean, professional bar chart with a title, three horizontal bars of varying lengths, and clear labels for the x-axis (LTV Percentage) and y-axis (Transaction Type).

3. ASCII Layout Reference:

```

+------------------------------------------------------------------+

| Typical Maximum LTV for DSCR Loans |

|------------------------------------------------------------------|

| |

| Purchase [##########80%################] |

| |

| Rate/Term Refi [##########80%################] |

| |

| Cash-Out Refi [#########75%#############] |

| |

| |----|----|----|----|----|----|----|----| |

| 0% 20% 40% 60% 80% 100% |

| LTV Percentage |

+------------------------------------------------------------------+

```

4. Image section breakdown:

- **Title:**](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773254279707_0ly3in.jpg?alt=media&token=5949a20f-4b36-40d9-a3e1-43314cefa740)

Prepayment Penalties

This is one of the most important and often misunderstood terms in a DSCR loan. Because these are not owner-occupied loans, they are not subject to the same consumer protection regulations, and prepayment penalties are common. A prepayment penalty is a fee charged if you pay off the loan within a specified period.

- Common Structures:

- 5/4/3/2/1: This is a 5-year penalty. If you pay off the loan in year 1, the penalty is 5% of the outstanding balance. In year 2, it's 4%, and so on, until it disappears after year 5.

- 3/2/1: A 3-year penalty following the same step-down pattern.

- No Penalty: Some lenders offer options with no prepayment penalty, but these almost always come with a significantly higher interest rate.

- Why It Matters: Your investment strategy dictates your need for flexibility. If you plan to hold the property for 10+ years, a 5-year penalty in exchange for a lower rate is a great trade-off. However, if you think you might sell the property in year 2 or want the option to refinance if rates drop, a shorter penalty (or no penalty) might be worth the higher rate.

Minimum FICO & DSCR Requirements

These are the two primary underwriting benchmarks.

- FICO Score: Most lenders require a minimum credit score of 620, but the best pricing and highest LTVs are reserved for borrowers with scores of 720 or higher. A lower FICO score will result in a higher interest rate and a lower LTV. It's crucial to know your credit score before you start shopping. You can get your score from services like Experian or Credit Karma.

- DSCR: The Debt Service Coverage Ratio is calculated as:

Gross Monthly Rent / Monthly PITI(Principal, Interest, Taxes, Insurance).- A DSCR of 1.0x means the rent exactly covers the debt service (a breakeven property).

- Most lenders require a minimum DSCR of 1.20x for 30-year amortizing loans. This means the rent must be at least 20% higher than the PITI.

- For interest-only loans or lower credit scores, the minimum DSCR might be higher (e.g., 1.25x or 1.30x).

- Some lenders offer programs for properties with a DSCR below 1.0x (i.e., negative cash flow), but these come with much lower LTVs and higher rates, and are typically for properties in high-appreciation markets.

Loan Terms & Amortization

- Term: The vast majority of DSCR loans have a 30-year term.

- Amortization: This is the schedule of principal and interest payments over the life of the loan.

- 30-Year Amortization: The standard option, where your payments are calculated to pay off the loan completely in 30 years.

- Interest-Only (IO): A popular option for maximizing cash flow. For an initial period (often the first 10 years), you only pay the interest on the loan. This results in a significantly lower monthly payment. After the IO period ends, the loan re-amortizes over the remaining 20 years, causing the payment to increase substantially.

- 40-Year Amortization: Some lenders offer a 40-year term, which can also lower the monthly payment compared to a 30-year term, though you build equity more slowly.

Seasoning Requirements

This applies specifically to cash-out refinances. Seasoning is the length of time you have owned the property. Lenders impose seasoning requirements to prevent risky "quick flips" where an investor buys a property and immediately tries to refinance it at a higher, inflated value.

- Typical Requirement: Most lenders require you to have owned the property for at least 6 months before you can do a cash-out refinance based on a new, higher appraised value.

- No Seasoning Options: Some lenders offer "delayed financing" exceptions, which allow you to do a cash-out refinance almost immediately if you originally purchased the property with cash. This is a powerful tool for investors who use cash to win deals.

The Step-by-Step Vetting Process

Armed with a deep understanding of the key comparison criteria, you can now approach the selection process like a professional. Follow this checklist to ensure you find the best possible financing partner for your deal.

1. Define Your Loan Needs Before you even talk to a lender, get crystal clear on your objective.

- Transaction Type: Is this a purchase, a rate/term refinance, or a cash-out refinance?

- Property Type: Is it an SFR, a 2-4 unit, a 5+ unit, a short-term rental, or a condo?

- Desired LTV: How much do you want to borrow? Are you trying to maximize leverage or keep your LTV low for better cash flow?

- Investment Horizon: How long do you plan to hold this property? This will determine your tolerance for a prepayment penalty.

- Key Priority: What is most important to you on this deal? Lowest rate? Highest LTV? Fastest closing? Best customer service?

2. Get Quotes from 3-5 Top Lenders Never take the first offer you receive. The lending market is competitive, and rates and fees can vary significantly from one day to the next.

- Reach out to a curated list of lenders. This should include a top-rated direct lender like OfferMarket, a lender specializing in your property type (e.g., Lima One for multi-family), and perhaps a trusted mortgage broker.

- Provide each lender with the exact same information to ensure you can make an accurate comparison.

3. Compare Loan Estimates Side-by-Side Once the quotes come in, don't just glance at them. Print them out and put them next to each other. The standardized Loan Estimate form from the CFPB is designed for this.

- Page 1: Compare the Loan Amount, Interest Rate, and Monthly P&I. Most importantly, check the "Estimated Closing Costs" and "Estimated Cash to Close."

- Page 2: This is where the details are. Focus on "Box A: Origination Charges." This is what the lender is directly charging you. Compare these fees carefully.

- Check the APR: Find the APR on page 3. This is your best tool for an all-in cost comparison.

4. Read Reviews and Ask for References A loan quote only tells you part of the story. You also need to know what it's like to actually work with the lender.

- Online Reviews: Search for the lender on Google, Yelp, and industry forums like BiggerPockets. Look for recent reviews and pay attention to any recurring themes, both positive and negative.

- Ask for References: Don't be afraid to ask your loan officer if they can connect you with another investor they've recently closed a loan for. A good lender will be happy to do this.

5. Interview the Loan Officer The loan officer is your primary point of contact and can make or break your experience. You are hiring them for a critical job. Conduct a brief "interview" to gauge their expertise and communication style.

- Key Questions to Ask:

- "What is your average closing time for a DSCR loan like mine?"

- "Can you walk me through your process from application to funding?"

- "Who will be my point of contact after the application is submitted?"

- "What are the most common reasons a loan gets delayed in your process, and how do you prevent them?"

- "How familiar are you with the real estate market in [Your City/State]?"

By following this disciplined process, you move from being a passive rate-shopper to a proactive, informed investor who is in control of their financing. You'll not only secure a better deal but also find a lending partner you can trust for years to come.

![1. Task: Create an infographic that outlines a step-by-step process for real estate investors to vet and choose a DSCR lender.

2. Visual Structure: A vertically oriented infographic with a title and five numbered steps, each with a distinct icon, a heading, and a short description. The steps should flow downwards, connected by a subtle dotted line or arrows.

3. ASCII Layout Reference:

```

+------------------------------------------+

| How to Choose Your DSCR Lender: 5 Steps |

|------------------------------------------|

| [Icon: Magnifying Glass on Document] |

| 1. Define Your Loan Needs |

| (Purchase/Refi, LTV, Property Type) |

| | |

| v |

| [Icon: Three Quote Bubbles] |

| 2. Get 3-5 Competing Quotes |

| (Include top contenders like OfferMarket)|

| | |

| v |

| [Icon: Side-by-side Papers] |

| 3. Compare Loan Estimates |

| (Focus on APR and lender fees in Box A)|

| | |

| v |

| [Icon: Star Ratings] |

| 4. Read Reviews & Get References |

| (Check Google, BiggerPockets, etc.) |

| | |

| v |

| [Icon: Person with Headset] |

| 5. Interview the Loan Officer |

| (Assess expertise and communication) |

+------------------------------------------+

```

4. Image section breakdown:

- **Header:**](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773254283955_2kzol8.jpg?alt=media&token=7ba2ffc4-3bb6-4bd2-a43e-f2cd3a2b445b)

The OfferMarket Advantage: More Than Just a Lender

In a sea of lenders, OfferMarket stands out not just for its competitive rates and fees, but for its fundamental approach to real estate investing. We are not a traditional bank or a sales-driven mortgage company. We are a technology company built by a team of active real estate investors who grew frustrated with the slow, opaque, and expensive financing options available in the market. We built the platform we wished we had for our own deals.

This investor-first DNA is evident in every aspect of our platform, creating a seamless and powerful ecosystem designed to help you scale your rental portfolio with speed, confidence, and a clear competitive edge.

Built for Speed and Simplicity

We understand that in real estate, time is money. A delayed closing can mean losing a deal, incurring extension fees, or missing out on rental income. That's why we've engineered our entire process around two core principles: speed and simplicity.

Our "no-doc" philosophy is at the heart of this. We focus on the property's performance, not your personal finances. This means:

- No Pay Stubs

- No W-2s

- No Tax Returns

- No K-1s

By eliminating the need to collect and analyze mountains of personal financial documents, we cut weeks of unnecessary work from the traditional underwriting process. Our streamlined digital application takes just minutes to complete, and our technology automates many of the tedious tasks that slow other lenders down. The result? We can often move from application to clear-to-close in as little as 10-15 business days, giving you the power to compete with cash buyers and close deals with certainty.

The OfferMarket Ecosystem: A 360-Degree Investor Platform

Our vision extends far beyond a single loan transaction. We aim to be your long-term, strategic partner for your entire investment journey. To achieve this, we've built an integrated ecosystem that provides value at every stage of the process.

- Listings Marketplace: Our platform includes a marketplace for off-market and wholesale properties. This isn't just a feature; it's a source of powerful market intelligence. By analyzing deal flow across the country, we have a real-time pulse on property values, rental rates, and market trends. This data-driven expertise informs our underwriting, allowing us to make faster, more accurate valuation decisions and get you better terms.

- Integrated Insurance: Securing property and casualty insurance is a critical but often frustrating part of the closing process. We've solved this by integrating insurance services directly into our platform. We can provide you with competitive quotes from top-rated carriers, ensuring you get the right coverage without the hassle of shopping around. This streamlines the underwriting process and prevents last-minute insurance-related delays.

- Diverse Loan Products: The DSCR loan is our flagship product for rental investors, but our support doesn't end there. We offer a full suite of financing solutions to meet your evolving needs, including fix and flip loans for your BRRRR projects, bridge loans for acquisitions, and HELOANs (Home Equity Loans) to tap into the equity of your existing properties. We are built to be the only financing partner you'll ever need.

The Process: From Instant Quote to Close

We've replaced the traditional, clunky mortgage process with a simple, transparent, and user-friendly experience. Here's how it works:

Step 1: Get Your Instant Quote

It all starts with our free, no-obligation quote tool. In less than 60 seconds, you can see your potential interest rate, monthly payment, and closing costs without providing sensitive personal information or impacting your credit score. This transparency empowers you to analyze deals quickly and make informed decisions on the spot. Get your instant DSCR loan quote today!

Step 2: Simple Digital Application

If you like the terms, you can move forward with our intuitive online application. The entire process is digital. You can upload the required property documents (like the lease and purchase contract) directly to our secure portal from your computer or smartphone. No printing, no scanning, no faxing.

Step 3: Dedicated Advisor Support

Once your application is submitted, you'll be paired with a dedicated Loan Advisor. This isn't a call center representative; this is an experienced professional who will be your single point of contact throughout the entire process. They are there to answer your questions, provide strategic advice, and proactively manage your file to ensure a smooth journey to the closing table.

Step 4: Fast, Efficient Closing

Our operations team works in parallel to move your loan through underwriting, appraisal, and title review as quickly as possible. You'll receive real-time updates through your online portal, so you're never left wondering about the status of your loan. We coordinate directly with the title company and closing agent to ensure a seamless and on-time closing, getting the keys to your new investment property in your hands faster.

Pre-Qualify Your Property in Seconds

Wondering if your investment property has what it takes to qualify for a DSCR loan? The first step is to run the numbers. Before you even apply, you can assess the viability of your deal with our powerful, easy-to-use calculator.

This free tool allows you to input the property's rent, purchase price, and estimated expenses to see its Debt Service Coverage Ratio instantly. It's the perfect first step to determine if your property's cash flow meets the requirements. By understanding your DSCR upfront, you can approach your financing with confidence and focus on the deals that have the highest probability of success.

Before you apply, use our free DSCR Calculator to see if your property's cash flow meets the requirements. It's the perfect first step to assess your deal's viability.

OfferMarket Loans

Check your rate

60 seconds · no credit pull