Debt Service Coverage Ratio Calculation: Step-by-Step Guide for Real Estate Investors

Last Updated: June 25, 2025

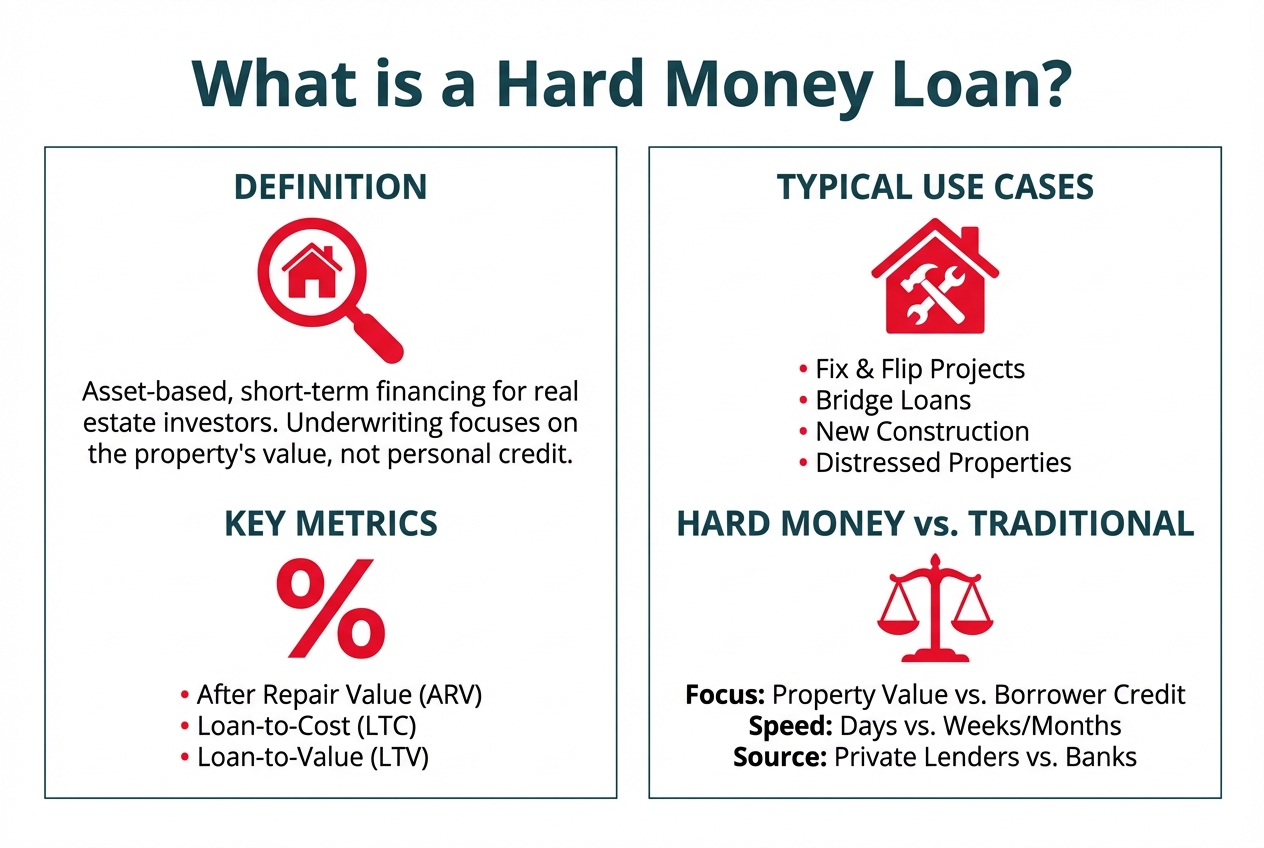

Understanding Debt Service Coverage Ratio (DSCR)

Debt service coverage ratio (DSCR) helps evaluate your ability to cover loan-related expenses using property income. Mastering DSCR ensures accurate financial analysis for investment and lending decisions.

What Is Debt Service Coverage Ratio?

Debt service coverage ratio is a financial ratio that measures how efficiently your rental income pays for specific debt service obligations. For DSCR calculation in rental real estate, use this formula:

DSCR = Rent / PITIA,

where PITIA combines Principal, Interest, Taxes, Insurance, and Association Dues.

Some analysts reference DSCR as NOI / Total Debt Service—where NOI (Net Operating Income) deducts property management, maintenance, taxes, and insurance from rent, and debt service totals principal plus interest payments.

Use the Rent / PITIA formula for consistent and relevant DSCR values when evaluating rental property finances.

Importance of DSCR in Financial Analysis

Debt service coverage ratio directly impacts loan approval processes and investment decisions. Financial institutions rely on DSCR to assess risk exposure, requiring higher DSCR values for safer loans. DSCR provides clarity on how comfortably your property covers payments—if DSCR exceeds 1, rental income exceeds PITIA, lowering risk of default.

Investors use DSCR to screen potential acquisitions and judge portfolio performance. A consistent DSCR calculation gives insights into property viability, lender requirements, and overall financial health.

Key Terms to Know

- Rent: Gross rental income from the property

- PITIA: Sum of Principal, Interest, Taxes, Insurance, Association Dues

- DSCR Formula: Rent divided by PITIA

- Principal: Repayment portion of the mortgage

- Interest: Cost of borrowing included in payments

- Taxes: Real estate taxes assessed by local authorities

- Insurance: Property insurance premiums

- Association Dues: Periodic fees for homeowners or condo associations

- Alternative DSCR Formula: NOI divided by Total Debt Service (not used in primary calculation)

- NOI (Net Operating Income): Rent minus property management, maintenance, taxes, and insurance

- Debt Service: Combined principal and interest payments

Use the correct DSCR formula for accurate, relevant financial analysis of rental property and debt obligations.

Materials and Information Needed

Accurate debt service coverage ratio calculation depends on collecting specific financial records and relevant data. Use these details to ensure your DSCR formula works for rental properties and provides reliable results.

Financial Statements Required

Income statement extracts:

Pull rent amounts directly from monthly or annual rental income lists. Use documented gross rent values to strengthen your debt service coverage ratio calculation, avoiding the use of net operating income or properties that only show NOI.

Mortgage statements:

Provide both principal and interest components. Obtain the most recent amortization schedule to detail loan terms for your DSCR calculation.

Property tax records:

Show annual or semiannual property tax amounts from reliable statements. Use tax payment receipts or county assessor documentation for DSCR formula accuracy.

Insurance bills:

List current yearly insurance premiums covering property risk. Ensure these are official insurance documents for your debt service coverage ratio calculation.

Homeowner association dues (HOA):

Add regular HOA fees, using invoices or official payment schedules to reflect association dues in your DSCR calculation.

Gathering Debt Obligations Data

Identify all fixed debt payments:

Include principal and interest by examining loan statements or payment coupons, ensuring each loan's complete cost is considered in your debt service coverage ratio calculation.

Exclude non-relevant property expenses:

Do not use management costs, maintenance, or other operating expenses for the DSCR calculation using the rent/PITIA formula. If a source lists net operating income or alternative versions (e.g., DSCR = NOI / Total Debt Service), verify you only capture rent and PITIA components for consistent debt service coverage ratio calculation.

Assemble data by property:

Keep rent totals, principal payments, interest amounts, property taxes, insurance premiums, and association dues clearly organized for each asset under analysis to maintain the integrity of your debt service coverage ratio calculation.

Verify information accuracy:

Review documents for recent changes, such as altered tax rates, new loan terms, or insurance policy adjustments, to avoid skewing the DSCR calculation with outdated figures.

Each entry ensures your materials fit the rent/PITIA formula, securing the most reliable debt service coverage ratio calculation for your rental real estate goals.

Steps for Debt Service Coverage Ratio Calculation

Steps for debt service coverage ratio calculation use a property-specific method for rental properties. Debt service coverage ratio calculation requires accurate data entry and consistent use of the DSCR formula.

Step 1: Determine Net Operating Income (NOI)

Calculate net operating income using rent as the main income component for the debt service coverage ratio calculation. Net operating income in the debt service coverage ratio calculation excludes property management costs, maintenance fees, property taxes, and insurance because the preferred formula focuses on gross rent and loan expenses.

Net operating income for this specific debt service coverage ratio calculation uses only monthly rental income. Do not subtract management, maintenance, or insurance in this instance. Verify that the rent amount is current and directly tied to the property being analyzed for the most reliable debt service coverage ratio calculation.

Some formulas include net operating income as NOI = Rent - Property Management - Maintenance - Taxes - Insurance. For the most common version of the debt service coverage ratio calculation in rental real estate, use straight rent, not NOI adjusted for expenses. Reserve adjusted NOI calculations for scenarios using a general DSCR = NOI / Total Debt Service formula, which does not apply here.

Organize the rent figures property by property if analyzing multiple rentals for batch debt service coverage ratio calculation. This method supports consistent comparison and easier tracking through the debt service coverage ratio calculation process.

Continue to focus on accurate rent data inputs as you progress through the remaining steps of the debt service coverage ratio calculation.

Step 2: Identify Total Debt Service

After establishing your rent figures, focus on the total debt service calculation to ensure a precise debt service coverage ratio calculation for each property.

What Constitutes Debt Service?

Total debt service components directly affect the debt service coverage ratio calculation. Use the PITIA formula:

PITIA = Principal + Interest + Taxes + Insurance + Association Dues

For your debt service coverage ratio calculation, include property tax, insurance premiums, homeowner association dues, principal, and interest payments.

Exclude maintenance, management fees, and utilities since these do not meet the PITIA framework.

Other formulas for debt service coverage ratio calculation sometimes use only principal and interest for the denominator (Total Debt Service), but this approach does not align with the rent/PITIA calculation. Do not mix net operating income–based methods or deduct property expenses like property management, maintenance, or insurance from rent when calculating the debt service coverage ratio according to PITIA.

Rely on the PITIA method for consistency in your debt service coverage ratio calculation. Reference combined sources such as Fannie Mae and Freddie Mac for multifamily loan underwriting and property lending, which prioritize this structure.

Considering Principal vs. Interest Payments

Both principal and interest payments play a critical role in the debt service coverage ratio calculation.

Principal pays down the mortgage balance, while interest represents the lending cost.

Debt service coverage ratio calculation with the PITIA method always includes both principal and interest, alongside property taxes, insurance, and association dues, to capture your actual loan obligations for the period.

Alternative approaches to the debt service coverage ratio calculation, like NOI/Total Debt Service, only use principal plus interest for debt service, but these omit costs relevant for your rent/PITIA ratio.

Maintain alignment with rent/PITIA for all your debt service coverage ratio calculation steps to produce reliable and comparable ratios across rental properties.

Debt service coverage ratio calculation accuracy depends on correct inclusion of each PITIA component for every financed property. Consistently check mortgage statements, tax bills, and insurance declarations to determine payments for the debt service coverage ratio calculation.

If multiple loans exist, sum the PITIA for every mortgage to determine the overall denominator for the debt service coverage ratio calculation. This structured approach ensures your debt service coverage ratio calculation matches lender requirements and best practices.

Step 3: Apply the DSCR Formula

Step 3 covers how you apply the debt service coverage ratio calculation using the property-specific formula accepted by most real estate lenders. Rely on your verified rent income and consistent PITIA numbers for every debt service coverage ratio calculation.

The Standard DSCR Formula Explained

Apply the debt service coverage ratio calculation using the standard formula for rental properties:

DSCR = Rent / PITIA

- Rent covers the gross rental income only for the specific property in your debt service coverage ratio calculation.

- PITIA stands for Principal, Interest, Taxes, Insurance, and Association Dues, which together reflect your full required property loan payment for debt service coverage ratio calculation purposes.

The industry sometimes presents a different formula:

DSCR = NOI / Total Debt Service

- NOI means Net Operating Income, which subtracts property management fees, maintenance, taxes, and insurance from rent.

- Total Debt Service combines just the principal and interest from the loan.

Use only the Rent / PITIA method for debt service coverage ratio calculation with rental real estate to align with lender requirements, unless the context specifically requests NOI-based analysis. This approach removes variables that can skew results and keeps every debt service coverage ratio calculation accurate and comparable property to property.

Example DSCR Calculation

Follow this process for a clear debt service coverage ratio calculation example:

- Rent (Gross Rental Income): $2,500 per month

- PITIA (Total Monthly Debt Payment):

- Principal: $700

- Interest: $300

- Taxes: $200

- Insurance: $100

- Association Dues: $50

- Total PITIA: $1,350

Debt Service Coverage Ratio Calculation Table

| Component | Value | Description |

|---|---|---|

| Rent | $2,500 | Monthly rental income |

| PITIA | $1,350 | Debt obligation total |

- Insert numbers into the formula:

DSCR = Rent / PITIA

DSCR = $2,500 / $1,350

- Calculate:

DSCR = 1.85

A debt service coverage ratio calculation result of 1.85 shows the property generates $1.85 in rental income for every $1 owed in PITIA payments, qualifying for most lender minimums in your debt service coverage ratio calculation.

Maintain your debt service coverage ratio calculation using the Rent / PITIA model. Avoid the NOI-based formula for these analyses, as lender standards and accurate debt service coverage ratio calculation demand a focus on gross rental income and complete PITIA breakdown. For every new property considered, repeat this debt service coverage ratio calculation using the latest rent and PITIA figures to support confident loan and investment decisions.

Interpreting the DSCR Results

Understanding how to interpret the debt service coverage ratio calculation helps you evaluate a property’s financial performance and make practical investment decisions. When you interpret DSCR results, consider lender expectations and recognize how DSCR influences your capacity to secure loans or refinance.

What Is a Good DSCR?

A good debt service coverage ratio calculation result means the property’s rental income clearly exceeds its debt obligations. A DSCR above 1.25 represents a financially healthy property in most real estate contexts. Lenders and investors favor DSCR values such as 1.25, 1.5, or higher, because these numbers mean the rental income comfortably covers monthly PITIA payments. For example, if your property yields a DSCR of 1.5, it generates $1.50 in rent for every $1 of PITIA. A DSCR below 1.0 signals inadequate rent to fulfill loan commitments and represents a significant credit risk. Properties at or below a 1.0 DSCR—such as 0.98, 0.85, or lower—often struggle to qualify for conventional loans. When running your own debt service coverage ratio calculation, always use the Rent / PITIA formula:

DSCR = Rent / PITIA

Rent covers the property’s gross monthly rental income, while PITIA incorporates Principal, Interest, Taxes, Insurance, and Association Dues. Some models use a different debt service coverage ratio calculation formula—DSCR = NOI / Total Debt Service—but you avoid this for property-specific analyses. In the NOI formula, Net Operating Income (NOI) removes property management, maintenance, taxes, and insurance from rent, while total debt service only counts principal and interest. For clear and lender-accepted debt service coverage ratio calculation results, stick with Rent / PITIA.

How Lenders Use DSCR

Lenders use your debt service coverage ratio calculation as a primary metric when reviewing real estate loans, refinance requests, or portfolio purchases. Banks and institutions verify DSCR values from your property’s most recent financial data, applying the Rent / PITIA debt service coverage ratio calculation. Minimum standards often vary by lender type, loan size, and property type, but most require a DSCR above 1.20 for investment and rental properties. The DSCR informs lenders about your capacity to cover debt payments from property operating income, not personal resources. When DSCR values exceed 1.25 or 1.35, lenders classify your loan application as low risk and may offer lower interest rates or higher loan-to-value ratios. If your debt service coverage ratio calculation falls below lender thresholds, banks may deny your application or require a larger down payment, higher reserves, or additional guarantees. When you compare results with alternative debt service coverage ratio calculation methods—such as NOI / Total Debt Service—the lender’s preference for Rent / PITIA ensures consistency across underwriting standards. This comparison reinforces the importance of correct formula usage in your DSCR assessments.

Impact of DSCR on Borrowing Capacity

Your borrowing capacity directly depends on the outcome of your debt service coverage ratio calculation. Higher DSCR results significantly increase your maximum eligible loan amount and improve negotiation leverage with lenders. For instance, a property with a calculated DSCR of 1.5 may qualify for 75 to 80 percent loan-to-value (LTV), while a DSCR at 1.20 could limit you to a 65 to 70 percent LTV. If debt service coverage ratio calculation results fall, lenders reduce available loan amounts to ensure future PITIA payments remain manageable. When you optimize rent collection or reduce monthly PITIA, your DSCR improves and your borrowing power increases. Consistently applying the Rent / PITIA debt service coverage ratio calculation, you can model loan scenarios and recognize how principal paydown or rent increases adjust your financial profile. Reviewing DSCR with each loan-related decision enables you to respond effectively to lender requirements and capture financing opportunities without risk of default. Simultaneously, avoiding the NOI-based debt service coverage ratio calculation preserves lender confidence and supports a stronger financial application.

| DSCR Value | Typical Lender View | Borrowing Impact |

|---|---|---|

| 1.25 and above | Low risk | Greater approval odds, higher LTV, better terms |

| 1.0 to 1.24 | Moderate risk | Reduced approval odds, limited loan amount |

| Below 1.0 | High risk | Frequently denied or requires personal guarantees |

Debt service coverage ratio calculation remains central to all lending and investment strategies. Use Rent / PITIA consistently for clear communication with banks, and reference prior debt service coverage ratio calculation results to support your financial goals.

Tips, Warnings, and Common Mistakes

Accurate debt service coverage ratio calculation prevents loan issues and supports property investment planning. Attention to formula use and input data ensures consistency throughout the DSCR calculation process.

Common Calculation Errors to Avoid

- Misapplying the Debt Service Coverage Ratio Calculation Formula

Correct debt service coverage ratio calculation uses the Rent / PITIA formula for rental property analysis. PITIA combines Principal, Interest, Taxes, Insurance, and Association Dues. If you use Net Operating Income or NOI instead of gross Rent, or substitute Total Debt Service for PITIA, the debt service coverage ratio calculation may not reflect the standard used by most lenders.

Debt service coverage ratio errors often result from confusing the second formula (DSCR = NOI / Total Debt Service), which subtracts property management, maintenance, and other costs from Rent before dividing by a narrower definition of debt payments. Lenders and analysts generally disregard DSCR results obtained using the NOI method for property underwriting. Reference only gross Rent and annualized PITIA items to align your calculations with best practices.

- Including Irrelevant Expenses in Debt Service Coverage Ratio Calculation

Include only Principal, Interest, Taxes, Insurance, and Association Dues in PITIA during debt service coverage ratio calculation. Exclude management fees, maintenance, utilities, and other property operations costs for reliable DSCR calculations. Non-mortgage expenses distort debt service coverage ratio calculation results, misleading underwriters.

- Using Inconsistent Time Periods for Debt Service Coverage Ratio Calculation Inputs

Align Rent and PITIA for the same monthly or annual time period in every debt service coverage ratio calculation. Mismatched periods invalidate DSCR interpretation and lead to overstated or understated results.

Adjustments for Variable Income or Seasonal Businesses

- Period-Averaged Rent in Debt Service Coverage Ratio Calculation

Compute gross Rent based on 12 months of historical income if your rental properties experience seasonal fluctuations. Rely on a single peak or trough month only when calculating debt service coverage ratio distorts lender perception of your cash flow stability. For hospitality or vacation rentals, use a rolling average of gross rental income for precise debt service coverage ratio calculation.

- Document Income Volatility for Debt Service Coverage Ratio Calculation

Attach clear supporting schedules showing seasonal or irregular Rent so that your DSCR calculation remains transparent. Lenders reviewing debt service coverage ratio calculation require evidence of income sustainability, especially if your business model relies on variable monthly receipts.

- Adjust PITIA Timelines for Balloon Payments in Debt Service Coverage Ratio Calculation

Review mortgage terms for irregular or balloon payments and include these in your overall PITIA figure when performing debt service coverage ratio calculation. Failure to capture one-off or accelerated payments skews your debt service coverage ratio and results in unforeseen cash shortfalls.

DSCR vs. Other Financial Ratios

- Debt Service Coverage Ratio Calculation as Loan Qualification Metric

Rely on the debt service coverage ratio calculation for the primary assessment of loan-repayment capacity in property finance. Unlike Loan-to-Value or Debt-to-Income ratios, debt service coverage ratio calculation quantifies how much your gross Rent exceeds required loan payments, including tax and insurance obligations. This direct approach makes the debt service coverage ratio calculation central to property underwriting standards.

- Debt Service Coverage Ratio Calculation vs. NOI-Based Metrics

Recognize that the traditional debt service coverage ratio calculation (Rent / PITIA) produces a different result from any NOI-based ratio. NOI calculations subtract property management, maintenance, tax, and insurance expenses before division by debt service, introducing more variables and less consistency for rentals or multifamily buildings. Standard lender analyses prefer pure Rent over PITIA because debt service coverage ratio calculation highlights gross cash flow leverage rather than operational efficiency.

- Interpreting Debt Service Coverage Ratio Calculation Alongside Other Ratios

Supplement debt service coverage ratio calculation with metrics like Cap Rate or Cash-on-Cash Return for a comprehensive property financial review. Only debt service coverage ratio calculation ranks primary for demonstrating debt sustainability in credit review scenarios and investor reports.

| Formula Used | Numerator | Denominator | Common Context | Preferred in Real Estate |

|---|---|---|---|---|

| Rent / PITIA | Rent | PITIA (P+I+T+I+A) | Rental Property Underwriting | Yes (DSCR calculation) |

| NOI / Total Debt Service | Gross Rent - Expenses | Principal + Interest | Commercial Real Estate, Other | No |

Debt service coverage ratio calculation directly impacts your loan eligibility and investment risk, especially when consistent methods and accurate timeframes support your reports. Accurate and consistent debt service coverage ratio calculation builds lender and investor confidence while unnecessary formula changes cause confusion and delays.

Troubleshooting DSCR Calculations

Debt service coverage ratio calculation accuracy depends on using the correct formula and reliable financial data. Even with careful planning, issues and outliers can affect results.

Dealing with Incomplete or Inaccurate Data

Identifying data gaps improves debt service coverage ratio calculation consistency. Common sources for errors include missing rent records, outdated PITIA breakdowns, or incomplete property tax statements. Reviewing recent lease agreements, mortgage statements, and insurance bills avoids outdated DSCR inputs. Cross-checking rental income reports with deposits helps catch discrepancies. For multi-family properties, reconciling rent totals by unit and month ensures debt service coverage ratio calculation accuracy.

Collecting current association dues statements confirms the correct PITIA value for an accurate debt service coverage ratio calculation. If documentation is missing, requesting official copies from banks or associations supports reliable calculations. Documenting any unavoidable estimates with footnotes allows later review and potential recalculation.

What If the DSCR Is Too Low?

A low debt service coverage ratio calculation value signals that rental income cannot cover property debt payments. Lenders typically reject loan applications when the DSCR falls below 1.0, denying financing to high-risk borrowers.

Increasing rental income, for example by filling vacancies, raising rents, or improving tenant retention, can immediately impact the ratio. Reducing PITIA—by refinancing for a lower interest rate, reducing principal, or lowering insurance premiums—improves results. Negotiating lower property taxes or association dues increases your DSCR as well. For properties with variable monthly cash flow, averaging rent across a 12-month period provides a more stable DSCR calculation.

If enhancing income or reducing PITIA does not raise the ratio above the lender’s minimum, delaying new loans or seeking alternative financing avoids costly rejections. Always use the Rent / PITIA formula for your DSCR calculation; including improper adjustments or switching to NOI-based formulas introduces errors that undermine financial assessments.

Alternative Methods for Complex Scenarios

Special circumstances such as mixed-use buildings, multiple loans, or short-term rental operations complicate debt service coverage ratio calculation efforts. For these, using the correct method clarifies financial strength for lenders. Always prioritize the standard formula: DSCR = Rent / PITIA is accepted for most rental real estate and aligns with lender requirements.

Alternative methods, such as DSCR = NOI / Total Debt Service—where Net Operating Income (NOI) deducts property management, maintenance, taxes, and insurance from rent, and debt service covers only principal and interest—do not apply to most rent-based property loans. Mixing formulas causes confusion; lenders might reject NOI-based DSCR results for not matching loan underwriting criteria.

For properties with multi-loan structures, adding the PITIA of each loan in the denominator of the Rent / PITIA formula matches how lenders assess the debt service coverage ratio calculation in portfolio or multi-property reviews. For portfolios of different property types, calculating the DSCR separately for each asset avoids skewing results caused by non-uniform rental or PITIA figures.

If your scenario demands the NOI approach (for instance, in certain commercial real estate transactions), clarify calculation details and source documentation for every entity involved. When possible, stick to the Rent / PITIA method in debt service coverage ratio calculation for transparency and loan application success. Consistent application reduces errors and builds lender confidence in your DSCR results.

Conclusion

Mastering the debt service coverage ratio puts you in control of your financial decisions whether you're investing in real estate or applying for a business loan. By using the right formula and keeping your data accurate you'll build confidence with lenders and set a solid foundation for growth. Approach each calculation with care and you'll be well equipped to make informed choices that support your long-term financial success.

Frequently Asked Questions

What is the Debt Service Coverage Ratio (DSCR)?

The Debt Service Coverage Ratio (DSCR) is a financial metric that measures if your rental property’s income can cover its debt payments. It’s calculated by dividing gross rent by your monthly debt payments (PITIA: Principal, Interest, Taxes, Insurance, Association Dues). A higher DSCR means your income comfortably covers your loan obligation.

Why is DSCR important for business loans and real estate investing?

DSCR is crucial because lenders use it to assess if your property or business generates enough income to meet loan payments. A strong DSCR increases your chances of loan approval and helps you manage debt responsibly, ensuring long-term financial stability.

How do you calculate DSCR for rental property?

To calculate DSCR for rental property, use the formula: DSCR = Rent / PITIA. Rent is your gross monthly rental income, and PITIA stands for Principal, Interest, Taxes, Insurance, and Association dues. This gives you a clear picture of your property's ability to cover its debt.

What financial records do I need to calculate DSCR accurately?

You need accurate rent statements, mortgage statements, property tax records, insurance bills, and homeowner association dues. Make sure the data is up-to-date and organized by property. Exclude unrelated expenses like maintenance or utilities to avoid skewing the results.

What is considered a “good” DSCR by lenders?

Most lenders look for a DSCR above 1.25. This means your property earns at least $1.25 in rent for every $1 in debt payments. A higher DSCR indicates lower risk for lenders and may help you qualify for larger loans or better terms.

What is PITIA in the DSCR calculation?

PITIA stands for Principal, Interest, Taxes, Insurance, and Association dues. It represents your total monthly debt service for a property and is used as the denominator in the DSCR formula to assess whether rental income covers all loan-related obligations.

What are common mistakes when calculating DSCR?

Common mistakes include using the wrong formula (like including Net Operating Income or other expenses), mixing time frames for rent and PITIA, and using outdated financial data. Always use gross rent and make sure PITIA is accurate and consistent.

How can I improve my DSCR?

You can improve DSCR by increasing your property’s rental income or by lowering your monthly debt payments. Refinancing a loan at a lower rate or paying off some principal can help, as can finding strategies to boost rent while keeping occupancy high.

What should I do if my DSCR is below 1.0?

A DSCR below 1.0 means your rental income isn’t enough to cover your debt payments. Consider raising rent, cutting costs, or restructuring your loan to reduce monthly payments. You should address this quickly, as lenders may view your property as high-risk.

How does DSCR compare to other financial ratios in real estate?

DSCR is one of the most important ratios for lenders because it directly reflects your ability to repay loans. While other ratios (like loan-to-value or cap rate) are also considered, a strong DSCR is often a deciding factor for loan approval.

DSCR Calculation and Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull