*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Debt Service Coverage Ratio (DSCR) Loan Guide

Last Updated: October 7, 2025

As a real estate investor focused on single-family and small multifamily (1-4 unit) rental properties, you're always looking for financing options that align with your goals of building wealth through cash-flowing assets. Enter the DSCR loan—a powerful tool designed specifically for investors like you. Unlike traditional mortgages that scrutinize your personal income, DSCR loans qualify you based on the property's rental income, making them ideal for scaling your portfolio without the hassle of tax returns or W-2s.

In this comprehensive DSCR loan guide, we'll cover everything from the basics of what a DSCR loan is to advanced strategies for optimizing your rates and terms. Whether you're a first-time investor or a seasoned pro using the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), this guide provides actionable insights to help you secure the best financing. At OfferMarket, our mission is to empower rental investors with low-cost DSCR loans, transparent terms, and tools like our instant quote system—no credit pull required.

Get your personalized DSCR loan quote in just 1 minute—no obligation, no credit impact.

What Is a DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a type of non-qualified mortgage (Non-QM) tailored for real estate investors. It allows qualification based on the cash flow generated by the investment property itself, rather than your personal income or employment history. This makes DSCR loans a game-changer for self-employed investors, those with multiple properties, or anyone with complex finances that don't fit traditional lending boxes.

Lenders calculate the DSCR by comparing the property's gross rental income to its total monthly debt obligations (known as PITIA: Principal, Interest, Taxes, Insurance, and HOA fees). If the ratio meets or exceeds the lender's threshold—typically 1.0 or higher—the loan can proceed. This focus on property performance shifts the emphasis from you as the borrower to the asset's viability, enabling faster approvals and more flexible underwriting.

DSCR loans are business-purpose loans, meaning they're exclusively for investment properties like single-family homes, duplexes, triplexes, or quadplexes. You can't use them for primary residences. They're available for purchases, rate-and-term refinances, or cash-out refinances, with loan amounts ranging from $50,000 to $2,000,000.

Key Features of DSCR Loans

Here's a quick overview of what sets DSCR loans apart:

| Feature | Details |

|---|---|

| Qualification Criteria | Based on property’s cash flow (DSCR ≥ 1.0–1.25), not personal income. |

| Ideal Borrowers | Real estate investors, self-employed individuals, or those with limited income proof. |

| Loan Types | Purchase, refinance (rate-and-term or cash-out), fixed or adjustable rates. |

| Documentation | Minimal—no tax returns, W-2s, or employment verification. |

| Loan Amount | $50,000–$2,000,000. |

| Credit Score Minimum | 660 (US citizens/green card holders); no score required for foreign nationals. |

| Down Payment (Purchase) | 20–35% depending on credit and property type. |

| Seasoning (Refinance) | None or 90 days with OfferMarket; up to 6 months with other lenders. |

How Does a DSCR Loan Work?

At its core, a DSCR loan evaluates the property's ability to "service" its debt. The process starts with an appraisal that determines the property's market value and potential rental income. Lenders then use this data to compute the DSCR.

DSCR Formula and Calculation

The DSCR formula is simple yet powerful:

DSCR = Gross Rental Income ÷ PITIA

- Gross Rental Income: Annual rent from the property (e.g., from long-term leases, mid-term rentals, or short-term like Airbnb).

- PITIA: Principal + Interest + Taxes + Insurance + HOA fees

For example, if a duplex generates $60,000 in annual rent and has $50,000 in annual PITIA, the DSCR is 1.2 ($60,000 ÷ $50,000). A ratio above 1.0 indicates positive cash flow, which most lenders require. OfferMarket prefers a DSCR of at least 1.0, but higher ratios can unlock better rates and higher loan-to-value (LTV) ratios.

Lenders may adjust rental income for vacancies (e.g., applying a 5–10% vacancy rate) or use appraiser-provided rent schedules for short-term rentals. Once approved, the loan funds like any mortgage, but with streamlined documentation—often just a credit check, property appraisal, and lease agreements.

Eligibility Requirements for DSCR Loans

Qualifying for a DSCR loan is straightforward, but you must meet borrower and property criteria.

Borrower Criteria

- Credit Score: Minimum 660 for US citizens or green card holders. Higher scores (720+) yield better rates and higher LTVs. Foreign nationals may qualify without a score.

- Experience: Not required at OfferMarket—we work with investors of all levels.

- Liquidity: Cash to close plus 9 months of PITIA reserves (12 months for foreign nationals). HELOC funds aren't officially allowed for verification, but guidelines check only recent bank statements.

- Borrowing Entity: LLCs, corporations, partnerships, or revocable trusts are eligible.

Property Eligibility

- Rental Income: Must cover PITIA to achieve the required DSCR.

- Property Types: Single-family, 2–4 unit multifamily, condos, townhomes, short-term rentals (i.e. Airbnb), rural properties (with lender discretion), mixed-use.

- Condition: C1–C4 rating; deferred maintenance must be cured before funding.

- Size: Minimum 700 sq ft for single-family, 500 sq ft per unit for multifamily.

- Appraisal: Required to confirm value and rental potential.

Important: Properties must be investment-focused. For short-term rentals, lenders scrutinize occupancy rates and may use projected income.

Property Types Eligible for DSCR Loans

DSCR loans support a wide range of 1–4 unit residential properties. Here's a breakdown:

- Single-Family Homes: standalone rentals and townhomes for long-term tenants—easiest to finance.

- Multi-Unit Properties (2–4 Units): Higher yields but slightly higher rates; max LTV often 70–80%.

- Condos: non-warrantable can cause issues with approval

- Short-Term Rentals: Airbnb/VRBO eligible, expect higher rates and lower LTV

- Rural Properties: Allowed but may have lower LTVs due to appraisal challenges.

- Mixed-Use: Residential with commercial elements

For 5+ units, rates and terms are less favorable.

How to Calculate DSCR Loan Rates

DSCR loan rates are dynamic and investor-friendly when structured right. The formula is:

DSCR Loan Rate = 5-Year US Treasury Yield + Credit Spread

- 5-Year US Treasury: The "risk-free" benchmark—volatile based on economic factors like inflation and Fed policy.

- Credit Spread: 2.5–4.5% premium reflecting risk; influenced by credit score, LTV, DSCR, property type, prepayment penalty, and market demand.

At OfferMarket, our credit spread is often 0.1–0.25% below the national average due to competitive institutional partnerships.

Factors Affecting Credit Spread

| Factor | Impact on Credit Spread |

|---|---|

| Credit Score | Higher score = lower spread (e.g., 760+ = base; 660–679 = +0.50%). |

| LTV | Lower LTV = lower spread (e.g., 80% = +0.4%; <60% = +0.0%). |

| DSCR | Higher DSCR = lower spread. |

| Property Type | Lower unit count/non-rural = lower spread. |

| Prepayment Penalty | Longer penalty = lower spread (e.g., 5-4-3-2-1 = base; no penalty = +0.28125%). |

| Loan Amount | Higher amount = lower spread (e.g., $150K+ = base; <$50K = +0.5%). |

| Market Demand | High demand = lower spread; uncertainty widens it. |

Current rates are attractive but volatile—monitor the 5-Year Treasury and get an instant quote for personalized pricing.

Benefits of DSCR Loans

DSCR loans shine for portfolio growth:

- No Personal Income Docs: Perfect for self-employed or complex finances.

- Unlimited Properties: No cap on financed assets.

- Fast Approvals: Minimal paperwork means quicker closings (15–25 days at OfferMarket).

- Flexible Terms: Fixed/ARM, interest-only options, full amortization.

Drawbacks of DSCR Loans

Be aware of trade-offs:

- Higher Rates: 0.4–0.75% above conventional loans.

- Down Payments: 20–35% required.

- Property Dependency: Low-income properties may not qualify.

- Prepayment Penalties: Common for 1–5 years.

DSCR Loans vs. Conventional Loans

DSCR loans offer flexibility at a cost:

| Aspect | DSCR Loan | Conventional Loan |

|---|---|---|

| Qualification | Property cash flow | Personal income/credit |

| Documentation | Minimal | Extensive (taxes, pay stubs) |

| Down Payment | 20–35% | 5–20% |

| Property Types | Investment only | Primary/secondary/investment |

| Interest Rates | Higher (e.g., 6–8%) | Lower (e.g., 5–7%) |

| Approval Time | Faster (15–30 days) | Longer (30–60 days) |

| Property Limit | Unlimited | Typically 10 financed |

How to Improve Your DSCR

Boost your ratio for better terms:

- Increase Rental Income: raise rents or add amenities.

- Lower PITIA: Shop insurance, appeal taxes, or refinance at lower rates.

- Property Upgrades: Renovations enhance value and rents.

Use our DSCR calculator to test scenarios.

Steps to Apply for a DSCR Loan

- Find a deal: Best deals are off market properties.

- Run your numbers: Verify property eligibility.

- Get quote: Instant quote and pre-approval from OfferMarket.

- Processing: Submit loan application, borrowing entity docs, authorize appraisal.

- Finalize terms: secure terms post-approval with a rate lock.

- Close: Fund in 15–30 days.

Case Study: Scaling with DSCR Loans

An investor used the BRRRR method on a duplex: Purchased for $200K, rehabbed for $50K, rented for $50K/year annual income. PITIA: $32.5K. DSCR: 1.54. Cash-out refi yielded $25K plus $1,458/month cash flow—reinvested into another deal.

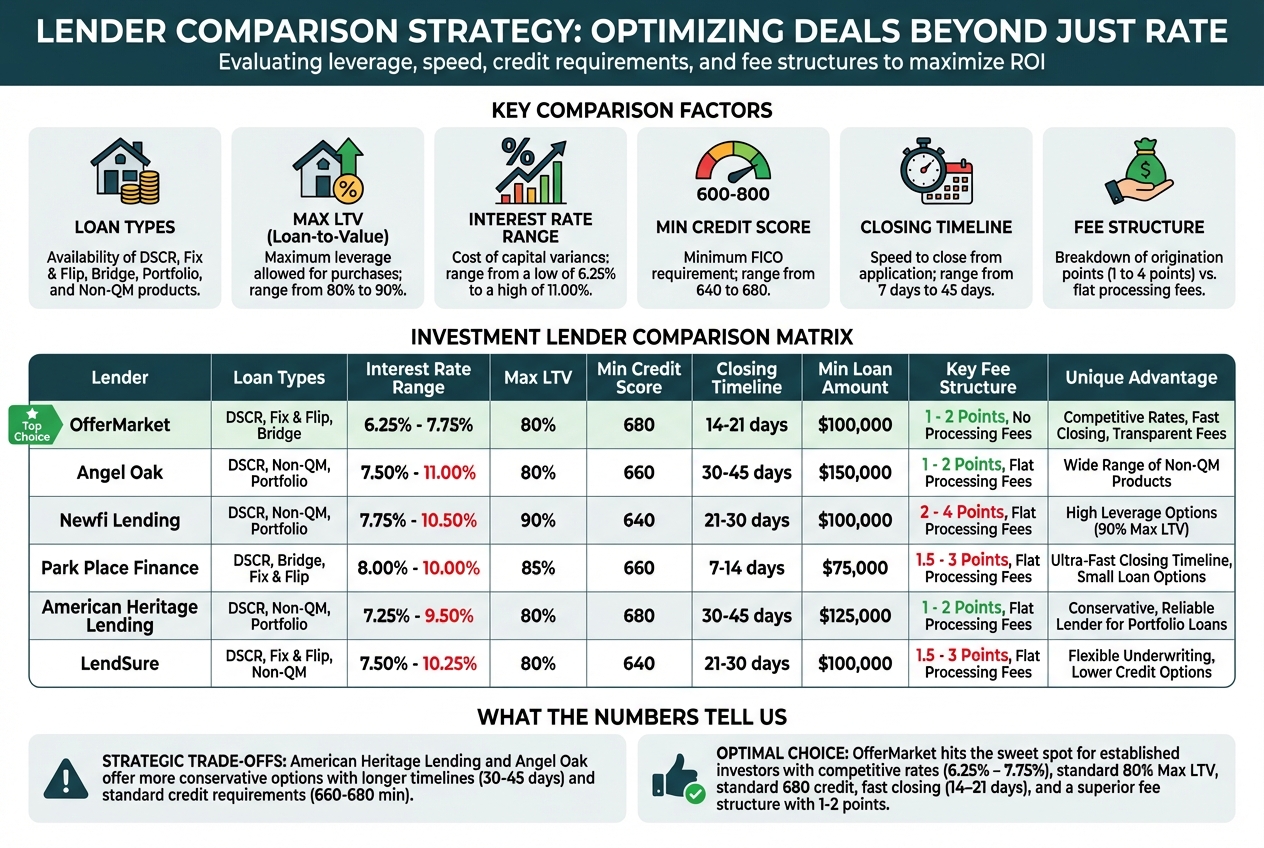

Tips for Finding the Best DSCR Loan Lenders

- Specialization: Seek DSCR experts.

- Compare Terms: Rates (including APR), LTV, fees.

- Flexible Credit: Look for soft pulls.

- Transparency: Avoid hidden fees.

| Lender Feature | OfferMarket | Lender A | Lender B |

|---|---|---|---|

| Minimum DSCR | 1.00 | 1.00 | 1.25 |

| Credit Spread | 2.5–3.5% | 3.25% | 3.5% |

| Maximum LTV | 80% (purchase) | 80% | 75% |

| Prepayment Penalties | Flexible options | Yes | No |

| Origination Fee | 0.5–1% | 1% | 1.5% |

| Lender Fees | $1,495–$1,995 | $1,495 | $1,995 |

Cash-Out Refinance with No Seasoning

Traditional lenders require 6 months of ownership before cash-out refinances, but OfferMarket offers no seasoning (or 90 days) for faster capital recycling—ideal for BRRRR investors.

| No Seasoning Terms | Guidelines |

|---|---|

| Interest Rate | Instant quote |

| Min Loan Amount | $55,000 |

| Max LTV | 80% |

| Max LTC | 110% (no seasoning); 140% (90+ days) |

| Min Verified Rehab | 10% of purchase price (no seasoning) |

| Origination Fee | 0.5 to 1 points ($1,500 minimum) |

| Time to Close | 15–25 days |

This eliminates delays, letting you scale faster.

OfferMarket DSCR Loan Program Guidelines

| Criteria | Guidelines |

|---|---|

| Loan Amount | $50K–$2M |

| Min As-Is Value | $100K (single); $71.5K (portfolio) |

| Experience | Not required |

| Min Credit Score | 660 (US); none (foreign) |

| Liquidity | Cash to close + 3 to 9 months PITIA |

| Borrowing Entity | LLC, Corporation, LP, Revocable Trust |

| Max LTV | Purchase: 80%; Cash-Out: 75% or 80% |

| Term | 30 years |

| Amortization | Full or interest-only (5/25 or 10/20) |

| Prepayment Penalty | 5-4-3-2-1, 4-3-2-1, 3-2-1, 2-1, 1-0, 0-0-0 |

| Recourse | Full (51% guarantee) |

| Condition Rating | C1–C4 |

| Min Sq Ft | 700 (SF); 500/unit (multifamily) |

| Max Lot Size | 5 acres |

| Rural Properties | Discretion; lower LTV |

| Foreign Nationals | Max LTV 65–70%; 12 months reserves |

Glossary of DSCR Loan Terms

- DSCR: Ratio of rental income to debt.

- PITIA: Total monthly payment.

- LTV: Loan-to-value ratio.

- Non-QM: Non-qualified mortgage.

- Cash-Out Refi: Refinance pulling equity.

- Prepayment Penalty: Fee for early payoff.

- NOI: Net operating income.

- Cap Rate: NOI / Property Value.

For full terms, see our resources.

Frequently Asked Questions

How does a DSCR loan work?

It qualifies based on property income covering PITIA.

What is the downside?

Higher rates and down payments.

Is it hard to qualify for a DSCR loan?

No, with 660+ credit, clean background, liquidity and strong DSCR.

What is the minimum down payment for a DSCR loan purchase transaction?

20%

Can I get a DSCR loan with no money down?

No, max 80% LTV (20% down payment).

What is the current DSCR loan rate?

See our DSCR Loan Interest Rate Index™.

Can I get a DSCR loan for primary residence?

No, investment purpose only. You will be required to sign a "business purpose affidavit" attesting to the fact that you will not use the property a personal residence.

How does DSCR loan compare to hard money?

| DSCR Loan | Hard Money | |

|---|---|---|

| Term | 30 years | 6 to 24 months |

| Interest rate | Low | High |

| LTV (cost) | 75% to 80% | 80% to 100% |

| Prepayment penalty | Common | Not common |

| Origination fee | 0.5% to 3% | 1% to 4% |

| Appraisal | Required | May not be required |

| Secondary valuation | Required | Not required |

| Property condition | C1 - C4 | Typically C4 - C6 |

| Liquidity verifiaction | Yes, 6-12 months of reserves | Not strict |

Can I get a DSCR loan without a job?

Yes, there is no income verification. DSCR loans are therefore popular among self-employed real estate investors and real estate professionals (i.e. contractors, agents).

Do banks offer DSCR loans?

Yes, some banks offer DSCR loans but private lenders like OfferMarket are often faster because banks typically require more extensive underwriting including tax returns. Banks that offer DSCR loans often offer lower LTV (i.e. 75% instead of 80%) and shorter term (i.e. 20 or 25 years instead of 30 years).

Can I get a DSCR loan with no experience?

Yes! With no rental property experience, some DSCR loan program guidelines will have the following conditions:

- Lower credit score (i.e. 660 - 699) -- may be required to have a property manager agreement in place.

- Lower LTV -- you may be subjected to a 5% LTV "haircut". i.e. if max LTV is 80%, you will be offered 75%.

As a new investor, it's important to keep it simple. Focus on 1-4 unit properties, unfurnished long-term rental (12 month lease). Avoid condos as they frequently run into approval issues due to warrantability (i.e. too much investor ownership, under reserved condo association, underinsured condo association, etc.).

What are DSCR loan closing costs?

Typically 2% to 4% for all lender fees.

Is there a minimum holding period?

A prepayment penalty may apply depending on state and property type. If there is a high probability you will sell the property or refinance in the near term, you should opt for a low or no prepayment penalty which will carry a slightly higher rate or buydown.

What are the alternatives to a DSCR loan?

Conventional loan (full underwriting), hard money (more expensive, shorter term).

Does a DSCR loan require appraisal?

Yes. DSCR loan guidelines have becomes standardized to require an appraisal ordered by the lender using an appraisal management company (AMC). A secondary valuation such as a CDA, ARR, or BPO will also be required as a way to quality control the appraisal report.

Can I use a DSCR loan for a property held in LLC?

Yes! In fact, most DSCR lender and loan programs strongly prefer or require property to be held in LLC as the borrower ("borrowing entity").

Can I pay off a DSCR loan early?

Yes, however your prepayment penalty applies to full and partial principal repayment ahead of the amortization schedule during the prepayment penalty period.

Can I get a DSCR loan for Airbnb or VRBO short term rentals (STR)?

Yes, though this will typically require a 5% LTV haircut from max LTV and possibly a slightly higher interest rate. DSCR loans for STRs are subjected to elevated scrutiny including operating experience because of volatility and risk in the short term rental market relative to long term rentals. Many institutional investors that buy DSCR loans strongly prefer long term rentals and seek to avoid STR.

Join OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors. We focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull