*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Refinance Rental Property DSCR Loan

Last Updated: February 28, 2025

If you’re looking to refinance rental property DSCR loan, you need to know about DSCR loans. DSCR loans are a fast-growing loan type designed for real estate investors, especially those without W2 salaried income, who want an easy and streamlined borrowing experience.

How DSCR Refinancing Differs: Focus on Property, Not Personal Income

DSCR loans qualify borrowers based primarily on the rental property’s income — not your personal W-2s, tax returns, or employment history. That makes them ideal for real estate investors who are self-employed, have complex finances, or own many properties. You can qualify without income verification, and you can finance an unlimited number of investment properties — as long as each meets DSCR requirements.

DSCR loans are typically 30 year fixed rate mortgages where the loan amount and interest rate is determined based on the cash flow of the rental property (DSCR), and your credit score and rental property investing experience.

DSCR stands for debt service coverage ratio, a simple cash flow metric where 1.0 indicates that the rental property operates at breakeven. A DSCR above 1 means the property generates free cash flow, while a DSCR below 1 means the property does not generate enough rent to cover its mortgage payments. Most DSCR loan programs, including ours, currently have a minimum DSCR of 1.1 to qualify for a given loan amount. As LTV (loan-to-value) increases, your DSCR decreases as a result of increased mortgage payment. This means that when your DSCR hits the minimum, that is your maximum LTV. Enough explaining, here's how to visualize the concept:

DSCR is calculated using the formula:

DSCR = Gross Rental Income / PITIA

Where:

- PITIA = Principal + Interest + Taxes + Insurance + (HOA dues if applicable)

For example, if a property earns $60,000 per year and PITIA is $50,000, the DSCR is 1.2, meaning the property generates 20% more income than needed to cover the debt.

Most lenders require a DSCR of at least 1.0, though 1.1 to 1.25 is typical for refinances. A higher DSCR means more cash flow and greater loan eligibility.

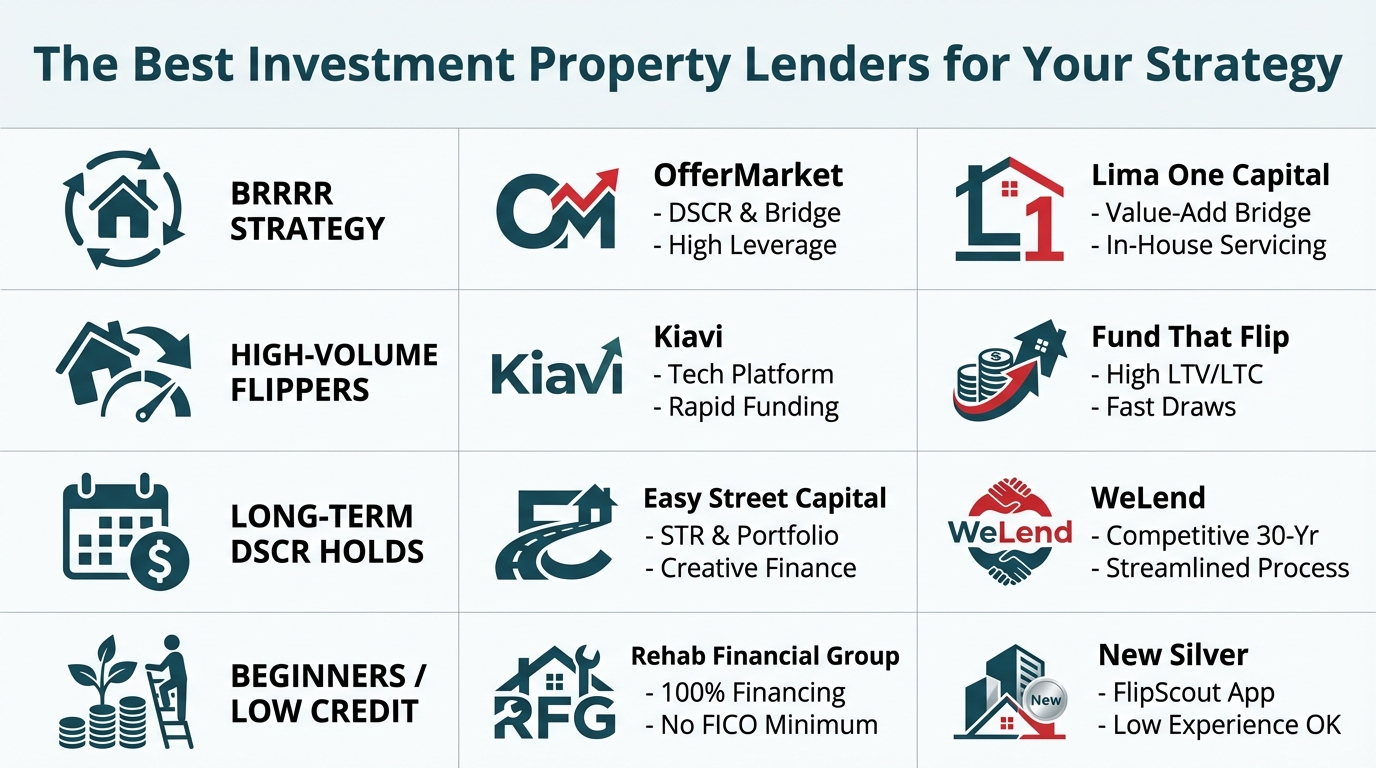

Why Investors Refinance with DSCR Loans

DSCR loans are built for investors who need long-term financing for income-generating properties. Common refinance scenarios include:

🛠️ Exiting a short-term rehab (fix and flip) or hard money loan

💸 Extracting equity via cash-out to fund your next deal

📉 Lowering interest rate and locking in fixed, long-term debt

🔁 Serving as the refinance leg of BRRRR (Buy, Rehab, Rent, Refinance, Repeat)

🏗️ Permanent financing for Build-to-Rent projects

These loans help keep your capital moving and minimize dependency on personal income documentation.

Can you refinance a DSCR loan

Yes! You can absolutely refinance a rental property DSCR loan, though you will want to make sure you will not be incurring an expensive prepayment penalty.

Prepayment Penalty for Refinance Rental Property DSCR Loan

Most DSCR loans carry a prepayment penalty. This means you pay a fee if you pay off the loan early. Most DSCR loan prepayment penalties are 3-2-1 or 5-4-3-2-1 "stepdown" penalties where you pay a declining percent of the outstanding principal loan balance as a penalty each of the 3 or 5 years of the penalty period.

For example, let’s say you’re in year 2 of a new loan with $100,000 remaining balance and a 3-2-1 prepayment penalty, and you decide to refinance your rental property DSCR loan to pull some cash out using a new DSCR loan. You will need to pay a 2% fee ($2,000) to your lender at settlement when you complete the refi.

Here's a helpful video that explains the prepayment penalty in more detail:

DSCR Cash Out Refinance: Everything You Need to Know

DSCR cash out refinance is the primary financing strategy used by BRRR method investors. Regardless of whether you buy your rental property with cash or a fix and flip loan, Once you complete your rehab and it’s time to pull cash out or refinance into a lower interest rate and a longer term, DSCR cash out refinance loans are the easiest way to complete your project so you can move on to the next project without wasting time and leaving cash trapped in the deal.

DSCR loan cash out refinance calculator

To calculate your loan amount and understand how the DSCR calculation will impact your refinance, we recommend using our DSCR Calculator.

Here are the inputs that affect your DSCR, and ultimately impact your loan amount:

💸 Rent

The lower the rent, the lower the DSCR at your target loan amount. With a DSCR cash out refinance, we use the lower of actual and market rent, so make sure you rent your property for market rent!

💸 Taxes

Taxes can really eat into your DSCR. BRRR strategy often protects against high taxes because the property was bought in distressed condition and the tax assessed value is still a lot lower than the value after repairs. Lower taxes, higher DSCR, higher LTV.

🔥 Insurance

The lower your insurance, the higher your net operating income, the higher your DSCR. Insurance for DSCR loans needs to follow specific guidelines including:

- Coverage type -- typically DP-3 "Special Form"

- Dwelling coverage -- typically replacement cost value ("RCV")

- General liability -- typically $500,000 per occurrence / $1,000,000 in the aggregate

- business interruption "loss of rent" -- typically 6 or 12 months of coverage so you get paid even if your property is damaged and your tenants need to move out and stop paying rent

We recommend shopping for the most cost effective landlord insurance from OfferMarket Insurance, our in-house insurance agency.

⚡ Utilities

If the owner pays utilities, it will reduce your net operating income, lowering your DSCR. For a DSCR cash out refinance, if tenants pay utilities, they will not be counted, so ideally, your lease will specify that your tenants pay all utilities (i.e. water, electric, gas).

📈 Interest Rate

Interest rate plays a major factor in calculating your DSCR. The higher the interest rate, the higher the mortgage payment, the lower the DSCR, and the lower the LTV you qualify for—especially when considering a DSCR cash out refinance (see chart above).

How long does a DSCR refi take?

A DSCR refi typically takes 30 to 45 days, though we can fund in as little as 15 to 20 days as long as you complete your processing items in your Loan File and we have an appraisal report and clear title.

Understanding DSCR Loan Costs and Terms

DSCR loans differ from conventional loans in several key ways:

Interest rates are typically higher

Down payment/equity required: usually 20–35%

Prepayment penalties are common (3-2-1 or 5-4-3-2-1 structures)

Terms: Most loans are 30-year fixed, no balloon

Rates and terms depend on your credit score, DSCR, loan amount, LTV, and the property's condition/location.

| OfferMarket | Other DSCR Lenders | |

|---|---|---|

| Origination points | 0.5 to 2 | 2 to 4 |

| Underwriting fee | $295 - $495 | $495 - $995 |

| Legal/doc prep fee | $695 to $995 | $995 |

| Appraisal fee | Market | Market |

| Appraisal review | $90 | $120 - $175 |

| Title | Market | Market |

DSCR Loan Cash Out Refinance: What You Should Know

Pulling cash out of your rental property with a DSCR loan cash out refinance can be one of the most practical ways to grow your rental portfolio because the loan term is typically 30 years at a fixed rate, which is often more attractive than personal or business loans or lines of credit.

Who Can Qualify?

To qualify for a DSCR refinance, you’ll typically need:

For Borrowers:

Credit score of 660+ (some lenders accept 620)

No W-2s, tax returns, or employment verification required

3 months of bank statements (usually)

Optional: prior experience with rental properties (preferred but not mandatory)

For Properties:

Must be non-owner-occupied

Types: Single-family homes, multi-units, condos, short-term rentals

Must generate enough rent to meet DSCR minimums

Appraisal required to verify market value and rental potential

DSCR Loan Refinance Guidelines

DSCR loan cash out refinance guidelines are standardized because most DSCR loans are sold to aggregators who pool these loans into mortgage-backed securitizations. As a result, guidelines are in place to ensure borrowers like you are not taking on too much risk.

Strategic Use of DSCR Loans in Real Estate Investing

DSCR loans are not just for refinancing — they’re part of a broader investing lifecycle. Investors use them to:

Refinance after rehabbing (as the "R" in BRRRR)

Replace expensive short-term financing (e.g., hard money)

Secure long-term financing in Build-to-Rent projects

Scale portfolios without the drag of personal income documentation

| Guidelines | Refinance |

|---|---|

| Minimum As Is Value | $100,000 |

| Minimum Loan Amount | $75,000 |

| Minimum DSCR | 1.1 |

| Maximum LTV | 75% (cash out), 80% (rate and term) |

| Rural | No |

| Bank Statements | 3 months |

| Minimum Credit Score | 660 |

| Tax Returns, W2 | No |

DSCR Refinance Seasoning Requirements

Seasoning refers to how long you must own a property before refinancing. Guidelines vary:

Rate and Term Refinance: Often no seasoning required (even immediately after rehab)

Cash-Out Refinance: Most lenders require 90 days of ownership

OfferMarket’s program has no seasoning requirement for cash-out refi if you can show value-add improvements, such as a light rehab or cosmetic updates.

It doesn't matter if you bought the property with cash or a short term loan, there is no seasoning requirement with our DSCR loan program.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull