*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Rental Loans - A Comprehensive Guide to Financing Your Real Estate Investments with Rental Loans

Looking to invest in real estate but don't have the funds to buy properties outright? Rental loans can be an excellent way to finance your real estate investment properties. In this comprehensive guide, we'll cover everything you need to know about rental loans, including how they work, the types of rental loans available, the pros and cons of using rental loans, how to qualify for a rental loan, and tips for finding the best rental loan for your investment needs.

We'll also explore important topics such as loan-to-value (LTV) ratios, interest rates, repayment terms, and fees associated with rental loans. Additionally, we'll provide practical advice on how to use rental loans to maximize your investment returns, including how to choose the right properties, how to negotiate with lenders, and how to manage your rental properties effectively.

Whether you're a seasoned real estate investor looking to expand your portfolio or a first-time investor just starting out, this guide will provide you with the knowledge and tools you need to succeed with rental loans. So why wait? Dive in and start learning about how rental loans can help you achieve your real estate investment goals today!

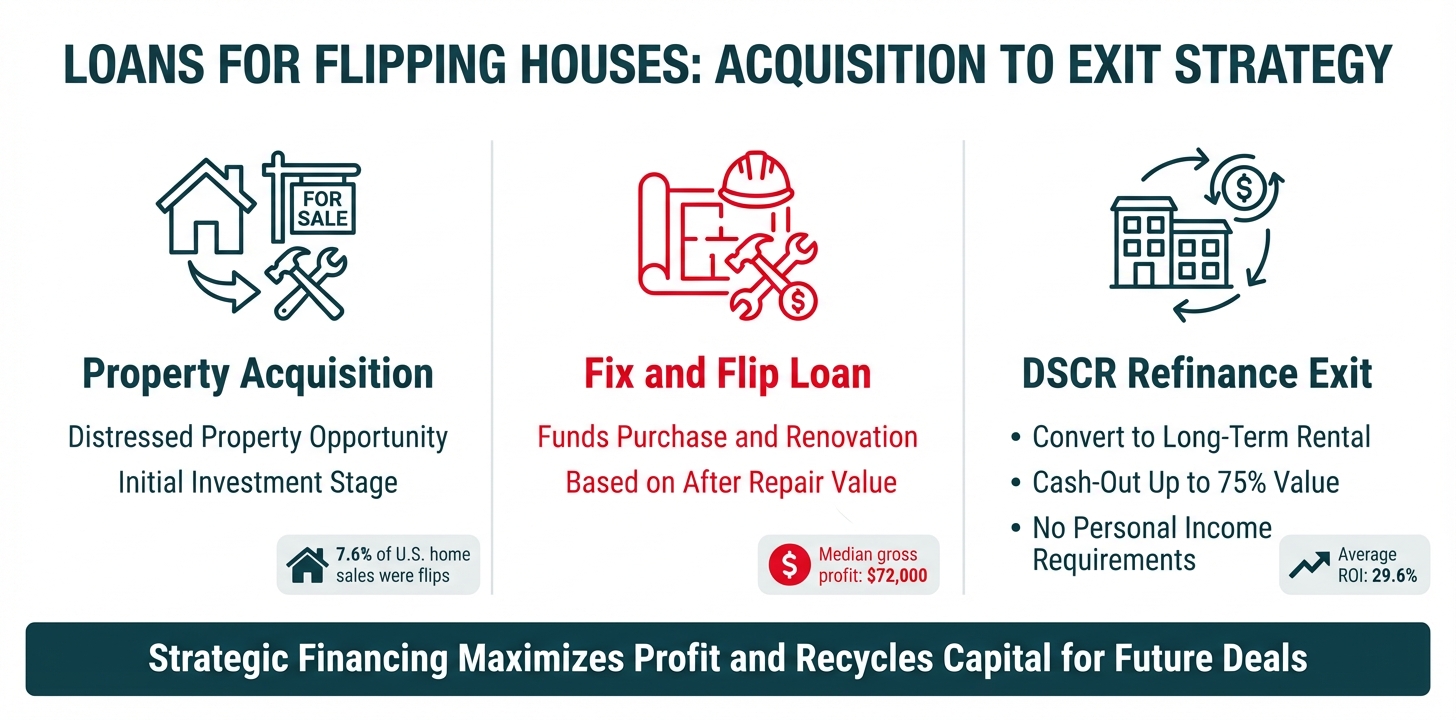

What is a rental loan?

A rental loan, also known as a real estate investment loan or a DSCR (debt service coverage ratio) rental loan, is a type of financing designed specifically for investment properties such as rental homes or multi-unit apartment buildings. Unlike traditional home loans, rental loans are not based on the borrower's personal income or credit score, but rather on the potential rental income of the property. This makes rental loans an attractive option for real estate investors looking to expand their rental property portfolios. With a rental loan, investors can access the funds needed to purchase and renovate properties, and then use the rental income generated by the property to pay back the loan.

How are rental loans different from normal mortgages?

Rental loans differ from traditional home mortgages in several ways. First, rental loans are based on the potential rental income of the property rather than the borrower's personal income or credit score. This means that the borrower's debt-to-income ratio is not a primary factor in determining loan approval. Second, rental loans often have higher interest rates and require larger down payments than traditional home mortgages due to the higher risk associated with investment properties. Additionally, rental loans typically have shorter repayment terms and require borrowers to meet certain occupancy and income requirements to qualify. Rental loans are a specialized financing option designed specifically for real estate investors looking to purchase and manage rental properties.

Why would someone use a rental loan?

A real estate investor may use a rental loan for several reasons. Firstly, rental loans can provide the necessary capital to purchase an investment property with the goal of generating rental income. Rental loans also offer investors the flexibility to finance multiple investment properties, enabling them to grow their portfolios over time. Additionally, rental loans can help investors leverage their existing assets to acquire new rental properties without having to tap into their personal savings. By using rental loans, investors can also benefit from potential tax deductions related to their rental properties, such as mortgage interest, property taxes, and depreciation.

What are the types of rental loans?

There are several types of rental loans available for real estate investors. These include traditional mortgages, portfolio loans, blanket loans, commercial loans hard money loans/ DSCR (Debt Service Coverage Ratio) loans.

Conventional rental loans are offered by traditional lenders and are typically backed by Fannie Mae or Freddie Mac. These loans are generally suited for investors who are looking to purchase a single rental property or a small number of rental properties. These loans typically require income verification and W-2 verification which limits their use to non-professional real estate investors that depend on another job for their main source of income.

Portfolio rental loans, on the other hand, are designed for investors who own a portfolio of rental properties. These loans provide investors with the ability to finance multiple properties under a single loan, simplifying the financing process and potentially lowering interest rates.

Blanket loans are another type of rental loan that allows investors to finance multiple properties under a single loan. Unlike portfolio loans, however, blanket loans do not require all properties to be similar in type or location.

Commercial rental loans are available to investors looking to purchase commercial properties, such as office buildings, retail spaces, or industrial properties. These loans often have higher interest rates and stricter qualification requirements due to the increased risk associated with commercial properties.

Finally, hard money/DSCR loans are based on the property's cash flow and do not require personal income verification.

In summary, traditional mortgages and commercial loans are typically offered by banks and credit unions, while portfolio loans and blanket loans are provided by private lenders. Hard money loans are often used for short-term financing and require higher interest rates and fees. The type of rental loan that an investor chooses will depend on their investment strategy, portfolio size, and the type of property they are looking to finance.

What are the risks of rental loans?

Like any type of loan, rental loans come with risks to the borrower. One of the primary risks is the possibility of defaulting on the loan, which could lead to foreclosure and the loss of the property. Additionally, there is the risk of the property not generating enough rental income to cover the loan payments, leaving the borrower responsible for making up the difference. Other risks include unexpected maintenance or repair costs, changes in the local rental market, and the potential for interest rate increases.

To mitigate these risks, lenders will typically require a down payment and will carefully evaluate the borrower's creditworthiness and ability to repay the loan. Lenders may also require the borrower to maintain certain levels of insurance, such as hazard insurance and flood insurance. To ensure that the property generates enough rental income to cover the loan payments, lenders may also require a debt service coverage ratio (DSCR) calculation to ensure that the property generates enough rental income to cover the loan payments. Lenders may also require regular inspections of the property to ensure that it is being maintained and is generating rental income as expected.

What can you do to mitigate risk of rental loans?

As a borrower, there are several steps you can take to mitigate the risks associated with rental loans. Firstly, it's important to have a thorough understanding of the rental market and ensure that you can generate enough rental income to cover the loan payments. Having a margin of safety, in terms of a rent cushion, can help mitigate risks by providing a buffer for unexpected vacancies, repairs, or rent decreases.

Secondly, it's important to have a solid plan for managing the property and a reliable team in place to help you. If your a remote landlord, having a property manager who can handle tenant screenings, repairs, and other day-to-day operations. A good property manager can help ensure that the property is well-maintained, tenants are paying on time, and potential issues are addressed promptly. If you are self-managing, then all the items mentioned above must be promptly and professionally handled by you.

Lastly, it's crucial to conduct due diligence before taking out a rental loan. This includes researching the lender's reputation, reading the loan documents carefully, and having a solid understanding of the terms and conditions of the loan. By being proactive and taking steps to mitigate risks, you can increase the chances of a successful rental property investment with utilization of a rental loan.

How do you find the best terms for a rental loan?

To find the best terms for a rental loan, it is recommended to research and compare multiple lenders. Start by identifying reputable lenders that specialize in rental property financing. Check online reviews, consult with local real estate agents, and ask for recommendations from other investors.

Once you have identified potential lenders, you should request loan quotes and compare the terms and fees. Look at the interest rate, loan amount, loan term, prepayment penalties, closing costs, and other fees. Be sure to read the fine print carefully and understand all terms and conditions.

When comparing loan quotes, it is important to consider the total cost of the loan, not just the interest rate. A loan with a lower interest rate may have higher closing costs, making it more expensive in the long run.

To obtain quotes, you can request them directly from lenders or work with a mortgage broker who can provide quotes from multiple lenders. It is recommended to obtain quotes from at least three different lenders to ensure that you are getting the best possible terms.

To get the best possible terms for a rental loan, it is important to have a good credit score, a solid financial history, and a strong rental property portfolio. Lenders are more likely to offer favorable terms to borrowers who present a lower risk.

What can you do to improve your terms for a rental loan?

To improve your chances of getting the best possible terms for a rental loan, you can take several steps.

First, work on improving your credit score by paying down debt, making timely payments, and avoiding opening new credit accounts. You can also request a free copy of your credit report from each of the three major credit reporting agencies and review it for errors or inaccuracies that may be negatively impacting your score. It vital to improve the credit score in the short term to 'put your best foot forward'. While yes, credit score isn't a perfect measure of your credit worthiness and is often wrong, your lenders will use it to evaluate your application because the capital providers for your lenders will have certain minimum requirements on the credit score scale for cutoffs on the rental loan products.

Second, lenders may also look at your background report to assess your overall financial stability and ability to repay the loan. This may include reviewing any criminal or financial issues. Most rental loans don't require income verification, but do require character verification. Lenders are trying to make sure you have paid off debts in the past and have no defaults of bankruptcies. Additionally, severity of criminal record does impact the risk of the loan, thus consider addressing any negative items on your report, such as expunging any criminal records if possible.

Third, having cash on hand in your bank account can demonstrate to lenders that you have the ability to cover unexpected expenses or vacancies in your rental property. This can make you a more attractive candidate for a loan and even better terms in many cases.

To compare terms and fees, it's recommended to shop around and request quotes from multiple lenders. This can help you get a better understanding of what terms and fees are typical for rental loans and allow you to choose the best option for your needs. Look for lenders who specialize in rental loans, as they may offer more favorable terms and understand the unique needs of rental property investors.

OfferMarket Loans

Check your rate

60 seconds · no credit pull