*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Bad Boy Carve Outs

What are Bad Boy Carve Outs?

Bad Boy Carve Outs are provisions in non-recourse DSCR loans that protect the lender in the event members of the borrowing entity conduct themselves in an illegal or fraudulent manner. Bad boy carveouts allow the lender to hold one or more individuals of the borrowing entity personally liable for repayment of the loan.

Examples that trigger Bad Boy Carveouts

Bad Boy Carve Outs can be triggered by several different violations of loan covenants, so it is important to read your loan docs carefully and consult your real estate attorney.

Examples include:

- taking on subordinate (i.e. 2nd position) financing without express written consent from the 1st position lender

- forged or fraudulent tax returns, bank statements, financial statements, operating documents (i.e. rent roll)

- illegal business conduct at the subject property

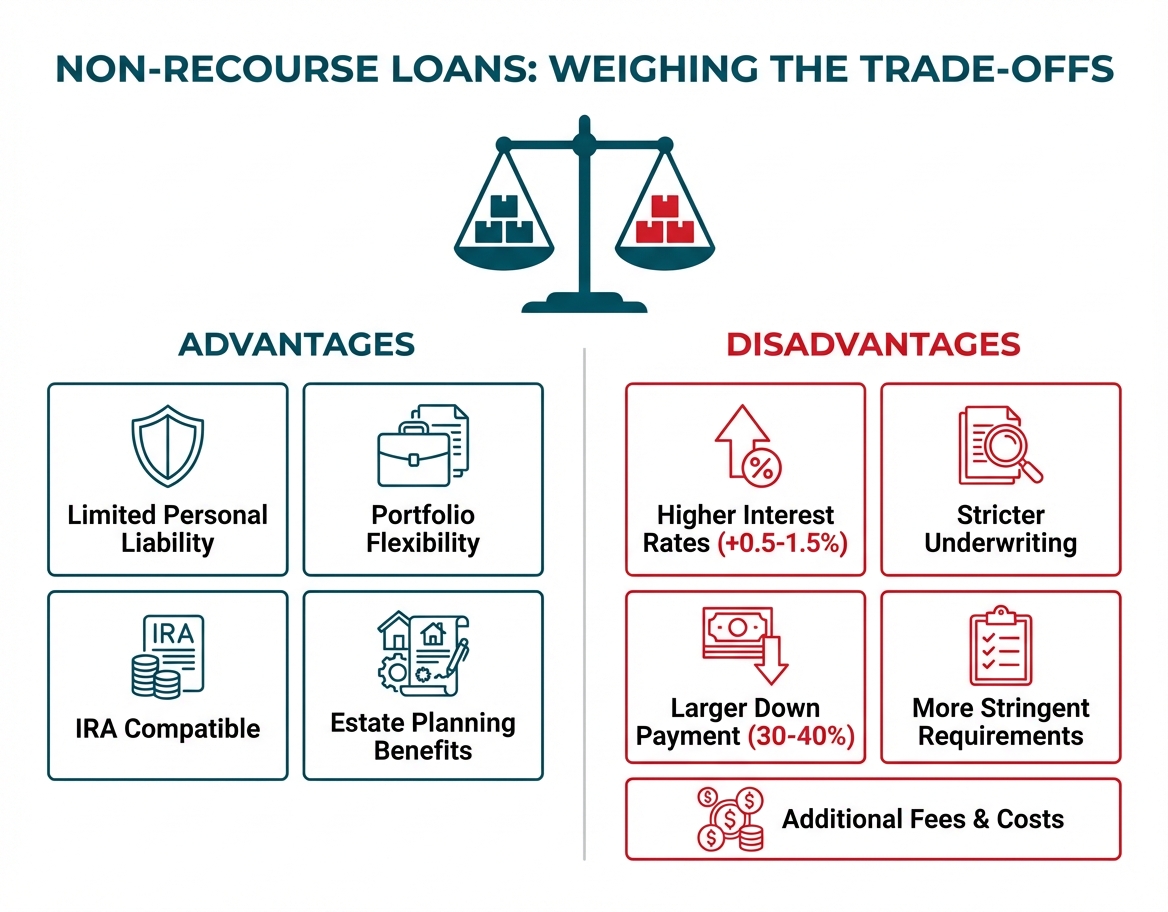

Non-Recourse DSCR Loans

Non-Recourse DSCR Loans are cash-flow based loans where personal guarantee is not required.

Bad Boy Guaranty

Bad Boy Guaranties or Bad Boy Guarantees are the same concept as Bad Boy Carveouts.

Are Bad Boy Carevouts Required?

Removing bad boy carveouts from your loan is unlikely and may depend on several factors:

- securitization program guidelines and requirements: if the lender will be selling the loan to an investor that will be securitizing the loan as part of a mortgage-backed security, then it is unlikely you would be able to remove the bad boy carve out.

- quality of collateral: if the collateral (subject property) is of high quality, the lender may be willing to accept the removal of a bad boy carveout, knowing that they will have an easier time recouping their loan through foreclosure or pledge of shares.

- pledge of equity: if the lender's pledge of shares agreement is signed by the borrower, the lender may be willing to remove a bad boy carve out.

- LTV capitalization: if the loan to value is conservative (i.e. 65% instead of 80%), then the lender may be willing to remove the bad boy provision from the loan agreement because the property is worth considerably more than the loan, and liquidation through foreclosure or pledge of shares should adequately allow the lender to recoup their loan principal and any fees.

OfferMarket Loans

Check your rate

60 seconds · no credit pull