*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

5 Types of Rental Property Loans & How to Get Approved (2026)

Securing the right rental property loan is crucial for scaling a real estate portfolio. The best financing option depends entirely on your investment strategy, the property's characteristics, and your financial position. For investors focused on long-term cash flow, the most common and effective loan types are the DSCR Loan, the Rental Property HELOAN, the Slow Flip Loan, the Fix and Flip Loan, and the Ground-Up Construction Loan. Each serves a distinct purpose, from acquiring a turnkey rental with no personal income verification to funding the purchase and renovation of a value-add property.

The Debt Service Coverage Ratio (DSCR) loan, for instance, is ideal for investors whose properties generate sufficient income to cover their debt obligations, regardless of the borrower's personal W-2 income. This asset-based approach allows for rapid portfolio expansion. In contrast, a Home Equity Loan (HELOAN) on an existing rental property allows you to tap into trapped equity to fund down payments or renovations for other projects. Understanding the nuances of each product is the first step toward aligning your financing with your investment goals.

The 5 Essential Rental Property Loans for Real Estate Investors

Choosing the correct loan is as important as choosing the right property. The financing structure impacts your cash flow, leverage, and ability to execute your business plan. Below is a high-level comparison of the five primary loan types available to real estate investors, each tailored to a specific strategy and investor profile.

Comparison of Rental Property Loan Types

| Feature | DSCR Loan | Rental HELOAN | Slow Flip Loan | Fix and Flip Loan | Ground-Up Construction |

|---|---|---|---|---|---|

| Ideal Investor | Portfolio Scaler | Equity Harvester | BRRRR Investor | Property Flipper | Builder/Developer |

| Qualification | Property Cash Flow | Property Equity / DSCR | High Credit / Liquidity | Property ARV | Borrower Experience |

| Typical Term | 30 Years | 10–30 Years | 5 Years | 12 Months | 12–18 Months |

| Speed to Fund | Moderate (10–19 days) | Moderate (10–21 days) | Fast (14–21 days) | Very Fast (10–21 days) | Slow (10–21 days) |

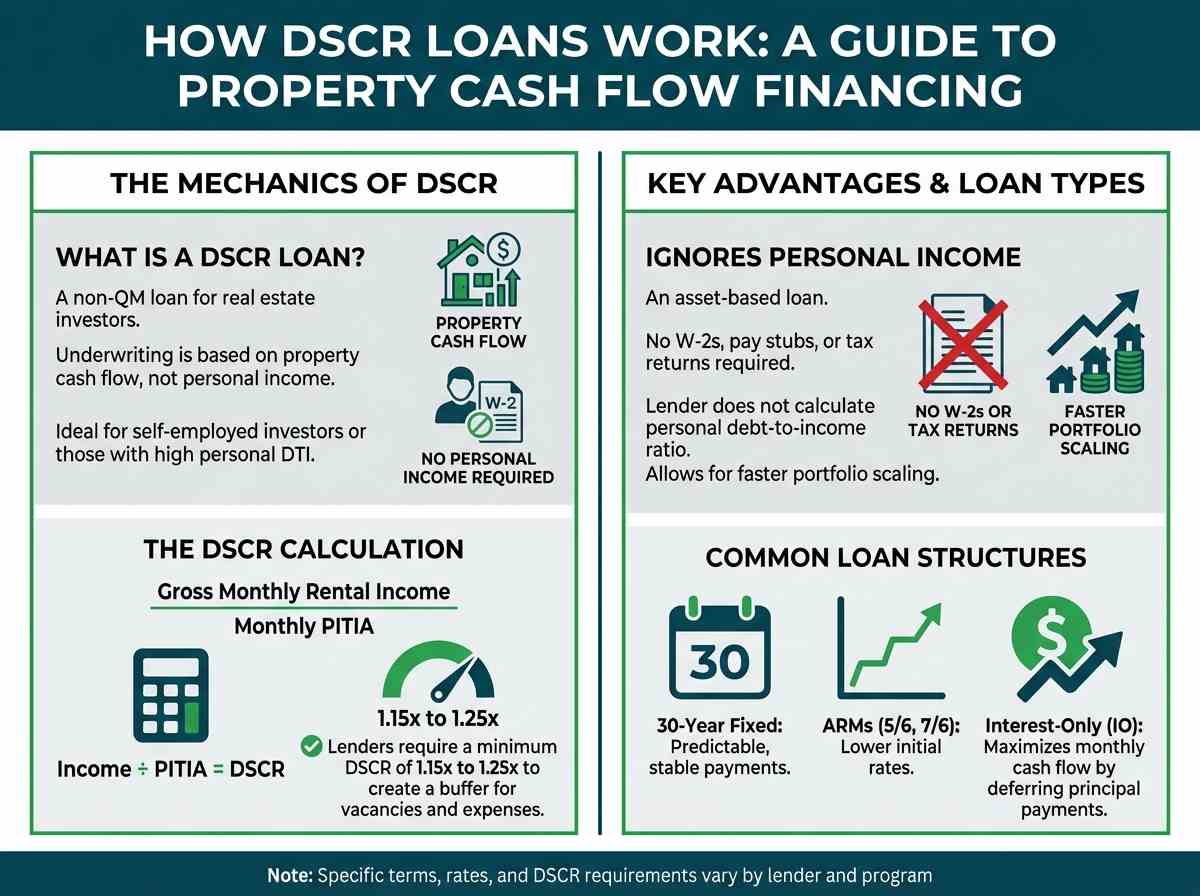

Type 1: The DSCR Loan - Scaling Your Portfolio with Property Cash Flow

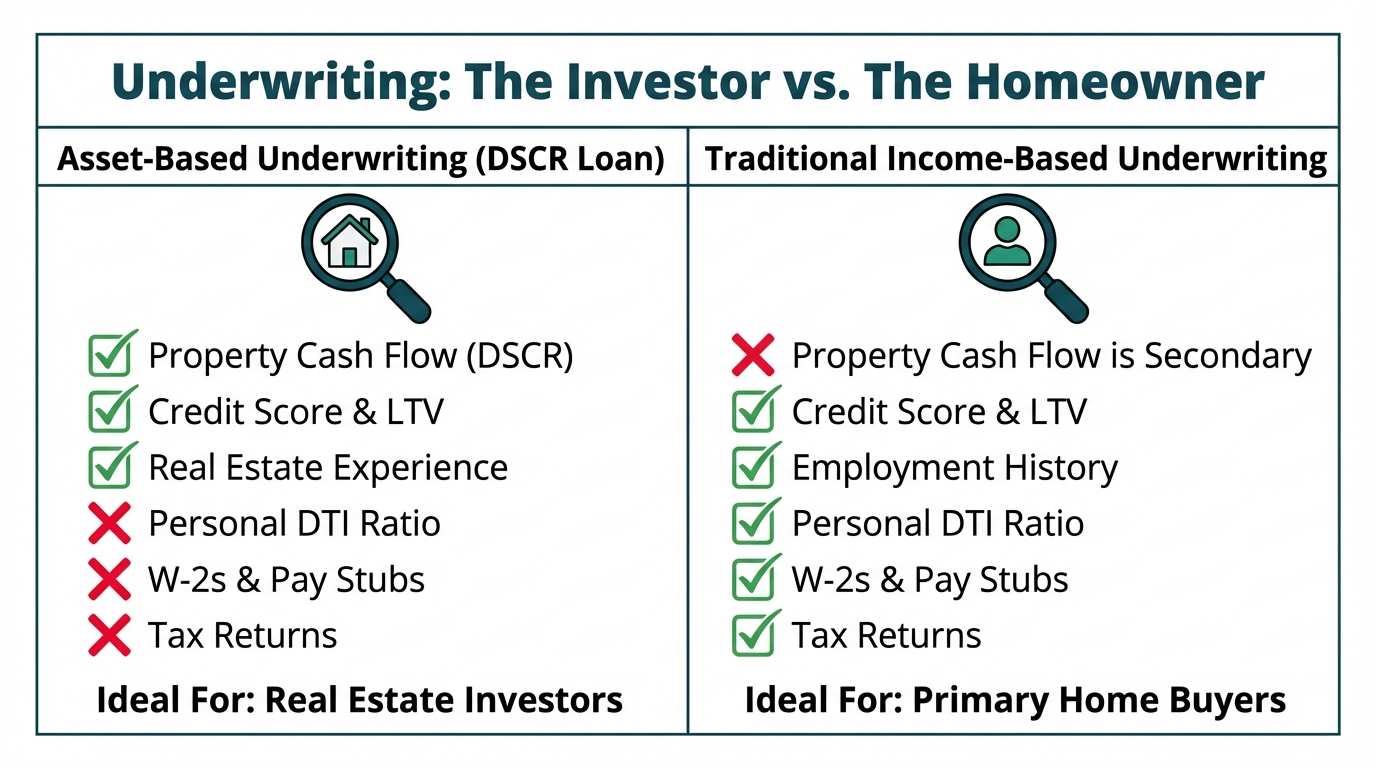

A DSCR loan is a type of non-qualified mortgage (Non-QM) designed specifically for real estate investors. Its primary underwriting criterion is the property's ability to generate enough income to cover its mortgage debt, rather than the borrower's personal income. This makes it a powerful tool for investors who are self-employed, have complex tax situations, or have a high personal debt-to-income (DTI) ratio from multiple mortgages.

How Lenders Calculate DSCR

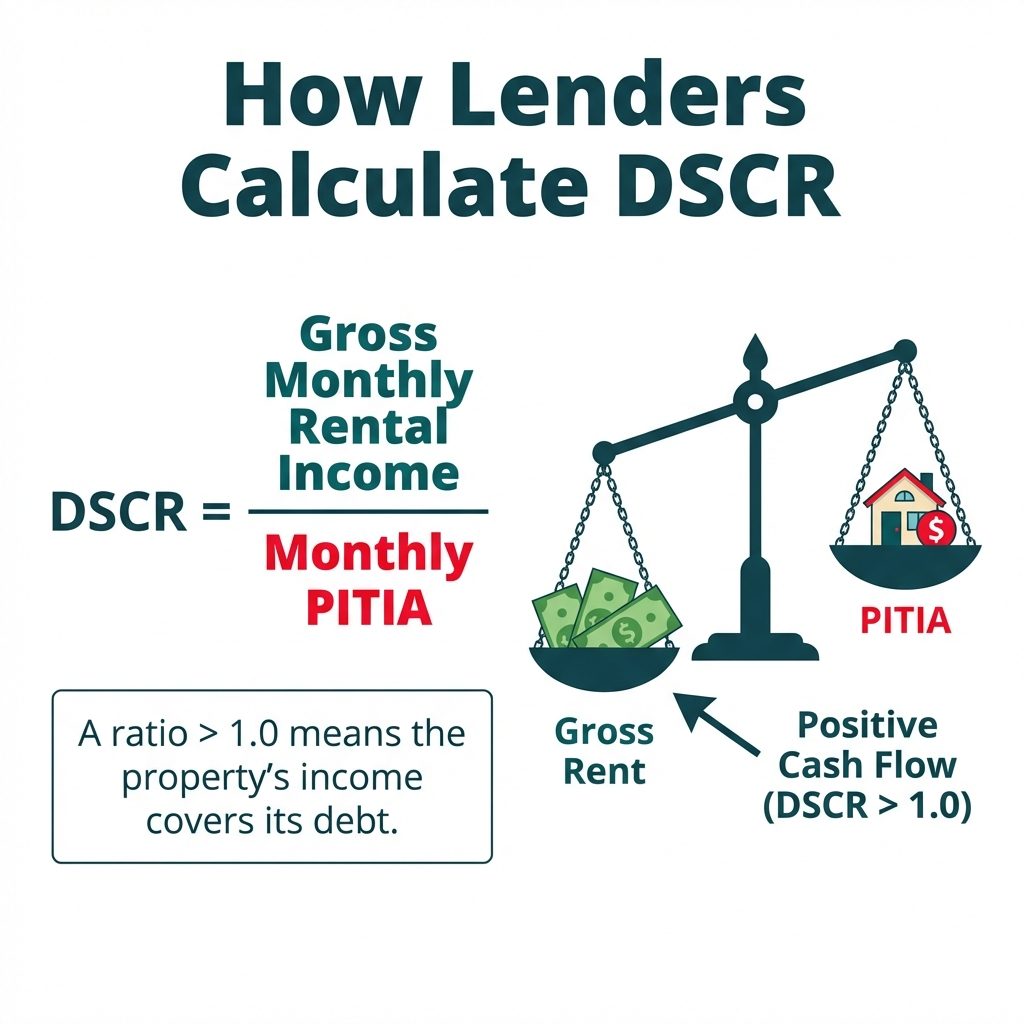

The core of the DSCR loan is the Debt Service Coverage Ratio itself. Lenders use a simple formula to determine if a property's cash flow is sufficient:

DSCR = Gross Monthly Rental Income / Monthly PITIA

- Gross Monthly Rental Income: This is the total potential rent from the property. For a new purchase, lenders typically use the lesser of the appraiser's market rent opinion (from a Form 1007) or the actual rent from the executed lease agreement.

- Monthly PITIA: This stands for Principal, Interest, Taxes, Insurance, and any Association (HOA) fees. It represents the total monthly housing expense for the property.

A DSCR of 1.0x means the property's income exactly covers its expenses. Most lenders require a minimum DSCR of 1.15x to 1.25x to provide a buffer for vacancies and maintenance. A higher DSCR often results in a better interest rate and more favorable loan terms. You can use a free DSCR calculator to quickly analyze a potential deal's viability.

Why DSCR Loans Ignore Personal Income

The revolutionary aspect of the DSCR loan is that it is asset-based. Because the loan is secured by the property and its ability to generate income, the lender is less concerned with your personal financial documents. This means:

- No W-2s or Pay Stubs: Your employment status is not a primary factor.

- No Tax Returns: Self-employed investors don't have to worry about business write-offs reducing their qualifying income.

- No Personal DTI Calculation: The lender does not analyze your existing personal debts (car loans, student loans, primary mortgage) against your personal income.

This approach allows investors to acquire properties based on the merit of the deal itself, enabling them to scale their portfolios much faster than they could with conventional loans, which are limited by Fannie Mae and Freddie Mac guidelines.

Common DSCR Loan Terms

DSCR loans are structured to be long-term financing solutions, mirroring the 30-year term of a traditional mortgage. Common options include:

30-Year Fixed Rate: The interest rate is locked for the entire 30-year term, providing predictable monthly payments. This is the most popular option for buy-and-hold investors.

Adjustable-Rate Mortgages (ARMs): These loans, such as a 5/6, 7/6, and 10/6 ARMs, offer a lower fixed rate for an initial period (5, 7, or 10 years) before adjusting annually. They can be a good option if you plan to sell or refinance before the adjustment period begins.

Interest-Only (IO) Options: An IO feature allows you to pay only the interest portion of the mortgage for a set period (typically the first 10 years). This significantly lowers the monthly payment, maximizing cash flow. The principal balance remains unchanged during the IO period.

OfferMarket's streamlined DSCR loan program is built for speed and efficiency, allowing investors to get an instant quote online, close quickly, and grow their rental portfolio without the paperwork burdens of conventional lending.

Perfect Use Case for a DSCR Loan

An experienced real estate investor owns eight rental properties, all financed with conventional loans. Her personal debt-to-income ratio is maxed out, and traditional banks will no longer lend to them, despite their excellent credit and significant cash reserves. She finds a new fourplex that generates strong rental income, easily covering its proposed mortgage, taxes, and insurance.

Using a DSCR loan, she can secure financing based solely on the fourplex's cash flow. The lender ignores her other mortgages and personal DTI, allowing her to add another high-performing asset to her portfolio and continue scaling her business.

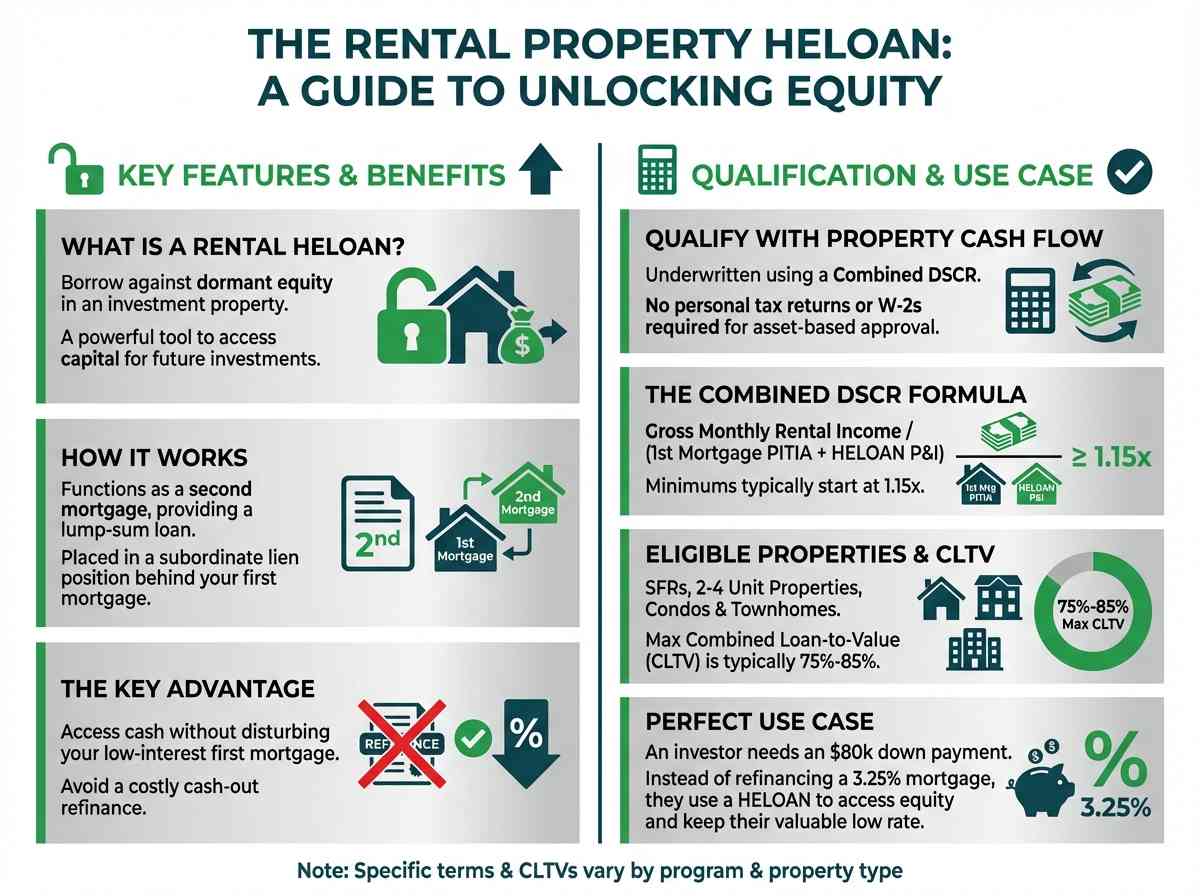

Type 2: The Rental Property HELOAN - Unlocking Your Portfolio's Equity

A Home Equity Loan (HELOAN) allows a property owner to borrow against the equity they have built in a property. While most people associate these with primary residences, savvy investors can use a HELOAN on an existing investment property to unlock capital for future investments. This is a powerful tool for accessing "dead equity"—value that is sitting dormant in a property—and putting it to work.

How a HELOAN Works for Investment Properties

A HELOAN on a rental property functions as a second mortgage. It is a lump-sum loan with a fixed interest rate and a fixed repayment term, placed in a subordinate lien position behind your existing first mortgage. This is a critical advantage: you can access cash without disturbing your current low-interest first mortgage through a cash-out refinance.

For example, if you have a rental property worth $500,000 with a first mortgage balance of $250,000, you have $250,000 in equity. A lender might allow you to borrow up to 80% of the property's value ($400,000). After accounting for your first mortgage, you could potentially access up to $150,000 in cash ($400,000 - $250,000) through a HELOAN.

Qualifying Based on Property DSCR

Similar to a primary DSCR loan, a HELOAN on a rental property from an investor-focused lender like OfferMarket is underwritten based on the property's cash flow. The lender will calculate a "blended" or "combined" DSCR that includes the proposed new HELOAN payment alongside your existing first mortgage payment.

Combined DSCR = Gross Monthly Rental Income / (Monthly First Mortgage PITIA + Monthly HELOAN P&I)

As long as the property's income can support both debt obligations and still meet the lender's minimum DSCR requirement (e.g., 1.15x), you can get approved without providing personal tax returns or W-2s. This asset-based qualification makes it a seamless way for active investors to leverage one asset to acquire another.

Eligible Property Types and CLTV Requirements

HELOANs are available for a wide range of residential investment properties, including:

- Single-Family Residences (SFRs)

- 2-4 Unit Multi-Family Properties

- Condos and Townhomes

The key metric for a HELOAN is the Combined Loan-to-Value (CLTV). This is the ratio of all loans on the property to the property's appraised value. Most lenders cap the CLTV for an investment property HELOAN between 75% and 85%. This is a more conservative threshold than for primary residences, reflecting the perceived higher risk of investment properties.

Perfect Use Case for a HELOAN

An investor purchased a rental property in 2019 with a 30-year fixed mortgage at a 3.25% interest rate. Today, the property has appreciated significantly, and she has over $200,000 in equity. She wants to buy another rental but needs $80,000 for the down payment and closing costs.

A cash-out refinance would force her to give up her historically low interest rate. Instead, she applies for a DSCR-based HELOAN on her existing rental. The property's rent easily covers both the original mortgage and the new HELOAN payment. She is approved for a $100,000 loan, gets the cash she needs for her next purchase, and keeps her valuable 3.25% first mortgage intact.

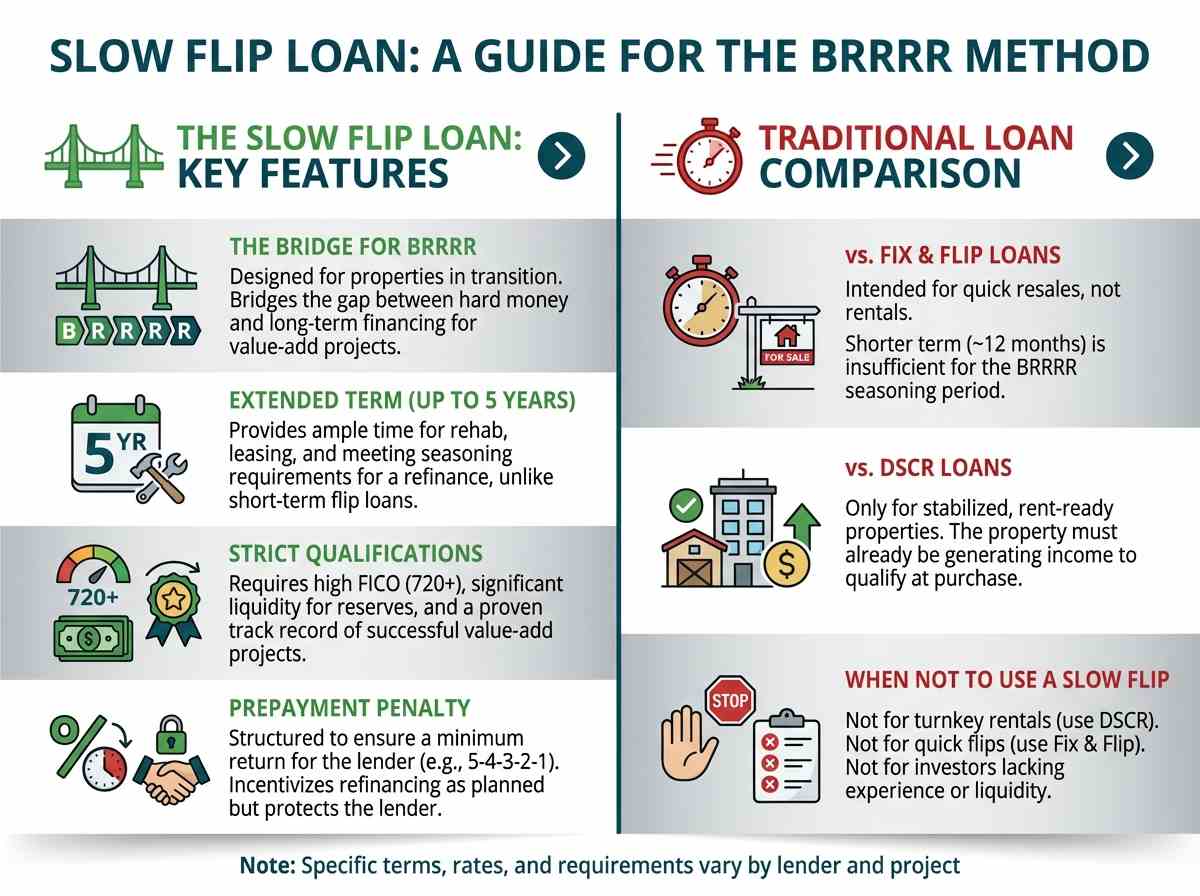

Type 3: The Slow Flip Loan - A Bridge for the BRRRR Method

The Slow Flip loan is a specialized, short-to-medium-term financing product designed for investors who need more time than a traditional 12-month fix and flip loan allows. It serves a unique niche, particularly for those executing the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, where a property needs to be acquired, renovated, and then "seasoned" with a tenant before it can be refinanced into long-term debt.

How It Differs from Other Loans

The Slow Flip loan bridges the gap between hard money and permanent financing:

vs. Fix and Flip Loan: A standard fix and flip loan has a term of around 12 months and is intended for properties that will be sold quickly. A Slow Flip loan offers a longer term, typically up to 5 years, accommodating the time needed to complete renovations, lease the property, and meet the seasoning requirements for a refinance.

vs. Long-Term Loan: A DSCR loan is for stabilized, rent-ready properties. A Slow Flip loan is designed for properties that are currently in a state of transition and not yet generating income, meaning they wouldn't qualify for a DSCR loan at purchase.

Strict Qualification Criteria

Because these loans are for non-stabilized assets, lenders impose stricter qualification requirements. Approval for a Slow Flip loan typically hinges on:

- High FICO Score: Borrowers often need a credit score of 720 or higher.

- Significant Liquidity: Lenders want to see that you have ample cash reserves to cover closing costs, interest payments during the renovation, and unforeseen project expenses.

- Proven Experience: A track record of successfully completing similar value-add projects is often required. Lenders want to see you have a history of managing renovations and turning non-performing assets into cash-flowing rentals.

Understanding the 5-Year Term and Prepayment Penalties

The typical 5-year term provides a generous runway to complete the BRRRR process. However, it's important to understand the prepayment penalty structure. These loans often have a penalty (e.g., 5-4-3-2-1, where the penalty is 5% of the loan balance in year one, 4% in year two, etc.) to ensure the lender earns a minimum amount of interest. This structure incentivizes you to refinance as planned but protects the lender if you sell the property very quickly.

Using a Slow Flip for the BRRRR Strategy

The Slow Flip loan is the perfect tool for the first two stages of BRRRR:

Buy: It provides the fast, asset-based financing needed to acquire a distressed property that wouldn't qualify for a conventional loan.

Rehab: The loan can be structured to include funds for the renovation, which are disbursed in draws as work is completed.

Once the rehab is finished and a tenant is in place (the "Rent" stage), the property is now a stabilized asset. The investor can then proceed to the "Refinance" stage, paying off the Slow Flip loan with a long-term DSCR loan, often pulling cash out in the process.

Perfect Use Case for a Slow Flip Loan

An investor identifies a single-family home that needs significant cosmetic updates but is in a high-demand rental area. Her plan is to execute the BRRRR method. The property is not currently habitable and thus won't qualify for a DSCR loan. A 12-month fix and flip loan is too short, as it could take 4 months to renovate and another 3-6 months to meet the lender's seasoning requirement for a cash-out refinance.

She secures a 5-year Slow Flip loan that covers 85% of the purchase price and 100% of her renovation budget. This gives her ample time to complete the work, place a high-quality tenant, and then refinance into a 30-year DSCR loan after 9 months, pulling out her initial capital to "Repeat" the process on another property.

Type 4: The Fix and Flip Loan - Short-Term Capital for Quick Profits

A fix and flip loan, often referred to as a hard money or bridge loan, is a short-term financing instrument purpose-built for investors who intend to buy, renovate, and sell a property for a profit, typically within 12 months. Speed and leverage are the defining features of this loan type, allowing flippers to act quickly and preserve their own capital for other aspects of the project.

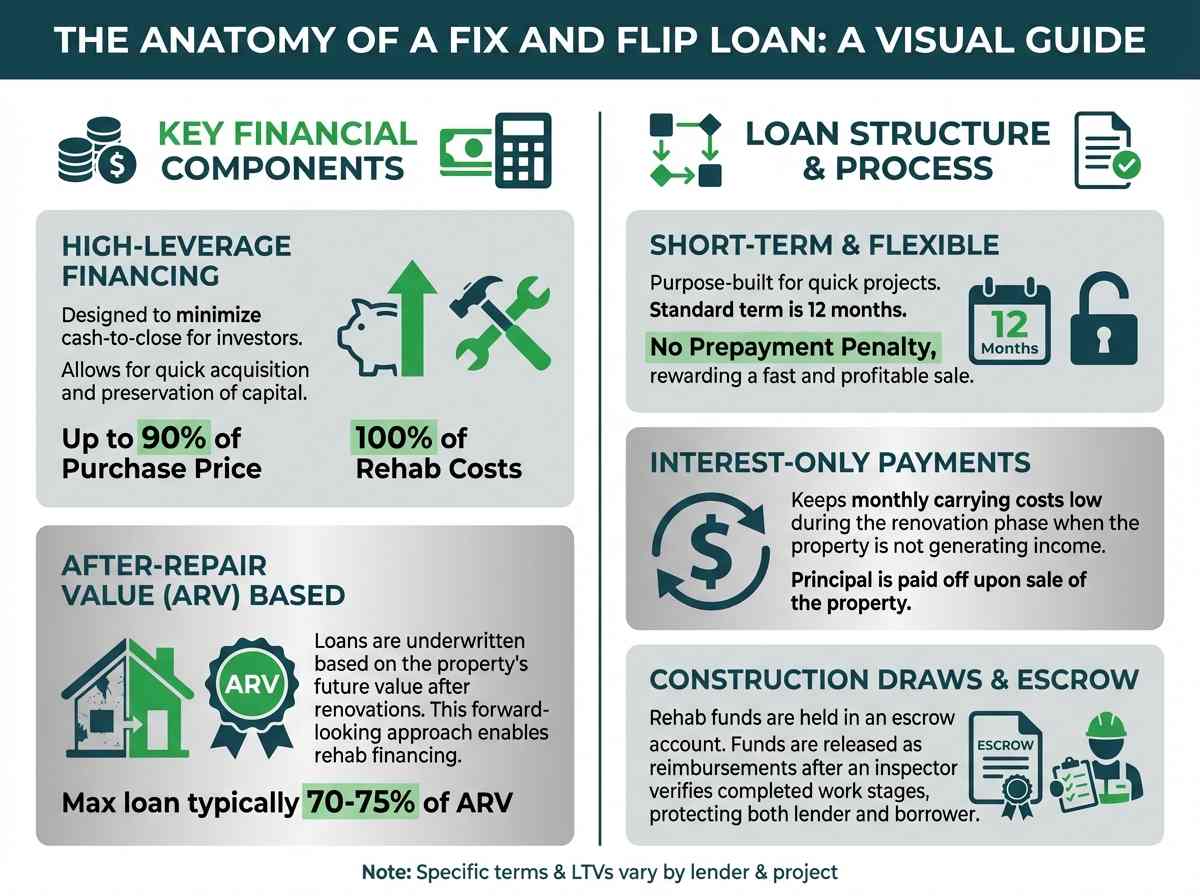

High-Leverage Financing

The most attractive feature of a fix and flip loan is the high leverage it offers. Lenders understand that the goal is to minimize the investor's cash-to-close. A typical structure includes:

- Up to 90% of the Purchase Price: The lender finances the vast majority of the acquisition cost.

- 100% of the Rehab Costs: The entire renovation budget is financed by the lender and held in an escrow account.

This structure allows an investor to acquire a property with a minimal down payment, sometimes as low as 10% of the purchase price, while having the renovation fully funded.

The Role of After-Repair Value (ARV)

Unlike conventional loans that are based on the current value of a property, fix and flip loans are underwritten based on the After-Repair Value (ARV). The ARV is a professional appraiser's opinion of what the property will be worth after all the planned renovations are completed.

This forward-looking valuation is critical. The loan amount is ultimately constrained by a percentage of the ARV, typically 70-75%. For example, if a property has a purchase price of $200,000, a rehab budget of $50,000, and an ARV of $350,000, the lender's maximum loan amount would be 75% of the ARV, or $262,500. Since the total project cost is $250,000, the deal fits comfortably within the lender's guidelines. This ARV-based approach is what enables lenders to finance 100% of the rehab.

Loan Structure and Terms

Fix and flip loans are designed for short-term holds and have distinct features:

- Term: Usually 12 months, with some options for a short extension.

- Interest: Payments are typically interest-only, which keeps the monthly carrying costs low during the renovation phase when there is no income.

- Prepayment Penalty: These loans almost never have a prepayment penalty, as the business model is to sell the property and pay off the loan as quickly as possible.

Construction Draws and Escrow

The 100% rehab financing is not given to the borrower as a lump sum at closing. Instead, it is held in an escrow account managed by the lender. The borrower funds the initial phase of construction out-of-pocket, then submits a draw request to the lender. The lender sends an inspector to the property to verify that the work has been completed according to the pre-approved Scope of Work. Once verified, the lender reimburses the borrower from the escrow account. This process repeats until the renovation is complete, protecting both the lender and the borrower by ensuring loan funds are used as intended.

Perfect Use Case for a Fix and Flip Loan

An experienced flipper finds an off-market property that needs a full gut renovation. It's a great deal, but the wholesaler requires a closing in 10 days. A conventional loan is impossible on this timeline, and the property's current condition makes it unfinanceable by traditional banks anyway.

The investor applies for a fix and flip loan and gets approved in 19 days. The loan covers 90% of the purchase price and 100% of the six-figure renovation budget. This speed allows him to secure the deal, and the high leverage lets him keep his cash free for another project he's running concurrently. He plans to complete the rehab in 5 months, sell in month 7, and pay off the loan with no penalty, maximizing his profit.

Type 5: The Ground-Up Construction Loan - Building New Inventory

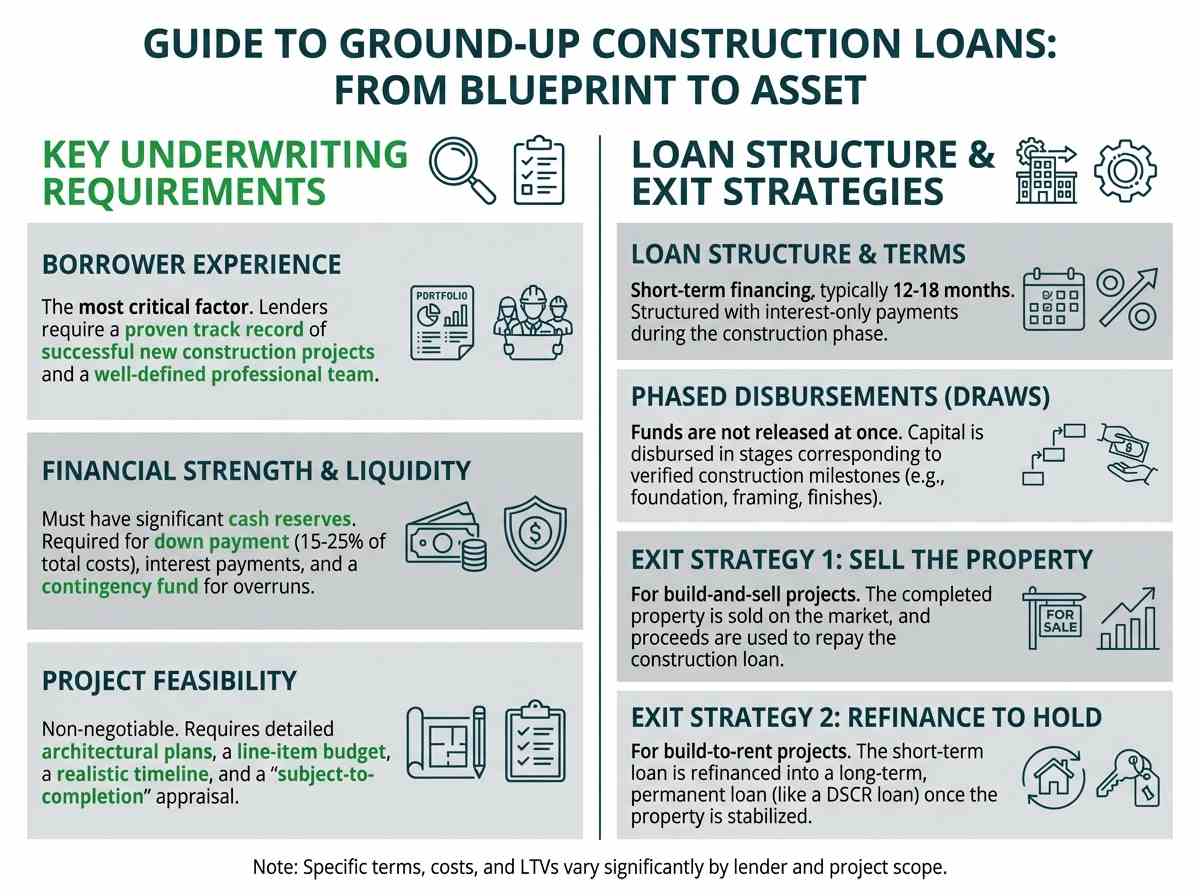

A ground-up construction loan is a specialized form of short-term financing for building a new property on vacant land or after tearing down an existing structure. This type of loan is distinct from other real estate financing because there is no existing asset to secure the loan against initially. Instead, the loan is underwritten based on the future value of the completed project, the feasibility of the construction plan, and, most importantly, the experience of the borrower.

The Importance of a Proven Track Record

For lenders, a ground-up construction loan carries significant risk. They are not just betting on a property, but on the developer's ability to manage a complex project on time and on budget. Consequently, underwriting focuses heavily on the borrower's experience. A strong application will demonstrate:

- A portfolio of successfully completed new construction projects.

- A well-defined team, including a reputable general contractor, architect, and engineer.

- Deep knowledge of the local market, including zoning laws and permit processes.

First-time builders may find it difficult to secure this type of financing without partnering with a more experienced developer.

Liquidity and Project Feasibility

In addition to experience, lenders will scrutinize the borrower's financial strength and the viability of the project itself. Key requirements include:

Liquidity: The borrower must have significant cash reserves to cover the down payment (typically 15-25% of total project costs), interest payments during construction, and a contingency fund for unexpected overruns.

Detailed Plans: A complete set of architectural plans, a line-item construction budget, and a realistic project timeline are non-negotiable.

Appraisal: An appraiser will provide a "subject-to-completion" valuation, which is the estimated market value of the property once it is built according to the plans. The loan amount will be based on a percentage of this future value.

Loan Structure and Phased Disbursements

Ground-up construction loans are structured similarly to fix and flip loans but on a larger scale. They are short-term (12-18 months) and interest-only. The loan funds are not disbursed all at once. Instead, they are released in stages (draws) that correspond to specific construction milestones.

For example, draws might be scheduled for:

- Land acquisition and site prep

- Foundation completion

- Framing and roofing

- Installation of mechanical systems (HVAC, plumbing, electrical)

- Drywall and interior finishes

- Final inspection and Certificate of Occupancy

This phased approach protects the lender by ensuring their capital is being used to create the asset that secures their loan.

The Path to Permanent Financing

Once construction is complete and the local municipality issues a Certificate of Occupancy, the short-term construction loan needs to be paid off. The investor's exit strategy is typically one of two paths:

Sell the Property: If the goal was to build and sell, the proceeds from the sale are used to repay the construction loan.

Refinance into a Permanent Loan: If the goal was to build and hold as a rental (a strategy sometimes called "Build-to-Rent"), the investor will refinance into a long-term DSCR loan. The property is now a stabilized, income-producing asset and can qualify for 30-year financing.

Perfect Use Case for a Ground-Up Construction Loan

A small-scale developer with a track record of building and selling three single-family homes identifies an infill lot in a desirable neighborhood with a shortage of rental inventory. Their strategy is to build a high-end duplex to hold as a long-term rental.

They presents the project to a lender with a strong portfolio, detailed architectural plans, a signed contract with a trusted general contractor, and a solid financial statement. They secures a 15-month ground-up construction loan that covers 80% of the land purchase and 100% of the construction costs. Upon completion and leasing both units, They will refinance the construction loan into a 30-year fixed-rate DSCR loan, creating a brand-new, cash-flowing asset for her portfolio.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Understanding Your Financing Options

The lending landscape for real estate investors is fundamentally different from the world of owner-occupied home loans. While a first-time homebuyer's primary goal is to secure a place to live, an investor's goal is to acquire a cash-flowing asset. This distinction is at the heart of why different financing tools are necessary.

Why Traditional Mortgages Fall Short for Investors

Conventional mortgages, backed by government-sponsored enterprises like Fannie Mae and Freddie Mac, are designed for W-2 employees with straightforward financial profiles. They come with significant limitations for serious investors:

Strict DTI Ratios: Conventional lenders adhere to strict debt-to-income ratios, making it difficult to qualify for new loans once you have a few mortgages on your credit report.

Extensive Paperwork: The application process requires tax returns, pay stubs, and letters of explanation for any credit anomalies, which can be burdensome for self-employed individuals or those with complex income streams.

Loan Limits: Fannie and Freddie impose a limit on the number of financed properties an individual can have (typically 10).

Slow Process: The underwriting process for a conventional loan can take 30-60 days, which is often too slow to compete for in-demand investment properties.

Matching the Right Loan to Your Investment Strategy

The most successful investors are masters of capital allocation, and that begins with choosing the right loan. Your strategy should dictate your financing, not the other way around.

Buy and Hold: If your goal is long-term cash flow from a stabilized property, a 30-year fixed-rate DSCR loan provides stability and predictability.

BRRRR: This strategy requires a two-step financing process: a short-term acquisition and rehab loan (like a Slow Flip loan) followed by a long-term refinance (a DSCR loan).

Flipping: For quick turnarounds, a 12-month, high-leverage fix and flip loan is the only tool that makes sense. It provides the speed and capital needed to execute the plan.

New Construction: Building a new rental requires a specialized ground-up construction loan to manage the build phase, followed by a permanent DSCR loan upon completion.

The Shift from Personal Income to Asset-Based Underwriting

The rise of Non-QM products like the DSCR loan represents a critical shift in the lending industry. Lenders now recognize that for an investment property, the asset's performance is a better indicator of risk than the borrower's personal W-2 income. This asset-based underwriting model empowers investors by allowing them to qualify for loans based on the quality of their deals. It removes the artificial ceiling imposed by personal DTI ratios and enables investors to scale their portfolios based on their ability to find profitable opportunities.

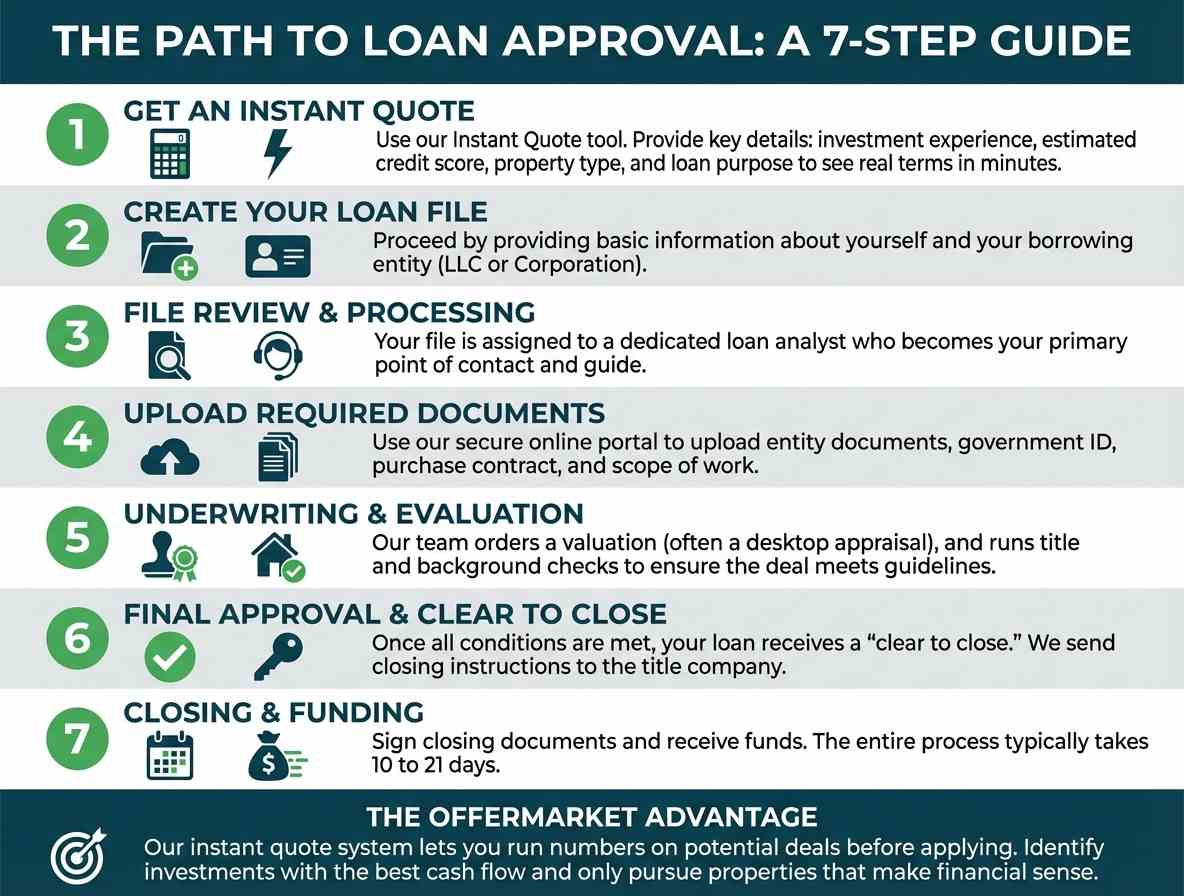

Your Step-by-Step Path to Loan Approval

Securing a rental property loan from an investor-focused lender like OfferMarket is a streamlined and transparent process. It's designed for efficiency, removing the roadblocks common in traditional lending. Here is the typical path from application to funding.

Step 1: Get an Instant Quote

At OfferMarket, we've streamlined this with our Instant Quote tool. Instead of filling out pages of paperwork and waiting days for a response, you can get real, transparent terms in minutes. You'll need to provide:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

OfferMarket Advantage: Our instant quote system lets you run the numbers on potential deals before you even submit a formal application. You can run multiple property scenarios through our calculator to identify which investments offer the best cash flow potential, ensuring you only submit applications for properties that make financial sense.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

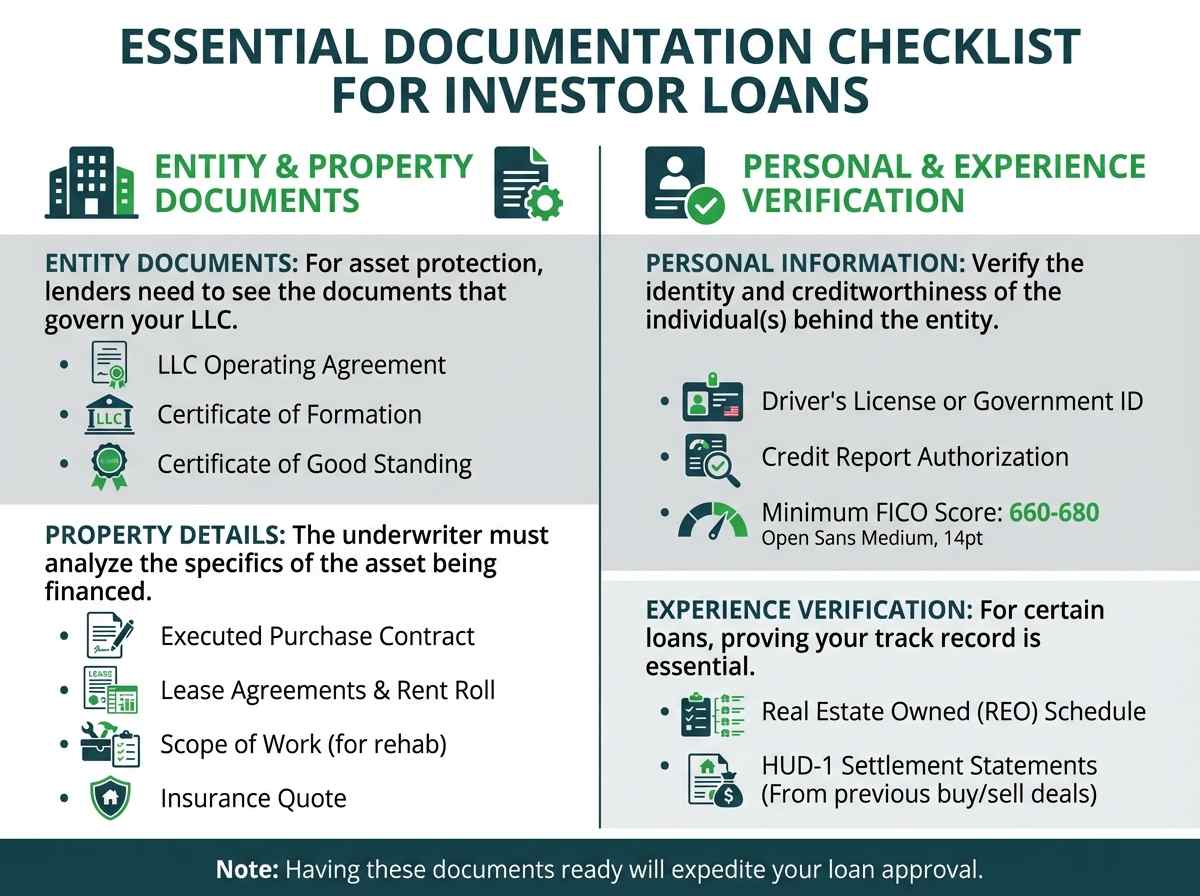

Essential Documentation Checklist for Underwriters

While investor loans require significantly less paperwork than conventional mortgages, you still need to provide specific documents to verify the borrower, the entity, and the property. Having these ready will expedite your loan approval.

Entity Documents

Most investors hold property in a Limited Liability Company (LLC) for asset protection. Lenders will need to see the documents that govern this entity.

- LLC Operating Agreement: This document outlines the ownership structure and management of the LLC.

- Certificate of Formation/Articles of Organization: The state-filed document that officially created the LLC.

- Certificate of Good Standing: A document from the Secretary of State confirming the entity is active and compliant.

Property Details

The underwriter needs to analyze the specifics of the asset they are lending on.

- Executed Purchase Contract: The fully signed agreement between you and the seller.

- Lease Agreements: If the property is currently occupied, provide copies of all leases.

- Rent Roll: A summary document showing all units, tenant names, lease terms, and monthly rents.

- Scope of Work (for rehab loans): A detailed, line-item budget of all planned renovations.

- Insurance Quote: A binder for a hazard insurance policy on the property.

Personal Information

Even on an asset-based loan, the lender needs to verify the identity and creditworthiness of the individual(s) behind the LLC.

- Driver's License or Government-Issued ID: For all members of the LLC.

- Credit Report Authorization: A form allowing the lender to pull your credit report. A minimum FICO score (often 660-680) is typically required.

Experience Verification

For certain loan types like fix and flip or ground-up construction, verifying your track record is essential.

- Real Estate Owned (REO) Schedule: A list of all properties you currently own.

- HUD-1 Settlement Statements: Closing statements from properties you have previously bought and sold can be used to prove flipping experience.

Take the Next Step: Secure Your Funding with OfferMarket

For serious real estate investors, the limitations of conventional financing are a major obstacle to growth. The paperwork, the slow timelines, and the focus on personal income create a bottleneck that prevents you from capitalizing on opportunities.

OfferMarket was built by investors, for investors. We understand that your time is valuable and that the quality of the deal should be the primary factor in a lending decision. Our technology-driven platform and focus on asset-based underwriting are designed to help you scale your portfolio efficiently.

Our flagship DSCR loan is the engine for portfolio growth, allowing you to secure 30-year fixed-rate financing based on your property's cash flow, not your personal tax returns. Before you make your next offer, use our free DSCR Loan Calculator to analyze the deal's profitability and see how it would perform as a rental.

When you're ready to move forward, you can get an instant, no-obligation quote online in just a few minutes. See your potential rate and terms today and discover a better way to finance your rental properties.

Run Your Numbers in 60 Seconds

Get a transparent breakdown of rates, terms, and max LTV for your next deal. No hard credit pull, no commitment.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull