*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Hard Money Fix & Flip Loans: The Complete 2026 Guide

Hard money fix and flip loans are short-term, asset-based financing solutions designed specifically for real estate investors who purchase properties to renovate and sell for a profit. Unlike traditional mortgages that focus heavily on a borrower's personal income and credit history, hard money loans are underwritten primarily based on the value of the real estate asset itself, specifically its After-Repair Value (ARV). This makes them an ideal tool for acquiring properties that wouldn't qualify for conventional financing, such as distressed or outdated homes.

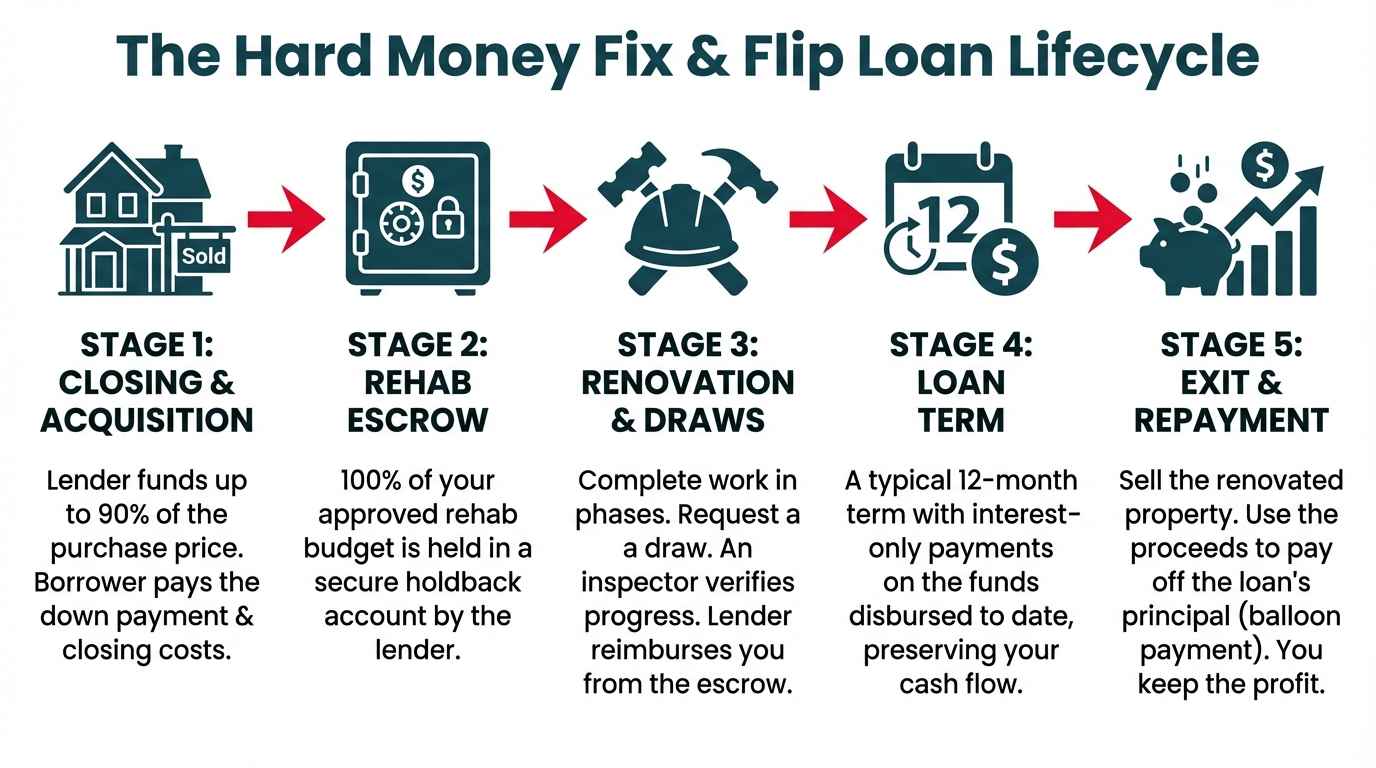

The core of a hard money fix and flip loan is its two-part funding structure, which covers both the purchase of the property and the cost of its renovation. The acquisition portion is funded at closing, while the renovation funds are placed into a construction holdback account (also known as a rehab escrow). These rehab funds are not given to the borrower upfront but are disbursed in stages, or "draws," as construction milestones are completed and verified by an inspector. Throughout the loan's typical 12-month term, the borrower makes interest-only payments, which keeps monthly costs low and preserves capital for the project. The full principal balance is then repaid in a single "balloon" payment at the end of the term, usually from the proceeds of selling the renovated property.

The Two-Part Funding Structure: Acquisition and Renovation

The genius of a fix and flip loan lies in its ability to finance nearly the entire project cost, not just the initial purchase. When you close on a property with a hard money loan, the funding is divided into two main components:

Acquisition Funds: This is the portion of the loan used to buy the property. Lenders will typically finance a percentage of the purchase price, often up to 90%. This amount is wired to the title company at closing, just like in a traditional real estate transaction.

Renovation Funds: This is the portion of the loan that covers your entire construction budget. These funds are not given to you at closing. Instead, they are set aside in a dedicated, non-interest-bearing account managed by the lender, known as a construction holdback or rehab escrow.

For example, if you buy a property for $200,000 with a $50,000 renovation budget, your total project cost is $250,000. A lender offering 90% Loan-to-Cost (LTC) might approve a total loan of $225,000. At closing, $180,000 (90% of the purchase price) would be used to buy the house. The remaining $45,000 of the loan, intended for the rehab, would be placed into the holdback account.

The Construction Holdback Account Explained

The construction holdback is a critical risk management tool for the lender. It ensures that the loan funds specifically allocated for renovation are used exactly for that purpose. By holding the funds in escrow, the lender guarantees that the property will be improved as planned, which is essential for it to reach its projected After-Repair Value (ARV). The ARV is the foundation of the lender's investment, so they have a vested interest in seeing the renovation completed successfully.

For the borrower, the holdback account provides a structured and disciplined approach to managing the construction budget. It prevents the commingling of funds and ensures that capital is available for each phase of the project. You can't use the rehab money to cover closing costs or other personal expenses; it is strictly tied to the approved Scope of Work (SOW).

The Draw Process: Funding Your Rehab in Stages

Once the loan is closed and the rehab funds are in the holdback account, you can begin construction. You will typically pay your contractors out-of-pocket for the first phase of work. When that phase is complete, you submit a "draw request" to the lender.

Here’s a step-by-step breakdown of the draw process:

Complete a Phase of Work: Following your SOW, you complete a defined portion of the renovation, such as demolition and framing, or installing plumbing and electrical systems.

Submit a Draw Request: You formally request reimbursement from the lender for the work completed. This request usually includes lien waivers from your contractors and any relevant receipts.

Schedule an Inspection: The lender sends a third-party inspector to the property. The inspector’s job is to verify that the work claimed in the draw request has been completed to a satisfactory standard and aligns with the SOW.

Lender Approval: Once the inspector submits a positive report, the lender approves the draw.

Funds are Released: The lender wires the funds from the holdback account directly to your bank account, reimbursing you for the expenses.

This cycle repeats for each phase of the project until the renovation is complete and the holdback account is empty. Most lenders charge a small fee for each draw inspection, typically ranging from $150 to $250.

Interest-Only Payments During the Loan Term

To maximize cash flow for the investor during the project, hard money fix and flip loans are structured with interest-only payments. This means your monthly payment only covers the interest that has accrued on the disbursed loan balance; you are not paying down the principal.

This structure is highly advantageous for flippers because it keeps carrying costs low while the property is not generating income. The full principal amount is due as a single balloon payment when the loan matures, which is paid off using the proceeds from the sale of the property. For example, on a $250,000 loan at a 10% interest rate, an interest-only payment would be approximately $2,083 per month, whereas a traditional principal-and-interest payment would be significantly higher. This preserved capital can be crucial for covering unexpected project costs or investing in your next deal.

Core Components: Leverage and Terms

Understanding the key metrics and terms of a hard money loan is essential for evaluating a deal and a lender's offer. These components define how much you can borrow, for how long, and under what conditions.

Loan-to-Cost (LTC): Financing Up to 90% Purchase and 100% Rehab

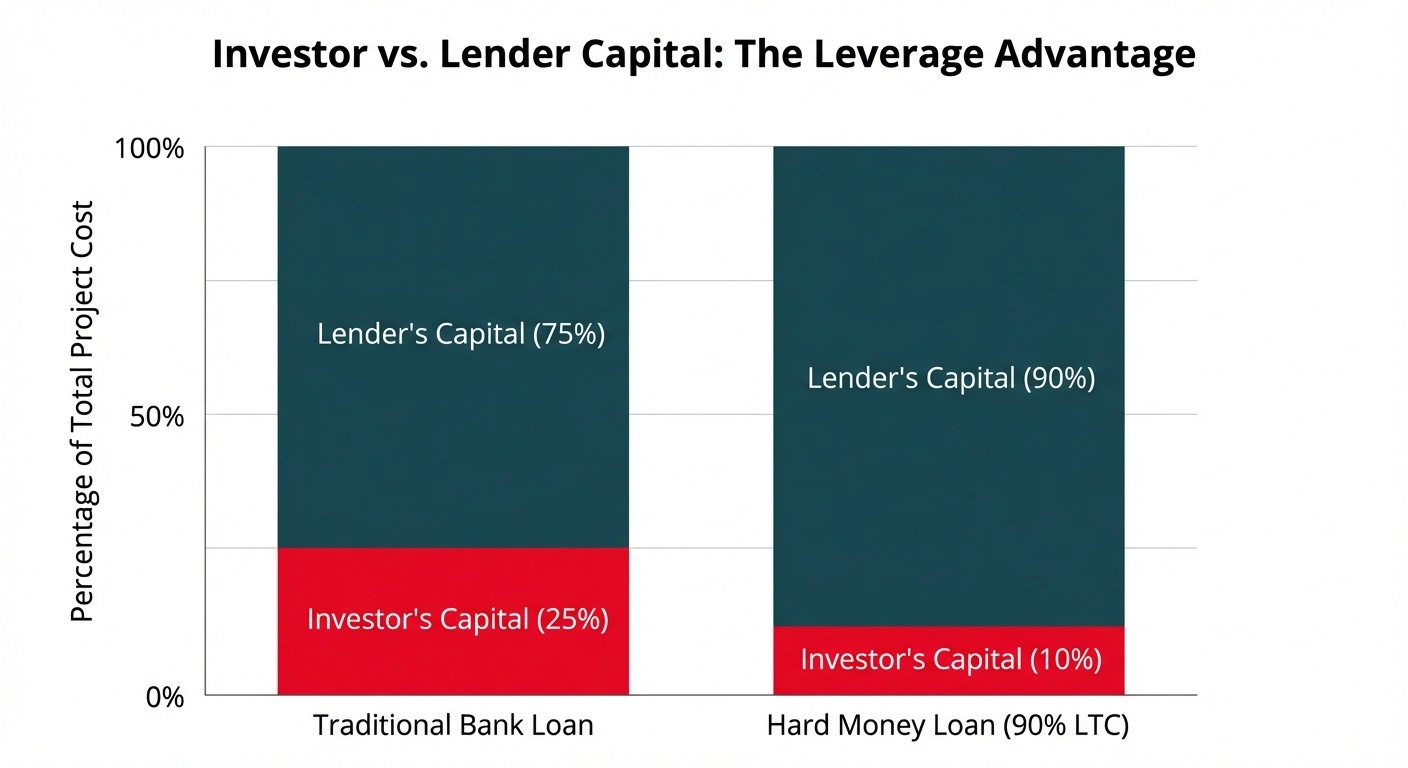

Loan-to-Cost (LTC) is a ratio that compares the total loan amount to the total project cost (purchase price + renovation costs). It is the primary metric lenders use to determine the maximum loan amount for a fix and flip project. OfferMarket, for instance, offers up to 90% LTC, which includes financing for up to 90% of the purchase price and 100% of the budgeted renovation costs.

Formula: LTC = (Loan Amount / (Purchase Price + Renovation Costs)

Example:

- Purchase Price: $300,000

- Renovation Budget: $75,000

- Total Project Cost: $375,000

- Lender's Maximum LTC: 90%

- Maximum Loan Amount: 90% of $375,000 = $337,500

In this scenario, the borrower would be responsible for the remaining 10% of the project cost ($37,500) plus closing costs as their down payment. The ability to finance 100% of the rehab is a massive advantage, as it allows investors to conserve their personal capital for other aspects of the business.

After-Repair Value (ARV): The Ultimate Cap on Your Loan

While LTC determines the loan amount based on your costs, the After-Repair Value (ARV) acts as the ultimate ceiling. ARV is the estimated market value of the property after all proposed renovations are completed. Lenders will not lend more than a certain percentage of the ARV, typically 75%. This is known as the Loan-to-Value (LTV) ratio, though in the context of a flip, it's based on the future value.

Formula: Maximum Loan Amount = ARV * Maximum LTV (e.g., 75%)

The lender will always use the lesser of the LTC and LTV calculations to determine your final loan amount. This protects them from over-leveraging a project where the costs are too high relative to the final value.

Example:

Purchase Price: $220,000

Renovation Budget: $80,000

Total Project Cost: $300,000

Estimated ARV: $420,000

LTC Calculation (at 90%): 0.90 * $300,000 = $270,000

LTV Calculation (at 75%): 0.75 * $420,000 = $315,000

In this case, the maximum loan amount would be $270,000, because it is the lower of the two figures. This ensures the investor maintains at least 25% equity in the completed project from the lender's perspective. You can use a construction loan calculator to model these scenarios and understand how leverage affects your deal's numbers.

Loan Term: Standard 12-Month Balloon Maturity

Hard money fix and flip loans are short-term instruments. The standard term is 12 months. This timeframe is typically sufficient for an investor to purchase, renovate, and sell a property. The entire loan principal is due at the end of this term in a single balloon payment.

Most reputable lenders understand that projects can face delays. Therefore, they often offer extension options, usually for a fee. A typical extension might be for 3 to 6 months and cost 1% of the outstanding loan balance. It's crucial to understand your lender's extension policy before signing the loan documents, as unforeseen issues with contractors or permitting can easily push a project beyond its initial timeline.

No Prepayment Penalties: A Key Feature for Flippers

A critical and highly favorable feature of most hard money fix and flip loans is the absence of prepayment penalties. This means you can sell the property and pay off the loan at any time within the 12-month term without incurring an extra fee.

This is essential for the fix and flip business model. If you complete a renovation in four months and find a buyer in the fifth month, you can close the sale, repay the loan, and realize your profits immediately. Traditional loans, and even some less scrupulous private lenders, may include prepayment penalty clauses that eat into your profits if you pay the loan off "too early." A lender like OfferMarket that offers no prepayment penalties aligns its success with the investor's goal: a fast and profitable flip.

The Economics of a Hard Money Loan: Rates and Fees

While hard money offers unparalleled speed and leverage, it comes at a higher cost than conventional financing. Understanding the full spectrum of rates and fees is crucial for accurately calculating your project's profitability.

Interest Rates: Typical Ranges and How They Are Determined

Interest rates for hard money fix and flip loans typically range from 9% to 12%, although they can be higher or lower depending on several factors. The final rate you receive is determined by the lender's assessment of the overall risk of the loan.

Key factors influencing your interest rate include:

Borrower Experience: A seasoned investor with a proven track record of successful flips will receive a more favorable rate than a first-time flipper. Lenders see experience as a significant risk-mitigating factor.

Credit Score: While hard money is asset-based, your personal credit score still matters. Borrowers with higher FICO scores (e.g., 720+) will qualify for better rates than those at the minimum threshold (e.g., 680).

Leverage (LTV/LTC): The more leverage you request, the higher the risk for the lender, which often translates to a slightly higher interest rate. A borrower putting more of their own cash into the deal may receive a rate discount.

Property Type and Location: A single-family home in a hot, stable real estate market is considered less risky than a multi-unit property in a more speculative area.

Origination Points: The Upfront Cost of Securing the Loan

Origination points are an upfront fee charged by the lender for creating and processing the loan. One point is equal to 1% of the total loan amount. For hard money loans, it's common to see origination fees ranging from 1 to 3 points.

Example:

- Total Loan Amount: $300,000

- Origination Fee: 2 points

- Cost of Points: 0.02 * $300,000 = $6,000

This $6,000 fee is typically deducted from the loan proceeds at closing, meaning you don't pay it out-of-pocket, but it reduces the net amount of funding you receive. When calculating your cash-to-close requirements, you must account for origination points alongside your down payment and other standard closing costs.

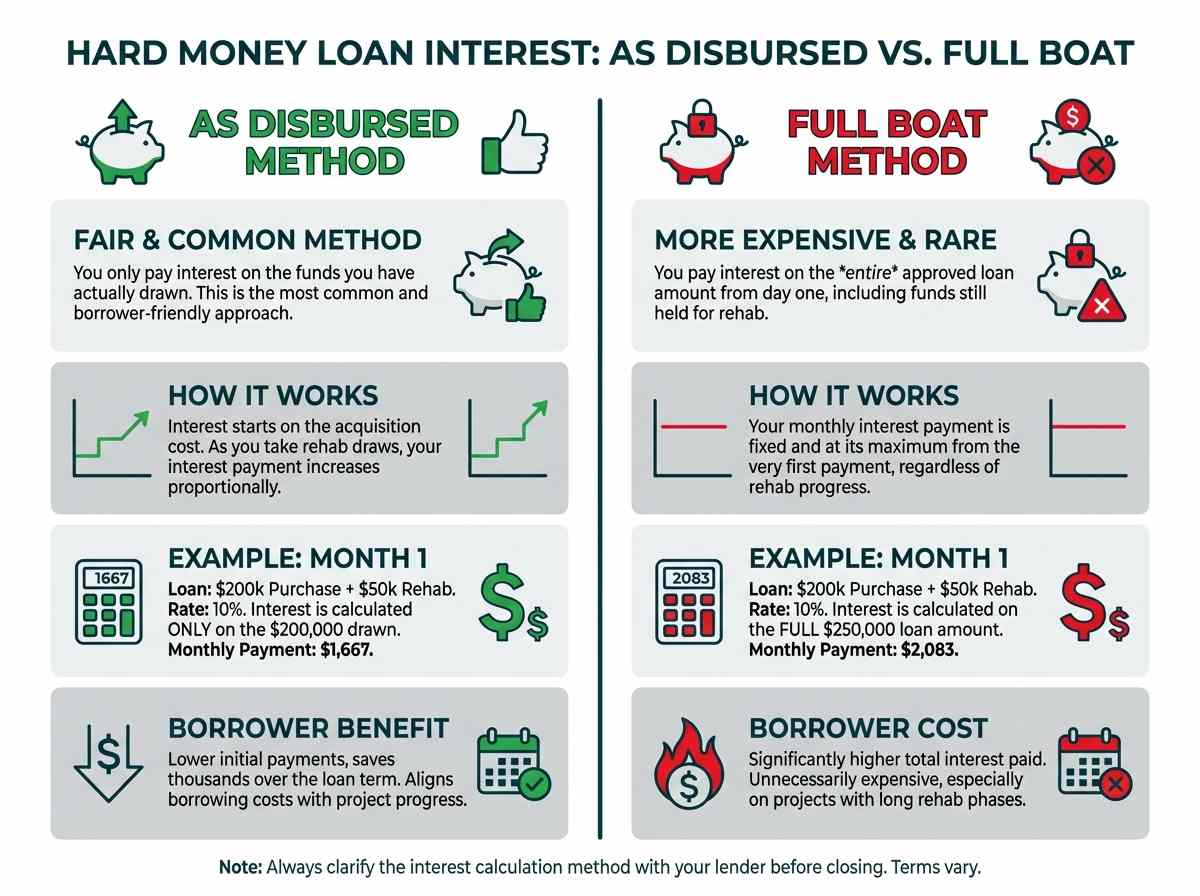

Calculating Interest: "As Disbursed" vs. "Full Boat"

How your interest is calculated can have a significant impact on your total borrowing costs. There are two primary methods:

"As Disbursed" (or "As-Used"): With this method, you only pay interest on the funds that have actually been paid out to you. At the start of the loan, you'll only pay interest on the acquisition portion. As you take draws from your rehab holdback, your principal balance increases, and so does your monthly interest payment. This is the most common and fairest method.

"Full Boat" (or "On Full Loan Amount"): Some lenders charge interest on the entire approved loan amount from day one, even on the rehab funds sitting in the holdback account. This is significantly more expensive for the borrower.

Example of the Difference:

Loan: $200,000 purchase + $50,000 rehab = $250,000 total loan.

Rate: 10% annual.

As Disbursed (Month 1): You've only drawn the $200,000 for purchase.

- Interest is calculated on $200,000.

- Monthly Payment: ($200,000 * 0.10) / 12 = $1,667

Full Boat (Month 1): You pay interest on the full $250,000.

- Interest is calculated on $250,000.

- Monthly Payment: ($250,000 * 0.10) / 12 = $2,083

Always clarify with your lender which method they use. A "full boat" interest calculation can add thousands of dollars to your project's cost over the life of the loan. Transparent lenders like OfferMarket use the "as disbursed" method.

Other Potential Fees

Beyond interest and points, there are other standard fees associated with securing a hard money loan. These are similar to the closing costs on any real estate transaction but may include some lender-specific items.

- Underwriting & Processing Fees: A flat fee to cover the administrative costs of evaluating your loan file. ($500 - $1,500)

- Appraisal & ARV Review Fee: The cost of the independent appraisal to determine the property's as-is value and After-Repair Value. ($500 - $1,000)

- Draw Inspection Fees: A fee charged for each construction draw inspection. ($150 - $250 per draw)

- Legal & Document Prep Fees: Covers the lender's attorney costs for preparing the loan documents. ($500 - $1,500)

- Title & Escrow Fees: Standard third-party costs for title insurance and closing services. (Varies by state and transaction size)

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Qualifying for Your Loan Part 1: The Borrower

Hard money lenders place a heavy emphasis on the deal itself, but the borrower's experience and financial stability are still crucial components of the underwriting process. Lenders often categorize borrowers into experience tiers, which directly impact the loan terms they can receive.

The Role of Experience Tiers in Underwriting

Lenders use experience tiers to quantify the risk associated with a borrower. An investor who has successfully completed ten flips is statistically far less likely to default than someone tackling their very first project. This experience translates directly into better terms: higher leverage, lower rates, and access to more complex loan products.

At OfferMarket, our experience tiers are structured to support investors at every stage of their growth, from novice to seasoned professional.

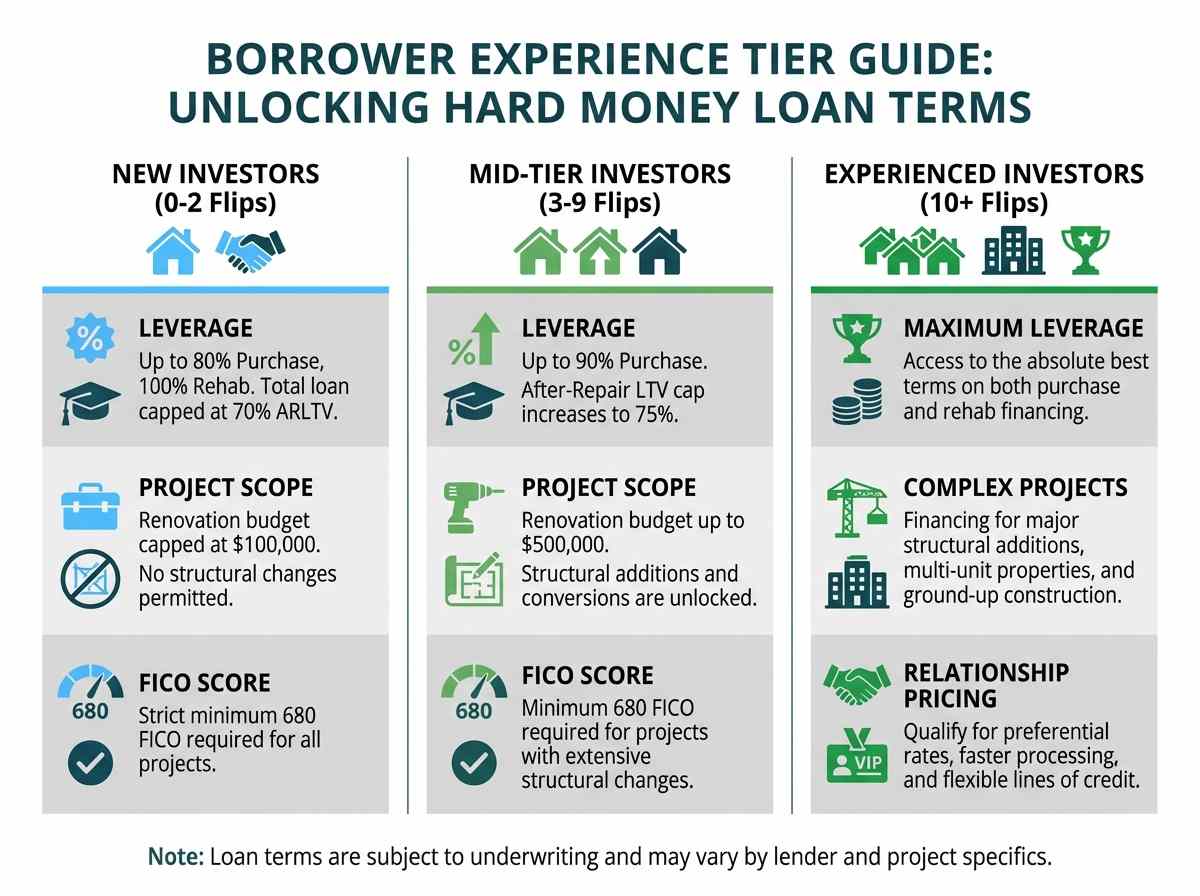

Tier 1: New Investors (0-2 flips)

This tier is for investors who are new to the fix and flip world, having completed zero, one, or two projects in the last 24-36 months.

This encompasses Tier 1 (0 past projects) and Tier 2 (1-2 past projects).

Leverage: Tier 1 is capped at 75% of the purchase price (or 80% if the borrower has a 720+ FICO). Tier 2 unlocks up to 80% of the purchase price. Both tiers finance 100% of the rehab, but the total loan is strictly capped at a 70% After-Repair Value (ARLTV).

Project Scope: The renovation budget is capped at $100,000 (and limited to 25% of the purchase price if the borrower has zero prior rehab experience). While they can do moderate-to-heavy internal renovations, they are strictly prohibited from structural changes like vertical/horizontal enlargements, condo conversions, or adding ADUs.

FICO Score: A strict minimum 680 FICO is required for both tiers.

Mid-Tier Investors (3-9 flips)

Once an investor has a few successful projects under their belt, they move into the mid-tiers. They have demonstrated an ability to manage a project from acquisition to disposition.

This covers Tier 3 (3-4 properties) and Tier 4 (5-9 properties).

Leverage: Initial leverage increases to 85% of the purchase price for Tier 3, and reaches the maximum 90% of the purchase price at Tier 4. The ARLTV cap increases to 75% for both tiers.

Project Scope: The maximum renovation budget increases to 2x the borrower's highest verified past budget, up to a $500,000 cap. These investors unlock the ability to execute extensive projects, including vertical/horizontal additions, conversions, and ADUs.

FICO Score: The minimum FICO requirement is 680 required if the investor is executing an extensive structural addition or conversion.

Tier 5: Experienced Investors (10+ flips)

This is the top tier, reserved for full-time, professional real estate investors and developers with an extensive track record.

Maximum Leverage: These borrowers have access to the absolute best terms, including maximum leverage on both purchase and rehab.

Complex Projects: They can secure financing for the most complex projects, including major structural additions, multi-unit properties, and even ground-up construction.

Relationship Pricing: Often, top-tier borrowers build relationships with lenders, leading to preferential pricing, faster processing, and more flexible underwriting. They may even qualify for lines of credit for multiple projects.

Qualifying for Your Loan Part 2: The Deal

For any hard money lender, the viability of the investment property is the most important factor. The lender is essentially your investment partner, and if the deal isn't profitable, they won't fund it. They assess the deal's strength through several key metrics.

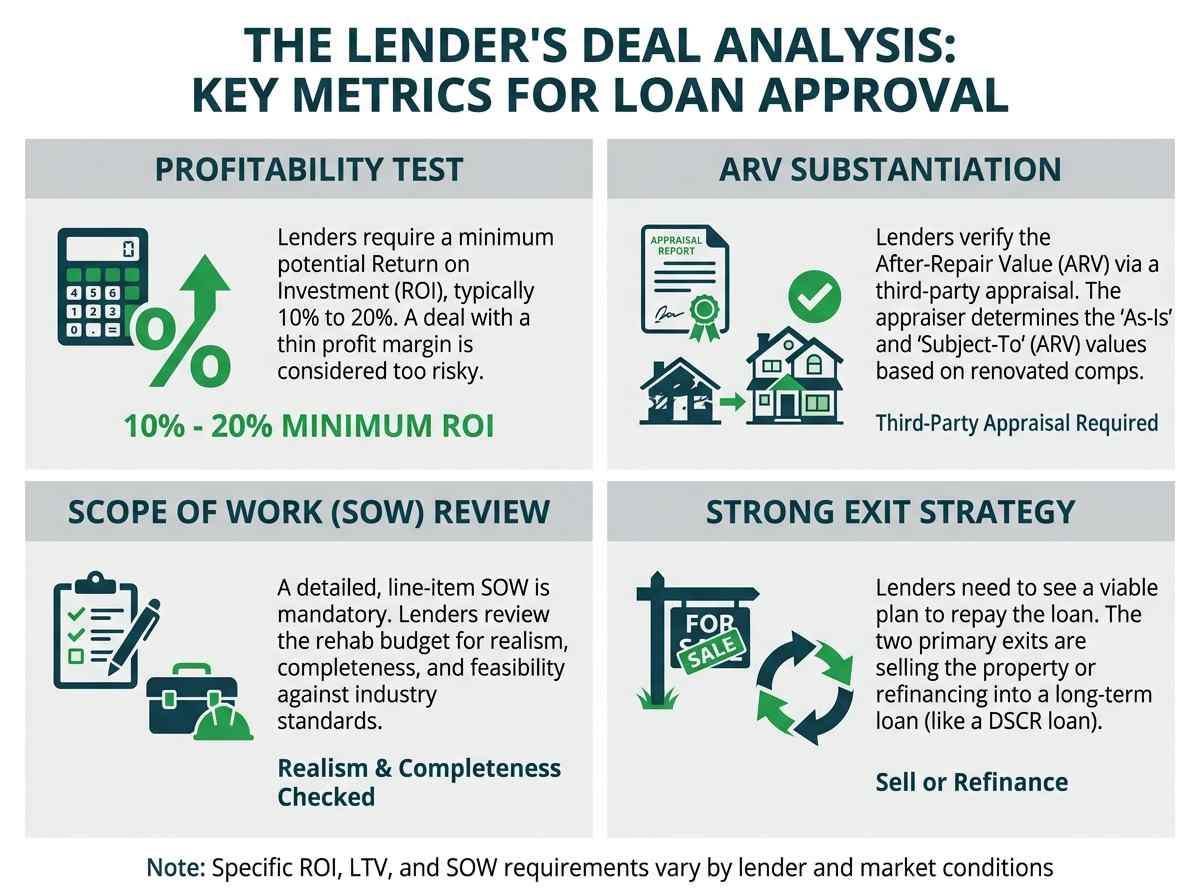

The Lender's Profitability Test: Requiring a 10% to 20% Minimum ROI

Lenders need to see a clear path to profit for the investor. A profitable deal for you means a successful loan repayment for them. Most lenders will run their own analysis on your numbers and will require the project to show a minimum potential Return on Investment (ROI), typically in the 10% to 20% range.

They will calculate this by taking your estimated net profit (ARV minus purchase price, rehab costs, financing costs, and selling costs) and dividing it by your total cash invested. If the potential ROI is too thin, the deal is considered too risky. A small, unforeseen repair or a slight dip in the market could erase the profit margin entirely, putting the loan at risk.

ARV Substantiation: How Lenders Verify the After-Repair Value

The After-Repair Value (ARV) is the cornerstone of the entire loan. An inflated ARV can lead to a disastrous over-leveraging of the property. Therefore, lenders are meticulous about verifying this number.

The primary tool for this is a third-party appraisal. The lender will order an appraisal from a licensed appraiser who has experience with renovated properties in the specific submarket. The appraiser will determine two values:

- "As-Is" Value: The current market value of the property in its distressed state.

- "Subject-To" Value: The projected market value of the property, subject to the completion of the proposed renovations outlined in your Scope of Work. This is the ARV.

The appraiser arrives at the ARV by finding recent sales of comparable, fully renovated properties (known as "comps") in the immediate vicinity. They will make adjustments based on differences in square footage, bed/bath count, lot size, and quality of finishes. Lenders will rely heavily on this independent, professional valuation to set the loan's LTV cap.

Scope of Work (SOW) Review: Ensuring the Rehab Budget is Realistic

A detailed and realistic Scope of Work (SOW) is a non-negotiable requirement. A vague or incomplete SOW is a major red flag for underwriters. Your SOW should be a line-item breakdown of every task to be performed, with associated costs for both labor and materials.

Lenders review the SOW for several reasons:

Realism: They compare your budget against industry-standard costs (often using software like RSMeans data) to ensure you haven't drastically under- or overestimated costs. An unrealistic budget is a leading cause of project failure.

Completeness: Does the SOW account for everything needed to bring the property to the standard of the comps used to justify the ARV? If the comps all have new roofs and your SOW doesn't include one, the lender will question your projected ARV.

Feasibility: Is the proposed work achievable within the loan term? A massive gut renovation might not be feasible in 12 months for an inexperienced investor.

A strong SOW demonstrates to the lender that you are a professional who has done their due diligence.

The Importance of a Strong Exit Strategy

The lender needs to know how you plan to pay back the balloon payment at the end of the 12-month term. For a fix and flip loan, there are two primary exit strategies:

Sell the Property: This is the most common exit. You list the renovated property on the market, sell it, and use the proceeds to pay off the hard money loan, pocketing the difference as profit.

Refinance into a Long-Term Loan: This is the "Rent" and "Refinance" part of the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy. You refinance the short-term, high-interest hard money loan into a long-term, lower-interest rental loan, such as a DSCR loan. This allows you to hold the property as an income-producing rental.

The lender will want to see that your chosen exit strategy is viable in the current market. For a sale, they'll look at the average days on market for similar properties. For a refinance, they'll check if market rents can support the debt service on a new loan.

Qualifying for Your Loan Part 3: Financial Requirements

While the "deal" is king in hard money, the borrower's personal financial standing provides a secondary layer of security for the lender. You must demonstrate that you have the financial capacity to handle your obligations for the loan.

Credit Score Requirements: The 680 FICO Minimum

Most reputable hard money lenders, including OfferMarket, have a minimum credit score requirement, typically 680 FICO. While a high credit score won't get a bad deal approved, a low credit score can certainly get a good deal denied.

Your credit score is seen as an indicator of your financial responsibility. A score below the minimum threshold suggests a higher risk of default on financial obligations. Additionally, scores at the lower end of the acceptable range may result in penalties, such as a higher interest rate or lower leverage, to compensate the lender for the increased risk. Significant recent credit issues like a bankruptcy, foreclosure, or a pattern of late payments can also be grounds for denial, even if your score is above the minimum.

Liquidity Verification: Cash for Down Payment, Closing Costs, and Reserves

Hard money lenders need to see that you have enough liquid cash to manage the project successfully. This is often referred to as "skin in the game." You will be required to provide recent bank statements, brokerage account statements, or retirement account statements to verify your liquidity.

The lender is looking for three things:

- Down Payment: You need enough cash to cover the portion of the purchase price not financed by the loan (e.g., 10-20%).

- Closing Costs & Origination Points: You must have funds to pay for all the fees associated with closing the loan.

- Reserves: This is crucial. Lenders require you to have additional cash reserves set aside after paying your down payment and closing costs. These reserves are for covering monthly interest payments and any unexpected project overruns. A common requirement is to show reserves equal to 3-6 months of interest payments.

Net Worth Requirements

Some lenders may have a minimum net worth requirement, especially for larger loan amounts. A common benchmark is a net worth equal to at least 10% of the loan amount. Your net worth is calculated as your total assets (real estate, investments, cash) minus your total liabilities (mortgages, car loans, credit card debt). This requirement provides an additional layer of assurance to the lender that you have the financial depth to withstand potential setbacks.

Entity Requirements: Borrowing as an LLC or Corporation

For liability protection and regulatory reasons, most hard money lenders will not lend to individuals. They require borrowers to take out the loan in the name of a business entity, most commonly a Limited Liability Company (LLC) or a corporation.

This structure separates your personal assets from your business assets. If something goes wrong with the project and you are sued, the lawsuit is directed at the LLC, protecting your personal home, savings, and other assets. If you don't already have an LLC, they are relatively easy and inexpensive to set up through your state's Secretary of State office or an online legal service. Lenders will require you to provide your entity's formation documents, such as the Articles of Organization and Operating Agreement, as part of the loan application.

The Hard Money Loan Process Step-by-Step

One of the primary advantages of hard money is speed. The application and underwriting process is streamlined to get you from quote to closing in a matter of weeks, not months. Here is a typical step-by-step guide to securing a hard money fix and flip loan with a modern lender like OfferMarket.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding in 10-21 Days

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Pros of Using Hard Money for Flips

For fix and flip investors, the advantages of hard money loans are substantial and often make deals possible that would otherwise be out of reach.

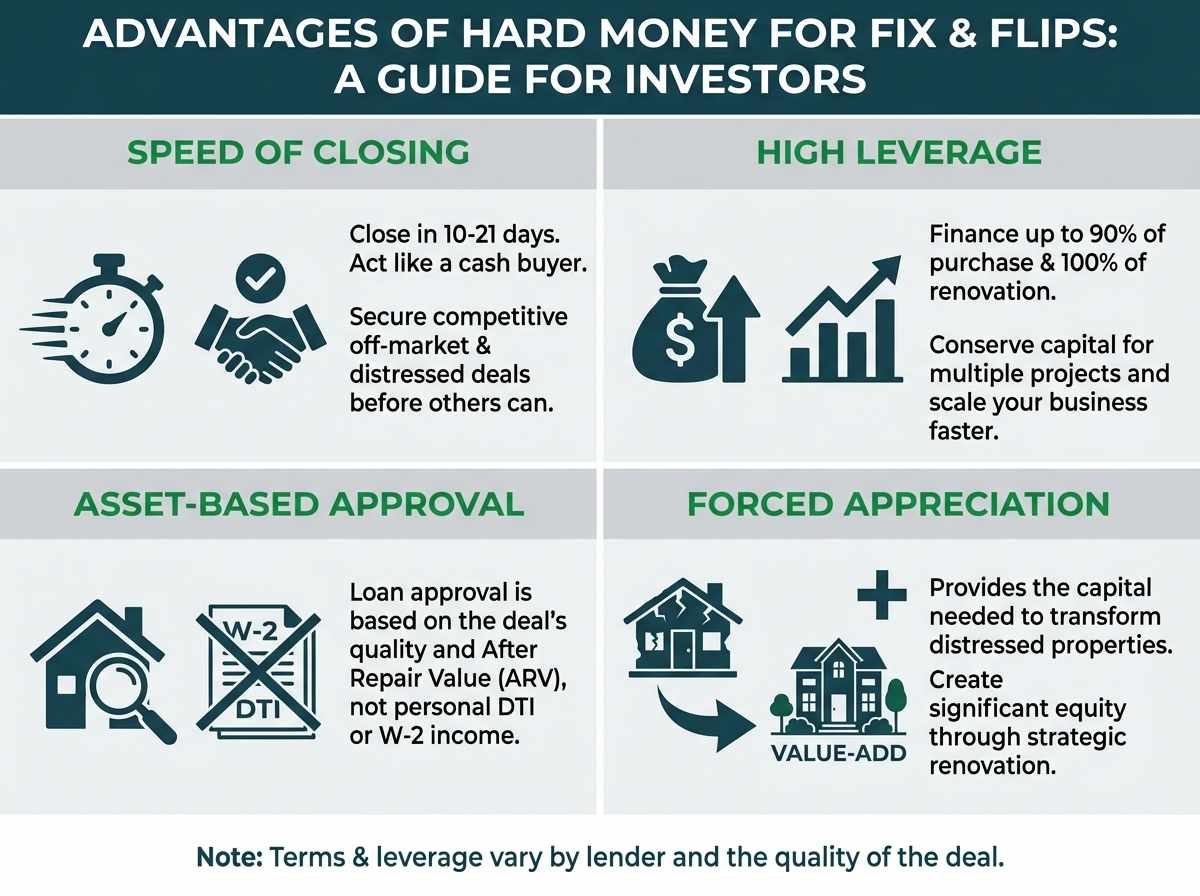

Speed of Closing: Securing Deals That Banks Cannot Finance in Time

In competitive real estate markets, the best deals are often off-market or require a quick close. Sellers of distressed properties are frequently looking for a fast, certain, all-cash-like offer. A traditional bank, with its lengthy underwriting process, simply cannot compete. A hard money lender's ability to close in 10-21 days gives you the power to act like a cash buyer, securing properties before your slower-moving competition.

High Leverage: Minimizing Cash Out-of-Pocket

The ability to finance up to 90% of the purchase and 100% of the renovation is a game-changer for investors. This high leverage allows you to conserve your capital. Instead of tying up all your cash in one project's down payment and rehab, you can spread your capital across multiple projects, scaling your business faster. It also provides a safety net, ensuring you have liquid reserves for unforeseen issues.

Asset-Based Approval: Your Deal's Strength Matters Most

Traditional lenders are obsessed with your personal debt-to-income (DTI) ratio and W-2 income. For many real estate investors, who may be self-employed or have income that is hard to document, this is a major hurdle. Hard money lenders focus on the asset. If you bring them a profitable deal with a solid ARV and a realistic budget, they are far more likely to approve the loan, even if your personal financial paperwork isn't perfect. The quality of the deal is what secures the loan.

Forced Appreciation: Provides the Capital to Transform a Distressed Asset

Hard money loans provide the necessary capital to execute a value-add strategy. You are not just buying a property; you are buying a property and the funds to transform it. This allows you to "force appreciation" by taking a distressed, undervalued asset and turning it into a desirable, market-ready home. The 100% rehab financing is the fuel for this entire business model, enabling you to create equity through construction, rather than just waiting for the market to appreciate.

Cons and Risks of Hard Money Loans

Despite their benefits, hard money loans are not without their risks and downsides. Investors must go into these loans with a clear understanding of the potential pitfalls.

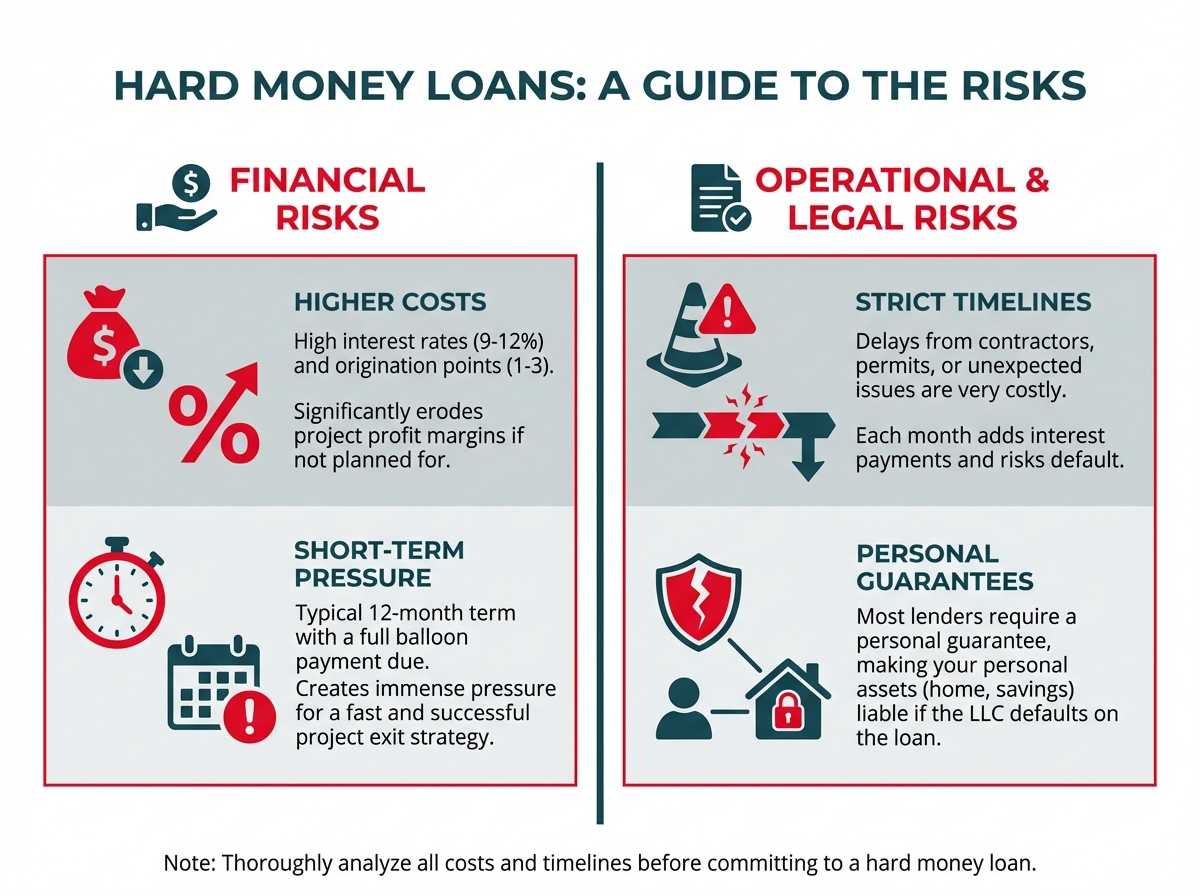

Higher Costs: Interest Rates and Points

The most obvious drawback is the cost. With interest rates between 9-12% and 1-3 origination points, hard money is significantly more expensive than a conventional 30-year mortgage. These costs must be carefully factored into your deal analysis. A project's profit margin must be substantial enough to absorb these higher financing costs and still provide a healthy return. Using a hard money loan on a deal with thin margins is a recipe for disaster.

Short-Term Nature: The Pressure of a 12-Month Balloon Payment

The 12-month term creates a hard deadline. You are on the clock from the day you close. The entire principal balance is due in one year, which puts immense pressure on you to complete the renovation and sell the property within that timeframe. Unlike a 30-year mortgage where you can ride out market fluctuations, a hard money loan requires a timely and successful exit.

Strict Timelines: Delays Can Jeopardize the Project

Any delay in the project can have severe financial consequences. Contractor issues, permit delays from the city, or unexpected structural problems can push your timeline back by weeks or months. Each month of delay means another month of interest payments, which eats directly into your profit. A significant delay could push you past your loan's maturity date, forcing you into a costly extension or, in a worst-case scenario, default.

Personal Guarantees: Most Hard Money Loans Require One

Even though the loan is made to your LLC, nearly all hard money lenders will require you, the principal of the LLC, to sign a personal guarantee (PG). This means that if the LLC defaults on the loan, the lender can pursue your personal assets—your home, savings, and investments—to repay the debt. The PG pierces the corporate veil of the LLC for the purpose of the loan, making you personally liable for the full amount. This is a significant risk that should not be taken lightly.

Tools and Resources for Fix and Flip Investors

Successful flipping requires more than just capital; it requires careful planning, analysis, and execution. Leveraging the right tools can make all the difference.

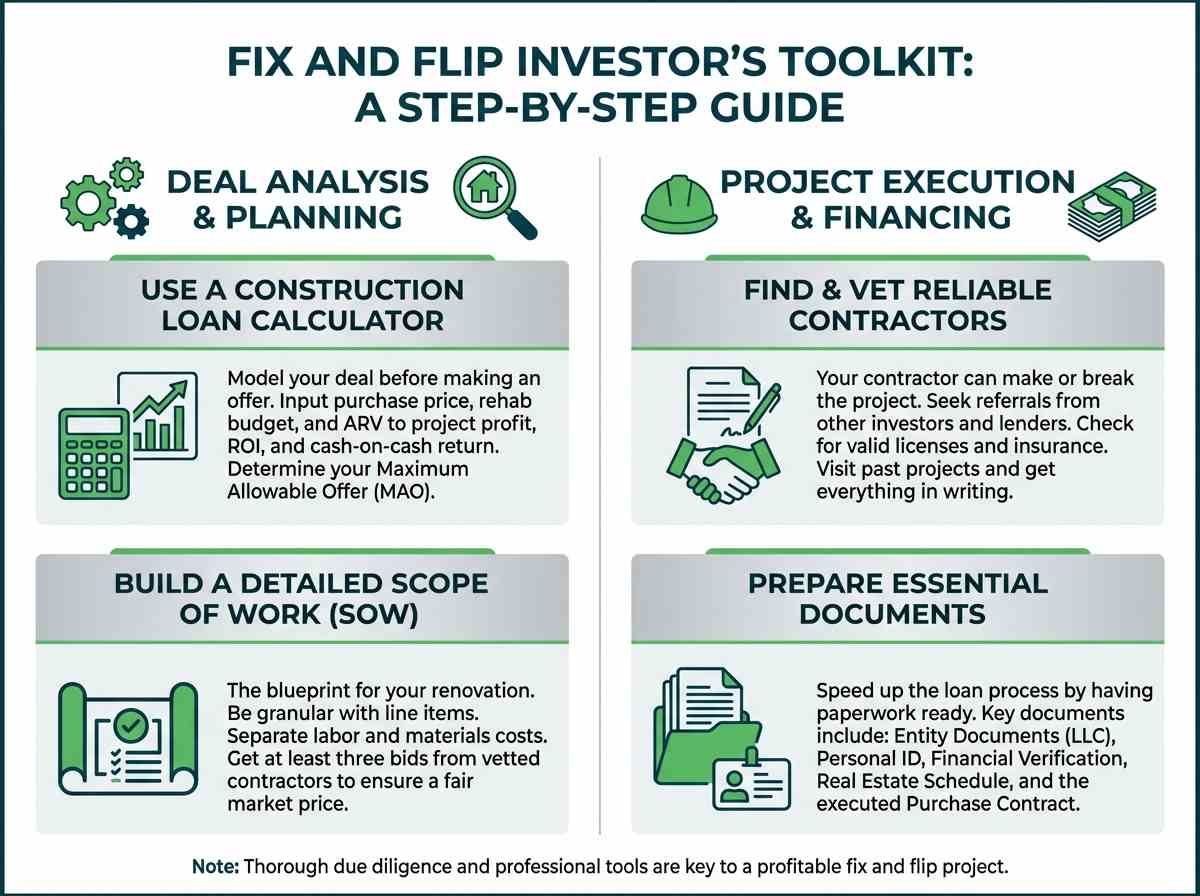

Using a Construction Loan Calculator to Model Your Deal

Before you ever make an offer, you need to run the numbers meticulously. A comprehensive construction loan calculator is an indispensable tool. It allows you to input all your key variables—purchase price, rehab budget, ARV, and financing terms (interest rate, points)—to instantly see your projected profit, ROI, and cash-on-cash return. This enables you to:

- Quickly evaluate how different loan scenarios impact your cost of capital.

- Run sensitivity analyses on interest rates, fees, and loan structure.

- Determine your maximum allowable offer (MAO) for a property to ensure it remains profitable.

How to Build a Detailed and Accurate Scope of Work

Your Scope of Work (SOW) is the blueprint for your entire renovation. A great SOW is the foundation of an on-time, on-budget project.

Be Granular: Don't just write "Renovate Kitchen." Break it down into line items: "Install 15 linear feet of shaker cabinets," "Install 40 sq. ft. of quartz countertops," "Install subway tile backsplash."

Separate Labor and Materials: Get itemized costs for both. This helps you spot where a contractor's bid might be inflated.

Get Multiple Bids: Always get at least three bids from vetted contractors for any major work. This ensures you're getting a fair market price.

Use a Template: Start with a professional Scope of Work template to ensure you don't miss any critical details.

Finding and Vetting Reliable Contractors

Your contractor can make or break your project. Finding a good one is paramount.

- Seek Referrals: Ask other local investors, real estate agents, or your hard money lender for recommendations.

- Check Licenses and Insurance: Verify that they have a valid contractor's license and carry both general liability and worker's compensation insurance. A great resource for this is the National Association of State Contractors Licensing Agencies (NASCLA).

- Visit Past Projects: Ask to see examples of their completed work and, if possible, speak with their previous clients.

- Get Everything in Writing: Never work on a handshake. A detailed contract that references your SOW and includes a payment schedule is non-negotiable.

Essential Documents for a Smooth Application Process

Having your paperwork organized before you apply will dramatically speed up the loan process. Create a digital folder with the following key documents ready to go:

- Entity Documents: Articles of Organization, Operating Agreement, and EIN confirmation letter for your LLC.

- Personal Identification: A clear copy of your driver's license or passport.

- Financial Verification: The two most recent statements for all bank and brokerage accounts you will use for liquidity verification.

- Real Estate Schedule: A simple spreadsheet listing all properties you currently own, their value, and any outstanding debt.

- For the Deal: A fully executed purchase contract and your detailed SOW.

Why Choose OfferMarket for Your Next Flip

Choosing the right lending partner is as important as choosing the right property. OfferMarket is built from the ground up to serve the unique needs of real estate investors with a focus on speed, transparency, and powerful leverage.

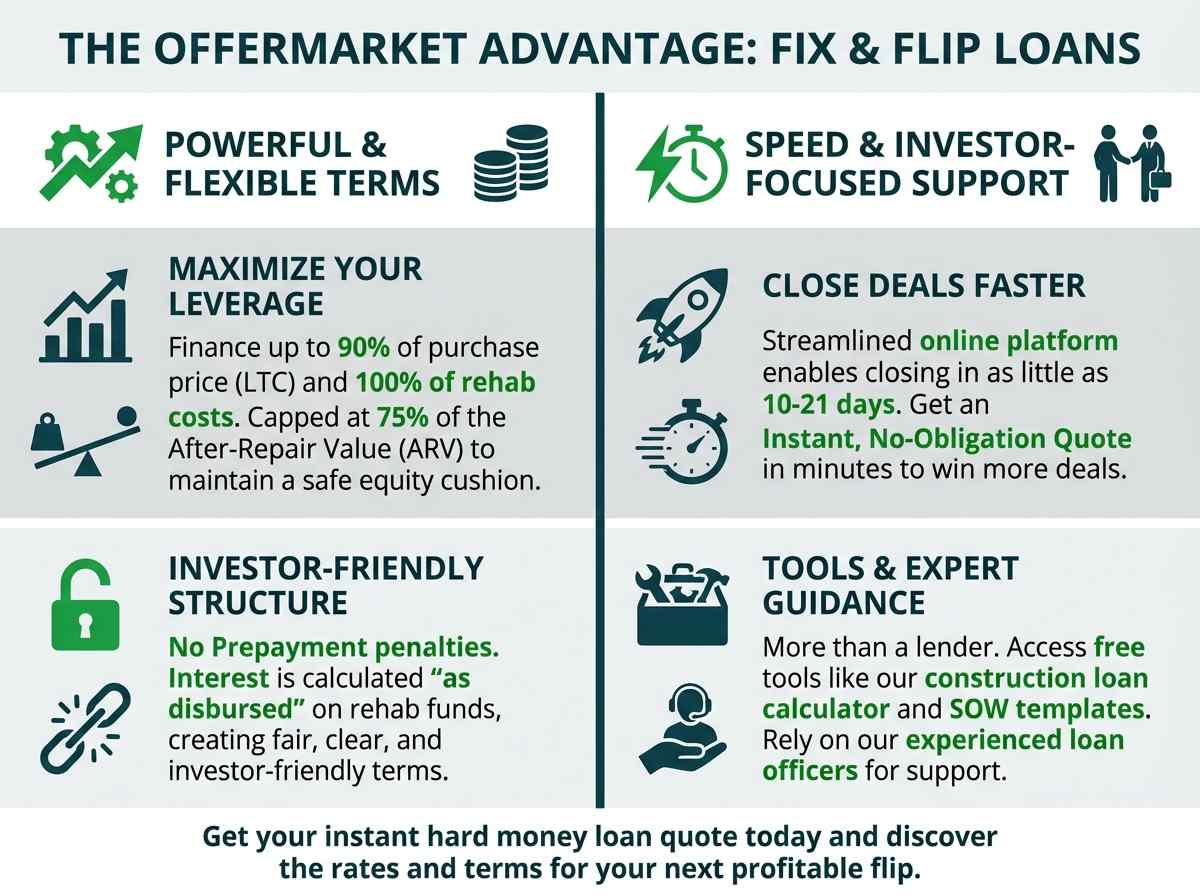

Competitive Terms: 90% LTC and 75% ARV Explained

We provide some of the most competitive leverage in the industry, allowing you to finance up to 90% of your purchase price and 100% of your rehab costs. This is all capped at a conservative 75% of the After-Repair Value, creating a structure that maximizes your capital while maintaining a safe equity cushion in the deal. These terms are designed to help you scale your business by doing more deals with less cash out-of-pocket.

Transparency and Speed: A Streamlined Process

Our online platform provides a transparent, streamlined process. You can get an instant, no-obligation quote in minutes and follow your loan's progress through our digital portal. We've eliminated the endless paperwork and bureaucratic delays of traditional lending to ensure you can close in as little as 10-21 days, giving you the competitive edge you need to win deals. With no prepayment penalties and "as disbursed" interest calculations, our terms are clear, fair, and investor-friendly.

Investor-Focused Tools and Support

We are more than just a lender; we are your partner. We provide a suite of tools, including our robust construction loan calculator and SOW templates, to help you analyze deals and plan your projects effectively. Our experienced loan officers understand real estate investing and are here to provide expert guidance throughout the process.

Get Your Instant Hard Money Loan Quote

Ready to see how our financing can work for your next project? The first step is to see your numbers. Enter your deal metrics and get your instant hard money loan quote today to discover the rates and terms available for your next profitable flip.

See Your Rate, Not Your Credit Score

Get an instant breakdown of rates, terms, and LTV for your next rental. No SSN required for your initial quote.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull