*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

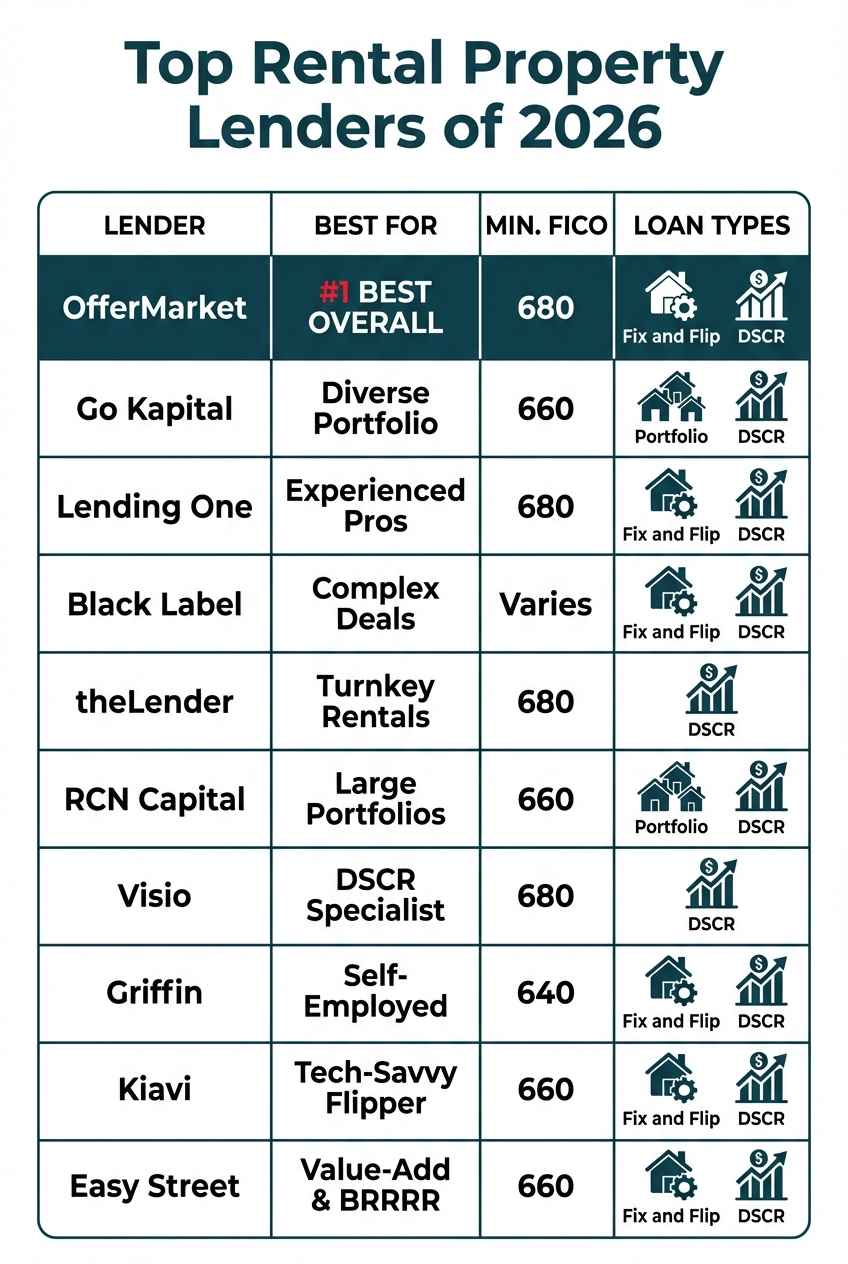

Top 10 Rental Property Lenders at a Glance

Finding the right lender is as critical as finding the right property. The best rental property lenders offer a combination of competitive rates, flexible loan products, and a streamlined process designed for real estate investors. Below is a quick comparison of the top lenders for 2026, highlighting their strengths to help you make a fast, informed decision. OfferMarket stands out as the best overall choice due to its blend of technology, speed, and dedicated investor support.

| Lender | Best For | Min. Credit Score (Typical) | Key Loan Types |

|---|---|---|---|

| OfferMarket | Overall Performance & Technology | 680 | DSCR, Fix and Flip, Ground Up, Slow Flip and HELOAN |

| Go Kapital | Diverse Loan Portfolio | 660 | DSCR, Bridge, Commercial, Fix and Flip |

| Lending One | Experienced, Established Investors | 680 | Rental Portfolio, DSCR, Fix and Flip |

| Black Label Capital | Complex & Creative Deals | Varies | Hard Money, Bridge, Non-QM |

| theLender | Stabilized, Turnkey Rentals | 680 | DSCR, Conventional-Style Investor Loans |

| RCN Capital | Large, Multi-State Portfolios | 660 | Fix and Flip, DSCR, Bridge, Multifamily |

| Visio Lending | DSCR Loan Specialization | 680 | DSCR, Rental Portfolio |

| Griffin Funding | Self-Employed Investors | 640 | Non-QM, Bank Statement, DSCR |

| Kiavi | Tech-Savvy Flippers | 660 | Fix and Flip, Bridge, Rental |

| Easy Street Capital | Value-Add & BRRRR Strategy | 660 | DSCR, Bridge, Multifamily |

In-Depth Lender Reviews: Ranking the Best of 2026

While a summary table is useful, selecting a financial partner requires a deeper dive. Here, we break down the pros, cons, and ideal customer profile for each of the top 10 rental property lenders.

1. OfferMarket: Best Overall Rental Property Lender

OfferMarket has earned its top spot by building a lending platform from the ground up with the modern real estate investor in mind. Where traditional lenders are often slow, paper-heavy, and rigid, OfferMarket combines cutting-edge technology with expert human support to deliver a superior borrowing experience. This focus on efficiency and service is why the company consistently receives high praise, reflected in its 4.5-star Google reviews.

The core mission is to empower investors to scale their portfolios faster. This is most evident in their funding timeline, which is a rapid 10-21 days from application to close. In a competitive market where speed wins deals, this is a significant advantage. The entire process is managed through a sleek online portal, eliminating the need for printing, scanning, and chasing down paperwork. From document submission to draw requests, every step is digitized and transparent.

OfferMarket Pros and Cons

Pros:

Innovative Tech Features: OfferMarket leverages technology to create real-world efficiencies. A prime example is their use of desktop appraisals, which can save investors over a week in closing time and hundreds of dollars compared to traditional, in-person appraisals. For renovation projects, their app-based draw approvals allow contractors to get paid faster, keeping projects on schedule and on budget.

Lower Overall Costs: By streamlining operations with technology, OfferMarket reduces its own overhead and passes those savings to the borrower. This often translates to lower loan origination fees and administrative costs compared to more traditional institutions. Their interest rates are highly competitive, ensuring your rental property cash flows effectively from day one.

Exceptional Client Support: Despite its tech focus, OfferMarket provides high-touch client support. Each borrower is paired with a dedicated loan officer who understands real estate investing and can provide guidance on complex deals. This combination of digital efficiency and human expertise is a key differentiator.

Wide Range of Investor-Focused Loans: They are not a one-trick pony. OfferMarket provides a full suite of loan products tailored specifically for investors, ensuring they can be a long-term financial partner as your strategy evolves.

Cons:

- Minimum Credit Score of 680: To maintain their speed and competitive pricing, OfferMarket requires a minimum FICO score of 680. While this is a reasonable benchmark for serious investors, it may exclude some beginners who are still building their credit profile.

OfferMarket Loan Products

OfferMarket's product suite is designed to cover the entire lifecycle of a real estate investment:

DSCR Loans: The cornerstone for buy-and-hold investors. These loans qualify based on the property's rental income, not your personal debt-to-income ratio, making it easier to scale your portfolio. They are perfect for long-term financing of single-family rentals, condos, and small multifamily properties.

Fix and Flip Loans: For investors focused on short-term projects, these hard money loans provide fast access to capital. They can finance up to 90% of the purchase price and 100% of the renovation costs, with terms typically lasting 12 months.

Ground Up Construction Loans: For investors building new properties, these loans cover everything from land acquisition to vertical construction. Underwriting is stricter, requiring significant investor experience.

Slow Flip Loans: A unique hybrid product for renovations that may take longer than a typical flip. With a 5-year term, it gives investors breathing room for projects with permitting delays or more extensive rehabs, avoiding the pressure of a 12-month deadline.

Home Equity Loans: Allows investors to tap into the equity of their existing rental properties without refinancing the primary mortgage. This is an excellent tool for unlocking capital to acquire new assets.

For investors who value speed, efficiency, and a true partnership, OfferMarket is the clear leader. Get an instant quote to see your customized rates and terms in minutes.

2. Go Kapital

Go Kapital is a private lending firm that has built a reputation for offering a wide spectrum of financing solutions that cater to various niches within the real estate investment landscape. They position themselves as a one-stop shop for investors, providing everything from short-term bridge loans to long-term rental financing and commercial property loans. This breadth of products is their primary strength, appealing to investors who manage a diverse portfolio of assets and strategies.

Their team often emphasizes a relationship-based approach, working to understand the specifics of a deal rather than relying solely on algorithmic underwriting. This can be beneficial for investors with slightly more complex situations that don't fit neatly into a standard lending box.

Go Kapital Pros and Cons

Pros:

Broad Range of Loan Products: Go Kapital's extensive menu of options is a major draw. An investor can secure a fix and flip loan, then refinance into a DSCR loan with the same lender, simplifying the financing lifecycle of a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) project. They also venture into commercial and multifamily spaces, which is a plus for investors looking to scale beyond 1-4 unit properties.

Flexible Underwriting: Compared to conventional banks, Go Kapital is known for more flexible and creative underwriting. They are often willing to look at the story behind the deal and the borrower's experience, not just the raw numbers on a credit report.

Nationwide Lending: They operate in most states, providing a consistent financing source for investors who are expanding their operations across different markets.

Cons:

Potentially Longer Funding Times: While more flexible, their relationship-based, manual underwriting process can sometimes translate into longer funding timelines compared to tech-first lenders like OfferMarket or Kiavi. For time-sensitive acquisitions in a hot market, this could be a drawback.

Less Transparent Fee Structure: Some borrowers have reported that the fee structures can be complex, with various points and processing fees that may not be as straightforward as those from more streamlined online lenders. It's crucial to get a detailed term sheet and review all costs carefully.

Technology Lag: Their online portal and application process, while functional, may not be as intuitive or feature-rich as platforms designed with a "digital-first" mindset. This can mean more manual follow-up via email and phone calls.

Best for: Go Kapital is an excellent choice for experienced investors with a diverse portfolio of property types (residential, multifamily, commercial) who value a single lending relationship and require more customized or creative financing solutions.

3. Lending One

Lending One is one of the more established and well-recognized names in the private lending space for real estate investors. Backed by the significant capital and resources of its parent company, Lending One has the scale to handle a high volume of loans across the country. They have a strong reputation for reliability and have been a consistent presence in the market for years.

Their primary focus is on providing financing for non-owner-occupied residential properties, with a core offering of rental loans, portfolio loans, and fix and flip financing. They cater to seasoned investors who have a proven track record and are looking for a dependable capital partner to help them scale.

Lending One Pros and Cons

Pros:

Strong Reputation and History: Having funded billions in loans, Lending One has a long and established track record. This provides a level of trust and security for investors who may be wary of newer, less proven lenders. Their history is a testament to their stability through various market cycles.

Portfolio Loan Specialist: They excel at providing blanket loans for investors with larger portfolios of rental properties. This allows an investor to consolidate multiple properties under a single loan, simplifying management and potentially unlocking better terms.

Competitive Rates for Experienced Investors: For borrowers with a strong history of successful projects and good credit, Lending One can offer very competitive interest rates and terms, leveraging their scale to reduce the cost of capital.

Cons:

More Traditional Process: Their application and underwriting process can feel more like a conventional bank than a modern fintech lender. This may involve more paperwork, manual document uploads, and a less transparent step-by-step online tracking system.

Less Flexibility for New Investors: Lending One's underwriting tends to be more rigid and heavily weighted towards experience. New investors or those with a limited track record may find it more difficult to get approved or may be offered less favorable terms compared to lenders who place a greater emphasis on the asset's quality.

Slower to Adopt New Technology: While they have an online presence, they are not typically seen as being on the cutting edge of lending technology. Features like desktop appraisals or app-based draw management are less common, which can slow down the overall process.

Best for: Lending One is ideal for experienced, high-volume investors and those looking to secure a portfolio loan for five or more properties. They are a great fit for borrowers who prioritize stability and reputation over cutting-edge speed and technology.

4. Black Label Capital

Black Label Capital operates in a specific and valuable niche within the rental property lending world: creative financing and complex deals. They are a hard money lender that prides themselves on their ability to fund deals that other, more conventional lenders would turn away. This could include properties with unique zoning, borrowers with credit or income documentation challenges, or deals that require exceptionally fast, non-contingent closing.

Their approach is highly entrepreneurial. They underwrite the deal and the asset's potential first and foremost. While borrower credit and experience are considered, they are often secondary to the viability of the project. This makes them a go-to lender for opportunistic investors who find high-value but unconventional opportunities.

Black Label Capital Pros and Cons

Pros:

Specializes in Complex Deals: If you have a property that is mid-construction, has title issues, or is otherwise "hairy," Black Label Capital has the expertise to navigate the complexities and get the loan funded. They are true problem-solvers.

Asset-Based Lending Focus: Their primary underwriting criterion is the "as-repaired value" (ARV) of the property. This means an investor with a fantastic deal but less-than-perfect credit can still secure financing.

Speed for Non-Standard Loans: Because they are a direct hard money lender with their own capital, they can make decisions and fund loans very quickly, often in a matter of days, even for complicated scenarios.

Cons:

Higher Rates and Fees: This flexibility and speed come at a cost. Hard money loans from lenders like Black Label Capital will almost always have higher interest rates (often in the double digits) and more points (origination fees) than DSCR loans or other more conventional investor products. They are a tool for short-term situations, not long-term holds.

Not Ideal for Long-Term Rentals: Their loans are typically short-term bridge or rehab loans. An investor would use them to acquire and stabilize a property, then refinance out with a long-term lender like OfferMarket. They are not a permanent financing solution.

Less Structured Process: The process can be less standardized than with other lenders. It's highly dependent on the individual loan officer and the specifics of the deal, which can lead to a less predictable experience for the borrower.

Best for: Black Label Capital is the perfect lender for experienced investors, flippers, and wholesalers who encounter unique opportunities that require fast, flexible, asset-based financing and are prepared to pay a premium for that service.

5. theLender

theLender is a mortgage company that serves both the consumer (owner-occupied) and investor markets. For real estate investors, their primary value proposition is offering products that feel almost like conventional loans but are specifically designed for investment properties. They are particularly strong in the DSCR loan space, providing a straightforward, no-income-verification product for turnkey rental properties.

They appeal to investors who may be graduating from using conventional Fannie Mae/Freddie Mac loans and are looking for a specialized lender who speaks their language but still offers a familiar, traditional process. They are less focused on the heavy value-add or fix and flip space and more on financing stabilized, cash-flowing assets.

theLender Pros and Cons

Pros:

Competitive on Rates for Standard DSCR: For a straightforward DSCR loan on a clean, turnkey property with a strong-credit borrower, theLender is often very competitive on interest rates. Their cost of capital is low, and they can pass those savings on.

Familiar, Conventional-Style Process: For investors who are comfortable with the traditional mortgage process, theLender provides a sense of familiarity. Their loan officers are knowledgeable and the underwriting, while thorough, is predictable.

Strong Focus on Stabilized Properties: They have deep expertise in underwriting and financing properties that are already rented or are rent-ready. Their process is optimized for this specific type of asset.

Cons:

Less Focus on Value-Add Projects: They are not the ideal choice for BRRRR investors or flippers. Their loan products and underwriting are not typically designed to fund heavy renovations or construction.

Can Be Slower and More Paper-Intensive: Similar to Lending One, their process is not as technologically advanced as some competitors. Expect to provide a full suite of documents and be prepared for a more traditional 30-day closing timeline.

Limited Product Diversity for Investors: While strong in DSCR, their offerings for other investment strategies like flipping or new construction are less robust compared to a specialist like OfferMarket.

Best for: theLender is an excellent choice for buy-and-hold investors who focus on acquiring stabilized, turnkey rental properties and are primarily seeking the most competitive interest rate for a long-term DSCR loan.

6. RCN Capital

RCN Capital is a major national player in the private lending industry, known for its extensive reach and broad array of loan programs for real estate investors. They have been in business for over a decade and have a well-earned reputation for being a reliable source of capital for both short-term and long-term projects. Their size and experience allow them to handle a large volume of loans across nearly every state.

They offer a comprehensive suite of products, including fix and flip loans, DSCR loans for long-term rentals, bridge loans, and financing for multifamily properties. This makes them a viable option for investors at various stages of their careers, from first-time flippers to seasoned landlords managing large portfolios.

RCN Capital Pros and Cons

Pros:

Extensive Experience and National Footprint: RCN Capital has seen thousands of deals and operates nationwide. This experience means they understand the nuances of different markets and have a refined process for underwriting and closing loans efficiently at scale.

Wide Array of Loan Programs: Similar to Go Kapital, they offer a full menu of investor loan products. This allows investors to use them for different strategies, whether it's a 12-month flip or a 30-year rental loan.

Reliable and Well-Capitalized: As one of the larger private lenders, they have a strong balance sheet and a consistent ability to fund their commitments. In uncertain markets, this reliability can be a significant advantage.

Cons:

Can Be Less Flexible on Terms: Due to their size, their underwriting criteria can be more institutional and rigid. For less experienced borrowers or deals that are slightly outside the box, they may be less flexible on leverage and pricing compared to smaller, more nimble lenders.

Process Can Feel Impersonal: As a high-volume lender, the borrower experience can sometimes feel less personal. You may interact with multiple different people throughout the loan process (an originator, a processor, an underwriter, a closer), which can be less streamlined than having a single point of contact.

Not Always the Cheapest Option: While their rates are competitive, they are not always the absolute lowest in the market. They sell on reliability and certainty of execution, which sometimes comes with a slight price premium.

Best for: RCN Capital is a strong choice for seasoned investors who are scaling large, multi-state portfolios and need a reliable, well-capitalized lending partner with a national presence and a diverse product line.

7. Visio Lending

Visio Lending has carved out a very specific and dominant niche in the investor finance world: they are the nation's leader in DSCR loans. For over a decade, their entire business model has been built around providing long-term financing for buy-and-hold investors. This singular focus has allowed them to become true experts in this product, refining their process to a science.

They are known for their "Landlord Loans," which are exclusively underwritten based on the cash flow of the property. If the property's rent can cover the mortgage payment, taxes, insurance, and association dues (PITIA), the borrower is likely to be approved, regardless of their personal income.

Visio Lending Pros and Cons

Pros:

Deep Expertise in DSCR Loans: No one knows the DSCR loan product better than Visio. Their entire team, from sales to underwriting to servicing, is specialized in this type of financing. This expertise leads to a smooth and predictable process for qualifying deals.

Streamlined Process for Rentals: Their application and underwriting process is highly optimized for rental properties. They know exactly what documents to ask for and how to analyze a lease agreement, which can speed up closing times for this specific loan type.

Competitive Pricing for their Niche: Because of their volume and specialization in DSCR loans, they are able to offer very competitive rates and terms for this product, especially for experienced landlords.

Cons:

Limited Product Offerings: The biggest drawback is their lack of diversity. If you are a flipper, a builder, or need a short-term bridge loan, Visio is not the lender for you. They are a one-trick pony, albeit a very good one.

Not Suitable for Value-Add Projects: Their loans are designed for stabilized, cash-flowing properties. They are not structured to finance the purchase and renovation of a distressed property. An investor would need a different lender for the "rehab" phase of a BRRRR project.

Can Be Rigid on DSCR Requirements: As specialists, they have very specific and non-negotiable requirements for their DSCR calculation (typically requiring a ratio of 1.2 or higher). If your property's cash flow is borderline, you may have trouble getting approved.

Best for: Visio Lending is the undisputed best choice for buy-and-hold investors who focus exclusively on acquiring turnkey, cash-flowing rental properties and want to partner with a lender that is a master of the DSCR loan.

8. Griffin Funding

Griffin Funding is a mortgage lender that specializes in non-qualified mortgage (Non-QM) loans. While they serve a variety of borrowers, they have developed a strong reputation among real estate investors, particularly those who are self-employed or have non-traditional income streams. Traditional lenders rely heavily on W-2s and tax returns, which can be a major hurdle for business owners, self employed, and full-time investors.

Griffin Funding solves this problem by offering alternative documentation loans. Their most popular programs for investors include bank statement loans (where they analyze business bank account deposits to determine income) and asset-based lending (where they qualify the borrower based on their liquid assets).

Griffin Funding Pros and Cons

Pros:

Excellent for Self-Employed Investors: Griffin Funding is a lifeline for investors who can't qualify for conventional loans due to the way their income is structured. Their bank statement program is a game-changer for entrepreneurs.

Flexible Income Verification: They offer a variety of ways to prove income beyond tax returns, including asset depletion, 1099-only loans, and profit & loss (P&L) statement programs. This flexibility opens the door to financing for many otherwise-qualified borrowers.

Offers DSCR and other Non-QM products: In addition to their unique income verification methods, they also offer a standard DSCR loan, making them a versatile option for investors with different needs.

Cons:

Process Can Be Slower: Underwriting alternative documentation loans is inherently more complex and time-consuming than a standard W-2 loan. Borrowers should be prepared for a more involved process with more requests for documentation, potentially leading to longer closing times.

Higher Rates for Non-QM Loans: The flexibility of Non-QM loans comes with a higher risk for the lender, which is passed on to the borrower in the form of slightly higher interest rates and fees compared to a conventional or standard DSCR loan.

May Not Be Ideal for W-2 Investors: If you are a real estate investor with a straightforward W-2 job, you may find more competitive pricing and a simpler process with a lender that specializes in standard DSCR or conventional investor loans.

Best for: Griffin Funding is the top choice for self-employed real estate investors, business owners, and those with significant assets but complex or hard-to-document income who need flexible underwriting to grow their rental portfolio.

9. Kiavi

Kiavi (formerly known as LendingHome) is a pioneer in applying technology to the hard money and investor lending space. Their entire platform is built around a data-driven, algorithmic approach to underwriting and funding loans. This allows them to provide investors with pre-approvals in minutes and close loans in a fraction of the time of traditional lenders.

Their primary focus has historically been on the fix and flip market, where speed is paramount. They have since expanded their offerings to include rental loans, making them a viable option for both short-term and long-term investors who prioritize a fast, seamless, and entirely digital experience.

Kiavi Pros and Cons

Pros:

Unmatched Speed and Efficiency: Kiavi's technology platform is their biggest strength. Investors can get pre-approved, upload documents, and track their loan status 24/7 through a sophisticated online portal. Their ability to close loans in as little as 10 days is a massive competitive advantage.

Streamlined Online Experience: For tech-savvy investors who prefer to manage the process themselves, Kiavi's platform is best-in-class. It's intuitive, transparent, and minimizes the need for phone calls and emails.

Data-Driven Valuations: They leverage vast amounts of property data to help determine a property's after-repair value (ARV), which can provide investors with an extra layer of confidence in their numbers.

Cons:

Heavily Reliant on Algorithms: The data-driven model can be a double-edged sword. If a deal has unique characteristics or a story that the algorithm can't comprehend, it can be difficult to get an exception. The process can lack the personal touch and flexibility needed for complex or non-standard deals.

Customer Service Can Be Less Personalized: While efficient, the customer service experience can sometimes feel transactional. Borrowers may not have a single, dedicated point of contact throughout the entire loan process.

Can Be More Expensive for Smaller Loans: Their fee structure and rates are optimized for volume and may not be the most competitive for smaller loan amounts or for investors who only do a few deals per year.

Best for: Kiavi is the ideal lender for tech-savvy, high-volume flippers and BRRRR investors who prioritize speed and a seamless digital experience above all else.

10. Easy Street Capital

Easy Street Capital is a direct private lender that has built a strong reputation for being flexible and solution-oriented, particularly in the DSCR and bridge loan space. They are known for their "make sense" approach to underwriting, where they are willing to listen to the story behind the deal and work with investors to find creative solutions.

They are particularly well-regarded for their ability to finance value-add projects, including multifamily properties. They understand the BRRRR strategy inside and out and have loan products designed to facilitate it, such as bridge loans that can be seamlessly refinanced into their own long-term DSCR product.

Easy Street Capital Pros and Cons

Pros:

Flexible and Creative Underwriting: Easy Street Capital's biggest differentiator is their willingness to be flexible. They are known for working with borrowers on properties with lower DSCR ratios, unique property types, and investors who may not fit the perfect credit/experience mold.

Strong Support for BRRRR and Value-Add: They are an excellent partner for investors focused on forcing appreciation through renovations. Their bridge-to-perm loan options streamline the BRRRR process.

Focus on Multifamily: In addition to 1-4 unit properties, they have a strong appetite for financing smaller multifamily buildings (5-20 units), which is a niche that not all private lenders serve well.

Cons:

May Not Be as Competitive on Price: This high degree of flexibility and personalized service can sometimes translate to slightly higher rates or fees compared to larger, more volume-focused institutions that are competing solely on price for A-paper deals.

Smaller Scale than National Giants: While they lend nationwide, they do not have the same scale or brand recognition as a lender like RCN Capital or Lending One. This is not necessarily a negative, but something to be aware of.

Process is Less Tech-Driven: While they have an online presence, their process relies more on the expertise of their loan officers than on a fully automated tech platform like Kiavi's. This results in a more personal but potentially less "on-demand" experience.

Best for: Easy Street Capital is a fantastic choice for investors focused on the BRRRR strategy, value-add projects, or small multifamily properties who need a lender with flexible, common-sense underwriting.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

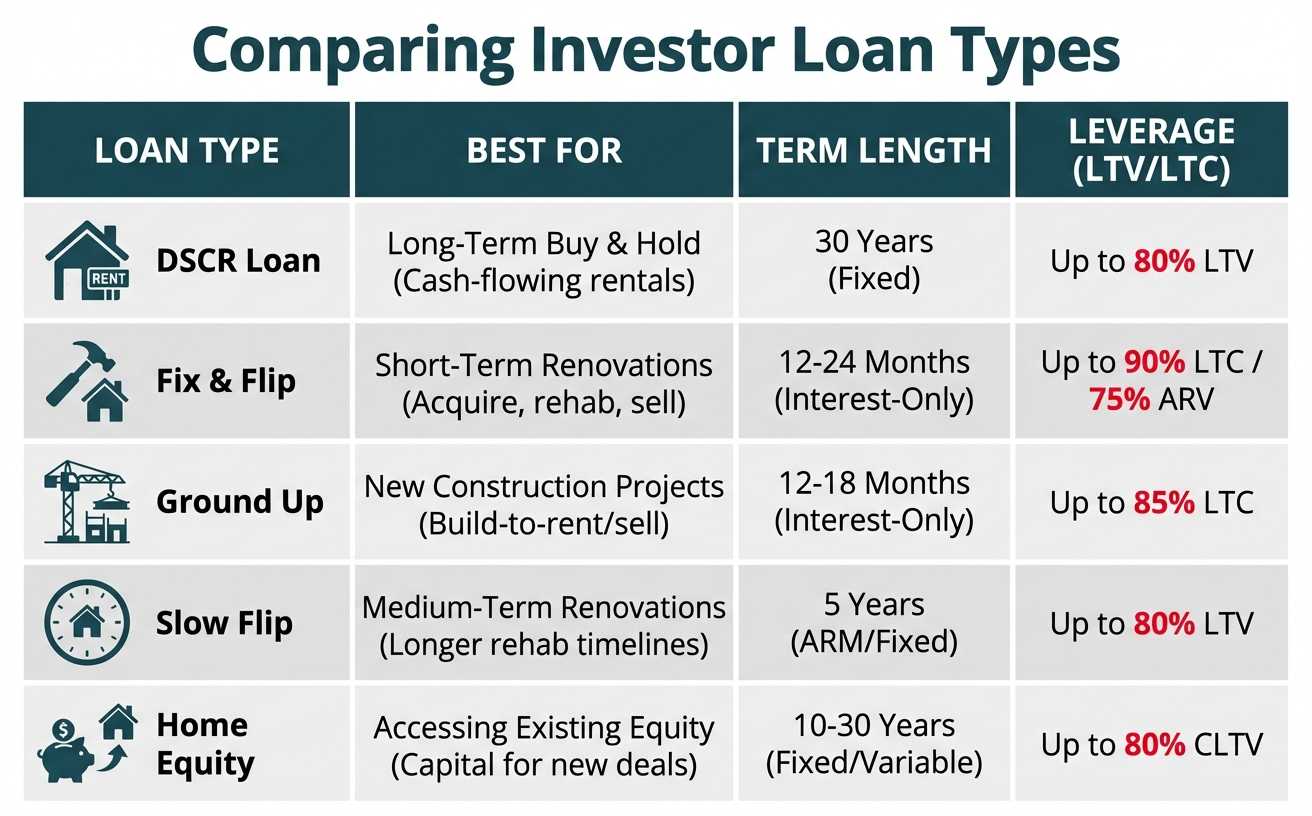

Get Your Quote →Types of Rental Property Loans Explained

Understanding the different loan types available is crucial to matching your financing with your investment strategy. Using the wrong loan can cost you time and money, or even put your project at risk. Here’s a breakdown of the most common loan types for real estate investors.

DSCR Loans: Financing Based on Cash Flow

A Debt Service Coverage Ratio (DSCR) loan is the workhorse for long-term buy-and-hold investors. Unlike conventional loans that scrutinize your personal income and debt-to-income (DTI) ratio, a DSCR loan qualifies based on the subject property's income-generating potential. The lender's primary concern is whether the property's monthly rent can "cover" the monthly mortgage payment.

Best for: Long-term (30-year) financing of stabilized, rent-ready properties, from single-family homes to 4-unit multifamily buildings.

How it Works: The lender calculates the DSCR by dividing the property's Monthly Rental Income by the proposed total debt service (Principal, Interest, Taxes, Insurance, and any HOA fees). Most lenders, including OfferMarket, require a DSCR of 1.2 or greater, which indicates the property generates 20% more income than is needed to pay the mortgage and expenses.

Key Requirements:

- Minimum Credit Score: Typically 680 or higher.

- Down Payment: Usually 20-25% of the purchase price. A larger down payment can result in a better interest rate.

- Entity Vesting: DSCR loans allow and often encourage you to purchase the property in the name of an LLC or corporation. This is a critical feature for serious investors looking to protect their personal assets and build a scalable business, a benefit not typically offered by conventional Fannie Mae loans.

Fix and Flip Loans: Short-Term Renovation Financing

Fix and flip loans, often referred to as hard money or bridge loans, are short-term financing instruments designed for acquiring and renovating a property with the intent to sell it for a profit. Speed and leverage are the key features of this loan type.

Best for: Acquiring, renovating, and reselling properties within a short timeframe (typically 6-18 months).

How it Works: These are asset-based loans, meaning the lender is more focused on the property's After-Repair Value (ARV) than the borrower's personal income. The loan is structured to cover both the acquisition and the renovation costs. For example, a lender might finance 90% of the purchase price and 100% of the planned rehab budget, up to a maximum of 75% of the ARV.

Key Requirements:

Investor Experience: Leverage is heavily dependent on the investor's verified track record. A first-time flipper will receive lower leverage than a seasoned pro with 10+ successful flips.

Detailed Scope of Work: A credible and detailed budget and renovation plan is required for the lender to approve the rehab portion of the loan.

Interest-Only Payments: The loan term is typically 12 months and features interest-only payments, which keeps the monthly holding costs low while the property is being renovated and is not generating income.

Ground Up Construction Loans: Building New Properties

For investors looking to build a property from scratch, a ground up construction loan provides the necessary capital. These are among the most complex and highest-risk loans for a lender, and therefore have the strictest underwriting requirements.

Best for: Experienced developers and builders pursuing build-to-rent or build-to-sell investment strategies.

How it Works: The loan is disbursed in stages or "draws" as construction milestones are completed. The loan amount is based on the total project cost (land acquisition + hard and soft construction costs) or the completed property's appraised value. The lender will require detailed architectural plans, a line-item budget, and permits before closing.

Key Requirements:

Significant Investor Experience: Lenders will need to see a portfolio of successfully completed past construction projects. This is not a loan for beginners.

Strong Financials: The borrower must have significant liquidity (cash reserves) to cover potential cost overruns and carrying costs.

Qualified General Contractor: The builder or general contractor on the project must be vetted and approved by the lender.

Slow Flip Loans: For Medium-Term Projects

The slow flip loan is an innovative hybrid product that fills the gap between a short-term, 12-month fix and flip loan and a long-term, 30-year rental loan. It's designed for projects that need more time.

Best for: Renovations that may exceed 12 months due to their scale, permitting delays, or market timing. It's also great for smaller projects (up to $50,000 in rehab) where the investor wants to avoid the pressure of a looming hard money deadline.

How it Works: It offers a flexible 5-year term, giving the investor ample time to complete the rehab, season the property with a tenant if desired, and then sell or refinance at the optimal moment. It features a step-down prepayment penalty (e.g., 3% in year one, 2% in year two, 1% in year three), providing more exit flexibility than a traditional 30-year loan.

Key Requirements:

High Minimum Credit Score: Due to the flexible nature of the loan, lenders often require a higher FICO score, typically 720+.

Strong Liquidity: The borrower must demonstrate strong cash reserves to qualify.

Home Equity Loans: Tapping Into Existing Equity

A rental property home equity loan is a second-position mortgage that allows you to borrow against the equity you've built in an existing rental property. It's a powerful tool for accessing capital without disrupting the favorable interest rate you may have on your primary mortgage.

Best for: Accessing capital from your portfolio to use as a down payment on a new acquisition, fund renovations on another property, or for any other business purpose.

How it Works: The lender determines the maximum loan amount based on the property's current value and the balance of the existing first mortgage. The Combined Loan-to-Value (CLTV) is typically capped at 80%. For example, if your rental is worth $500,000 and you have a $300,000 first mortgage, you have $200,000 in equity. A lender might allow you to borrow up to an 80% CLTV, or $400,000 total. This would allow for a home equity loan of up to $100,000 ($400,000 - $300,000).

Key Requirements:

Sufficient Equity: You must have a significant amount of equity in the property.

Property Type Restrictions: These loans are typically ineligible for properties used as short-term rentals (like Airbnb) or for condominiums in some cases.

No Cash Reserves Required: A unique benefit is that these loans often do not require the borrower to have post-closing cash reserves, making it easier to qualify.

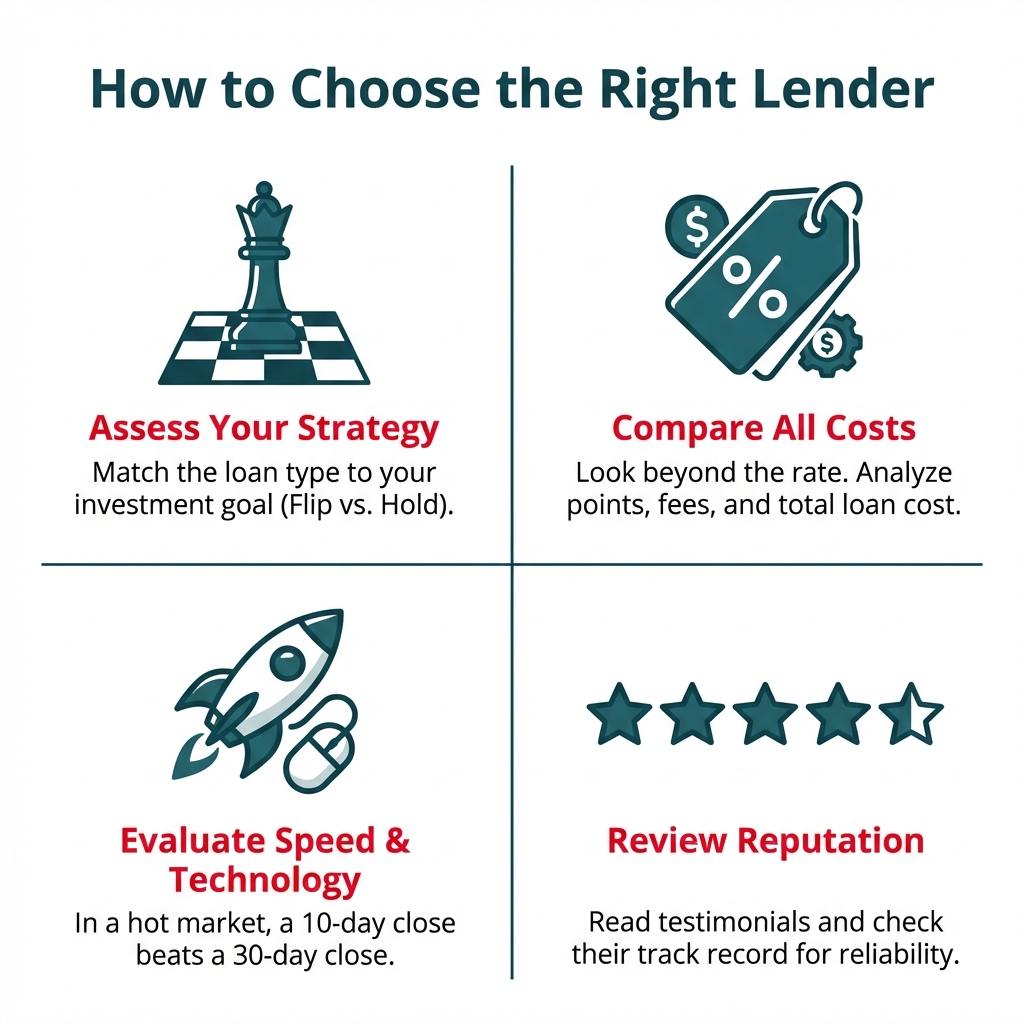

How to Choose the Right Rental Property Lender

Selecting the right lender is a strategic decision that impacts your profitability and ability to scale. Beyond the interest rate, consider these four critical factors to find a true financial partner.

Assess Your Investment Strategy and Required Loan Type

Your investment strategy is the single most important factor. Are you a BRRRR investor? A fix and flipper? A buy-and-hold landlord focused on turnkey properties? Each strategy demands a different type of financing. A lender like Visio Lending is perfect for a turnkey portfolio but useless for a flip. Conversely, a hard money lender is essential for a heavy rehab but would be a disastrously expensive choice for a 30-year hold. Choose a lender like OfferMarket that offers a full suite of products so they can grow with you as your strategy evolves.

Compare Interest Rates, Points, and Total Loan Fees

The interest rate is just one piece of the puzzle. To understand the true cost of a loan, you must compare the Annual Percentage Rate (APR), which includes other fees. Pay close attention to:

- Origination Points: One point is equal to 1% of the loan amount. A 2-point fee on a $300,000 loan is $6,000.

- Processing/Underwriting Fees: These can range from a few hundred to a few thousand dollars.

- Prepayment Penalties: Common on DSCR loans, this fee is charged if you pay off the loan within a certain period (typically 3-5 years). Understand the terms of the penalty (e.g., "3-2-1" step-down).

Always ask for a detailed loan estimate or term sheet from each lender and compare them line by line. Sometimes a loan with a slightly higher rate but lower fees can be the cheaper option overall.

Evaluate the Lender's Technology and Funding Speed

In today's competitive real estate market, speed is a weapon. The ability to close a deal in 14 days versus 45 days can be the difference between winning a contract and losing it. Lenders who have invested in technology have a massive advantage. Look for:

A Fully Online Portal: Can you apply, upload documents, and track your loan status 24/7?

Digital Solutions: Do they offer desktop appraisals to save time and money? Can you manage construction draws through a mobile app?

A Proven Closing Timeline: Ask for their average time from application to funding. A lender who can consistently close in under 21 days, like OfferMarket, gives you a significant edge.

Review Client Testimonials and Customer Support Reputation

A loan is a long-term relationship. When a problem arises—and in real estate, they always do—you want a lender who will pick up the phone and help you solve it. Don't underestimate the value of great customer support.

Read Online Reviews: Check Google, BiggerPockets, and other third-party sites. Look for patterns in the feedback. Are they praised for communication and problem-solving? Or are there complaints about delays and unreturned calls?

Assess Responsiveness: During your initial inquiry, how quickly and thoroughly do they respond? This is often a good indicator of the service you'll receive once you're a client. A lender with a dedicated loan officer model ensures you have a single point of contact who understands your goals.

Analyze Your Next Deal: Use a DSCR Calculator

The most critical metric for a rental property is its Debt Service Coverage Ratio (DSCR). This simple calculation is the first thing a lender will look at to determine if your property has enough cash flow to be a safe investment for them.

A DSCR greater than 1.0 means the property generates more income than it costs to own, resulting in positive cash flow. A DSCR below 1.0 means you would be losing money each month—a situation no lender will approve. Most lenders require a DSCR of at least 1.20 to 1.25 to provide a buffer against unexpected vacancies or repairs.

Manually calculating this can be tedious, as you need to account for gross rents, vacancy rates, property taxes, insurance, maintenance, and property management fees. Using an online tool simplifies this process immensely. A good DSCR calculator allows you to plug in your numbers and instantly see if a potential property meets the lender's requirements. This empowers you to:

- Quickly analyze multiple properties and discard the ones that don't cash flow.

- Negotiate with sellers from a position of strength, armed with hard data.

- Submit loan applications with confidence, knowing your deal is solid.

Get Your Instant Rental Loan Quote from OfferMarket

Navigating the world of rental property lenders can be complex, but the right partner makes all the difference. OfferMarket was built to be that partner for serious real estate investors. We combine the speed and efficiency of a modern tech company with the dedicated, expert support you need to confidently grow your portfolio.

With a full suite of investor-focused loan products, from DSCR and fix and flip to ground up construction, we can finance your deals at every stage of your investment journey. Our streamlined online process and innovative features like desktop appraisals mean you close faster—in as little as 10-21 days—giving you the competitive edge you need.

Don't guess what your financing options are. Take the next step and see your specific rates and terms in minutes.

Get Your Instant Quote Today and experience the future of rental property lending.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull