*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Loans for Flipping Houses: The Complete Lifecycle from Acquisition to Exit

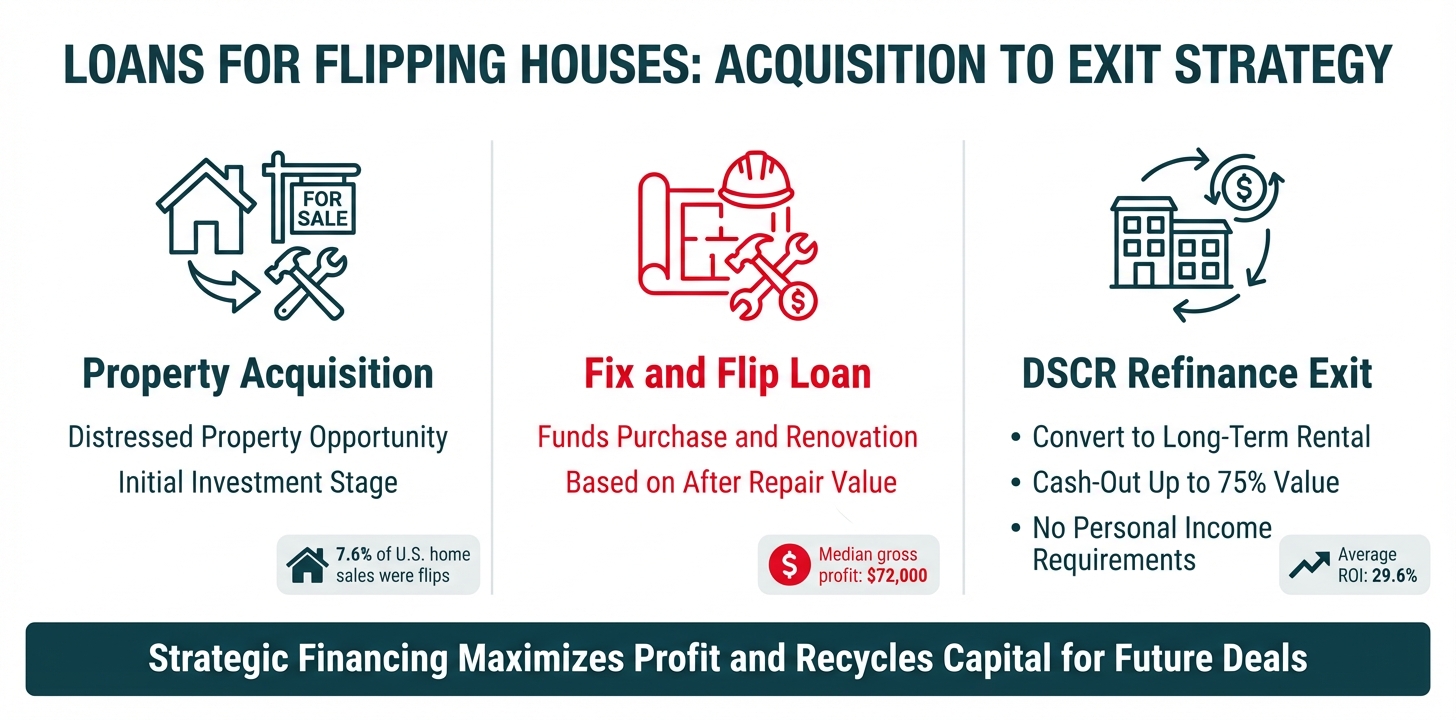

House flipping remains a proven wealth-building strategy for real estate investors, even as market dynamics continue to evolve. In 2025, home flips represented 7.6% of all U.S. home sales, with investors achieving a median gross profit of $72,000 per flip—translating to an average return of 29.6% on investment. However, flipping activity declined 7.7% compared to the prior year, highlighting the importance of strategic financing and careful exit planning in today's market.

Successful house flipping requires more than just finding the right property—it demands a comprehensive understanding of the complete loan lifecycle. From the moment you identify a distressed property to the day you either sell it for profit or refinance it into a long-term rental, your financing strategy will directly impact your returns. This is where understanding the interplay between Fix and Flip loans and DSCR refinance loans becomes critical.

The Entry Point: Fix and Flip Loans

Fix and Flip loans, also known as hard money loans, serve as your entry vehicle into a flipping project. These short-term financing solutions are specifically designed to fund both the acquisition of an investment property and its complete renovation. Unlike traditional mortgages that focus on your personal income and the property's current condition, Fix and Flip loans are underwritten based on the property's After Repair Value (ARV)—what the property will be worth after you complete the renovations.

This asset-based approach allows you to secure financing for properties that traditional banks would immediately reject. That distressed property with outdated systems, structural issues, or cosmetic damage? A Fix and Flip loan can fund not only the purchase but also the entire renovation budget needed to transform it into a market-ready asset.

The typical structure of a Fix and Flip loan includes:

- Short-term duration: Usually 12 to 24 months, giving you time to complete renovations and execute your exit strategy

- Interest-only payments: Minimizing monthly carrying costs during the renovation period

- High leverage: Financing up to 90% of the purchase price and 100% of renovation costs

- Rapid closing: Often funding within 10-21 days, allowing you to compete with cash buyers

- Rehab draw process: Disbursing construction funds in stages as work is completed

The Exit Point: DSCR Refinance Loans

While many investors plan to sell their flipped properties immediately after renovation, sophisticated investors understand the power of having a secondary exit strategy: the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). This is where DSCR (Debt Service Coverage Ratio) refinance loans come into play.

A DSCR loan is a long-term financing product designed specifically for rental properties. Unlike conventional mortgages that qualify you based on your personal W-2 income and debt-to-income ratio, DSCR loans underwrite based solely on the property's ability to generate rental income. The lender calculates whether the monthly rent covers the mortgage payment, property taxes, insurance, and other expenses—typically requiring a DSCR of 1.0 or higher (meaning the rent equals or exceeds all property expenses).

Here's why a DSCR refinance is powerful for house flippers:

- Cash-out capability: You can refinance for up to 75% of the property's current value, pulling out the equity you've created through renovation

- No seasoning requirements: With OfferMarket's DSCR loans, you don't have to wait the traditional 6-12 months of ownership before refinancing

- Long-term fixed rates: Lock in 30-year financing, converting your short-term flip into a stable rental asset

- No personal income limitations: Your ability to grow your portfolio isn't capped by your W-2 income or existing debt ratios

- Recycled capital: The cash you pull out can fund your next flip, allowing you to repeat the cycle without bringing new money to the table

Why Both Strategies Matter From Day One

The critical mistake many new flippers make is focusing exclusively on the acquisition and renovation without planning their exit strategy. In today's market, where flipping activity has declined from recent peaks, having a dual exit strategy isn't just smart—it's essential for protecting your investment.

Consider this scenario: You purchase a property with a Fix and Flip loan, planning to sell it after renovation. But during your 4-month renovation period, the local market cools, inventory increases, and buyer demand softens. Properties similar to yours are sitting on the market for 60+ days instead of the 14 days you projected. Your Fix and Flip loan is approaching maturity, and you're facing extension fees or the pressure to sell at a discount.

Now imagine the same scenario, but you planned for both exits from the beginning. You ensured the property would generate sufficient rental income to qualify for a DSCR loan. You maintained your credit metrics throughout the project. When the sales market softened, you simply pivoted to Plan B: you placed a tenant, stabilized the property, and refinanced with a DSCR loan. You pulled out most of your invested capital, converted to long-term fixed-rate financing, and now own a cash-flowing rental property. Meanwhile, you have the funds to start your next flip.

This flexibility is the hallmark of sophisticated real estate investing—and it's only possible when you understand and plan for the complete loan lifecycle.

OfferMarket: Your Partner for the Complete Lifecycle

OfferMarket provides both critical financing tools you need to execute this strategy successfully:

Fix and Flip Loans: Fast, flexible hard money financing for acquisition and renovation, with competitive rates and high leverage to maximize your returns on the front end.

DSCR Refinance Loans: Long-term rental financing with no seasoning requirements, allowing you to execute the BRRRR strategy and recycle your capital immediately.

By working with a single lender who understands the complete lifecycle of your investment, you benefit from:

- Streamlined processes: Your Fix and Flip lender already knows your property when it's time to refinance

- Consistent underwriting: No surprises or conflicting requirements between loan products

- Strategic guidance: Working with lenders who understand both entry and exit strategies

- Faster execution: Reduced timeline from flip completion to cash-out refinance

The most successful house flippers don't just think about buying and renovating properties—they think in complete cycles. They understand that every acquisition decision should be made with both exit strategies in mind. They know that a property that works for a flip should also work as a rental. And they partner with lenders like OfferMarket who can support them through the entire journey, from acquisition through exit and on to the next deal.

In the sections that follow, we'll dive deep into each component of this lifecycle: how to get funded with OfferMarket, the mechanics of Fix and Flip loans, the strategic considerations for both exit paths, the power of DSCR refinancing, and how to optimize every aspect of your financing to maximize profitability. Whether you're planning your first flip or your fiftieth, understanding this complete lifecycle is the foundation of sustainable, scalable success in real estate investing.

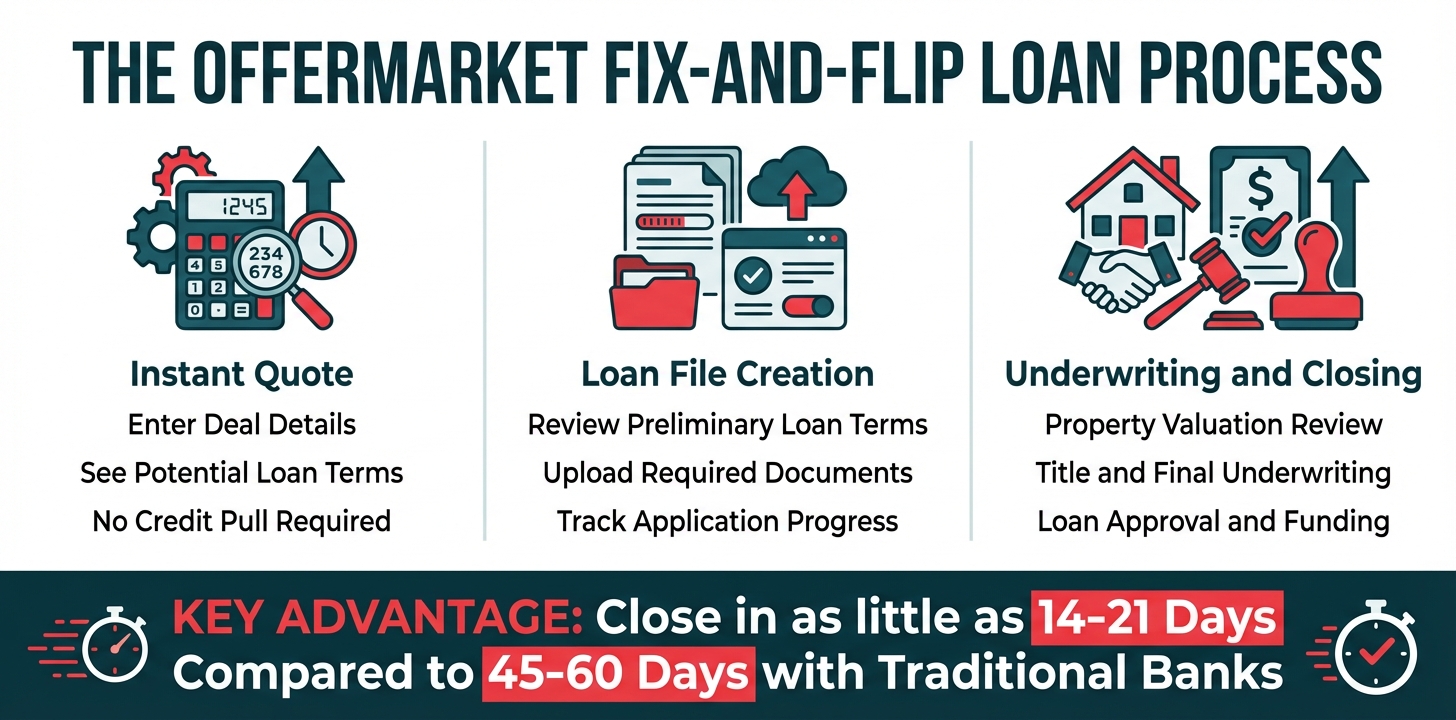

Getting Your Flip Project Funded: The OfferMarket Loan Process

Starting your house flipping journey with OfferMarket is designed to be straightforward, transparent, and remarkably fast. Unlike traditional banks that can take 45-60 days to close a loan, OfferMarket's streamlined process allows investors to move from initial quote to funded deal in a fraction of that time. This speed advantage can mean the difference between securing a competitive property and watching it slip away to another buyer. Let's walk through each step of the process so you know exactly what to expect.

Step 1: Get an Instant Quote to See Your Potential Terms

Your journey begins with OfferMarket's instant quote tool—a powerful starting point that provides immediate clarity on your financing options. By entering basic information about your proposed flip project, including the purchase price, estimated renovation costs, and after-repair value (ARV), you'll receive a preliminary quote showing your potential loan amount, interest rate, and key terms.

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

This instant quote serves multiple purposes. First, it gives you immediate feedback on whether your project falls within OfferMarket's lending parameters. Second, it provides the critical numbers you need to evaluate whether the deal makes financial sense before you invest time in a full application. Third, it establishes realistic expectations about your leverage—typically expressed as Loan-to-Cost (LTC) and After-Repair Loan-to-Value (ARLTV) ratios—so you can accurately calculate your required capital contribution.

The instant quote process requires no commitment and no credit pull at this stage. You're simply gathering information to make an informed decision. This transparency empowers you to move quickly when you find the right property, knowing you have a clear picture of your financing capacity.

Step 2: Create Your Loan File – Detailing Your Project

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Here's why this matters for your bottom line. Traditional lenders often surprise you with hidden fees at closing. We take a different approach—laying out all costs upfront so you can review every line item, understand exactly what you're paying for, and calculate your true all-in costs before committing.

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

Step 3-7: Move to Processing & Expedite with Document Uploads

After reviewing the preliminary Loan Terms in your Loan File, you are prepared to initiate the formal underwriting stage. To signal your intent to proceed, simply click "Move to processing" within your account. This milestone notifies the OfferMarket team that you are ready to move forward and are prepared to submit your supporting documentation.

The Document Upload Phase:

Once initiated, navigate to the "Processing" area of your Loan File. There, you will find a prioritized checklist of the specific items required to move your file toward approval.

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket provides specialized insurance solutions for Fix and Flip properties if you need assistance)

OfferMarket's Speed Promise: Closing in 1-3 Weeks

Speed is where OfferMarket maintains a distinct advantage over traditional financing. While standard banks often take 30 to 60 days—and even some private lenders linger for several weeks—we aim to reach the closing table in as little as 1 to 3 weeks. Most of our investors secure funding within 14 to 21 days from the initial application.

This efficiency is more than just a convenience; it is a competitive lever. In a crowded market, your capacity to close rapidly can win the contract even against higher bids. Sellers prioritize certainty; a guaranteed two-week close backed by verified financing consistently outperforms a 45-day conventional loan.

Your Role in Expediting the Process:

To maintain this accelerated pace, OfferMarket relies on the immediate submission of all required materials. Here is a breakdown of the typical transition from application to funding:

- Days 1-3: Document evaluation and preliminary underwriting

- Days 4-7: Property valuation, title search, and final underwriting review

- Days 8-14: Loan approval and preparation of closing packages

- Days 14-19: Final closing and disbursement of funds

This schedule remains accurate when complete and precise documentation is provided immediately upon moving to the processing stage. Any delay in submission adds a corresponding delay to your closing date. Furthermore, incomplete files require the underwriting team to request clarifications, which can extend the timeline further.

Pro Tips for Fast Processing:

- Submit a complete package: Rather than uploading piecemeal, collect every item on your checklist and submit the full file at once.

- Prioritize legibility: Ensure all scanned documents are clear, high-resolution, and include every page of the original document.

- Be highly responsive: If the processing team requests a follow-up, aim to reply within hours rather than days.

- Maintain availability: Stay reachable via phone and email during standard business hours for quick administrative questions.

- Brief your contractor: Ensure your contractor is ready to provide any necessary details regarding the scope of work without delay.

The gap between a 10-day and a 20-day closing is usually determined by the borrower’s responsiveness. Investors who treat the documentation phase with a sense of urgency consistently outpace the competition and begin generating ROI sooner.

By following OfferMarket’s streamlined seven-step system and maintaining open communication, you can capitalize on profitable deals with maximum efficiency. Our platform is built to match your speed—the faster you provide the essentials, the sooner you get funded.

What to Expect from Underwriting Through Closing

Once your application is submitted with complete documentation, OfferMarket's underwriting team moves quickly to evaluate your deal. According to industry data, while conventional lenders take 45-60 days for loan approval, specialized hard money lenders can close in 14-21 days. OfferMarket targets the faster end of this spectrum, with many loans closing in as little as 14-19 days from complete application to funding.

During underwriting, the team evaluates three primary factors: the property's current value and condition, the credibility of your ARV estimate, and your ability to execute the renovation successfully. They may order a broker price opinion (BPO) or appraisal to validate values. They'll review your scope of work to ensure the renovation budget is adequate and realistic. And they'll assess your experience and financial capacity to complete the project.

You may receive questions or requests for additional information during this phase. Responding promptly keeps your timeline on track. The underwriting team is working to get to "yes" while ensuring the loan is structured appropriately for the risk profile of your specific project.

Once underwriting approval is granted, you'll receive a formal loan commitment letter outlining all terms and conditions. Review this carefully to ensure it matches your expectations from the initial quote. Any discrepancies should be addressed immediately.

The closing process itself is streamlined through a title company or attorney, depending on your state's requirements. You'll review and sign loan documents, provide your down payment funds (typically wired to the title company), and receive confirmation of recording. At this point, the acquisition funds are released to purchase the property, and you officially own your flip project.

Speed and Efficiency: Your Competitive Advantage

The speed of OfferMarket's process isn't just about convenience—it's a genuine competitive advantage in the real estate investing marketplace. When you're competing for a property against other buyers, the ability to close in 14-21 days versus the 30-60 days required by traditional banks can be the deciding factor that convinces a seller to accept your offer.

Many distressed property sellers are motivated by their own timeline pressures. They may be facing foreclosure, dealing with an inherited property they want to liquidate quickly, or simply eager to move on from a property that's become a burden. Your ability to close quickly with certainty makes your offer more attractive, even if it's not the absolute highest price.

This speed advantage extends beyond just winning deals. It also means you can start your renovation sooner, get the property back on the market faster, and realize your profit more quickly. In real estate investing, time literally is money—every month a property sits in your inventory is another month of holding costs eating into your returns.

OfferMarket's efficiency also reduces the stress and uncertainty that can plague real estate transactions. With clear communication, defined timelines, and a streamlined process, you spend less time worrying about whether your financing will come through and more time focusing on what you do best: finding great deals and executing profitable renovations.

The combination of speed, transparency, and reliability makes OfferMarket an ideal lending partner for serious house flippers who understand that the right financing structure is just as important as finding the right property. With your funding secured efficiently, you can focus your energy on the renovation work and exit strategy that will determine your ultimate success.

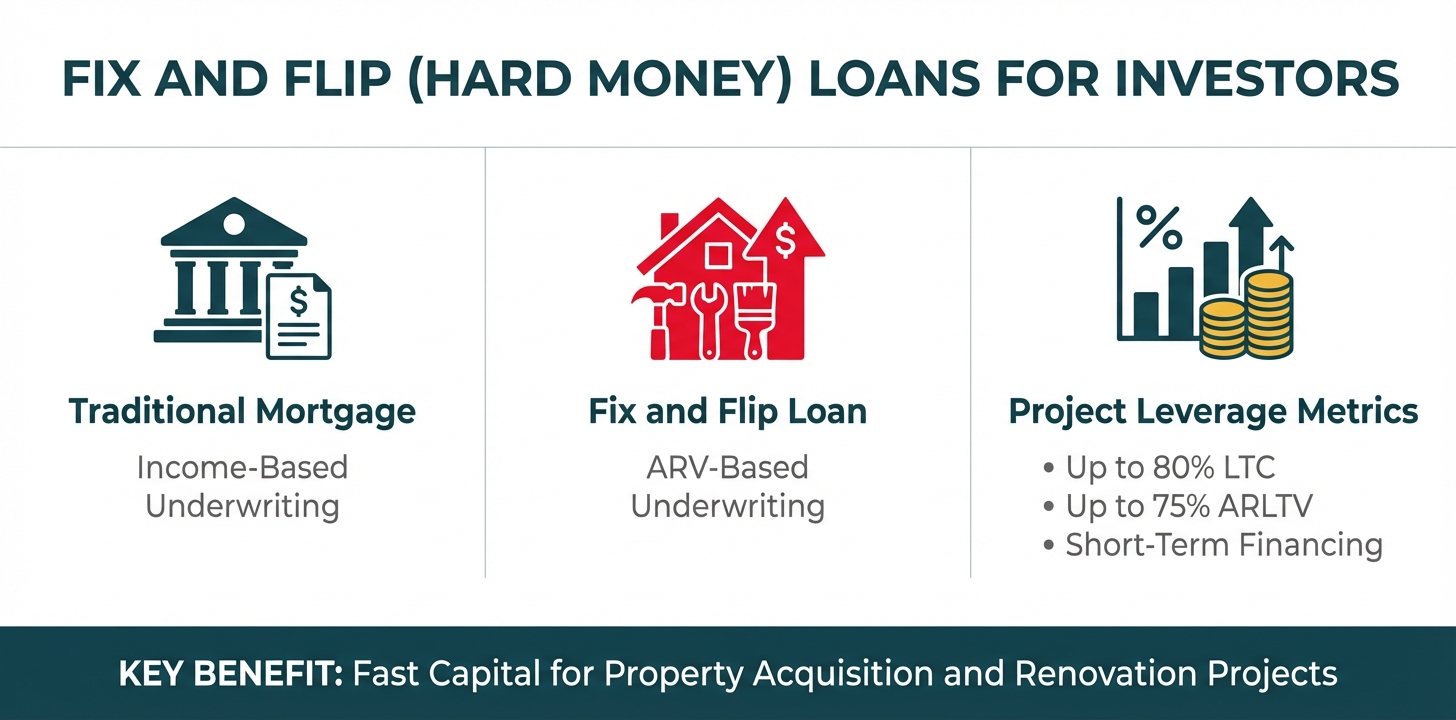

The Workhorse of Your Flip: A Deep Dive into Fix and Flip (Hard Money) Loans

Fix and flip loans, commonly known as hard money loans, serve as the financial engine that powers real estate investors' property transformation projects. Unlike traditional mortgage products designed for homeowners, these specialized financing tools are purpose-built for one specific mission: acquiring distressed or undervalued properties and funding the renovations needed to maximize their market value.

What Makes Fix and Flip Loans Different

The fundamental distinction of fix and flip financing lies in what lenders actually evaluate when making their lending decision. Traditional banks focus heavily on your personal financial profile—your W-2 income, tax returns, debt-to-income ratio, and employment history. Fix and flip lenders take a radically different approach: they underwrite the property's potential, not your paycheck.

The centerpiece of this underwriting philosophy is the After Repair Value (ARV)—the estimated market value of the property once all renovations are complete. Lenders analyze comparable sales in the area, review your renovation plans, and assess whether the finished product will command a price that ensures profitability for both you and them. This forward-looking evaluation allows investors to secure financing based on what the property will be worth, rather than what it's worth today in its distressed state.

Project profitability takes center stage in the approval process. Lenders want to see a clear path to profit that accounts for acquisition costs, renovation expenses, carrying costs, and a healthy margin for unexpected issues. Your experience as an investor matters—lenders prefer borrowers with a proven track record of successful flips—but the deal itself must stand on its own merits.

The Structure: Built for Speed and Flexibility

Fix and flip loans are designed as short-term financing instruments, typically structured with terms ranging from 12 to 24 months. This timeframe aligns perfectly with the typical house flipping cycle: acquire the property, complete renovations, and exit through either a sale or refinance.

The payment structure reflects the unique cash flow dynamics of flipping houses. Most fix and flip loans feature interest-only monthly payments during the loan term, with the entire principal balance due as a balloon payment at maturity. This structure serves two critical purposes:

First, it minimizes your monthly carrying costs during the renovation period when the property generates no income. Instead of making principal and interest payments that could total thousands of dollars monthly, you're only covering the interest expense, freeing up capital for renovation work and unexpected costs.

Second, it acknowledges the reality of how flips are monetized. You don't gradually pay down the loan over time like a traditional mortgage—you pay it off in full when you sell the property or refinance into long-term financing. The balloon payment structure aligns the loan's repayment with your actual exit strategy.

Leverage: Maximizing Your Capital Efficiency

One of the most powerful features of fix and flip loans is the high leverage they offer through two key metrics: Loan-to-Cost (LTC) and After-Repair Loan-to-Value (ARLTV).

Loan-to-Cost (LTC) measures how much of your total project cost the lender will finance. Typical hard money loans for fix and flip properties offer LTC allowances up to 80%, meaning if your total project costs $200,000 (including purchase price and renovation budget), the lender might provide $160,000, requiring you to bring just $40,000 to the table.

The LTC calculation is straightforward:

LTC Ratio = (Loan Amount / Total Project Cost) × 100

Where Total Project Cost = Purchase Price + Renovation Budget + Closing Costs

After-Repair Loan-to-Value (ARLTV) measures the loan amount as a percentage of the property's projected ARV. Lenders typically cap ARLTV at 75% to ensure adequate equity cushion once the property is renovated. This metric protects both you and the lender by ensuring the project has built-in equity at completion.

For example, if your property will be worth $300,000 after repairs, a 75% ARLTV would limit your loan to $225,000. However, your actual loan amount will be the lower of the LTC or ARLTV calculation, ensuring the deal makes sense from both a cost and value perspective.

This high leverage is transformative for investors. Instead of tying up $100,000 of your own capital in a single flip, you might only need $25,000-$40,000, allowing you to run multiple projects simultaneously and dramatically accelerate your business growth.

The Rehab Draw Process: Funding Your Renovation

Unlike a traditional mortgage where you receive all funds at closing, fix and flip loans disburse renovation funds through a structured draw process that protects both the investor and lender while ensuring work progresses as planned.

Here's how the typical draw process works:

Initial Disbursement: At closing, you receive funds to purchase the property and often an initial percentage of the renovation budget to begin work immediately.

Draw Schedule: Your renovation budget is divided into stages or milestones aligned with major phases of construction—demolition, framing, mechanical systems, finishes, etc. Each stage has a predetermined dollar amount allocated.

Inspection and Release: When you complete a phase of work, you request a draw by submitting documentation (photos, receipts, contractor invoices). The lender sends an inspector to verify the work is complete and meets quality standards. Once approved, the lender releases the funds for that phase.

Progressive Funding: This process repeats through each stage of renovation until the project is complete. Some lenders release 100% of each phase's budget upon approval; others hold back 10% until final completion to ensure contractors finish all punch-list items.

Final Draw: Once all work is complete and the property passes final inspection, the lender releases any remaining renovation funds and holdbacks.

This controlled disbursement process serves multiple purposes. It ensures renovation funds are actually used for their intended purpose rather than diverted elsewhere. It protects the lender's collateral by verifying work quality at each stage. And it provides you with a structured framework that keeps your project on track and properly capitalized through completion.

The draw process does require organization and documentation on your part—you'll need to maintain receipts, coordinate inspections, and plan your cash flow around draw timing. However, this discipline ultimately benefits your project by imposing accountability and ensuring you don't overextend on early phases at the expense of finishing work.

Speed: The Competitive Advantage

Perhaps the most valuable benefit of fix and flip loans is speed. While traditional bank financing can take 45-60 days (or longer) to close, hard money lenders can often fund deals in 10-21 days. This rapid closing capability provides decisive competitive advantages:

Winning in Multiple Offer Situations: When you're competing against other buyers, the ability to close quickly—often with cash or proof of funds from your lender—makes your offer significantly more attractive to sellers.

Seizing Time-Sensitive Opportunities: The best deals often require fast action. Whether it's a motivated seller who needs to close quickly, a foreclosure auction, or an off-market opportunity, speed of execution can be the difference between securing a profitable deal and watching it go to a competitor.

Minimizing Carrying Costs: Every day a property sits in contract without closing costs you money in lost opportunity. Quick closings get you into the property faster, allowing you to begin renovations sooner and ultimately exit sooner.

Flexibility for Distressed Properties: Traditional banks won't finance properties in poor condition, creating a catch-22 for investors. Fix and flip lenders specialize in exactly these situations, providing both acquisition and renovation funding in one package.

The Bottom Line

Fix and flip loans are purpose-built financial instruments designed to match the unique requirements of property flipping. By focusing on ARV and project profitability rather than personal income, offering high leverage through favorable LTC and ARLTV ratios, providing structured funding for renovations through the draw process, and delivering rapid closings that create competitive advantages, these loans serve as the essential tool that transforms real estate investing from a capital-intensive hobby into a scalable, profitable business.

Understanding how these loans work—and how to use them strategically—is the foundation for building a successful house flipping operation. With the right financing partner like OfferMarket, you can access the capital, speed, and flexibility needed to execute deals that traditional financing simply cannot support.

Planning Your Exit: The Two Paths to Profitability

Before you ever sign on the dotted line for a fix and flip loan, you need to answer one critical question: How will I get out of this deal? Your exit strategy isn't just an afterthought—it's the foundation of your entire investment thesis. The difference between a profitable flip and a costly mistake often comes down to how well you've planned your exit before you even acquire the property.

In the world of house flipping, there are two primary exit strategies that successful investors rely on: the traditional sale and the BRRRR method. Understanding both paths—and having a viable plan for either—is what separates sophisticated investors from those who get caught holding properties they can't afford to keep.

The Primary Exit: Selling for Immediate Profit

The most straightforward exit strategy is also the most common: sell the renovated property and pocket the profit. This is the classic flip model that most people envision when they think about house flipping. You purchase a distressed property, complete the renovations, list it on the market, and sell it to an end buyer—typically a homeowner who will occupy the property.

The appeal of this strategy is its simplicity and speed. Once you close on the sale, you receive your profit in a lump sum, which you can immediately reinvest into your next project. This creates a clear, linear path: acquire, renovate, sell, repeat. For investors who thrive on active deal-making and prefer to keep their capital liquid, the sale exit is often the preferred route.

However, the sale exit comes with its own set of considerations. You're entirely dependent on market conditions at the time you're ready to sell. If the market softens, buyer demand decreases, or interest rates rise significantly during your renovation period, you may face longer holding times or need to reduce your asking price to attract buyers. This is why experienced flippers always build a buffer into their profit projections—they understand that the market won't always cooperate with their timeline.

The sale exit also means you're subject to short-term capital gains taxes if you sell within a year of purchase, which can significantly impact your net profit. Despite these considerations, selling remains the most popular exit strategy because it provides immediate liquidity and allows investors to quickly move on to their next opportunity.

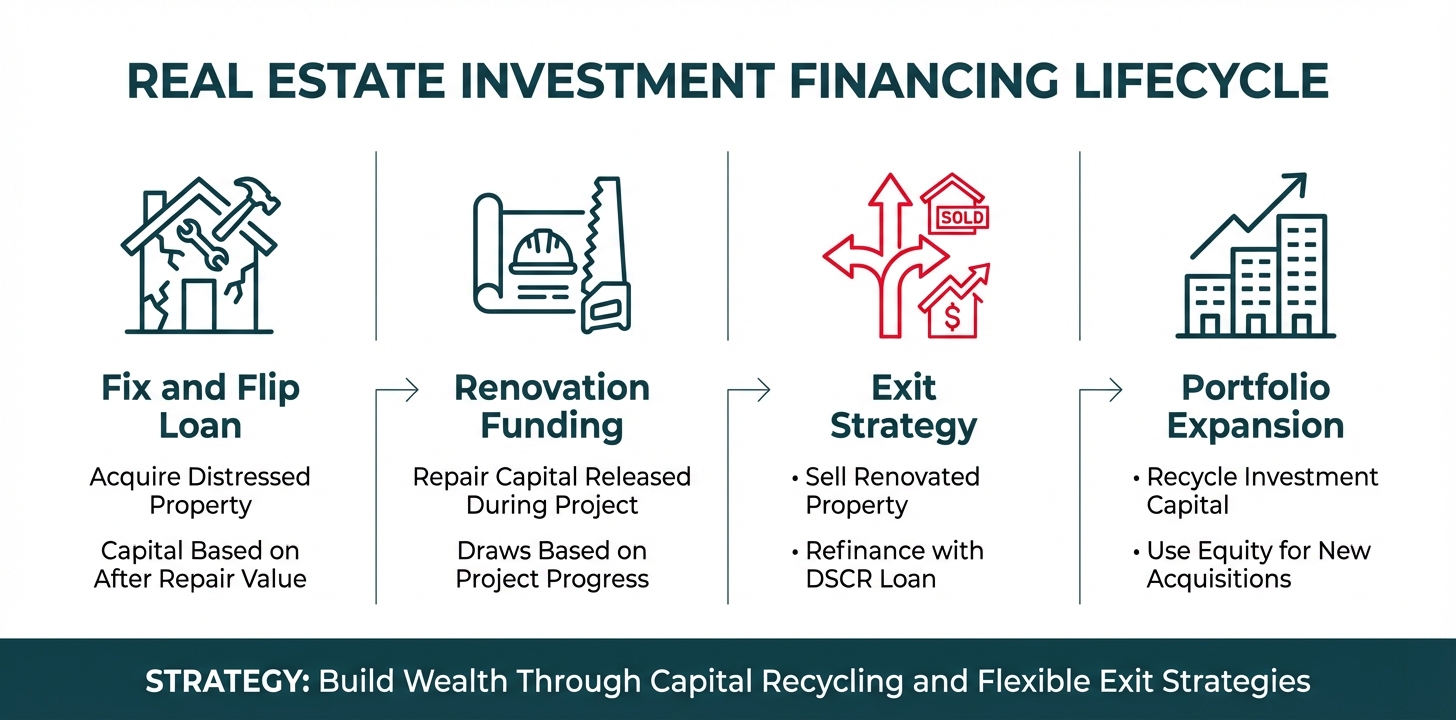

The Secondary Exit: The BRRRR Method

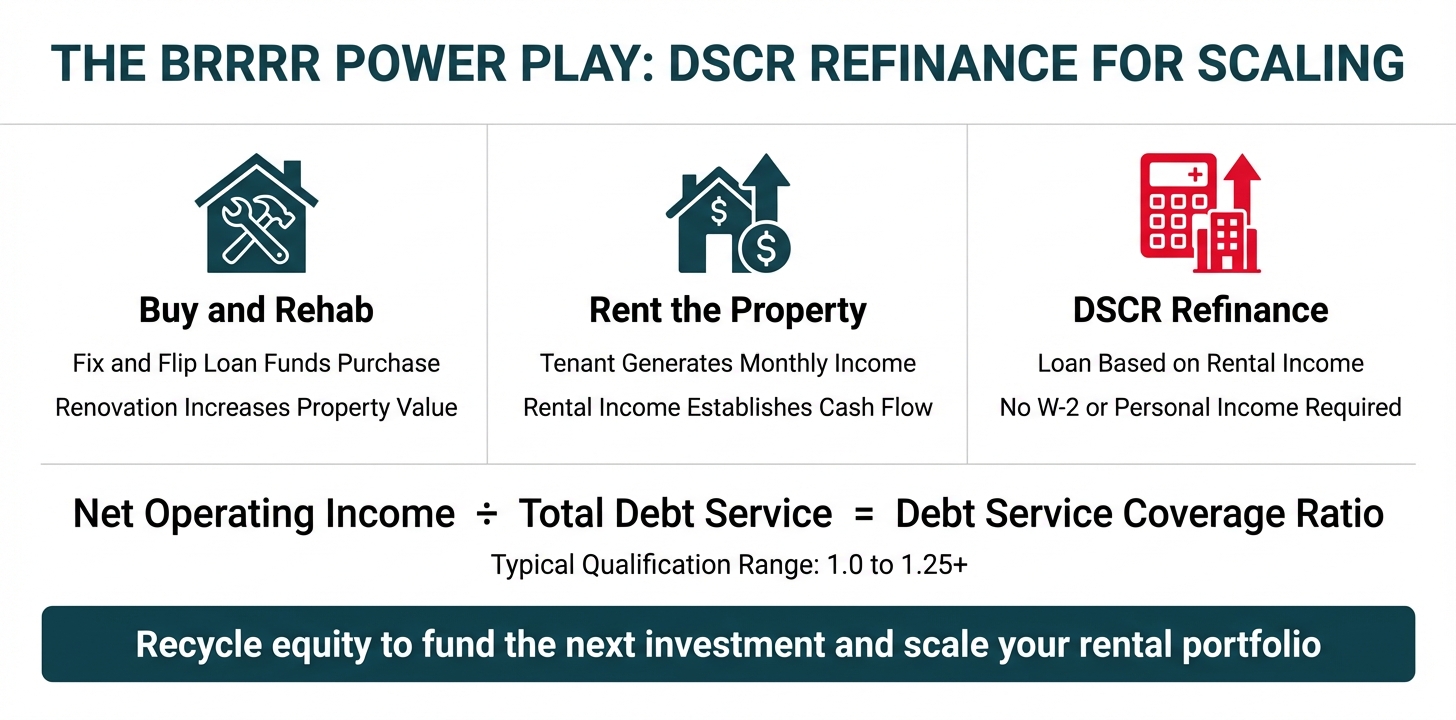

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—has gained tremendous popularity among real estate investors over the past decade, and for good reason. This strategy transforms what would be a one-time flip into a long-term wealth-building asset while still allowing you to recycle your capital into new deals.

Here's how it works: Instead of selling the property after renovation, you place a qualified tenant and hold the property as a rental. Once the property has been rented and is generating cash flow, you refinance out of your short-term fix and flip loan into a long-term rental loan—typically a DSCR (Debt Service Coverage Ratio) loan. This refinance allows you to pull out most or all of your initial investment, which you can then use as the down payment for your next flip.

The beauty of the BRRRR method is that it allows you to build a portfolio of cash-flowing rental properties while continuously recycling the same capital. Instead of paying capital gains taxes on each flip, you're building long-term wealth through appreciation and cash flow while deferring taxes indefinitely. Many investors who started as house flippers have transitioned to the BRRRR method as their primary strategy because it creates passive income alongside active flipping profits.

However, the BRRRR method requires more sophisticated planning and comes with its own risks. You need to ensure the property will generate sufficient rental income to support a long-term mortgage payment. You also need to be comfortable with the responsibilities of being a landlord—or have systems in place for property management. Most importantly, you need to ensure you can qualify for the refinance, which brings us to a critical consideration that many investors overlook.

The Critical Importance of Dual Exit Strategy Planning

Here's a truth that separates successful flippers from those who fail: you should never enter a flip with only one viable exit strategy. The market doesn't care about your plans, and conditions can change rapidly during the 6-12 months you're holding and renovating a property.

According to real estate investment experts, every exit strategy you choose can either lock in short-term profits or set you up for long-term wealth—the key is having flexibility to choose the path that makes the most sense when you're ready to exit.

This is why sophisticated investors always underwrite their deals with both exit strategies in mind. Before purchasing a property, they analyze:

For the sale exit:

- What is the realistic ARV based on comparable sales?

- What is the expected time to sell in the current market?

- What profit margin remains after accounting for holding costs and selling expenses?

- What happens to my profit if I need to reduce the price by 5-10%?

For the BRRRR exit:

- What is the realistic monthly rent based on comparable rentals?

- Does the rent support a DSCR of at least 1.0 (and preferably 1.25)?

- Can I refinance enough cash out to move on to my next project?

- What are my credit metrics, and can I qualify for the refinance?

By analyzing both scenarios before you buy, you ensure that you have a profitable path forward regardless of how market conditions evolve. If the sales market is hot when you complete renovations, you can sell for maximum profit. If the sales market has cooled but rental demand is strong, you can pivot to the BRRRR method without taking a loss.

How Market Conditions Influence Your Optimal Exit Path

The real estate market is cyclical, and understanding where we are in the cycle should heavily influence which exit strategy you pursue. Different market conditions favor different approaches, and being able to read these signals is a crucial skill for any house flipper.

In a strong seller's market:

- Home prices are rising

- Days on market are low

- Buyer demand exceeds supply

- Multiple offers are common

In these conditions, the sale exit is typically optimal. You can maximize your profit by selling quickly at top dollar, and the opportunity cost of holding the property as a rental (missing out on peak sale prices) may outweigh the long-term benefits of keeping it.

In a cooling or buyer's market:

- Home prices are flat or declining

- Days on market are increasing

- Inventory is rising

- Buyers have more negotiating power

In these conditions, the BRRRR method often becomes more attractive. Rather than selling at a discount or waiting months for a buyer, you can pivot to rental mode, lock in a long-term tenant, and refinance when the market stabilizes. You're essentially choosing to wait out the market cycle while generating cash flow rather than taking a reduced profit on a sale.

In a high interest rate environment:

- Mortgage rates are elevated

- Buyer purchasing power is reduced

- Rental demand often increases (as fewer people can afford to buy)

- DSCR loan rates may also be high but rental income helps offset this

High interest rates create a unique dynamic. While they reduce buyer demand for sales, they often increase rental demand as more people are priced out of homeownership. This can make the BRRRR method more attractive, especially if you can lock in a long-term tenant at a strong rent that supports refinancing.

The key insight is this: market conditions will change during your project, and you need the flexibility to adapt. The investors who succeed long-term are those who can pivot between strategies based on what the market is telling them, rather than being locked into a single approach regardless of conditions.

The Bottom Line: Flexibility is Profitability

The most successful house flippers aren't the ones who are married to a single exit strategy—they're the ones who maintain maximum flexibility and can adapt to market conditions in real-time. Before you acquire any property, you should be able to confidently answer these questions:

- Can I sell this property for a profit in the current market?

- Can I rent this property and refinance if the sales market softens?

- Do I have the credit metrics to qualify for a refinance if needed?

- What is my break-even point for each exit strategy?

By planning both exit strategies from day one and maintaining the credit health to execute either path, you're not just hoping for success—you're engineering it. You're giving yourself the flexibility to maximize profits in any market condition, which is ultimately what separates consistently profitable investors from those who struggle when conditions change.

In the next section, we'll dive deep into how the BRRRR method works in practice, exploring how DSCR loans enable you to refinance and scale your portfolio without the traditional income limitations that hold many investors back.

The BRRRR Power Play: Using DSCR Loans to Refinance and Scale

Once you've successfully renovated your flip property, the DSCR (Debt Service Coverage Ratio) loan becomes your gateway to sustained portfolio growth. Unlike traditional mortgages that scrutinize your W-2 income and tax returns, DSCR loans shift the underwriting focus entirely to the property's ability to generate cash flow. This fundamental difference transforms how real estate investors can scale their portfolios.

Understanding DSCR: Property Performance Over Personal Income

A DSCR loan is a long-term financing tool designed specifically for rental properties. The lender calculates the Debt Service Coverage Ratio by dividing the property's monthly rental income by its monthly debt obligations (principal, interest, taxes, insurance, and HOA fees). A DSCR of 1.0 means the property generates exactly enough income to cover its expenses. Most lenders require a minimum DSCR of 1.0 to 1.25, depending on the loan program and property type.

What makes DSCR loans revolutionary for investors is what they don't require: your personal income documentation. No W-2s, no tax returns, no pay stubs. The property itself qualifies for the loan based on its rental performance. This means a property generating $3,000 per month in rent can secure financing regardless of whether you're a full-time investor with no traditional employment or a high-earning professional with multiple properties already on your personal credit report.

The No-Seasoning Advantage: Immediate Access to Your Equity

Traditional refinancing typically requires "seasoning"—a waiting period of 6 to 12 months of ownership before you can access your equity through a cash-out refinance. This delay can significantly hamper your ability to move quickly on new opportunities. However, select DSCR lenders, including OfferMarket, offer no-seasoning or low-seasoning cash-out refinance options that allow you to tap into your newly created equity immediately after completing renovations.

No-seasoning DSCR loans enable investors to refinance based on the current appraised value of the renovated property, not the original purchase price. This means you can access the equity you've created through strategic improvements without waiting months to do so. For active investors flipping multiple properties, this acceleration can mean the difference between completing two deals per year versus six or more.

With unlimited cash-out and no seasoning requirements, you can extract the capital you need to fund your next acquisition while maintaining ownership of a cash-flowing rental property. This approach preserves your investment portfolio while simultaneously providing the liquidity to continue growing it.

Breaking Free from the DTI Ceiling

Perhaps the most powerful advantage of DSCR loans is how they eliminate the personal Debt-to-Income ratio as a limiting factor in your investment journey. Traditional mortgages count against your DTI, which typically caps at 43-50% for most borrowers. If you have a $10,000 monthly income, you might only qualify for $4,300-$5,000 in total monthly debt obligations across all your mortgages, credit cards, and other loans.

This DTI ceiling creates a hard stop for portfolio growth. After acquiring 4-10 properties (depending on your income and existing debts), you simply can't qualify for additional traditional financing, even if every property in your portfolio is profitable and cash-flowing positively.

DSCR loans shatter this ceiling. Because the property's rental income qualifies the loan—not your personal income—each new property is evaluated independently. A property with strong cash flow can secure financing regardless of how many other properties you own or what your personal income statement looks like. This structure enables truly unlimited portfolio growth, constrained only by your ability to find profitable deals and manage your properties effectively.

The BRRRR Cycle in Action: A Real-World Example

Let's walk through a complete BRRRR cycle using OfferMarket's loan products to illustrate how DSCR refinancing enables repeatable wealth building:

Step 1: Buy with a Fix and Flip Loan

You identify a distressed property listed at $180,000 in a neighborhood where renovated homes rent for $2,400/month and sell for $280,000. You secure a fix and flip loan from OfferMarket with these terms:

- Purchase price: $180,000

- Renovation budget: $50,000

- Total project cost: $230,000

- Loan amount at 90% LTC: $207,000

- Your cash investment: $23,000 (down payment and closing costs)

Step 2: Rehab the Property

Over the next 90 days, you complete a comprehensive renovation: new kitchen and bathrooms, updated flooring, fresh paint, new HVAC system, and landscaping improvements. You draw funds from your construction budget as work progresses, paying only interest on the disbursed amounts.

Step 3: Rent the Property

Instead of immediately selling, you place a quality tenant at $2,400/month. The property now generates consistent rental income and has an appraised value of $280,000 based on comparable sales in the area.

Step 4: Refinance with a DSCR Loan

After placing your tenant, you immediately apply for a DSCR cash-out refinance with OfferMarket (no seasoning required). Here's how the numbers work:

- Appraised value: $280,000

- DSCR loan at 80% LTV: $224,000

- Monthly rent: $2,400

- Estimated monthly PITIA: $1,900 (principal, interest, taxes, insurance, association)

- DSCR: 1.26 ($2,400 ÷ $1,900) ✓ Qualifies

From the $224,000 refinance proceeds, you pay off the original fix and flip loan balance of approximately $210,000 (including accrued interest). After closing costs of roughly $5,000, you receive approximately $9,000 in cash back to your bank account.

Step 5: Repeat with Amplified Capital Now you own a cash-flowing rental property worth $280,000 with a $224,000 loan, giving you $56,000 in equity. You've also recovered your initial $23,000 investment plus an additional $9,000, giving you $32,000 in liquid capital—more than you started with. Your property generates approximately $500/month in positive cash flow after all expenses.

With your $32,000 in hand, you're ready to acquire your next flip property. But this time, you also have a rental property building equity and generating monthly income. After completing your second BRRRR cycle, you'll have two rental properties and even more capital to deploy. By the third cycle, you might have $50,000-$60,000 to invest, allowing you to tackle larger projects or multiple properties simultaneously.

This compounding effect is the true power of the BRRRR strategy combined with no-seasoning DSCR refinancing. Each cycle not only adds a cash-flowing asset to your portfolio but also increases your available capital for the next deal. Within 2-3 years, investors using this method can build portfolios of 10-20 properties while maintaining substantial liquidity for ongoing opportunities.

The key to making this cycle work is maintaining the discipline to refinance into sustainable, long-term financing rather than over-leveraging or extracting too much equity. The DSCR loan serves as both your exit from the short-term hard money loan and your entry into long-term wealth building through rental income and appreciation.

Unlocking Hidden Capital: Leveraging HELOANs for Your Next Down Payment

For real estate investors with existing rental properties in their portfolio, one of the most powerful yet underutilized financing tools is the Investment HELOAN—a home equity loan structured as a second-lien loan against properties you already own. Unlike a traditional refinance that replaces your existing mortgage, a HELOAN sits behind your first mortgage as a subordinate lien, allowing you to tap into your property's accumulated equity without disturbing your current financing structure.

This distinction becomes critically important in today's fluctuating interest rate environment. Imagine you purchased a rental property three years ago and secured a first mortgage at 3.5%. That property has since appreciated significantly, and you've paid down the principal, creating substantial equity. If you wanted to access that equity through a traditional cash-out refinance, you'd be forced to replace your low-rate first mortgage with a new loan at today's higher rates—potentially 7% or more. The increased interest expense on your entire loan balance would dramatically impact your property's cash flow and overall profitability.

A HELOAN solves this problem elegantly. By taking a second-lien position, you can extract the equity you need while preserving that favorable first mortgage rate. You only pay the higher current rates on the additional amount you're borrowing, not on your entire loan balance. This makes HELOANs particularly attractive for investors who locked in historically low rates during 2020-2021 and now need capital for their next acquisition but don't want to sacrifice their existing financing advantage.

The Strategic Use Cases for Investment HELOANs

The most common and strategic use of an Investment HELOAN is to generate liquid capital for your next property acquisition. Real estate investors often find themselves in a catch-22 situation: their wealth is growing through property appreciation and equity buildup, but that wealth is trapped in illiquid real estate. They see compelling new investment opportunities but lack the readily available cash for down payments.

According to Bankrate, home equity loans on investment properties can provide the capital needed to expand your portfolio without liquidating existing assets. A HELOAN converts that paper wealth into spendable capital, providing the down payment for your next fix and flip project or rental acquisition. This allows you to scale your portfolio without selling performing assets or waiting years to accumulate cash through rental income alone.

Beyond acquisition financing, Investment HELOANs serve multiple strategic purposes in a sophisticated investor's toolkit:

Capital for Major Renovations: If you have a rental property that needs significant updates to command higher rents or improve its market value, a HELOAN on another property in your portfolio can fund those improvements without disrupting the subject property's existing financing.

Bridge Financing for Time-Sensitive Opportunities: Real estate deals often require quick action. A pre-approved HELOAN gives you ready access to capital, allowing you to move decisively when an exceptional opportunity arises, even if you're between property sales or waiting for another financing source to close.

Portfolio Rebalancing: Investors sometimes need to shift capital between properties—perhaps paying down a higher-interest loan on one property using equity from another, or consolidating debt to improve overall portfolio cash flow.

Emergency Reserves: Experienced investors know that unexpected expenses are inevitable. A HELOAN can serve as a financial safety net, providing access to capital for major repairs, periods of vacancy, or other unforeseen circumstances without forcing a distressed property sale.

Business Expansion Costs: Beyond property acquisition, real estate investing involves various business expenses—marketing costs, legal fees, entity formation, insurance, property management setup, and more. A HELOAN can fund these operational needs as you scale your business.

Understanding HELOAN Underwriting: Two Paths to Qualification

One of the most attractive features of Investment HELOANs is the flexibility in underwriting approaches. Lenders like OfferMarket recognize that real estate investors have diverse financial profiles, and a one-size-fits-all approach doesn't serve this market effectively. That's why Investment HELOANs typically offer two distinct qualification pathways, allowing you to choose the route that best aligns with your financial situation.

Property-Based Qualification (DSCR Method)

The first qualification path focuses exclusively on the property's ability to service the combined debt of both the first mortgage and the new HELOAN. This is where the Debt Service Coverage Ratio (DSCR) becomes the primary underwriting metric. The lender calculates the property's monthly rental income and compares it to the total monthly debt obligations (first mortgage payment plus the new HELOAN payment).

For example, if your rental property generates $3,000 per month in rent, and the combined monthly payments on the first mortgage and HELOAN total $2,400, your DSCR would be 1.25 ($3,000 ÷ $2,400). Most lenders require a minimum DSCR of 1.0 to 1.25, meaning the property's income must equal or exceed the total debt payments by at least 25%.

This qualification method is particularly powerful for investors who have built substantial portfolios but show limited personal income on their tax returns due to depreciation deductions and other real estate tax strategies. Your personal W-2 income, tax returns, and debt-to-income ratio become largely irrelevant—the property's performance is what matters.

The Mechanics of HELOAN Financing: Structure and Terms

Investment HELOANs are structured as lump-sum, closed-end loans, meaning you receive the entire loan amount at closing in a single disbursement. This differs from a HELOC (Home Equity Line of Credit), which functions more like a credit card with a revolving credit line you can draw from repeatedly during a specified draw period.

The lump-sum nature of a HELOAN makes it ideal for specific, planned expenses where you know exactly how much capital you need. If you're purchasing a property with a $75,000 down payment requirement, a HELOAN gives you that exact amount upfront. You're not paying interest on unused credit capacity, and you have predictable, fixed monthly payments throughout the loan term.

Typical Investment HELOAN terms include:

Loan-to-Value Limits: Most lenders will allow you to borrow against your property's equity up to a combined loan-to-value (CLTV) ratio of 75-80%. This means the sum of your first mortgage balance and your new HELOAN cannot exceed 75-80% of the property's current market value. If your property is worth $400,000 and you have a $200,000 first mortgage, you could potentially access $100,000-$120,000 through a HELOAN, depending on the lender's specific CLTV limits.

Loan Terms: Investment HELOANs typically feature terms ranging from 5 to 30 years, with 15-20 year terms being most common. These loans are fully amortizing, meaning your monthly payment includes both principal and interest, and the loan will be completely paid off at the end of the term if you make all scheduled payments.

Interest Rates: As a second-lien loan on an investment property, HELOANs carry higher interest rates than first mortgages on primary residences. Rates are typically 2-4 percentage points higher than first mortgage rates, reflecting the increased risk to the lender from the subordinate lien position and the investment property classification. However, these rates are generally lower than unsecured business loans or credit cards, making HELOANs a cost-effective source of investment capital.

Fixed vs. Variable Rates: Most Investment HELOANs offer fixed interest rates, providing payment stability and protection against future rate increases. This predictability is valuable for investment planning and cash flow projections.

Closing Costs and Fees: Like any mortgage product, HELOANs involve closing costs—typically 2-5% of the loan amount. These may include appraisal fees, title insurance, recording fees, and lender fees. Some lenders offer reduced-cost or no-closing-cost options where fees are rolled into the interest rate or loan balance.

Strategic Considerations: When a HELOAN Makes Sense

While Investment HELOANs are powerful tools, they're not the right solution for every situation. Strategic investors carefully evaluate whether a HELOAN aligns with their specific circumstances and goals.

A HELOAN makes strong strategic sense when:

You Have Significant Equity in Existing Properties: The more equity you have, the more capital you can access. Properties with substantial equity—typically at least 30-40% equity—provide meaningful borrowing capacity that justifies the effort and costs of obtaining a HELOAN.

You Want to Preserve a Low First Mortgage Rate: This is perhaps the most compelling reason to choose a HELOAN over a cash-out refinance. If your first mortgage rate is significantly below current market rates, a HELOAN allows you to access equity without sacrificing that rate advantage.

You Have a Specific Capital Need: HELOANs work best when you have a defined purpose and amount in mind—a down payment on a specific property, a planned renovation budget, or a particular business investment. The lump-sum structure and closing costs make HELOANs less suitable for vague or uncertain capital needs.

You're Confident in Your Property's Cash Flow: Adding a second monthly payment increases your property's debt service. You need confidence that the rental income will reliably cover both payments with adequate margin for vacancies, repairs, and other expenses. Running the numbers carefully before taking on additional debt is essential.

You Have a Clear Plan for Generating Returns: The capital you extract through a HELOAN should be deployed in ways that generate returns exceeding the cost of the loan. If you're paying 8% interest on a HELOAN, your investment of those funds should generate returns well above 8% to justify the leverage.

Conversely, a HELOAN may not be appropriate when:

Your Property Cash Flow is Marginal: If your property barely covers its existing debt service, adding a HELOAN payment could push it into negative cash flow, requiring you to subsidize the property from other income sources.

You're Uncertain About Your Capital Needs: If you're not sure exactly how much money you'll need or when you'll need it, a HELOC's flexibility might be more appropriate than a HELOAN's lump-sum structure.

You Plan to Sell the Property Soon: Taking out a HELOAN involves closing costs and establishes a new loan. If you're planning to sell the property within a year or two, those costs may not be justified, and you'd be better off waiting to access the equity through the sale.

You're Overleveraging Your Portfolio: Adding debt across multiple properties can amplify both gains and losses. If a market downturn occurs, highly leveraged portfolios face greater risk of negative equity and financial distress. Maintaining adequate equity cushions across your portfolio is prudent risk management.

Integrating HELOANs into Your Investment Strategy

Sophisticated real estate investors view HELOANs as one component of a comprehensive financing strategy, not an isolated transaction. The most successful investors integrate HELOANs strategically into their long-term wealth-building plans.

The Equity Recycling Strategy: As your rental properties appreciate and you pay down mortgages, equity accumulates. Rather than letting that equity sit idle, you can systematically extract it through HELOANs and redeploy it into new acquisitions. This "equity recycling" accelerates portfolio growth by keeping your capital actively working across multiple properties simultaneously.

The Liquidity Reserve Approach: Some investors establish HELOANs not for immediate deployment but as a financial safety net. Having access to capital provides peace of mind and flexibility to handle unexpected situations or capitalize on time-sensitive opportunities without scrambling to arrange financing under pressure.

The Portfolio Optimization Method: Investors with multiple properties can use HELOANs strategically to optimize their overall portfolio structure—perhaps extracting equity from a property in a slower-growth market to invest in a higher-growth area, or pulling equity from a property with strong appreciation to improve another property's cash flow through renovations.

The HELOAN-to-DSCR Refinance Cycle: An advanced strategy involves using a HELOAN to fund the down payment on a new property, then later refinancing that HELOAN into a longer-term, lower-rate DSCR loan once the property has seasoned and you've established rental income history. This allows you to access capital quickly and then optimize your long-term financing structure.

At OfferMarket, we understand that Investment HELOANs are powerful tools for portfolio expansion and capital optimization. Our underwriting team has extensive experience evaluating both DSCR-based and DTI-based qualification paths, ensuring you can access your equity through the method that best fits your financial profile. Whether you're looking to fund your next fix and flip down payment, renovate an existing property, or simply establish a financial reserve, our Investment HELOAN products provide the flexibility and capital you need to keep your real estate business growing.

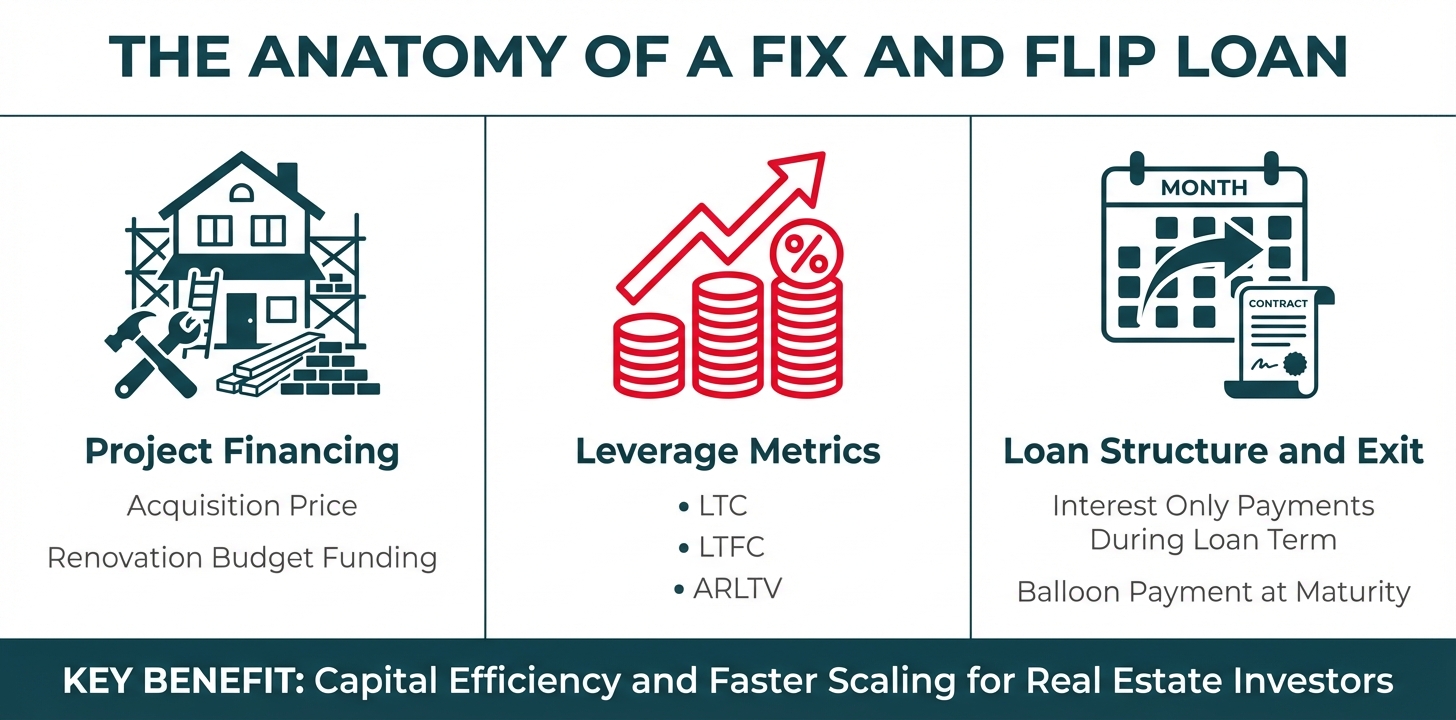

The Anatomy of a Fix and Flip Loan: Understanding Terms, Costs, and Profit Optimization

When you're evaluating a fix and flip loan, understanding the fundamental structure and cost components is essential to accurately projecting your profitability. These loans differ significantly from traditional mortgages in their terms, leverage calculations, and interest structures—and each element directly impacts your bottom line.

What a Fix and Flip Loan Finances

A fix and flip loan is designed to cover two major cost categories: the acquisition price of the property and the complete renovation budget. Unlike a traditional mortgage that only finances the purchase, a fix and flip loan recognizes that distressed properties require capital improvements before they can be sold at market value.

The acquisition price is straightforward—it's what you're paying the seller for the property in its current, as-is condition. The renovation budget, however, encompasses all the costs required to bring the property to its After Repair Value (ARV).

This includes:

- Structural repairs and foundation work

- Roof replacement or repairs

- HVAC, plumbing, and electrical upgrades

- Kitchen and bathroom renovations

- Flooring, paint, and finishes

- Landscaping and curb appeal improvements

- Permit fees and contractor labor

By financing both components, fix and flip loans eliminate the need for investors to have substantial cash reserves to fund renovations out of pocket. This leverage allows you to take on larger projects and scale your flipping business more rapidly.

Standard Term Lengths and Balloon Payment Structure

Fix and flip loans are short-term financing instruments, typically structured with terms ranging from 12 to 24 months. This timeframe aligns with the realistic timeline for purchasing a property, completing renovations, and either selling it or refinancing into long-term debt.

The loan structure features interest-only monthly payments during the term, which keeps your carrying costs predictable and manageable. You're not paying down principal each month—you're simply covering the interest accrued on the outstanding balance. This structure preserves your cash flow during the renovation and marketing phases when you're not yet generating income from the property.

At the end of the loan term, the entire principal balance comes due in what's called a balloon payment. This is when you execute your exit strategy: either by selling the renovated property and using the proceeds to pay off the loan, or by refinancing into a long-term DSCR loan that pays off the fix and flip loan and allows you to retain the property as a rental.

The short-term nature of these loans means speed is essential. Every month you hold the property costs you interest payments, property taxes, insurance, and utilities. Efficient project management directly translates to higher profits.

Understanding Leverage Metrics: LTC, LTFC and ARLTV

Three critical metrics determine how much capital a lender will provide for your project: Loan-to-Cost (LTC), Loan-to-Total-Cost (LTFC), and After-Repair-Loan-to-Value (ARLTV).

Loan-to-Cost (LTC) and 100% Rehab Financing

In the fix-and-flip space, leverage is typically broken down into the purchase phase and the renovation phase. LTC specifically measures the initial loan amount divided by the purchase price. Most lenders offer LTC ratios between 80% and 90% for the purchase, meaning your down payment is only based on the acquisition cost. Crucially, most fix-and-flip lenders will then fund 100% of your renovation budget.

The overall leverage on the project is measured by your LTFC, which is the total loan amount divided by the total project cost (purchase price + construction budget).

For example, if you're buying a property for $200,000 and budgeting $50,000 for renovations (Total Project Cost: $250,000), a lender offering 90% LTC would provide:

- Purchase Funding: $180,000 (90% of the $200,000 purchase price)

- Renovation Funding: $50,000 (100% of the rehab budget)

- Total Loan Amount: $230,000

Because the lender covers 100% of the rehab costs, you only need to bring a 10% down payment on the purchase price ($20,000), rather than a percentage of the total project costs. This structure allows investors to maximize their capital efficiency and significantly boost their cash-on-cash returns while ensuring they have skin in the game.

After-Repair-Loan-to-Value (ARLTV)

ARLTV measures the total loan amount as a percentage of the property's projected After Repair Value—what the property will be worth after renovations are complete. Using the same example, if the ARV is appraised at $350,000, and your total loan amount is $230,000, your ARLTV would be 65.7%.

The formula:

ARLTV = (Total Loan Amount / After Repair Value) × 100

Lenders typically cap ARLTV at 70-75% to maintain a protective equity cushion. This metric ensures that even if the market softens or the renovation costs exceed projections, there's sufficient equity in the property to protect the lender's position.

These metrics work together as guardrails. The LTC and LTFC ensure you have adequate capital to complete the project without bringing too much cash out of pocket, while the ARLTV ensures the completed project has sufficient value to support the maximum loan amount.

Two Types of Interest Calculation: Full Boat vs. As Disbursed

The way interest is calculated on your fix and flip loan can have a dramatic impact on your carrying costs and overall profitability. There are two primary methods: Full Boat and As Disbursed.

Full Boat Interest Calculation

With the Full Boat method, interest is charged on the entire loan amount from day one, regardless of whether you've drawn down the full renovation budget. If you're approved for a $225,000 loan at 11% annual interest, you're paying interest on the full $225,000 from the moment you close—even if $50,000 of that is sitting in a renovation holdback account waiting to be disbursed.

This method is simpler administratively but more expensive for borrowers. You're essentially paying to borrow money you haven't yet used. For smaller loans (typically under $100,000), lenders may use this method because the administrative overhead of tracking multiple draws isn't justified by the loan size.

As Disbursed Interest Calculation

The As Disbursed method charges interest only on the funds that have actually been disbursed to you. When you close on the property, you receive the acquisition funds immediately and begin paying interest on that portion. The renovation funds remain in a holdback account. As you complete phases of the renovation and request draws, those funds are released, and you begin paying interest on the newly disbursed amounts.

This structure is significantly more cost-effective for borrowers on larger projects. You're not paying interest on money sitting in an account—you're only paying for what you're actively using. For loans over $100,000, most lenders use this method because the interest savings for borrowers are substantial, and the administrative tracking is worthwhile.

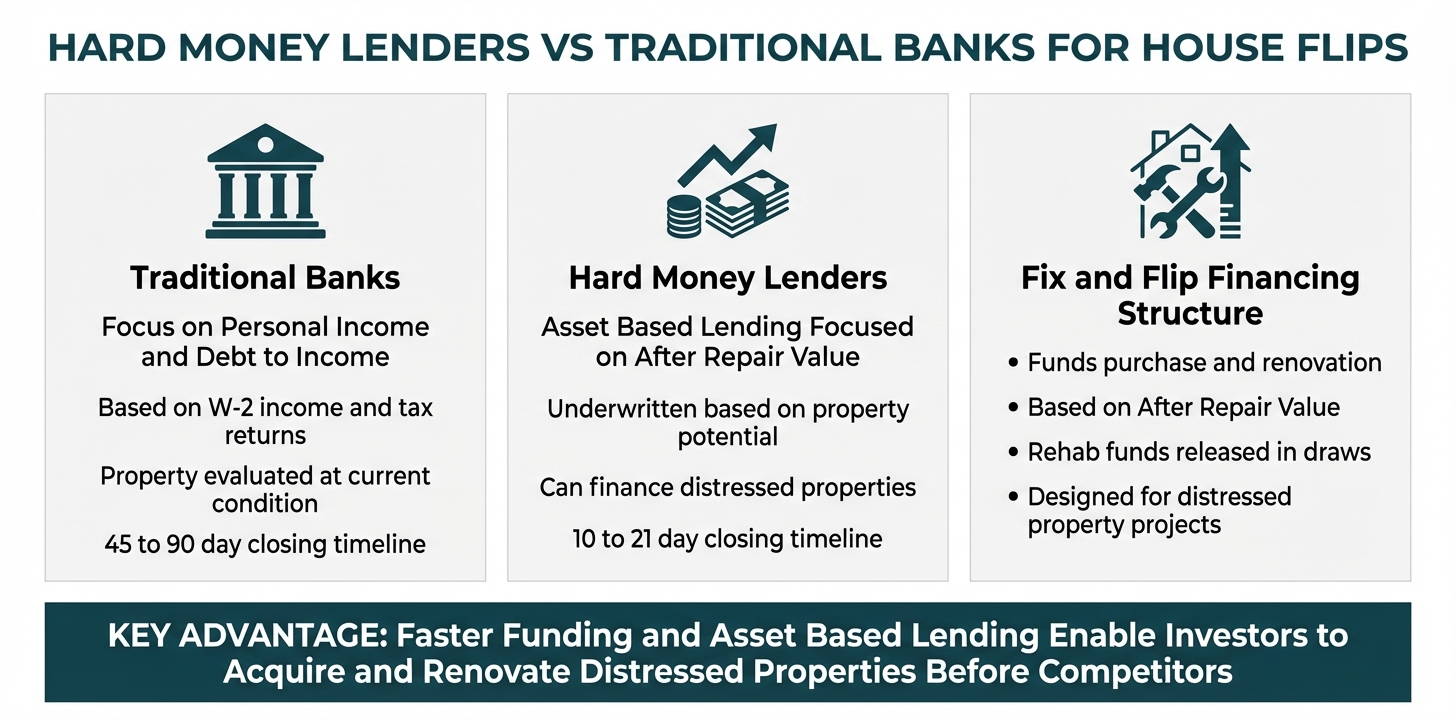

Hard Money Lenders vs. Traditional Banks: A Tale of Two Underwriters

When it comes to financing a house flip, understanding the fundamental differences between hard money lenders and traditional banks can mean the difference between seizing an opportunity and watching it slip away. These two lending approaches operate on entirely different philosophies, timelines, and underwriting criteria—each designed for distinct purposes in the real estate investment landscape.

The Bank's Lens: Conservative Evaluation of Your Personal Finances

Traditional banks approach real estate lending with a focus squarely on the borrower's personal financial stability and the property's current condition. When you apply for a conventional mortgage or business loan at a bank, underwriters will meticulously examine your W-2 income, tax returns from the past two years, credit score, and debt-to-income (DTI) ratio. They're assessing whether you, as an individual, can afford the monthly payments based on your documented income history.

Banks also evaluate the property based on its as-is value—what it's worth in its current condition. If you're looking at a distressed property that needs $75,000 in renovations, the bank will appraise it at its current dilapidated state, not its future potential. This creates an immediate problem for house flippers: banks typically won't lend on properties that don't meet minimum property standards or require substantial repairs. A home with a damaged roof, outdated electrical systems, or structural issues simply won't qualify for traditional financing because it doesn't provide adequate collateral in its present state.

Furthermore, the bank's reliance on your [personal DTI ratio](https://www.offermarket.us/blog/how-to calculate-your-dti-ratio) creates a ceiling on how much you can borrow. Even if you're an experienced investor with a proven track record of successful flips, if your personal income and existing debts don't support additional monthly payments, the bank will deny your application. This personal income limitation becomes a significant bottleneck for investors looking to scale their portfolios beyond one or two properties.

The Hard Money Advantage: Asset-Based Underwriting Focused on Potential

Hard money lenders operate from an entirely different framework. Rather than focusing primarily on your personal income, hard money loans are asset-based , meaning the underwriting decision centers on the property's value and profit potential. The key metric is the After Repair Value (ARV)—what the property will be worth once renovations are complete.

When a hard money lender evaluates your flip project, they're asking fundamentally different questions: What will this property be worth after repairs? Is the renovation budget realistic? Does the borrower have the experience to execute this project successfully? What's the profit margin built into this deal? This approach allows hard money lenders to finance distressed properties that traditional banks won't touch, because they're underwriting based on the property's future value rather than its current condition.

This asset-based approach also removes the personal income ceiling that constrains traditional bank borrowing. An investor with modest W-2 income but substantial real estate experience can secure multiple hard money loans simultaneously, because each loan is evaluated on the individual property's merits rather than the borrower's cumulative debt-to-income ratio. This is precisely why hard money lending enables investors to scale their portfolios rapidly—your personal income statement becomes far less relevant than your track record and the quality of your deals.

Why Banks Can't Finance Your Flip: The Distressed Property Problem

The reality is that most profitable house flips involve properties that banks simply cannot finance. Banks are heavily regulated institutions with strict guidelines about property conditions, and they typically require properties to meet Federal Housing Administration (FHA) or conventional loan standards. A property with foundation issues, mold, missing HVAC systems, or significant code violations won't qualify.

Additionally, banks are not equipped to disburse construction funds in draws as renovation work progresses. They provide a lump sum at closing based on the purchase price, leaving you to fund the entire renovation out of pocket. For a flip requiring $100,000 in repairs, this creates an enormous cash flow challenge that most investors cannot overcome without separate financing.

Hard money lenders, by contrast, are specifically designed to fund both the acquisition and the renovation budget. They understand construction timelines, work with contractors, and release funds in stages as work is completed. This structure makes the entire flip financially feasible for investors who don't have six figures sitting in a bank account.

Speed: The Competitive Edge That Wins Deals

Perhaps the most critical advantage of hard money lending is speed. Traditional bank loans can take 45 to 90 days to close, involving extensive documentation, multiple appraisals, committee approvals, and bureaucratic processes. Hard money lenders, operating with streamlined underwriting focused on the asset, can close loans in as little as 10 to 21 days.

In competitive real estate markets, this speed difference is not just convenient—it's essential. When you're making an offer on a distressed property, sellers often need to close quickly. They may be facing foreclosure, dealing with an estate sale, or simply wanting to liquidate an unwanted asset. A cash-equivalent offer that can close in three weeks will beat a conventional financed offer every time, even if the conventional offer is slightly higher.

This speed advantage allows hard money borrowers to negotiate better purchase prices, secure properties before other investors can mobilize financing, and capitalize on time-sensitive opportunities. In the house flipping business, where profit margins often depend on acquisition price, the ability to move quickly translates directly to increased profitability.

Flexibility and Adaptability: Tailored Solutions for Real Investors

Beyond speed, hard money lenders offer flexibility that traditional banks cannot match. If your renovation uncovers unexpected issues—perhaps the electrical panel needs upgrading or there's water damage behind the walls—a hard money lender can often adjust the loan terms or increase the rehab budget. Traditional banks, locked into their initial underwriting and loan documents, have little ability to accommodate mid-project changes.

Hard money lenders also understand the business of house flipping in ways that bank loan officers typically don't. They've seen hundreds or thousands of similar projects, understand realistic timelines, and can provide guidance beyond just financing. This expertise becomes an invaluable resource, especially for investors tackling their first few flips or entering new markets.

The Right Tool for the Right Job

Ultimately, the choice between hard money and traditional bank financing isn't about one being universally better than the other—it's about using the right tool for the right job. Traditional bank loans excel for owner-occupied properties, long-term buy-and-hold investments in good condition, and situations where you have ample time and strong personal financials.

Hard money loans are the superior choice for house flipping because they're specifically designed for this use case: short-term financing of distressed properties based on future value, with fast closings and construction fund disbursement. They enable you to compete effectively for deals, execute renovations with proper funding, and scale your business beyond personal income limitations.

For investors serious about building a house flipping business, understanding and leveraging hard money financing isn't optional—it's fundamental to your competitive positioning and growth trajectory.

The OfferMarket Advantage: A Holistic Platform for Real Estate Investors

In the competitive world of real estate investing, success often hinges on more than just securing financing—it requires access to deals, comprehensive insurance, and a seamless process that connects all these elements. OfferMarket has built a holistic platform that goes far beyond traditional lending, creating an integrated ecosystem designed specifically for the needs of real estate investors flipping houses and building rental portfolios.

Beyond Lending: An Integrated Marketplace for Deals and Capital

While many platforms focus exclusively on either capital or deal flow, OfferMarket uniquely combines both by offering a comprehensive marketplace that serves as a one-stop solution for investors at every stage of their journey.

The platform's marketplace component provides investors with access to off-market listings, connecting them with properties that have genuine flip potential. This integration means you're not just getting a loan—you're getting access to the deals themselves, along with the capital to execute on them. For investors, this eliminates the friction of working with multiple disconnected services and streamlines the entire acquisition process.

Right-Sized Insurance for Investment Properties

One of the most overlooked aspects of house flipping is securing appropriate insurance coverage. Standard homeowner's policies don't cover vacant properties under renovation, and finding specialized coverage can be time-consuming and expensive. OfferMarket has addressed this pain point by providing streamlined insurance solutions specifically designed for investment properties.

The platform offers right-sized insurance products that protect investors during the renovation phase without the excessive premiums often associated with vacant property coverage. This includes builder's risk insurance for properties under construction, liability coverage for contractor activities, and property insurance that bridges the gap between acquisition and either sale or tenant occupancy.

By integrating insurance services directly into the platform, OfferMarket eliminates the need to shop around for coverage, ensures compliance with lender requirements, and provides policies that are appropriately priced for the actual risk profile of fix-and-flip projects. This integration also means faster closings, since insurance requirements are handled seamlessly as part of the loan process rather than becoming a last-minute obstacle.

The Speed Advantage: Technology Meets Expertise

Time is money in real estate investing, and OfferMarket's integrated platform delivers unprecedented speed throughout the entire transaction lifecycle. From the moment you request an instant quote to the day you close on your loan, the platform's technology and streamlined processes work in concert to eliminate delays.

The instant quote system provides preliminary loan terms in minutes, not days, allowing you to make confident offers on properties knowing your financing is ready. The application process is entirely digital, with intelligent document collection that requests only what's necessary for your specific loan type and property situation.

This speed advantage extends to the draw process during renovation. Because OfferMarket understands the rhythm of fix-and-flip projects, the platform has optimized draw inspections and fund disbursements to keep your contractors paid and your project on schedule. No more waiting weeks for a draw request to be processed—OfferMarket's streamlined approach typically processes draws within days.

Cost-Effectiveness Through Integration

The integrated nature of OfferMarket's platform doesn't just save time—it saves money. When marketplace access, lending, and insurance all flow through a single ecosystem, the efficiencies compound into real cost savings for investors.

Traditional approaches require investors to pay separate fees to deal finders, mortgage brokers, appraisal companies, insurance agents, and various other service providers. Each intermediary adds their markup, and coordination between these disconnected services creates inefficiencies that ultimately cost investors both time and money. OfferMarket's model eliminates many of these redundant costs by bringing services in-house and creating operational efficiencies that are passed along to investors.